IP Multimedia Subsystem (IMS) Services Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 3.92 Billion |

| Market Size (2031) | USD 7.29 Billion |

| Growth Rate (2026 - 2031) | 13.24% CAGR |

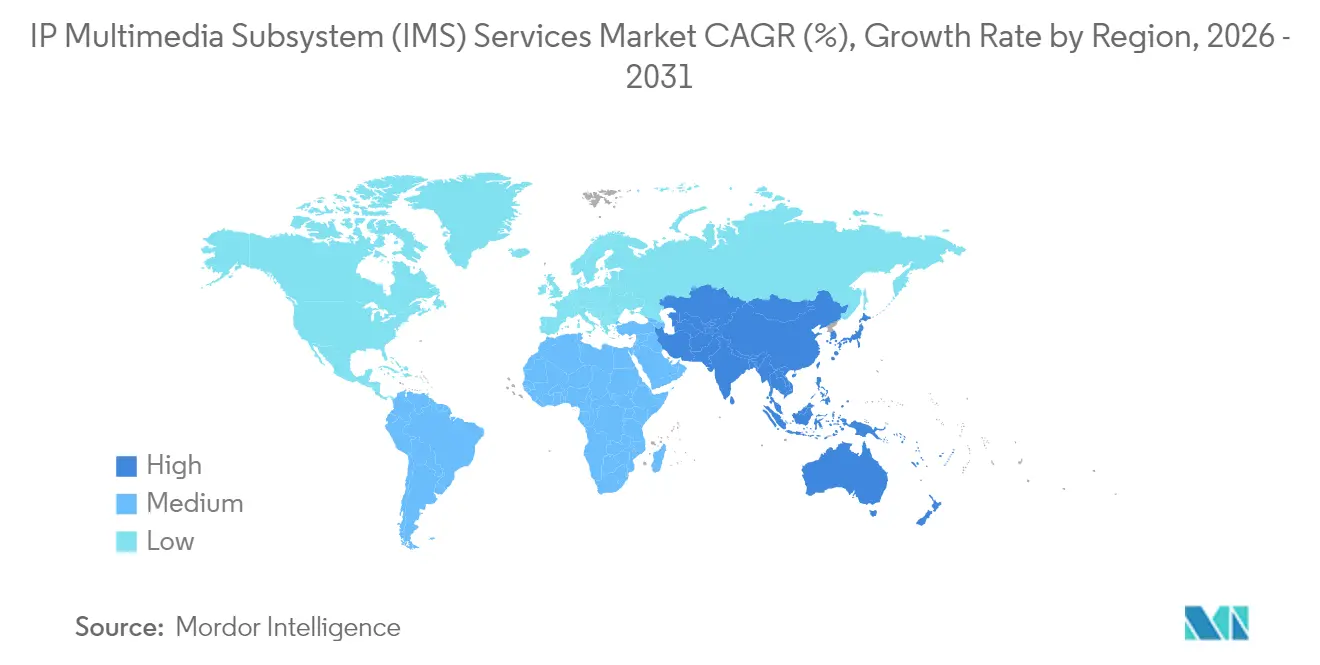

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

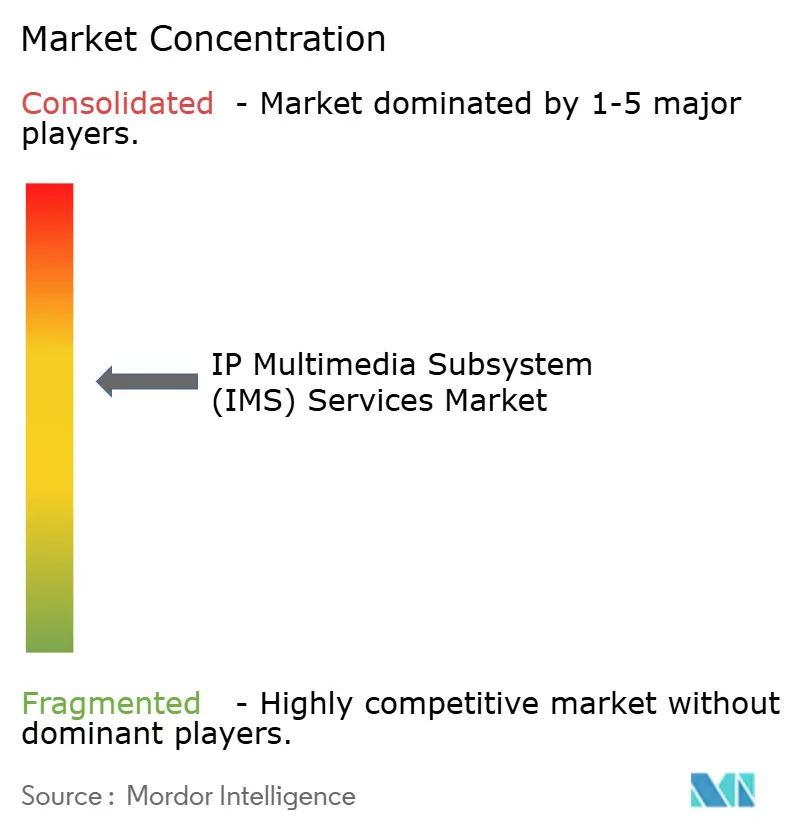

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

IP Multimedia Subsystem (IMS) Services Market Analysis by Mordor Intelligence

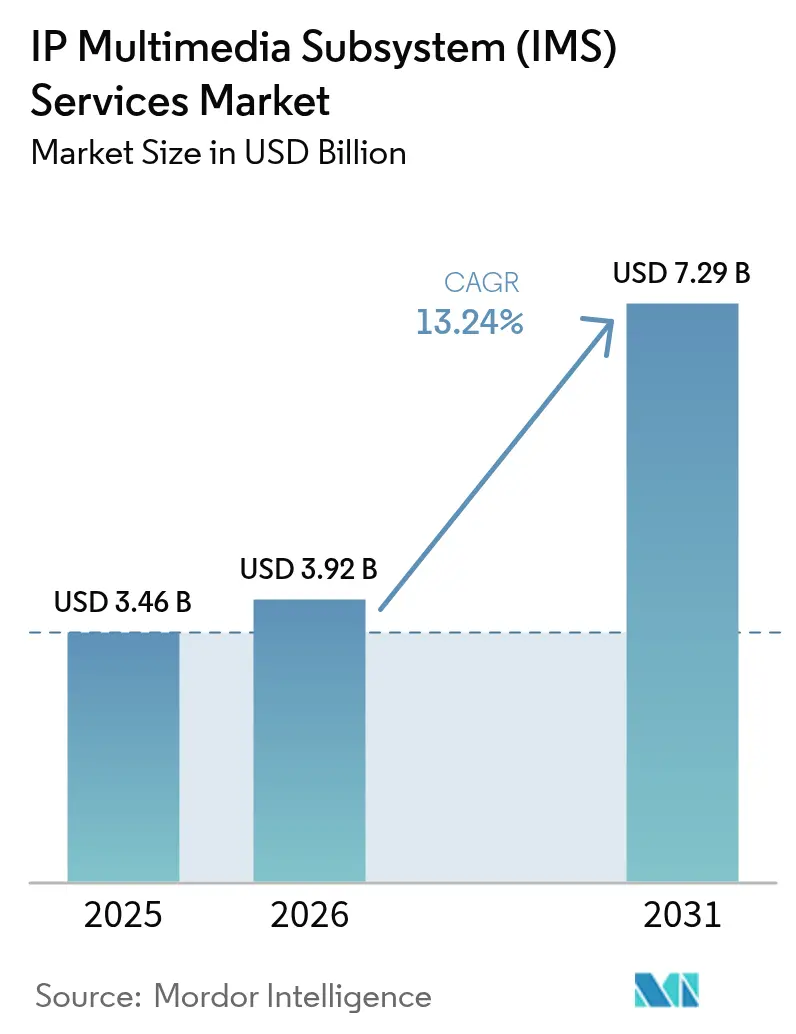

The IP Multimedia Subsystem (IMS) Services market size is expected to grow from USD 3.46 billion in 2025 to USD 3.92 billion in 2026 and is forecast to reach USD 7.29 billion by 2031 at 13.24% CAGR over 2026-2031. Operators are accelerating migrations from circuit-switched voice to all-IP session control because standalone 5G cores require native Voice over New Radio (VoNR) and because cloud-native network functions reduce capital intensity while accelerating new-service rollouts. Regulators are adding momentum by refarming spectrum and setting firm 2G and 3 G sunset dates, forcing carriers to shift voice workloads onto IMS or face service disruptions.[1]Federal Communications Commission, “FCC Approves Supplemental Coverage from Space Rules,” FCC.GOV Growing business-messaging traffic, led by Rich Communication Services (RCS), is expanding the addressable user base for IMS data channels, while private 5G networks in manufacturing, logistics, and public safety verticals are spawning new enterprise-centric use cases. Vendors that package IMS as cloud software are removing integration roadblocks and providing smaller operators with an on-ramp to advanced voice and messaging capabilities without requiring heavy upfront investment.

Key Report Takeaways

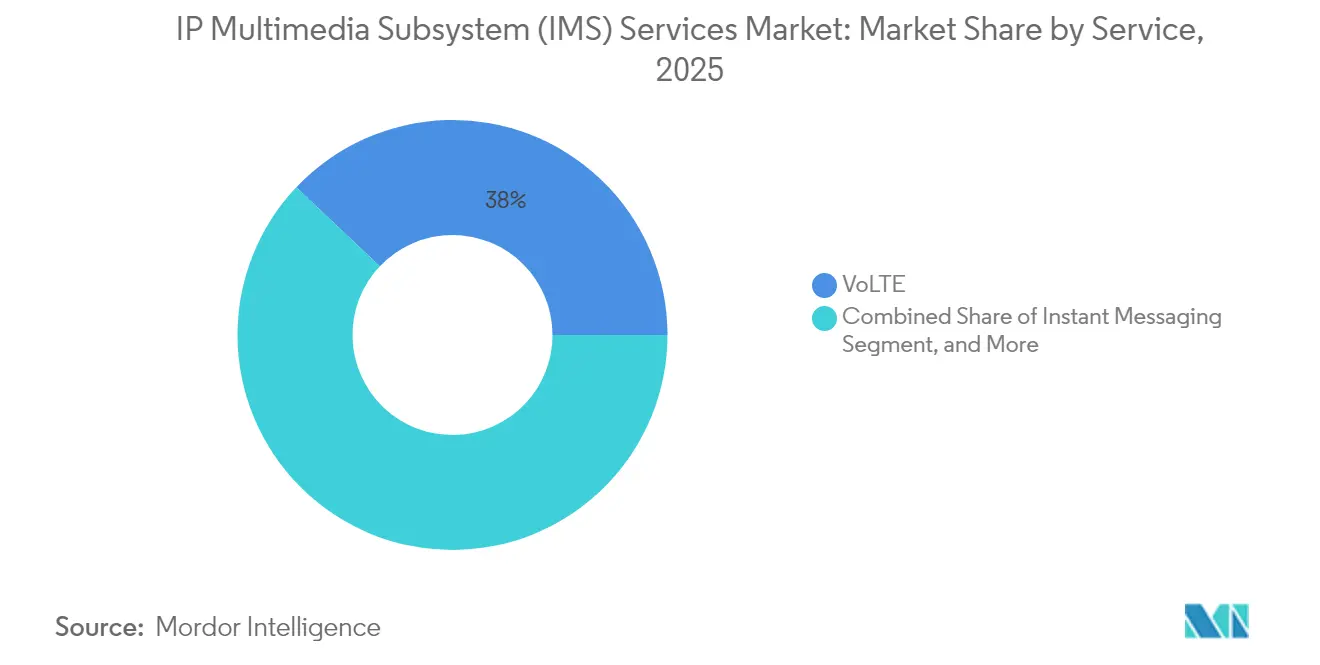

- By service, VoLTE led the IP Multimedia Subsystem (IMS) Services market with a 37.95% market share in 2025; however, Instant Messaging is expected to advance at a 14.41% CAGR through 2031.

- By component, products accounted for 71.88% of the IP Multimedia Subsystem (IMS) Services market size in 2025, whereas services are expected to expand at a 14.93% CAGR between 2026 and 2031.

- By deployment model, on-premises installations retained an 80.42% share in 2025, while cloud-based models are set to grow at a rate of 17.35% per year.

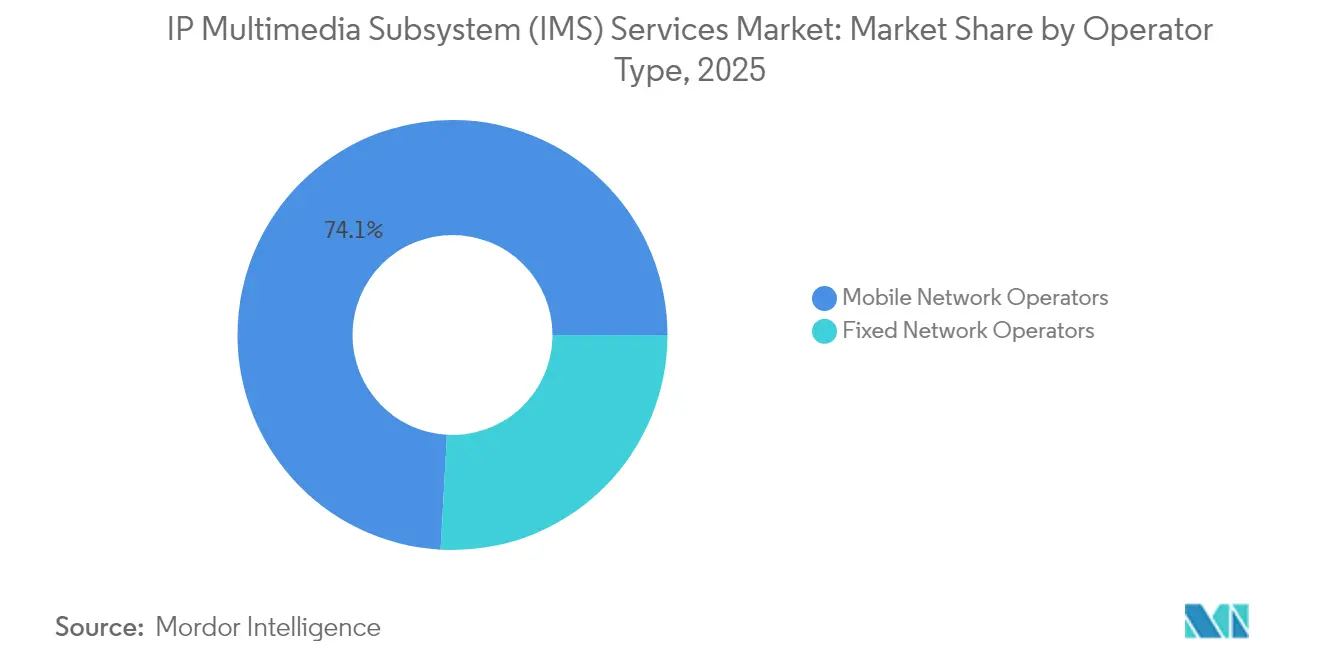

- By operator type, mobile network operators captured a 74.12% share in 2025 and are forecast to rise at a 13.62% CAGR.

- By end user, telecommunication operators held a 66.05% share in 2025, yet enterprises are on track for a 15.21% CAGR during the outlook period.

- By geography, North America commanded a 41.26% revenue share in 2025; the Asia Pacific is the fastest-growing region, with a 14.37% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global IP Multimedia Subsystem (IMS) Services Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing popularity of LTE and VoLTE and emergence of 5G | +3.2% | Global, strongest in North America, Europe, Asia Pacific | Medium term (2-4 years) |

| Soaring demand for Rich Communication Services in business messaging | +2.1% | Global, led by North America and Europe; Asia Pacific consumer scale | Short term (≤ 2 years) |

| Surging operator investments in cloud-native IMS architectures | +2.8% | North America and Europe are early adopters, while the Asia Pacific and the Middle East are following. | Medium term (2-4 years) |

| Rapid transition to Voice over New Radio in standalone 5G networks | +2.4% | Asia Pacific core, early Europe, and selective North America | Medium term (2-4 years) |

| Emergence of satellite direct-to-device voice services | +1.3% | North America and Australia are pioneering | Long term (≥ 4 years) |

| Government-backed spectrum refarming initiatives are accelerating IMS upgrades | +1.9% | North America, Europe, Asia Pacific | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Increasing Popularity of LTE and VoLTE and Emergence of 5G

Standalone 5G deployments detach voice from legacy LTE anchors, prompting carriers to adopt VoNR, which relies on IMS session control for call setup, codec negotiation, and quality-of-service enforcement.[2]Free Mobile, “Launches First 5G Standalone Network with VoNR,” FREE.FR Commercial launches by Free Mobile in France, Viettel in Vietnam, and O2 UK demonstrate that VoNR is production-ready rather than experimental. Operators see additional upside because an IMS-anchored core supports network slicing and low-latency use cases that monetize 5G beyond connectivity. A September 2024 network-API venture formed by Ericsson and 12 leading carriers exposes CAMARA-compliant APIs, allowing developers to trigger bandwidth on demand or location services, thereby turning IMS into a programmable asset for third-party applications. This shift positions voice as only one of many revenue-bearing IMS functions.

Soaring Demand for Rich Communication Services in Business Messaging

RCS traffic reached 50 billion messages in 2025, and revenue is on track to reach USD 4.2 billion by 2029, solidifying IMS-based messaging as a compelling alternative to legacy SMS. Apple’s decision to add RCS to iOS 18 removed the last major interoperability barrier between Android and iPhone ecosystems. With read receipts, verified sender IDs, and rich media, enterprises can now push interactive campaigns across the entire handset base, generating higher engagement and trusted identities that over-the-top apps cannot match. Carriers are launching RCS-as-a-service platforms that integrate with customer relationship management suites, generating sticky recurring fees while offsetting SMS revenue erosion. Each new RCS tenant increases attachment rates for IMS presence, messaging, and security functions, and extends the market from voice into data channels.

Surging Operator Investments in Cloud-Native IMS Architectures

Containerized IMS components running on Kubernetes reduce capital expenditure by 30-40% compared to virtual appliances, as resources scale horizontally and updates roll out with zero downtime. Deutsche Telekom moved 17 million fixed-line subscribers onto a multi-vendor cloud stack in February 2024, and Telefónica Germany followed with a five-year extension that converts its virtualized IMS into a stateless web-scale core. Cloud models also support hybrid layouts, in which control functions reside in public hyperscale regions, while user plane functions are moved to edge nodes, thereby satisfying latency requirements for mission-critical services and aligning with ETSI NFV Release 4 specifications.[3]ETSI, “NFV Release 4 and Release 5 Specifications,” ETSI.ORG The resulting agility lets operators introduce features such as video ringing or real-time translation in weeks rather than quarters, driving faster revenue realization.

Rapid Transition to Voice over New Radio in Standalone 5G Networks

Carriers recognize that running parallel 4G and 5G voice cores raises operational complexity and delays payback on 5G spectrum, so they are accelerating VoNR rollouts. e& UAE and Huawei showcased “New Calling” features like remote assistance and augmented-reality overlays, enabled by IMS data channels that ride alongside VoNR audio. China Mobile’s new calling trials pair IMS with augmented-reality translation and aim to scale VoNR to its 810 million-strong 5G base by the end of 2024. 3GPP Release 16 streamlines mobility between 5G and LTE, enabling the retirement of circuit-switched cores without service gaps. As VoNR becomes common, IMS graduates from legacy voice interconnect to the control layer underpinning immersive communication services.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Shortage of skilled IMS professionals | -1.8% | Global, acute in the Asia Pacific and the Middle East emerging markets | Medium term (2-4 years) |

| Complexity of integrating IMS with legacy circuit-switched networks | -2.2% | Global, especially where the 2G and 3 G installed base remains high | Short term (≤ 2 years) |

| Heightened cybersecurity and signaling fraud risks | -1.6% | Global | Short term (≤ 2 years) |

| Capital-intensive upfront deployment costs in emerging markets | -1.4% | Asia Pacific, Middle East, Africa, South America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Shortage of Skilled IMS Professionals

Cloud-native IMS requires expertise in microservices orchestration, CI/CD pipelines, and multi-vendor API integration, yet most telecom engineers grew up on monolithic or virtualized cores and lack hands-on Kubernetes experience. Operators facing talent gaps often delay migrations or over-rely on vendor-managed services, which drives up costs and risk. Certification programs from the TM Forum and vendor-sponsored boot camps are expanding, but the pace of training still lags behind deployment timelines, particularly in high-growth markets such as India and Saudi Arabia.[4]TM Forum, “Open Digital Architecture Conformance Test Kits,” TMFORUM.ORG Vendors are incorporating AI-assisted configuration and auto-healing into their products, enabling fewer engineers to manage larger networks; however, human expertise remains the bottleneck.

Complexity Integrating IMS with Legacy Circuit-Switched Networks

Brownfield operators must run IMS and circuit-switched cores in parallel during cutover, maintain dual numbering plans, and reconcile billing data across heterogeneous OSS stacks. HCLTech’s 2024 whitepaper revealed that inventory mismatches lead to order-fulfillment errors and billing disputes when services transition to new cores. Operators are adopting TM Forum Open APIs to mask vendor differences, yet proprietary mediation layers persist, prolonging integration programs. The resulting overhead saps capex savings from IMS and can slow service launches, especially where 2G and 3 G are still revenue-relevant.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service: Instant Messaging Accelerates on Universal RCS

The service segment generated the largest single-stream revenue from VoLTE, capturing 37.95% of the IP Multimedia Subsystem (IMS) Services market share in 2025. Adoption rose when 4G coverage matured, and VoLTE remains foundational for voice continuity because handsets universally support it. However, enterprise marketing and customer-care teams are pivoting to RCS-enabled Instant Messaging, projected to grow at a 14.41% annual rate through 2031. Apple’s RCS adoption eliminates fragmentation, enabling brands to create a single campaign for the entire smartphone universe, complemented by read receipts and rich media. The higher engagement rate is prompting carriers to launch revenue-sharing models that give them a direct stake in business messaging.

Messaging growth influences traffic patterns on the IP Multimedia Subsystem (IMS) Services market. Because RCS runs over IMS data channels, each enterprise customer lifts the utilization of presence, group chat, and file-transfer functions. As carriers monetize APIs for verified sender IDs or rich cards, value migrates from simple voice minutes to orchestrated multimedia sessions. VoNR and VoWiFi also gain, but their incremental growth is lower because penetration already nears handset saturation in mature markets. The result is a diversified service mix that buffers operators against flat voice revenue.

By Component: Services Gain Momentum in a Product-Led Base

IMS core equipment still accounted for 71.88% of overall revenue in 2025, reflecting the hardware and perpetual license heritage of telecom procurement. Session control functions, media gateways, and signaling firewalls dominate capital layouts, especially for greenfield 5G cores in Asia and the Middle East. Yet the fastest expansion is in managed and professional services, set to climb 14.93% annually as carriers outsource the entire lifecycle from design to operations. Telefónica Germany’s five-year cloud-native agreement with Mavenir illustrates the pivot: the operator shifts to a subscription model where the vendor absorbs upgrade risk while guaranteeing performance.

In markets with lean engineering teams, operators prefer turnkey cloud stacks that bundle Kubernetes clusters, continuous-integration pipelines, and in-line security. This demand gives system integrators and software specialists a larger revenue slice while compressing hardware margins. Over time, software-as-a-service contracts linked to active subscriber counts could bring the services slice approach closer to parity with products, further reshaping the revenue mix within the IP Multimedia Subsystem (IMS) Services market.

By Deployment Model: Cloud Traction vs. On-Premises Resilience

On-premises deployments accounted for 80.42% of installations in 2025, as sovereign data policies in China, Russia, and parts of the Middle East require voice records to be stored locally. Large incumbents have sunk costs in private data centers and prefer to scale existing clusters. Yet, cloud-based models are advancing at a rate of 17.35% per year, as smaller or converged operators prioritize agility over asset ownership. Deutsche Telekom’s 17 million-line migration demonstrates that even tier-ones see capex relief and faster innovation from containerized IMS in public or hybrid clouds.

Regulators in the United States and Europe now accept voice session control in certified public cloud regions, provided call detail records reside in local zones, unlocking additional addressable demand. Hybrid topologies—combining control in a public cloud with media at the edge—offer a compromise that reduces idle capacity while meeting latency targets for emergency calls or industrial robotics. Because cloud models rely on usage-based charging, they can align cost curves with traffic growth, making them a powerful draw for greenfield private 5 G deployments in factories and mines. As those use cases multiply, the IP Multimedia Subsystem (IMS) Services market size tied to the cloud will widen.

By Operator Type: Mobile Dominance with Fixed-Line Innovation

Mobile network operators generated 74.12% of 2025 revenue, propelled by nationwide VoLTE reach and near-term VoNR upgrades. Their traffic volumes far surpass those of other segments, and handset migrations dictate the urgency of their roadmap. Nevertheless, fixed-line operators are often the first movers in cloud-native IMS because they must replace end-of-life PSTN switches and can test microservices without incurring the risk of mobile subscriber issues. Deutsche Telekom’s fixed voice migration and AT&T’s plan to retire copper by 2029 exemplify an investment super-cycle for fiber-to-the-home voice and video leveraging IMS.

Mobile carriers are also embracing network APIs that expose quality of service or location, converting the IMS session broker into a programmable platform for developers. Early adopters, such as AT&T and Bharti Airtel, aim to capture non-connectivity revenue by charging per-API call, an expansion path that is not available in legacy architectures. This symbiosis, fixed operators driving platform maturity and mobile operators scaling monetization, keeps the IP Multimedia Subsystem (IMS) Services market in double-digit growth.

By End User: Enterprise Uptake Via Private 5G and Critical Comms

Telecommunication operators still accounted for 66.05% of IMS solutions in 2025, but enterprise demand is growing at a rate of 15.21% annually as factories, ports, and emergency services deploy private 5G cores that require IMS-like control for push-to-talk, video, and telemetry. Ericsson and Swisscom offer a standalone private network where all sensitive data and call control reside on-premises, enabling 4K video inspections and autonomous guided vehicles. Nokia’s Digital Automation Cloud serves hundreds of industrial sites with local voice and messaging anchored by compact IMS cores.

Public-safety agencies are transitioning to LTE- and 5G-based Mission-Critical Push-to-Talk, which requires IMS for session control and priority handling. Ecrio’s tie-up with Casa Systems and Kyocera packages rugged devices with embedded VoNR and RCS, showing how solution kits bring IMS beyond traditional telecom. As private networks proliferate, enterprise spend will tilt the IP Multimedia Subsystem (IMS) Services market toward smaller, scalable cores optimized for localized traffic patterns.

Geography Analysis

North America retained the leading 41.26% revenue share in 2025. AT&T invested USD 21 billion to USD 22 billion in its network, plans nationwide mid-band 5G reaching 300 million POPs by 2026, and targets 70% Open RAN traffic the same year. T-Mobile’s six-carrier aggregation reached 3.6 Gbps, while Verizon installed 130,000 Open RAN-ready radios, all of which require IMS supervision to ensure synchronized voice and video. The FCC’s Supplemental Coverage from Space ruling enables satellite direct-to-device voice, with partnerships between operators and LEO constellations creating new revenue pools for IMS-anchored calling in rural areas.

The Asia Pacific is forecast to expand at a 14.37% CAGR due to massive 5G adoption. China Mobile counts 810 million 5G connections and is piloting augmented-reality New Calling features using IMS data channels. In India, Reliance Jio has surpassed 1 million 5G sites and is testing network slicing for gaming and enterprise broadband. Bharti Airtel has joined the network-API venture to monetize quality-on-demand. Telstra achieved 340 Mbps uplink on standalone 5G and signed with Starlink for satellite voice coverage. These initiatives enhance the IP Multimedia Subsystem (IMS) Services market size in the Asia Pacific, as every incremental 5G user requires an IMS endpoint.

Europe is modernizing its core through cloud projects. Telefónica Germany signed a five-year cloud-native contract with Mavenir in February 2025, and Deutsche Telekom completed a 17 million-line migration one year prior. Free Mobile launched the first commercial VoNR network in September 2024, while O2 UK lit 14 standalone cities in February 2024. The EU’s Digital Decade targets require EUR 148 billion in new connectivity spending, with a significant portion earmarked for all-IP cores that can scale to support 5G standalone traffic. Orange’s Sylva project standardizes telco-cloud blueprints, allowing operators to port IMS workloads across countries without extensive reintegration.

The Middle East and Africa show rapid cloudification. Saudi Telecom Company migrated 74% of voice subscribers to cloud IMS and achieved 54.7% 5G coverage across 8,993 sites. e& UAE demonstrated New Calling with visualized voice, while du UAE reached 5.1 Gbps indoor speeds, highlighting experiential services that rely on IMS data channels. GSMA expects mobile revenues in the region to rise from USD 66 billion in 2023 to USD 88 billion by 2030, resulting in a steady increase in IMS spend.

South America lags in capex but is catching up via cloud-native approaches. Mavenir and Whitestack rolled out an IMS core for an unnamed tier-one carrier in August 2024, demonstrating that multi-vendor best-of-breed stacks can reduce acquisition costs and shorten the time to market. As spectrum auctions finalize in Brazil, Chile, and Colombia, carriers are lining up funding from development banks to underwrite VoLTE and later VoNR, supporting the gradual penetration of IP Multimedia Subsystem (IMS) services.

Regulatory Landscape

IMS services are shaped largely by globally harmonized standards that regulators and national bodies increasingly cite for interoperability and public-safety obligations. In January 2026, ITU-T issued Recommendation Q.5035 for IMT-2020 network interconnection with IMS, reinforcing common interconnect expectations for 5G-era voice and multimedia services. Operators and vendors also align implementations to GSMA profiles such as NG.114 (voice, video, and messaging over 5GS) and to 3GPP stage-3 specifications (including interfaces such as 29.175 and 29.176), which define interoperable IMS behavior across multi-vendor networks.

National-level actions are turning technical conformance into enforceable requirements, especially as 2G and 3G sunsets and fraud controls intensify. On June 9, 2026, India's Department of Telecommunications adopted TSDSI-transposed 3GPP standards (Releases 13-17) as National Telecom Standards, covering 4G/5G radio, core, and IMS stacks and tightening compliance expectations for operators building VoLTE and VoNR on shared IMS cores. Separately, Finland's Traficom enforced new interoperability rules effective May 4, 2026, requiring operators to block or modify spoofed calling numbers from international interfaces, which increases the need for IMS-adjacent signaling controls and policy enforcement at interconnect points.

Value Chain Analysis

The IMS services value chain starts with standards and specifications (3GPP, ETSI, ITU-T, and GSMA profiles) that shape product roadmaps and multi-vendor interoperability, then moves to IMS core software and network-function suppliers that provide session control, media functions, messaging enablers, and security layers. Infrastructure is delivered through operator private clouds and public or hybrid cloud platforms, with Kubernetes-based deployment and CI/CD pipelines increasingly part of the core product bundle. Systems integrators and managed service providers bridge vendors and operators to design, integrate, test, and operate IMS across legacy interworking and 5G standalone requirements.

Downstream, mobile and fixed operators monetize IMS through VoLTE, VoWiFi, VoNR, and RCS-based messaging, and increasingly through enterprise use cases in private 5G and critical communications that need localized session control and policy. Interconnect and identity management (numbering, routing, and anti-spoofing controls) and OSS/BSS integration remain key gating steps before scaling new IMS-enabled services. A representative upstream-to-operator collaboration is Ericsson's June 2024 partnership expansion with Videotron to enhance core network capabilities, showing how vendor upgrades and operator modernization programs translate into improved IMS readiness for 5G-era services.

Competitive Landscape

Huawei remains the largest supplier of IMS networks, with a cumulative deployment of over 420 cores and serving more than 1.7 billion VoLTE users worldwide. Its end-to-end portfolio is attractive in Asia and Africa; yet, geopolitical restrictions open up space for Western vendors. Mavenir won a high-profile five-year renewal with Telefónica Germany and supplies Deutsche Telekom’s multi-vendor stack, positioning itself as a cloud-native alternative with no vendor lock-in. Ericsson, Nokia, and Cisco secure national contracts by bundling IMS with radio and transport gear, while Ribbon Communications pursues USD 75 million in maintenance revenue after Microsoft chose to divest Metaswitch to Alianza.

Start-ups see opportunity in private 5G. Ecrio integrates compact IMS servers with Casa Systems' small cells and Kyocera's rugged devices for critical communications, while Ataya embeds zero-trust segmentation into session control for operational technology convergence. Hyperscalers are recalibrating strategies: Microsoft exits network-function software to focus on Azure infrastructure services, enabling cloud platforms to host partner IMS workloads rather than sell their own stacks. The TM Forum’s Open Digital Architecture certification, available in January 2025, will accelerate the adoption of best-of-breed solutions by outlining conformance tests, reducing integration risk, and fostering competition.

White-space exists in satellite direct-to-device calling, where Starlink, AST SpaceMobile, and Lynk aim for global roaming agreements. IMS vendors that optimize codecs for half-second latency over non-terrestrial links could lock in early mover advantage. Meanwhile, artificial-intelligence-driven automation emerges as table stakes: any supplier that cannot offer closed-loop assurance and predictive resource scaling risks margin erosion when carriers benchmark against cloud-native leaders.

IP Multimedia Subsystem (IMS) Services Industry Leaders

Telefonaktiebolaget LM Ericsson

Cisco Systems, Inc.

Nokia Corporation

Huawei Technologies Co., Ltd.

International Business Machines Corporation

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

A primary opportunity is in operator voice-core modernization programs that converge VoLTE and VoNR onto cloud-native IMS, reducing duplication across 4G and 5G voice domains and enabling faster feature delivery. This shift is backed by concrete operator actions, such as Proximus selecting Nokia in January 2026 to modernize its voice core for full-scale VoNR on 5G standalone, alongside multi-year core modernization frameworks that include cloud IMS capabilities. As networks move to 5G standalone, the operational need to maintain consistent voice, video, and messaging behavior across roaming and device ecosystems increases demand for implementations aligned with GSMA NG.114 and IR.92 profiles and 3GPP interworking requirements.

A second opportunity is the expansion of IMS beyond traditional operator voice into programmable and enterprise-centric communications, where IMS data channels and network APIs support richer calling experiences and sector-specific applications. The market already reflects enterprise pull through standalone private 5G offerings from vendors and operators, where on-premises control and security requirements favor compact, deployable IMS cores and managed services. Additional whitespace also appears in compliance-driven upgrades at international interconnects, as regulators mandate stronger anti-spoofing behavior and push operators to invest in IMS-adjacent signaling policy and fraud mitigation integrated with the voice core.

Recent Industry Developments

- July 2026: Huawei announced that GlobalData recognized its Single Voice Core (SVC) as the sole leader in a 2026 IMS and voice core competitive landscape assessment. The update reinforced Huaweis positioning around converged, AI-assisted voice core capabilities and its ability to compete for multi-service IMS transformations where operators want a single core for VoLTE, VoNR, and richer calling features.

- March 2026: Ericsson signed a multi-year framework agreement with SoftBank Corp. in Japan to expand and modernize the operator's core network, including deployment of Ericsson Cloud IMS. The agreement supports SoftBank's 5G standalone evolution and strengthens Ericssons footprint in cloud-native IMS as operators consolidate voice and multimedia control into software-defined cores.

- August 2024: Ericsson and Spark New Zealand announced a collaboration to enhance network resiliency using Ericsson IMS. The move highlighted how operators use IMS modernization to improve voice continuity and service reliability while preparing core networks for broader 5G-era service evolution.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers revenue generated from IP Multimedia Subsystem (IMS) services and related platforms used to deliver IP-based voice, messaging, video calling, and presence capabilities across fixed and mobile networks, including deployments run on-premises or in cloud environments.

Scope exclusions: Consumer device hardware, generic IP routers and switches, and pure over-the-top communication apps that do not use operator-grade IMS core functions are excluded.

Segmentation Overview

- By Service

- Instant Messaging

- VoIP

- VoLTE

- VoWiFi

- Other Services

- By Component

- Products

- Services

- By Deployment Model

- On-Premises

- Cloud-Based

- By Operator Type

- Mobile Network Operators

- Fixed Network Operators

- By End User

- Telecommunication Operators

- Enterprises

- Emergency Services

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Mexico

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- India

- Japan

- Australia

- South Korea

- Rest of Asia Pacific

- Middle East and Africa

- Middle East

- Saudi Arabia

- United Arab Emirates

- Qatar

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Nigeria

- Rest of Africa

- Middle East

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk work starts by mapping what is counted as IMS services revenue, then aligning it to operator modernization programs and enterprise communications rollouts. We rely on public references such as ITU ICT indicators, GSMA publications, 3GPP standards releases, FCC and European Commission telecom updates, and OECD communications data to keep definitions consistent and timelines realistic.

On the commercial side, annual reports, earnings transcripts, and investor decks from network and software suppliers, plus operator capex and network transformation commentary, help set direction on spending mix. We also use paid subscriptions for company financials and intelligence, plus patent databases, to cross-check who is investing in cloud-native IMS, VoLTE, VoWiFi, and RCS enablement. The desk research sources listed here are illustrative, and many other public documents and data points were also used for collection, clarification, and validation.

Primary Interviews and Surveys

Primary inputs come from interviews and structured surveys with telecom operator teams, IMS platform specialists, system integrators, and enterprise communication stakeholders, so assumptions are not built only on published statements. Since this is a global market, views are balanced across Americas, EMEA, and APAC, and then used to confirm service scope, pricing direction, and the pace of cloud migration by operator type.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 28% | CXOs: 12% | APAC: 43% |

| Mid tier: 58% | Functional/Unit leaders: 43% | EMEA: 32% |

| Smaller Players: 14% | Managers: 45% | Americas: 25% |

Market-Sizing & Forecasting

Market sizing is built using a top-down approach where operator network upgrade activity and service adoption signals are used to reconstruct the annual demand pool for IMS capabilities, then translated into revenue using realistic pricing and deployment mix. We corroborate totals with selective bottom-up checks, such as rolling up a sample of supplier revenue disclosures, using channel feedback on deal sizes, and validating sampled ASP ranges against deployment scale.

Key inputs in the model include the pace of VoLTE and VoWiFi rollouts, RCS enablement momentum, the share of cloud-based IMS versus on-premises, operator type split between mobile and fixed networks, and enterprise use cases like emergency services communications where service continuity requirements are stricter. Forecasts are developed using scenario analysis, where near-term drivers (5G core upgrades, virtualized network function migration, and modernization budgets) are stress-tested with expert views, and the final path is selected after the assumptions align across regions. When bottom-up signals are missing for smaller countries or smaller vendors, we fill gaps with proxy ratios based on operator subscriber scale and known network transformation timing, and the assumptions are later rechecked during validation calls.

Data Validation & Update Cycle

Validation is done by comparing the modeled totals against independent signals, such as operator modernization timelines, regional network investment trends, and shifts in deployment model adoption, and then checking whether the implied per-operator spend stays within a believable range. Any sharp year-to-year jumps are reviewed again, and the drivers are rechecked with targeted follow-ups when a variance cannot be explained by rollouts, pricing, or scope.

Before sign-off, the model and assumptions go through multiple analyst review steps, including consistency checks across service types (VoIP, VoLTE, VoWiFi, and messaging) and across regions. Reports are refreshed annually, and interim updates are made when material events occur, such as large-scale network sunsets, major operator migration announcements, or policy changes that move timelines. Right before delivery, a final pass is completed so the view reflects the latest public disclosures and verified expert inputs.

Mordor Intelligence's Ip Multimedia Subsystem Ims Services Market Size Compared With Other Published Estimates

Published market numbers for IMS services can vary because the scope is not always the same, and because different teams use different timing for currency conversion, deployment mix assumptions, and what they treat as service revenue versus product revenue. We see spreads most often when one estimate leans more on supplier-side disclosures, while another leans more on operator spending patterns.

A practical gap driver in this market is whether the model counts only IMS service and platform revenues tied to operator-grade functions (like VoLTE, VoWiFi, and RCS enablement) or whether it also folds in adjacent network software and broader next-generation communication stacks. Another driver is the assumed speed of cloud-based IMS adoption, since aggressive cloud migration can lift near-term spend in some models, while more conservative models delay that ramp based on integration and migration constraints.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 3.92 B (2026) | |

| Global Consultancy A | USD 3.33 B (2024) | Uses an earlier base year and a broader IMS framing that blends products and services, which can compress near-term value when pricing and deployment mix are not re-based to operator modernization timing. |

| Industry Publisher B | USD 6.93 B (2025) | Appears to include adjacent categories beyond IMS services and applies a different growth path over a longer horizon, which can inflate the stated current size if service-only revenue is not separated cleanly. |

The spread in these figures mainly comes from what is counted inside the IMS services bucket and how quickly cloud-based deployments are assumed to replace on-premises, which directly changes the revenue curve. When operator-grade IMS services are isolated from adjacent network software and the service mix is rechecked with operator and integration stakeholders, the estimate stays easier to trace back to real rollout signals, which is the approach applied here by Mordor Intelligence.

Key Questions Answered in the Report

How large is the IP Multimedia Subsystem (IMS) Services market in 2026?

It is valued at USD 3.92 billion and is projected to climb to USD 7.29 billion by 2031.

What is the main growth driver for IMS services?

Standalone 5G rollouts that require native VoNR and rely on IMS for session control are the single largest catalyst.

Why are operators shifting IMS workloads to the cloud?

Containerized microservices cut capex by up to 40% and allow new features to launch in weeks, not quarters.

Which service category is growing fastest?

Instant Messaging using RCS is expanding at a 14.41% CAGR through 2031 as enterprises adopt rich business messaging.

Which region will see the highest IMS revenue growth through 2031?

Asia Pacific is forecast to grow at 14.37% annually due to massive 5G adoption and network-API monetization plans.

How are private 5G networks influencing demand for IMS?

Enterprises implementing on-premises 5G cores need IMS-like control for push-to-talk, video, and quality of service, boosting vendor revenue from compact session controllers.

Page last updated on: