Angola Agriculture Market Analysis by Mordor Intelligence

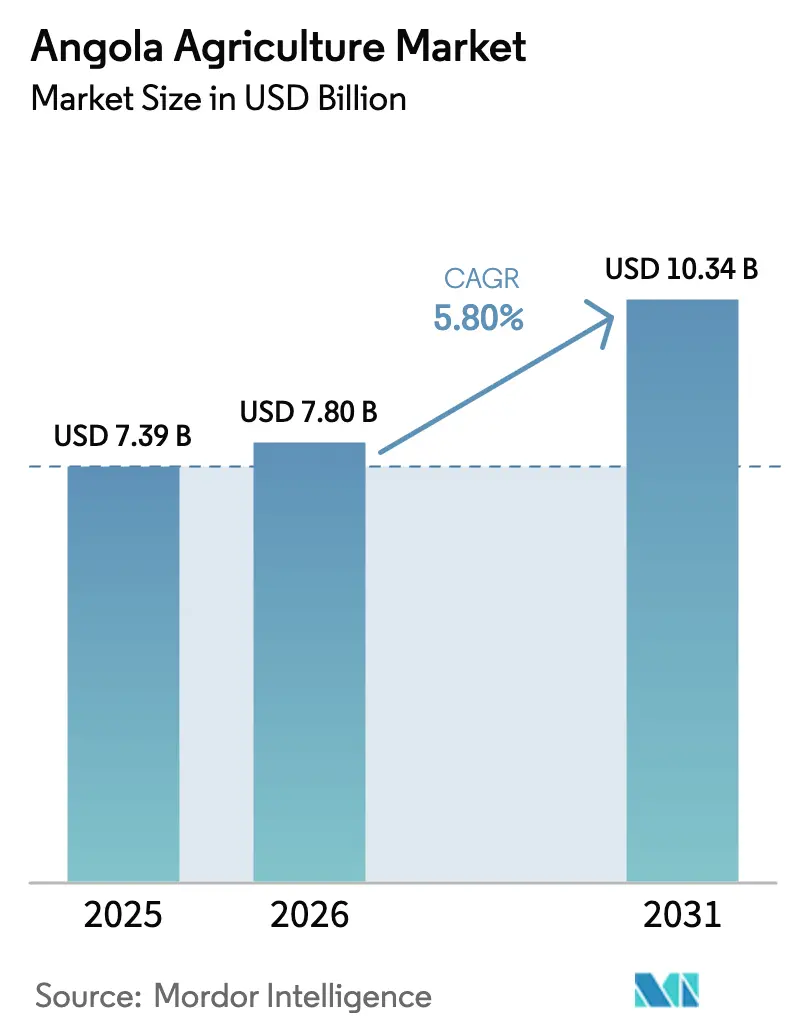

The Angola agriculture market size is projected to expand from USD 7.39 billion in 2025 and USD 7.80 billion in 2026 to USD 10.34 billion by 2031, registering a CAGR of 5.80% between 2026 to 2031. Shifts away from oil dependence, a surge in concessionary Chinese capital for mechanization, and stepped-up government irrigation programs are reshaping the competitive landscape and accelerating the formalization of value chains. Cereals and grains dominate production volumes, yet vegetables are emerging as the fastest-growing segment, driven by investments in cold chains that unlock regional and European Union market access. Multi-billion-dollar integrated food parks in Benguela and planned facilities in the north signal robust downstream demand for locally sourced crops, while satellite data and climate-smart seed programs strengthen resilience against El Niño-type droughts. At the same time, tariff realignments tied to Angola’s upcoming entry into the Southern African Development Community Free Trade Area widen export corridors for coffee, beans, and specialty horticulture.

Key Report Takeaways

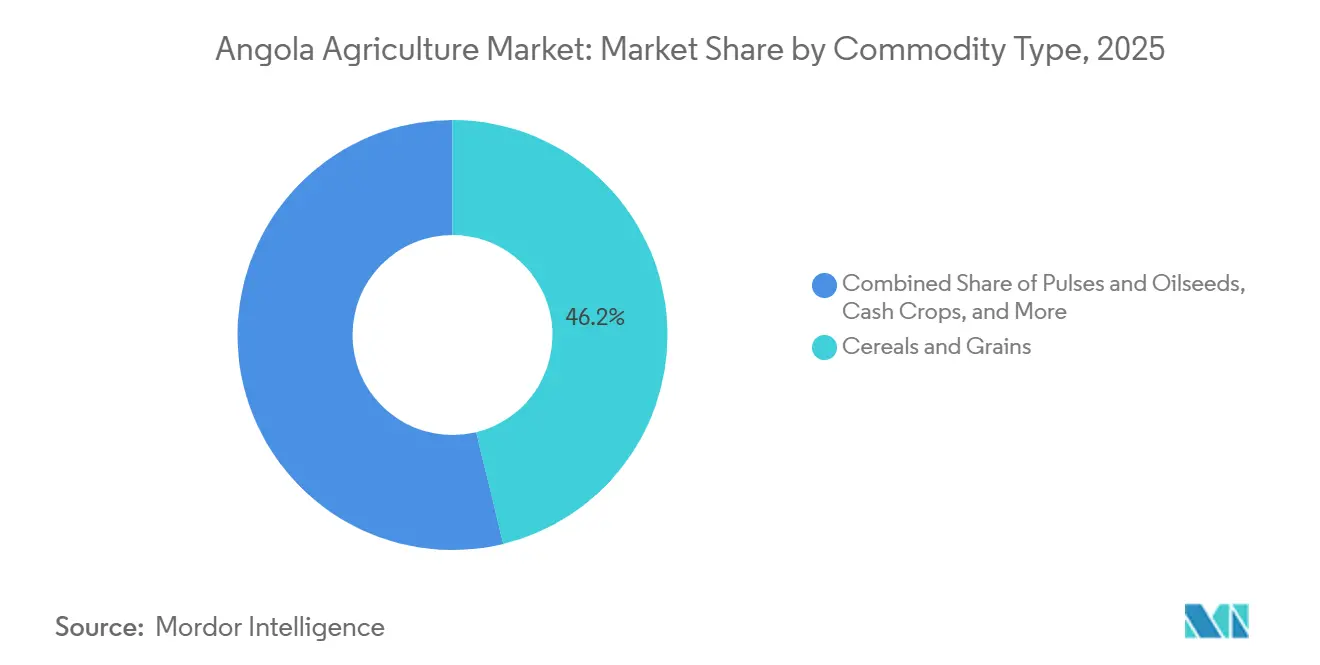

- By commodity type, cereals and grains held 46.2% of Angola agriculture market share in 2025, while vegetables are projected to expand at an 8.7% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Angola Agriculture Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Government-backed fertilizer subsidy expansion | +1.2% | National, with concentration in Huambo, Bié, Malanje, and Huíla | Medium term (2-4 years) |

| Revival of public irrigation schemes | +0.8% | Bengo, Malanje, Cuanza Norte, and Cuanza Sul | Medium term (2-4 years) |

| Surge in Chinese concessionary credit lines for farm mechanization | +1.5% | Eastern provinces (Malanje, Cuanza Norte, Lunda Norte, Moxico, Cuando Cubango, and Bié) | Short term (≤ 2 years) |

| Growing domestic demand for convenience-food ingredients | +0.6% | Urban centers (Luanda, Benguela, Huambo, and Lubango) | Long term (≥ 4 years) |

| Emergence of climate-smart "dry-land" maize hybrids | +0.7% | Southern provinces (Cunene, Namibe, and Huíla) and central highlands | Medium term (2-4 years) |

| Advent of satellite-enabled crop-insurance pilots | +0.4% | National, early pilots in Huambo, Bié, and Malanje | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Government-Backed Fertilizer Subsidy Expansion

Angola's Ministry of Agriculture and Forestry has embedded fertilizer subsidies into the National School Feeding Programme, launched in April 2025, by linking procurement contracts to domestic smallholder cooperatives that receive subsidized inputs in exchange for guaranteed off-take[1]Source: Food and Agriculture Organization, “Building on Strong Collaboration and Partnership Towards Sustainable Agrifood Systems Transformation in Angola,” fao.org. Linking subsidies to captive demand reduces Angola’s USD 3 billion food-import bill and crowds in private agronomy training financed by the International Finance Corporation. The International Finance Corporation partnered with Grupo Carrinho in December 2021 to train 300 agricultural technicians supporting these farmers, focusing on soybean and poultry value chains that integrate subsidized inputs with downstream processing capacity.

Revival of Public Irrigation Schemes

The World Bank's Smallholder Agriculture Productivity and Commercialization Project allocated USD 20 million specifically for farmer-led irrigation, targeting 15,600 farmers and 6,200 hectares between 2022 and 2029[2]Source: World Bank, “Development Projects: Angola Commercial Agriculture Development Project (PDAC) – P159052,” worldbank.org. This investment complements the Caxito Rega irrigation perimeter in Bengo, which has been operational for decades but received rehabilitation funding in 2024 to expand coverage and modernize canal systems. Brazilian-operated Fazenda Pipe installed 15 center-pivot systems irrigating 1,500 hectares in Malanje, achieving corn yields of 150 bags per hectare and soy yields of 66 bags per hectare, well above the national average.

Surge in Chinese Concessionary Credit Lines for Farm Mechanization

SinoHydro Group committed over USD 100 million in August 2025 to develop 30,000 hectares across six eastern provinces, subdivided into plots of 500 to 1,000 hectares for commercial farms and community-led initiatives, with a 25-year tax-free land concession. These deals solve Angola's capital-access problem by bundling land concessions with guaranteed Chinese off-take, effectively pre-financing mechanization through future export revenues. The strategic calculus for China centers on diversifying soybean supply away from the United States, which supplied approximately 20% of China's 105 million metric tons of soybean imports in 2024.

Growing Domestic Demand for Convenience-Food Ingredients

Grupo Carrinho's 43-hectare food park in Benguela houses 17 factories with a combined annual capacity of 610,000 metric tons for rice, wheat flour, and maize flour, employing over 4,000 workers and contracting 50,000 farmers in a pilot phase that will scale up to 1 million farmers. The park integrates milling, packaging, and distribution, targeting urban retailers and the hospitality, restaurant, and catering sectors in Luanda, Benguela, and Huambo. A EUR 57 million (USD 60 million) Deutsche Bank facility guaranteed by Italian Export Credit Agency (SACE) and Banco de Desenvolvimento de Angola financed a turnkey soybean and sunflower crushing plant in Lobito with a capacity of 4,000 metric tons per day for soybeans or 2,400 metric tons per day for sunflower seeds, described as the largest of its kind in Africa. Rising minimum wages and expanding poultry demand lift consumption of fortifiable flours and refined oils.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Chronic post-harvest infrastructure gaps | -1.0% | National, acute in Bié, Moxico, Cuando Cubango, and Lunda Norte | Short term (≤ 2 years) |

| Volatile foreign-exchange availability for input imports | -0.8% | National, concentrated impact on commercial farms and agro-processors | Short term (≤ 2 years) |

| Aging small-holder farmer demographic | -0.5% | Rural areas nationwide, particularly southern and central provinces | Long term (≥ 4 years) |

| Soil salinization in coastal plains | -0.3% | Bengo and Cuanza Sul coastal zones | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Chronic Post-Harvest Infrastructure Gaps

Post-harvest losses range from 30 to 40% across cereals, pulses, and horticulture due to inadequate storage, limited cold-chain facilities, and poor rural road networks. Fruits destined for export markets face rejection rates of 15 to 20% due to spoilage during transit from farm to port, eroding margins for smallholder cooperatives. The Regional Cassava Leadership Centre in Malanje, nearing completion in 2025, will provide processing and storage capacity for cassava, but similar facilities for maize, beans, and horticulture remain absent in Moxico, Cuando Cubango, and Lunda Norte.

Volatile Foreign-Exchange Availability for Input Imports

A kwanza depreciation from 852 to 917 per United States dollar in late 2024 raised landed fertilizer and pesticide costs by up to 15%, while new import bans squeezed allocations available for agricultural inputs[3]Source: United States Department of Agriculture Foreign Agricultural Service, “Poultry and Products Annual,” usda.gov. Limited private credit deepens currency-hedging challenges for farmers. Inflation reached 27.5% in December 2024 before moderating to 19% by July 2025, but private credit remains constrained at approximately 6% of GDP, limiting farmers' ability to hedge currency risk through forward contracts.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Commodity Type: Cereals and Grains Anchor Food Security as Vegetables Gain Export Momentum

Cereals and grains captured 46.2% of Angola agriculture market share in 2025, with dominant cassava staples that supply both rural consumption and industrial milling. Continued tariff increases on imported wheat flour and rice incentivize domestic substitution, while the milling capacity in Benguela shortens local supply chains. Strategic silos embedded in upcoming grain estates shield against storage deficits, positioning cereals and grains as the backbone of food-security policy and livestock feed expansion.

Vegetables are forecast to expand at an 8.7% CAGR from 2026 to 2031, the fastest among all segments, as solar-powered cold rooms and reefer trucking reduce post-harvest spoilage and unlock demand in the European Union. Premier estates such as Fazenda Novagrolíder cultivate 8,500 hectares of mixed horticulture and export to Portugal, Spain, and France, demonstrating commercial viability. Electronic Certificates of Origin, set for 2026, are projected to streamline trade within the Southern African Development Community, thereby widening market access for onions, potatoes, and citrus. The Angola agriculture market size for vegetables is projected to grow over the forecast horizon as nutritional awareness rises among urban consumers.

Geography Analysis

Production clusters in the central highlands of Huambo, Bié, and Malanje account for more than 60% of cereal and pulse output, benefiting from fertile Ferralsols and cooler elevations that deliver higher rain-fed yield ceilings. Provincial growth is supported by the World Bank's projection of a 4.3% expansion in agriculture by 2026, expected to moderate to 3.4% by 2027 as mechanization becomes more widespread. Benguela’s food-processing corridor links coastal ports to inland farms, reducing freight costs and enabling rapid market entry for milled products, while Malanje houses both SinoHydro’s grain estate and the Cassava Leadership Centre that upgrades root-crop processing.

Southern provinces Cunene, Namibe, and Huíla face the highest drought exposure, yet climate-smart seed adoption and vegetable gardens supported by a World Bank humanitarian grant have begun reversing acute food-insecurity spikes. Lunda Norte’s rice initiative under the Angola-Vietnam Action Plan targets 10 officers trained abroad to propagate lowland rice suited to local hydrology, while coastal Bengo and Cuanza Sul wrestle with soil salinity that forces a crop mix pivot toward cassava.

Trade corridors are evolving as Angola prepares to ratify the Southern African Development Community Free Trade Area protocols, which will remove tariff and non-tariff barriers with Namibia, Zambia, and South Africa. The USD 4 billion Lobito rail line could eventually shift mineral-centric cargo toward high-value horticulture once rural road feeders and cold-storage nodes come onstream. Cuanza Sul’s Quibala district is anchored in horticulture, seed multiplication, and emerging coffee acreage, leveraging its plateau climate and proximity to Luanda markets.

Regulatory Landscape

Angola's agriculture policy and compliance environment is overseen primarily by the Ministry of Agriculture and Forestry (MINAGRIF), together with the Ministry of Industry and Commerce (MINCO), while the National Directorate of Agriculture handles plant-related import permits and phytosanitary controls. In April 2024, Angola implemented a new customs tariff schedule that raised import duties on selected staple foods, reinforcing import substitution signals for grains and processed staples circulating through formal channels.

In 2026, the Presidency of the Republic issued two linked measures for seeds and biotechnology: Presidential Decree No. 56/26 (April 7, 2026) prohibiting the introduction of transgenic or genetically modified seeds and grains, and Presidential Decree No. 81/26 (April 29, 2026) establishing biosafety norms and inspection mechanisms for genetically modified organisms. For inbound shipments and trade documentation, Angola continues to rely on Codex Alimentarius benchmarks where national food safety rules are not comprehensive, and exporters to Angola also need to account for cargo certification requirements such as loading certificates administered by ARCCLA (Regulatory Agency for Cargo and Logistics Certification).

Value Chain Analysis

Angola's crop value chain spans (i) inputs (seed, fertilizer, crop protection, mechanization), (ii) primary production dominated by smallholders and expanding commercial estates, (iii) aggregation through cooperatives and off-take arrangements, (iv) post-harvest handling (drying, storage, basic grading), and (v) domestic distribution into urban wholesale and modern retail, with corridors linking inland production areas to coastal processing and ports. The constraints are most visible at the post-harvest and logistics stages, where limited rural roads, irrigation gaps, and storage shortages contribute to high loss rates and quality downgrades, particularly for cereals, pulses, and horticulture.

Public and development-finance programs are increasingly organizing the chain around corridor-based investment and coordinated platforms. In January 2026, the government established the Lobito Corridor Development Company (SDCL) to manage and promote investment along the corridor. In June 2026, the Government of Angola and the World Bank Group launched the AgriConnect Compact as a national framework to mobilize funding for agrifood system transformation. In July 2026, MINAGRIF launched the AgroCorridors Angola program to coordinate public and private investments across the Lobito and Malanje economic corridors, creating a clearer pathway for private operators in storage, cold chain, aggregation, and service provision to integrate with structured financing and public infrastructure rollouts.

Competitive Landscape

The Angola agriculture market includes state entities such as Gesterra E.P. (Government of Angola) and Companhia de Bioenergia de Angola - Biocom, operating alongside emerging private groups. Grupo Carrinho Holding exemplifies vertical integration by contracting with 50,000 farmers and processing 610,000 metric tons annually, thereby capturing both upstream supply and downstream retail margins.

Companhia de Bioenergia de Angola - Biocom’s USD 750 million sugar-to-ethanol estate spans 42,000 hectares and produces 254,000 metric tons of sugar each season, translating to a double-digit share of national cash-crop revenue. Chinese-backed SinoHydro and CITIC leverage concessionary debt and guaranteed soybean offtake to accelerate land clearing and mechanization, potentially consolidating their influence in the grain market over the next five years.

White-space opportunities include cold-chain logistics and digital agronomy services, with current smartphone-based advisory pilots reaching only a few hundred farmers. Brazilian-run Fazenda Pipe achieves yields 60% above national averages by combining center-pivot irrigation and precision fertilization, signaling a competitive advantage to operators that can finance modern equipment. Intensifying research on locally bred hybrid seeds underpins future competitive differentiation.

Market Opportunities and Future Outlook

Opportunities are concentrating where policy-backed funding and corridor coordination overlap with persistent supply chain gaps. The AgriConnect Compact launched in June 2026 provides an umbrella framework to mobilize USD 1.45 billion for agrifood system transformation and food security actions, while the African Development Bank approved USD 211.4 million in November 2025 for the Eastern Region Agricultural Value Chain Development Project (ERAVACDEP) to strengthen cereal and rice value chains across six provinces through 2031. Together, these programs create near-term opportunities for irrigation services, mechanization contracting, certified seed multiplication, and aggregation models that connect smallholders to formal offtake.

Downstream pull from large domestic processors and corridor infrastructure also expands demand for structured sourcing and logistics. Grupo Carrinho's integrated food park in Benguela (17 factories, 610,000 metric tons per year of combined milling capacity) points to the need for consistent grain and oilseed supply, while the Lobito and Malanje corridor focus under AgroCorridors Angola (July 2026) supports investment cases for storage hubs, reefer and dry bulk trucking, and quality management systems that help reduce the 30 to 40% post-harvest loss burden across key crop categories. April 2026 regulatory signals restricting the introduction of genetically modified seeds and grains also redirect innovation toward conventional breeding, climate-smart hybrids, and locally certified seed systems, reinforcing the commercial case for compliant seed testing, certification, and distribution networks.

Recent Industry Developments

- June 2026: The Government of Angola and the World Bank Group launched the AgriConnect Compact to mobilize USD 1.45 billion for agrifood system transformation and food security actions. The initiative formalizes a national financing and coordination umbrella that can accelerate bankable projects in irrigation, services, and market linkages for small and medium farmers.

- May 2026: Food Life began construction of an agro-food facility in Camanongue, Moxico, designed to process 20,000 tonnes of rice per year. The project adds localized offtake capacity in an eastern province where logistics constraints and limited processing have historically depressed farmgate realizations.

- November 2025: The African Development Bank approved a USD 211.4 million financing package for the Eastern Region Agricultural Value Chain Development Project (ERAVACDEP). The program targets cereal and rice value chains across six provinces, strengthening investment momentum for storage, aggregation, and extension-linked commercialization models.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market is defined as the annual value of crop, plantation, and horticulture output produced in Angola and sold at the farm gate, including typical on-farm post-harvest handling that is directly linked to crop sales.

Scope exclusions: livestock, fisheries, forestry, agro-processing revenues, and farm inputs such as fertilizers and machinery are excluded.

Segmentation Overview

- By Commodity Type

- Grains and Cereals

- Production Analysis (Volume)

- Overview

- Area Harvested and Yield

- Consumption Analysis (Value and Volume)

- Trade Analysis (Value and Volume)

- Import Market Analysis

- Overview

- Key Supplying Markets

- Export Market Analysis

- Overview

- Key Destinations Markets

- Import Market Analysis

- Wholesale Price Trend Analysis and Forecast

- Seasonality Analysis

- Production Analysis (Volume)

- Pulses and Oilseeds

- Production Analysis (Volume)

- Overview

- Area Harvested and Yield

- Consumption Analysis (Value and Volume)

- Trade Analysis (Value and Volume)

- Import Market Analysis

- Overview

- Key Supplying Markets

- Export Market Analysis

- Overview

- Key Destinations Markets

- Import Market Analysis

- Wholesale Price Trend Analysis and Forecast

- Seasonality Analysis

- Production Analysis (Volume)

- Fruits

- Production Analysis (Volume)

- Overview

- Area Harvested and Yield

- Consumption Analysis (Value and Volume)

- Trade Analysis (Value and Volume)

- Import Market Analysis

- Overview

- Key Supplying Markets

- Export Market Analysis

- Overview

- Key Destinations Markets

- Import Market Analysis

- Wholesale Price Trend Analysis and Forecast

- Seasonality Analysis

- Production Analysis (Volume)

- Vegetables

- Production Analysis (Volume)

- Overview

- Area Harvested and Yield

- Consumption Analysis (Value and Volume)

- Trade Analysis (Value and Volume)

- Import Market Analysis

- Overview

- Key Supplying Markets

- Export Market Analysis

- Overview

- Key Destinations Markets

- Import Market Analysis

- Wholesale Price Trend Analysis and Forecast

- Seasonality Analysis

- Production Analysis (Volume)

- Cash Crops

- Production Analysis (Volume)

- Overview

- Area Harvested and Yield

- Consumption Analysis (Value and Volume)

- Trade Analysis (Value and Volume)

- Import Market Analysis

- Overview

- Key Supplying Markets

- Export Market Analysis

- Overview

- Key Destinations Markets

- Import Market Analysis

- Wholesale Price Trend Analysis and Forecast

- Seasonality Analysis

- Production Analysis (Volume)

- Grains and Cereals

Data Sources, Market Sizing, and Validation

Desk Research

For desk research, we start by building the baseline demand and supply picture for Angola crops, then we layer it with data that can be checked year to year. Public agriculture output and harvested area series, trade quantities, and producer price series are used to set realistic ranges and to spot sudden jumps that need an explanation.

Illustrative sources include agriculture statistics releases from national agencies and agriculture ministry publications, FAOSTAT-style crop balance indicators, UN Comtrade trade flows, World Bank agriculture value added series for macro cross-checks, and customs and port updates shared through official channels. We also use company filings, investor presentations, and reputable press coverage to understand capacity additions, irrigation projects, and procurement behavior. Where needed, a paid subscription for company financials and an import-export shipment-level database are used to verify exporter activity and pricing direction. These desk sources are not exhaustive, and many other public references were used to collect data, validate it, and clarify gaps.

Primary Interviews and Surveys

Primary work was used to confirm what is actually being sold in Angola, how prices move across the year, and which crops are scaling faster in different provinces. We spoke with growers, aggregators, exporters, input distributors, and local advisors, then we checked the same assumptions with commercial buyers so the model reflects real purchasing volumes and storage practices across the country.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 39% | CXOs: 15% | APAC: 48% |

| Mid tier: 45% | Functional/Unit leaders: 40% | EMEA: 34% |

| Smaller Players: 16% | Managers: 45% | Americas: 18% |

Market-Sizing & Forecasting

Sizing starts with a top-down rebuild of the farm-gate value pool. Crop-wise production volumes and harvested area trends are translated into value using average producer prices, then adjusted for post-harvest handling that remains on-farm. The total is corroborated with selective bottom-up checks such as sampled crop output multiplied by typical farm-gate price bands, procurement channel checks on volumes, and exporter-focused volume and price signals, so the totals stay realistic.

Key model inputs include crop production and yield trends, harvested area shifts, import and export quantities for major crops, farm-gate and wholesale price spreads, and the pace of irrigation and mechanization adoption reported by stakeholders. For the forecast, we use scenario analysis supported by a multivariate regression, with the strongest drivers being acreage expansion, expected yield improvement, and price direction under inflation and currency movement. When bottom-up information is patchy for informal trade and smallholder volumes, the gap is handled through conservative penetration ranges that are re-tested with primary respondents before finalizing.

Data Validation & Update Cycle

Outputs are checked against independent signals such as agriculture value added movement, trade direction for key crops, and year-on-year price behavior, then reviewed again for outliers at the crop level. If a sudden jump is seen in value, we re-check whether it came from volume, price, or a one-time shock, and the assumption is revisited with additional calls.

Before sign-off, the model and narratives go through multi-step analyst reviews so definitions, units, and currency handling are consistent. Reports are refreshed annually, and interim updates are made when material events occur such as policy changes, major weather disruptions, or large investment announcements. Right before delivery, a final pass is completed so the numbers reflect the latest available public releases and interview inputs.

Mordor Intelligence's Angola Agriculture Market Estimate Compared With Other Published Estimates

Published market sizes for Angola agriculture can look far apart, even when they seem to describe the same space, because authors often mix different boundaries like farm-gate crops versus total agriculture sector value. Differences also come from the year used, whether values are in current dollars or adjusted, and whether informal production and post-harvest handling are treated as part of the market.

By tracking crop-wise output and farm-gate pricing inputs, Mordor Intelligence keeps the estimate tied to crops, plantations, and horticulture sales at the farm gate, while some sources lean on agriculture value added or broad investor narratives that can fold in forestry, fishing, and wider activity.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 7.39 B (2025) | |

| Trade Journal A | USD 14.86 B (2024) | Uses a broader agriculture framing with limited clarity on whether values represent total sector activity, and it does not separate crop farm-gate sales from adjacent categories or pricing bases. |

| Industry Data Portal B | USD 13.21 B (2024) | Represents agriculture value added in current USD, which is a macro net-output metric that includes forestry, hunting, and fishing, so it is not aligned to a crop-only farm-gate market boundary. |

The spread in the table is mainly explained by what is being counted, not just math. When the scope is kept at crop farm-gate value with clear price and volume drivers, the result is easier to trace and repeat, and it stays comparable across years as assumptions are refreshed.

Key Questions Answered in the Report

What is the projected market size of the Angola agriculture market by 2031?

The Angola agriculture market size is projected to reach USD 10.34 billion by 2031.

Which commodity segment held the largest share of the Angola agriculture market in 2025?

Cereals and grains held the largest share of the Angola agriculture market, accounting for 46.2% of the total market share in 2025.

Which crop segment shows the fastest revenue growth?

Vegetables lead with an expected 8.7% CAGR from 2026 to 2031, driven by cold-chain expansion and growing export demand.

Which provinces dominate Angola's agricultural output?

Huambo, Bié, and Malanje collectively generate more than 60% of national cereal and pulse production.

Page last updated on: