Ionic Liquid Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

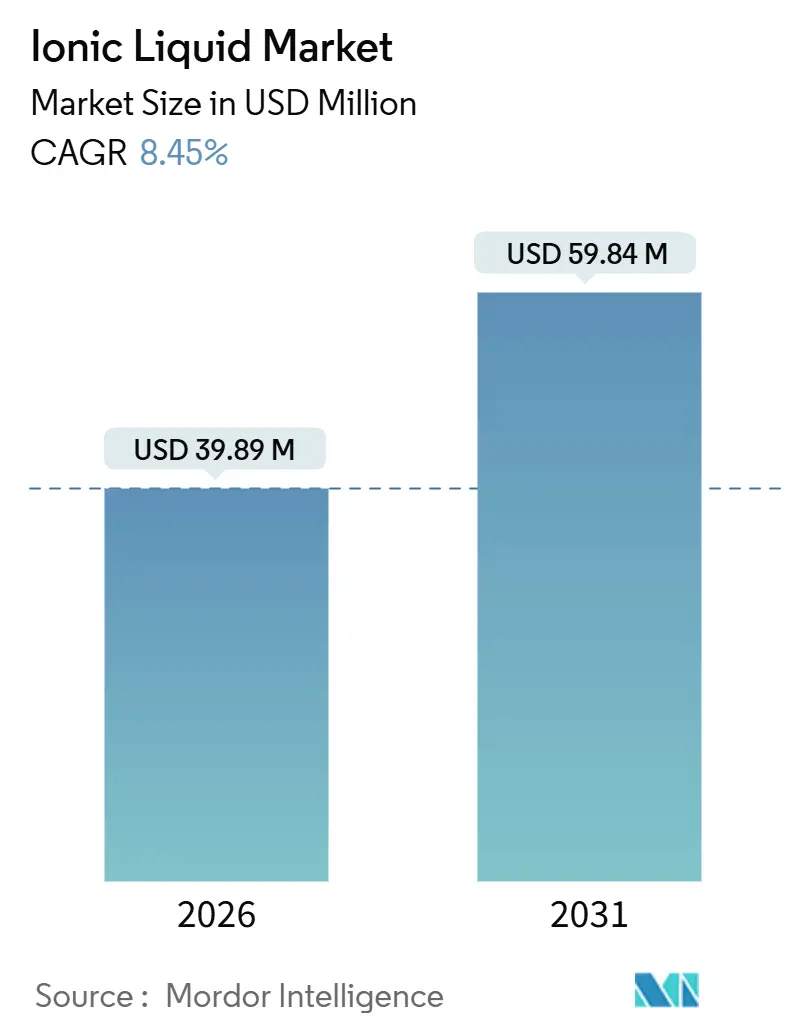

| Market Size (2026) | USD 39.89 Million |

| Market Size (2031) | USD 59.84 Million |

| Growth Rate (2026 - 2031) | 8.45% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

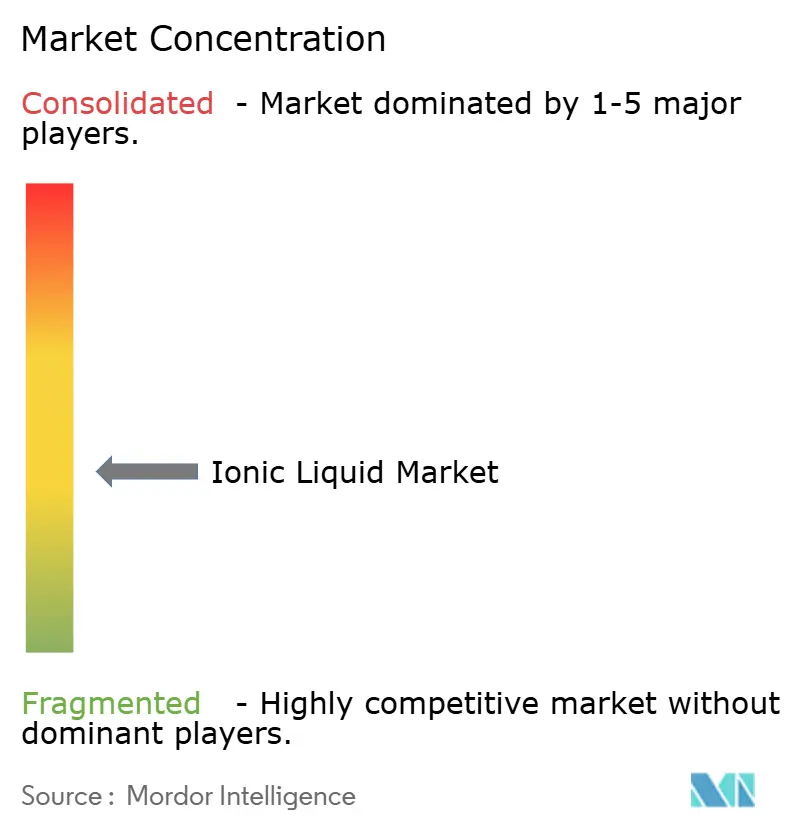

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Ionic Liquid Market Analysis by Mordor Intelligence

The Ionic Liquid Market size is estimated at USD 39.89 million in 2026, and is expected to reach USD 59.84 million by 2031, at a CAGR of 8.45% during the forecast period (2026-2031). This expansion underscores the transition of ionic liquids from academic curiosities to production-scale enablers supporting electric-vehicle batteries, green-solvent programs, and precision electronics. Regulatory caps on volatile-organic-compound (VOC) emissions in the European Union, China, and the United States are accelerating solvent substitution, while demand from Asia-Pacific gigafactories for high-voltage electrolytes continues to intensify. Suppliers are differentiating through task-specific formulations that command price premiums exceeding USD 500 per kilogram, and continuous-flow production is beginning to trim manufacturing costs. Competitive rivalry remains high because the top five suppliers account for less than 40% ionic liquids market share, leaving space for regional specialists and captive production at downstream manufacturers.

Key Report Takeaways

- By application, Solvents and Catalysts led with 36.68% ionic liquids market share in 2025 and is expanding at an 8.58% CAGR through 2031.

- By type, the Cation segment held 58.23% revenue share in 2025, while the Anion segment posted the fastest growth at a 9.01% CAGR through 2031.

- By function, Process Chemicals accounted for 57.44% of the ionic liquids market size in 2025; Performance Chemicals are forecast to advance at a 9.56% CAGR to 2031.

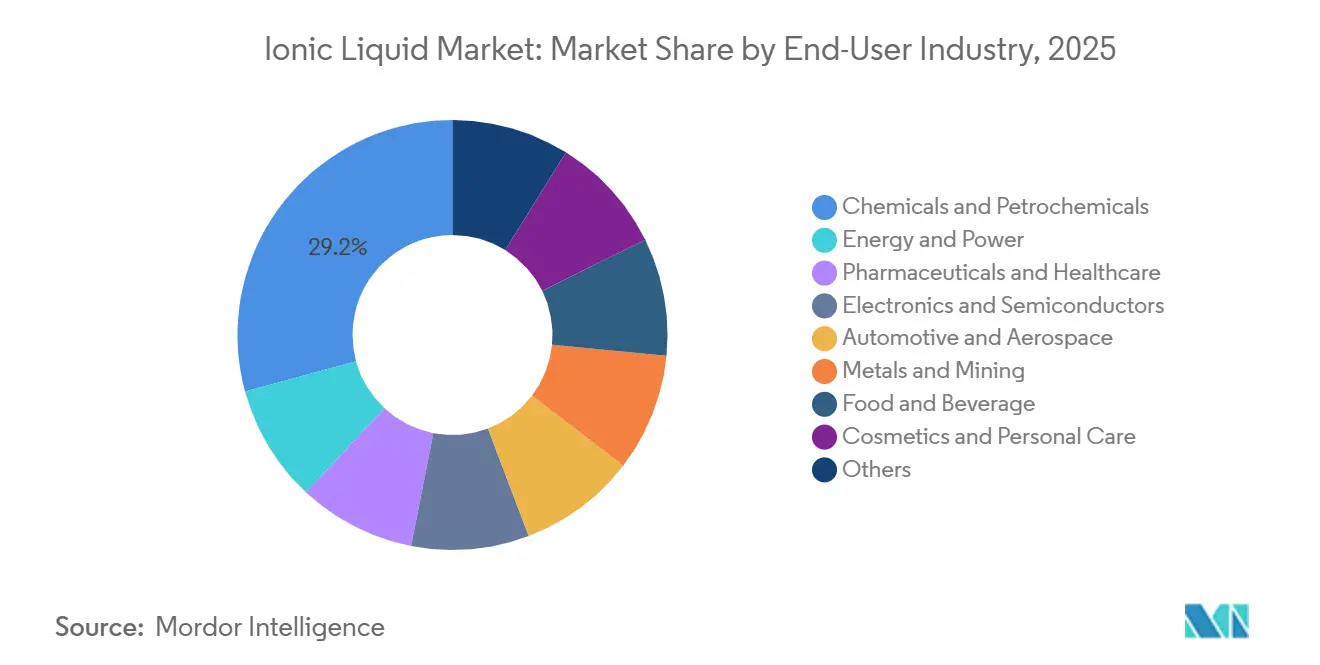

- By end-user industry, Chemicals and Petrochemicals captured 29.23% share in 2025; Energy and Power is on course for the highest 10.13% CAGR through 2031.

- By geography, Asia-Pacific dominated with a 47.13% share in 2025 and is projected to sustain a 10.12% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Ionic Liquid Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |

|---|---|---|---|---|

| Stringent VOC-emission caps catalyzing green-solvent uptake | +1.8% | European Union, North America, China | Medium term (2-4 years) | |

| Surging demand for high-voltage electrolytes from Asian EV gigafactories | +2.3% | Asia-Pacific core, spill-over to North America | Short term (≤ 2 years) | |

| Superior thermal and chemical stability enabling high-performance applications | +1.5% | Global | Long term (≥ 4 years) | |

| Electronics sector pull for antistatic and electrochemical devices | +1.2% | Japan, South Korea, Taiwan, spill-over to EU | Medium term (2-4 years) | |

| Green biorefinery process intensification with task-specific ILs | +1.0% | North America, European Union, Brazil | Long term (≥ 4 years) | |

| Source: Mordor Intelligence | ||||

Stringent VOC-Emission Caps Catalyzing Green-Solvent Uptake

The European Union cut permissible VOC emissions from coating operations to 50 g m⁻² in 2024, pushing formulators toward solvents with negligible vapor pressure, such as ionic liquids. Vapor pressures below 10⁻⁸ Pa eliminate fugitive emissions and help manufacturers sidestep costly oxidizers. China’s GB 37822-2019 regulation enforced an 80 g L⁻¹ VOC limit for interior paints in 2025, prompting a 22% rise in domestic ionic-liquid purchases[1]China Ministry of Ecology and Environment, “GB 37822-2019 Architectural Coatings Standard,” mee.gov.cn. The US Environmental Protection Agency updated its National Emission Standards in 2024 and will oblige legacy facilities to comply by 2027, reinforcing global demand for non-volatile alternatives. Automotive refinishing and industrial-maintenance coatings now specify ionic liquids that ensure substrate adhesion and fast cures while remaining VOC-free.

Surging Demand for High-Voltage Electrolytes from Asian EV Gigafactories

Asia-Pacific battery plants produced 1,200 GWh of lithium-ion cells in 2025, a 28% jump over 2024, with high-nickel cathodes operating above 4.5 V. Conventional carbonate electrolytes degrade at such voltages, whereas pyrrolidinium ionic liquids paired with fluorinated sulfonyl-imide anions retain stability to 5.2 V and enable cell energy density gains of 15-20%. Fast-charge programs above 3C on platforms such as CATL’s Qilin battery employ ionic-liquid co-solvents to suppress lithium plating. South Korea committed KRW 45 billion (USD 34 million) in 2025 to bolster domestic ionic-liquid output and curb reliance on Chinese intermediates[2]Ministry of Trade, Industry and Energy Korea, “Domestic Ionic-Liquid Supply-Chain Initiative,” motie.go.kr.

Superior Thermal and Chemical Stability Enabling High-Performance Applications

Operating windows from −80°C to +400°C position ionic liquids as irreplaceable heat-transfer media in concentrated solar power plants and as aerospace hydraulic fluids. Siemens Energy trialed ionic-liquid additives that cut stainless-steel corrosion by 40% and lengthened maintenance intervals at its Gemasolar site. Pharmaceutical syntheses employing ionic liquids reduced hazardous waste by 35% across three commercial processes in 2025. Perfluorinated variants deliver chemical inertness that meets stringent purity thresholds in uranium-hexafluoride handling and semiconductor plasma etching.

Electronics Sector Pull for Antistatic and Electro-Chemical Devices

Organic light-emitting diode production reached 720 million panels in 2025, utilizing ionic liquids as hole-injection layers that lower drive voltages by 0.8–1.2 V and extend luminance half-life to beyond 100,000 hours. Ionic-liquid copper-plating baths replaced chromic acid, eliminating hexavalent chromium waste while achieving ±2 µm thickness uniformity over 600 mm × 600 mm printed-circuit panels. Japan earmarked JPY 8 billion (USD 53 million) in 2025 for pilot lines at Hitachi Chemical and Mitsubishi Materials to validate ionic-liquid processes in advanced packaging.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |

|---|---|---|---|---|

| Manufacturing cost > USD 500 kg⁻¹ vs. conventional solvents | −1.5% | Global | Short term (≤ 2 years) | |

| Limited eco-toxicity data delaying REACH registrations | −0.8% | European Union, spill-over to North America | Medium term (2-4 years) | |

| HF-feedstock volatility constraining fluorinated-anion supply | −0.6% | Global, acute in Asia-Pacific | Short term (≤ 2 years) | |

| Source: Mordor Intelligence | ||||

Manufacturing Cost more than USD 500 kg⁻¹ vs. Conventional Solvents

Raw materials for imidazolium-bis(trifluoromethylsulfonyl)imide cost USD 380-420 kg⁻¹ before purification, whereas N-methyl-2-pyrrolidone averages USD 2 kg⁻¹. Multistep recrystallization adds 12–18% to processing costs, and fluorinated-anion precursors trade at USD 85-110 kg⁻¹ with 16-week lead times. Continuous-flow plants demonstrated by Evonik in 2024 cut unit costs to USD 290-340 kg⁻¹, yet capital expenditure for 100-t yr⁻¹ capacity tops USD 18 million. Until volumes scale past 500 t yr⁻¹, plastics and lubricant markets remain price sensitive.

Limited Eco-Toxicity Data Delaying REACH Registrations

Fewer than 30 ionic-liquid formulations had complete REACH dossiers by December 2025. Imidazolium cations exhibit EC50 values of 10-100 mg L⁻¹ in Daphnia magna assays, triggering “harmful to aquatic life” labeling. Fluorinated anions persist in activated sludge for more than 180 days, complicating biodegradation assessments. A EUR 4.5 million industry consortium launched in 2024 aims to close data gaps for 12 high-volume products by 2027.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Application: Catalysis Anchors Volume, Energy Storage Drives Margin

Solvents and catalysts accounted for 36.68% revenue in 2025 and will grow at an 8.58% CAGR. Whether stabilizing palladium complexes or pretreating biomass, they form the volume backbone of the ionic liquids market. Energy storage applications, though smaller, will grow with a significant CAGR as redox-flow batteries and hybrid supercapacitors adopt ionic-liquid electrolytes that operate from –40°C to +70°C without auxiliary heating. Process fluids, such as heat-transfer, hydraulic, and lubricant grades, face cost competition from mineral oils priced an order of magnitude lower. Plastics uptake sits largely in antistatic additives for high-value resins, where the ionic liquids market size for engineering polymers is projected to expand modestly, given current price floors near USD 500 kg⁻¹.

Bio-refineries stand out as the fastest-growing niche. Task-specific formulations dissolve lignocellulosic biomass at lower temperatures, raising sugar yields by up to 30% and meeting US Department of Energy cost targets for cellulosic ethanol. Gas-separation membranes, electrochromic windows, and actuator fluids together face lengthy commercialization paths. Overall, applications with direct sustainability benefits and regulatory pull show the strongest momentum within the ionic liquids market.

By Ionic Species: Cation Dominance Meets Anion Innovation

Cation-based products held 58.23% revenue in 2025, anchored by proven imidazolium and pyrrolidinium cores and extensive toxicity data easing approvals. Yet anion-centric innovation drives future growth at a 9.01% CAGR as fluorinated anions widen electrochemical windows and cut viscosity. Bis(trifluoromethylsulfonyl)imide enables lithium-ion conductivities above 10 mS cm⁻¹ at 25 °C, facilitating 8–12% quicker charging in electric-vehicle packs. Phosphonium cations, though less than 5% of volume, are capturing attention for applications above 200 °C where imidazolium decomposes. Suppliers now market modular anion libraries to fine-tune properties, signaling a shift from cation-driven standardization to anion-enabled performance differentiation within the ionic liquids market.

By Function: Task-Specific ILs Command Premium Pricing

Process chemicals, comprising general solvents and reaction media, still generate 57.44% revenue but face price pressure as first-generation patents expire and low-cost Asian producers enter. The functional split is reshaping supplier focus from volume to value, with global majors retreating from commodity segments and doubling down on custom synthesis for pharmaceutical and electronics clients. Performance chemicals, designed for single-function tasks such as CO₂ capture or metal extraction, are growing at a 9.56% CAGR. Functional groups like hydroxyl or amine increase selectivity and justify 50–80% price premiums. BASF’s Basionics line absorbs up to 1.0 mol CO₂ per mol ionic liquid at 40 °C and 1 bar, trimming regeneration energy by 30%.

By End-User Industry: Energy Sector Leads Growth, Chemicals Anchor Volume

Chemicals and petrochemicals contributed 29.23% of 2025 sales, leveraging non-volatile ionic liquids to simplify product separation and slash fugitive emissions. The energy sector will log the fastest 10.13% CAGR as batteries, flow cells, and solar-thermal plants scale. Pharmaceuticals gain from ionic-liquid reaction media that reduce solvent waste by 35%. Electronics deploy ionic-liquid electrolytes, plating baths, and antistatic coatings, supported by Japanese and South Korean investments in advanced displays and packaging. Aerospace and automotive uptake remains limited by multiyear qualification cycles, while metals and mining pilot ionic liquids for rare-earth recovery with efficiencies topping 92%. Together, these sectors reinforce the broadening scope of the ionic liquids market.

Geography Analysis

Asia-Pacific dominated revenue with 47.13% in 2025 and is on a 10.12% CAGR track through 2031. China produced 620 t of ionic liquids in 2025, representing 54% of output, underpinned by vertically integrated supply chains that shave 25–30% off production costs. Domestic policies funding gigafactory electrolytes, semiconductors, and pharmaceutical APIs strengthen demand visibility. South Korea earmarked KRW 45 billion for supply-chain security in 2025, while Japan’s life-sciences sector adopted ionic liquids in 12 commercial active-pharmaceutical-ingredient syntheses, cutting hazardous waste by 28%.

In North America, the US demand benefits from Department of Energy biomass projects and Environmental Protection Agency solvent regulations. Occidental Chemical’s HF facility, slated for 2027, will mitigate fluorinated-anion bottlenecks and shift the regional ionic liquids market size upward. Canada’s oil sands employ task-specific variants for lower-temperature bitumen extraction, whereas Mexico’s EV supply chain is qualifying ionic-liquid thermal-interface materials.

In Europe, Germany, France, and the United Kingdom lead adoption, although limited REACH registrations restrict new-product launches. Continuous-flow synthesis demonstrated by Fraunhofer in 2025 reduced European costs to USD 305-350 kg⁻¹. Brazil anchors South American growth by integrating ionic liquids into sugarcane bagasse biorefineries, while Saudi Arabia pilots them for natural-gas sweetening. Collectively, South America and the Middle East & Africa offer headroom once regional pilot programs convert to commercial scale.

Value Chain Analysis

The ionic liquids value chain begins with upstream chemical intermediates for cation and anion building blocks, where fluorinated-anion precursors and HF-linked inputs are a key constraint and pricing driver. These feedstocks then move into multi-step synthesis and purification, where raw materials make up the bulk of manufacturing cost, and recrystallization or extraction steps add time and yield loss. This cost structure helps explain why many grades still trade above USD 500 per kg, and why process intensification, including continuous-flow synthesis demonstrated by Evonik in 2024, has become a focal point for scaling.

Midstream participants include specialty IL producers and custom synthesis houses that formulate battery-grade electrolytes, solvent and catalyst grades, and task-specific performance chemistries. They also qualify products through customer-specific testing covering electrochemical stability, impurity control, corrosion behavior, and toxicology documentation. Downstream channels are mainly direct sales into chemicals and petrochemicals, energy storage supply chains, electronics materials, and biorefinery programs, where qualification cycles and REACH dossier completeness affect time-to-revenue in Europe. Fewer than 30 formulations had complete REACH dossiers by December 2025, and new end-use pull is also shaping integration patterns, including the 1,000-ton ionic liquid-based regenerated cellulose fiber plant started in Henan Province in July 2025, which shows how large consumers can anchor demand and accelerate localization of supply and recovery infrastructure.

Competitive Landscape

The Ionic Liquid market is moderately fragmented. Missing synthesis standards and dense intellectual-property portfolios force buyers to dual-source or build captive capacity, sustaining fragmentation. Patent filings for ionic-liquid electrolytes rose 18% in 2025, with Chinese applicants accounting for 52%, hinting at future regional shake-ups. Commodity producers compete mainly on price and scale, whereas specialty players leverage application know-how to secure premium margins inside the ionic liquids market.

Ionic Liquid Industry Leaders

Evonik Industries AG

Iolitec Ionic Liquids Technologies GmbH

Merck KGaA

Solvay

BASF

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Near-term whitespace is concentrated in areas where buyers pay for performance or compliance and where qualification can be tied to clear benchmarks, especially high-voltage battery electrolytes, electronics materials, and VOC-free solvent substitution programs. Asia-Pacific battery production reached 1,200 GWh in 2025, and platforms such as CATL's Qilin battery use ionic-liquid co-solvents to address fast-charge lithium plating. This combination creates opportunities for battery-grade purity, tailored anion libraries for wider electrochemical windows, and regional supply security initiatives such as South Korea's KRW 45 billion domestic ionic-liquid output program in 2025.

A parallel opportunity is the shift from lab-scale novelty to industrialized process platforms, where scale, recovery, and lifecycle proof points drive procurement decisions. The start-up of a 1,000-ton ionic liquid-based regenerated cellulose fiber project in China in July 2025 provides a visible commercialization reference for large-volume solvent-loop operations. It also supports ongoing demand for task-specific formulations linked to bio-refinery process intensification. R&D and product-development workflows are changing as well, with machine-learning approaches from Nanjing Tech University in January 2026 and patent activity that includes Asahi Kasei in 2025 pointing to formulation intelligence as a differentiator in screening, safety, and performance tradeoffs. Opportunities remain gated by data and compliance readiness, as Safe and Sustainable by Design and standardized LCA expectations are emphasized in 2026 literature, reinforcing the need to pair scale-up with toxicity and biodegradability evidence that supports faster approvals and customer qualification.

Recent Industry Developments

- May 2026: Nanjing Tech University reported machine-learning methods that cut ionic liquid candidate screening time from over 1,200 seconds to 4.12 seconds. Faster down-selection supports more rapid electrolyte and solvent formulation cycles, which can shorten development timelines for task-specific ionic liquids in batteries and industrial process applications.

- July 2025: The Institute of Process Engineering under the Chinese Academy of Sciences started operations of a 1,000-ton-scale project in Henan Province producing regenerated cellulose fibers using ionic liquids. This commissioning validates ionic liquids in a large-volume solvent-loop use case and supports downstream pull for supply, recovery, and purification capacity tied to textile-grade processes.

- April 2024: Arkema acquired a majority stake of nearly 78% in Proionic, a start-up specializing in ionic liquids for lithium-ion battery electrolytes. The acquisition expands Arkema's position in non-flammable electrolyte chemistries and links ionic liquid development more closely to next-generation battery supply chains.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers ionic liquids that are salts in liquid form below 100 C and are supplied at usable purity for industrial and lab use, mainly as solvents, catalysts, electrolytes, and process or performance fluids across end-use industries.

Scope exclusions: Deep eutectic solvents and molten salts that stay liquid only above 100 C are excluded.

Segmentation Overview

- By Application

- Solvents and Catalysts

- Process and Operating Fluids

- Plastics

- Energy Storage

- Bio-refineries

- Others

- By Type

- Cation

- Anion

- By Function

- Process Chemicals

- Performance Chemicals (Task-specific Ionic Liquids)

- By End-user Industry

- Chemicals and Petrochemicals

- Energy and Power

- Pharmaceuticals and Healthcare

- Electronics and Semiconductors

- Automotive and Aerospace

- Metals and Mining

- Food and Beverage

- Cosmetics and Personal Care

- Others

- By Geography

- Asia-Pacific

- China

- India

- Japan

- South Korea

- Thailand

- Indonesia

- Malaysia

- Vietnam

- Rest of Asia-Pacific

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Russia

- Rest of Europe

- South America

- Brazil

- Argentina

- Colombia

- Rest of South America

- Middle East and Africa

- Saudi Arabia

- United Arab Emirates

- South Africa

- Qatar

- Nigeria

- Egypt

- Rest of Middle East and Africa

- Asia-Pacific

Data Sources, Market Sizing, and Validation

Desk Research

Desk work starts with mapping where ionic liquids are actually consumed so the numbers are not built from a chemistry definition alone. We refer to public sources such as USGS mineral and materials statistics, U.S. EPA chemical reporting and regulatory updates, Eurostat industrial production and trade tables, UN Comtrade customs data, and OECD industry indicators to set demand signals by region and end market.

After that, basic commercial signals are checked through company annual reports, investor presentations, peer reviewed journal articles on ionic liquid applications, and association websites covering chemicals and batteries. We also use trusted press coverage of capacity additions or new product launches. Paid subscriptions are used selectively for company financials and for patent databases, mainly to confirm activity levels and to avoid missing emerging application areas. These examples are not exhaustive, and many other public sources were also used for data collection, validation, and clarification during the research.

Primary Interviews and Surveys

Primary work focuses on validating where adoption is real today and what is still at pilot scale, since ionic liquids can be discussed more than they are purchased. We spoke with producers, formulators, distributors, and downstream users in chemicals, electronics, and energy storage across APAC, EMEA, and the Americas, and then used these inputs to confirm pricing ranges, purity norms, and volume patterns before finalizing assumptions.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 35% | CXOs: 12% | APAC: 45% |

| Mid tier: 46% | Functional/Unit leaders: 37% | EMEA: 30% |

| Smaller Players: 19% | Managers: 51% | Americas: 25% |

Market-Sizing & Forecasting

Sizing is built using a top-down approach where end-use demand pools are reconstructed from chemical production activity, trade flows, and adoption rates of ionic liquids in the main application buckets. Once totals are formed, they are cross-checked with selective bottom-up approximations such as sampled supplier revenue ranges, channel checks, and simple volume by average selling price calculations for a few high-visibility use cases.

Key inputs that move the model include observed purity requirements (for example, 95% and above products for industrial use), the share of ionic liquids used as solvents and catalysts versus process and operating fluids, and the pace of energy storage and electrochemistry projects that specify ionic electrolytes. We also account for the rate of substitution away from conventional volatile solvents where regulations tighten, and regional manufacturing intensity for chemicals and electronics. Where bottom-up signals are incomplete, gaps are handled by applying conservative penetration bands and then stress testing them with interview feedback until the implied pricing and volumes look realistic.

For forecasting, scenario analysis is used so growth can be flexed based on how quickly new applications move from lab work to scaled purchasing. Assumptions on application adoption and price progression are reviewed with experts, and the final trajectory is kept consistent with visible production expansion and patenting intensity, rather than a single straight-line CAGR.

Data Validation & Update Cycle

Model outputs are validated through triangulation across demand indicators, supplier and buyer feedback, and macro signals such as industrial output and trade trends. If a region shows a jump that is not supported by these checks, the drivers are re-opened and the assumptions are reworked, and follow-up calls are triggered when a mismatch cannot be explained with public data.

Before sign-off, the numbers go through multi-step analyst reviews that include variance checks across years, price-volume sanity checks, and consistency tests across related chemical markets. The report is refreshed annually, and interim updates are made when material events occur, such as capacity changes or major regulatory moves that affect solvent choices. Right before delivery, we run a fresh pass to ensure the latest public signals and expert inputs are reflected.

Mordor Intelligence's Ionic Liquid Market Estimate Compared With Other Published Estimates

Published market values for ionic liquids can look far apart because different publishers count different chemistries, treat pilot scale demand differently, and do not always use the same base year or currency timing. In practice, even a small change in what is included can shift the total because this is still a relatively small market by value.

The main gap comes from whether adjacent solvent classes are mixed in, where Mordor Intelligence counts only ionic salts that are liquid below 100 C and explicitly excludes deep eutectic solvents, which keeps the total tied to purchasable ionic liquid volumes and realistic pricing. Differences also show up when one estimate assumes rapid battery scale-up everywhere, while another leans on today's solvents and catalysts demand, and when price is projected using a flat average rather than adjusting by purity and application. Update cadence matters too, since new capacity announcements and regulatory changes can quickly alter the near-term outlook.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 39.89 M (2026) | |

| Industry Publisher A | USD 58.20 M (2024) | Uses an earlier base year framing with a longer horizon, and the scope is organized mainly by cation families, which can lead to broader inclusion of niche formulations and different pricing mixes versus application-led demand pools. |

| Industry Research Group B | USD 53.46 M (2023) | Anchors on a different base year and forecast window, and the application grouping can treat small-volume specialty uses as fully commercialized, which can push up the implied volume and average selling price assumptions. |

The spread in the table is best explained by scope and timing first, and then by how adoption and pricing are carried forward year to year. When inclusions are kept narrow and variables like purity, application mix, and scale stage are checked with real buyers and suppliers, the final size becomes easier to trace and repeat for future updates.

Key Questions Answered in the Report

What is the projected value of the ionic liquids market in 2031?

The ionic liquids market size is expected to reach USD 59.84 million by 2031 based on an 8.45% CAGR during 2026-2031.

Which region will lead future demand for ionic liquids?

Asia-Pacific is forecast to remain the largest and fastest-growing region, registering a 10.12% CAGR through 2031.

Why are ionic liquids gaining traction in electric-vehicle batteries?

Pyrrolidinium and fluorinated-anion ionic liquids widen electrochemical stability windows to 5.2 V, raising battery energy density by up to 20% while suppressing lithium dendrites.

What is the main cost barrier to wider ionic-liquid adoption?

Batch synthesis still exceeds USD 500 kg⁻¹, roughly two orders of magnitude higher than conventional aprotic solvents such as N-methyl-2-pyrrolidone.

How are regulatory agencies influencing ionic-liquid demand?

VOC emission limits in the European Union, China, and the United States are encouraging solvent substitution with non-volatile ionic liquids, accelerating market uptake in coatings and chemical synthesis.

Page last updated on: