Egypt Agriculture Market Analysis by Mordor Intelligence

The Egypt agriculture market size is projected to expand from USD 6.40 billion in 2025 and USD 6.72 billion in 2026 to USD 8.41 billion by 2031, registering a CAGR of 4.59% between 2026 to 2031. Sustained export momentum in citrus, grapes, and potatoes, rising private investment in drip irrigation, and government procurement guarantees for wheat, cotton, and sugarcane underpin this expansion of the Egypt agriculture market. Voluntary carbon-credit revenue, blended-finance vehicles, and duty-free access to Brazil, Argentina, Paraguay, and Uruguay through the Egypt-Mercosur framework are broadening profit pools, even as climate-driven water scarcity and freight cost spikes constrain margins. Precision irrigation programs financed by a USD 500 million World Bank loan are cutting on-farm water use by up to 40%, while the Grand Ethiopian Renaissance Dam’s downstream flow reductions force farmers to switch from rice to less water-intensive crops. Freight volatility following the 2024 Red Sea attacks highlighted the need for resilient logistics networks, prompting vertically integrated exporters to build cold-chain and overland corridors that protect perishables and stabilize the Egypt agriculture market.

Key Report Takeaways

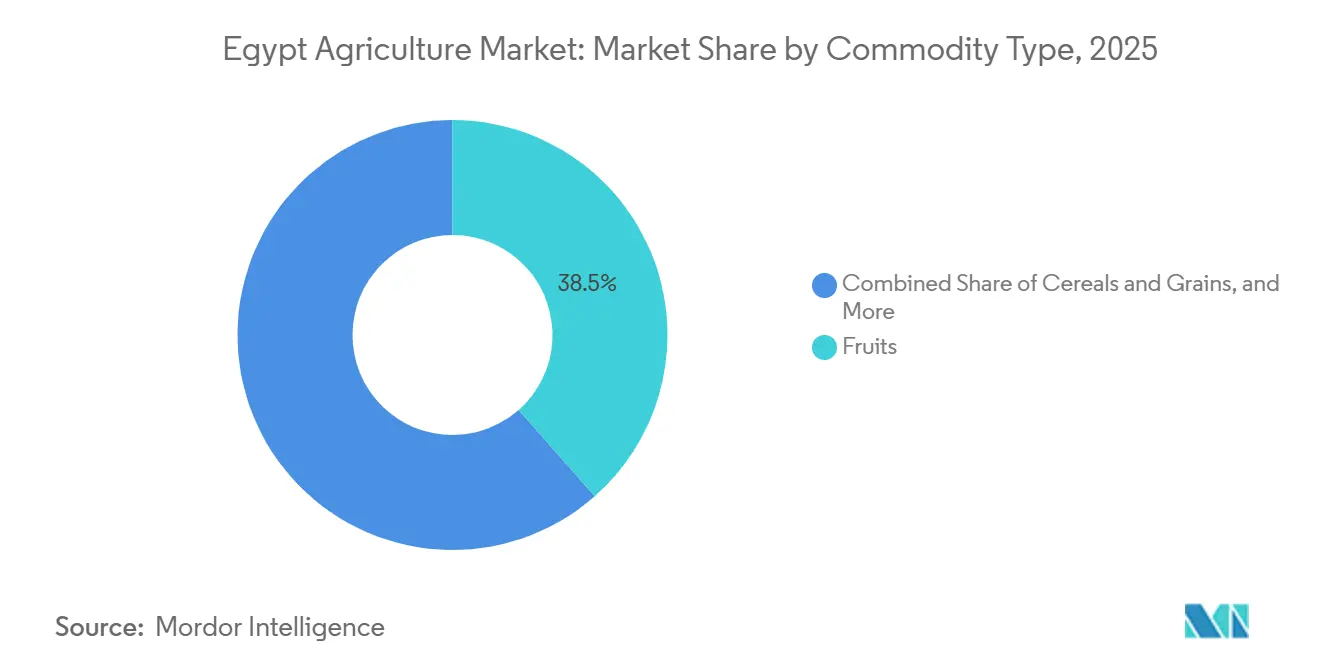

- By commodity type, fruits led with a 38.5% Egypt agriculture market share in 2025, while oilseeds and pulses posted the highest projected 5.0% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Egypt Agriculture Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Population-driven calorie demand growth | +0.8% | Nationwide, concentrated in Greater Cairo, Alexandria, and Giza | Medium term (2-4 years) |

| Expansion of agriculture export preferential trade agreements | +0.6% | Nationwide gains to the European Union, Southern Common Market, European Free Trade Association, and Common Market for Eastern and Southern Africa | Long term (≥ 4 years) |

| Accelerating adoption of precision irrigation systems | +0.5% | Nile Delta, Beheira, Dakahlia, and desert reclamation zones | Medium term (2-4 years) |

| Rise of agriculture focused blended finance funds | +0.3% | Early traction in Upper Egypt and Minya | Long term (≥ 4 years) |

| Carbon-credit monetization of regenerative acreage | +0.3% | Fayoum, New Valley, and desert reclamation zones | Long term (≥ 4 years) |

| Blockchain-enabled commodity tokenization | +0.2% | Pilot stage in Alexandria and Damietta ports | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Population-Driven Calorie Demand Growth

Wheat has been a vital food staple in Egypt for centuries and remains one of the key crops for food security in the country. It currently accounts for one-third of the average Egyptian's daily calorie intake. The crop contributes approximately 10% to the total value of agricultural production and around 20% of all agricultural imports, highlighting the significant food security challenges faced by the country[1]Source: International Center for Agricultural Research in the Dry Areas (ICARDA), "Political Economy of the Wheat Sector in Egypt: Seed Systems, Varietal Adoption, and Impacts," icarda.org. The subsidized baladi bread program, benefiting 70 million people, sustains a consistent structural demand for cereals. Rising urban incomes are driving dietary changes, with increased consumption of poultry and aquaculture. This has led to soybean meal inclusion rates of 19.4% in poultry feed and up to 30% in aquaculture feed. These dietary trends directly link oilseed imports to protein supply chains, ensuring that improvements in yield contribute significantly to the growth of Egypt's agricultural market. Additionally, the reliance on imports highlights the importance of global trade partnerships and the need for strategic investments in domestic agricultural productivity to reduce dependency on external sources.

Expansion of Agriculture Export Preferential Trade Agreements

Preferential agreements facilitated USD 10.6 billion in agricultural exports in 2025, representing a 21% year-on-year increase. The Southern Common Market agreement, finalized in 2024, allows tariff-free access for Egyptian citrus, grapes, and strawberries to four South American countries, which collectively import over 4 million metric tons of fresh produce annually. This agreement significantly enhances market penetration opportunities for Egyptian exporters, enabling them to compete more effectively in these high-demand markets. Additional concessions under the European Free Trade Association agreement and the long-standing European Union Association Agreement reduce landed costs by 8% to 15%, thereby increasing addressable demand and supporting export-driven value growth in the Egypt agriculture market.

Accelerating Adoption of Precision Irrigation Systems

A USD 500 million World Bank modernization loan, approved in 2024, supports the conversion from drip and sprinkler irrigation systems to more efficient systems on 500,000 feddans in the Nile Delta[2]Source: World Bank Group, “Egypt Water Resources and Irrigation Modernization Project,” worldbank.org. The International Fund for Agricultural Development complements this with a USD 52.8 million climate-resilient agriculture facility targeting smallholders in Beheira, Dakahlia, and Kafr El Sheikh. Al Dahra Holding demonstrated 40% water savings and 18% yield gains on 1,500 acres of sesame using Dragon Line drip technology, providing a compelling commercial case for rapid diffusion. With the Ministry of Agriculture and Land Reclamation mandating drip irrigation on all new acreage, precision systems are set to become the agronomic baseline for the Egypt agriculture market.

Rise of Agriculture Focused Blended Finance Funds

Blended finance operates by strategically utilizing concessional public funds, such as International Fund for Agricultural Development (IFAD) loans and grants, to mitigate risks associated with investments that commercial lenders may deem too high, particularly those involving small-scale farmers and agribusinesses. This approach has enabled greater access to financial resources for these entities, fostering their growth and resilience. The International Finance Corporation’s equity investment in Raya Foods in 2024 supports the establishment of a USD 40 million freeze-dried facility, adding 50,000 tons of processing capacity. This facility is projected to enhance value addition and improve supply chain efficiency in the agriculture sector. By integrating concessional capital with commercial returns, these financial structures reduce the weighted average cost of capital, promoting investment in crushing plants, cold-chain infrastructure, and regenerative farming practices. This, in turn, supports the growth of the agriculture market in Egypt.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Climate-induced water-scarcity stress | -0.6% | Nile Delta, Fayoum, Minya, and Upper Egypt | Short term (≤ 2 years) |

| Trade-route disruptions and freight spikes | -0.5% | Nationwide, acute for Alexandria, Damietta, and Port Said exporters | Short term (≤ 2 years) |

| Soil salinity creep in reclaimed desert lands | -0.4% | Toshka, New Delta, and Sinai reclamation zones | Medium term (2-4 years) |

| Limited availability of agriculture-specific green hydrogen | -0.2% | Concentrated in Suez Canal Economic Zone | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Climate-Induced Water-Scarcity Stress

Renewable water availability is currently at 560 cubic meters per capita, significantly below the United Nations' scarcity threshold of 1,000 cubic meters. This limited water availability poses a significant challenge to agricultural sustainability in the region. The initial filling of the Grand Ethiopian Renaissance Dam in 2024 reduced Nile flows by 10 to 15%, compelling farmers in Minya and Aswan to shift from rice cultivation to wheat and maize, which are less water-intensive crops. Government-imposed rice acreage limits of 1.1 million feddans, combined with saltwater intrusion in the Nile Delta, have further reduced the production of Egypt's most water-intensive crop. These measures aim to conserve water resources but have also impacted the agricultural output and income of farmers. Although drip irrigation has helped mitigate some losses, its uneven adoption among smallholders continues to hinder short-term growth prospects, highlighting the need for broader implementation and support for sustainable farming practices.

Soil Salinity Creep in Reclaimed Desert Lands

Salinity impacts approximately 35% of cultivated land, with Toshka reporting electrical conductivity exceeding 4 deciSiemens per meter in 20% of plots[3]Source: Ministry of Agriculture and Land Reclamation Egypt, “Agricultural Development Strategy 2024-2030,” agr.gov.eg. Reclamation efforts require five to eight years, as farmers must leach salts using 1.5 to 2 times the standard water application, which conflicts with water conservation mandates. This process is labor-intensive and requires significant resources, further complicating efforts to achieve timely reclamation. While organic matter amendments and gypsum provide some relief by improving soil structure and reducing salinity levels, financial constraints hinder widespread adoption. This delays the anticipated yield improvements from the government’s 3.5 million feddan expansion program in 2023, thereby moderating growth in the Egyptian agriculture market. Additionally, the lack of adequate infrastructure and technical support exacerbates the challenges faced by farmers in addressing salinity issues effectively.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Commodity Type: Fruits Exports Anchor Value Growth

Fruits generated 38.5% of the Egypt agriculture market share in 2025, underpinned by 3.8 million metric tons of orange output and 2.1 million metric tons of citrus exports valued at USD 1.9 billion[4]Source: Food and Agriculture Organization of the United Nations Statistics, “Egypt Agricultural Production Statistics 2024,” fao.org. Grapes reached 1.8 million tons and strawberries 700,000 metric tons, while citrus supplied more than 50 international destinations during Europe’s off-season. Duty-free quotas from the European Union, Southern Common Market, and European Free Trade Association shave 8 to 15% off landed costs, sharpening competitiveness. Cold-chain upgrades such as Raya Foods’ 25,000-square-meter freeze-dried plant add 50,000 metric tons of processing capacity in 2024, extend shelf life, and reduce post-harvest losses to 10%. These factors collectively secure horticulture’s status as the dominant value generator in the Egypt agriculture market.

Oilseeds and pulses are the fastest-growing segment, projected to expand at a 5.0% CAGR through 2031. Al Dahra Holding’s sesame trials recorded 18% yield gains under zero-tillage and drip irrigation in desert zones, surpassing the Nile Delta in oilseed viability. Government tenders in January 2025 secured 30,000 metric tons of crude soybean oil and 10,000 metric tons of sunflower oil, confirming robust downstream demand. Capital inflows into crushing and feed plants position oilseeds to deliver the highest incremental revenue to the Egypt agriculture market.

Geography Analysis

The Nile Delta governorates of Beheira, Dakahlia, and Kafr El Sheikh are renowned for their intensive production of wheat, rice, and vegetables on fertile alluvial soils. However, Mediterranean saltwater intrusion affects 15,000 to 20,000 feddans annually, necessitating the use of salt-tolerant cultivars and precision leaching techniques to mitigate soil degradation. To address water scarcity and sustain agricultural productivity, drip and sprinkler irrigation retrofits, funded by the World Bank, aim to cover 500,000 feddans. These retrofits are projected to achieve water savings of 30% to 40%, ensuring the maintenance of agricultural yields despite increasing water stress conditions in the region.

Upper Egypt governorates, including Minya, Aswan, and Sohag, focus on sugarcane, cotton, and aromatic herbs. Flow reductions from the Grand Ethiopian Renaissance Dam resulted in a 20% decrease in rice acreage by 2025, prompting growers to switch to maize and wheat. SEKEM’s pilot in Minya converted 1,300 farmers to biodynamic practices, delivering 15% input savings and a 20% organic price premium that bolsters household income and diversifies output quality within the Egypt agriculture market.

The desert reclamation zones of Toshka, the New Delta, and Sinai represent the growth frontier, with 3.5 million feddans slated for cultivation. Toshka targets 540,000 feddans yet grapples with high salinity, and 20% of surveyed plots exceed 4 deciSiemens per meter. Al Dahra Holding’s 147,000 acre footprint uses zero-tillage and Dragon Line drip irrigation to overcome these constraints, recording 18% sesame yield gains in 2024. Proximity to Alexandria and Damietta ports positions the New Delta to become a future export hub for citrus and grapes, once irrigation infrastructure is fully commissioned, broadening regional gains for the Egypt agriculture market.

Competitive Landscape

Smallholders managing plots of one to five feddans constitute nearly 70% of the cultivated area. In contrast, large vertically integrated companies, including Al Dahra Holding LLC, Wadi Holdings S.A.E., PICO for Modern Agriculture Co. S.A.E., and SEKEM Holding SE for Modern Agriculture, dominate export logistics and processing activities. Al Dahra invested USD 30 million in 2024 to expand its operations to 147,000 acres, establishing itself as Egypt’s largest private wheat producer with 450,000 metric tons delivered over three years and achieving a top-ten position in citrus exports.

Strategic differentiation centers on long-term supply contracts, precision irrigation, and regenerative farming that qualify for future carbon credits. Raya Foods’ USD 40 million freeze-dried facility aims to cut post-harvest losses and target premium institutional buyers willing to pay 30 to 40% above commodity benchmarks. Oilseed crushing offers white-space upside as poultry and aquaculture feed demand accelerates, while blockchain tokenization pilots reduce settlement times and financing costs for grain exporters once regulatory clarity emerges.

Smaller cooperatives utilize blended finance to consolidate volumes and engage with bulk buyers, reducing the weighted average cost of capital and enhancing competitiveness. By pooling resources, these cooperatives can negotiate more favorable terms with buyers and suppliers, thereby improving their market position. Government procurement programs ensure minimum prices for wheat, cotton, and sugarcane, providing stability but reducing incentives for efficiency improvements. While these programs provide a safety net for farmers, they may also discourage innovation and hinder cost optimization. Companies excelling in precision irrigation, carbon-credit monetization, and diversified trade corridors are well-positioned to outperform competitors and achieve significant gains in the Egypt agriculture market. These firms utilize advanced technologies and sustainable practices to boost productivity and expand their market reach, thereby securing a competitive edge.

Recent Industry Developments

- November 2025: Egypt and Poland's Feerum have established Feerum Egypt, a joint venture focused on manufacturing grain silos locally in East Port Said. This initiative aims to enhance Egypt's food security by reducing dependence on imports, generating employment opportunities, and achieving 80% local production within three years. Supported by substantial investment, this project aligns with Egypt's national objectives to localize industries, develop the Suez Canal Economic Zone, and strengthen strategic grain reserves.

- November 2025: Novastar Ventures, a venture capital and impact investing firm with a focus on Africa, has allocated USD 50 million to support climate-tech startups in the agriculture sector in Egypt. This allocation is part of a larger USD 200 million fund. The funding originates from the firm's Third Investment Fund, with a substantial equity investment approved by the Green Climate Fund (GCF).

- October 2025: Mauritania has partnered with Egypt to enhance its cereal production, including wheat, rice, and maize, by utilizing Egypt's agricultural expertise, research, and technology. Plans include establishing a branch of the Egyptian Agricultural Research Center in Nouakchott, which will function as a regional hub for knowledge transfer. This partnership aims to improve local yields, develop crop varieties adapted to Mauritanian conditions, and reduce dependence on imported staples, thereby bolstering food security.

- June 2025: Egypt has introduced Jirian City, a new desert metropolis near Cairo, utilizing approximately 7% of its Nile water quota for urban development, luxury housing, and the expansive New Delta agricultural project. The initiative aims to increase land value and generate employment amid water scarcity and economic challenges.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines Egypt's agriculture market as the total farm-gate value, in U.S. dollars, of all domestically grown field crops, fruits, vegetables, oilseeds, pulses, and key cash crops such as cotton and sugarcane that move into either domestic supply or export channels in a given year.

Scope exclusion: livestock, aquaculture, and post-farm processing activities fall outside this boundary.

Segmentation Overview

-

By Commodity Type

-

Cereals and Grains

-

Production Analysis

- Overview

- Area Harvested and Yield

- Consumption Analysis (Value and Volume)

-

Trade Analysis (Value and Volume)

-

Import Market Analysis

- Overview

- Key Supplying Markets

-

Export Market Analysis

- Overview

- Key Destination Markets

-

Import Market Analysis

- Wholesale Price Trend Analysis and Forecast

- Seasonality Analysis

-

Production Analysis

-

Oilseeds and Pulses

-

Production Analysis

- Overview

- Area Harvested and Yield

- Consumption Analysis (Value and Volume)

-

Trade Analysis (Value and Volume)

-

Import Market Analysis

- Overview

- Key Supplying Markets

-

Export Market Analysis

- Overview

- Key Destination Markets

-

Import Market Analysis

- Wholesale Price Trend Analysis and Forecast

- Seasonality Analysis

-

Production Analysis

-

Fruits

-

Production Analysis

- Overview

- Area Harvested and Yield

- Consumption Analysis (Value and Volume)

-

Trade Analysis (Value and Volume)

-

Import Market Analysis

- Overview

- Key Supplying Markets

-

Export Market Analysis

- Overview

- Key Destination Markets

-

Import Market Analysis

- Wholesale Price Trend Analysis and Forecast

- Seasonality Analysis

-

Production Analysis

-

Vegetables

-

Production Analysis

- Overview

- Area Harvested and Yield

- Consumption Analysis (Value and Volume)

-

Trade Analysis (Value and Volume)

-

Import Market Analysis

- Overview

- Key Supplying Markets

-

Export Market Analysis

- Overview

- Key Destination Markets

-

Import Market Analysis

- Wholesale Price Trend Analysis and Forecast

- Seasonality Analysis

-

Production Analysis

-

Cash Crops

-

Production Analysis

- Overview

- Area Harvested and Yield

- Consumption Analysis (Value and Volume)

-

Trade Analysis (Value and Volume)

-

Import Market Analysis

- Overview

- Key Supplying Markets

-

Export Market Analysis

- Overview

- Key Destination Markets

-

Import Market Analysis

- Wholesale Price Trend Analysis and Forecast

- Seasonality Analysis

-

Production Analysis

-

Cereals and Grains

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed growers, export aggregators, irrigation-equipment dealers, extension officers, and input distributors across the Delta, Middle Egypt, and newly reclaimed desert zones. These conversations clarified yield ranges, typical farm-gate price premiums, and adoption timelines for water-saving technologies, allowing us to adjust secondary figures and close data gaps.

Desk Research

We began by compiling production and trade statistics from public sources such as CAPMAS, the Ministry of Agriculture and Land Reclamation, FAOSTAT, UN Comtrade, and USDA-FAS reports. Macroeconomic inputs came from the Central Bank of Egypt and the World Bank, while regional crop-price series were tracked through commodity exchanges and auction bulletins. To enrich company and supply-chain perspectives, we tapped paid datasets, notably D&B Hoovers for farm-operator financials, Dow Jones Factiva for news sentiment, and Volza for shipment micro-data. These inputs built the foundational database; however, many additional open documents, academic papers, and policy notes were reviewed for cross-checks.

Market-Sizing and Forecasting

A top-down model converts official production tonnage by crop into value using weighted average farm-gate prices, followed by regional re-allocation that mirrors harvested-area patterns. Results are stress-tested through selective bottom-up roll-ups of sampled hectare counts multiplied by localized yields and cost-inflated price quotes. Key variables like planted area shifts, yield per feddan, drip-irrigation penetration, export rebate rates, fertilizer cost inflation, and real GDP per capita feed a multivariate regression with ARIMA overlays to project 2025-2030 growth. Where bottom-up estimates diverge beyond a three-percent band, we reconcile to the more verifiable series.

Data Validation and Update Cycle

Every draft model passes two analyst reviews that flag outliers versus long-run commodity trends, neighboring-country benchmarks, and seasonality checks. We refresh figures annually, and if drought shocks, subsidy changes, or currency swings exceed preset thresholds, our team issues an interim update so clients receive the latest view.

Why Mordor's Egypt Agriculture Baseline Commands Reliability

Published estimates often vary because consultancies mix different crop baskets, use alternate price levels, or quote output at processor gate rather than farm gate. Our disciplined crop-only scope, annual refresh, and dual-track modeling keep numbers traceable and current.

These comparisons show that wide figures stem from scope inflation or dated inputs, whereas our crop-focused, price-verified approach delivers a balanced baseline that decision-makers can replicate and trust.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 5.37 B (2025) | Mordor Intelligence | - |

| USD 5.20 B (2024) | Regional Consultancy A | Relies on 2023 average prices and omits newly reclaimed desert output |

| USD 43.10 B (2024) | Global Consultancy B | Combines livestock, fisheries, and agro-processing values with crop output |

These comparisons show that wide figures stem from scope inflation or dated inputs, whereas our crop-focused, price-verified approach delivers a balanced baseline that decision-makers can replicate and trust.

Key Questions Answered in the Report

What is the current value of the Egypt agriculture market and its growth outlook?

The Egypt agriculture market size stands at USD 6.72 billion in 2026 and is projected to reach USD 8.41 billion by 2031, reflecting a 4.59% CAGR.

Which commodity segment contributes the most revenue?

Fruits dominate with a 38.5% share in 2025, anchored by Egypt’s position as the top global orange exporter.

How are water-scarcity risks being managed?

A USD 500 million World Bank project and mandatory drip irrigation on new land aim to cut water use up to 40% and sustain yields.

What logistics challenges affect agricultural exports?

Red Sea security incidents in 2024 tripled freight costs and extended transit times, prompting investment in alternative overland routes and private cold-chain capacity.

How can farmers monetize regenerative practices?

Zero-tillage and cover cropping can generate USD 10 to USD 18 per feddan in carbon-credit revenue once Egypt’s planned national registry becomes operational.

Page last updated on: