Israel Agriculture Market Analysis by Mordor Intelligence

The Israel Agriculture Market size was valued at USD 13.09 billion in 2025 and estimated to grow from USD 13.58 billion in 2026 to reach USD 16.33 billion by 2031, at a CAGR of 3.75% during the forecast period (2026-2031). Accelerating investment in agrifood technology, abundant desalinated water, and a renewed national focus on food security create favorable tailwinds for the Israel agriculture market. Precision irrigation uptake, government Research and Development subsidies, and rising specialty-crop exports collectively lift margins even as producers confront high labor costs. Capital inflows of USD 2.80 billion into more than 400 Israeli agrifood-tech companies in 2023 underscore investor confidence. Desalinated water priced near USD 0.40 per metric ton gives growers a cost-predictable input base, while the rapid scale-up of sensor-guided fertigation curbs fertilizer waste. Together, these forces position the Israel agriculture market for stable yet innovation-led expansion through 2030.

Key Report Takeaways

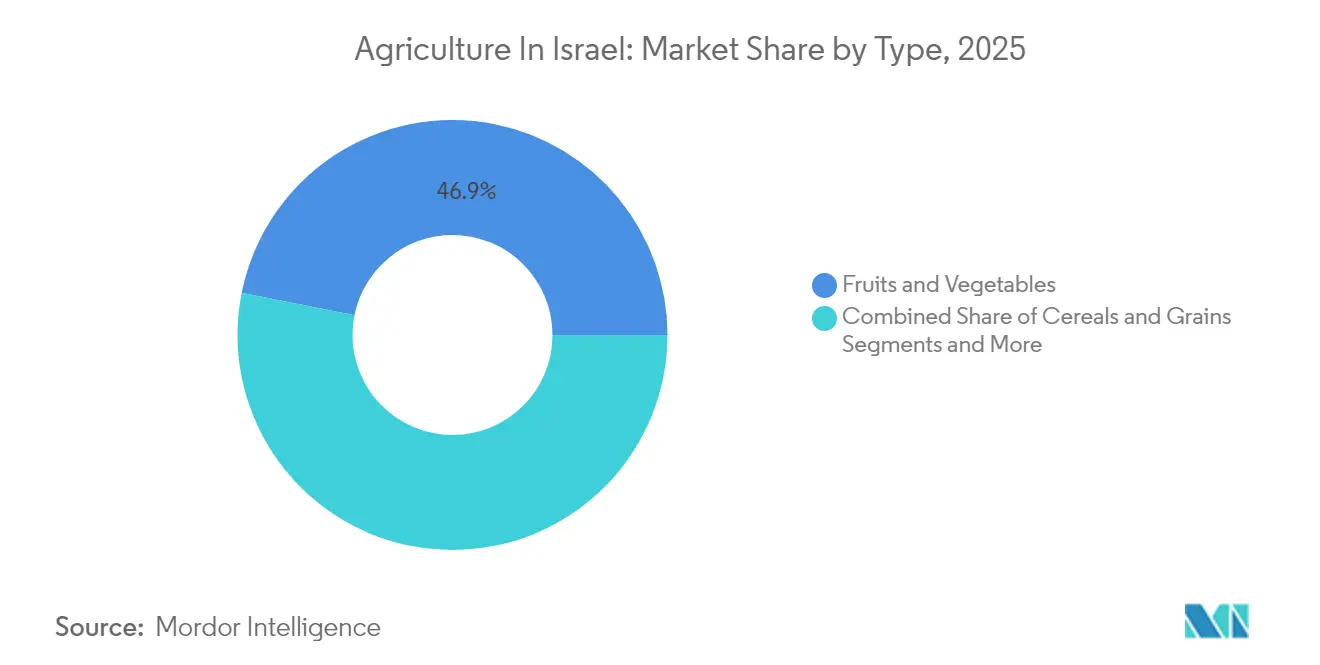

- By type, Fruits and Vegetables led with 46.85% of Israel agriculture market share in 2025, and Commercial Crops are forecast to expand at a 4.23% CAGR by 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Israel Agriculture Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Advancement in agricultural technology | +1.2% | Northern and Southern Districts | Medium term (2-4 years) |

| Favorable government initiatives and subsidies | +0.8% | National, periphery focus | Short term (≤ 2 years) |

| Widespread precision-irrigation adoption | +0.7% | Negev and Arava regions | Long term (≥ 4 years) |

| Post-conflict food-security imperatives | +0.6% | Gaza Envelope recovery | Short term (≤ 2 years) |

| Regenerative desert-farming export boom | +0.4% | Southern District and Negev | Long term (≥ 4 years) |

| Pesticide Ban by Importing Countries Creating Export Window | +0.3% | EU-oriented markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Advancement in Agricultural Technology

Venture investors continue to fund Israeli crop science and ag-automation firms at scale. Greeneye Technology closed a USD 20 million Series A in April 2024 to commercialize AI-enabled spot spraying that cuts herbicide use by 88% while protecting yields. Netafim augmented its drip-irrigation leadership with real-time plant-monitoring software through an October 2024 partnership with Phytech, enabling irrigation that follows actual sap flow rather than set schedules. This integration of sensors, computer vision, and machine learning accelerates on-farm decision-making and reinforces Israel’s reputation as a global exporter of water-efficient know-how. A USD 500 million debt package secured by Netafim in late 2024 further signals institutional appetite for scaling Israeli water tech. As platforms mature from pilots to revenue-generating tools, technology adoption is anticipated to raise average yields and keep the Israel agriculture market on its current growth arc.

Favorable Government Initiatives and Subsidies

Institutional realignment came in June 2024 when the ministry was rebranded the Ministry for Agriculture and Food Security, reflecting heightened strategic priority. The Renewal Administration now channels targeted reconstruction grants toward automation, irrigation, and protected cultivation infrastructure. Israel’s Innovation Authority earmarked additional agritech Research and Development funding for peripheral regions to narrow the center-periphery income gap. KANAT’s disaster-insurance framework keeps liquidity available for growers facing climate or conflict disruptions. Meanwhile, the extended United States-Israel Agricultural Trade Agreement assures duty-free access for certain exports through 2025, tempering near-term demand volatility.[1]U.S. Federal Register, “Extension of the United States-Israel Agricultural Trade Agreement,” federalregister.gov These coordinated policies shorten payback periods on capital investments and underpin the Israel agriculture market’s steady expansion.

Widespread Precision-Irrigation Adoption

Sensor-driven irrigation is evolving beyond conventional drip lines. Treetoscope’s in-tree sap sensors, backed by USD 7 million in early 2024 seed capital, deliver real-time data on water uptake to optimize irrigation volumes and timing. Five large seawater desalination plants already supply more than 50% of national freshwater, enabling growers to tap a cost-stable supply priced at USD 0.40 per metric ton. Academic-industry collaboration through the AGRISOL project piloted solar-powered desalination for farms straddling the Israel-Jordan border, illustrating a scalable model for arid-zone cultivation.[2]Ben-Gurion University of the Negev, “AGRISOL Solar Desalination Field Trial,” bgu.ac.il Fertigation specialists such as Haifa Group now combine precision irrigation with nutrient dosing to elevate yield per liter applied. AI-enhanced modeling from Phytech forecasts water demand based on micro-climate data, further reducing resource waste. These innovations collectively sustain the Israel agriculture market’s productivity gains even under water scarcity.

Post-Conflict Food-Security Imperatives

The Gaza Envelope supplied over half of the nation’s caloric intake before recent hostilities, spotlighting a geographic concentration risk. Field surveys by Israel’s northern district authorities show 89% of growers enduring conflict-related damage, creating urgency for protected cultivation and automation investment. Temporarily halting tomato imports in 2024 to shield domestic producers indicates a policy shift that privileges local production when feasible. Grants now prioritize robotics that reduces labor dependency, mitigating future harvest interruptions. The ministry’s food-security mandate integrates agricultural resilience into broader national-security planning, ensuring multi-year budget allocations for technology-based recovery. This imperative injects both public and private capital into the Israel agriculture market and accelerates the adoption of labor-saving equipment.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Dependence on staple-crop imports | -0.9% | National supply chain | Short term (≤ 2 years) |

| High production costs and labor shortages | -0.6% | Conflict-affected zones | Medium term (2-4 years) |

| Climatic-insurance premium inflation | -0.4% | Peripheral regions | Long term (≥ 4 years) |

| Regional trade-route disruptions | -0.3% | Export-oriented sectors | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Dependence on Staple-Crop Imports

Domestic wheat output is forecast to dip to 90,000 metric tons in the 2025-2026 season, trailing the five-year average of 108,000 metric tons, forcing mills to continue sourcing from the Black Sea Basin.[3]Foreign Agricultural Service, “Israel Grain and Feed Annual 2025,” usda.gov The sudden halt of Turkish produce shipments in 2024 required rapid supply-chain rerouting for tomatoes, olive oil, and cucumbers. Israel also imports 70% of laying-hen feed and most live cattle shipments, underscoring its exposure to external shocks. Switzerland, the Netherlands, and the United States together shipped about USD 1.16 billion in foodstuffs to Israel in 2024. Long-term liberalization reduced producer subsidies and amplified import reliance, complicating domestic self-sufficiency goals. This dependency subtracts an estimated 0.9 percentage points from the forecast CAGR for the Israel agriculture market.

High Production Costs and Labor Shortages

Conflict-driven labor gaps hampered about 70% of poultry operations in the southern corridor in 2024. Wage pressures amplify greenhouse heating and irrigation-pumping costs, while volatile energy markets squeeze already thin margins. KANAT’s rising payout ratio to farmers drives premium increases that elevate fixed costs. Although desalinated water remains affordable, electricity tariffs for pumping systems erode the advantage. Automation mitigates labor risk, but capital expenditure remains prohibitive for smallholders, accelerating consolidation inside the Israel agriculture market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Commercial Crops Drive Innovation

Fruits and Vegetables retained leadership with a 46.85% share of Israel agriculture market share in 2025, thanks to Mediterranean micro-climates and mature logistics links to European buyers. EU importers purchased EUR 979 million (USD 1.12 billion) worth of Israeli horticultural produce in 2024. Sensor-guided fertigation slashed nutrient runoff and bolstered shelf life. Meanwhile, cereals and grains slowed as wheat output lagged behind rainfall cycles, although barley held steady at 14,000 metric tons. Oilseeds, led by sunflower seed, are slated to grow 33% to 4,000 metric tons by 2025-2026, aided by precision seeding and pest-prediction analytics. Start-ups like Wonder Veggies, which raised USD 3 million to launch probiotic lettuce in 2025, reveal how biotech can reposition even mature categories. As technology percolates across crop types, Israel agriculture market participants extract higher margins from each irrigated hectare.

Commercial Crops commanded the fastest growth path with a 4.23% CAGR projected for 2026-2031, reflecting Israel’s pivot toward high-margin specialty output. In value terms, Commercial Crops will account for USD 4.23 billion of Israel agriculture market size by 2031, up from USD 3.44 billion in 2026. Export-oriented greenhouse systems enable premium strawberries, herbs, and flowers to hit EU shelves year-round. Technology layers such as AI-assisted climate control and robotic harvesters lift labor productivity, enticing institutional investors. Cotton harvests climbed from 40,000 to 65,000 bales between the 2024-2025 and 2025-2026 seasons, illustrating how climate-controlled programs can revive erstwhile marginal crops.

Geography Analysis

The Northern District commanded a prominent role in the national agricultural output, giving it the single-largest Israel agriculture market share. Higher rainfall and the presence of research hubs such as MIGAL foster biotechnology and precision-farming breakthroughs that bolster orchard, dairy, and poultry yields. Haifa District leverages its coastal location for intensive vegetable production and functions as a logistics gateway through nearby ports, while the more urbanized Central and Tel-Aviv Districts increasingly turn to high-value crops and vertical-farming projects to offset shrinking farmland.

The Southern District is projected to expand, adding momentum to the Israel agriculture market as greenhouse complexes and desert-farming innovations scale across the Negev and Arava valleys. Haifa Group’s ammonia and solar-powered infrastructure anchors large-scale cultivation in this arid zone. Before recent hostilities, the Gaza Envelope supplied 75% of national vegetable output and 20% of fruit production, underscoring its strategic role in food security. Advanced greenhouse designs and precision-irrigation systems support year-round harvests that compete effectively in export markets despite harsh climatic conditions.

Israel’s National Water Carrier moves fresh water from northern sources to southern farms, enabling crop production in regions that would otherwise remain uncultivated. The Innovation Authority’s peripheral development program channels agritech grants to both northern and southern districts, stimulating innovation-led rural growth. Jerusalem District, though land-constrained, contributes through specialized research and policy formulation that guide national strategies. The rapid adoption of desert agriculture techniques has generated exportable expertise, positioning the southern model as a blueprint for sustainable farming in arid economies worldwide.

Regulatory Landscape

Israel’s agriculture sector is regulated mainly by the Ministry of Agriculture and Food Security, with the Plant Protection and Inspection Service (PPIS) running plant-health controls under the Plant Protection Law (1956) and associated import procedures for plants and plant products. Food safety and composition requirements also operate under the Protection of Public Health Law (Food) (2015), and Israel has moved to adopt more than 40 European Union food standards as of 2024, which raises compliance requirements for producers and packers serving export and premium domestic channels.

On trade, a permanent United States-Israel Agreement on Trade in Agricultural Products entered into force on January 1, 2026, implemented via US action and managed through quota bulletins. It creates defined duty-free access for specified quantities, while Israel retains protections for a limited set of sensitive products through 2035. On domestic support, applied-agricultural R&D funding is set through multi-year programs, including allocations of up to ILS 20 million annually for 2026-2028 via regional applied research centers, reinforcing the linkage between food-security priorities and on-farm technology uptake.

Value Chain Analysis

Israel’s agriculture value chain starts with high-tech and resource-constrained inputs, including seeds and crop protection, irrigation hardware and desalinated-water supply, fertilizers and biologicals, and farm machinery and automation, with growers balancing high land, labor, and energy costs. Production is concentrated in intensive horticulture and protected cultivation, while grains and feed inputs remain import-dependent, which ties livestock and poultry economics to global commodity and logistics conditions. Post-harvest, value depends on sorting, cold chain, and packing operations that connect to domestic retail and export channels, with a sizable share of horticultural output oriented to European markets.

Downstream linkages reflect a concentrated food and beverage processing sector (with major incumbents such as Tnuva, Strauss Group, and Osem-Nestle). Export-focused horticulture also includes vertically integrated operators such as Mehadrin, spanning cultivation through global sales. The agrifood-tech ecosystem (reported at over 750 companies) increasingly feeds into the chain through sensors, decision software, and robotics to offset labor constraints, while public programs that allocate land and water resources continue to shape farm-scale economics and investment timing.

Market Opportunities and Future Outlook

Border-region rehabilitation and infrastructure hardening are creating near-term whitespace across farm infrastructure, irrigation efficiency, and protected cultivation. In March 2026, the Ministry of Agriculture and Food Security announced a NIS 47 million allocation for agricultural infrastructure in the Gaza Envelope and northern border communities (including water pipelines, storage, and pumps). This expands addressable demand for irrigation equipment, on-farm energy optimization, storage, and controlled-environment systems that reduce labor and climatic risk.

Commercial pathways for agritech scale-up are also widening through government-backed innovation infrastructure and clearer export access rules. In June 2026, the Ministry of Economy inaugurated the Foodtech Avenue complex in Kiryat Shmona alongside the National Agro-Tech Center at the Orchard Farm (Neot Mordechai), supported by a NIS 30 million investment. This strengthens the pipeline from applied research to commercialization across areas such as precision agriculture, multi-layer land use, and climate resilience included in the 2026-2028 applied R&D roadmap. On trade, the permanent US-Israel Agreement on Trade in Agricultural Products effective January 1, 2026 provides a more stable framework for duty-free access for specified product quantities. Separately, ongoing public consultations in early 2026 on food improvement-agent rules and pesticide maximum residue levels point to continued tightening and harmonization that rewards compliant, traceable production systems.

Recent Industry Developments

- July 2026: Groundwork BioAg and Syngenta announced a strategic partnership to commercialize mycorrhizal technology and soil carbon solutions for farmers. The tie-up links an Israeli biologicals platform with a global input distributor, which broadens commercialization channels for regenerative and input-efficiency offerings relevant to high-cost production environments.

- September 2025: CropX acquired Acclym (formerly Agritask) to expand its enterprise farm-management and sustainability data capabilities. The deal strengthens end-to-end digital monitoring and reporting across crop operations, aligning with grower needs for labor-saving decision tools and for traceability demanded by export and premium domestic buyers.

- April 2024: Greeneye Technology closed a USD 20 million Series A to scale AI-enabled spot spraying designed to reduce herbicide use while maintaining yields. The funding supports commercialization of precision application systems that can lower variable input costs and help growers meet tightening residue and stewardship requirements in export-oriented horticulture.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market is defined as the farm-gate value generated within Israel from crop cultivation and from livestock and aquaculture outputs that are sold for food, feed, or fiber.

Scope exclusions: Greenhouse ornamentals, forestry activities, and downstream food-processing revenues are excluded from this sizing.

Segmentation Overview

- By Type (Production Analysis (Volume), Consumption Analysis (Value and Volume), Import Analysis (Value and Volume), Export Analysis (Value and Volume), and Price Trend Analysis)

- Cereals and Grains

- Oilseeds and Pulses

- Fruits and Vegetables

- Commercial Crops

Data Sources, Market Sizing, and Validation

Desk Research

Desk work starts by anchoring the country agriculture value using official Israel production and price series, then using trade and consumption signals to explain demand swings across crop groups and animal categories. We typically refer to public sources such as Israel Central Bureau of Statistics releases, FAOSTAT production and yield tables, UN Comtrade and national customs summaries, and World Bank macro indicators linked to food and agriculture.

To keep assumptions practical, we also read ministry and regulator updates (such as agriculture, water, and food safety bodies), peer-reviewed crop and irrigation studies, and reputable press coverage for weather events and policy moves. Company filings and investor presentations are used to understand product mix and exposure to crops, livestock, or aquaculture, and a paid subscription focused on company financials and news is used selectively to validate revenue direction for larger suppliers and exporters. These sources listed are illustrative, and many other public references were also used for data collection, validation, and clarification during the research.

Primary Interviews and Surveys

Primary work focuses on checking how farm-gate prices form, what farmers are actually planting or harvesting, and how water availability and export demand are shifting decisions during the season. We speak with growers, cooperatives, agronomists, exporters, and processors that buy at the farm gate, plus input and equipment participants, and we validate responses across Israel's main producing belts and trading routes.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 27% | CXOs: 12% | APAC: 40% |

| Mid tier: 59% | Functional/Unit leaders: 37% | EMEA: 33% |

| Smaller Players: 14% | Managers: 51% | Americas: 27% |

Market-Sizing & Forecasting

Sizing is built by reconstructing total farm-gate value from production and trade data, where crop and livestock volumes are aligned to observed farm-level pricing and then rolled up to an Israel total. Our model is then cross-checked using selective bottom-up approximations, such as sampled area under cultivation times yield, plus a few price checks by major produce lines, which helps us adjust for reporting lags.

Inputs are chosen because they are easy to track on a client call and they map directly to farming outcomes. Key examples include harvested area and yield for major crops, irrigation water availability and cost signals, farm-gate price direction by produce group, livestock and aquaculture output trends, export volumes for high-value produce, and weather variability that affects yields. Where product-level information is missing, gaps are handled through peer-group ratios and seasonality patterns that are later confirmed through interviews.

Forecasts are produced using scenario analysis tied to the same drivers, with scenarios calibrated using expert views on planting intentions, water constraints, export demand, and expected price behavior. As the forecast is built, one assumption is updated at a time and checked for reasonableness before the next driver is applied, so the output stays traceable.

Data Validation & Update Cycle

Validation is done through multiple checks that link model outputs back to independent signals, then investigating outliers before numbers are finalized. We compare implied price and volume movements against official releases, trade totals, and field feedback, and we re-check any year showing a sudden jump that cannot be explained by weather, policy, or price changes.

Before sign-off, the work is reviewed in steps so that assumptions, formulas, and units are consistent across crops and animal products. Reports are refreshed annually, and interim updates are triggered if major events occur, such as acute drought conditions, new water rules, or meaningful export disruptions. Right before delivery, a final pass is completed so clients receive the latest updated view.

Mordor Intelligence's Israel Agriculture Market Size Measured Against Other Published Estimates

Published market sizes for agriculture in Israel can appear far apart even when they refer to similar farming activity, because the boundary is not always the same. Differences usually come from the value point used (farm-gate versus downstream), the treatment of livestock and aquaculture, and how currency timing and inflation are applied in the base year.

Export volumes for key produce and official production and price series are used to keep Mordor Intelligence's estimate connected to farm-gate value for crops plus livestock and aquaculture, rather than mixing in retail or food-processing revenues. The remaining spread across other figures typically comes from broader definitions that pull in distribution channels, technology spending, or mixed end-user value, and from base years that are not refreshed in the same way after weather-driven yield swings.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 13.09 B (2025) | |

| Global Consultancy A | USD 12.09 B (2023) | Uses an earlier base year and a broader segmentation lens that can blend farm output with adjacent agriculture value pools, which makes inflation and recovery years drive a different total. |

| Industry Bulletin B | USD 2.76 B (2024) | Appears to size only a narrower value slice and may emphasize traded categories and channel activity, which can undercount full farm-gate output across crops, livestock, and aquaculture. |

Looking at the three numbers together, most of the gap is explained by what is counted and the year used for pricing and conversion, not by a disagreement on the direction of growth. By keeping the scope at farm-gate output and then verifying it against production, trade, and price signals, the estimate stays repeatable and easier to reconcile to public data.

Key Questions Answered in the Report

What is the current size of the Israel agriculture market?

The market is valued at USD 13.58 billion in 2026 and is forecast to reach USD 16.33 billion by 2031.

Which segment holds the largest share in Israel agriculture market?

Fruits and Vegetables hold the top position, representing 46.85% of Israel agriculture market share in 2025.

Which crop segment is growing fastest in Israel agriculture market?

Commercial Crops lead with a 4.23% forecast CAGR for 2026-2031.

What government policies support growth of Israel agriculture market?

The Renewal Administration’s reconstruction grants, Innovation Authority Research and Development funding, and the Israel-U.S. duty-free trade extension collectively enhance investment conditions.

Page last updated on: