Qatar Investment Opportunities Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

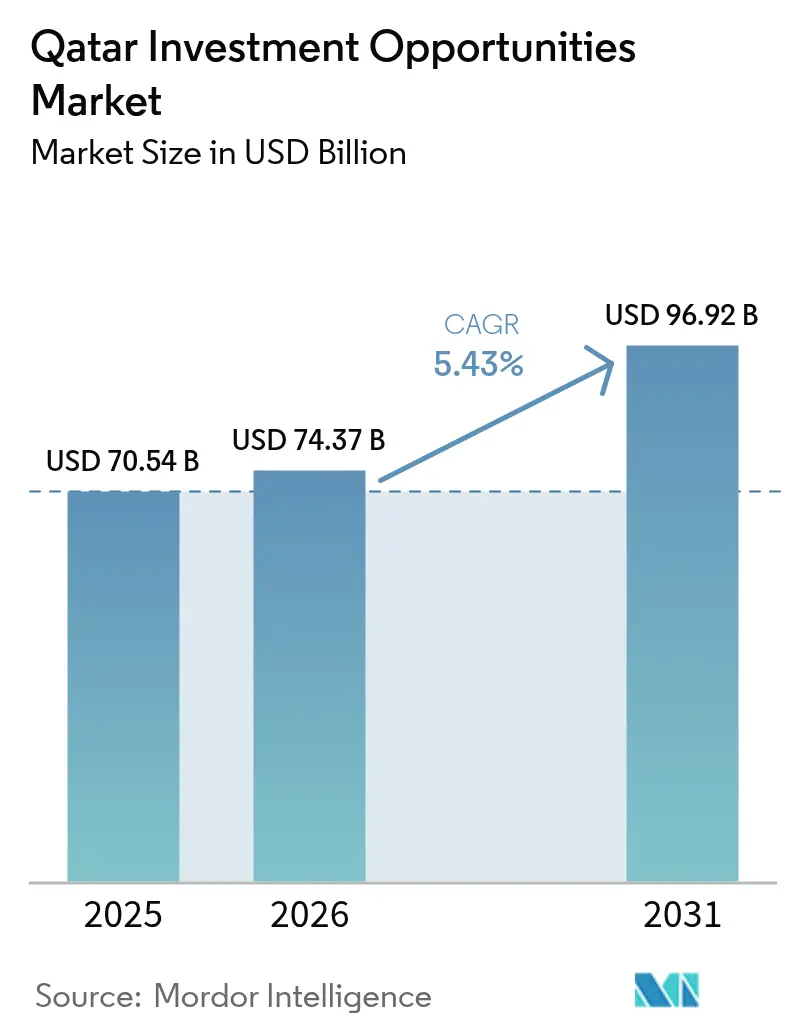

| Base Year Market Size (2025) | USD 70.54 Billion |

| Market Size (2026) | USD 74.37 Billion |

| Market Size (2031) | USD 96.92 Billion |

| Growth Rate (2026 - 2031) | 5.43% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Qatar Investment Opportunities Market Analysis by Mordor Intelligence

The Qatar Investment Opportunities Market size market size in 2026 is estimated at USD 74.37 billion, growing from 2025 value of USD 70.54 billion with 2031 projections showing USD 96.92 billion, growing at 5.43% CAGR over 2026-2031. Robust execution of the USD 225 billion National Vision 2030 capital pipeline, a record-setting North Field LNG expansion, and accelerating digital transformation propel steady value creation[1]https://imo.gov.qa/media-centre/insights/which-key-sectors-will-shape-qatar-s-future-economy. Public-sector spending remains the anchor, yet liberalized foreign-ownership rules and a USD 1 billion incentive program channel faster capital inflows from abroad. Diversification gains traction as information and communication technology (ICT) outpaces all other sectors, while tourism leverages World Cup legacy assets to amplify visitor arrivals. Greenfield megaprojects dominate project flow, reflecting a policy preference for purpose-built, technology-ready infrastructure that embeds sustainability from inception.

Key Report Takeaways

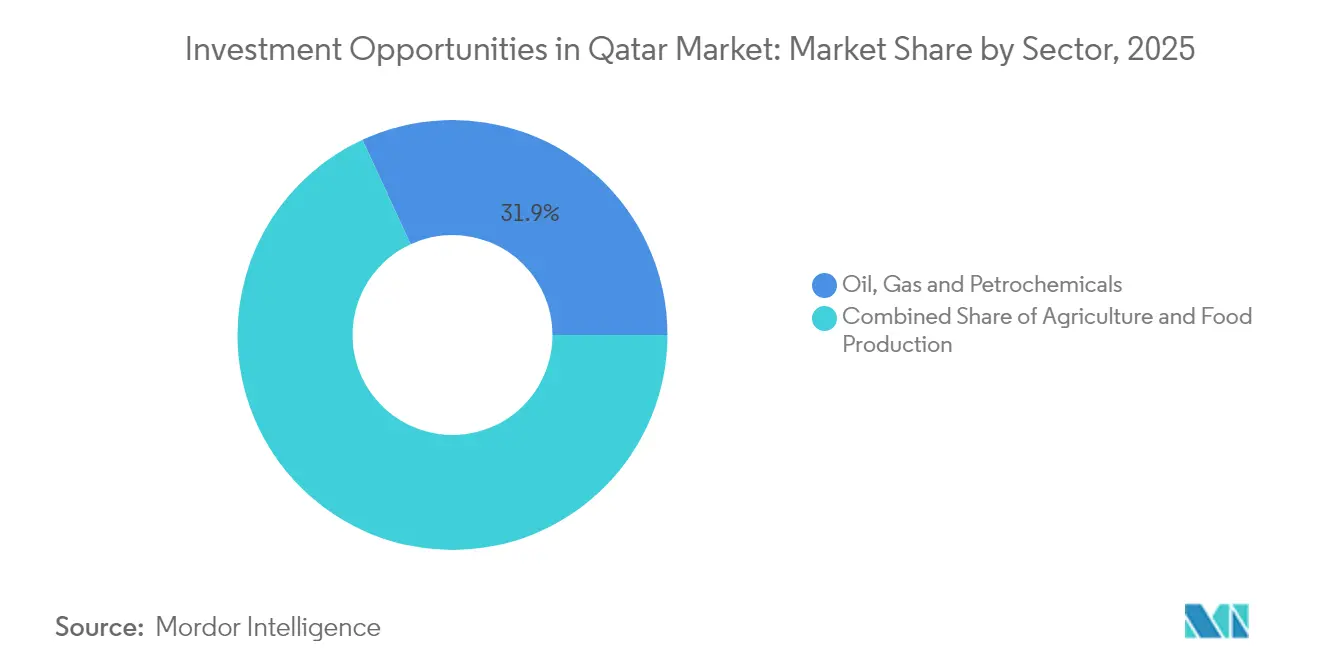

- By sector, Oil, Gas & Petrochemicals led with 31.88% Qatar Investment Opportunities Market share in 2025, while Information & Communication Technology recorded the highest projected CAGR at 11.62% through 2031.

- By financing source, public-sector CAPEX accounted for 47.02% of the Qatar Investment Opportunities Market size in 2025, whereas foreign direct investment is expected to advance at a 9.31% CAGR to 2031.

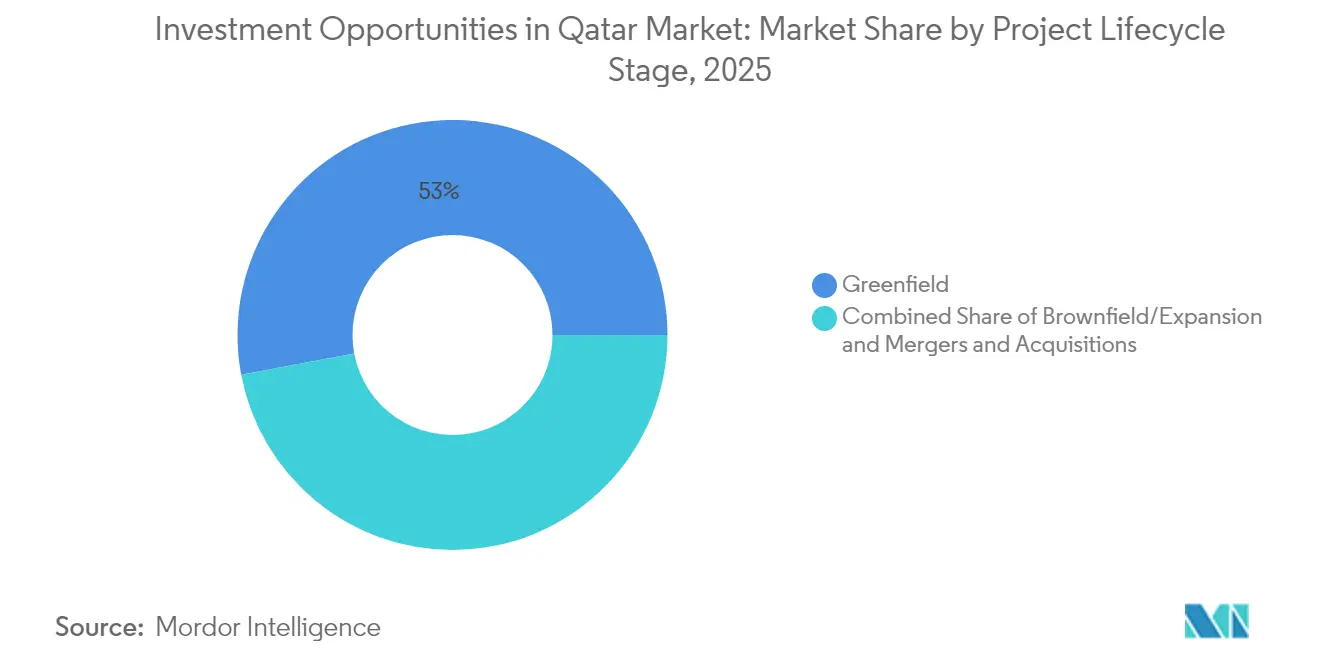

- By project lifecycle stage, greenfield developments commanded 52.96% of the Qatar Investment Opportunities Market size in 2025 and are expanding at a 7.15% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Qatar Investment Opportunities Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| 10-year, USD 225 billion National Vision 2030 CAPEX allocations | +2.1% | National, with spillover to regional GCC markets | Long term (≥ 4 years) |

| Robust government-backed infrastructure pipeline | +1.8% | Global, with core focus on Qatar domestic projects | Medium term (2-4 years) |

| World-class LNG expansion funding (2025-2029) | +1.4% | Global, with primary operations in Qatar and international partnerships | Medium term (2-4 years) |

| Rapid digital-banking & fintech adoption (post-Qatar FinTech Hub) | +1.2% | National, with technology transfer to regional markets | Short term (≤ 2 years) |

| Mandatory local-content rules for state procurement | +0.9% | National, with emphasis on Doha, Lusail, and industrial zones | Short term (≤ 2 years) |

| Satellite free-zone regime attracting Industry 4.0 manufacturers | +0.7% | National, concentrated in Qatar Free Zones and Lusail City | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

10-Year, USD 225 Billion National Vision 2030 CAPEX Allocations

The Third National Development Strategy steers capital toward tourism, digitalization, and manufacturing, lowering dependence on raw hydrocarbons. Manufacturing alone targets QAR 70.5 billion (USD 19.36 Billion) in value-added output by 2030, opening demand for industrial automation and supply-chain solutions. Financial‐services reforms embedded in the Third Financial Sector Strategic Plan lift sectoral GDP contribution to QAR 84 billion (USD 23.06 Billion) by 2030, carving space for fintech, takaful, and sukuk structuring. Education partnerships flourish as Doha invites global universities to co-locate research centers that bolster human-capital objectives. The multi-sector mix cuts concentration risk and allows investors to redeploy capital across complementary verticals, improving portfolio resilience.

Robust Government-Backed Infrastructure Pipeline

Ashghal’s QAR 81 billion (USD 22.23 Billion) capital program accelerates highway, utility, and urban upgrades, weaving smart-city sensors and GSAS sustainability standards into every tender. Contractors able to certify ISO 14001 and OHSAS 18001 compliance gain a clear edge, since regulatory audits now form part of milestone payments. Hamad International Airport and Hamad Port deliver multimodal connectivity to more than 100 destinations, raising the value proposition for logistics, construction materials, and facility management firms. Predictable funding and phased procurement reduce counterparty risk and encourage long-term teaming agreements with international engineering majors. Parallel investments in public transit and district cooling widen the addressable market for green technology providers and environmental-monitoring services.

World-Class LNG Expansion Funding (2025-2029)

The North Field East, South, and West phases lift LNG capacity from 77 million tpa to 142 million tpa, the largest single addition worldwide. QatarEnergy’s ventures with ExxonMobil and Shell call for advanced liquefaction trains, cryogenic heat exchangers, and marine export terminals that amplify contract opportunities in engineering, rotating equipment, and maintenance. Integrated blue-ammonia capacity of 1.2 million tpa by 2026 anchors the country’s low-carbon hydrogen roadmap, attracting carbon-capture suppliers and green-shipping insurers. Long-term offtake contracts with China, India, and several European utilities strengthen revenue visibility, thereby improving debt headroom for ancillary petrochemical and shipping projects.

Rapid Digital-Banking & Fintech Adoption (Post-Qatar FinTech Hub)

Qatar Central Bank’s FAWRAN instant-payments rail and sandbox regime shortens product-to-market cycles for e-wallets, reg-tech, and blockchain applications. The Qatar Financial Centre’s Digital Asset Framework permits tokenization of real-world assets under Sharia principles, drawing custody vendors and cybersecurity startups to Doha. Commercial lenders mimic Qatar Islamic Bank’s mobile-first model, spurring competition in robo-advice, cross-border remittances, and buy-now-pay-later services. Government cloud-first mandates propel hyperscale datacenter builds and encourage uptake of AI-driven analytics across ministries and utilities. Sector digitalization thus broadens revenue streams for software integrators and managed-services providers.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Tight labour-market localisation quotas | -1.1% | National, affecting all sectors with Qatarization requirements | Long term (≥ 4 years) |

| Carbon-intensity scrutiny from EU CBAM & global investors | -0.8% | Global, particularly affecting energy exports to European markets | Medium term (2-4 years) |

| Persistent Tier-2 sanctions risk in wider GCC politics | -0.6% | Regional GCC, with spillover effects on international partnerships | Medium term (2-4 years) |

| High project execution costs vs. Bahrain & Oman peers | -0.4% | National, with regional competitive implications across GCC markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Tight Labour-Market Localisation Quotas

Law 12 of 2024 obligates employers to prioritize nationals, pushing multinationals to re-engineer workforce mixes and invest in productivity software. Tawteen’s ICV certification increases administrative burden, yet fosters joint-venture structures that nurture domestic SMEs. HR analytics, vocational institutes, and e-learning platforms benefit as corporates scramble to close skills gaps. International firms establish apprenticeship schemes that pipeline graduates directly into technician and supervisory roles. Performance-based evaluation replaces headcount ratios, favoring companies able to demonstrate tangible knowledge transfer and career progression for Qatari employees.

Carbon-Intensity Scrutiny from EU CBAM & Global Investors

The EU Carbon Border Adjustment Mechanism applies embedded-carbon tariffs on steel, aluminum, cement, fertilizers, and hydrogen exports, prompting retrofits in process heat and fugitive-emission control equipment. Qatar’s USD 2.5 billion green-bond issuance in 2024 finances renewable integration and environmental audits, catalyzing demand for ESG advisers and portfolio-impact software. Utility-scale solar plants at Al-Kharsaah and Dukhan lower grid carbon intensity, enabling exporters to claim cleaner power inputs. Investors elevate due diligence thresholds, requiring third-party assurance of Scope 1-3 data, which boosts revenue for specialized auditors and consultancies. Mandatory GSAS certification on public megaprojects locks in long-run demand for energy-efficient building materials.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Sector: Energy Dominance Drives Diversification

Oil, Gas & Petrochemicals accounted for 31.88% of the Qatar Investment Opportunities Market Share in 2025 and remains the backbone, even as its CAGR moderates to mid-single digits. The segment’s anchor, the North Field scale-up, lifts LNG capacity from 77 mtpa to 142 mtpa by 2030, ensuring durable feedstock for downstream players. Information & Communication Technology, while smaller, delivers the fastest momentum with an 11.62% CAGR, fueled by hyperscale cloud zones and a sandbox-backed fintech cluster that diversifies digital revenue streams. Construction & infrastructure rides the USD 225 billion Vision 2030 pipeline, embedding smart-city sensors and GSAS standards that widen adoption of green materials. Travel, tourism & hospitality targets 6 million visitors by 2030 as event-led demand keeps occupancy elevated, translating to double-digit growth in hotel keys. Manufacturing & industrial production eyes QAR 70.5 billion (USD 19.36 Billion) ) in value-added output, harnessing competitively priced fuel to scale specialty chemicals and food processing lines. Healthcare & life sciences expand through tertiary-care PPP hospitals and regional medical-tourism inflows, rounding out a multisector fabric that dilutes single-commodity risk.

By Financing Source: Public Leadership Enables Private Growth

Public-sector CAPEX supplied 47.02% of total deployment in 2025, anchoring the Investment opportunities in qatar market with sovereign balance-sheet strength. Yet foreign direct investment, projected at a 9.31% CAGR, accelerates fastest as 100% foreign ownership and simplified licensing unlock project pipelines. Domestic private investment layers on via venture rounds and QSE listings, leveraging incubators like Qatar FinTech Hub to crowd in capital. Sovereign & pension funds, led by QIA’s USD 500 billion U.S. commitment, spread allocations across infrastructure and digital platforms, deepening portfolio diversification.

By Project Lifecycle Stage: Greenfield Preference Reflects Development Strategy

Greenfield ventures represented 52.96% of the Qatar Investment opportunities in the market in 2025 and are growing at a 7.15% CAGR, epitomized by the QAR 20 billion (USD 5.49 Billion) Simaisma tourism city that integrates IoT and net-zero power from inception. Brownfield/expansion programs modernize legacy LNG trains and petrochemical complexes, offering lower execution risk but still meaningful contract value. M&A remains muted, as policymakers reward investors who build capabilities locally rather than merely swap assets

Competitive Landscape

The market exhibits moderate concentration: state-backed entities QatarEnergy, Qatar Investment Authority, and Industries Qatar anchor core sectors, together controlling an estimated 55% of deployed capital. International partners succeed when they participate in local content plans, set up knowledge centers, and endorse multi-decade offtake structures. For example, QatarEnergy’s North Field joint ventures with ExxonMobil and Shell combine financial muscle with cutting-edge liquefaction technology, accelerating project timelines while sharing geological risk.

Across ICT, global hyperscalers pair with Ooredoo and Meeza to build cloud regions, adding managed-service layers that advance digital-first public-service objectives. In construction, Hyundai Engineering and CCC leverage modular fabrication yards to overcome local labor quotas, meeting schedule targets while training Qatari managers. The finance arena witnesses cross-listing agreements that let Qatari start-ups tap regional exchanges, raising growth capital without early exits.

Strategic themes converge around sustainability, digitalization, and regional scale-ups. Corporations embed AI for predictive maintenance in process industries, pilot carbon-capture units in gas plants, and deploy blockchain for trade-finance digitization. These moves align with Vision 2030 criteria, making them eligible for preferential land grants and tax exemptions. Competitive intensity is therefore measured more by integration depth and compliance agility than by raw bidder counts.

Qatar Investment Opportunities Industry Leaders

QatarEnergy

Ooredoo Q.P.S.C.

Qatar Airways Group

Industries Qatar

Qatar Diar Real Estate Co.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Qatar Investment Authority announced a USD 500 billion investment commitment for US markets over the next decade, establishing QIA as one of the largest sovereign wealth fund allocations to American assets and creating opportunities for co-investment and partnership structures across multiple sectors.

- December 2024: Qatar Tourism reported surpassing 5 million visitors in 2024, representing a 25% increase from 2023 and exceeding the targeted 8.8 million room nights with over 10 million room nights sold, demonstrating sustained post-World Cup momentum and tourism sector resilience.Concurrently, Sauber is actively fortifying its future, recently unveiling a series of new recruits.

- November 2024: Formula 1 Qatar Airways Grand Prix generated record hotel performance with 83.6% occupancy (+17.5% YoY) and 42% RevPAR increase, highlighting Qatar's success in leveraging major events to drive tourism and hospitality sector growth.

- October 2024: QatarEnergy and Chevron Phillips Chemical Company finalized a USD 6 billion petrochemical project agreement, increasing polyethylene production capacity by 82% with operations scheduled to commence by 2026, strengthening Qatar's downstream energy sector positioning.

- June 2024: Bloomberg reported Qatar's Simaisma Project launch, featuring QAR 20 billion (USD 5.5 billion) investment in tourism development including a theme park larger than Disney's Magic Kingdom, demonstrating Qatar's commitment to large-scale diversification projects.

Qatar Investment Opportunities Market Report Scope

Analysis of Key Sectors and Investment Opportunities in Qatar Market is segmented by sector (agriculture, dairy, and meat, manufacturing, oil & gas, construction, real estate, distributive trade (wholesale and retail trade), travel and tourism, financial services, healthcare, information and communication technology, transportation and storage). For each segment, the market sizing and forecasts have been done on the basis of value (USD). The Report covers a comprehensive background analysis of Investment opportunities in the Qatar Market covering the current market trends, restraints, technological updates and detailed information on various segments and competitive landscape of the industry.

| Agriculture & Food Production |

| Manufacturing & Industrial Production |

| Oil, Gas & Petrochemicals |

| Construction & Infrastructure Development |

| Real Estate & Property Development |

| Trade & Logistics |

| Travel, Tourism & Hospitality |

| Financial Services & Investments |

| Healthcare & Life Sciences |

| Information & Communication Technology (ICT) |

| Others |

| Public-Sector CAPEX |

| Domestic Private Investment |

| Foreign Direct Investment (FDI) |

| Sovereign & Pension Fund Capital |

| Greenfield |

| Brownfield/Expansion |

| Mergers & Acquisitions |

| By Sector | Agriculture & Food Production |

| Manufacturing & Industrial Production | |

| Oil, Gas & Petrochemicals | |

| Construction & Infrastructure Development | |

| Real Estate & Property Development | |

| Trade & Logistics | |

| Travel, Tourism & Hospitality | |

| Financial Services & Investments | |

| Healthcare & Life Sciences | |

| Information & Communication Technology (ICT) | |

| Others | |

| By Financing Source | Public-Sector CAPEX |

| Domestic Private Investment | |

| Foreign Direct Investment (FDI) | |

| Sovereign & Pension Fund Capital | |

| By Project Lifecycle Stage | Greenfield |

| Brownfield/Expansion | |

| Mergers & Acquisitions |

Key Questions Answered in the Report

How large is the Investment Opportunities in Qatar Market in 2026?

USD 74.37 billion, with a path toward USD 96.92 billion by 2031.

Which sector grows fastest within the Investment Opportunities in Qatar Market?

Information & Communication Technology posts an 11.62% forecast CAGR.

What proportion of funding is foreign direct investment?

FDI is the fastest-rising slice, growing at a 9.31% CAGR although public CAPEX still holds 47.02% share.

Why do greenfield ventures dominate new capital?

Policymakers favor purpose-built assets, giving greenfield projects 52.96% share and a 7.15% CAGR.

Page last updated on: