Iran Agriculture Market Size and Share

Iran Agriculture Market Analysis by Mordor Intelligence

The Iran agriculture market size was valued at USD 70 billion in 2025 and estimated to grow from USD 72.14 billion in 2026 to reach USD 83.92 billion by 2031, at a CAGR of 3.06% during the forecast period (2026-2031). Solid government investment, valued at USD 35 million for irrigation modernization, anchors stable expansion even as water scarcity and sanctions complicate day-to-day farming operations[1]Source: Ali Rezaei, “Water Scarcity and Modern Irrigation Adoption in Iran,” Shenasname, shenasname.ir. Cereals hold the largest Iran agriculture market share, yet decisive policy shifts now favor high-value fruits, vegetables, and specialty crops destined for export, cushioning farmers against domestic price volatility. New trade corridors negotiated with China and BRICS partners expand market reach for pistachios, saffron, and fresh citrus, creating fresh income streams that reinforce rural livelihoods. Fragmented farm structures limit large-scale mechanization, but targeted subsidy schemes, technology transfers, and precision irrigation are steadily narrowing productivity gaps.

Key Report Takeaways

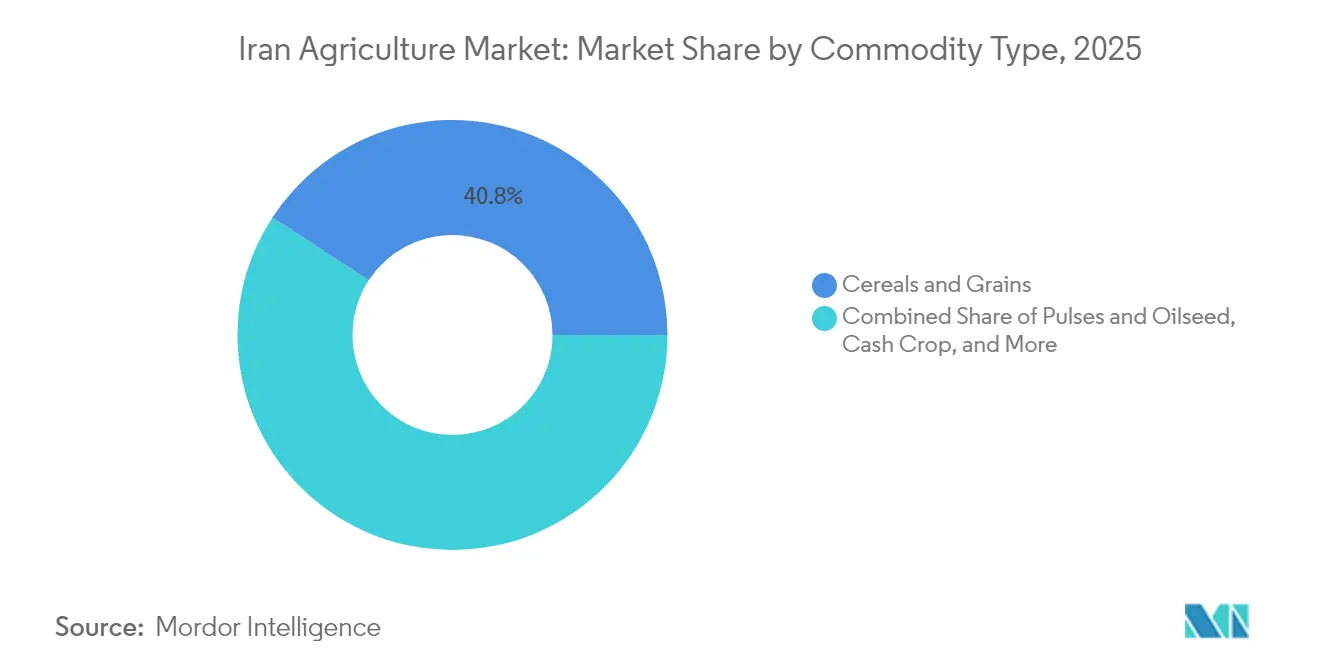

- By commodity type, cereals and grains led with 40.80% of Iran agriculture market share in 2025, while fruits and vegetables are forecast to expand at a 5.48% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Iran Agriculture Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Digital irrigation and on-farm IoT adoption | +0.8% | National, concentrated in Fars and Tehran provinces | Medium term (2-4 years) |

| Expansion of domestic high-tech greenhouses | +0.6% | National, with early gains in Kerman and Yazd | Long term (≥ 4 years) |

| Government wheat-price guarantees and input subsidies | +0.4% | National, the strongest impact in grain-producing regions | Short term (≤ 2 years) |

| Growing demand for high-value horticulture exports | +0.7% | National, export-oriented provinces | Medium term (2-4 years) |

| Rise of agrifood e-commerce platforms | +0.3% | National, urban-adjacent agricultural zones | Short term (≤ 2 years) |

| Ag-startup financing via National Innovation Fund | +0.2% | National, technology hubs in major cities | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Digital Irrigation and On-Farm IoT Adoption

Water scarcity has catalyzed the rapid adoption of precision irrigation technologies, with the government allocating USD 35 million specifically for modern irrigation infrastructure in 2024. Government mandates requiring smart water meters on all legal wells are accelerating farmer adoption, creating a USD 200-300 million annual market for irrigation technology providers. The convergence of water scarcity and digital solutions positions Iran as a testing ground for next-generation precision agriculture technologies adapted to arid climates.

Expansion of Domestic High-Tech Greenhouses

Iran's greenhouse sector has emerged as a critical component of agricultural modernization, with controlled environment agriculture offering yields up to 10 times higher than traditional field cultivation while using 90% less water[2]Source: Hossein Darvish, “Greenhouse Performance under Semi-Arid Conditions,” MDPI, mdpi.com. The sector benefits from Iran's abundant natural gas resources, providing cost-effective heating for year-round production cycles that can generate 3-4 harvests annually compared to single outdoor seasons. Integration of AI-powered environmental control systems enables precision management of temperature, humidity, and CO2 levels to optimize plant growth and resource utilization.

Government Wheat-Price Guarantees and Input Subsidies

Iran's agricultural subsidy framework provides critical income stability for grain producers through guaranteed minimum prices and input cost support, with the 2024 budget allocating substantial resources for wheat procurement at predetermined rates. The government's commitment to purchasing domestic wheat at guaranteed prices shields farmers from volatile international commodity markets while supporting food security objectives through strategic grain reserves. Fertilizer subsidies have become increasingly important as international sanctions limit access to imported agricultural inputs, with domestic production facilities receiving government support to maintain farmer access to essential nutrients.

Growing Demand for High-Value Horticulture Exports

Iran's strategic shift toward high-value agricultural exports has accelerated following recent trade agreements, particularly the landmark approval for citrus exports to China, which opens access to a market consuming over 70 million tons of citrus annually[3]Source: Zahra Vakili, “Post-Harvest Losses in Iranian Horticulture,” Acta Horticulturae, actahort.org. Post-harvest technology investments, including advanced drying systems for pistachios that reduce processing time by 40% while maintaining product quality, are enhancing export competitiveness. Trade facilitation through digital platforms and improved logistics networks are reducing export transaction costs and enabling smaller producers to access international markets.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Severe aquifer depletion and water-bankruptcy zones | -1.2% | National, critical in the central and southern regions | Long term (≥ 4 years) |

| Sanctions restricting access to farm inputs | -0.7% | National, affecting technology and input imports | Medium term (2-4 years) |

| Fragmented land holdings limiting mechanization scale-up | -0.8% | National, particularly affecting smallholder regions | Long term (≥ 4 years) |

| Post-harvest loss due to cold-chain gaps | -0.5% | National, concentrated in fruit and vegetable regions | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Severe Aquifer Depletion and Water-Bankruptcy Zones

Iran confronts an unprecedented water crisis with major reservoirs operating at critically low levels, including the Amir Kabir and Latyan dams serving Tehran at only 13% capacity, forcing consideration of emergency water rationing measures. The crisis has forced fundamental changes in cropping patterns, with farmers abandoning water-intensive crops and shifting toward drought-resistant varieties, though this transition constrains overall agricultural output. Emergency measures, including deep well drilling, risk contaminating remaining groundwater supplies, creating potential public health disasters that could further destabilize rural agricultural communities.

Fragmented Land Holdings Limiting Mechanization Scale-Up

Iran's agricultural sector is characterized by extreme land fragmentation, with average farm sizes below 2 hectares creating fundamental barriers to mechanization adoption and economies of scale realization. Research in Fars Province indicates that household income, per capita arable land, and family size significantly influence fragmentation patterns, with social and cultural factors often preventing consolidation efforts.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Commodity Type: Cereals Lead While Fruits Accelerate

Cereals and Grains commanded the largest market share at 40.80% in 2025, reflecting Iran's strategic emphasis on food security through domestic grain production supported by government price guarantees and input subsidies. The segment benefits from established infrastructure and farmer expertise, though productivity constraints from aging machinery and water limitations constrain growth potential.

Fruits and Vegetables represent the fastest-growing segment with a 5.48% CAGR through 2031, driven by export market expansion and higher profit margins that incentivize farmer adoption despite increased production complexity. Recent market access agreements with China for citrus exports and strengthened trade relationships with BRICS partners are accelerating this segment's growth trajectory.

Geography Analysis

Iran's agricultural geography reflects diverse climatic zones and water availability patterns that fundamentally shape production capabilities and market dynamics across the country. The northern provinces, including Mazandaran and Gilan, benefit from higher precipitation levels and more favorable growing conditions, supporting rice production and diverse horticultural crops despite facing projected temperature increases of 0.82-1.1°C and precipitation decreases of 7.1-31.3 mm through 2050.

Central provinces, particularly Fars and Isfahan, serve as major grain production centers with mechanization levels significantly above national averages, though they face acute water stress from depleted aquifers and reduced river flows. The Zayandeh Rud basin in central Iran exemplifies the challenges facing agricultural regions, with population growth from 420,000 in 1956 to 2.3 million by 2000, creating unsustainable water demand that threatens long-term agricultural viability.

Southern and eastern provinces are adapting to extreme water scarcity through the adoption of drought-resistant crops and advanced irrigation technologies, with some regions exploring fog water harvesting as an alternative water source capable of yielding 25-65 liters per square meter daily. Climate change projections indicate southern regions may face extreme heat and drought conditions that could force fundamental shifts in agricultural land use, while northern areas might experience increased precipitation and flood risks requiring adaptive management strategies.

Regulatory Landscape

Iran's agricultural sector is primarily regulated by the Ministry of Jihad-e-Agriculture (MAJ), with the Seed and Seedling Registration and Certification Research Institute (SSRCRI) overseeing seed and seedling registration, certification, and standard compliance under the Act on Plant Varieties Registration, Control and Certification of Seeds and Seedlings (2003). Biosafety oversight, including governance for living modified organisms in agriculture, is handled through the countrys GMO regulatory framework referenced by international regulatory repositories.

Trade-facing rules have tightened around water and perishability management, while easing select import constraints tied to foreign exchange availability. In April 2026, Customs of the Islamic Republic of Iran began enforcing a virtual water tariff on water-intensive agricultural and food exports under Article 38 of the Seventh Five-Year Development Plan, set at 1% of export value with scheduled annual increases. In February 2026, MAJ issued a directive to accelerate customs clearance for 16 perishable agricultural tariff codes (fast-track clearance), and in July 2026 the ministry announced liberalization for certain agricultural imports using private currency sources, expanding access for products previously restricted when importers secure their own foreign exchange.

Value Chain Analysis

Iran's agriculture value chain covers input supply (seed systems, fertilizers, pesticides, machinery, irrigation equipment), primary production across diverse agro-climatic zones, aggregation and first-stage processing (milling, oil crushing, packing, drying), and domestic wholesale and retail plus export logistics. State policy and procurement mechanisms remain central in staples, while higher-value horticulture increasingly depends on private aggregators, packhouses, and export traders that can meet destination protocols and cold-treatment requirements.

The main frictions between farmgate and markets stem from fragmented landholdings (often below 2 hectares), which constrain mechanization economics, and from aging equipment plus irrigation constraints that reduce yield stability, reflected in cereal production pressure (2025 cereal output estimated at 19.5 million tonnes, more than 10% below the five-year average amid dry conditions). Post-harvest losses and limited refrigerated transport capacity continue to cap realized value in fruits and vegetables, while sanctions-linked import frictions and quota-based input distribution (notably pesticides) can disrupt seasonal farm operations. Public spending has targeted enabling links in the chain, including mechanization and agro-industries investment (about USD 360 million committed between March 2024 and January 2025) and the Seventh Five-Year Development Plan focus on optimal cropping patterns and water efficiency.

Market Opportunities and Future Outlook

A near-term opportunity set is forming around productivity-led growth, rather than land expansion, anchored by named national programs and measured output outcomes. In February 2026, the Ministry of Agriculture Jihad reported open-field vegetable and horticultural production of 26.2 million tons for the 1403-1404 agricultural year, with a 5% output lift over the 10-year average despite a 22% reduction in cultivated area. This performance strengthens the case for agronomy improvements, protected cultivation, and precision irrigation in water-stressed provinces.

Technology and service whitespace remains concentrated in smart irrigation, extension, and export-enabling post-harvest systems. The ministry is running 110 pilot smart irrigation projects covering about 10,000 hectares (February 2026), and is scaling a national demonstration-farm network, launching 2,000 model farms focused on five strategic products (May 2026) while expanding the approach to 40,000 model farms (April 2026). Export monetization also pulls demand for grading, packing, cold chain, and standards compliance, supported by customs-reported agricultural exports of USD 5.2 billion for the 1403 calendar year ending March 2025 (up 29% year over year). Institutional mechanisms such as the Iran Commodity Exchange further support standardized trade in crops like saffron and dates, linking farm output to more transparent pricing and tradable specifications.

Recent Industry Developments

- July 2026: Iran's Ministry of Jihad-e-Agriculture announced a policy change to liberalize imports of certain agricultural commodities using private currency sources. The move allows importers with their own foreign exchange to bring in items that had faced restrictions, shifting part of import execution away from state FX allocation. It can change competitive dynamics for traders, distributors, and downstream buyers that rely on imported produce or specialty items.

- June 2026: The Government of Iran inaugurated 2,209 agricultural projects across multiple provinces, with total investment reported above 30 trillion tomans. The breadth of project commissioning points to continued capital deployment across irrigation, production, and agro-industrial infrastructure, which can affect farm productivity and first-stage processing capacity.

- December 2025: MAPNA Group launched the AGREED project at the Genaveh Combined Cycle Power Plant, combining a 660 kW solar installation with hydroponic greenhouse farming. This integrated energy-agriculture model supports controlled-environment cultivation and offers a pathway to reduce greenhouse operators' exposure to power supply variability.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this methodology, the Iran agriculture market is defined as the value of domestically produced agricultural output measured at the farm gate and through first-stage processing, converted to USD for the base year.

Scope exclusions: Fully processed foods beyond the primary stage, craft beverages, and tobacco are excluded from the market value.

Segmentation Overview

- By Commodity Type

- Cereals and Grains

- Production Analysis (Volume)

- Consumption Analysis (Value and Volume)

- Export Analysis (Value and Volume)

- Import Analysis (Value and Volume)

- Price Trend Analysis

- Pulses and Oilseed

- Production Analysis (Volume)

- Consumption Analysis (Value and Volume)

- Export Analysis (Value and Volume)

- Import Analysis (Value and Volume)

- Price Trend Analysis

- Fruits and Vegetables

- Production Analysis (Volume)

- Consumption Analysis (Value and Volume)

- Export Analysis (Value and Volume)

- Import Analysis (Value and Volume)

- Price Trend Analysis

- Cash Crop

- Production Analysis (Volume)

- Consumption Analysis (Value and Volume)

- Export Analysis (Value and Volume)

- Import Analysis (Value and Volume)

- Price Trend Analysis

- Cereals and Grains

Data Sources, Market Sizing, and Validation

Desk Research

Desk work started with building a clean fact base for Iran agriculture using public series such as FAOSTAT, the World Bank national accounts indicators, UN Comtrade trade statistics, and national statistics releases and ministry publications where available. We also reviewed materials from bodies such as the Islamic Republic of Iran Customs Administration, selected peer-reviewed journals on Iranian agronomy and water use, and reputable press coverage to understand seasonality, policy shifts, and supply constraints.

To translate these signals into a consistent value view, company filings and investor presentations were used for directional checks on pricing, processing yields, and procurement patterns. In a few places, we also relied on paid subscription data for company financials and news context, and another paid source for shipment-level import and export data, mainly to cross-check trade-linked commodities and currency timing. The desk sources listed above are illustrative only, and many other public and paid references were used for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary work focused on validating what is counted at farm gate versus first-stage processing, and on sense-checking unit prices, yield changes, and channel margins that are not always visible in public series. We spoke with a mix of growers, processors, traders, input distributors, and sector specialists across the main producing and consuming pockets, then used follow-up questions to close gaps where desk numbers were inconsistent.

Because agriculture can move quickly with weather and policy, assumptions were rechecked for the current year through short surveys, and the final inputs were aligned to a common USD conversion timing before the totals were locked.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 34% | CXOs: 14% | APAC: 37% |

| Mid tier: 51% | Functional/Unit leaders: 36% | EMEA: 37% |

| Smaller Players: 15% | Managers: 50% | Americas: 26% |

Market-Sizing & Forecasting

The size model was built using a top-down approach where national production and trade series are reconstructed into a domestic supply picture, which is then valued using farm-gate and first-stage price benchmarks. After that, selective bottom-up checks were applied using sampled price-by-volume builds from key commodities and processor throughput discussions, and the totals were adjusted when the two views did not align.

A few practical inputs that shaped the model included cultivated area and yield trends for key crops, livestock headcount and output indicators, import and export volumes for trade-linked items, observed farm-gate and primary processing price movements, and water availability and policy signals that influence planting decisions. Where a bottom-up check could not cover smaller crops or informal trade fully, gap factors were applied based on expert inputs and then tested against national accounts and trade balances.

For forecasting, scenario analysis was used, because the sector is sensitive to rainfall variability, input availability, and policy on subsidies and trade controls. Each scenario was anchored to expert expectations on yields and planted area, then rolled into a base-case outlook with transparent assumptions that can be revisited each year.

Data Validation & Update Cycle

Outputs were validated through multiple passes, starting with internal consistency checks between production, trade, and implied domestic availability, and then moving to reasonableness checks on price and value growth versus known sector events. If a commodity line showed an unusual jump, the underlying drivers were reopened, and targeted re-contacts were triggered to confirm whether the change was real or a data timing issue.

Before sign-off, the full model is reviewed by another analyst who checks formulas, unit conversions, and whether exclusions are being applied consistently across all lines. The report is refreshed annually, and interim updates are made when there are material changes such as major policy revisions, currency shifts, or severe weather impacts. Right before delivery, a final pass is completed so clients receive the most current view available.

Mordor Intelligence's Iran Agricultural Sector Analysis Market Estimate Compared With Other Published Estimates

Published market values for Iran agriculture do not always match, because different studies count different parts of the value chain and they also vary in the way they handle prices, currency conversion timing, and updates after policy or weather shocks.

Some estimates extend into broader agribusiness activity and include downstream food processing, distribution, or retail margins, which can lift the number quickly. In Mordor Intelligence, the total is limited to farm-gate value plus first-stage processing for domestic crop, livestock, fishery, and forestry output, with fully processed foods beyond the primary stage, craft beverages, and tobacco kept out of scope.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 70 B (2025) | |

| Global Consultancy A | USD 11.14 B (2025) | This estimate appears to use a narrower product basket that covers selected agribusiness categories and specific regions, which can undercount the full national agriculture output that includes fisheries and forestry and the wider crop mix. |

| Sector Publisher B | USD 93.02 B (2034) | This figure is a forward-year projection for a wider agribusiness framing, and it can also reflect added value from downstream processing and distribution steps, which makes it not directly comparable to a farm-gate plus first-stage definition for a current-year baseline. |

The spread across sources is mainly explained by what parts of the chain are included and which year is being quoted, followed by pricing and currency-handling choices. By keeping the counting rule tied to observable production and trade signals and then checking prices with field inputs, the final number stays traceable to clear steps that can be repeated on the next update.

Key Questions Answered in the Report

How large is the Iran agriculture market today?

The Iran agriculture market reached USD 72.14 billion in 2026 and is forecast to reach USD 83.92 billion by 2031, expanding at a 3.06% CAGR.

Which commodity holds the largest share within the Iran agriculture market?

Cereals and grains led with 40.80% of Iran agriculture market share in 2025 due to government price guarantees and input subsidies.

What is the fastest-growing segment in Iran agriculture market?

Fruits and vegetables are projected to grow at a 5.48% CAGR through 2031, supported by greenhouse expansion and new export agreements.

Why are high-tech greenhouses important for Iran agriculture market?

Greenhouses boost yield up to ten times, cut water use by 90%, and enable year-round production, making them central to export growth and water conservation goals.

How do water shortages affect Iran agriculture market growth?

Aquifer depletion and reservoir shortages exert a −1.2% drag on CAGR, forcing crop shifts, irrigation upgrades, and stricter groundwater regulations.

What role do subsidies play in Iran’s cereal production?

Guaranteed wheat procurement prices and fertilizer subsidies stabilize farmer income, support domestic grain reserves, and maintain cereal dominance despite resource constraints.

Page last updated on: