Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

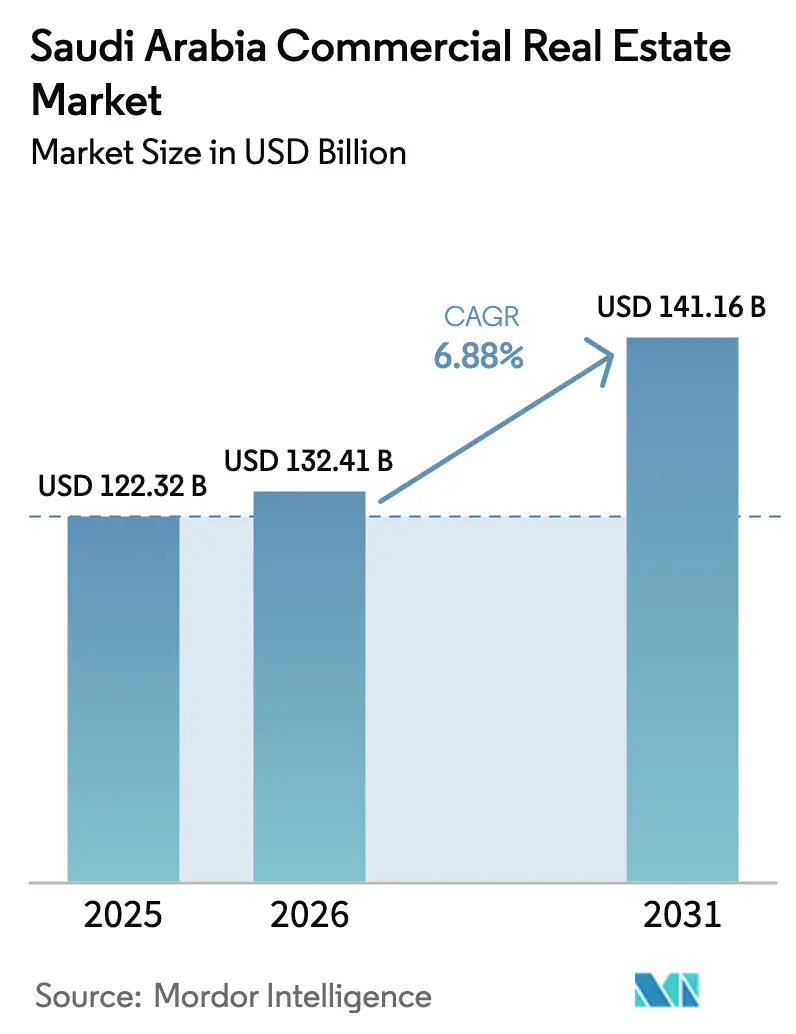

| Base Year Market Size (2025) | USD 122.32 Billion |

| Market Size (2026) | USD 132.41 Billion |

| Market Size (2031) | USD 141.16 Billion |

| Growth Rate (2026 - 2031) | 6.88% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Saudi Arabia Commercial Real Estate Market Analysis by Mordor Intelligence

The Saudi Arabia commercial real estate market size is USD 132.41 billion in 2026 and is projected to reach USD 141.16 billion by 2031, reflecting a 6.88% CAGR over the forecast period. Growth is reinforced by ongoing giga-project execution, active public-sector developers, and policy initiatives that continue to unlock demand for prime office, retail, and logistics assets. Office fundamentals remain strong in the capital due to the Regional Headquarters policy and sustained leasing from multinational corporations. Logistics demand benefits from rapid e-commerce adoption, a growing network of logistics centers, and new large-scale warehousing investments. Hospitality and mixed-use districts aligned to tourism and entertainment programs add to the pipeline of commercial spaces as real estate becomes a key channel for diversification.

Key Report Takeaways

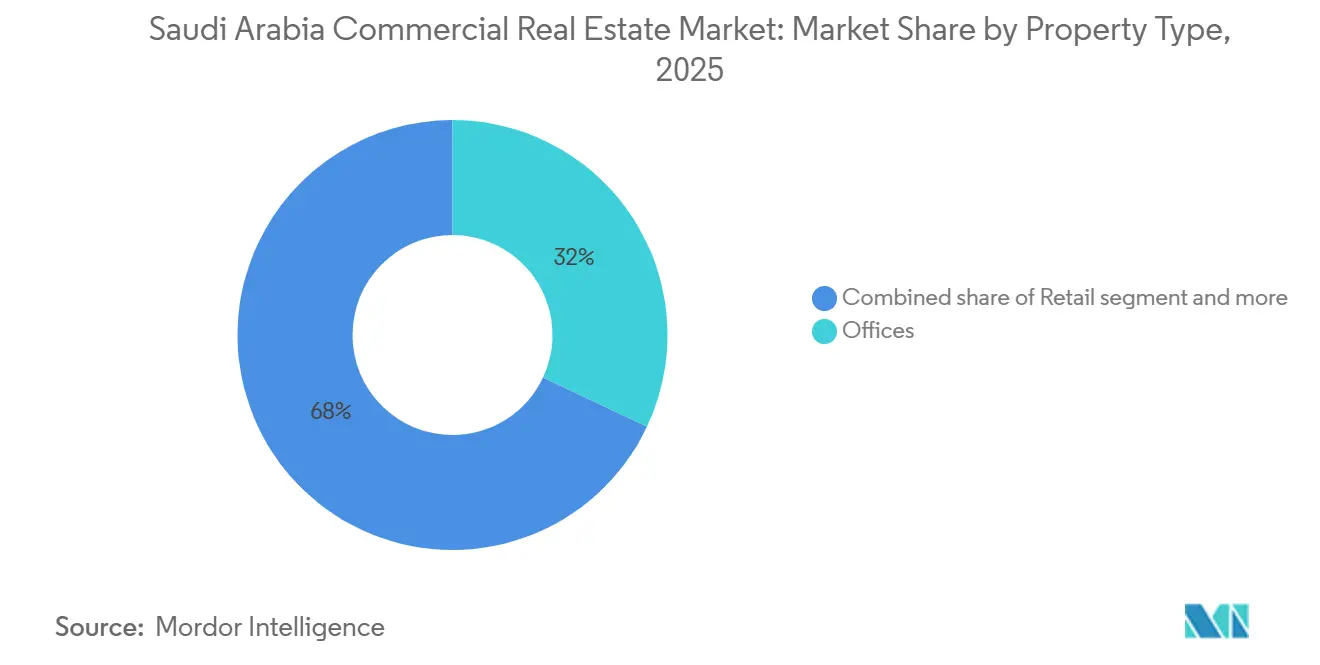

- By property type, Offices accounted for a 32% share of the Saudi Arabia commercial real estate market size in 2025, while Logistics posted the fastest growth at a 7.88% CAGR through 2031.

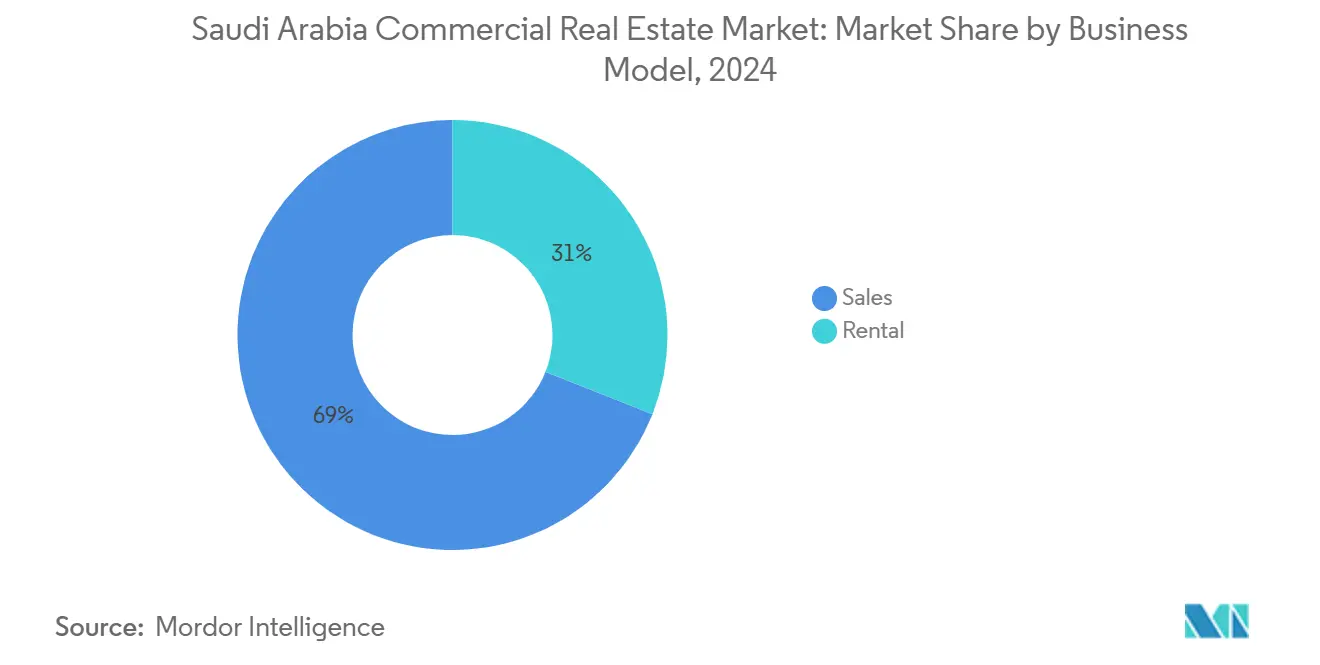

- By business model, Sales held 71% in 2025, while Rental recorded the highest projected growth with a 7.33% CAGR to 2031.

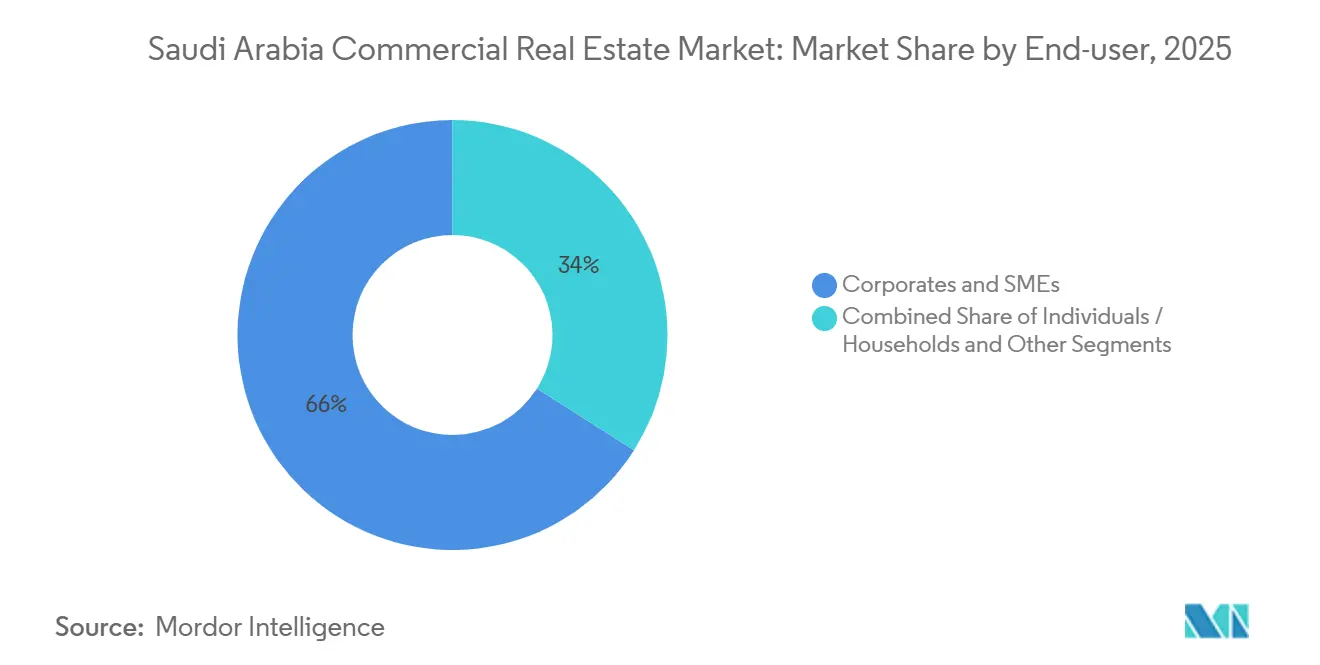

- By end-user, Corporates and SMEs led with 66% in 2025, while Individuals and Households are projected to expand at a 7.10% CAGR through 2031.

- By geography, Riyadh accounted for 49% in 2025, while Makkah is projected to expand at a 7.33% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Saudi Arabia Commercial Real Estate Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accelerated demand for prime industrial and logistics space driven by e-commerce | +1.8% | Riyadh, Jeddah, NEOM | Short term (≤ 2 years) |

| Government-backed infrastructure pipeline lifting commercial land values | +1.5% | Saudi Arabia | Long term (≥ 4 years) |

| Surge in institutional capital allocation to core office assets | +1.2% | Riyadh (King Abdullah Financial District), Jeddah | Medium term (2-4 years) |

| Re-rating of ESG-compliant green buildings unlocking premium rents | +0.9% | Riyadh, Jeddah, Eastern Province | Medium term (2-4 years) |

| Rebound in international tourism revitalising CBD hotel RevPAR | +0.7% | Makkah, Madinah, Red Sea, NEOM | Short term (≤ 2 years) |

| Data-localisation mandates fueling edge data-centre development | +0.6% | Riyadh, NEOM, Jeddah | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Accelerated Demand for Prime Industrial and Logistics Space Driven by E-Commerce

E-commerce order fulfillment rose to 290 million transactions in 2024, illustrating a step-change in distribution intensity and the need for modern, well-located warehouse space. Class A logistics sites near major airports and arterial highways are attracting multi-user developments from global operators, with one leading provider committing EUR 130 million (USD 140.4 million) for a large facility at Riyadh’s Special Integrated Logistics Zone, supported by bonded corridors and long-term land arrangements. Near-airport nodes and special zones have emerged as strategic anchors for automotive, technology, and retail supply chains, supporting temperature-controlled storage, value-added services, and compliance. Across the network, 23 activated logistics centers now cover 34.6 million square meters, with the Makkah region accounting for 20.4 million square meters, reinforcing regional fulfillment reach. As build quality improves and operating standards converge to global benchmarks, the Saudi Arabia commercial real estate market is positioned to see further consolidation of logistics footprints by multinational tenants.[1]https://www.stats.gov.sa/

Government-backed Infrastructure Pipeline Lifting Commercial Land Values

Large-scale urban programs, cultural assets, and mixed-use districts are redefining commercial corridors and elevating demand for surrounding plots. In Riyadh, New Murabba’s planned downtown redevelopment anchors prime offices, R&D spaces, and innovation hubs across 14 million square meters, with associated infrastructure catalyzing new corporate locations and retail-led experiences. Diriyah has rapidly executed awards across mixed-use clusters, including a major arena superblock with office towers and commercial amenities that broaden the occupier base and community services. Along the western coast, Red Sea Global’s phased resorts and mixed-use offerings are tying hospitality to retail and experiential spaces that require high standards for building performance and operations. These programmatic investments signal long-cycle demand creation and underpin the land value uplift that feeds into the Saudi Arabia commercial real estate market.[2]https://www.diriyahcompany.sa/en

Surge in Institutional Capital Allocation to Core Office Assets

Multinational corporations continue to scale their presence in Riyadh to align with the Regional Headquarters framework, reinforcing demand for Grade A offices in locations that concentrate policymaking and corporate decision centers. The requirement for substantive local operations has steered occupiers toward integrated districts with institutional property management and modern specs. King Abdullah Financial District has captured key tenants, including recent signings by global financial services firms, demonstrating sustained momentum for prime stock. The district’s extensive certified inventory and amenities support larger floorplates and higher space efficiency, improving occupier economics over long leases. As anchor tenants commit, institutional capital follows through acquisitions and development funding, deepening the liquidity profile of the Saudi Arabia commercial real estate market.[3]https://www.kafd.sa/

Re-rating of ESG-Compliant Green Buildings Unlocking Premium Rents

The Mostadam program has scaled local green building certifications, creating a clear pathway for projects to achieve recognized environmental and performance standards. International validation has strengthened the program’s credibility, allowing investors and tenants to benchmark outcomes against frameworks such as GRESB and LEED. KAFD’s concentration of LEED-certified assets and its smart neighborhood credential illustrate the leasing advantage of high-performing buildings, especially for multinationals with corporate sustainability commitments. Government-led schemes increasingly embed green standards from the outset, nudging private developers to adopt efficient MEP systems, smart energy management, and water-saving features to remain competitive. As operational savings accumulate and tenant preferences shift, ESG enhancements support stronger pricing and occupancy in the Saudi Arabia commercial real estate market.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Elevated construction costs and labour shortages delaying project delivery | -1.1% | Saudi Arabia | Short term (≤ 2 years) |

| Persistent work-from-home adoption softening CBD office net absorption | -0.8% | Riyadh, Jeddah | Medium term (2-4 years) |

| Monetary tightening and rising cap rates compressing transactions | -0.6% | Saudi Arabia | Short term (≤ 2 years) |

| Heightened climate-risk exposure raising insurance premiums for coastal assets | -0.4% | Jeddah, Red Sea Coast, NEOM | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Elevated Construction Costs and Labour Shortages Delaying Project Delivery

Input cost inflation and tight contractor capacity are pressuring delivery schedules for complex mixed-use and hospitality projects. Official construction cost indices showed persistent year-on-year increases through late 2025, driven by non-residential categories and high materials demand. Project owners are adopting modular construction and BIM-enabled coordination to improve productivity and protect timelines. Labor-market policies that promote localization are also reshaping workforce planning and wage structures across project ecosystems. These dynamics raise near-term execution risk and may stagger supply additions in the Saudi Arabia commercial real estate market.

Persistent Work-from-Home Adoption Softening CBD Office Net Absorption

As hybrid work practices mature, some occupiers are recalibrating space needs, adjusting layouts, and consolidating non-core locations. CBD Grade A remains supported by mandates that require senior executives to be present and by large organizations that prioritize proximity to government stakeholders. However, secondary submarkets with older buildings may experience slower leasing velocity as tenants seek flexible agreements and higher fit-out standards. Flexible workspace providers are expanding tailored solutions that blur the line between serviced offices and traditional leases. Over the medium term, selective softness in peripheral nodes may persist, even as prime CBD assets in the Saudi Arabia commercial real estate market maintain tight conditions.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Property Type: Core Office Strength Contrasts with Logistics Surge

Offices held the largest share at 32% in 2025, supported by policy-driven corporate relocation and the clustering benefits of integrated business districts. Prime office districts with LEED-certified assets and smart infrastructure have attracted leading financial and professional services firms that value proximity to regulators and clients. At King Abdullah Financial District, global tenants have expanded footprints and deepened long-term commitments, creating a base of stable demand. Complementing office momentum, retail and hospitality components within mixed-use districts are being calibrated to new lifestyle and experiential formats. Select large projects in Riyadh, including New Murabba and Diriyah, continue to expand the corporate and retail ecosystem that supports the Saudi Arabia commercial real estate market.

Logistics is the fastest-growing segment with a 7.88% CAGR, reflecting e-commerce fulfillment scaling to 290 million transactions in 2024 and continued investment in modern warehousing. International operators are committing capital to near-airport multi-user facilities, such as EUR 130 million (USD 140.4 million) allocated for a 53,000-square-meter site in Riyadh’s Special Integrated Logistics Zone. Nationwide, 23 activated logistics centers now cover 34.6 million square meters, with the Makkah region alone at 20.4 million square meters, extending last-mile reach for merchants. Riyadh’s prime office rents have also increased in recent years, with benchmark Grade A locations commanding premium annual rates around SAR 2,700 per square meter (USD 720), supported by constrained vacancy in the most sought-after assets. In parallel, evolving retail formats are aligning with mixed-use strategies that integrate F&B, entertainment, and hospitality to enhance dwell times and capture broader consumer spend within the Saudi Arabia commercial real estate market.

By Business Model: Sales Dominance Yields to Rental Momentum

Sales led with 71% in 2025, reflecting strong activity across master-planned communities, corporate plots, and pre-sales in integrated neighborhoods. Public-sector developers and partners continue to execute large residential and mixed-use agreements that expand community footprints and critical services. In the capital, flagship districts catalyze surrounding land sales as infrastructure deployment unlocks new corridors. Premium inventory tied to major nodes has seen consistent buyer interest from both local and expatriate households. These transactions reinforce construction pipelines that feed into the Saudi Arabia commercial real estate market.

The Rental segment is the fastest-growing model at a 7.33% CAGR as investors seek predictable income and as institutional-quality assets enter the market. Regulatory enhancements by the Capital Market Authority have expanded flexibility for real estate funds and REITs, including development participation in select markets and structured distribution policies. Large districts are exploring capital recycling through income funds, with assets that meet modern ESG and digital infrastructure standards gaining attention from long-horizon investors. Rental performance benefits from tightening in prime nodes and from operational improvements that reduce opex and enhance occupier experience. As balance sheets adjust to the rate environment, income assets remain central to capital deployment in the Saudi Arabia commercial real estate market.

By End-user: Corporate Giants Meet Rising Household Demand

Corporates and SMEs accounted for 66% in 2025, supported by the Regional Headquarters program that concentrates executive teams, consolidates decision-making, and increases demand for Grade A space. High-spec business districts that offer LEED-certified environments and resilient digital infrastructure continue to attract multinational businesses. KAFD’s tenant roster illustrates the appeal of integrated, amenitized hubs where financial services, advisory, and technology firms can co-locate. Corporate distribution footprints are also expanding due to e-commerce growth, with national logistics center coverage enabling faster deliveries across major routes. These occupier behaviors reinforce a broad base of demand and leasing depth within the Saudi Arabia commercial real estate market.

Individuals and Households are the fastest-growing cohort at 7.10% CAGR as policy reforms and master-planned communities enhance accessibility and lifestyle amenities. Large-scale communities continue to add apartments and townhomes that broaden the product mix beyond detached villas. Residential anchors connect residents to retail, education, and healthcare within short distances, improving live-work convenience. As new phases launch, integrated neighborhoods are attracting first-time buyers and long-stay tenants who value community services and modern building standards. This consumer-led momentum complements corporate demand, supporting mixed-use vitality in the Saudi Arabia commercial real estate market.

Geography Analysis

Riyadh captured 49% of 2025 turnover, reflecting its central role in headquarters consolidation and public investment activity. Flagship districts such as KAFD anchor blue-chip tenants, supported by LEED-certified buildings and sophisticated digital infrastructure. New Murabba advances plans for a 14-million-square-meter downtown with a signature mixed-use landmark and significant commercial and R&D space, while the broader corridor benefits from transit and amenities. Major logistics commitments include a EUR 130 million (USD 140.4 million) multi-user facility at the Special Integrated Logistics Zone near King Khalid International Airport, strengthening air cargo-led distribution. The pipeline of Grade A offices and logistics infrastructure reinforces Riyadh’s appeal to corporates and long-horizon capital in the Saudi Arabia commercial real estate market.

Jeddah’s coastal economy supports diversified commercial assets, including offices, logistics, and retail formats serving a large resident and visitor base. Grade A offices continue to attract professional services, with annual rent benchmarks in prime buildings around SAR 1,393 per square meter (USD 371.5) and healthy occupancy at the top end. Large retail destinations are being aligned with experiential concepts and stronger entertainment offerings to lengthen dwell times. Port-led logistics expansion and related industrial growth add to warehouse demand near key corridors. These features position Jeddah for steady leasing in high-quality assets within the Saudi Arabia commercial real estate market.

Makkah is projected as the fastest-growing region with a 7.33% CAGR, driven by religious tourism and accompanying mixed-use development. Jabal Omar’s multi-phase destination adjacent to the Holy Mosque integrates hotels, retail, and residences that elevate capacity and visitor services. Continued progress on adjoining transport and urban upgrades supports better circulation and expands commerce. Growth in hotel keys and retail adjacencies feeds into spillover demand for back-of-house logistics and workforce housing solutions. As the region scales, balanced planning around access, services, and environmental performance will be central to sustaining momentum in the Saudi Arabia commercial real estate market.

Regulatory Landscape

Saudi Arabia's commercial real estate market operates under a multi-agency framework led by the Real Estate General Authority (REGA) for the non-government real estate sector, alongside the Ministry of Municipalities and Housing (MOMAH) for municipal licensing and related development permissions. A key policy shift was the Law of Real Estate Ownership by Non-Saudis entering into force on 22 January 2026, followed by the Council of Ministers approving its Implementing Regulations on 23 June 2026, which moves foreign ownership permissions toward a more rules-based model tied to designated geographic zones.

Transaction formalization and compliance are increasingly supported by government digital platforms, including REGA's Aqari application for viewing contracts, licenses, and title deeds, and the Real Estate Registry (RER) for centralized property registration and subsequent transactions. For public land and assets, MOMAH's Regulations for the Disposition of Municipal Real Estate require public tenders for investing municipal land and buildings, shaping how developers and operators access municipally controlled commercial plots and premises.

Value Chain Analysis

The commercial real estate value chain in Saudi Arabia is shaped by public-sector master developers and affiliated entities that assemble land, sequence infrastructure, and award large, multi-package construction contracts, alongside private developers that finance, build, lease, and operate income assets. Downstream, brokers and agents support occupier sourcing and transactions, while property managers and facilities operators differentiate assets through building performance, tenant experience, and digital enablement, especially in Grade A offices, retail centers, and institutional logistics parks.

On the supply side, contractors and building materials suppliers face execution constraints linked to cost inflation, imported input dependence, and logistics volatility. Construction costs rose by 2% in March 2026 versus March 2025, driven by higher equipment rental, labor, and energy costs, while mega-project procurement volumes remain high, including awards exceeding SAR 30.03 billion in May 2026 and large single-project packages such as Rua Al Madinah's SAR 8 billion superblock award (April 2026) and the SAR 6 billion Khalidiyah redevelopment contract (June 2026). These dynamics increase the emphasis on procurement planning, localization initiatives promoted by the Public Investment Fund (PIF), and contract structures that can absorb shifts in labor, energy, and freight conditions.

Competitive Landscape

Public-sector developers and affiliates play a defining role, with giga-project sponsors influencing land assembly, infrastructure sequencing, and urban design at the national scale. ROSHN Group is building multi-asset communities that integrate retail, education, and health services, with SEDRA in Riyadh and MARAFY in Jeddah representing deep pipelines. Diriyah Company continues to award contracts across mixed-use nodes, expanding office clusters and residential districts that reinforce the capital’s growth corridors. Red Sea Global advances destinations with sustainability embedded, elevating standards for hospitality and retail integration. This platform-led approach enables consistent delivery and standard-setting in the Saudi Arabia commercial real estate market.

Private developers are pivoting toward asset operation and recurring income, complementing sales-led strategies. Mixed-use placemaking emphasizes walkability, convenience, and curated retail that lifts tenant performance and asset values. District-scale owners are exploring income vehicles and potential public listings to recycle capital while holding stabilized assets. Grade A office districts leverage certifications and smart infrastructure to attract global tenants and enhance rent resilience through cycle turns. This rebalancing underscores how operational capability is becoming a competitive differentiator in the Saudi Arabia commercial real estate market.

Global brands and operators continue to enter strategic partnerships that raise service standards and brand equity. Retail groups are aligning with international mall platforms to strengthen events, merchandising, and customer loyalty programs. Logistics operators are committing capital to multi-user sites in special zones to support growth in technology, retail, and automotive verticals. Hospitality partners are expanding luxury and lifestyle concepts in flagship destinations, adding high-end F&B and experiential elements that benefit adjacent commercial assets. These moves accelerate capability transfer and broaden investor participation in the Saudi Arabia commercial real estate market.

Saudi Arabia Commercial Real Estate Industry Leaders

Cenomi Centers

Hamat Holding

Unified Real Estate Development

KINAN International Real Estate

Alandalus Property

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

The 2026 shift in foreign ownership policy creates an opportunity set for institutional investors, developers, and operators targeting designated zones, supported by REGA's move toward a more standardized framework after the Law of Real Estate Ownership by Non-Saudis entered into force on 22 January 2026 and Implementing Regulations were approved by the Council of Ministers on 23 June 2026. Alongside this, large mixed-use and destination-led pipelines continue to translate into demand for offices, retail, hospitality, and supporting logistics space in key nodes such as Riyadh and the western regions, where flagship districts and redevelopment programs are expanding the investable stock of commercial assets.

Capital formation and operating model upgrades are also opening up near-term opportunities as the market broadens beyond sales-led development into income strategies, regulated funds, and tech-enabled operations. Evidence includes funding commitments for mixed-use development, such as the King Salman Park Foundation securing SAR 14.2 billion in commitments from two real estate funds (March 2026), and growing alignment between large developers and PIF-linked platforms, including the Cenomi Centers MoU with Saudi Downtown (February 2026) and the PIF and TMG MoU to assess cooperation on mixed-use projects (June 2026). Regulatory sandboxes further support PropTech deployment at asset and city scale, with REGA approving a Real Estate Sandbox framework (January 2026) and MOMAH launching a municipal and housing regulatory sandbox for urban innovation and smart city technologies (April 2026), enabling faster piloting of leasing, customer engagement, and building-operations solutions across commercial portfolios.

Recent Industry Developments

- June 2026: Unified Real Estate Development signed a memorandum of understanding with Al Rajhi Capital to explore collaboration on real estate funds. The agreement supports institutional capital formation around development-to-income strategies and adds another channel for structuring and distributing commercial real estate exposure in Saudi Arabia.

- May 2026: Cenomi Centers launched Cenomi Plus, a digital loyalty platform integrating shopping, dining, and entertainment across its mall portfolio. The platform supports tenant monetization and customer retention through first-party data, strengthening retail asset performance and portfolio-wide operating leverage.

- December 2024: Unified Real Estate Development signed a memorandum of understanding with SEDCO Capital to establish a SAR 1 billion real estate development fund. The agreement reflects the market's push toward scalable, fund-backed development models that can aggregate projects and broaden investor participation.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this methodology, the market covers the value created by completed, income-generating non-residential properties in Saudi Arabia, captured through sale and rental income potential across the core commercial asset base.

Scope exclusions: Vacant land, purely residential units, and standalone property-management services are excluded from the market value.

Segmentation Overview

- By Property Type

- Offices

- Retail

- Logistics

- Others (Industrial estate, Hospitality, etc.)

- By End-user

- Individuals / Households

- Corporates & SMEs

- Others

- By Region

- Riyadh

- Jeddah

- Makkah

- Rest of Saudi Arabia

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to set the fact base on supply additions, demand signals, and policy context that shape commercial property performance in Saudi Arabia. We relied on public sources such as official publications from the General Authority for Statistics, Saudi Central Bank releases on credit and macro indicators, Ministry of Municipal and Rural Affairs and Housing updates, and the Saudi Exchange filings for listed real estate and related firms.

To avoid building the model on a single data series, supporting inputs were also taken from sources such as customs and trade releases relevant to construction materials, peer-reviewed real estate and urban economics papers, and reputable press coverage of project completions and leasing activity. For company-level cross checks, annual reports, investor presentations, and audited financial statements were referenced where available, and a paid subscription was used for company financials and structured news screening. The sources listed here are illustrative rather than exhaustive, and additional public datasets and documents were also reviewed for collection, validation, and clarification.

Primary Interviews and Surveys

Primary work focused on validating how space is being absorbed and priced, and how quickly projects are moving from announcement to completion and leasing. We spoke with a balanced mix of developers, asset managers, brokers, occupiers, lenders, and advisors to pressure-test desk assumptions and to align the model with on-the-ground leasing and investment behavior.

Given this is a Saudi Arabia-focused study, the discussions were anchored around the main commercial hubs, and they were extended to secondary cities where new supply is being developed and demand is emerging.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 32% | CXOs: 14% | |

| Mid tier: 48% | Functional/Unit leaders: 34% | |

| Smaller Players: 20% | Managers: 52% |

Market-Sizing & Forecasting

Sizing started with a top-down build where the commercial stock and delivered pipeline were reconstructed by asset class using completion signals, leasing activity, and investment flows, which were then translated into value using achievable rent and price ranges. Once that structure was in place, selective bottom-up checks were added through sampled project roll-ups, broker channel checks, and simple rate times area sanity tests to adjust totals where the top-down path looked stretched.

Key inputs that shaped the market numbers included new completions entering the usable stock (linked to completion certification timing), occupancy and pre-lease trends, prime rent and effective rent movements, capitalization rate expectations, and the pace of new corporate registrations and tourism-related demand that can lift retail and hospitality performance. For forecasting, scenario analysis was used so that supply delivery timing, financing conditions, and rent growth could be flexed in a controlled way, and then aligned with what interviewees see as a realistic base case. Where bottom-up project information was incomplete, gaps were handled by using comparable project benchmarks by city and asset type, followed by a final consistency check against the overall demand pool.

Data Validation & Update Cycle

Validation was done through multi-step checks so the final totals are consistent with independent signals and with what practitioners report in the market. We compared outputs against proxy indicators such as construction delivery patterns, leasing momentum, and listed-company real estate revenue direction, and then reviewed any large variances by city and asset type before sign-off.

If an assumption moved the market meaningfully, it triggered a re-check of the source trail and, when needed, a follow-up with primary respondents to confirm what changed. Reports are refreshed annually, and interim updates are made when material events occur, such as policy shifts, sharp financing moves, or major project delivery changes. Before delivery, a fresh review pass is completed so clients receive the latest consistent view.

Mordor Intelligence's Saudi Arabia Commercial Real Estate Market Size Versus Other Published Estimates

Published market values for Saudi Arabia commercial real estate often differ because each publisher counts a slightly different thing, even when the title looks the same. The usual gaps come from how property income is defined, whether only completed assets are counted, and how rent and price assumptions are converted into a single USD market value.

A second driver is how supply timing is treated, since some estimates may bring projects into the market at announcement or construction stage, while others wait until assets are actually operational and earning. Another common difference is whether adjacent areas such as land sales, residential-led mixed-use value, or service fees are bundled into the total, which changes the number quickly without reflecting the same commercial demand pool. Counting developments only after official completion certification, and keeping land and standalone services out, explains much of the spread seen versus the table, a modeling choice applied by Mordor Intelligence.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 122.32 B (2025) | |

| Global Consultancy A | USD 45.20 B (2024) | This estimate appears to use a narrower value base and a different year, and it may mix revenue concepts such as appreciation with operating income, which reduces comparability to an income-potential view for completed commercial stock. |

| Regional Consultancy B | USD 67.00 B (2024) | The scope looks broader across asset types and can blend project references without a consistent completion-timing rule, which can shift the total up or down depending on how pipeline is treated. |

Overall, the table shows that year selection, what gets counted as commercial, and when a project is considered live are the practical reasons numbers diverge. By keeping inputs tied to observable stock delivery and market pricing signals, and then checking them through interviews and simple cross checks, we arrive at a market value that can be explained and repeated with the same steps.

Key Questions Answered in the Report

What is the current size and 5-year outlook for the Saudi Arabia commercial real estate market?

The Saudi Arabia commercial real estate market size is USD 132.41 billion in 2026 and is projected to reach USD 141.16 billion by 2031 at a 6.88% CAGR.

Which property type leads and which is growing fastest in Saudi Arabia commercial real estate?

Offices led with 32% of the Saudi Arabia commercial real estate market share in 2025, while Logistics is the fastest-growing at a 7.88% CAGR through 2031.

What is driving logistics demand in the Saudi Arabia commercial real estate market?

E-commerce fulfillment reached 290 million transactions in 2024 and major operators committed new capital to multi-user facilities near airports and special logistics zones.

Which business model is expanding quickest in Saudi Arabia commercial real estate?

Rental is the fastest-growing model at a 7.33% CAGR due to investor appetite for income assets and supportive fund regulations.

Which region is growing fastest and why in Saudi Arabia commercial real estate?

Makkah is projected at a 7.33% CAGR, supported by religious tourism and mixed-use projects expanding hotel and retail capacity.

How are ESG and green building policies influencing the Saudi Arabia commercial real estate market?

Mostadam certifications and LEED-aligned assets like KAFD are attracting tenants and investors, supporting premiums and operational savings.

Page last updated on: