Norway Data Center Construction Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

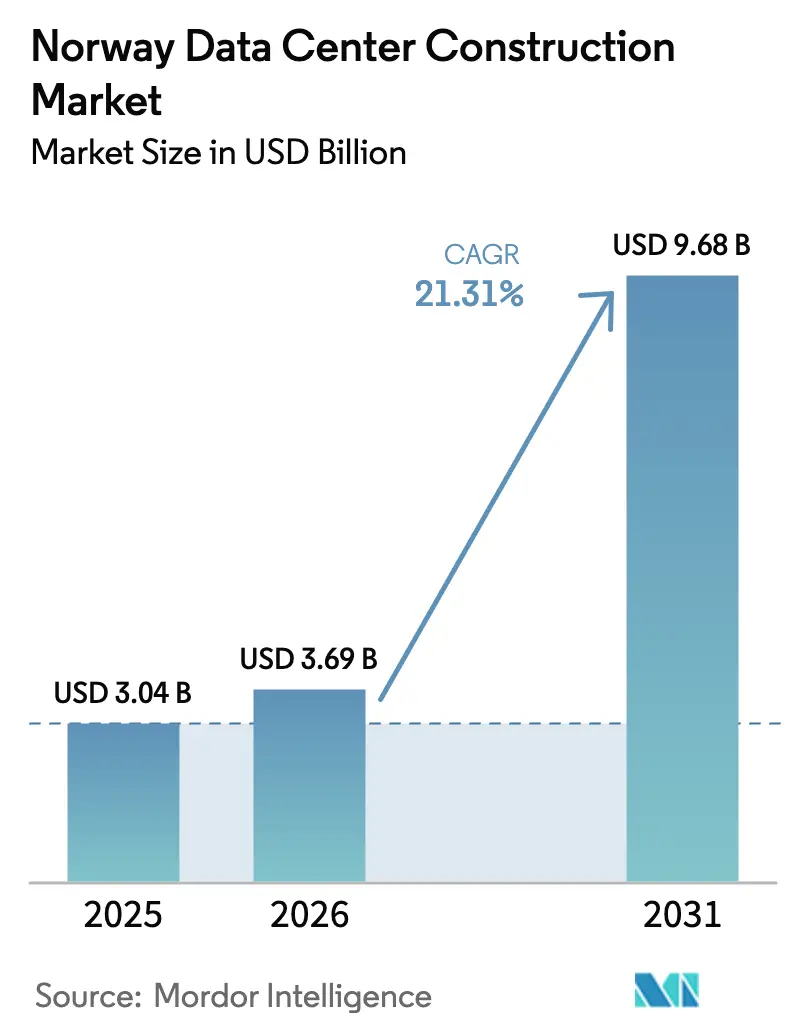

| Base Year Market Size (2025) | USD 3.04 Billion |

| Market Size (2026) | USD 3.69 Billion |

| Market Size (2031) | USD 9.68 Billion |

| Growth Rate (2026 - 2031) | 21.31% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Norway Data Center Construction Market Analysis by Mordor Intelligence

The Norway data center construction market size was valued at USD 3.04 billion in 2025 and estimated to grow from USD 3.69 billion in 2026 to reach USD 9.68 billion by 2031, at a CAGR of 21.31% during the forecast period (2026-2031). This growth trajectory rests on Norway’s hydro-powered electricity mix, where hydropower already supplies 92% of generation and shields operators from carbon pricing or volatile fossil-fuel costs. Policy-led risk relief of NOK 60 billion(USD 5.93 billion), hyperscaler capital expenditure programs, and a cool Nordic climate that lowers power usage effectiveness (PUE) strengthen the investment case. Google’s GBP 600 million (USD 808.34 million) build in Skien requiring 840 MW, Bulk Infrastructure’s multi-hundred-megawatt campuses, and Vantage Data Centers’ billion-dollar funding round validate near-term demand while raising the bar on delivery speed. At the same time, rising construction costs and potential grid bottlenecks pose execution risks that require tighter project controls and innovative power-distribution solutions.

Key Report Takeaways

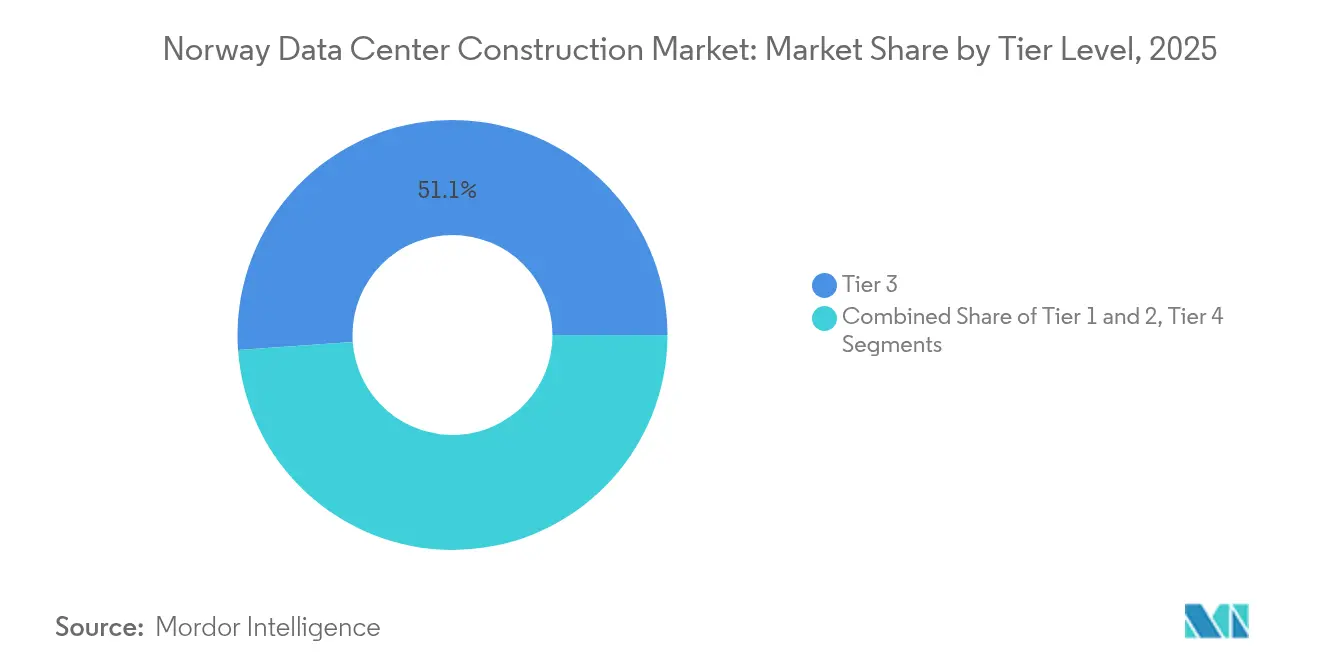

- By tier type, Tier 3 facilities held 51.12% of Norway data center construction market share in 2025, whereas Tier 4 is set to expand at a 23.62% CAGR to 2031.

- By data center type, colocation services captured 56.48% revenue in 2025, while hyperscaler self-builds are forecast to rise at a 23.23% CAGR through 2031.

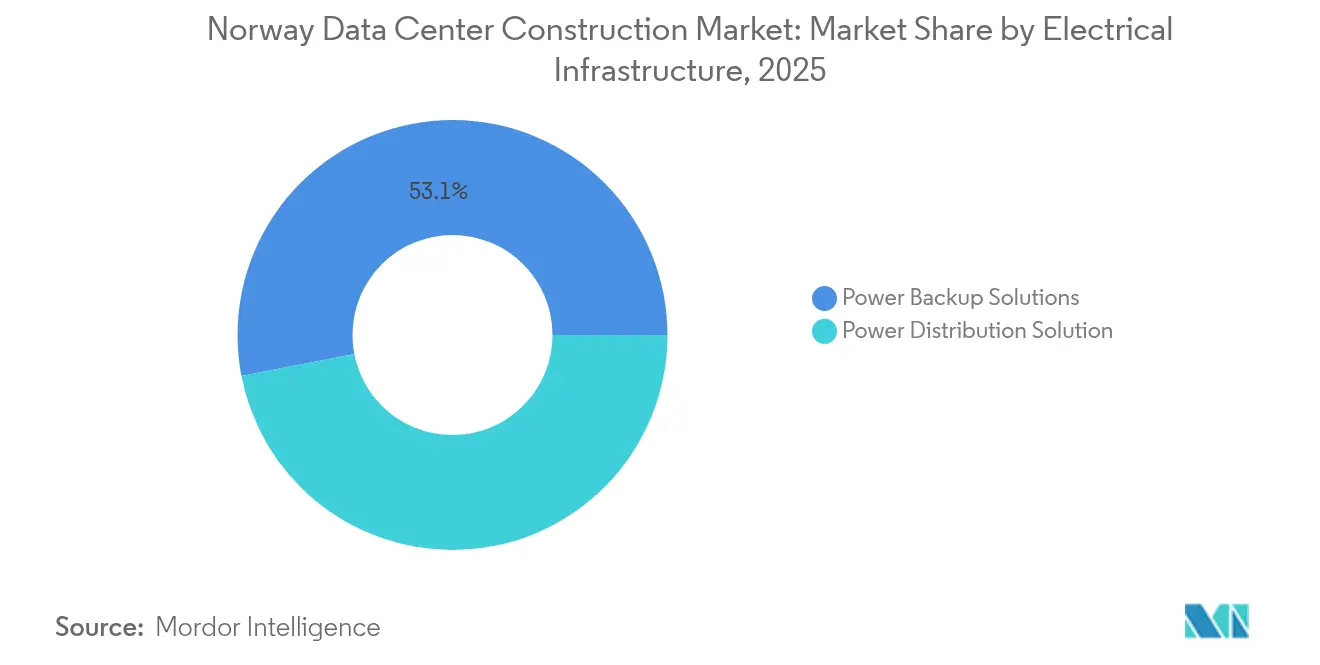

- By electrical infrastructure, power backup accounted for 53.05% share of the Norway data center construction market size in 2025; power-distribution systems are growing the fastest at 23.81% CAGR.

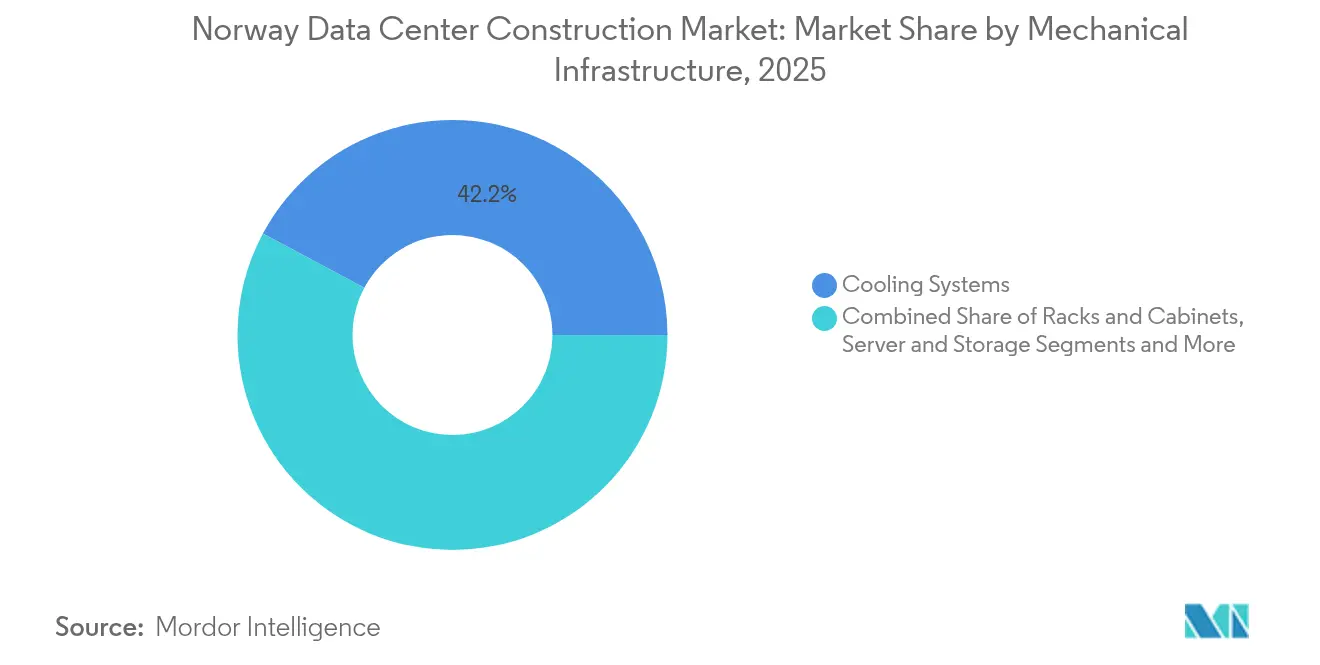

- By mechanical infrastructure, cooling systems commanded 42.18% share of the Norway data center construction market size in 2025 and servers plus storage are advancing at a 22.49% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Norway Data Center Construction Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Government incentives and supportive regulation | +4.2% | National, with concentrated benefits in Skien, Oslo, Kristiansand | Medium term (2-4 years) |

| Hyperscale/cloud provider capex acceleration | +6.8% | Global impact, with primary deployment in southern Norway | Short term (≤ 2 years) |

| Abundant renewable (hydro-based) power availability | +5.1% | National, with premium access in western fjord regions | Long term (≥ 4 years) |

| Cool Nordic climate lowering PUE | +2.3% | National, with enhanced benefits in northern regions | Long term (≥ 4 years) |

| AI/HPC density push requiring immersion and liquid cooling | +3.8% | Global trend, concentrated in Oslo, Skien technology corridors | Medium term (2-4 years) |

| Crypto-mining migration toward green jurisdictions | +1.4% | Regional Nordic focus, with spillover to remote hydro areas | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Government incentives and supportive rules

Norway uses clear permitting tracks, predictable taxes, and state-backed loan guarantees to de-risk new capacity, reinforcing the Norway data center construction market as Europe’s green hub.[1]Norwegian Ministry of Trade and Industry, “Green Industry Package,” regjeringen.noThe NOK 60 billion green-industry package earmarks digital infrastructure, helping investors lock grid connections faster than in peer nations. Google’s Skien schedule was trimmed by almost two years through accelerated environmental and interconnection approvals. Mandatory registration adopted in January 2025 has added compliance tasks, yet it also reserves megawatt slots and reduces application overlap. The Norwegian Water Resources and Energy Directorate has already set aside 8,000 MW of new consumption capacity, signalling long-run commitment.

Hyperscaler and cloud-provider CAPEX surge

Global cloud majors are pivoting toward sovereign hosting and AI-ready designs, funnelling unprecedented capital into the Norway data center construction market.[2]NRK Staff, “Google bygger datasenter i Skien,” nrk.no Microsoft’s USD 80 billion fiscal-2025 plan, Google’s Skien outlay, and TikTok’s full utilisation of Green Mountain’s three sites show that hyperscalers seek reliable hydro energy, cold climate, and GDPR alignment. AI racks draw 40–140 kW, multiplying traditional power densities and necessitating fresh builds rather than retrofits. As EU data-sovereignty mandates tighten, self-owned campuses in Norway are emerging instead of cross-border server farms, pushing 2025-2027 groundbreakings to record levels

Hydro-based renewable electricity dominance

Hydropower covers 92% of national supply, letting operators guarantee carbon-free uptime and sidestep renewable-energy certificates, a differentiator inside the Norway data center construction market.[3]International Energy Agency, “Norway 2024 Energy Profile,” iea.org Å Energi alone plans NOK 30 billion of hydropower upgrades, underscoring future headroom aenergi.no. Polar DC’s DRA01 site runs entirely on hydro and provides 12 MW for AI training, proving the model’s viability. As global digital firms pledge science-based net-zero targets, Norwegian kilowatt hours deliver immediate compliance, cutting the negotiation time linked to power-purchase agreements elsewhere.

Restraints Impact Analysis*

| Restraint | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Inefficient heat-reuse integration with district heating | -2.1% | Urban centers: Oslo, Bergen, Trondheim | Medium term (2-4 years) |

| Rising construction costs and skilled-labour shortages | -3.4% | National, with acute impact in remote hydro regions | Short term (≤ 2 years) |

| Grid bottlenecks in remote hydro regions | -2.8% | Western fjord regions, northern Norway | Long term (≥ 4 years) |

| Lengthy permitting and local community opposition | -1.9% | Rural municipalities, environmentally sensitive areas | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising construction costs and labour gaps

Specialist trades across mechanical and electrical disciplines remain scarce, pushing wages well above general inflation and stretching project timelines in the Norway data center construction marke. Research from NTNU reveals that only 21% of cost items benefit from automated take-off, leaving manual workflows that amplify scheduling risk. Operators now phase builds into smaller modules or import prefabricated components to control variability, yet near-term inflation continues to hinder margin certainty.

Grid bottlenecks near remote hydro sources

While generation is plentiful, transmission into fjords and northern zones is limited by ageing lines and contested rights-of-way, creating a ceiling on new megawatt allocations. Statnett’s NOK 150 billion (USD 14.83 billion) upgrade program targets this gap, yet it will not fully conclude before 2034, leaving interim congestion in the Norway data center construction market. Local stress forced the closure of the Stokmarknes crypto-mine, showing how 80 GWh of annual draw can destabilize rural grids. Heimdall Power’s Neuron sensors promise a 40% capacity uplift on installed lines through dynamic rating, but fleet-wide rollout is still in the early stages.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Tier Type: Premium reliability lifts Tier 4 adoption

Tier 4 builds, though costlier, are racing ahead at a 23.62% CAGR as AI workloads cannot afford unplanned downtime. Tier 3 sites currently hold 51.12% of Norway's data center construction market share, yet their margin over Tier 4 narrows each year. Polar DC’s DRA01 demonstrates how a Tier 3 design can embed Tier 4-like redundancies via dual utility feeds and N+2 cooling to deliver a near-perfect service level. Operators also use hybrid designs where less-critical zones follow Tier 3 protocols while AI training halls follow Tier 4, aligning investment with workload sensitivity. Growth in the Norway data center construction market, therefore, reflects a premium shift rather than uniform expansion across all tiers. Enterprises eyeing GPU clusters now favour the highest availability rating even if it inflates CAPEX, since a brief outage can invalidate millions of compute-hours. Suppliers respond by pre-engineering Tier 4 modules to compress build cycles, trimming historical cost premiums.

By Data Center Type: Hyperscaler self-build raises sovereign capacity

Hyperscaler campuses under direct ownership are climbing at 23.23% CAGR and are on pace to match colocation volume inside the Norway data center construction market by 2031. Google’s Skien build typifies the model, combining 840 MW of reserved capacity with purpose-built waterless cooling to support proprietary AI frameworks. Colocation still provides 56.48% share in 2025, driven by enterprises that prefer operational agility to capital outlay. However, hyperscalers want tighter control over power distribution, security, and custom chip deployment, prompting build-to-suit deals that bypass multitenant designs. Operators such as Bulk respond with joint ventures where land and power come from local partners while design and operation remain with cloud majors, balancing risk while keeping the Norway data center construction market diversified. Smaller edge and enterprise builds coexist, serving workloads that require sub-10-millisecond latency or local regulatory hosting inside rural municipalities.

By Electrical Infrastructure: Smart distribution eclipses static backup

Power backup retains 53.05% of spending, yet growth pivots toward intelligent distribution gear that can reroute load in milliseconds and feed real-time analytics into hyperscaler network operations centers. Power-distribution systems are registering a 23.81% CAGR, the highest among electrical categories in the Norway data center construction market. Operators upgrade to solid-state transfer switches, busway architectures, and software-defined monitoring so they can tap hydropower peaks and flex with AI load variation. Heimdall Power’s dynamic-line-rating sensors feed live capacity data straight into data-center energy-management platforms, allowing operators to draw additional power headroom during colder weather. Although UPS and diesel generators remain procurement staples, their performance envelope is maturing, so investment tilts toward distribution that maximizes existing kilowatts rather than stacked redundancy.

By Mechanical Infrastructure: Server refresh and liquid cooling steer capex

Servers and storage now advance at 22.49% CAGR as enterprises chase GPU performance curves that refresh every 18 months, thereby swelling the mechanical component of Norway data center construction market size. Cooling retains a 42.18% share, reflecting its enduring criticality even in a cool climate. Next-generation immersion cooling tanks cut water use by up to 95% and reduce footprint, freeing white space that operators can rededicate to compute. Microsoft’s zero-water pledge by 2026 has spurred wider adoption of closed-loop coolant exchanges that fit Nordic environments where external ambient air can help chill secondary loops. Racks and containment systems, while smaller in budget terms, are evolving toward 70 kW average load ratings, more than triple 2022 levels, supporting new AI nodes. Mechanical suppliers form consortia with semiconductor designers to certify thermals before chips reach market, reducing commissioning risk in the Norway data center construction market.

Geography Analysis

Southern Norway hosts the densest cluster of projects due to grid headroom, subsea-cable landing points, and proximity to the Oslo metro market. Google’s landmark Skien investment, scheduled to go live in 2026, underscores regional magnetism as it alone demands an 840 MW allocation. Bulk Infrastructure’s N01 campus near Kristiansand has secured 400 MW and seeks permits for a 1 GW future envelope, marking one of Europe’s largest single-site ambitions . Western fjords offer unrivalled hydro access but face limited transmission, so projects there often build private substations or deploy battery storage to smooth draw. Northern Norway, benefiting from colder air and available land, is attracting AI or crypto loads able to tolerate higher latency; yet labour scarcity and longer supply chains elevate costs. Cross-border links make the broader Nordic corridor a single logical footprint for multinationals, as illustrated by GlobalConnect’s 3 Pbit/s Sweden-Finland route that tightens Nordic interdependence. Regional operators can therefore market pan-Nordic resiliency while keeping compute in the Norway data center construction market for renewables and compliance. Coastal municipalities now offer district-heating networks ready to capture server waste heat, though pipeline reach remains limited outside Oslo and Bergen, tempering full valorisation of heat reuse.

Competitive Landscape

Competition divides between Nordic-bred specialists and cash-heavy global entrants. Green Mountain, Bulk Infrastructure, and atNorth leverage decades of hydro relationships and brownfield military facilities adaptable for data centers, giving them a first-mover land bank and power rights in the Norway data center construction market. Azrieli Group’s USD 850 million acquisition of Green Mountain in 2024 validated Norwegian equity stories and accelerated the company’s 520 MW pipeline. Vantage Data Centers, Equinix, and Digital Realty deploy multibillion-dollar programs that emphasise modular design and heat-export schemes suited to Nordic municipalities. Partnership models emerge in which foreign capital funds shell buildings while Norwegian firms deliver local engineering, aligning risk with expertise. Sustainability credentials have become the new currency of differentiation, prompting operators to publish real-time emissions dashboards and sign long-term power contracts with Å Energi and Statkraft. Technical chops around liquid cooling and AI workload orchestration now carry equal weight with land price in winning hyperscaler mandates inside the Norway data center construction market. White-space opportunities centre on district-heating synergies, heat-to-greenhouse agriculture, and grid-flex solutions that monetize idle generator capacity.

Norway Data Center Construction Industry Leaders

Skanska AB

Coromatic AB

COWI A/S

CTS Nordics

Rider Levett Bucknall

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Polar DC commissions the 12 MW DRA01 hydro-powered AI center in Tørdal, the first purpose-built Norwegian site tuned for immersion cooling

- April 2025: TikTok finalises full occupancy across Green Mountain’s three facilities, consolidating European content delivery in Norway

- January 2025: Norway introduces mandatory data-center registration, offering transparent capacity queues and unified security auditing.

- January 2025: GlobalConnect completes Sweden-Finland optical route supporting 3 Pbit/s, reinforcing Nordic cross-border traffic flows.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the Norway data center construction market as all capital expenditure spent inside Norway to design, erect, fit-out, and commission new carrier-neutral, self-built hyperscale, enterprise, and edge facilities, including site works, structural shells, electrical distribution, back-up power, cooling systems, racks, monitoring software, and associated professional services. According to Mordor Intelligence, financial outlays linked only to mechanical or electrical upgrades inside already live halls are counted when they form part of an expansion phase, not routine maintenance.

Scope exclusion: Recurring IT hardware refresh, managed hosting contracts, and daily operations OPEX are outside this study.

Segmentation Overview

- By Tier Type

- Tier 1 and 2

- Tier 3

- Tier 4

- By Data Center Type

- Colocation

- Self-build Hyperscalers (CSPs)

- Enterprise and Edge

- By Infrastructure

- By Electrical Infrastructure

- Power Distribution Solution

- Power Backup Solutions

- By Mechanical Infrastructure

- Cooling Systems

- Racks and Cabinets

- Servers and Storage

- Other Mechanical Infrastructure

- General Construction

- Service - Design and Consulting, Integration, Support and Maintenance

- By Electrical Infrastructure

- Tier 1 and 2

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed electrical contractors, EPC project directors, colocation facility managers in Oslo and Vestland, and equipment distributors to validate average megawatt build costs, deployment timelines, and pipeline probability scores. Short surveys with hyperscale procurement leads confirmed current liquid cooling penetration and renewable power contracting practices that influence future spend.

Desk Research

We mapped the market through publicly available datasets such as Statistics Norway building cost indices, the Norwegian Water Resources and Energy Directorate's power grid connection queue, Eurostat construction output, and Uptime Institute's Tier certification register. Company financials retrieved from D&B Hoovers, project news archived in Dow Jones Factiva, and import values for switchgear from UN Comtrade helped anchor unit costs. Additional insights came from white papers posted by the Norwegian Data Center Industry Association and consultation minutes released by the Ministry of Digital Governance. The sources listed are illustrative; many further references were reviewed to complete evidence gathering.

Market-Sizing & Forecasting

A top-down model started with 2024 building permits and announced project CAPEX, reconstructed by multiplying planned IT load (MW) with verified cost per MW norms, then segmented by tier type. Results were stress tested against a bottom-up roll-up of sampled supplier ASP multiplied by delivered volumes across twenty recent sites. Key variables like hydropower tariff trends, krone-denominated construction material index, hyperscale cloud CAPEX, rack density progression, and Tier 4 adoption rate feed a multivariate regression that projects spend to 2030. Gaps in supplier disclosures are bridged through regional benchmarks and confirmed with expert feedback before numbers finalize.

Data Validation & Update Cycle

Outputs pass variance checks versus electricity grid connection data and independent investment trackers; anomalies trigger re-contact with original respondents. Two analysts review every revision. The model refreshes annually, with interim updates when large project announcements or policy shifts occur, ensuring clients always receive the latest view.

Norway Data Center Construction Baseline: Why It Stands Up

Published estimates often diverge because firms choose different cost scopes, project probability filters, and refresh cadences.

Key gap drivers include whether mechanical infrastructure is bundled, if self-built hyperscale projects without third-party contractors are captured, currency conversion year, and the point at which provisional permits are recognized. Mordor's disciplined scope definition and annual reconciliation with live build milestones provide a dependable midpoint that decision makers can trace back to explicit variables.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 3.04 B (2025) | Mordor Intelligence | - |

| USD 1.55 B (2024) | Regional Consultancy A | Excludes mechanical infrastructure and counts only projects reaching full financial close |

| USD 2.82 B (2023) | Global Consultancy B | Blends construction CAPEX with operating colocation revenue and applies lower Tier 4 penetration assumptions |

These comparisons show that while other publishers either narrow cost components or mix revenue streams, our balanced, clearly scoped approach yields a transparent baseline clients can replicate and stress test with confidence.

Key Questions Answered in the Report

What is the current value of the Norway data center construction market?

The market stands at USD 3.69 billion in 2026, with a forecast value of USD 9.68 billion by 2031.

How fast is the Norway data center construction market expected to grow?

It is projected to register a 21.31% CAGR between 2026 and 2031.

Which tier category leads the market today?

Tier 3 sites hold 51.12% of Norway data center construction market share in 2025, though Tier 4 is growing faster.

Why are hyperscalers investing directly in Norway?

They are seeking sovereign-data compliance, renewable hydro power, and cool ambient temperatures that cut operating costs and emissions.

Page last updated on: