Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Historical Data Period | 2020 - 2024 |

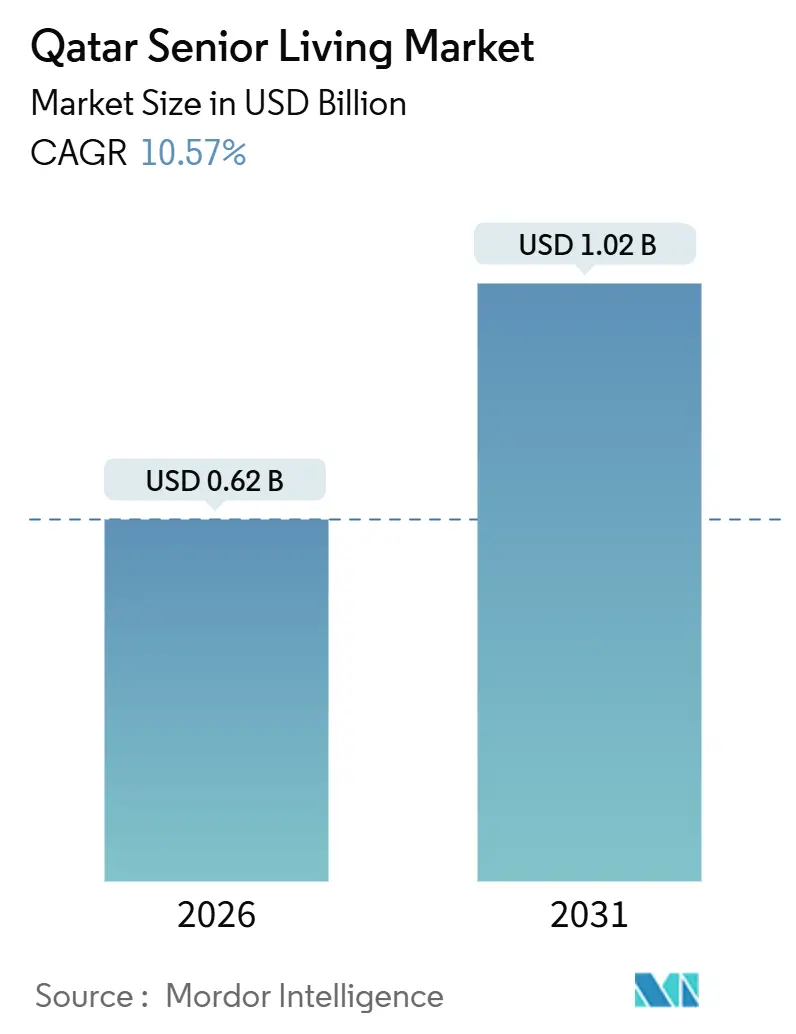

| Market Size (2026) | USD 0.62 Billion |

| Market Size (2031) | USD 1.02 Billion |

| Growth Rate (2026 - 2031) | 10.57% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Qatar Senior Living Market Analysis by Mordor Intelligence

The Qatar Senior Living Market size is estimated at USD 0.62 billion in 2026, and is expected to reach USD 1.02 billion by 2031, at a CAGR of 10.57% during the forecast period (2026-2031). Robust household wealth, the National Health Strategy 2024-2030, and mandatory health-insurance coverage are lifting demand for continuum-of-care communities. Operators are focusing on medically integrated campuses that blend post-acute rehabilitation, memory care, and tele-enabled independent units, while large mixed-use masterplans in Doha and Lusail supply land and infrastructure. Workforce availability remains a pressure point, yet new “Home Nurse” licensing and telemedicine reimbursement codes are reducing clinical staffing thresholds. Construction costs are high, but sovereign capital and bank financing continue to flow into hybrid projects that pair real-estate ownership with subscription-based services, supporting steady expansion of the Qatar senior living market.

Key Report Takeaways

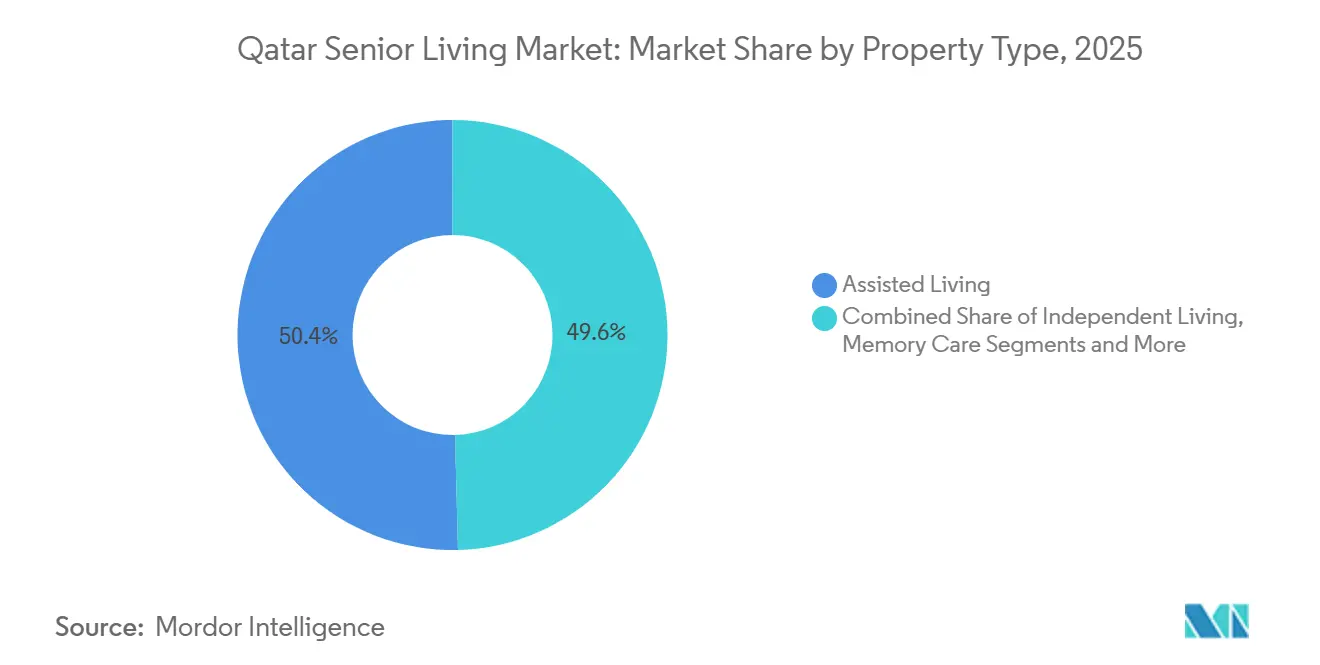

- By property type, Assisted Living held 50.4% of the Qatar senior living market share in 2025; Memory Care is forecast to expand at an 11.87% CAGR to 2031.

- By business model, the Long-Lease format led with 62.3% revenue share in 2025, while Hybrid structures are projected to advance at an 11.95% CAGR through 2031.

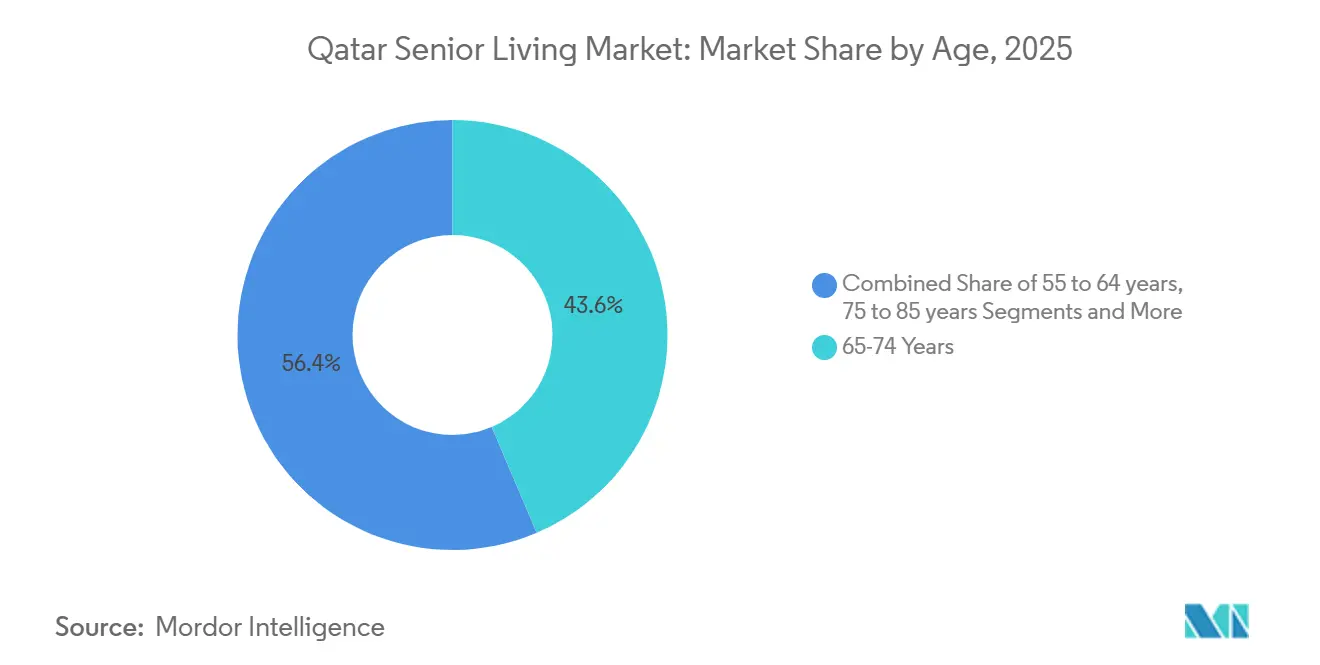

- By age band, the Above-85-year cohort accounted for 12% of the Qatar senior living market size in 2025 and is advancing at a 12.32% CAGR through 2031.

- By city, Doha captured 59.7% share of the Qatar senior living market in 2025; Lusail is on track for a 12.80% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Qatar Senior Living Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High per-capita income and strong insurance/healthcare coverage supporting premium, medically integrated communities | 3.1% | National, with the highest purchasing power in Doha, Lusail | Medium term (2-4 years) |

| The gradual aging of Qatari nationals increasing the need for independent, assisted, and memory care options | 2.8% | National, concentrated in Doha, Al Rayyan, Al Wakrah | Long term (≥ 4 years) |

| Government investment in healthcare and rehabilitation, enabling continuum-of-care models with hospitals/clinics | 2.5% | National, anchored by Doha-based HMC facilities, expanding to Lusail | Medium term (2-4 years) |

| Large mixed-use master plans suitable for age-friendly, accessible housing concepts | 1.4% | Lusail, Msheireb Downtown Doha, Gewan Island, Al Wakrah | Long term (≥ 4 years) |

| Tech-forward design improving outcomes and operating efficiency | 1.2% | National, led by TASMU Smart Qatar initiatives in Doha, Lusail | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Per-Capita Income And Strong Insurance/Healthcare Coverage Supporting Premium, Medically Integrated Communities

Qatar’s GDP per capita hit USD 71,054 in 2024, ranking within the world’s top-ten economies[1]. Wealthy households readily self-fund services that exceed Seha insurance limits, while expatriates carry mandatory private coverage under Law No. 22 of 2021. Developers are weaving longevity clinics and rehab suites into residential towers, illustrated by the 14,000-square-meter Pearl International Hospital launched in 2024. Premium pricing is therefore accepted for integrated care models, sustaining above-market growth for the Qatar senior living market.

Gradual Aging Of Qatari Nationals Increasing Need For Independent, Assisted, And Memory Care Options

Life expectancy reached 81.8 years in 2024, and national policy now targets 82.6 years, compressing morbidity into a shorter period and raising demand for higher-acuity care[2]. The National Ageing Survey, fielded in 2024-2025, gives operators the first detailed picture of mobility, cognition, and social networks among citizens aged 60+, enabling sharper product-mix decisions. Early findings indicate a faster-than-expected transition from assisted-living to memory-care needs, mirroring global longevity trends. Physicians are encouraged to direct post-acute patients toward community settings, reinforcing occupancy for private operators. Together, these elements add long-run momentum to the Qatar senior living market.

Government Investment In Healthcare And Rehabilitation Enabling Continuum-of-Care Models

Hamad Medical Corporation’s 2024-2030 strategy modernises Hamad General Hospital and strengthens pathways to the Qatar Rehabilitation Institute, allowing smoother discharge into private communities[3]. Parallel expansion by the Primary Health Care Corporation broadens chronic-disease support in outpatient settings. Newly formalised “Home Nurse” licensing lets practical nurses perform wound care and medication administration within residences, lowering acuity thresholds. Smart-building pilots with Qatar Science & Technology Park embed telehealth and remote monitoring, further tightening clinical linkages. Collectively, these initiatives anchor the Qatar senior living market within the national continuum of care.

Large Mixed-Use Masterplans Suitable For Age-Friendly, Accessible Housing Concepts

Lusail’s USD 250 billion city plan applies universal-design principles - wide sidewalks, sheltered crossings, and transit-first layouts - that facilitate ageing in place. Msheireb Downtown Doha’s QAR 20 billion (USD 5.5 billion) redevelopment follows a similar blueprint focused on walkability and LEED certification. Sovereign wealth backing, seen in Qatar Investment Authority’s 49% stake in Msheireb Properties, affirms confidence in age-friendly urbanism. Developers can thus test senior-living demand using standard residential stock before deploying specialised campuses, which extends supply flexibility and supports steady growth in the Qatar senior living market.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cultural preference for multigenerational living limiting institutional senior-housing adoption | -1.9% | National, strongest in traditional Qatari households | Long term (≥ 4 years) |

| Small addressable population and workforce constraints in geriatrics/nursing pressuring scale and costs | -1.6% | National, acute in Doha, Al Rayyan, Lusail | Medium term (2-4 years) |

| High land/build costs and evolving regulations/licensing complicating feasibility for new entrants | -1.3% | Doha, Lusail, Al Wakrah | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Cultural Preference For Multigenerational Living Limiting Institutional Adoption

Family obligations remain powerful across the Gulf, and moving elders into facilities can be viewed as social abandonment. Ehsan’s four-day care centres serve 261 seniors, yet stop short of residential care, underscoring persistent stigma. Early survey data show fewer than 10% of Qatari seniors deem institutional living acceptable. Operators, therefore, market communities as medically necessary rather than lifestyle choices, narrowing the addressable pool. This cultural headwind dampens the Qatar senior living market’s upside despite demographic ageing.

Small Addressable Population And Workforce Constraints Pressuring Scale And Costs

Only 60,000 citizens were aged 65+ in 2024, and even a 10% facility-placement rate equates to 6,000 beds—insufficient for economy-of-scale efficiencies. Hospitals and primary-care centres compete aggressively for geriatric nurses, inflating wage bills and staff turnover. Operators import caregivers from South Asia, but face visa quotas and mandatory training costs under Department of Healthcare Professions rules. Tight labour supply forces premium pricing, which elevates barriers to entry and constrains expansion of the Qatar senior living market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Property Type: Memory Care Outpaces Assisted-Living Growth

Assisted Living captured 50.4% of the Qatar senior living market share in 2025, reflecting its role as the default transition from multigenerational homes. Memory Care, however, is projected to expand at an 11.87% CAGR through 2031, eclipsing overall market performance by 130 basis points. Developers are positioning purpose-built dementia wings inside mixed-use precincts—Pearl International Hospital’s geriatric suites being a prime example—to monetise premium pricing that runs 30%-50% above Assisted Living rates. The National Ageing Survey’s cognitive-screening modules promise granular prevalence data, unlocking more accurate underwriting of unit counts.

Beneath the headline, independent-living supply remains thin because cultural norms still favour family care for active elders. Yet “Home Nurse” licensing and ubiquitous broadband are extending the life of independent units by layering tele-nursing atop lifestyle amenities. Nursing-care beds command the highest staffing ratios and face the steepest wage inflation, so operators are sequencing their developments: independent and assisted blocks open first, with memory and nursing wings added once occupancy stabilises. As longevity rises and diagnostic rates improve, Memory Care’s share of the Qatar senior living market size is poised to climb steadily.

By Business Model: Hybrid Structures Test Market Flexibility

Long-Lease contracts held 62.3% of revenue in 2025, favoured by both Qatari families who preserve liquidity for healthcare costs and expatriates planning repatriation. Hybrid schemes—unit purchase paired with monthly service fees—are forecast to grow at an 11.95% CAGR, reflecting appetite for real-estate ownership as a hedge against inflation while retaining service flexibility. Barwa Real Estate’s 96%-occupied Barwa Village demonstrates that mixed-tenure blocks can absorb older residents without age-segmented branding.

Hybrid models de-risk operators’ cash flows by separating property proceeds from operating income. United Development Company’s Crystal Residence, which pre-sold 46% of units by late 2024, shows how freehold apartments inside leisure-rich precincts attract both investors and prospective seniors. Sovereign backing, exemplified by Qatar Investment Authority’s stake in Msheireb Properties, suggests capital markets view hybrid senior stock as mainstream real estate rather than niche healthcare. This blending of ownership and rental underpins durable expansion for the Qatar senior living market.

By Age: Above-85-Years Cohort Drives Acuity Mix

The 65-to-74-year band accounted for 43.6% of occupancy in 2025, yet the Above-85-year cohort is on track for a 12.32% CAGR, the fastest across all age groups. As early retirees age into higher-dependency phases, operators must front-load investment in skilled-nursing and memory-care beds. Hamad Medical Corporation’s push to shorten hospital stays sends more very-old patients directly to community facilities, raising acuity-mix complexity.

Telemedicine rules are lengthening the time younger seniors can remain in independent apartments, but once frailty sets in, transitions to care-intensive units are swift. The National Ageing Survey’s functional-assessment data will sharpen forecasts of daily-living limitations, guiding design ratios between Assisted Living, Memory Care, and Nursing Care. Age-stratified product planning thus remains central to sustaining margins across the Qatar senior living market.

Geography Analysis

Doha retained 59.7% of occupied beds in 2025, supported by Hamad General Hospital, the Qatar Rehabilitation Institute, and December 2024’s Pearl International Hospital launch, which collectively channel post-acute referrals into nearby communities. High GDP per capita and a walkable downtown redevelopment in Msheireb further enhance resident appeal. Sovereign investment into age-friendly districts keeps absorption strong despite premium pricing, cementing Doha’s leadership in the Qatar senior living market.

Lusail is the fastest-rising geography, forecast for a 12.80% CAGR through 2031. Its vast mixed-use footprint allows purpose-built accessibility, while upcoming health nodes tied to Hamad Medical Corporation will shorten critical-care transfer times. Early sales at Gewan Island and strong uptake of Crystal Residence signal lifestyle pull factors that resonate with affluent seniors seeking alternatives to Doha’s costlier core.

Al Rayyan and Al Wakrah together contributed roughly one-quarter of 2025 demand, buoyed by lower land prices yet constrained by thinner clinical ecosystems. Rural districts remain marginal because staffing, transport, and emergency-care gaps outweigh affordability benefits. Consequently, the Qatar senior living market will stay concentrated in the capital corridor, with Lusail absorbing the lion’s share of incremental growth.

Competitive Landscape

The market is moderately concentrated, with land-rich state-linked developers - Barwa Real Estate, Qatari Diar, Msheireb Properties, and United Development Company - controlling most prime locations. None, however, operates a dedicated senior-living brand, leaving supply fragmented across mixed-use assets and home-care providers. Barwa’s USD 824 million financing line and USD 5.5 billion pipeline show readiness to pivot into hybrid senior projects once cultural acceptance improves.

Competition increasingly centers on embedding care capability inside broader master plans. Msheireb Downtown’s USD 5.5 billion outlay and Lusail’s USD 250 billion budget demonstrate scale plays where senior units complement retail and hospitality rather than stand alone. United Development Company’s smart-building MOU with Qatar Science & Technology Park highlights technology as a differentiator that extends resident independence.

International operators eye white-space in memory care and skilled nursing, segments growing fastest yet undersupplied. Licensing clarity around telemedicine now permits asset-light entrants to lead with care-coordination models, partnering with local developers for real-estate delivery. As projects mature, the Qatar senior living market will likely shift from fragmented offerings toward branded, medically integrated platforms.

Qatar Senior Living Industry Leaders

Ehsan – Center for Empowerment & Elderly Care

Hamad Medical Corporation

Barwa Real Estate Company

Qatari Diar Real Estate Investment Company

United Development Company

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Qatar Investment Authority purchased 49% of Msheireb Properties, injecting sovereign capital into the USD 5.5 billion Msheireb Downtown Doha redevelopment.

- March 2025: United Development Company unveiled The Pearl International Hospital, a 14,000 m² full-service facility to be run by Ruzgar Healthcare Holding. Placing a hospital inside a luxury neighborhood on The Pearl-Qatar should channel patients straight into nearby senior-living communities and could become a model for pairing housing and healthcare.

- February 2025: QLM Life & Medical Insurance teamed up with Aspetar to start direct billing for its top-tier “Prestige” members from March 2025. It is Aspetar’s first arrangement of this kind with an insurer and shows how closer insurer-provider links can simplify covered services for older residents.

- January 2025: Qatari Diar updated its Lusail City blueprint, confirming space for more than 200,000 residents plus built-in clinics, parks, and barrier-free streets. The plan gives senior-living operators a ready-made, wellness-oriented setting.

Qatar Senior Living Market Report Scope

Senior living is a concept that refers to a variety of housing and lifestyle options for senior citizens that are adapted to the challenges of aging, such as limited mobility and susceptibility to illness. The report offers a complete analysis of the Qatar Senior Living Market, including a market overview, market size estimation for key segments emerging trends by segments, and market dynamics. The report also offers the impact of COVID-19 on the market.

Qatar's senior living market is segmented by property type (assisted living, independent living, memory care, and nursing care) and by city (Doha, Al Wakrah, Al Rayyan, and Umm Salal Muhammad).

The report offers market size and forecasts for the senior living market in value (USD) for all the above segments.

By Property Type

| Assisted Living |

| Independent Living |

| Memory Care |

| Nursing Care |

By Business Model

| Outright Sale (Freehold) |

| Long-Lease / Rental |

| Hybrid (Sale + Lease) |

By Age

| 55 to 64 years |

| 65 to 74 years |

| 75 to 85 years |

| Above 85 years |

By Key Cities

| Doha |

| Al Rayyan |

| Al Wakrah |

| Lusail |

| Rest of Qatar |

| By Property Type | Assisted Living |

| Independent Living | |

| Memory Care | |

| Nursing Care | |

| By Business Model | Outright Sale (Freehold) |

| Long-Lease / Rental | |

| Hybrid (Sale + Lease) | |

| By Age | 55 to 64 years |

| 65 to 74 years | |

| 75 to 85 years | |

| Above 85 years | |

| By Key Cities | Doha |

| Al Rayyan | |

| Al Wakrah | |

| Lusail | |

| Rest of Qatar |

Key Questions Answered in the Report

What is the current size of the Qatar senior living market?

The Qatar senior living market size is USD 0.62 billion in 2026.

How fast is the Qatar senior living market expected to grow?

The market is forecast to post a 10.57% CAGR, reaching USD 1.02 billion by 2031.

Which property type is expanding quickest in Qatar’s senior housing landscape?

Memory Care leads growth with an 11.87% CAGR forecast to 2031.

Why is Lusail considered the fastest-growing city for senior living projects?

Lusail’s USD 250 billion masterplan integrates universal design and planned healthcare nodes, driving a 12.80% CAGR to 2031.

What workforce challenges confront senior-living operators in Qatar?

Limited local geriatric specialists and competition from public hospitals elevate wage costs and turnover, pressuring margins.

How are hybrid business models changing Qatar’s senior-living financing?

Hybrid formats let residents buy units while paying monthly service fees, diversifying developer revenue and appealing to asset-oriented families.

Page last updated on: