Hydrofluoric Acid Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 4.23 Billion |

| Market Size (2031) | USD 5.36 Billion |

| Growth Rate (2026 - 2031) | 4.86% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Hydrofluoric Acid Market Analysis by Mordor Intelligence

The Hydrofluoric Acid Market size was valued at USD 4.03 billion in 2025 and estimated to grow from USD 4.23 billion in 2026 to reach USD 5.36 billion by 2031, at a CAGR of 4.86% during the forecast period (2026-2031). Moderate but steady expansion is underpinned by semiconductor‐driven demand for high-purity grades, the refrigerant industry’s transition toward low-GWP fluorocarbons, and ongoing investments in refinery alkylation technology. Supply chain resilience remains a critical concern because acid-grade fluorspar from China still accounts for more than 60% of global feedstock, exposing producers to price and geopolitical shocks. Regulatory pressure on PFAS emissions and on-site safety protocols continues to reshape production economics, favoring vertically integrated companies with robust compliance systems. Regional capacity additions in South Korea, Mexico, and the United States are gradually diversifying upstream supply while enhancing access to premium-grade volumes for electronics and specialty chemicals.

Key Report Takeaways

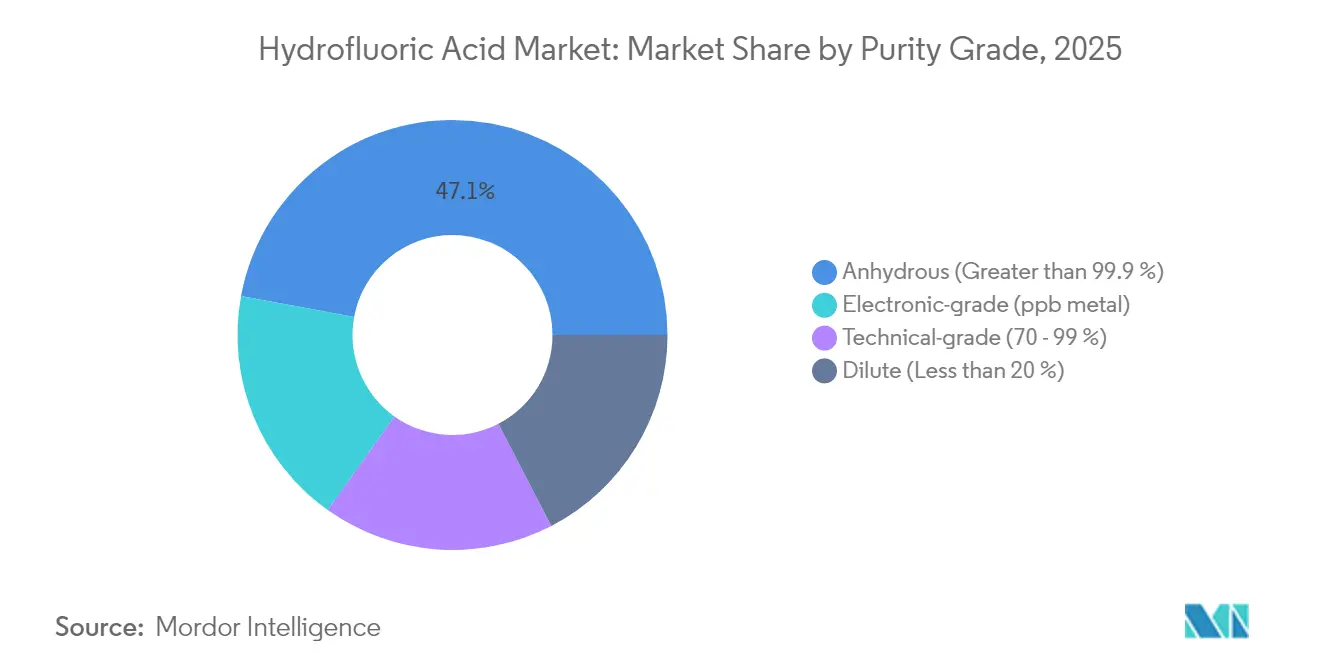

- By purity grade, anhydrous hydrofluoric acid accounted for 47.10% share of the hydrofluoric acid market size in 2025; electronics-grade variants post the fastest growth at 6.18% CAGR.

- By application, fluorocarbon production led with 40.55% of the hydrofluoric acid market share in 2025, while electronic-grade etching is forecast to expand at a 5.85% CAGR to 2031.

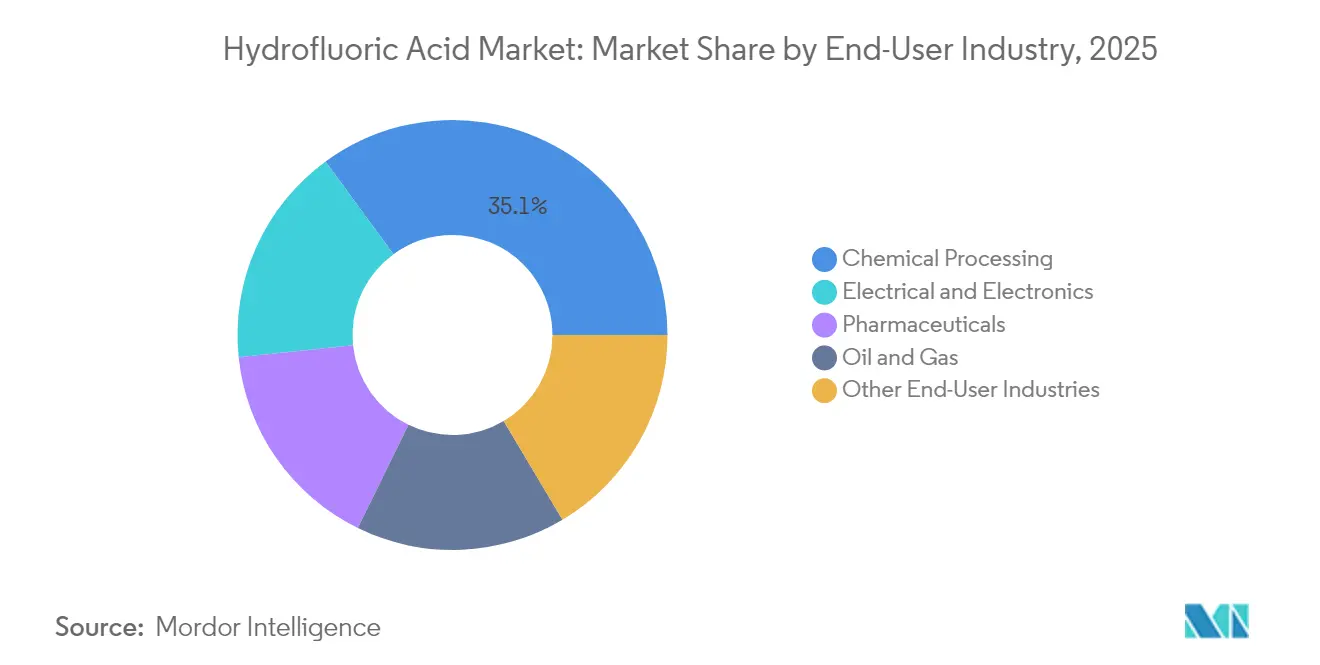

- By end-user industry, chemical processing commanded 35.05% share of the hydrofluoric acid market size in 2025 and electronics are advancing at a 5.92% CAGR through 2031.

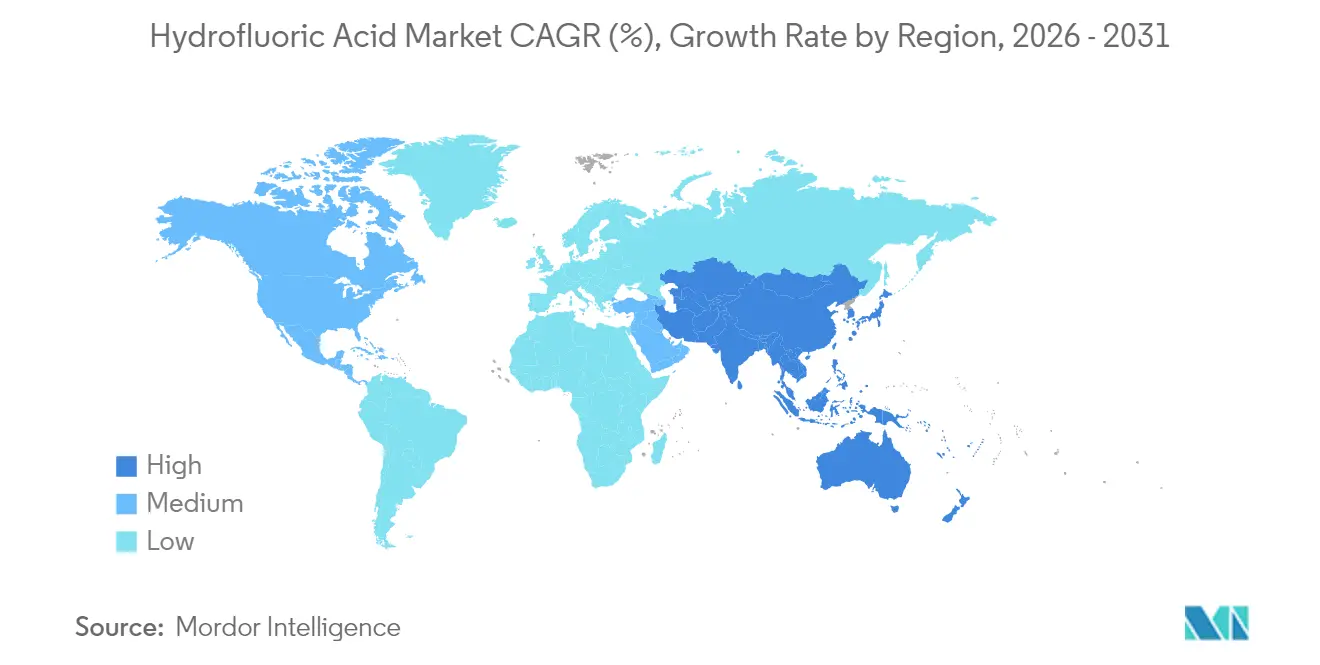

- By geography, Asia-Pacific captured 44.05% revenue share in 2025 and is projected to grow at a 5.73% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Hydrofluoric Acid Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Shift toward electronics-grade hydrofluoric acid in advanced semiconductor fabs | +1.8% | Asia-Pacific core, spill-over to North America | Medium term (2-4 years) |

| Rising fluorocarbon demand for refrigerants | +1.2% | Global | Long term (≥ 4 years) |

| Regulatory push for cleaner alkylation catalysts in refineries | +0.9% | North America & Europe | Short term (≤ 2 years) |

| Increasing demand from chemical processing industry | +0.7% | Global | Long term (≥ 4 years) |

| Growing utilization in glass and optic production | +0.5% | Asia-Pacific & Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Shift Toward Electronics-Grade Hydrofluoric Acid in Advanced Semiconductor Fabs

Growing chip complexity forces fabs to tighten metallic impurity thresholds to parts-per-billion levels, a specification that transforms cost structures because electronics-grade acid prices can sit three to five times higher than technical grades. South Korean suppliers have doubled purification capacity to secure domestic demand and shorten lead times for multinational device makers, illustrating how localization strategies insulate the hydrofluoric acid market from export controls[1]Honeywell, “Investor Presentation Q2 2025,” honeywell.com . Fab expansions in Texas, Arizona, and Dresden echo this pattern, with procurement teams insisting on dual sourcing to mitigate single-country risk. Ultra-high-purity volumes require proprietary distillation, ion exchange, and sub-ppb filtration trains that commodity producers often lack. Capital intensity runs above USD 50 million for a 20 kilotons per year electronics-grade line, creating natural barriers to entry. Because semiconductors embed hydrofluoric acid in multiple wet-bench and vapor-phase etch steps, per-wafer consumption scales directly with line‐width reduction, locking in long-term pull for the hydrofluoric acid market.

Rising Fluorocarbon Demand for Refrigerants

Hydrofluoric acid remains unavoidable in hydrofluorocarbon and hydrofluoro-olefin synthesis, which together consume nearly 60% of industrial hydrogen fluoride output. Air-conditioning adoption in Southeast Asia and Latin America is pushing new capacity for HFO-1234yf, HFO-1234ze, and related blends, all of which require higher intermediate purity compared with legacy HCFCs. Honeywell’s Solstice range demonstrates how each kilogram of next-generation refrigerant embeds roughly 0.6 kilograms of hydrofluoric acid despite lower global warming potential, lifting aggregate acid offtake in step with regulatory phase-downs. Regional quotas under the Kigali Amendment accelerate line-debottlenecking in China, India, and the Gulf, reinforcing the structural link between fluorocarbon growth and the hydrofluoric acid market. Because end-user industries pay green-premium pricing for compliant refrigerants, margin capture shifts upstream to integrated producers that can supply both acid and finished fluorochemicals.

Regulatory Push for Cleaner Alkylation Catalysts in Refineries

Roughly 90% of United States gasoline refining capacity relies on hydrofluoric acid alkylation, yet major incidents in 2019-2024 prompted OSHA and the US Chemical Safety Board to strengthen inspections[2]US Chemical Safety Board, “Investigation Report 2024-05,” csb.gov . New fencing distance, water curtain, and remote-operation requirements add as much as USD 200 million in retrofit costs for a single refinery, shifting demand from low-purity bulk acid toward stabilized blends with proprietary inhibitor packages. The hydrofluoric acid market therefore gains a value-over-volume tailwind as refiners favor suppliers offering cradle-to-grave technical stewardship. Alternative sulfuric acid alkylation technology carries higher spent-acid disposal costs and energy penalties, leaving hydrofluoric acid catalysts competitively entrenched. Short-cycle demand spikes arise when Tier-3 gasoline sulfur mandates force refiners to maximize octane-rich alkylate output, further tightening near-term supply.

Increasing Demand from Chemical Processing Industry

Fluorinated pharmaceuticals, agrochemicals, and specialty polymers all rely on hydrofluoric acid’s capacity to create strong carbon-fluorine bonds that enhance molecular stability. One in four approved small-molecule drugs released since 2024 contains at least one fluorine atom, lifting acid-derived reagent demand across contract manufacturing organizations. Stainless-steel pickling still absorbs large technical-grade volumes because hydrofluoric acid efficiently removes chromium-rich oxide scales at lower bath temperatures than nitric mixtures, improving throughput for rolled sheet producers. The fluoropolymer segment adds incremental pull as battery and hydrogen applications employ PTFE, PVDF, and FEP components for chemical resistance. Diverse downstream consumption cushions cyclicality in any single vertical and broadens the hydrofluoric acid market footprint.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Extreme toxicity driving stricter on-site inventory limits | -1.4% | Global | Short term (≤ 2 years) |

| Volatility in raw material prices | -0.8% | Global | Medium term (2-4 years) |

| High operational and transport costs | -0.6% | Global | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Extreme Toxicity Driving Stricter On-Site Inventory Limits

Hydrofluoric acid causes rapid tissue necrosis and systemic calcium depletion, compelling regulators to tighten permissible exposure limits to 3 ppm over an eight-hour shift. Facilities must stock calcium gluconate antidote, install redundant scrubber systems, and train medical staff, elevating fixed costs for new entrants. The EPA’s expansion of PFAS oversight under CERCLA extends cradle-to-grave liability for fluorine-bearing waste streams, forcing users to upgrade containment liners and flare systems. Insurance premiums for high-hazard chemical plants have risen 25% since 2024, and underwriters often cap hydrofluoric acid inventories at 10 days of normal consumption. Smaller firms without balance-sheet depth consequently outsource processing steps, limiting direct demand growth for the hydrofluoric acid market.

Volatility in Raw Material Prices

Acid-grade fluorspar averages 70-80% of variable production cost, exposing margins to price spikes when Chinese mines suspend output for environmental audits. Spot prices hit USD 450 per ton in late 2024, up 5% year on year, compressing profitability for independent converters. Mexico supplies nearly three-quarters of United States fluorspar imports, which mitigates shipping distance but concentrates geopolitical risk. Pilot plants recovering hydrofluosilicic acid from fertilizer waste streams show promise, yet capex intensity and product purity issues keep commercialization three to five years away. Until secondary feedstock solutions scale, the hydrofluoric acid market remains tethered to fluorspar price cycles, complicating long-term contract negotiations with downstream customers.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Purity Grade: Electronics Demand Reconfigures Spec Requirements

Anhydrous hydrofluoric acid retained 47.10% revenue share in 2025 because low-water content remains indispensable for fluorocarbon and alkylation processes that cannot tolerate dilution. Electronics-grade material, although representing a smaller base, posts the quickest climb with a 6.18% CAGR as next-generation wafer fabs lock in multiyear offtake agreements. The hydrofluoric acid market size for electronics-grade volumes is projected to reach USD 1.16 billion by 2031, reflecting sustained fab expansion in the United States, South Korea, and Taiwan. Ultra-purity vendors leverage proprietary distillation, membrane filtration, and point-of-use submicron polishing to meet sub-10 ppb metal targets. These capabilities require advanced analytics, including ICP-MS and TOC monitoring, which elevate barrier-to-entry thresholds.

Technical-grade hydrofluoric acid continues to serve mature niches such as glass frosting, silicon cleaning for solar cells, and titanium pickling, where cost outweighs ultra-pure characteristics. Nonetheless, incremental substitution is visible when display manufacturers migrate toward cleaner chemistries to minimize pixel defects, subtly boosting demand for mid-range purity blends. Because auditorium-sized flat-panel glass substrates exceed 8 m², even fractional yield gains translate into tangible savings, positioning the hydrofluoric acid market as an enabler of capital efficiency in display fabrication.

By Application: Etching Surges Beyond Refrigerant Foundations

Fluorocarbon production dominated with 40.55% of 2025 revenue, anchored by large-scale installations in China, the United States, and the Gulf that feed HVAC, aerosol, and foam insulation chains. Refrigerant formulators seek low-GWP molecules such as HFO-1234yf, lifting per-kilogram acid consumption due to multi-step synthesis routes that incorporate additional chlorination and isomerization stages. In parallel, electronic-grade etching rides a 5.85% CAGR on the back of rising lithography complexity and 3D NAND structures that demand repeat oxide removal cycles. The hydrofluoric acid market size for semiconductor etching is projected to jump from USD 920 million in 2026 to USD 1.22 billion by 2031.

Alkylation remains a resilient demand pillar because gasoline blending norms limit options for octane enhancement. While refinery counts contract in Europe, throughput concentrates into mega-sites that maintain or upgrade existing hydrofluoric acid units, insulating aggregate acid pull. Cleaning agents in precision optics, photovoltaic cells, and quartzware sustain niche consumption patterns. Organofluorine compound synthesis within pharma and agrochem benefits from medicinal chemistry’s tilt toward fluorination that improves bioavailability, offering upside to specialized suppliers fluent in high-selectivity fluorination technologies.

By End-User Industry: Electronics Outpaces Legacy Chemicals

Chemical processing held 35.05% of revenue in 2025 because fluoropolymer, fluorocarbon, and specialty intermediates rely on hydrofluoric acid for strategic bond-formation steps. Electronics manufacturing, however, grows fastest at 5.92% CAGR, lifting the hydrofluoric acid market share for this segment as fabs scale 5 nm to 2 nm nodes. Each 100 mm wafer run can require more than 25 discrete HF etch or clean cycles, magnifying sensitivity to contamination and supply disruption. Device makers therefore enter take-or-pay contracts to lock in stable, high-purity deliveries, deepening vertical integration between acid producers and semiconductor chemical suppliers.

Oil and gas’s reliance on hydrofluoric acid for alkylate production provides baseline demand, yet growth remains muted as EV adoption trims gasoline consumption in OECD economies. Pharmaceutical innovation offsets this headwind because 30% of pipeline small-molecule drugs now contain at least one fluorinated motif that demands hydrofluoric acid inputs. Renewable energy storage pushes further diversification; PVDF binders in lithium-ion cells and fluorinated membranes for hydrogen electrolyzers both embed hydrofluoric acid in their supply chains, ensuring continued relevance for the hydrofluoric acid market across the energy transition.

Geography Analysis

Asia-Pacific accounted for 44.05% of 2025 revenue and is set to advance at a 5.73% CAGR, anchored by integrated fluorochemical hubs in China and rapid semiconductor investment across South Korea and Taiwan. China controls more than 60% of global acid-grade fluorspar extraction, providing cost advantage yet concentrating geopolitical risk. Seoul’s national materials program spurred Soulbrain and other producers to lift electronics-grade capacity, reducing exposure to Japanese supply chains once dominant in ultra-pure acid. India’s pharmaceutical cluster in Gujarat and Andhra Pradesh underwrites additional technical-grade demand, while ASEAN panel makers in Vietnam and Thailand adopt HF-based cleaning lines for glass substrates.

North America ranks second due to refinery alkylation assets and the CHIPS and Science Act, which accelerates fab construction in Arizona, Texas, and New York. Sunlit Chemical’s USD 100 million Phoenix plant will supply up to 30 kilotons per year of electronics-grade hydrofluoric acid to nearby fabs, underscoring localization moves that reshape the regional hydrofluoric acid market. Mexico’s dominance in US fluorspar imports enhances supply security yet highlights concentration risk in the event of mining disruptions or port bottlenecks along the Gulf Coast.

Europe shows steady but slower growth as PFAS action plans raise compliance costs. France targets a phased ban on PFAS in consumer products by 2030, motivating refiners and fluoropolymer firms to invest in abatement technologies that include closed-loop HF recovery. Germany’s BASF and Arkema maintain captive fluorspar contracts to shield against price spikes, while Belgium’s integrated chemical corridor leverages Honeywell-licensed technology for low-carbon plastics that still require hydrofluoric acid intermediates. These moves sustain the hydrofluoric acid market despite tougher environmental rules.

The Middle East and Africa present nascent opportunities tied to petrochemical diversification. Saudi Arabia’s EV Metals Group complex in Jubail includes lithium-ion cathode materials that will incorporate PVDF binders, driving localized hydrofluoric acid needs. UAE refrigerant ventures targeting African HVAC markets also drive incremental volumes. Latin America benefits from air-conditioning growth in Brazil and Mexico, prompting regional refrigerant synthesis that consumes domestically produced acid.

Competitive Landscape

The hydrofluoric acid market displays moderate fragmentation, with the top five producers controlling roughly 45% of global capacity. Honeywell, Solvay, Daikin, and Mexichem maintain vertical integration into fluorspar or fluorochemical derivatives, hedging raw-material volatility and unlocking economies in logistics. Daikin’s development of anhydrous hydrofluoric acid synthesis using Mexican fluorspar reduces reliance on Chinese feedstock, reflecting geographic hedging strategies.

Smaller regional players struggle with compliance costs for OSHA, EPA, and REACH requirements, leading to consolidation opportunities. Patent filings covering additive-free purification and low-temperature fluorspar activation reached a ten-year high in 2024, indicating a technological race toward cost-effective ultra-pure production.

Hydrofluoric Acid Industry Leaders

Honeywell International Inc.

LANXESS

Solvay

DAIKIN INDUSTRIES, Ltd.,

Orbia Fluor & Energy Materials

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: In Ulsan, South Korea, Toyo Engineering Korea clinched a turnkey contract from BGF Ecospecialty to construct a 50,000 tpa anhydrous hydrogen fluoride plant, with operations set to commence in 2026. This project aims to strengthen the region's chemical manufacturing capabilities.

- October 2024: Tanfac Industries, through internal accruals, undertook an expansion worth INR 100 crore (approximately USD 12 million), successfully doubling its hydrofluoric acid capacity to 29,500 MTPA. This expansion positions the company to meet growing domestic and international demand while boosting its market competitiveness.

Global Hydrofluoric Acid Market Report Scope

The Hydrofluoric Acid Market report includes:

| Anhydrous (Greater than 99.9 %) |

| Electronic-grade (ppb metal) |

| Technical-grade (70 - 99 %) |

| Dilute (Less than 20 %) |

| Oil Refining |

| Cleaning Agent |

| Etching Agent |

| Fluorocarbon Production |

| Organofluorine Compounds |

| Other Applications |

| Oil and Gas |

| Chemical Processing |

| Pharmaceuticals |

| Electrical and Electronics |

| Other End-User Industries |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle East and Africa |

| By Purity Grade | Anhydrous (Greater than 99.9 %) | |

| Electronic-grade (ppb metal) | ||

| Technical-grade (70 - 99 %) | ||

| Dilute (Less than 20 %) | ||

| By Application | Oil Refining | |

| Cleaning Agent | ||

| Etching Agent | ||

| Fluorocarbon Production | ||

| Organofluorine Compounds | ||

| Other Applications | ||

| By End-User Industry | Oil and Gas | |

| Chemical Processing | ||

| Pharmaceuticals | ||

| Electrical and Electronics | ||

| Other End-User Industries | ||

| By Geography | Asia-Pacific | China |

| Japan | ||

| India | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current Hydrofluoric Acid Market size?

The market is valued at USD 4.23 billion in 2026 and is forecast to reach USD 5.36 billion by 2031 at a 4.86% CAGR.

Which region leads the hydrofluoric acid market?

Asia-Pacific holds 44.05% of 2025 revenue and posts the quickest regional CAGR of 5.73% through 2031, driven by semiconductor and refrigerant demand.

Why is electronics-grade hydrofluoric acid growing so fast?

Advanced semiconductor fabs require sub-ppb purity levels for wafer etching; these specifications push electronics-grade volumes to a 6.18% CAGR through 2031.

How do fluorspar prices affect the hydrofluoric acid market?

Fluorspar makes up 70-80% of variable costs, so price swings directly impact producer margins and can restrict supply when Chinese mines curtail output.

Page last updated on: