Investment Casting Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 18.45 Billion |

| Market Size (2031) | USD 23.82 Billion |

| Growth Rate (2026 - 2031) | 5.25% CAGR |

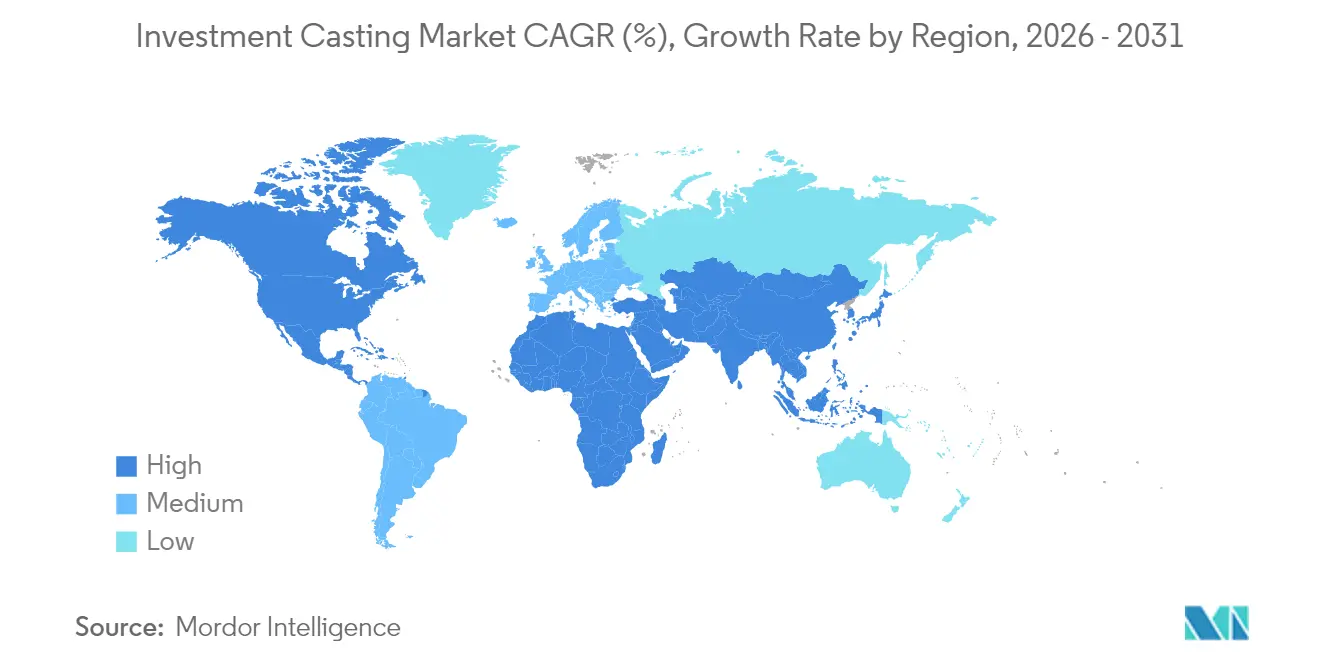

| Fastest Growing Market | North America |

| Largest Market | Asia Pacific |

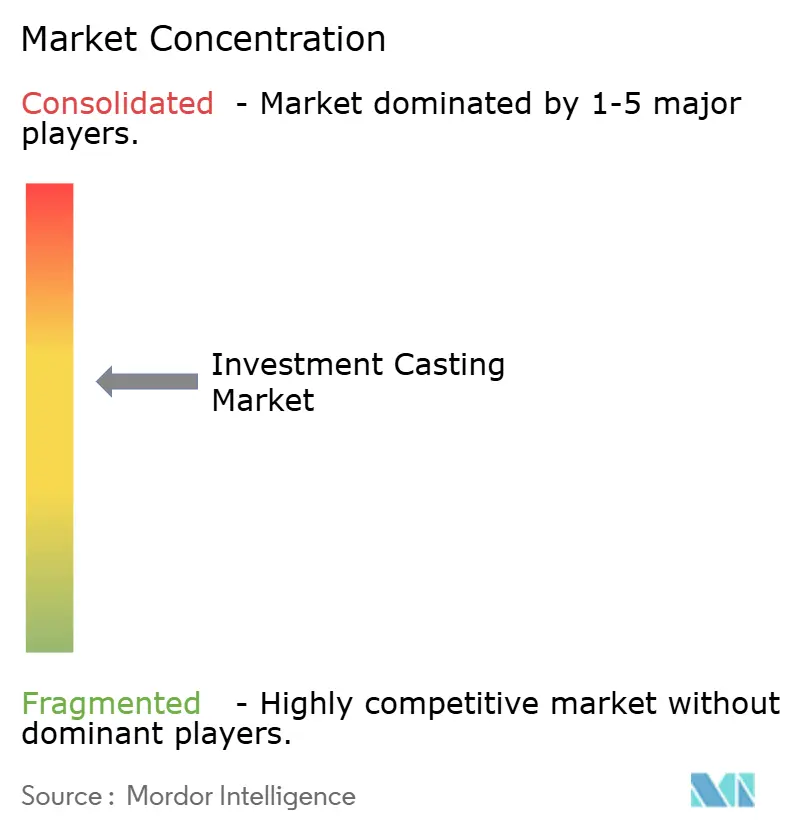

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Investment Casting Market Analysis by Mordor Intelligence

Investment Casting Market size in 2026 is estimated at USD 18.45 billion, growing from 2025 value of USD 17.53 billion with 2031 projections showing USD 23.82 billion, growing at 5.25% CAGR over 2026-2031. The investment casting market functions as a precision-manufacturing backbone for aerospace fleet renewals, automotive lightweighting programs, and next-generation energy systems. Demand benefits from near-net-shape capabilities that cut machining steps, slash scrap rates, and help OEMs meet stringent sustainability targets. Silica-sol shell systems, 3D-printed patterns, and hybrid ceramic technologies collectively raise quality standards while compressing lead times.

Key Report Takeaways

- By process type, silica-sol accounted for 50.78% revenue share of the investment casting market size in 2025, while hybrid and other processes are forecast to register a 5.30% CAGR to 2031.

- By material, stainless steel commanded 32.98% of the investment casting market size in 2025; super-alloys are poised for the quickest advancement at a 5.76% CAGR from 2026-2031.

- By end-user, aerospace and defense captured 36.07% of the investment casting market share in 2025; energy and power is expected to grow the fastest at 5.58% CAGR through 2031.

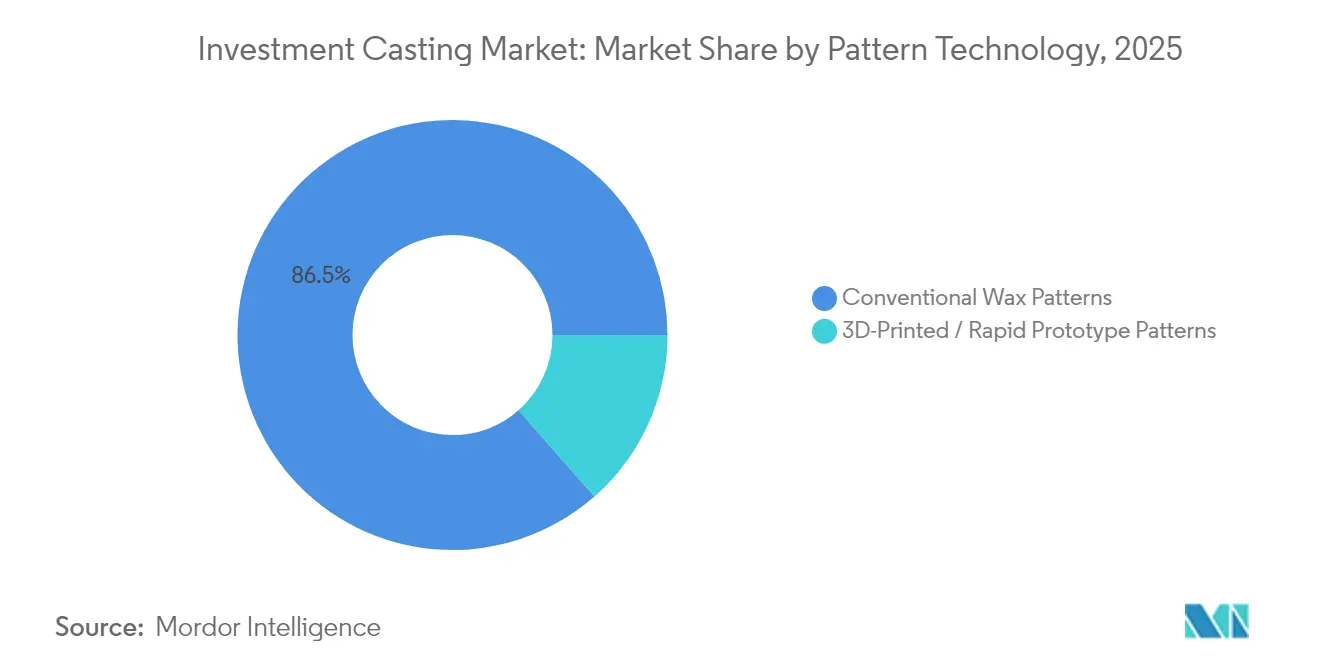

- By pattern technology, conventional wax patterns retained 86.47% revenue share in 2025; 3D-printed patterns are expanding at a 5.74% CAGR over the forecast period.

- By component weight, 1–10 kg parts held 51.94% of the investment casting market share in 2025, while components up to 1 kg are projected to register the fastest 5.31% CAGR through 2031.

- By geography, Asia-Pacific led with 43.97% of the investment casting market share in 2025; North America is projected to deliver the fastest regional CAGR at 5.36% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Investment Casting Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fleet-renewal programs | +1.2% | Global, with early gains in North America, Europe, Asia-Pacific | Long term (≥ 4 years) |

| Shift to hydrogen & e-fuel turbines | +0.9% | Europe and North America, with expansion to Asia-Pacific | Long term (≥ 4 years) |

| Lightweighting push in automotive components | +0.8% | Global, with a concentration in North America and the EU | Medium term (2-4 years) |

| Near-net-shape casting lowers machining scrap | +0.7% | Global | Medium term (2-4 years) |

| Rapid prototyping | +0.6% | North America and EU core, spill-over to Asia-Pacific | Short term (≤ 2 years) |

| Supply-chain re-localisation incentives | +0.5% | North America and EU | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Fleet-Renewal Programs in Commercial & Defense Aviation

Commercial aviation rebound lifts turbine blade and vane demand, evidenced by Precision Castparts Corp reporting a 22.7% year-over-year revenue increase to drastically in 2023. Simultaneously, defense ministries accelerate fighter and unmanned-aerial-system procurements that rely on nickel and cobalt super-alloy castings. Suppliers such as PBS Velka Bites manufacture integrally cast airfoil components up to 400 mm diameter, eliminating assembly joints that add weight and inspection complexity. AS 9100 and NADCAP certifications allow direct delivery into Tier-1 engine programs, streamlining qualification cycles. Improved material yield, design consolidation, and thermal-efficiency benefits collectively boost the investment casting market as airlines and defense agencies modernize fleets through 2030.

Shift to Hydrogen & E-Fuel Turbines Needing Complex Hot-Section Parts

Power producers upgrade gas-turbine fleets for hydrogen blends, e-fuels, and carbon-capture compatibility. Advanced hot-section castings require internal cooling passages and high-temperature super-alloys. Research on Ti-6Al-4V investment casting shows yield strengths of 636 MPa and ultimate tensile strengths of 687 MPa, meeting turbine stress thresholds. Novel calcium-zirconate crucibles raise melt purity for titanium and nickel alloys. Investment casting eliminates weld joints, reducing crack-propagation risks under hydrogen combustion. European utilities and North American independents procure these precision parts to retrofit existing assets and equip new high-efficiency turbines, underpinning long-run growth for the investment casting market.

Lightweighting Push in Automotive Components

Automakers intensify weight-reduction targets to extend electric-vehicle driving ranges and meet fuel-economy mandates. Tesla’s gigacasting strategy collapses multi-piece chassis assemblies into singular cast sections that drop cost and tooling complexity.[1] “2024 Impact Report,” Tesla Inc., tesla.com Ford and Volvo have invested EUR 855 million in megacasting lines to apply similar concepts across mainstream vehicle programs.[2]“Torslanda Plant EUR 855 Million Electrification Upgrade,” Ford Motor Company, corporate.ford.com Investment casting complements these die-casting megastructures by supplying complex aluminum and magnesium brackets, suspension knuckles, and heat-management parts that cannot be produced by high-pressure die casting alone. Near-net-shape output removes multiple machining passes, cuts cycle energy, and lowers embedded carbon footprints. These advantages position the investment casting market for sustained volume gains as OEMs broaden integrated-casting platforms across luxury, commercial, and utility vehicle lines.

Rapid Prototyping Boosts Low-Volume Precision Casting Demand

Additive manufacturing slashes traditional wax-tooling lead times from weeks to hours, yielding 50-90% cost savings for complex prototypes. 3D Systems and Kimura Foundry America employ printed patterns and ceramic shells that bring design iterations into rapid cycles, especially for aerospace, medical, and motorsport customers requiring batches of 1–500 parts. The printed investment casting shell (PICS) technique bypasses wax entirely, printing ceramic molds able to withstand pour temperatures above 1,600 °C. This digital shift helps foundries win new business segments where first-article approval speed and design flexibility are decisive. As a result, the investment casting market captures incremental demand traditionally lost to machining or metal-additive services.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Capital-intensive automation | -0.8% | Global, with higher barriers in emerging markets | Medium term (2-4 years) |

| Volatility in nickel & refractory ceramic prices | -0.7% | Global, with higher impact in Asia-Pacific | Short term (≤ 2 years) |

| Shortage of metallurgical talent | -0.6% | Global, with acute impact in North America and EU | Long term (≥ 4 years) |

| Strict environmental norms on foundry emissions | -0.4% | North America and EU, expanding to Asia-Pacific | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Volatility in Nickel & Refractory Ceramic Prices

Nickel and rare-earth element price spikes compress margins for aerospace-grade alloy castings. Super-alloy supply tightness—EU classifies rhenium and ruthenium as critical raw materials—forces foundries to institute hedging programs and seek long-term agreements with miners. Recycling gains strategic value, with companies like Greystone Alloys deploying pyrometallurgical systems to reclaim high-value elements from machining swarf and end-of-life blades. The investment casting market partially mitigates cost pressure via low-scrap, near-net-shape geometries, yet sustained volatility remains a headwind for profitability in the short term.

Strict Environmental Norms on Foundry Emissions & Waste Wax

The United States EPA Metal Molding and Casting Effluent Guidelines govern 28 process segments, compelling foundries melting above 20,000 tons annually to invest in filtration, wax-reclamation, and closed-loop water systems. In the United Kingdom, the Climate Change Agreement mandates phased emission-reduction targets while adjusting buy-out fees. These regulations elevate capital expenditure burdens for small players and add administrative complexity around reporting. Foundries that integrate energy-efficient furnaces and high-recovery wax systems maintain competitiveness, whereas laggards risk penalties and contract losses, tempering overall growth in the investment casting market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Process Type: Silica-Sol Dominance Drives Quality Standards

Silica-sol shells delivered 50.78% of the investment casting market revenue in 2025, reflecting robust demand from turbine-blade and orthopedic-implant programs that specify surface roughness below Ra 1.6 µm. Hybrid shells that pair printed ceramic cores with silica-sol face coats post the fastest 5.30% CAGR, aided by lower wax consumption and faster burnout cycles. Sodium-silicate processes continue serving cost-sensitive pump and valve orders within the investment casting market, although their share erodes as buyers elevate finish requirements. Emerging printed investment casting shell workflows allow tool-less production, trimming pattern lead times and enabling on-the-fly geometry changes for rapid-prototype lots. Shell material research indicates finer alumina powders and polymer binders reduce thermal expansion mismatch, cutting crack rework rates below 2%.

Process engineers increasingly apply real-time thermal imaging and IIoT sensors to monitor shell dehydration and sintering profiles. These data streams feed machine-learning models that adjust slurry viscosity and air-flow velocities, boosting first-time-through yields. Collectively, silica-sol and hybrid technologies anchor quality benchmarks, while digital control accelerates throughput, reinforcing the dominant role this segment plays within the investment casting market.

By Material: Super-Alloys Lead Innovation Despite Stainless Steel Dominance

Stainless steel retained 32.98% revenue in 2025 given its versatility for corrosive fluid-handling and chassis components. Conversely, super-alloys chart the highest 5.76% CAGR as engine OEMs certify nickel-, cobalt-, and titanium-based chemistries for hydrogen-ready turbines. Feeding studies reveal that high-nickel alloys require 18% shorter gating distances than low-alloy steels, spurring specialized mold-flow software updates. Recycling initiatives concentrate on reclaiming rhenium and ruthenium from spent blades, bolstering circular supply chains for the investment casting industry.

Carbon-steel and alloy-steel castings support the automotive and agricultural segments, where performance requirements balance cost targets. Aluminum and magnesium alloys tap lightweighting momentum, particularly for gearbox housings and battery-case brackets in electric vehicles. Continuous alloy development, such as TiAl turbocharger wheels, widens application boundaries and raises the value proposition for the investment casting market.

By End-User: Energy Sector Accelerates While Aerospace Leads

Aerospace and defense applications captured 36.07% global revenue in 2025 as OEMs re-engine core platforms and defense ministries upgrade fighter engines. The segment relies on integrally cast airfoils and structural brackets that cut part counts by up to 60%. Energy and power constitutes the quickest-rising end-user at 5.58% CAGR, propelled by hydrogen-combustion turbine retrofits and e-fuel demonstration plants.

Automotive volumes rebound with electric-drive component demand, while industrial machinery orders track global capital-equipment cycles. Medical implants maintain niche but high-margin revenues due to titanium alloy biocompatibility and regulatory hurdles that favor certified suppliers.

By Pattern Technology: 3D-Printed Patterns Disrupt Traditional Methods

Conventional wax patterns accounted for 86.47% revenue in 2025, sustained by mature tooling infrastructure and predictable dimensional control. Nonetheless, 3D-printed patterns scale at a 5.74% CAGR through 2031 as jet-binder technologies and photopolymer resins reach consistent burn-out performance. The investment casting market size for printed patterns is set to grow exponentially through 2031, reflecting adoption in aerospace prototyping, custom medical implants, and aftermarket turbine spares. Direct-shell printing bypasses wax entirely, creating intricate lattice cores for enhanced cooling efficiency. Hybrid production, where printed cores pair with wax over-molding, offers a transitional path for foundries.

Quality metrics continue to tighten: CT-scan inspection verifies wall thickness to ±50 µm, while real-time mold-fill simulations adjust gating prior to physical trials. Foundries integrating digital pattern workflows cut non-recurring engineering costs roughly 40%, an advantage that accelerates new-program nominations across the investment casting market.

By Component Weight: Mid-Range Components Drive Market Growth

Parts weighing 1-10 kg generated 51.94% revenue in 2025, aligning with turbine wheels, suspension arms, and compressor housings. This weight band balances complexity and yield, fitting most ceramic shell furnaces without special fixturing. Components under 1 kg are forecast to rise 5.31% CAGR, led by medical-device screws, dental abutments, and UAV turbine impellers requiring miniaturized channels. Conversely, parts above 10 kg address aircraft structural nodes and industrial pump casings, where investment casting’s near-net-shape efficiency delivers 15-30% material savings relative to forgings.

Process optimization now tailors shell thickness and slurry rheology to part mass, ensuring uniform dewaxing and minimizing hot tearing. Spinner discs used in glass-fibre manufacturing illustrate scale flexibility: PBS Velka Bites produces 9-30 kg discs that achieve 50% longer service life courtesy of refined grain structures. Weight-based segmentation underscores the versatility that keeps the investment casting market embedded across disparate industries.

Geography Analysis

Asia Pacific generated 43.97% of 2025 revenue in the investment casting market, topping global rankings as Chinese and Indian foundries scale aerospace-grade capacity. NADCAP-accredited lines running silica-sol shells supply turbine hot-section parts to global OEMs. Regional CAGR stands at 4.82% through 2031, buoyed by defence offsets, automotive electrification, and continued infrastructure build-outs. Research institutes in Japan and South Korea focus on additive-assisted pattern creation and super-alloy recycling, widening technological depth.

North America remains a technology stronghold and is projected to deliver the fastest regional CAGR at 5.36% through 2031, anchored by commercial-aviation clusters and Department of Defense procurement. The USD 1.2 trillion Infrastructure Investment and Jobs Act allocates USD 550 billion to metal-intensive projects, enabling order pipelines for valve bodies, rail couplers, and pump housings. Over 90% of surveyed foundries plan capital expenditures in grinding robotics, shell automation, and environmental controls, reinforcing competitiveness within the investment casting market.

Europe showcases leadership in emissions-control compliance and lightweight structural design. Georg Fischer invests 3% of annual revenue in R&D, pioneering high-silicon aluminum castings for battery-housing and hydrogen fuel-cell stacks. Foundries across Germany, France, and the United Kingdom adopt hybrid shell systems and AI-based defect prediction to satisfy demanding aerospace and energy customers. Regional operational costs remain elevated, yet value-added specialization sustains margin resilience. Collectively, the three core regions keep global supply balanced, mitigating single-point vulnerabilities in the investment casting market.

Competitive Landscape

Competitive intensity ranks moderate, with the top five players controlling a considerable share of global revenue. Precision Castparts Corp leads, reinforced by acquisitions such as Carlton Forge Works and Titanium Metals that extend from molten metal to finished assemblies. The company reported USD 9.3 billion revenue in 2023 and a 27.5% Q2 2024 earnings surge as engine deliveries ramp.[3]“FY 2024 Second-Quarter Earnings Release,” Precision Castparts Corp., pcc.com Winsert expanded cobalt-alloy capacity by acquiring Alloy Cast Products, securing a foothold in aerospace and power-generation wear components. Georg Fischer emphasizes R&D-led differentiation, channeling funds toward lightweight alloys and digital foundry systems.

Small and midsize firms survive by specializing in materials like TiAl or offering rapid prototype services paired with low-volume series production. Certifications—AS 9100, ISO 14001, NADCAP—form entry barriers, and clients increasingly award bundled contracts covering casting, finish machining, and heat treatment.

Environmental compliance costs and labour shortages challenge newcomers, nudging the investment casting market toward further consolidation. Nevertheless, niche innovators using printed shell technologies or recycled super-alloy feedstocks secure venture funding, maintaining a dynamic equilibrium between established giants and emerging specialists.

Investment Casting Industry Leaders

Precision Castparts Corp.

Alcoa Corporation

Impro Precision Industries

Signicast

Hitachi Metals Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2024: Versevo added 3D sand-printing technology for molds and cores, expanding rapid-prototyping capacity for complex geometries.

- September 2023: Zollem GmbH & Co. KG commissioned a new IGT/AERO investment casting line featuring DS/SX shelling equipment from VA Technology and seven-axis ABB robots.

Global Investment Casting Market Report Scope

Investment casting which is also considered as the precising and low wax casting. It ias the manufacturing process under which the wax is utilized to take the shape of disposable ceramic molds.

The Investment Casting Market is Segmented By Type (Sodium Silicate Process, Tetraethyl Orthosilicate/ Silica Sol Process), End-user Type (Automotive, Aerospace and Military, General Industrial Machinery, Medical, and Other End User Types), and Geography(North America, Europe, Asia-Pacific, and Rest of the World).

| Sodium-Silicate / Water Glass |

| Silica-Sol / Colloidal Silica |

| Hybrid & Other Processes |

| Carbon & Alloy Steel |

| Stainless Steel |

| Aluminum & Magnesium Alloys |

| Super-alloys (Ni, Co) |

| Others |

| Automotive |

| Aerospace & Defense |

| Industrial Machinery |

| Energy & Power |

| Medical & Dental |

| Others |

| Conventional Wax Patterns |

| 3D-Printed / Rapid Prototype Patterns |

| Up to 1 kg |

| 1–10 kg |

| Above 10 kg |

| North America | United States |

| Canada | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Spain | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East & Africa | Saudi Arabia |

| United Arab Emirates | |

| Egypt | |

| Turkey | |

| South Africa | |

| Rest of Middle East & Africa |

| By Process Type | Sodium-Silicate / Water Glass | |

| Silica-Sol / Colloidal Silica | ||

| Hybrid & Other Processes | ||

| By Material | Carbon & Alloy Steel | |

| Stainless Steel | ||

| Aluminum & Magnesium Alloys | ||

| Super-alloys (Ni, Co) | ||

| Others | ||

| By End-User | Automotive | |

| Aerospace & Defense | ||

| Industrial Machinery | ||

| Energy & Power | ||

| Medical & Dental | ||

| Others | ||

| By Pattern Technology | Conventional Wax Patterns | |

| 3D-Printed / Rapid Prototype Patterns | ||

| By Component Weight | Up to 1 kg | |

| 1–10 kg | ||

| Above 10 kg | ||

| By Geography | North America | United States |

| Canada | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | Saudi Arabia | |

| United Arab Emirates | ||

| Egypt | ||

| Turkey | ||

| South Africa | ||

| Rest of Middle East & Africa | ||

Key Questions Answered in the Report

What is the current size of the investment casting market?

The investment casting market is valued at USD 18.45 billion in 2026 and is forecast to reach USD 23.82 billion by 2031.

How fast is the investment casting market expected to grow?

The market is projected to expand at a 5.25% compound annual growth rate (CAGR) between 2026 and 2031.

Which region holds the largest share of the investment casting market?

Asia Pacific leads with 43.97% of global revenue in 2025, supported by aerospace expansion in China and defense procurement programs in India.

Which end-user sector drives the most demand for investment castings?

Aerospace and defense applications account for 36.07% of 2025 revenue thanks to fleet-renewal programs and defense modernization projects.

What process type dominates the market, and why?

Silica-sol investment casting commands 50.78% market share because it delivers the tight surface finish and dimensional accuracy required for turbine blades and medical implants.

How are new technologies such as 3D-printed patterns impacting the market?

3D-printed patterns reduce tooling costs and shorten lead times, supporting a 5.74% CAGR for this segment as foundries adopt rapid-prototype workflows for complex, low-volume parts.

Page last updated on: