Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

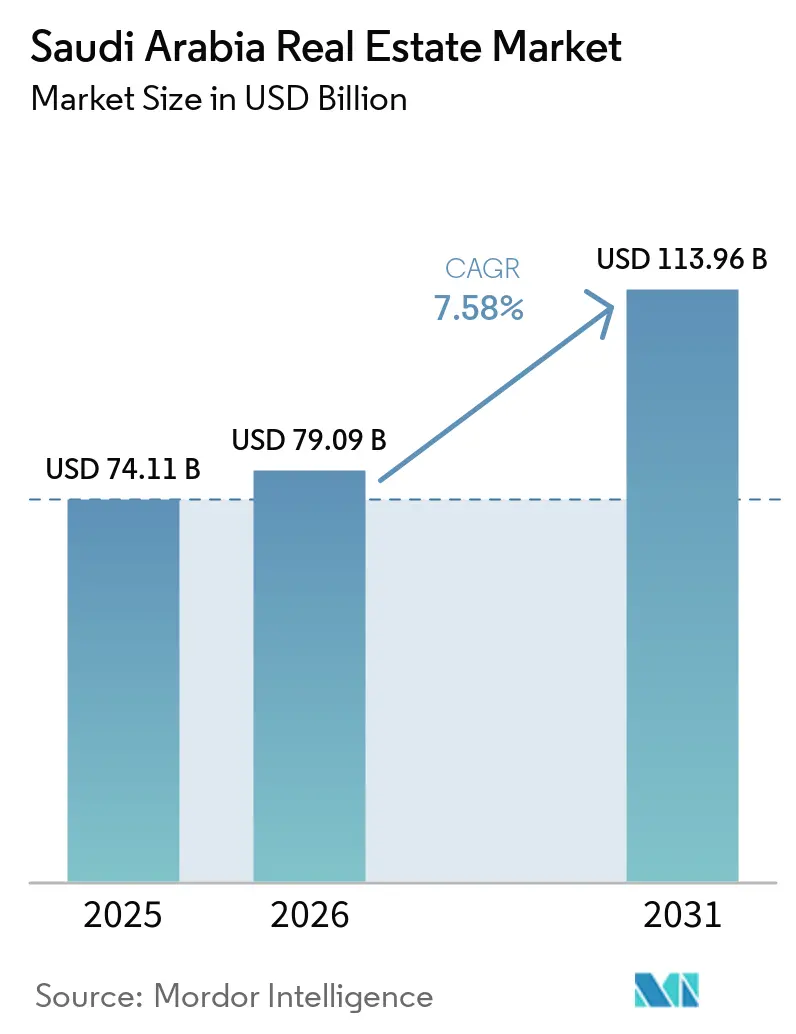

| Base Year Market Size (2025) | USD 74.11 Billion |

| Market Size (2026) | USD 79.09 Billion |

| Market Size (2031) | USD 113.96 Billion |

| Growth Rate (2026 - 2031) | 7.58% CAGR |

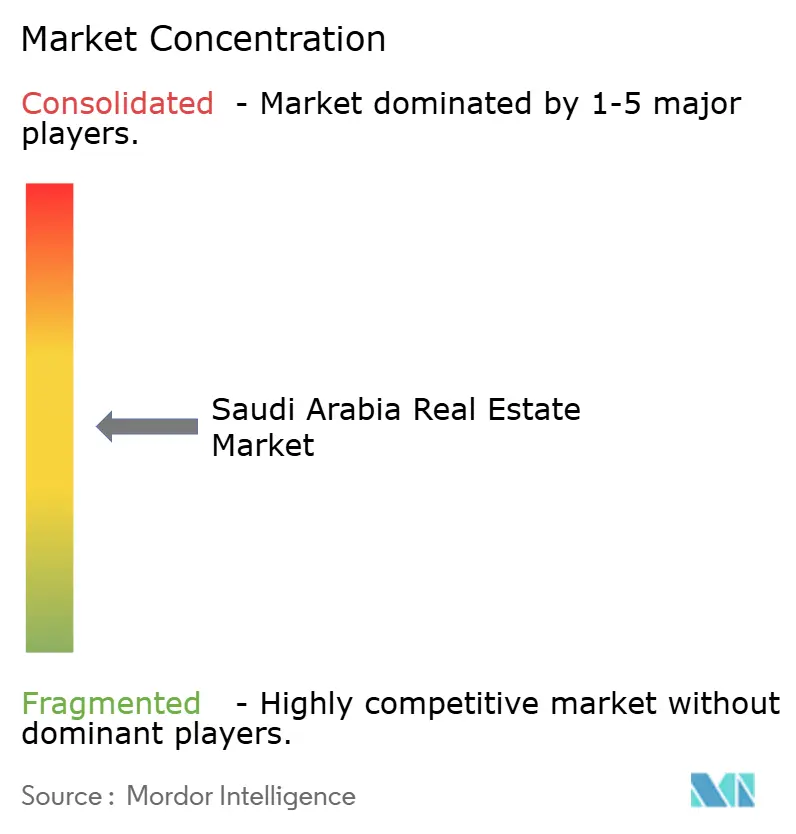

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Saudi Arabia Real Estate Market Analysis by Mordor Intelligence

The Saudi Arabia Real Estate Market size is projected to expand from USD 74.11 billion in 2025 and USD 79.09 billion in 2026 to USD 113.96 billion by 2031, registering a CAGR of 7.58% between 2026 to 2031.

The outlook is powered by Vision 2030’s giga-project pipeline, a demographic surge that lifts household formation, and capital-market reforms that broaden institutional participation. Public Investment Fund (PIF) financing of at least USD 40 billion a year keeps liquidity intact even as global conditions tighten, while a maturing mortgage system transforms speculative land into productive developments. Residential demand now skews toward mid-market apartments, yet logistics, data-center, and branded-hospitality assets command the fastest growth as e-commerce, manufacturing localization, and tourism targets converge. Regulatory upgrades—such as expanded REIT rules and premium residency permits—narrow the Kingdom’s risk premium relative to regional peers and open new exit routes for global investors. Against this backdrop, execution risks tied to labor shortages and cost inflation remain the chief headwinds that could temper the Saudi Arabia real estate market’s trajectory.

Key Report Takeaways

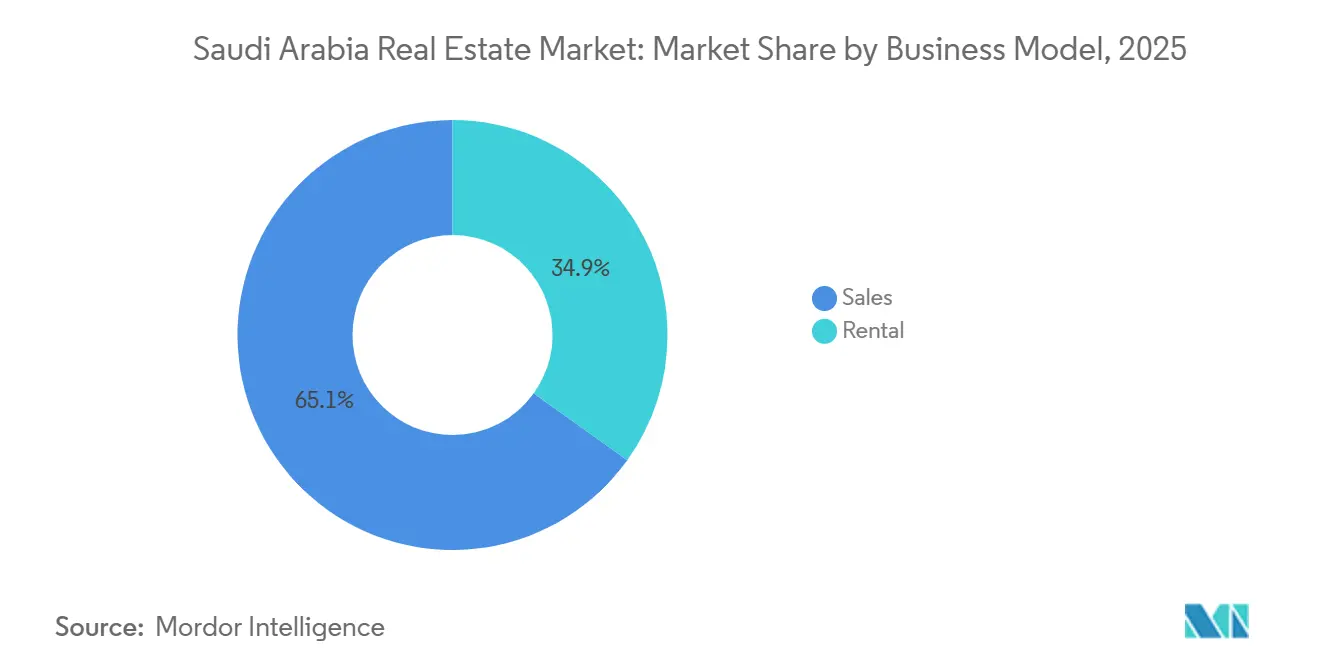

- By business model, sales dominated with 65.1% of the Saudi Arabia real estate market share in 2025, while the rental segment is set to grow at a 7.85% CAGR through 2031.

- By property type, residential captured 62.3% of value in 2025; logistics assets are forecast to expand at a 7.92% CAGR to 2031.

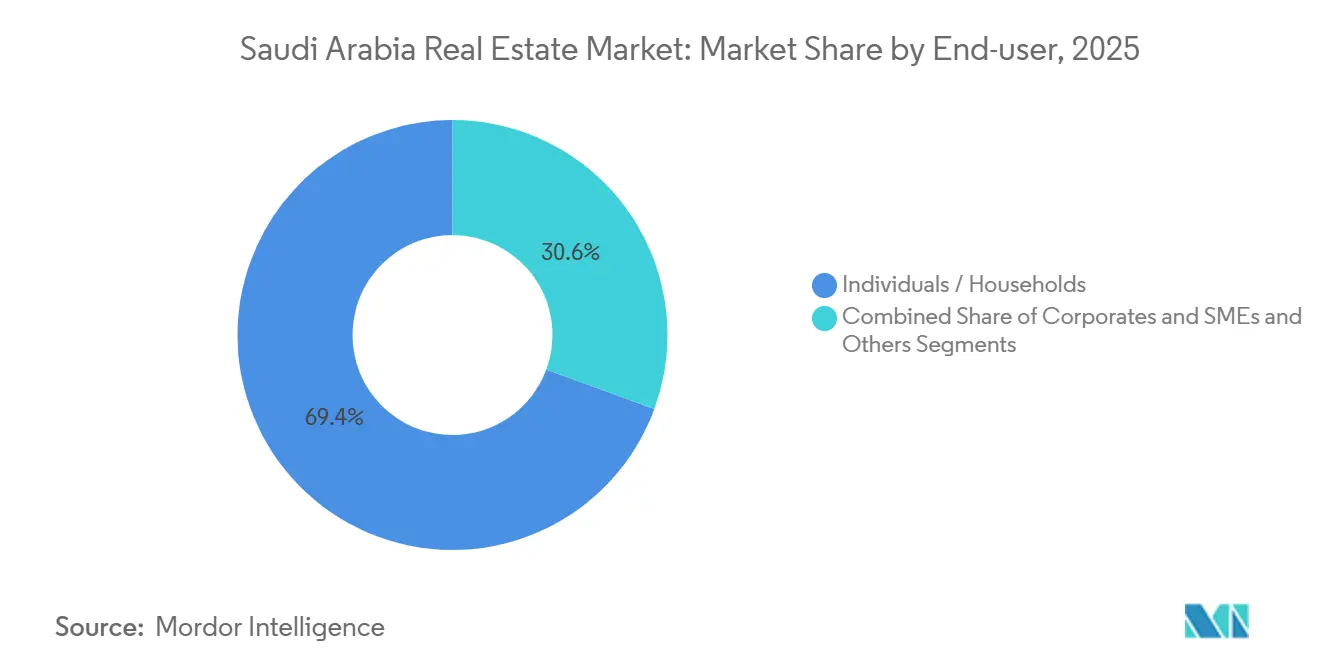

- By end-user, individuals and households held 69.4% of the Saudi Arabia real estate market size in 2025, whereas corporates and SMEs are expected to advance at an 8.02% CAGR through 2031.

- By city, Riyadh led with a 41.5% share of the real estate market in Saudi Arabia in 2025, while the Dammam Metropolitan Area posts the highest projected CAGR at 8.41% to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Saudi Arabia Real Estate Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % IMPACT ON CAGR FORECAST | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Vision 2030 giga-/mega-projects | +2.3% | National, concentrated in NEOM, Red Sea, Diriyah, Qiddiya, New Murabba | Long term (≥ 4 years) |

| Population growth and household formation | +1.6% | Riyadh, Jeddah, Dammam Metropolitan Area | Medium term (2–4 years) |

| Tourism surge and entertainment investments | +1.4% | Western coast, Makkah, Madinah, Riyadh | Medium term (2–4 years) |

| Industrial & logistics expansion | +1.0% | Eastern Province, Riyadh clusters, Jeddah hinterland | Short term (≤ 2 years) |

| Regulatory and capital-market maturation | +0.8% | Riyadh and Jeddah financial districts | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Vision 2030 Giga-Projects Anchor Multi-Decade Development Pipelines

The combined USD 1.3 trillion allocation for NEOM, Red Sea, Diriyah, Qiddiya, and New Murabba drives sustained demand across housing, hospitality, retail, and offices well past 2040[1]Knight Frank, “Saudi Arabia Vision 2030 Report,” knightfrank.com.sa. NEOM alone targets 1.5 million residents by 2030, translating into 500,000 homes and 10 million m² of commercial space. Red Sea Phase 1 infrastructure finished in 2024, clearing the way for 8,000 hotel rooms across 16 resorts, while Diriyah awarded USD 2.1 billion in luxury-hotel contracts that same year. New Murabba’s December 2025 fast-track zoning pact compresses permitting by 18 months and embeds 30% energy-reduction targets. Although the special-economic-zone model accelerates approvals, its scale can crowd out private developers that lack similar land pipelines and utility tie-ins.

Demographic Momentum Fuels Housing Deficit Despite Record Delivery

Saudi Arabia’s population reached 35.3 million in 2024, rising 4.7% year on year, and household sizes continue to shrink, creating annual demand for 115,000 homes[2]General Authority for Statistics, “Labor Force Survey 2024,” stats.gov.sa. Riyadh alone faces a 305,000-unit gap through 2034 despite cumulative delivery of 850,000 units by the Housing Program. Homeownership climbed to 65.4% in 2024, yet mid-market apartments priced between USD 133,000 and USD 400,000 still represent 72% of unmet demand. ROSHN’s USD 400 million in 2024 construction contracts cover only 30,000 units—well below the projected need. Limited secondary-market liquidity keeps mortgage penetration at 18% of GDP, half the emerging-market norm, even after the Saudi Real Estate Refinance Company’s USD 267 million portfolio acquisition.

Tourism and Entertainment Investments Reshape Hospitality and Mixed-Use Demand

Government targets for 150 million visitors by 2030 catalyze a 320,000-room hospitality pipeline that pulls global chains such as Hilton and Marriott deeper into the Saudi Arabian real estate market. Kingdom Holding revived the USD 7.2 billion Jeddah Tower in 2024, incorporating a 200-key luxury hotel and 120 serviced apartments to anchor Red Sea tourism. Mixed-use megaprojects like Wajhat Masar in Makkah add 24,000 hotel units and 13,000 homes, aimed at Umrah pilgrims who spend longer stays than Hajj visitors. Airline seat capacity and visa reforms must accelerate in parallel to avoid near-term oversupply flagged by CBRE[3]CBRE Saudi Arabia, “Riyadh Office Market Report Q1 2025,” cbre.com.sa.

Industrial and Logistics Expansion Driven by Manufacturing Localization and E-Commerce

The National Industrial Development and Logistics Program plans 59 logistics centers that will lift warehouse inventory to 15 million m² by 2030. Amazon’s 390,000-ft² Riyadh facility and Maersk’s USD 100 million Jeddah park underscore global appetite for Saudi logistics assets. A 30-year PPP for an 850,000-m² Dammam zone brings private capital into infrastructure, a template earmarked for rollout in Riyadh and Jubail. AWS’s USD 5.3 billion data-center pledge further validates industrial land, though hazardous-material permitting remains centralized and slow.

Restraints Impact Analysis*

| Restraints | (~) % IMPACT ON CAGR FORECAST | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Execution capacity limits and skilled-labor shortages | −0.9% | NEOM, Red Sea, Diriyah | Short term (≤ 2 years) |

| Higher construction and financing costs | −0.7% | National, especially secondary cities | Medium term (2–4 years) |

| Land, permitting, and utility tie-in complexities | −0.5% | Coastal and heritage zones, desert terrain | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Execution Capacity Constraints and Labor Shortages Threaten Delivery Timelines

Specialized trades now command 25%–40% wage premiums over 2022 levels as 2.8 million workers struggle to cover giga-project demand. NEOM’s workforce reached only 18,000 by mid-2024, far below the 50,000 units per year its schedule implies, and Red Sea Phase 2 resorts slipped six months due to 30% subcontractor turnover. Contractor margins compressed to mid-single digits, prompting three Riyadh mid-tier builders to file for bankruptcy in 2024. Saudization rules that require 30% local hires compound shortages because vocational training produces only one-third of the required graduates.

Construction Cost Inflation and Financing Pressures Squeeze Developer Feasibility

Cement and steel prices rose 25%–30% between 2023 and 2024, lifting overall build costs about 18%. Mortgage rates climbed to 6.5% in 2024, eroding buyer power by 12% and nudging activity toward lower-priced segments. Emaar The Economic City’s USD 307 million Q3 2024 loss and Jabal Omar’s pivot to land sales illustrate how inflation squeezes legacy players’ feasibility. International contractors now demand escalation clauses that add 15% contingencies to giga-project packages.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Business Model – Sales Dominate but Rental Gains Momentum

Sales transactions accounted for 65.1% of the Saudi Arabian real estate market in 2025, anchored by villa purchases in Riyadh’s Al Narjis and Jeddah’s Al Hamra districts. Rental activity is projected to grow at a 7.85% CAGR to 2031 as Build-to-Rent platforms, corporate relocations, and flexible-lease products mature. Knight Frank notes that first-time-buyer participation fell to 29% in 2024 after mortgage rates rose 230 basis points. Ejar recorded 3 million digital leases in 2024, up 35%, giving institutions data transparency that underpins underwriting.

Within the real estate market in Saudi Arabia, institutional investors favor rental yields that averaged 6.8% for Riyadh Grade A apartments in 2024, some 120 basis points above 10-year government bonds, and the 5% transfer tax tilts marginal buyers toward leasing. RAFAL’s 2024 co-living launch with HIVE and Sakani’s income-cap gaps create a rental cohort of 1.2 million households that will keep absorption robust. Consequently, the Saudi Arabia real estate market size for rentals is set to narrow the gap with sales by the end of the forecast period.

By Property Type – Residential Still Largest, Logistics Fastest

Residential held 62.3% of the 2025 market value, reflecting strong cultural preference for ownership and ongoing Sakani subsidies. Yet logistics assets will post the highest growth, at a 7.92% CAGR to 2031, propelled by the 59-hub national plan and Amazon, Maersk, and AWS commitments that validate industrial yield profiles. Apartments and condominiums gain traction as ROSHN’s USD 400 million contracts deliver high-density stock, although villas remain 68% of Sakani handovers.

Office take-up reached 1.2 million m² in Riyadh during 2024, driving a 21% rent jump to USD 527/m² as ministries and banks clustered in King Abdullah Financial District. Retail shows a two-tier pattern where super-regional malls stay full, but community centers risk oversupply. Hospitality, counted within “Others,” adds 320,000 pipeline rooms, yet tourism visa timelines must keep pace to prevent occupancy stress.

By End-User – Corporations and SMEs Accelerate

Individuals and households commanded 69.4% of the Saudi Arabian real estate market share in 2025, but corporates and SMEs are forecast to expand at an 8.02% CAGR, the fastest among end-users. Financial institutions leased 1.8 million m² in King Abdullah Financial District at premiums 11% above city averages, while SME co-working memberships doubled to 8,500 firms in 2024.

Government entities and PIF-affiliated giga-projects comprise a rising “Others” segment that absorbed 12% of the 2025 value. Sustainability clauses—30% energy cuts and 40% water savings—are set to become standard for government leases after New Murabba’s December 2025 agreement, likely nudging private landlords to retrofit assets for compliance.

Geography Analysis

Riyadh remains the center of gravity for the Saudi Arabian real estate market, holding a 41.5% share in 2025 and tracking a 7.0% CAGR to 2031 as New Murabba and King Abdullah Financial District reshape the skyline. Grade A office rents climbed 21% in 2024 to USD 527/m², yet residential supply lags demand, prompting ROSHN’s commitment to 30,000 additional units that still cover only a fraction of the 305,000-home gap. Qiddiya’s entertainment complex and King Salman Park’s USD 1 billion mixed-use district layer new leisure and green-space narratives onto the capital’s growth story.

Jeddah accounted for roughly 28% of market value in 2025, supported by its USD 20 billion central regeneration project and the high-rise ambition of Jeddah Tower. Office rents improved 13.6% to USD 375/m² in 2024 as logistics firms clustered near Jeddah Islamic Port. The city’s 29 investment prospects covering 1.4 million m² aim to diversify away from maritime trade and absorb 45,000 housing units by 2030, although older stock will need modernization to compete for institutional capital.

The Dammam Metropolitan Area, including Jubail, is set for the fastest expansion at an 8.41% CAGR, propelled by petrochemical joint ventures and a 59-hub logistics mandate that calls for 5 million m² of warehouses by 2030. Office vacancy still sits at 14%, hinting at legacy oversupply, but corporate compound acquisitions at USD 213,000 per unit provide a cost edge over Riyadh, encouraging workforce relocation. Elsewhere, mega-projects in Makkah, Madinah, and Tabuk (NEOM) capture 30.5% of value, leveraging religious tourism and special-economic-zone incentives, albeit tempered by infrastructure build-outs that remain only partially complete.

Competitive Landscape

Competition bifurcates between state-backed giants and legacy private developers. PIF-controlled ROSHN, Diriyah Company, and New Murabba collectively manage pipelines exceeding USD 100 billion and benefit from land grants, utility tie-ins, and cheap financing, allowing them to set benchmarks for sustainability and smart-city features. Their dominance raises entry barriers for mid-sized firms that struggle to match land costs or achieve scale economies.

In the real estate market in Saudi Arabia, legacy developers such as Emaar The Economic City and Jabal Omar are recalibrating strategies amid cost inflation. Emaar recorded a USD 307 million Q3 2024 loss and entered debt talks with PIF, while Jabal Omar shifted toward land monetization, lifting revenue 43.3% but signaling retreat from vertical construction. Smaller contractors have exited fixed-price contracts, evidenced by three Riyadh bankruptcies in 2024, and now negotiate escalation clauses to hedge commodity volatility.

International advisory and facilities-management firms intensify competition on the services front. JLL’s December 2025 acquisition of a major stake in FMTECH secures an operational role across giga-projects valued at more than USD 10 billion through 2035. CBRE, Knight Frank, and Colliers expand valuation, leasing, and project-management footprints, leveraging data transparency from platforms like Ejar and blockchain pilots at NEOM. Technology adoption thus evolves into a competitive differentiator, with blockchain titling and AI-driven facility analytics increasingly viewed as must-haves rather than novelties.

Saudi Arabia Real Estate Industry Leaders

Al Saedan Real Estate Co.

Kingdom Holding Company

Dar Al Arkan Real Estate Development

Jabal Omar Development Co.

SEDCO Development

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2025: JLL acquired a significant stake in FMTECH, positioning the firm to oversee giga-project operations valued above USD 10 billion.

- December 2025: New Murabba secured fast-track zoning with 30% energy and 40% water savings benchmarks.

- November 2025: King Salman Park Foundation, Ajdan Real Estate, and SEDCO Capital launched a USD 1 billion mixed-use district in Riyadh.

- November 2025: King Salman Gate signed six MoUs with Indonesian, Malaysian, and Bruneian funds for its 12-million-m² Makkah megaproject.

- November 2025: Emlak Konut and National Housing Company formed a USD 400 million joint venture for 1,014 villas in Makkah.

Saudi Arabia Real Estate Market Report Scope

Real estate is the buying and selling of land and buildings, including any permanent manmade additions, such as houses and other buildings. The Saudi real estate market is segmented By Property Type (Residential Estate (Apartments, Villas) and Commercial Real Estate (Offices, Retail, Hospitality, and Others). The report offers market size and forecasts for the Saudi real estate market in value (USD) for the above segments.

By Property Type

| Residential | Apartments & Condominiums |

| Villas & Landed Houses | |

| Commercial | Office |

| Retail | |

| Logistics | |

| Others (industrial, hospitality, etc.) |

By End-user

| Individuals / Households |

| Corporates & SMEs |

| Others |

By City

| Riyadh |

| Jeddah |

| DMA (Dammam Metropolitan Area) |

| Rest of Saudi Arabia |

| By Property Type | Residential | Apartments & Condominiums |

| Villas & Landed Houses | ||

| Commercial | Office | |

| Retail | ||

| Logistics | ||

| Others (industrial, hospitality, etc.) | ||

| By End-user | Individuals / Households | |

| Corporates & SMEs | ||

| Others | ||

| By City | Riyadh | |

| Jeddah | ||

| DMA (Dammam Metropolitan Area) | ||

| Rest of Saudi Arabia | ||

Key Questions Answered in the Report

How fast is the Saudi Arabian real estate market expected to grow between 2026 and 2031?

The market is projected to expand at a 7.17% CAGR, rising from USD 72.84 billion in 2026 to USD 102.96 billion by 2031.

Which segment is likely to record the highest growth within Saudi real estate?

Logistics assets are forecast to grow the fastest, advancing at a 7.92% CAGR as e-commerce and manufacturing localization spur warehouse demand.

Why is rental housing gaining importance in Saudi Arabia?

Higher mortgage rates, a 5% transfer tax, and Build-to-Rent platforms are nudging buyers toward leasing, with rental transactions expected to grow at 7.85% through 2031.

What drives Dammam’s position as the fastest-growing city?

An 850,000 m² PPP logistics zone and petrochemical expansions underpin an 8.41% CAGR forecast for the Dammam Metropolitan Area.

How are giga-projects influencing the competitive landscape?

PIF-backed developers such as ROSHN, Diriyah Company, and New Murabba leverage land grants and low-cost capital to dominate pipelines, raising entry barriers for private players.

What role do REITs play in the Saudi property sector?

Twenty-one listed REITs with a combined USD 10.4 billion market cap offer yields above 7%, attracting institutional investors and deepening market liquidity.

Page last updated on: