Qatar Residential Construction Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

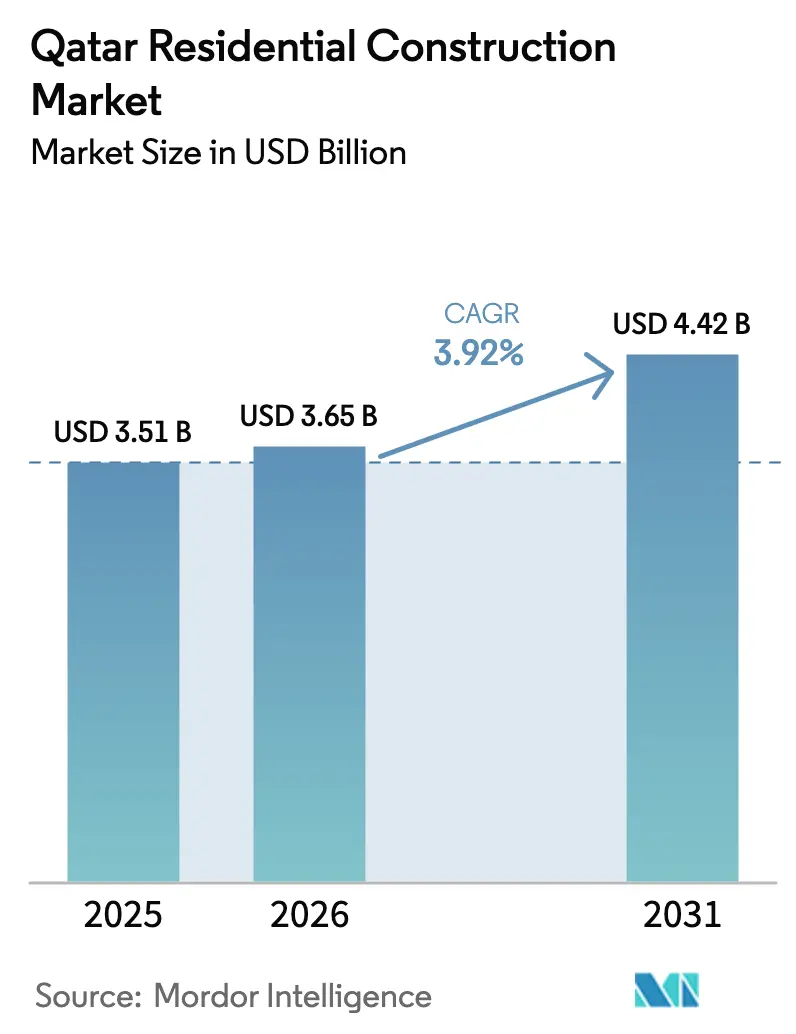

| Base Year Market Size (2025) | USD 3.51 Billion |

| Market Size (2026) | USD 3.65 Billion |

| Market Size (2031) | USD 4.42 Billion |

| Growth Rate (2026 - 2031) | 3.92% CAGR |

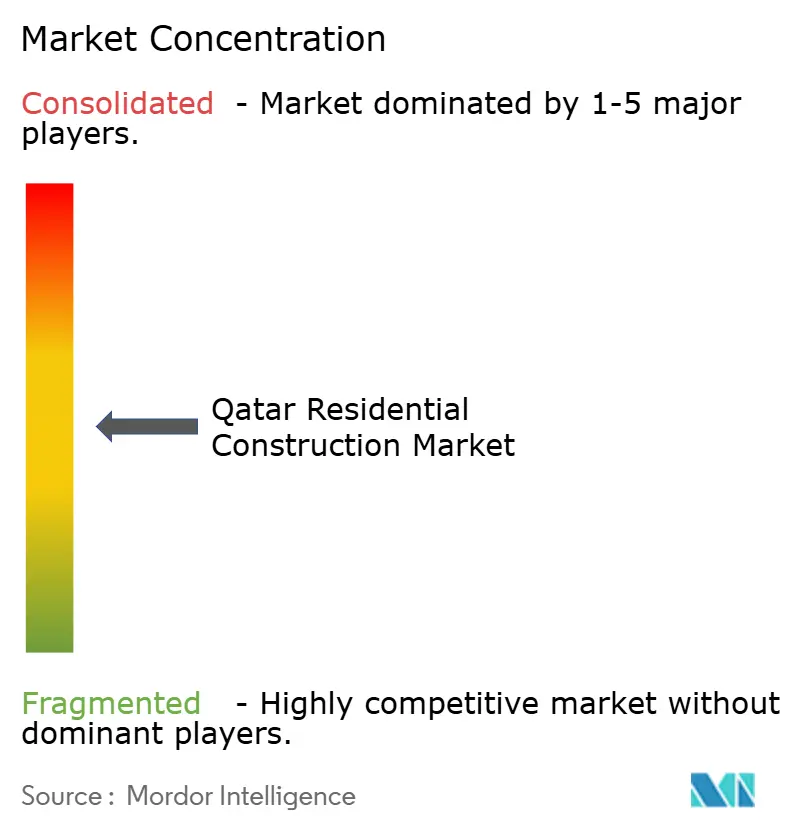

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Qatar Residential Construction Market Analysis by Mordor Intelligence

The Qatar residential construction market size is expected to grow from USD 3.51 billion in 2025 to USD 3.65 billion in 2026 and is forecast to reach USD 4.42 billion by 2031 at 3.92% CAGR over 2026-2031. The growth path reflects a shift from FIFA-driven megaprojects to demand that follows the Third National Development Strategy and the Qatar National Vision 2030. Population expansion, sustained expatriate inflows, public–private partnerships for affordable housing, and rising mortgage availability all reinforce a predictable pipeline of projects. Developers are also reallocating capital toward smart-home–ready units and mixed-use precincts that leverage the World Cup legacy infrastructure. Construction-technology adoption is accelerating as contractors confront labor-cost escalation and stricter nationalization rules, while demand gradually broadens beyond Doha into Al Khor and Al Rayyan.

Key Report Takeaways

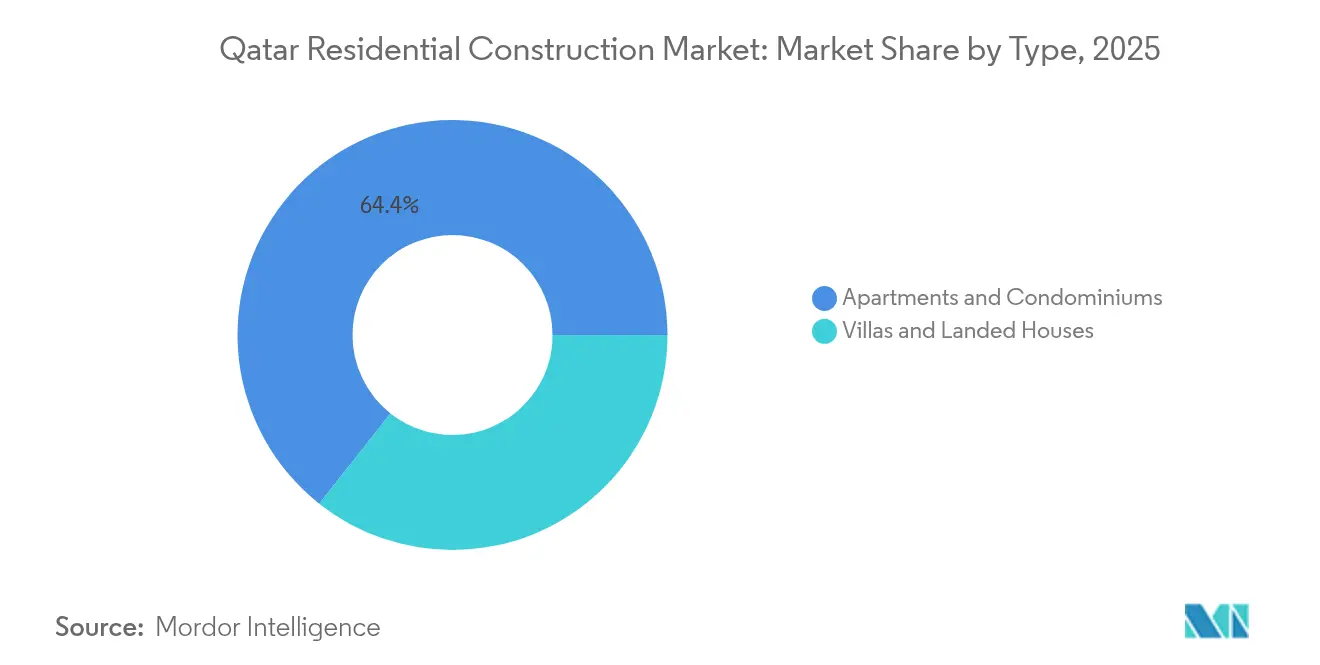

- By type, apartments and condominiums led with 64.35% of the Qatar residential construction market share in 2025, whereas villas and landed houses are projected to expand at a 4.25% CAGR to 2031.

- By construction type, new construction held 77.32% of the Qatar residential construction market size in 2025, while renovation activities represent the fastest pace at 4.16% through 2031.

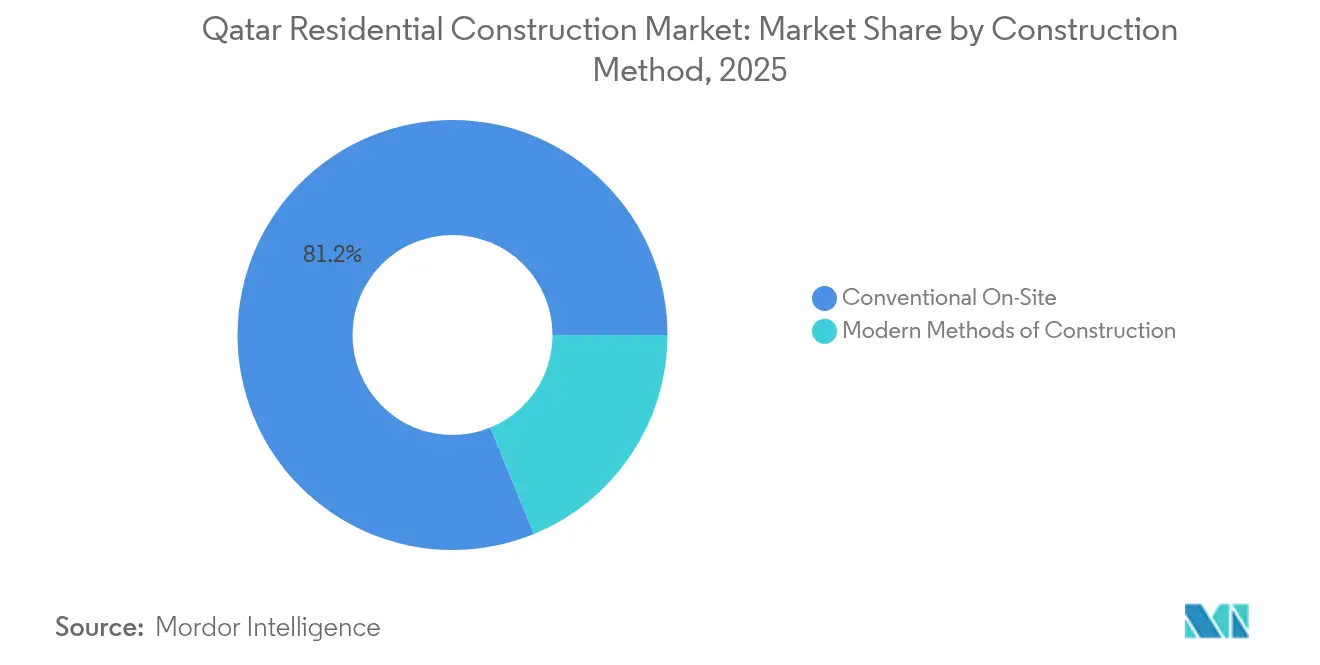

- By construction method, conventional on-site building retained 81.18% revenue share of the Qatar residential construction market in 2025; modern methods of construction are forecast to grow at 5.42% CAGR.

- By investment source, private capital controlled 67.14% share of the Qatar residential construction market in 2025, yet public investment is expected to rise at 5.02% CAGR on the back of affordable-housing programs.

- By geography, Doha accounted for 53.40% of the Qatar residential construction market size in 2025, whereas Al Khor is advancing at a 4.44% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Qatar Residential Construction Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Strong population growth & expatriate inflow | +0.8% | National; Doha, Al Rayyan | Medium term (2-4 years) |

| Government-backed affordable-housing programs | +0.6% | National; focus on Al Khor and rest of Qatar | Long term (≥ 4 years) |

| World Cup 2022 legacy infrastructure | +0.5% | Doha, Al Rayyan | Short term (≤ 2 years) |

| Expanding mortgage availability | +0.4% | National; strongest in urban centers | Medium term (2-4 years) |

| Shift toward smart-home-ready dwellings | +0.3% | Doha; selected projects in Al Khor | Long term (≥ 4 years) |

| Corporate demand for staff accommodation | +0.2% | Industrial zones; Doha business districts | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Strong Population Growth & Expatriate Inflow

Census data place the resident count at 2.85 million in 2024, with net immigration still trending upward. Revised residency rules now allow foreign buyers to secure permanent status with property investments starting at USD 200,000, effectively transforming transient workers into long-term homeowners. Real-estate transactions topped USD 2.24 billion in H1 2024, signalling a robust appetite for housing and supporting the Qatar residential construction market. Foreign-ownership liberalization across multiple sectors attracts multinational firms whose senior staff seek executive housing. Combined, these demographic and policy forces keep absorption rates healthy, even as Doha’s inventory swells[1]Noura Al-Thani, “Population and Housing Census 2024,” Planning and Statistics Authority, psa.gov.qa.

Government-Backed Affordable-Housing Programs

The QR 81 billion five-year infrastructure plan earmarks more than 5,500 serviced residential plots via public–private partnerships. Escrow rules under Law No. 6 of 2014 safeguard buyers, reducing risk premiums for budget projects. A 90% cut in business-registration fees that took effect in July 2024 trims soft costs for developers and contractors. The National Master Plan pushes mixed-income communities instead of isolated low-cost clusters, ensuring demand diversity and social buy-in. These measures enlarge the addressable buyer pool and underpin steadier growth in the Qatar residential construction market.

World Cup 2022 Legacy Infrastructure

Spending of USD 200-300 billion on stadiums, transport systems and utilities lowered future site-prep costs and expanded developable zones. Lusail City serves as a showcase of how mega-event assets morph into sustainable neighborhoods; the QNB–Qatari Diar tie-up on Huzoom Lusail underscores continuing institutional confidence. The Doha Metro extends the feasible commute radius, allowing residential projects in Al Sadd and similar nodes. Yet an oversupply of luxury stock downtown highlights the need to reposition certain assets. Effective reuse strategies will dictate whether these sunk costs translate into long-run gains for the Qatar residential construction market.

Expanding Mortgage Availability

Bank capital buffers near 20% enable competitive mortgage products despite higher provisioning after the World Cup cycle. A digital-assets framework introduced in September 2024 paves the way for tokenized real-estate finance that can cut transaction fees and improve transparency. Mortgage deals jumped 89% quarter-on-quarter in Q4 2024, indicating pent-up end-user demand that had been constrained by liquidity and paperwork hurdles. Middle-income expatriates newly eligible for permanent residency add further momentum. Easier credit broadens the funnel for apartment purchases and entry-level villa segments alike.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising land & construction-material costs | -0.7% | Nation-wide; acute in Doha core | Short term (≤ 2 years) |

| Potential housing oversupply in Doha core | -0.5% | Doha; spillover to Al Rayyan | Medium term (2-4 years) |

| Skilled-labor shortages post-megaproject peak | -0.4% | National; complex builds most affected | Short term (≤ 2 years) |

| Foreign-ownership caps outside free-hold zones | -0.3% | Non-designated areas | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Land & Construction-Material Costs

Input-price volatility stems from logistics bottlenecks and an overlapping public works agenda. Government procurement for roads, drainage and power grids competes directly with private residential builders for concrete, steel and skilled trades. Doha’s core districts command scarcity premiums, while fringe land often requires costly utility extensions. New localization rules that prioritize Qatari workers further elevate labor expense. Margin compression is most acute in affordable schemes, potentially slowing starts unless cost-saving modern methods gain broader adoption.

Potential Housing Oversupply in Doha Core

Investor surveys show 80% of stakeholders anticipate subdued price growth amid inventory overhang downtown. IMF commentary notes that transaction volumes and prices dipped post-World Cup, especially in the luxury tier. Modern metro connectivity mitigates some pressure by widening the commuter shed, yet vacant high-rise units act as a drag on headline performance. Successful developers are redirecting pipelines toward Al Khor and themed products like senior living, sidestepping the most saturated segments of the Qatar residential construction market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Apartments Anchor Demand while Villas Accelerate

Apartments and condominiums captured 64.35% of the Qatar residential construction market in 2025, underpinned by strong expatriate preference for maintenance-light living near employment hubs. This dominance translated into steady cash flows for developers that target long-stay renters and first-time buyers. High-density formats also align with urban land constraints and exploit the Doha Metro’s catchment area. Project launches in Lusail and Al Sadd feature compact floor plates paired with shared amenities, maximizing yield per square foot. The segment benefits from rising mortgage availability and digital-asset tokenization, which lower entry barriers for mid-income households.

Villas and landed houses remain a smaller slice today but are forecast to post the fastest 4.25% CAGR through 2031 as permanent residency reforms lure families seeking privacy and outdoor space. Developers have responded with master-planned communities in Al Khor and Al Rayyan, where land is cheaper and infrastructure pipelines are expanding. Smart-home-ready specifications and GSAS green-building standards differentiate offerings and support premium pricing. Villa projects thus widen revenue streams while moderating reliance on apartment sales concentrated in Doha. Together, both segments reinforce balanced growth in the Qatar residential construction market.

By Construction Type: New Builds Lead, Renovation Gains Traction

New construction represented 77.32% of the Qatar residential construction market size in 2025, owing to sustained population growth and delivery of plots under the QR 81 billion infrastructure plan. Developers enjoy shorter permitting paths on green-field sites designated in the National Master Plan, while public utilities installations are co-funded under public–private frameworks. High-rise apartment complexes and mid-market villa clusters form the bulk of current pipelines, leveraging economies of scale in procurement and labor deployment.

Renovation, however, is set to outpace with a 4.16% CAGR as the housing stock built during the 2000-2010 boom approaches refurbishment age. Owners choose upgrades to smart-home standards and energy-efficient façades to compete with the new supply. The strategy is cost-effective because it sidesteps land acquisition and benefits from escrow safeguards that assure buyers of title clarity. Mid-sized contractors specializing in retrofit services are scaling up, diversifying the competitive landscape of the Qatar residential construction market.

By Construction Method: Conventional Dominates, Modern Rises Quickly

Conventional on-site techniques still accounted for 81.18% of 2025 project value, reflecting entrenched contractor capabilities and regulatory familiarity. These builds rely on large labor pools and sequential workflows, leading to longer schedules yet offering flexibility for design adjustments during execution. Many apartment towers in central Doha continue to follow this path due to plot-specific customization demands and a perception of lower upfront risk among lenders.

Modern methods of construction, notably modular and prefabricated assemblies, are primed for a 5.42% CAGR as labor-cost inflation and nationalization quotas accelerate automation adoption. Gulf Contracting Company’s prefabrication arm and similar ventures by Midmac illustrate first-mover advantages. Factory-quality control reduces defects, while faster on-site assembly compresses financing costs. Remote projects in Al Khor and staff villages tied to industrial zones particularly favor off-site manufacturing, reinforcing technology-led evolution within the Qatar residential construction market.

By Investment Source: Private Capital Dominates, Public Commitments Intensify

Private investors held 67.14% of the Qatar residential construction market share in 2025 through freehold developments in Doha and co-development deals in Lusail. Aggressive landbanking before the World Cup enabled many local developers to maintain pipeline continuity with limited public dependence. Equity partners increasingly include regional family offices and sovereign funds attracted by stable rental yields.

Public-sector spending nevertheless records the higher 5.02% CAGR as the state channels resources into affordable housing and infrastructure-linked communities. The Ministry of Municipality partners with contractors via design-build-operate concessions that integrate roads, drainage, and community facilities. Such backing de-risks entry into secondary cities and supports social objectives without crowding out private innovation. Balanced funding sources, therefore, strengthen the resilience of the Qatar residential construction market.

Geography Analysis

Doha retained 53.40% of the 2025 project value on the strength of mature transport, education, and healthcare amenities that appeal to expatriates and nationals alike. The Doha Metro’s three lines broaden residential catchments to districts such as Al Sadd, easing congestion in core CBD areas and encouraging mixed-use vertical projects. Yet persistent luxury-unit oversupply moderates price appreciation, prompting developers to pivot toward mid-market offerings and retrofit programs. Real-estate transactions totaled USD 286 million in December 2024, a 12% monthly gain that signals liquidity even amid inventory gluts.

Al Rayyan’s suburban profile and cultural heritage sustain steady demand for villa compounds that balance privacy with access to Doha’s employment centers. Ongoing investments in healthcare facilities and international schools enhance liveability, while land values remain discounted to Doha’s prime corridors. The municipality’s planning approvals favor low-rise typologies, aligning with Qatari preferences for courtyard architecture. Emerging retail strips and community parks underpin rising absorption rates, positioning Al Rayyan as the stabilizing middle ground in the Qatar residential construction market.

Al Khor commands the fastest 4.44% CAGR through 2031 thanks to the USD 2 billion Al Khor Road that shrinks travel times to Doha International Airport and industrial zones. Government allocation of serviced plots under the QR 81 billion plan fast-tracks affordable and mid-market projects. Developers capitalize on lower land costs to offer larger floor plans, while GSAS guidelines ensure environmental standards are met. Public schools, healthcare clinics, and waterfront promenades are progressing in tandem, converting Al Khor into a viable alternative for families priced out of Doha. The city’s rise diversifies geographic risk for the Qatar residential construction market.

Competitive Landscape

The market exhibits moderate concentration, with QD-SBG Construction, Midmac Contracting, and HBK leading large residential contracts through established client relationships and end-to-end execution capacity. These firms leverage economies of scale in procurement and negotiate favorable payment terms, safeguarding margins even as materials costs fluctuate. Digital-twin tools and BIM platforms are increasingly embedded in tender requirements, nudging incumbents to upgrade technical capabilities.

International EPC players such as McDermott and China State Construction Engineering Corporation secure infrastructure-adjacent housing contracts by bundling advanced project-management systems and prefabrication know-how. Their presence raises quality benchmarks and encourages knowledge transfer to local subcontractors. Joint ventures with local sponsors help navigate regulatory frameworks and meet nationalization quotas, keeping competition dynamic within the Qatar residential construction market.

Mid-tier contractors like Gulf Contracting and Al-Balagh Trading & Contracting carve out niches in renovation, fit-out, and smart-home integration. Many have launched prefabrication subsidiaries to target Al Khor’s emerging pipeline, where off-site manufacturing shortens timelines. Fin-tech alliances that exploit the Digital Assets Framework offer smaller players alternative funding channels. White-space opportunities in senior-living and co-living formats remain largely uncontested, presenting entry points for agile firms.

Qatar Residential Construction Industry Leaders

QD-SBG Construction

Midmac Contracting Co. W.L.L.

Hamad Bin Khalid Contracting (HBK)

Galfar Al Misnad Engineering & Contracting

Porr Construction Qatar W.L.L.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Government unveiled the USD 22.2 billion 2025-2029 infrastructure plan, including 5,500 residential plots via PPPs Smart Water Magazine.

- January 2025: Qatar Public Works Authority allocated USD 3.6 billion for Q1 2025 capital works, prioritizing residential-linked infrastructure The Peninsula.

- January 2025: QNB Group partnered with Qatari Diar to finance land purchases for the Huzoom Lusail master plan Gulf Times.

- December 2024: KBN Group and Whirlpool surpassed deliveries of 50,000 connected appliances in the B2B segment The Peninsula.

Qatar Residential Construction Market Report Scope

Residential construction is the installation, maintenance, and repair of buildings and other stationary structures. Construction encompasses the processes involved in constructing buildings and infrastructure, as well as related operations, from start to finish.

A complete assessment of the Qatar Residential Construction Market includes an assessment of the economy and the contribution of sectors to the economy, a market overview, market size estimation for key segments, and emerging trends in the market segments. The report sheds light on market trends like growth factors, restraints, and opportunities in this sector. The competitive landscape of the Qatar residential construction market is depicted through the profiles of active key players. The report also covers the impact of COVID-19 on the market and future projections.

Qatar's residential construction market is segmented by type (apartments and condominiums, villas, and other types) and by construction type (new construction and renovation). The report offers market size and forecasts for the Global Container Terminal Operations Market in value (USD billion) for all the above segments.

| Apartments & Condominiums |

| Villas and Landed Houses |

| New Construction |

| Renovation |

| Conventional On-Site |

| Modern Methods of Construction |

| Public |

| Private |

| Doha |

| Al Rayyan |

| Al Khor |

| Rest of Qatar |

| By Type | Apartments & Condominiums |

| Villas and Landed Houses | |

| By Construction Type | New Construction |

| Renovation | |

| By Construction Method | Conventional On-Site |

| Modern Methods of Construction | |

| By Investment Source | Public |

| Private | |

| By Region | Doha |

| Al Rayyan | |

| Al Khor | |

| Rest of Qatar |

Key Questions Answered in the Report

What is the current size of the Qatar residential construction market?

The Qatar residential construction market is valued at USD 3.65 billion in 2026.

How fast is the market expected to grow?

Market value is projected to reach USD 4.42 billion by 2031, translating into a 3.92% CAGR.

Which segment holds the largest market share?

Apartments and condominiums dominate with 64.35% of 2025 value, reflecting strong urban-dweller and expatriate demand.

Which region is growing the quickest?

Al Khor is the fastest-expanding geography, forecast at a 4.44% CAGR through 2031 on the back of new transport links.

How are government policies supporting affordable housing?

The QR 81 billion 2025-2029 plan allocates over 5,500 serviced plots and offers fee abatements, lowering developer costs and widening buyer eligibility.

What construction technologies are gaining traction?

Modular and prefabricated methods are rising at a 5.42% CAGR as firms seek labor savings, quality gains and faster delivery times.

Page last updated on: