Energy & Power

30th JulyUnlocking Market Potential for Solid-State Transformers

3 Min Read

The Iraq Oil and Gas Market Report is Segmented by Sector (Upstream, Midstream, and Downstream), Location (Onshore and Offshore), and Service (Construction, Maintenance and Turn-Around, and Decommissioning). The Market Sizes and Forecasts are Provided in Terms of Value (USD).

Market Overview

| Study Period | 2020 - 2030 |

|---|---|

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

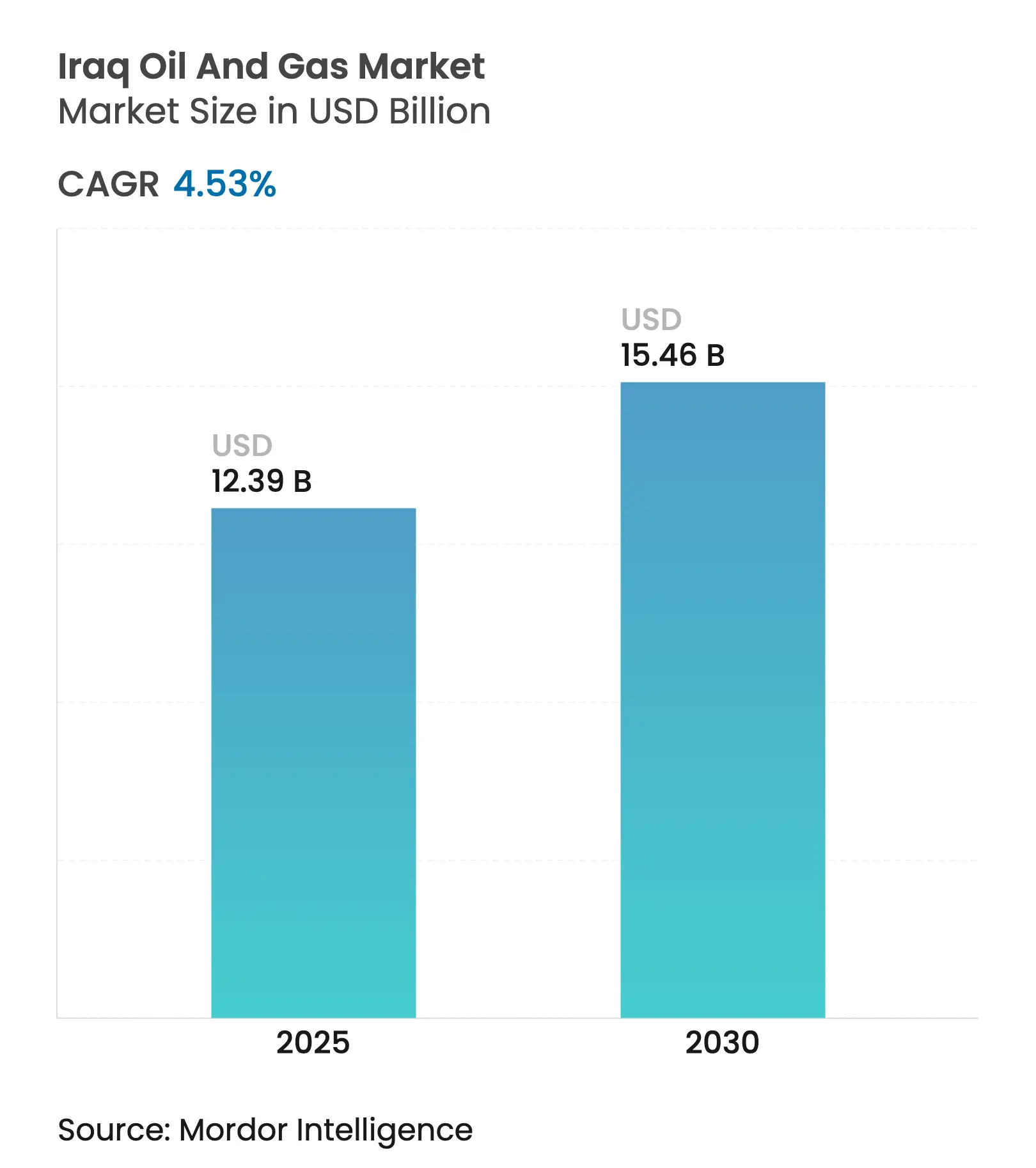

| Market Size (2025) | USD 12.39 Billion |

| Market Size (2030) | USD 15.46 Billion |

| Growth Rate (2025 - 2030) | 4.53 % CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order. Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

Robust proven reserves of more than 145 billion barrels and expansion targets beyond 6 million bpd underpin sustained upstream spending, while integrated gas‐processing projects convert previously flared gas into value-adding revenue streams. The re-entry of Western majors, the acceleration of construction of seawater injection systems, and a shift toward profit-sharing contracts further reinforce the outlook for growth in Iraq's oil and gas market. Midstream build-outs that remove export bottlenecks and monetize associated gas complement upstream momentum, and service providers able to deliver lifecycle solutions gain a competitive advantage. However, OPEC+ quotas, political frictions, and infrastructure deficits temper near-term production gains even as strategic mega-projects promise long-term upside.

Key Report Takeaways

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Accelerated

capacity-expansion target to >6 mbpd by 2029

Accelerated

capacity-expansion target to >6 mbpd by 2029

| +1.2% | National, concentrated in southern fields (Basra, Maysan) | Medium term (2-4 years) | (~) %

Impact on CAGR Forecast:

+1.2%

|

Geographic

Relevance

:

National,

concentrated in southern fields (Basra, Maysan)

|

Impact

Timeline

:

Medium

term (2-4 years)

|

Re-entry

of Western majors via mega-deals (BP, TotalEnergies)

Re-entry

of Western majors via mega-deals (BP, TotalEnergies)

| +0.8% | National, with focus on Kirkuk, Basra regions | Long term (≥ 4 years) | |||

Profit-sharing

contract regime attracts new investors

Profit-sharing

contract regime attracts new investors

| +0.6% | National, particularly greenfield developments | Medium term (2-4 years) | |||

Gas-flaring

capture boosts domestic gas supply & revenues

Gas-flaring

capture boosts domestic gas supply & revenues

| +0.5% | Southern Iraq, Basra governorate primarily | Short term (≤ 2 years) | |||

Common

Seawater Supply Project unlocks southern field output

Common

Seawater Supply Project unlocks southern field output

| +0.4% | Southern Iraq, Rumaila-West Qurna corridor | Medium term (2-4 years) | |||

New

Iraq–Turkey export pipeline enhances evacuation capacity

New

Iraq–Turkey export pipeline enhances evacuation capacity

| +0.3% | Northern Iraq, Kurdistan region | Long term (≥ 4 years) | |||

| Source: Mordor Intelligence | ||||||

Accelerated Capacity-Expansion Target Drives Infrastructure Investment

Iraq aims to lift output beyond 6 million bpd by 2029, compelling a surge of capital into drilling, gathering, and water-injection systems across West Qurna-1, Rumaila, and Zubair. Chinese EPC firms, such as CPECC, dominate early contracts; however, execution hinges on reliable electricity and sufficient injection water, which remain scarce in Basra. The capacity push supports incremental demand for rigs, OCTG, and digital reservoir management tools, keeping the Iraqi oil and gas market on an upward trajectory, even amid quota constraints.

Western Majors’ Re-Entry Reshapes Competitive Dynamics

BP’s USD 25 billion Kirkuk agreement and TotalEnergies’ USD 27 billion Basra package bring advanced EOR expertise, large-scale financing, and integrated gas solutions that are not available from the lowest-cost bidders alone. Their presence elevates ESG standards, accelerates gas monetization, and encourages co-investment from regional NOCs, reinforcing long-run resilience of the Iraq oil and gas market.

Profit-Sharing Contracts Attract Risk Capital

The shift from cost-plus technical service contracts to profit-sharing terms offers operators a direct slice of production revenue, aligning incentives toward efficiency and longer‐cycle field optimization. European independents and North American firms have already pre-qualified for the 2025 licensing round, signaling renewed appetite for Iraq's oil and gas market opportunities under the revised fiscal regime.

Gas-Flaring Capture Unlocks Domestic Revenue Streams

The expansions of the Basra Gas Company and the Ratawi gas center together add more than 1 bcf/d of capacity, converting waste gas into feedstock for power plants and petrochemicals. The incremental supply alleviates an 8 GW electricity shortfall, improves export carbon intensity, and stabilizes state fuel budgets, reinforcing demand across the Iraq oil and gas market.[1]Ministry of Electricity, “Generation Capacity Data 2025,” moelc.gov.iq

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Political

instability & Baghdad-Erbil disputes

Political

instability & Baghdad-Erbil disputes

| -0.9% | National, particularly Kurdistan region | Long term (≥ 4 years) | (~) %

Impact on CAGR Forecast:

-0.9%

|

Geographic

Relevance

:

National,

particularly Kurdistan region

|

Impact

Timeline

:

Long

term (≥ 4 years)

|

Electricity

& water scarcity at project sites

Electricity

& water scarcity at project sites

| -0.7% | National, acute in southern production areas | Medium term (2-4 years) | |||

OPEC+

quota limits near-term production growth

OPEC+

quota limits near-term production growth

| -0.5% | National production planning | Short term (≤ 2 years) | |||

Dependence

on Chinese EPCs poses supply-chain risk

Dependence

on Chinese EPCs poses supply-chain risk

| -0.4% | National, concentrated in major projects | Medium term (2-4 years) | |||

| Source: Mordor Intelligence | ||||||

Political Instability Creates Investment Uncertainty

Revenue-sharing tensions between Baghdad and Erbil have already shut down 450 kbpd of pipeline exports and complicate financing for new ventures. Investors factor in higher risk premiums, which can delay FIDs and dilute near-term gains in the Iraq oil and gas market.[2]State Organization for Marketing of Oil, “Pipeline Export Statistics 2024,” somo.oil.gov.iq

Infrastructure Deficits Constrain Operational Efficiency

Intermittent grid power forces operators to install diesel generators, which add USD 2–3/bbl to lifting costs, while limited freshwater necessitates the use of expensive treatment units for EOR. These shortcomings elevate breakeven thresholds across the Iraq oil and gas market and slow upgrade schedules.

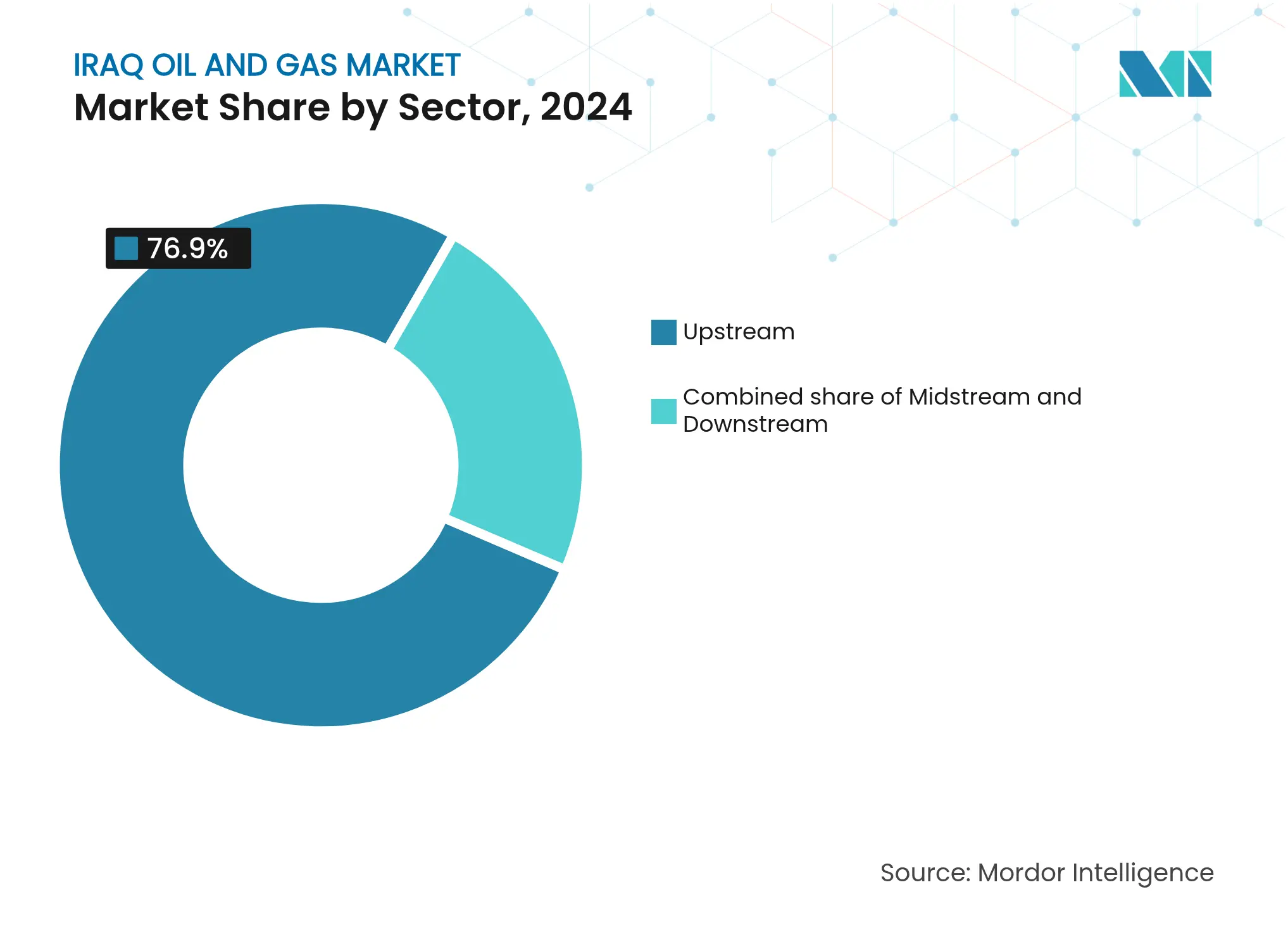

By Sector: Upstream Dominance Faces Midstream Acceleration

Upstream operations retained a 76.9% market share in the Iraqi oil and gas sector in 2024, thanks to low lifting costs of under USD 10/bbl at Rumaila and Kirkuk. Yet the midstream build-out is pacing a 5.2% CAGR to 2030 as processing hubs like Ratawi and Basra Gas drive incremental value from associated gas previously flared. Downstream remains the smallest slice but gains momentum from refinery revamps designed to cut product imports. The Iraq oil and gas market size for midstream assets is expected to increase in parallel with pipeline and storage expansions that debottleneck exports and feed petrochemical schemes.

In the second half of the period, integrated upstream-midstream packages, such as TotalEnergies’ Gas Growth Integrated Project, are expected to stabilize cash flows and free up capital for enhanced oil recovery, thereby bolstering the long-term resilience of the Iraqi oil and gas market.

Note: Segment shares of all individual segments available upon report purchase

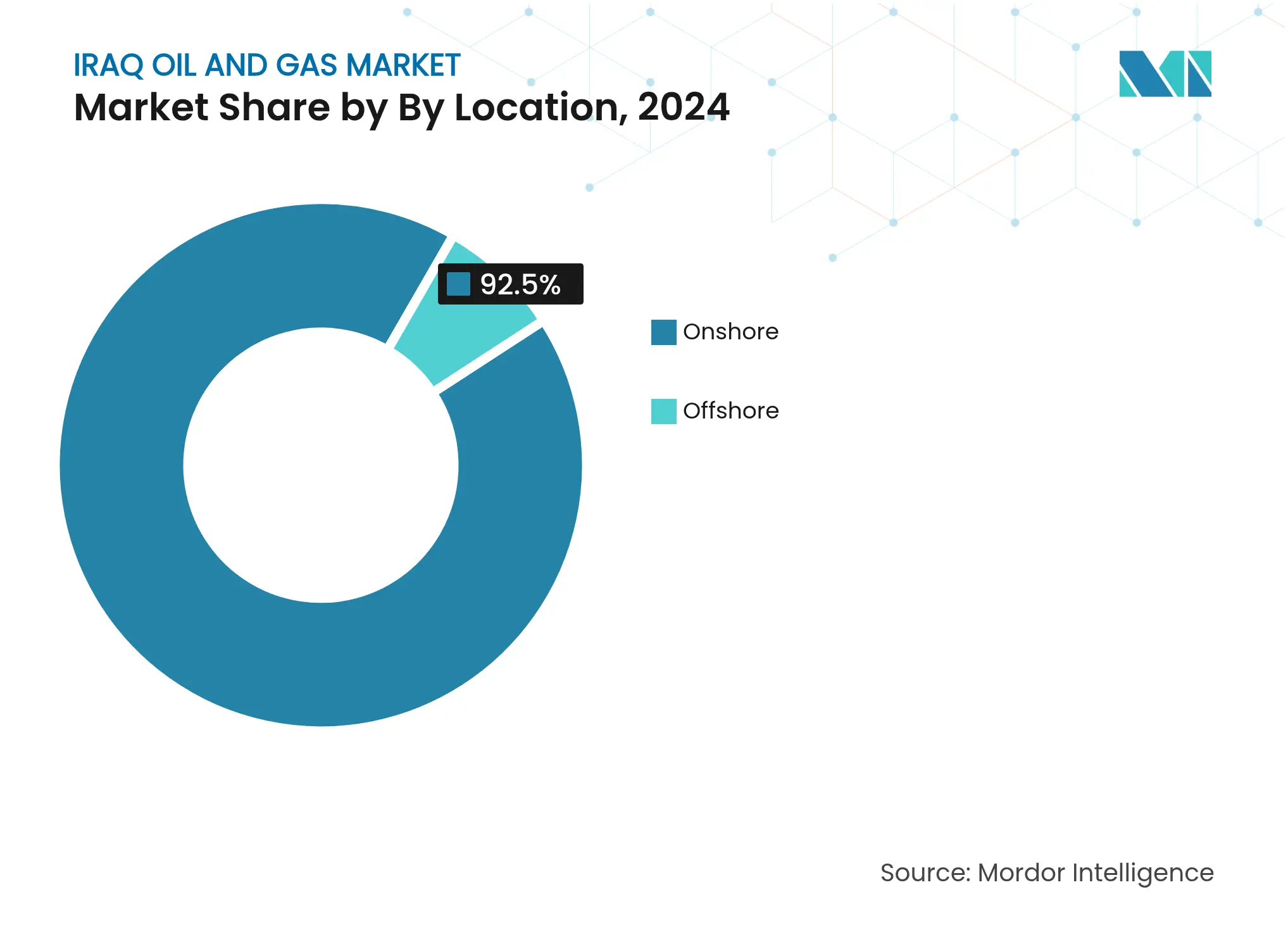

By Location: Onshore Fields Drive Growth Despite Offshore Potential

Onshore assets in Basra, Maysan, and Kirkuk accounted for 92.5% of national output in 2024 and continue to anchor the size of the Iraq oil and gas market as mature giants undergo water-injection upgrades. Offshore acreage in the Persian Gulf, however, is set to outpace onshore with a 6.9% CAGR as 12 newly awarded blocks transition into appraisal drilling. This diversification protects the Iraqi oil and gas market against surface-access limitations and offers service providers a niche in marine logistics.

As offshore projects ramp up, operators will lean on subsea tie-backs and FPSOs that complement existing southern export terminals, supporting both capital formation and technology transfer into the Iraq oil and gas market.

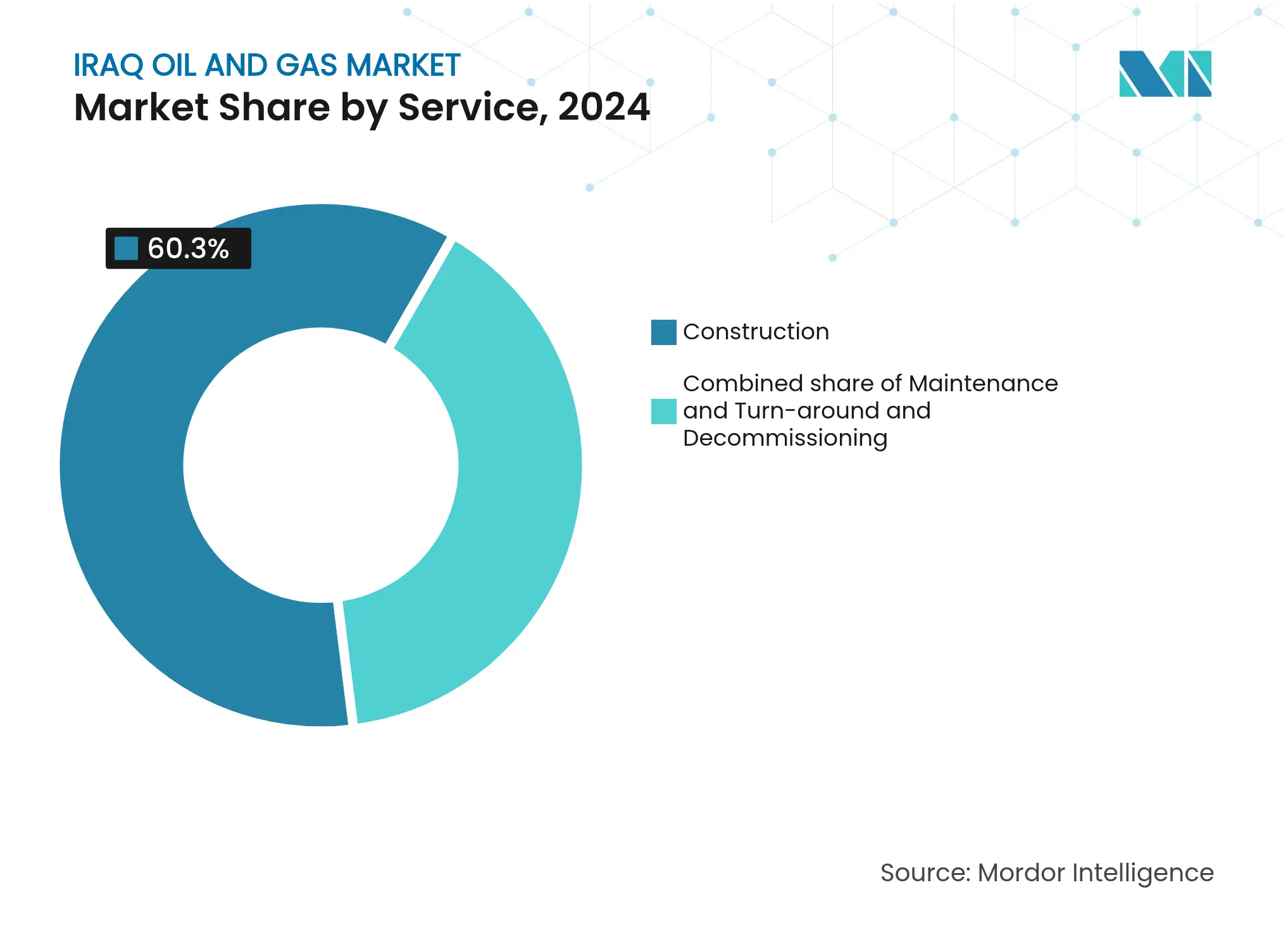

By Service: Construction Leads While Decommissioning Accelerates

Construction activities generated 60.3% of the revenue in 2024, driven by seawater injection plants, pipelines, and new processing capacity. Chinese EPCs deliver turnkey solutions that compress schedules and sustain the momentum of growth in the Iraqi oil and gas market. Decommissioning, although still emerging, is projected to post a 7.2% CAGR as wells drilled in the 1970s reach the end of their life. Baker Hughes and Weatherford are scaling plug-and-abandonment capabilities that comply with evolving environmental standards, thereby deepening their service breadth within the Iraqi oil and gas market.[3]Baker Hughes, “Well Decommissioning Contracts in Iraq,” bakerhughes.com

Lifecycle spending now spans new build, maintenance, and retirement, signaling the sector’s transition into a mature phase where value migrates toward optimization and environmental stewardship within the Iraq oil and gas industry.

Note: Segment shares of all individual segments available upon report purchase

Southern governorates produced almost 70% of national crude in 2024, with Basra alone exceeding 2.5 mbpd through BP–CNPC, Lukoil–Inpex, and ExxonMobil–PetroChina ventures.[4]BP plc, “Rumaila Operating Report 2024,” bp.com Access to the Al-Basra Oil Terminal and multiple single-point moorings translates into lower evacuation costs, reinforcing the South’s dominance in the Iraq oil and gas market. Completion of the Common Seawater Supply Project is poised to lift southern plateau capacity by another 1 mbpd by 2028, lengthening asset life and stabilizing output profiles.

Northern Iraq contributes roughly 450,000 barrels per day (kbpd) from assets such as Kirkuk, Taq Taq, and Shaikan; however, pipeline outages have curtailed export flexibility since 2023. BP’s redevelopment plan could double Kirkuk capacity over 15 years, while the potential resolution of the Iraq–Turkey pipeline arbitration would remove a major volume bottleneck. Gas resources in the Kurdistan Region remain underutilized, suggesting potential upside for integrated gas-to-power ventures that could diversify the Iraqi oil and gas market.

Central governorates host several undeveloped discoveries totaling more than 5 billion barrels. Security and infrastructure shortfalls have limited progress to date, but tender rounds scheduled for 2025 aim to attract new capital with profit-sharing terms. Proximity to domestic refineries and demand centers offers a strategic foothold for operators seeking balanced exposure across the Iraq oil and gas market.

Market Concentration

International oil companies pair Western technology with Asian financing in high-stakes upstream projects, giving consortia such as BP–CNPC and TotalEnergies–QatarEnergy a significant competitive advantage in reservoir management and integrated gas schemes. Chinese EPC contractors, such as CPECC, win the bulk of infrastructure contracts by bundling engineering, procurement, and construction at competitive prices that smaller rivals struggle to match. This two-tier structure shapes procurement patterns throughout the Iraq oil and gas market.

Service majors Schlumberger, Halliburton, and Baker Hughes compete aggressively in high-end segments, including digital oilfield solutions, complex completions, and plug-and-abandonment work. Their proprietary technologies deliver performance enhancements that outweigh higher unit costs, appealing to operators seeking to maximize ultimate recovery in the Iraqi oil and gas market. Niche players offering artificial lift, corrosion management, or subsea hardware exploit specialized gaps left by larger firms, preserving a moderately fragmented landscape.

Offshore exploration, unconventional resource appraisal, and gas-to-power integration represent emerging arenas where new entrants could secure anchor positions if they can marshal capital and expertise. The growing importance of ESG metrics also tilts contract awards toward contractors with low-carbon credentials, reinforcing the shift toward integrated and sustainable solutions throughout the Iraq oil and gas industry.

*Disclaimer: Major Players sorted in no particular order

1. Introduction

2. Research Methodology

3. Executive Summary

4. Market Landscape

5. Market Size & Growth Forecasts

6. Competitive Landscape

7. Market Opportunities & Future Outlook

The Iraq oil and gas market report includes:

Unlocking Market Potential for Solid-State Transformers

3 Min Read

When decisions matter, industry leaders turn to our analysts. Let’s talk.