Saudi Arabia Office Real Estate Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

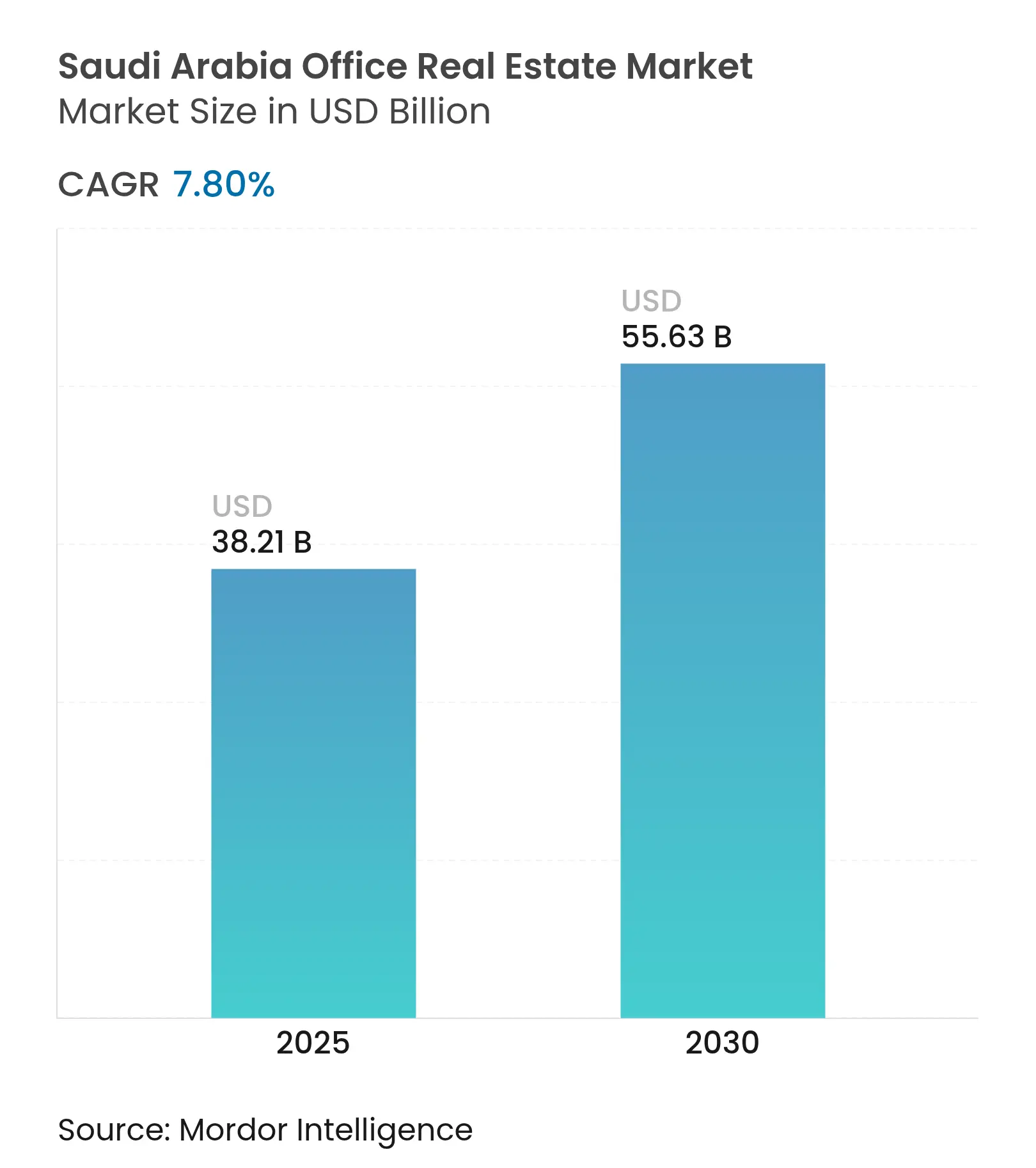

| Market Size (2025) | USD 38.21 Billion |

| Market Size (2030) | USD 55.63 Billion |

| Growth Rate (2025 - 2030) | 7.80 % CAGR |

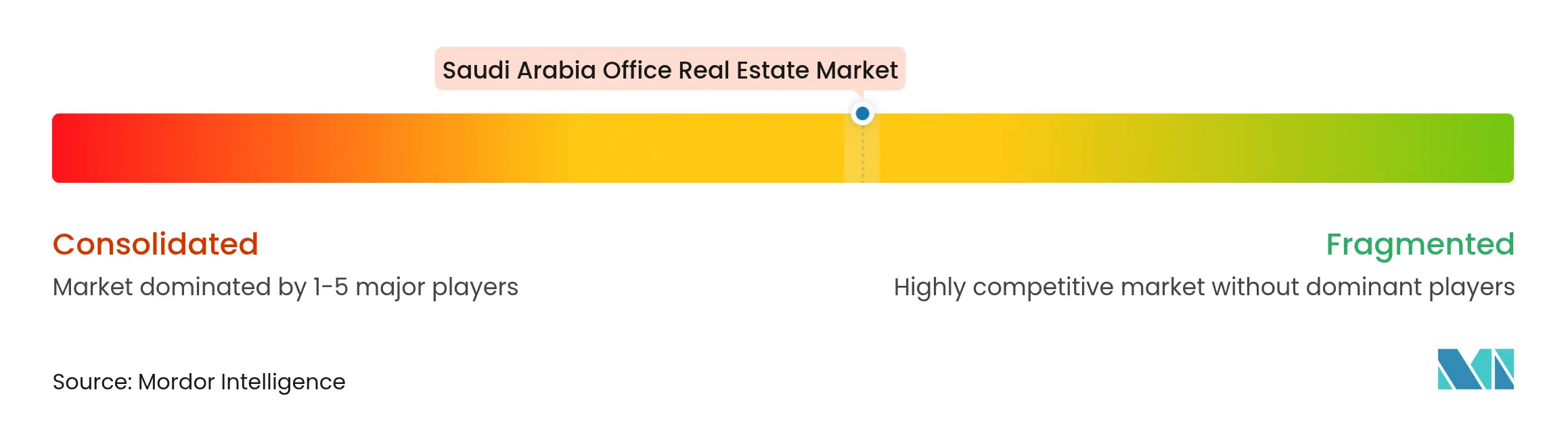

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order. Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

Saudi Arabia Office Real Estate Market Analysis by Mordor Intelligence

The Saudi Arabia office real estate market size stood at USD 35.32 billion in 2024 and is forecast to reach USD 55.63 billion by 2030, expanding at a 7.8% CAGR. This rise reflects Vision 2030 policies that require multinational corporations to locate regional headquarters in the Kingdom, which has sharply lifted demand for premium workspaces. Growing tax incentives, large-scale public spending, and rapid infrastructure upgrades are reinforcing leasing appetite, while grade upgrades, sustainability mandates, and smart-building retrofits are shaping investment strategies. Developers backed by sovereign wealth funds are entering the scene, adding deep pockets and intensifying rivalry. Rents for top-tier space in Riyadh and Jeddah continue to firm despite new supply, as relocation flexibility and long lease commitments temper vacancy risks. At the same time, high construction costs, potential oversupply in select corridors, and hybrid-work uncertainty require disciplined project phasing.

Key Report Takeaways

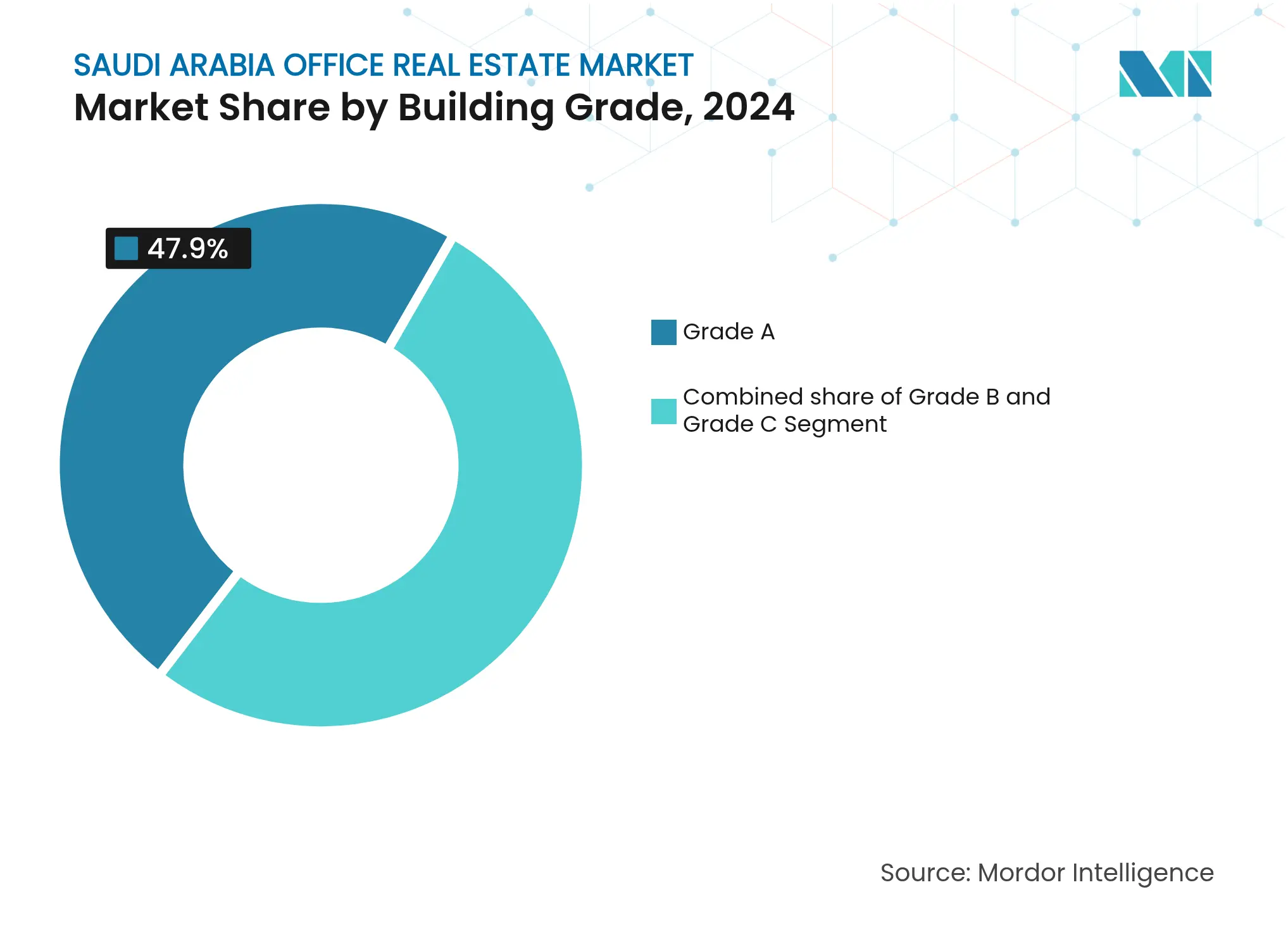

- By building grade, Grade A premises led with 47.9% of the Saudi Arabia office real estate market share in 2024; Grade A space is projected to expand at an 8.31% CAGR to 2030.

- By transaction type, the rental segment accounted for 80.3% of the Saudi Arabia office real estate market size in 2024, while sales recorded the highest projected CAGR at 8.55% through 2030.

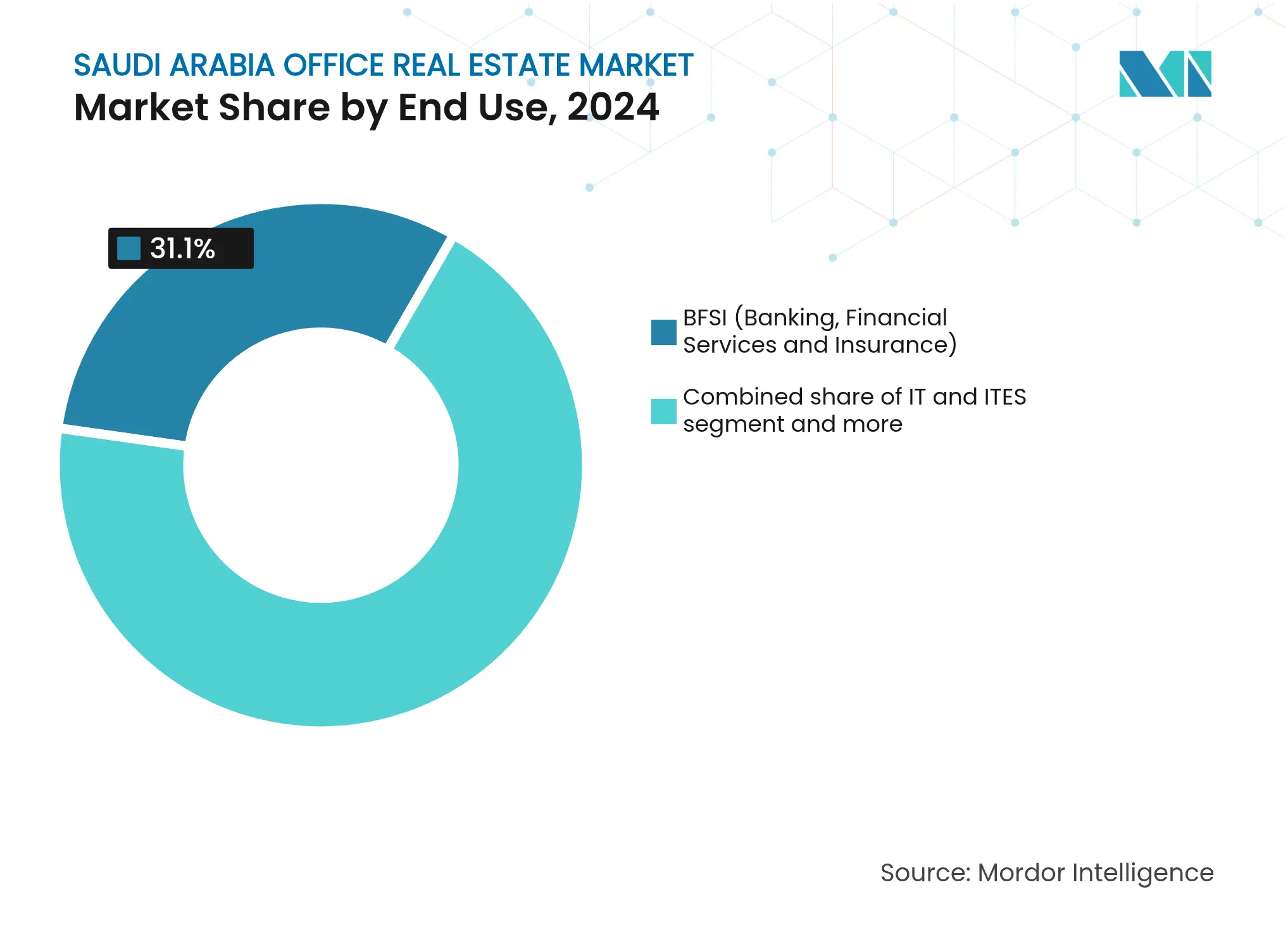

- By end use, banking, financial services, and insurance held 31.1% of the Saudi Arabia office real estate market size in 2024; consulting and professional services are advancing at an 8.71% CAGR to 2030.

- By city, Riyadh captured 51.1% of the Saudi Arabia office real estate market share in 2024, and the Dammam Metropolitan Area is progressing at a 9.09% CAGR through 2030.

Saudi Arabia Office Real Estate Market Trends and Insights

Drivers Impact Analysis

| Drivers | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Rising demand from multinational corporations under Vision

2030 diversification agenda

Rising demand from multinational corporations under Vision

2030 diversification agenda

| +2.1% | National, concentrated in Riyadh and Jeddah | Medium term (2-4 years) |

% Impact on CAGR Forecast

:

+2.1%

|

Geographic Relevance

:

National, concentrated in Riyadh and Jeddah

|

Impact Timeline

:

Medium term (2-4 years)

|

Government-led mega projects in Riyadh and Jeddah are creating

new office hubs

Government-led mega projects in Riyadh and Jeddah are creating

new office hubs

| +1.8% | Riyadh and Jeddah metropolitan areas | Long term (≥ 4 years) | |||

Strong growth in financial services, technology, and

professional sectors is boosting office leasing

Strong growth in financial services, technology, and

professional sectors is boosting office leasing

| +1.5% | National, with Riyadh and KAFD concentration | Short term (≤ 2 years) | |||

Urban infrastructure expansion is improving connectivity

and office corridor attractiveness

Urban infrastructure expansion is improving connectivity

and office corridor attractiveness

| +1.2% | National, prioritizing major cities | Long term (≥ 4 years) | |||

Increased preference for Grade A office spaces with

sustainability and smart features

Increased preference for Grade A office spaces with

sustainability and smart features

| +0.9% | National, led by Riyadh and Jeddah | Medium term (2-4 years) | |||

| Source: Mordor Intelligence | ||||||

Rising Demand from Multinational Corporations under Vision 2030

The Regional Headquarters program grants 30-year zero-tax status, so more than 350 global firms secured RHQ licenses by early 2024. Each license obliges at least 15 senior employees and decisions over two MENA markets, ensuring sticky head-count growth. Technology giants such as Amazon and Microsoft joined early, reinforcing investor confidence. As capacity in Grade A towers tightens, late entrants explore secondary corridors or accept longer leases in emerging districts. This corporate influx is sustaining the Saudi Arabia office real estate market even as hybrid work gains ground elsewhere[1]Aisha Al-Mahdi, “Vision 2030 Progress & Diversification Metrics 2025,” Vision 2030 Secretariat, vision2030.gov.sa.

Government-Led Mega Projects in Riyadh and Jeddah Creating New Office Hubs

Projects like the USD 50 billion New Murabba in Riyadh and the USD 12.5 billion Jeddah Central scheme are adding entire business districts and are timed to align with Expo 2030 and the 2034 FIFA World Cup. Diriyah Gate and NEOM’s Oxagon deepen geographic diversification and sector clustering. These developments fragment traditional demand, forcing occupiers to match location with talent pools and transport links. The pipeline enlarges total inventory yet also creates experiential hubs that defend premium asking rents. Successful phasing will depend on infrastructure readiness and tenant pre-commitments[2]Faisal Al-Ibrahim, “New Murabba Masterplan Overview,” International Trade Administration (ITA), trade.gov.

Strong Growth in Financial, Technology, and Professional Services

Saudi credit rose 16.26% year on year to USD 827.2 billion in March 2025, with real-estate lending up 40.5%. Fintechs thrive under sandbox regulations, boosting demand for smaller, tech-ready floorplates. EY opened an 11,691-square-meter MENA HQ in KAFD, joining other professional advisers as Vision 2030 accelerates transformation projects. PwC’s temporary advisory ban has freed shares for rivals and local specialists, stimulating further leasing. Landlords now upgrade connectivity, collaboration areas, and ESG credentials to attract these high-growth tenants.

Increased Preference for Grade A Space with Sustainability and Smart Features

KAFD’s 94 towers earned LEED Platinum, setting a benchmark for green credentials. Forbes International Tower is registered for Zero Carbon Certification, running on 100% clean energy split between hydrogen and solar. The Saudi Building Code 2024 enforces energy conservation, prompting retrofits and raising barriers for outdated stock. Corporate ESG targets push landlords to install IoT building management systems and renewable power. Consequently, rent spreads between Grade A and lower classes are widening, and secondary assets risk rapid obsolescence unless modernized[3]Sarah Al-Suhaimi, “King Abdullah Financial District Sustainability Report 2024,” KAFD DMC, kafd.sa.

Restraint Impact Analysis

| Restraints | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

High construction and fit-out costs impacting project

viability

High construction and fit-out costs impacting project

viability

| -1.4% | National, acute in major cities | Short term (≤ 2 years) |

% Impact on CAGR Forecast

:

-1.4%

|

Geographic Relevance

:

National, acute in major cities

|

Impact Timeline

:

Short term (≤ 2 years)

|

Oversupply risk in certain office districts creating

downward pressure on rents

Oversupply risk in certain office districts creating

downward pressure on rents

| -0.8% | Riyadh and Jeddah specific districts | Medium term (2-4 years) | |||

Regulatory approval timelines and land acquisition

complexities delaying delivery

Regulatory approval timelines and land acquisition

complexities delaying delivery

| -0.6% | National, varying by municipality | Medium term (2-4 years) | |||

| Source: Mordor Intelligence | ||||||

High Construction and Fit-Out Costs Impacting Project Viability

A USD 1.5 trillion national project pipeline strains labor and materials, lifting build costs above Gulf averages. Imported inputs expose developers to freight delays and currency shifts, while geopolitical frictions widen procurement buffers. Skilled-trade shortages enlarge wage bills and slow site progress. The 5% Real Estate Transaction Tax introduced in April 2025 adds financing friction. Although some commodity prices eased in 2024, the structural gap between supply and demand persists, squeezing speculative margins.

Oversupply Risk in Certain Office Districts Creating Rent Pressure

Simultaneous delivery of New Murabba, KAFD phases, and private towers could outpace organic absorption in Riyadh by late-decade. Government-backed stock may not always mirror market-driven demand, and slower-than-expected multinational expansion would accentuate vacancies. Tenant flight from older towers to smarter builds can leave secondary stock under-let, lowering average city rents. Developers with limited pre-leasing run higher default and refinancing risk in the event of a cyclical pause. Vigilant phasing and flexible floorplate design remain critical.

Segment Analysis

By Building Grade: Premium Properties Drive Leadership

Grade A offices controlled 47.9% of the Saudi Arabia office real estate market in 2024, and the cohort is projected to grow at an 8.31% CAGR through 2030. The King Abdullah Financial District shows how green credentials underpin this result, as LEED-certified assets achieve stronger leasing. Forbes International Tower adds technology stature by targeting Zero Carbon status. Developers retrofit Grade B stock to chase similar rents, while Grade C faces potential conversion to other uses. These trends elevate the Saudi Arabia office real estate market size captured by top-tier assets and deepen the bifurcation between grades.

Tenant expectations around IoT integration, renewable energy sourcing, and wellness amenities are reshaping design briefs. The Saudi Building Code 2024 embeds energy efficiency, accelerating demand for high-grade materials and smart systems. As global firms expand headcount under the RHQ regime, they favor modern towers offering reliable digital infrastructure and ESG compliance. This dynamic allows premium landlords to lock longer leases and to pass through higher operating costs. Lower-grade buildings risk rental discounts unless they fund major upgrades.

Note: Segment shares of all individual segments available upon report purchase

By Transaction Type: Rental Dominance Persists

Rentals represented 80.3% of the Saudi Arabia office real estate market size in 2024 and show an 8.55% CAGR outlook. International corporations choose leasing to maintain agility ahead of the January 2026 foreign-ownership reform. Government agencies also sign multi-year leases, anchoring cash flows for investors. Grade A rents in Jeddah climbed 15% to USD 320 per square meter in 2024, reflecting tight supply and rising fit-out standards. Sales remain a niche pursued by local investors and sovereign wealth arms.

Flexible lease clauses allow tenants to scale space as projects ramp up or wind down. Developers structure core-and-shell handovers to shorten fit-out intervals, which appeals to tech and consulting occupiers. The 5% transaction tax on disposals nudges businesses toward renting rather than buying. REIT structures provide indirect ownership exposure for institutions that favor stable dividend streams over operational control. These elements reinforce rental dominance across the Saudi Arabia office real estate market.

By End Use: Financial Services Lead, Consulting Accelerates

Banking, financial services, and insurance held 31.1% of the Saudi Arabia office real estate market share in 2024, driven by credit expansion and financial hub ambitions. Consulting and professional services, however, forecast the fastest 8.71% CAGR thanks to robust advisory demand. PwC’s advisory hiatus has opened market gaps that competitors and local players race to fill. Technology players also expand under national digitization mandates.

Financial institutions require proximity to regulators and prefer landmark Grade A towers that signal credibility. Professional advisers seek collaborative layouts and high-bandwidth connectivity to run hybrid workshops. Fintech startups look for smaller, flexible units within incubator clusters. Legal firms enlarge footprints to handle complex foreign investment filings tied to RHQ licensing. This diverse end-user mix supports absorption across multiple sub-segments of the Saudi Arabia office real estate market.

Note: Segment shares of all individual segments available upon report purchase

Geography Analysis

Riyadh controlled 51.1% of the Saudi Arabia office real estate market in 2024, reflecting political centrality, mega-project investment, and RHQ clustering. New Murabba, KAFD expansion, and the metro are broadening the CBD footprint. Premium vacancies are low and rents are rising, yet large supply waves scheduled from 2026 onward may test the equilibrium. The city’s airport and rail projects reinforce cross-border integration, sustaining long-term appeal.

Jeddah remains the maritime and commercial gateway. The USD 12.5 billion Jeddah Central project and the resumption of the Jeddah Tower inject confidence. Religious tourism growth and relaxed foreign-ownership rules can draw occupiers priced out of Riyadh. Rental gaps between Grade A and lower classes are narrowing as new waterfront offices set benchmarks. Developers eye mixed-use formats that blend hospitality with corporate suites.

The Dammam Metropolitan Area posts the fastest 9.09% CAGR as petrochemical, logistics, and public-sector agencies increase regional bases. Proximity to Saudi Aramco, industrial ports, and pipeline infrastructure secures steady leasing. Secondary cities such as Medina, Abha, and Tabuk emerge through Knowledge Economic City and AlWadi projects, offering cost-effective alternatives, albeit with thinner service ecosystems. These locations diversify the Saudi Arabia office real estate industry and reduce geographic concentration risk.

Reports are available across multiple geographies.

Gain in-depth market insights across regions to support informed decisions.

Competitive Landscape

Market Concentration

Government-backed entities, private developers, and global service providers create a layered field. ROSHN’s 4 million square meters of commercial pipeline shows sovereign scale. Al Akaria grew gross profit by 23% in 2024 despite revenue pressure, signaling operational resilience. REITs gain traction, with KAFD planning a USD 700 million launch to recycle capital. Technology adoption is a differentiator: KAFD uses IBM Maximo to manage over 100,000 assets and lift satisfaction scores by 95%.

Traditional developers respond by accelerating green certifications and partnering with international architects. Global investors like BlackRock opened Riyadh branches to source direct deals and joint ventures. Competitive focus has shifted from pure location to tenant experience, data analytics, and ESG performance. Moderate consolidation is likely as smaller players struggle to fund smart retrofits and to meet new code standards. Partnerships with energy and telecom firms emerge to deliver integrated smart-city infrastructure inside office campuses.

White-space opportunities persist in secondary cities and niche segments such as R&D labs and co-warehousing offices supporting e-commerce fulfillment. Hybrid work keeps workplace densities fluid, so landlords offer plug-and-play suites and amenity-rich community floors. Overall, the Saudi Arabia office real estate market stays attractive, yet operational excellence and capital strength remain decisive for long-term leadership.

Saudi Arabia Office Real Estate Industry Leaders

*Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: NEOM and DataVolt inked a USD 5 billion pact to establish the inaugural net-zero AI factory, set to commence operations in 2028. This factory aims to leverage advanced artificial intelligence technologies while adhering to sustainable practices, marking a significant step toward achieving carbon neutrality in industrial operations.

- January 2025: Kingdom Holding Company resumed construction on the Jeddah Tower, aiming for a height surpassing 1,000 meters, with an investment of USD 26.6 billion. Once completed, the tower is expected to become the tallest building in the world, symbolizing Saudi Arabia's ambition to lead in architectural innovation and urban development.

- December 2024: NEOM and Samsung C&T poured in USD 347 million to automate rebar assembly, slashing onsite labor needs by 80%. This investment focuses on enhancing construction efficiency and reducing project timelines, aligning with NEOM's vision of integrating cutting-edge technology into infrastructure development.

- November 2024: ROSHN underwent a rebranding and expanded its portfolio by adding 4 million m² of commercial, office, and hospitality spaces. This expansion reflects the company's commitment to diversifying its offerings and supporting Saudi Arabia's economic growth by catering to the increasing demand for mixed-use developments.

Table of Contents for Saudi Arabia Office Real Estate Industry Report

1. Introduction

- 1.1Study Assumptions & Market Definition

- 1.2Scope of the Study

2. Research Methodology

3. Executive Summary

4. Market Insights and Dynamics

- 4.1Market Overview

- 4.2Market Drivers

- 4.2.1Rising demand from multinational corporations under Vision 2030 diversification agenda

- 4.2.2Government-led mega projects in Riyadh and Jeddah creating new office hubs

- 4.2.3Strong growth in financial services, technology, and professional sectors boosting office leasing

- 4.2.4Urban infrastructure expansion improving connectivity and office corridor attractiveness

- 4.2.5Increased preference for Grade A office spaces with sustainability and smart features

- 4.3Market Restraints

- 4.3.1High construction and fit-out costs impacting project viability

- 4.3.2Oversupply risk in certain office districts creating downward pressure on rents

- 4.3.3Regulatory approval timelines and land acquisition complexities delaying delivery

- 4.4Value / Supply-Chain Analysis

- 4.4.1Overview

- 4.4.2Real Estate Developers and Contractors - Key Quantitative and Qualitative Insights

- 4.4.3Architectural and Engineering Companies - Key Quantitative and Qualitative Insights

- 4.4.4Building Material and Equipment Companies - Key Quantitative and Qualitative Insights

- 4.5Government Regulations and Initiatives in the Industry

- 4.6Technological Innovations in the Office Real Estate Market

- 4.7Insights into Rental Yields in the Office Real Estate Segment

- 4.8Insights into the Key Office Real Estate Industry Metrics (Supply, Rentals, Prices, Occupancy/Vacancy (%))

- 4.9Insights into Office Real Estate Construction Costs

- 4.10Insights into Office Real Estate Investment

- 4.11Impact of Remote Working on Space Demand

- 4.12Porter’s Five Forces

- 4.12.1Threat of New Entrants

- 4.12.2Bargaining Power of Buyers / Occupiers

- 4.12.3Bargaining Power of Developers / Landlords

- 4.12.4Threat of Substitutes (WFH, Flexible Space)

- 4.12.5Competitive Rivalry

5. Market Size & Growth Forecasts (Value, USD)

- 5.1By Building Grade

- 5.1.1Grade A

- 5.1.2Grade B

- 5.1.3Grade C

- 5.2By Transaction Type

- 5.2.1Rental

- 5.2.2Sales

- 5.3By End Use

- 5.3.1Information Technology (IT & ITES)

- 5.3.2BFSI (Banking, Financial Services and Insurance)

- 5.3.3Business Consulting & Professional Services

- 5.3.4Other Services (Retail, Life-science, Energy, Legal)

- 5.4By City

- 5.4.1Riyadh

- 5.4.2Jeddah

- 5.4.3DMA (Dammam metropolitan area)

- 5.4.4Rest of Saudi Arabia

6. Competitive Landscape

- 6.1Market Concentration

- 6.2Strategic Moves

- 6.3Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products & Services, Recent Developments)

- 6.3.1SEDCO Development

- 6.3.2Kingdom Holding Company

- 6.3.3Saudi Real Estate Company (Al Akaria)

- 6.3.4Abdul Latif Jameel Real Estate

- 6.3.5JLL Saudi Arabia

- 6.3.6Savills KSA

- 6.3.7CBRE Saudi Arabia

- 6.3.8Knight Frank Saudi Arabia

- 6.3.9Ezdihar Real Estate Development

- 6.3.10Al Basateen Real Estate

- 6.3.11Fawaz Alhokair Group Real Estate

- 6.3.12Knowledge Economic City

- 6.3.13Diriyah Gate Development Authority

- 6.3.14NEOM (Oxagon Commercial)

- 6.3.15Red Sea Global (Shura Office Park)

- 6.3.16Riyad Capital (Riyad REIT)

- 6.3.17Jadwa Investment (REIF)

- 6.3.18Al Rajhi Capital (Al Rajhi REIT)

- 6.3.19Dar Al Arkan Real Estate

- 6.3.20Umm Al-Qura Development (King Abdul-Aziz Rd)

7. Market Opportunities & Future Outlook

Saudi Arabia Office Real Estate Market Report Scope

Office real estate is the construction of buildings for leasing and selling purposes to companies from different sectors. A complete background analysis of the Saudi Arabia office real estate market, including the assessment of the economy and contribution of sectors in the economy, market overview, market size estimation for key segments, emerging trends in the market segments, market dynamics, and geographical trends, are covered in the report.

The Saudi Arabia office real estate market is segmented by major cities (Riyadh, Jeddah, and Makkah). The report offers market size and forecasts in value (USD) for all the above segments.