Emission Monitoring Systems Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

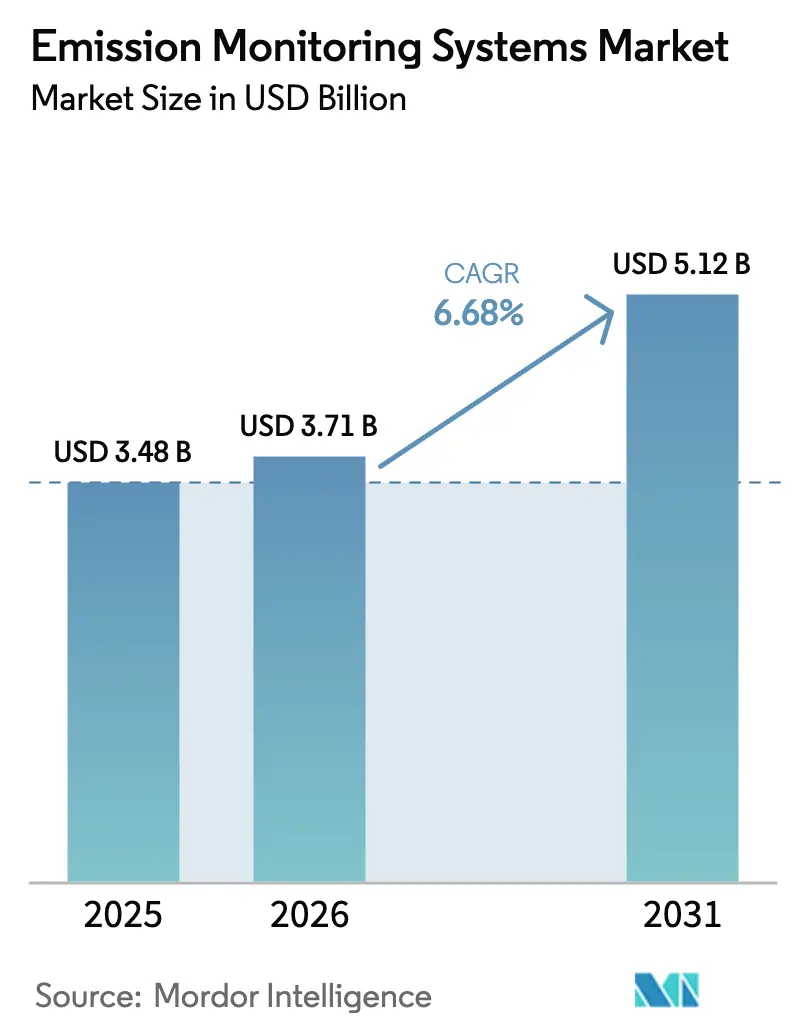

| Market Size (2026) | USD 3.71 Billion |

| Market Size (2031) | USD 5.12 Billion |

| Growth Rate (2026 - 2031) | 6.68% CAGR |

| Fastest Growing Market | Middle East |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Emission Monitoring Systems Market Analysis by Mordor Intelligence

The Emission Monitoring Systems Market size is projected to be USD 3.48 billion in 2025, USD 3.71 billion in 2026, and reach USD 5.12 billion by 2031, growing at a CAGR of 6.68% from 2026 to 2031. Carbon-pricing mandates in Europe, tax-credit verification in the United States, and ship-board rules under the International Maritime Organization (IMO) anchor demand, while cost-saving predictive models and cloud analytics reshape vendor strategies. Utilities and refiners treat high-accuracy stack data as a financial control point because a 1% measurement error can swing European Union Emissions Trading System (EU-ETS) allowance costs by millions of dollars per site. Asia Pacific remains the revenue leader thanks to India’s National Clean Air Programme retrofits and Southeast Asian waste-to-energy expansions, yet the Middle East delivers the fastest growth as refinery modernization accelerates ahead of potential carbon border adjustments. Hybrid continuous-predictive architectures, in-situ laser sensors, and cloud-hosted diagnostics cut total cost of ownership, but technician shortages and tropical humidity bias threaten timely commissioning and accurate reporting.

Key Report Takeaways

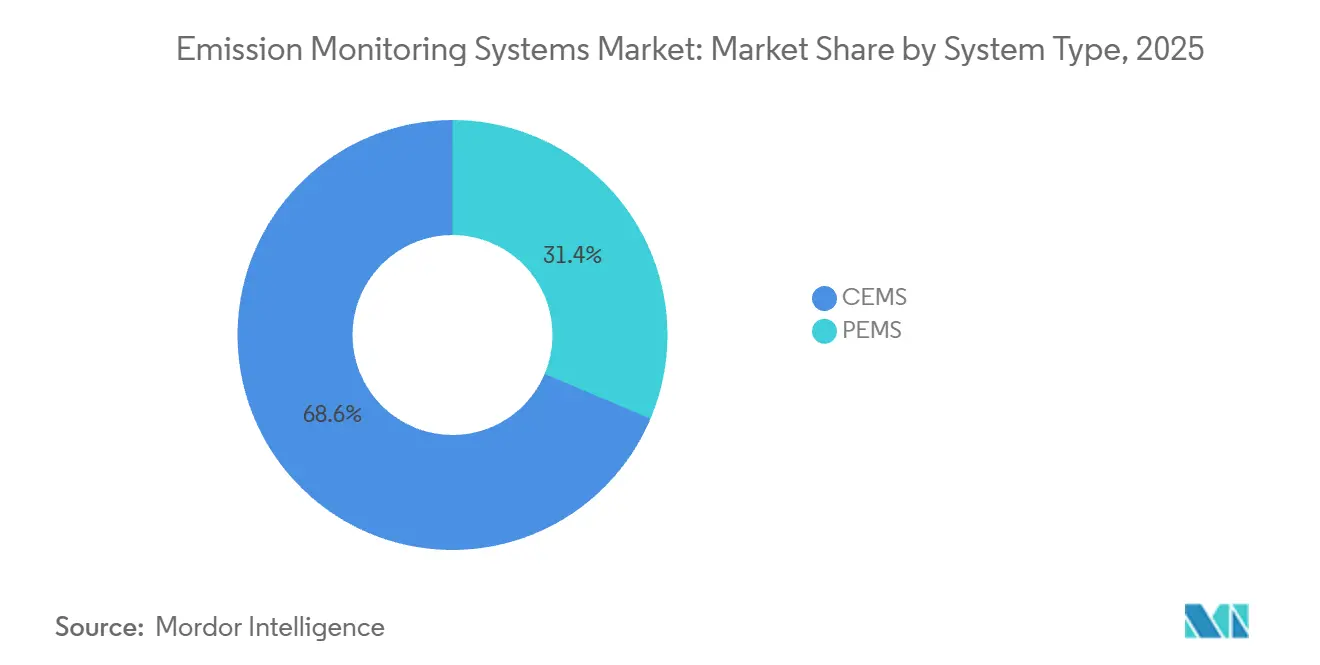

- By system type, continuous solutions led with 68.64% revenue share in 2025, while predictive models are on track for a 7.87% CAGR through 2031.

- By component, hardware represented 44.16% of 2025 spend, yet software is forecast to expand at an 8.27% CAGR to 2031.

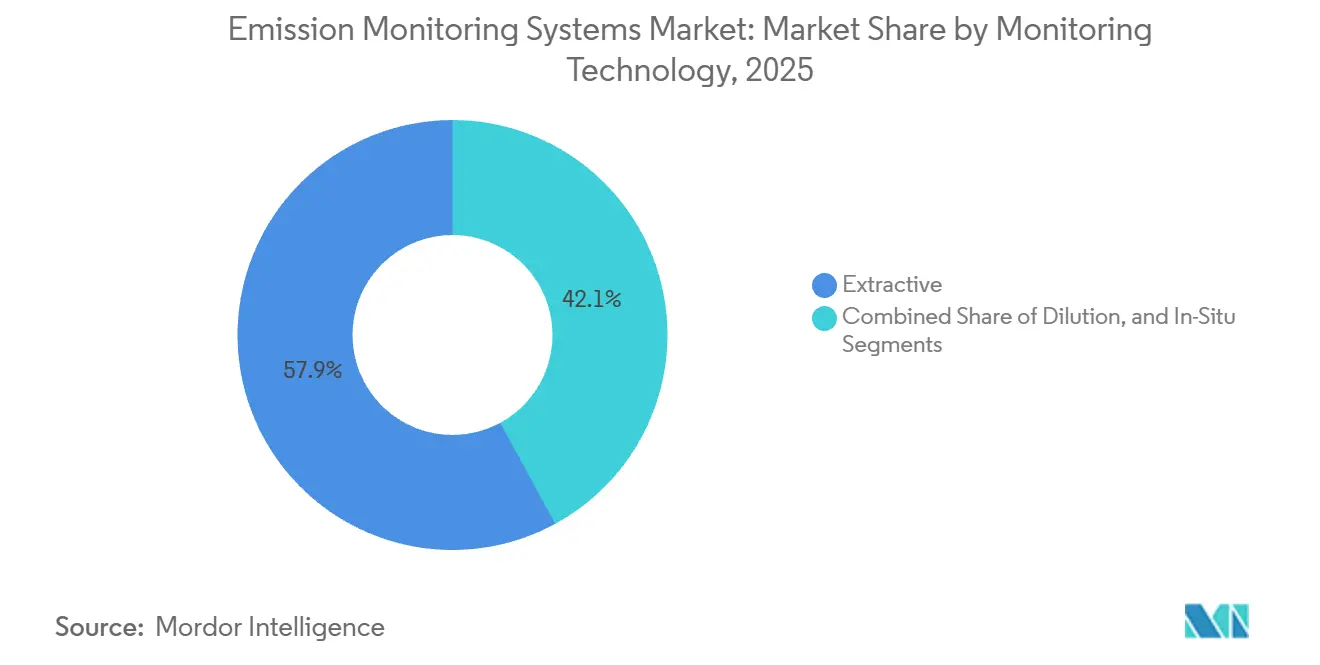

- By monitoring technology, extractive methods captured 57.93% of the emission monitoring systems market share in 2025, whereas in-situ tunable diode laser spectroscopy is projected to grow 8.19% annually to 2031.

- By end-user, power generation held 33.48% of the emission monitoring systems market size in 2025, but waste-to-energy facilities will post the quickest 9.19% CAGR to 2031.

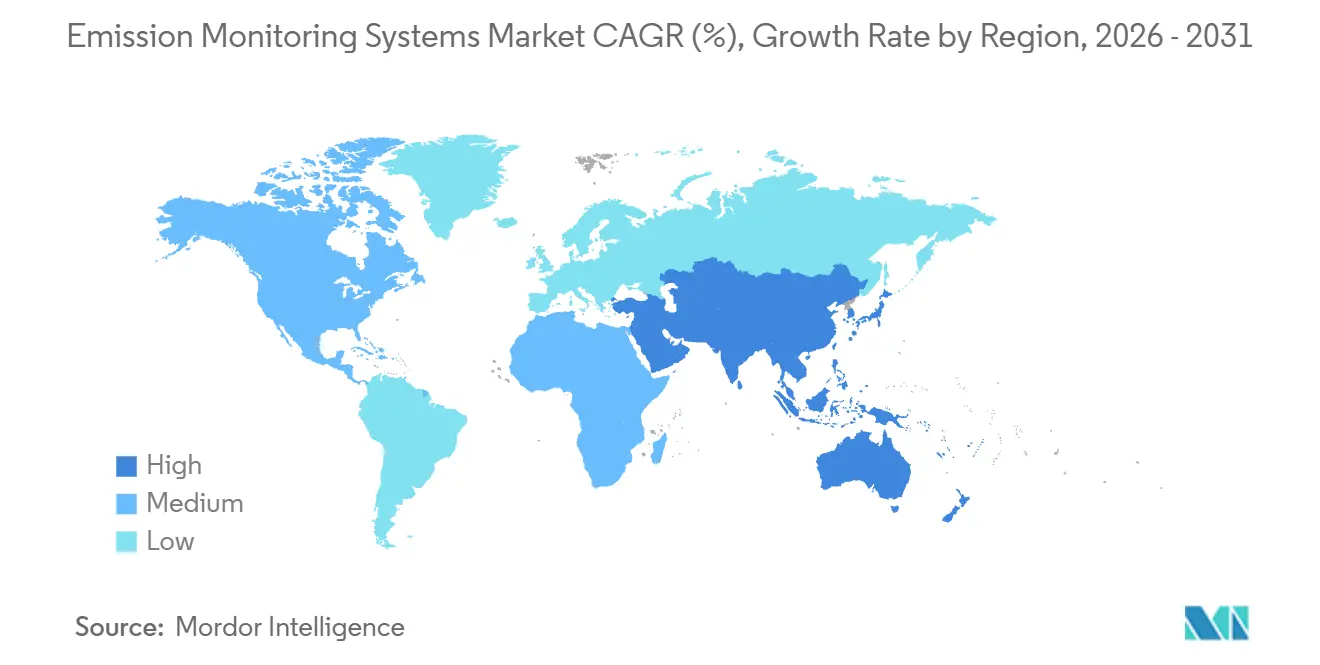

- By geography, Asia Pacific led with a 36.17% revenue share in 2025, while the Middle East is set to post the highest 8.19% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Emission Monitoring Systems Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Transition from CAPEX-heavy CEMS to hybrid CEMS-PEMS architectures in Europe | +1.2% | Europe, with early adoption in Germany, Netherlands, United Kingdom | Medium term (2-4 years) |

| Mandatory EU-ETS Phase IV carbon pricing driving stack-level monitoring, Europe | +1.5% | Europe, concentrated in Germany, Poland, Spain, Italy | Short term (≤ 2 years) |

| Inflation Reduction Act tax-credit verification creating surge in United States power-plant CEMS retrofits | +1.3% | United States, with concentration in Texas, Pennsylvania, West Virginia coal and gas regions | Short term (≤ 2 years) |

| In-situ laser-based sensors cutting lifecycle cost by 30% in Asia Pacific waste-to-energy plants | +1.1% | Asia Pacific core (China, India, Southeast Asia), spill-over to Middle East | Medium term (2-4 years) |

| National Clean Air Programme accelerating coal-fired CEMS roll-outs, India | +0.9% | India, with early gains in Delhi NCR, Maharashtra, Gujarat thermal clusters | Short term (≤ 2 years) |

| IMO 2023 EEXI and CII rules triggering ship-board SEMS installations, global maritime | +0.7% | Global, with highest uptake in European, Asian, and North American shipping lanes | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Transition From CAPEX-Heavy CEMS to Hybrid CEMS-PEMS Architectures in Europe

European operators overlay predictive emission monitoring models on existing continuous analyzers to curb capital spending, cut installation from 12 weeks to 4 weeks, and accelerate compliance reporting. Germany’s Federal Immission Control Act endorses predictive methods for low-emission units once quarterly crosschecks confirm model accuracy within ±10%. The Netherlands and United Kingdom grant similar flexibility for refinery flares, trimming hardware budgets 40%-50% for ancillary stacks. Utilities with mature data-science teams exploit process variables such as fuel flow, excess oxygen, and flame temperature to calculate nitrogen oxides and sulfur dioxide in real time, reducing unscheduled downtime for analyzer maintenance. Smaller plants struggle to maintain the statistical models, prompting a services opportunity for vendors that bundle software, calibration gases, and regulatory reporting. The hybrid path also supports faster technology refresh cycles because model coefficients update in software rather than through hardware swaps.

Mandatory EU-ETS Phase IV Carbon Pricing Driving Stack-Level Monitoring

EU-ETS Phase IV tightened the cap reduction factor to 4.3% in 2024, pushing spot prices to EUR 80-EUR 100 per metric ton (USD 90-USD 113) during 2025.[1]European Commission, “EU ETS Phase IV,” ec.europa.eu A 500 MW coal plant emitting 3 million tCO₂ per year faces EUR 240 million (USD 272 million) in annual allowance costs, so a ±2% measurement margin mandated by EN 14181 directly influences cash flow. Operators retrofit heated extractive lines, redundant analyzers, and automated drift diagnostics to meet the precision threshold. Poland and Spain alone represented 38% of new orders in 2025 as facilities rushed to secure monitoring-plan approvals before the 2026 deadline. Vendors with full EN 15267 certification libraries command premium pricing, although regional utilities increasingly demand remote calibration to overcome technician shortages.

Inflation Reduction Act Verification Creating United States Retrofit Surge

The 2022 Inflation Reduction Act grants up to USD 85 per metric ton for captured carbon dioxide, contingent on continuous baseline monitoring under 40 CFR Part 75. More than 200 gas and coal units in Texas, Pennsylvania, and West Virginia ordered analyzers in 2025 to qualify for transferable tax credits that can cut project payback to under 12 months. A single 400 MW combined-cycle plant capturing 500,000 tCO₂ yearly secures USD 42.5 million in credits against a USD 3 million monitoring package, making instrumentation a negligible cost of capital. Demand spikes have strained calibration-gas suppliers and lengthened third-party relative accuracy test audit queues into late 2026, underscoring the need for additional certified service capacity.

In-Situ Laser Sensors Cutting Lifecycle Cost by 30% in Asia Pacific Waste-to-Energy Plants

Tunable diode laser spectroscopy transmits a beam across the stack, eliminating pumps, filters, and drying systems. Jakarta’s 50 MW Sunter waste-to-energy plant cut 10-year ownership cost 32% after switching from cold-dry extractive units in 2024. Maintenance intervals lengthened from weekly to quarterly, and sensor life doubled to a decade. China’s 14th Five-Year Plan demands continuous monitoring at every facility processing more than 300 t/day of municipal waste, and provincial bureaus in Guangdong, Zhejiang, and Jiangsu pre-approved in-situ lasers to streamline permits. Southeast Asian plants in Thailand and Vietnam replicate this model to avoid humidity-related drift that plagues extractive hardware, tilting regional specifications toward in-situ technology.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Scarcity of TÜV and MCERTS-certified technicians delaying European commissioning | -0.8% | Europe, acute in Germany, Poland, Spain, Italy | Short term (≤ 2 years) |

| High humidity bias in tropical regions raising false-compliance risk | -0.6% | Southeast Asia, India, Middle East coastal zones, Sub-Saharan Africa | Medium term (2-4 years) |

| Legacy DCS-DAQ inter-operability gaps inflating retrofit costs in United States utilities | -0.5% | United States, concentrated in coal-heavy Midwest and Appalachian regions | Medium term (2-4 years) |

| Capital lock-in from long-term CEMS leasing models hindering PEMS adoption, Middle East | -0.4% | Middle East, particularly Saudi Arabia, UAE, Qatar refining and petrochemical sectors | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Scarcity of TUV and MCERTS-Certified Technicians Delaying European Commissioning

Field certification under EN 15267 requires accredited engineers to perform multi-point calibration, linearity checks, and relative accuracy testing. TUV SUD logged a 40% rise in requests during 2025 yet expanded its engineer roster only 12%, lifting average wait times from 8 weeks to 18 weeks in Germany, Poland, and Spain. Smaller operators defer upgrades or accept provisional permits that rely on manual stack tests, eroding real-time visibility for regulators. The shortage sparks price inflation for certification services and encourages larger utilities to self-fund technician training programs, but accreditation lead times restrain quick fixes.

High Humidity Bias Raising False-Compliance Risk in Tropical Regions

Extractive systems draw gas through sample lines where condensation forms if temperature drops below the dew point, distorting infrared and ultraviolet absorption. A 2024 field study showed 8%-15% sulfur dioxide over-reporting at Indonesian coal plants during monsoon months, inflating limestone consumption for flue-gas desulfurization.[2]Asian Development Bank, “Southeast Asia Energy Outlook 2024,” adb.org Conversely, moisture can suppress nitrogen oxide readings, risking non-detected exceedances and potential fines during quarterly audits. Heated sample lines or in-situ lasers solve the bias but add USD 50,000-USD 150,000 per stack, a hurdle for independent power producers with thin margins. Regulators across Southeast Asia now mandate humidity-compensated designs in new tenders, signaling tighter enforcement.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By System Type: Predictive Models Gain Ground Despite CEMS Dominance

Continuous solutions retained a 68.64% share in 2025, anchored by decades of codified requirements under EU-ETS, the United States Clean Air Act, and China’s ultra-low emission rules. Predictive models will register a 7.87% annual advance, capturing interest from operators keen to avoid analyzer duplication on ancillary stacks. The emission monitoring systems market size for predictive models is forecast to exceed USD 1.2 billion by 2031, reflecting their role in digitally mature utilities. Early adopters in Germany and the United States exploit real-time process variables to simulate nitrogen oxides within ±10% of extractive readings, satisfying regulators while shaving hardware budgets by nearly half. Middle Eastern refineries remain cautious because long-term leases signed a decade ago lock them into fixed continuous contracts until 2028-2030, but hybrid pilots on flare systems are underway with regulatory oversight from Saudi Arabia’s National Environment Strategy.[3]Saudi Ministry of Environment, Water and Agriculture, “National Environment Strategy 2024,” mewa.gov.sa

In North America, combined-cycle gas turbines use predictive algorithms during cycling operation to avoid downtime when extractive analyzers require maintenance. Asia Pacific utilities adopt a split strategy, retaining continuous analyzers on primary boilers and deploying predictive models on secondary units to align with China’s digital-twin policy for coal plants. Cloud vendors that combine neural-network modeling with enterprise carbon accounting gain traction because they simplify quarterly regulatory reporting. As more jurisdictions recognize predictive techniques, the emission monitoring systems market will likely see regulatory language shift from prescriptive hardware mandates to performance-based accuracy thresholds.

By Component: Cloud-Hosted Software Outpaces Hardware as Data Integration Deepens

Hardware accounted for 44.16% of 2025 spending, reflecting a mature installed base of gas analyzers, flow meters, and data acquisition units. Software will grow 8.27% each year through 2031 as operators integrate real-time stack data with enterprise resource planning and environmental, social, and governance dashboards. A 15-plant European utility consolidated data from 60 stacks into a cloud portal in 2025, trimming calibration labor 25% by automating drift alerts. Cloud platforms also underpin predictive maintenance, notifying technicians before sensor fouling degrades accuracy, thereby protecting compliance margins.

Services (installation, calibration, third-party certification, and multi-year maintenance) capture the balance of revenue and ride the cumulative installed base. Vendors tie software subscriptions to service agreements, offsetting hardware commoditization. Gas analyzers remain the revenue cornerstone, especially nondispersive infrared CO₂ cells and chemiluminescence nitrogen oxide detectors, yet open-protocol data acquisition hardware grows fastest as operators demand OPC UA and Ethernet to avoid vendor lock-in. As software penetration rises, the emission monitoring systems industry pivots toward recurring revenue models built on analytics rather than box sales.

By Monitoring Technology: In-Situ TDLS Gains Share in High-Moisture Applications

Extractive methods dominated 57.93% of deployments in 2025, especially at coal plants where EN 14181 specifies continuous extractive measurement for CO₂, SO₂, and NOₓ. The emission monitoring systems market anticipates an 8.19% CAGR for in-situ tunable diode laser spectroscopy through 2031 because it sidesteps sample conditioning and slashes maintenance hours by up to 70%. Southeast Asian waste-to-energy plants, operating in humid, particulate-rich gas streams, increasingly select laser sensors to avoid frequent filter clogging and moisture drift.

Dilution sampling occupies a niche on marine vessels where space constraints limit heater enclosures, but sensitivity trade-offs hinder adoption on stationary sources. Hot-wet extractive systems still appeal to high-sulfur processes, albeit at higher auxiliary power cost, while cold-dry variants save energy yet demand strict moisture correction in tropical climates. Regulatory endorsements such as China’s pre-approval of in-situ lasers for municipal waste plants and India’s ongoing evaluation for biomass co-firing indicate the technique’s mainstreaming by 2027. The emission monitoring systems market size linked to laser-based hardware could surpass USD 900 million by 2031 if certification bottlenecks ease.

By End-User Industry: Waste-to-Energy Leads Growth as Municipal Mandates Tighten

Power generation held 33.48% of 2025 demand, reflecting legacy coal fleets and modern gas turbines that already rely on extractive analyzers under strict air rules. Waste-to-energy, however, will record a 9.19% CAGR as municipal landfill-diversion targets force continuous monitoring at thousands of incinerators worldwide. The emission monitoring systems market share for waste-to-energy applications could reach 18% by 2031 as the European Union mandates diversion of 65% of municipal waste from landfills by 2035. China added 12 GW of waste-to-energy capacity in 2024 and requires continuous monitoring on every line exceeding 300 t/day throughput, leading to roughly 1,200 new systems annually.

Oil and gas remains significant, driven by flare monitoring on offshore platforms and refinery heaters, while cement, steel, and chemicals adopt multi-gas analyzers to meet both air-pollution and carbon-trading requirements. Pharmaceutical plants, though lower emitters, demand ultra-low detection limits for volatile organic compounds, spurring high-precision flame ionization detectors. Maritime retrofits accelerate as 15,000 vessels above 5,000 gross tonnage must comply with IMO EEXI and CII rules by 2027, adding ship-board analyzers and satellite telemetry to the overall emission monitoring systems market.

Geography Analysis

Asia Pacific retained 36.17% of revenue in 2025, anchored by China’s coal capacity, India’s National Clean Air Programme rollouts, and Southeast Asian waste-to-energy projects. The region’s policy mix of ultra-low emission standards and municipal-solid-waste directives sustains hardware replacement and software upgrades, while local fabricators in China and South Korea intensify price pressure on Western suppliers. The emission monitoring systems market size in Asia Pacific is forecast to climb steadily as in-situ laser uptake offsets extractive saturation.

The Middle East emerges as the fastest-growing region at an 8.19% CAGR through 2031. Saudi Arabia’s National Environment Strategy mandates continuous monitoring for thermal inputs above 50 MW by 2027, compelling refineries, desalination plants, and gas-fired power stations to install analyzers on stacks that previously relied on annual tests. The United Arab Emirates enacted Federal Decree-Law 24-2022, giving industrial operators three years to adopt best available techniques, including continuous monitoring. Refinery upgrades and petrochemical debottlenecking drive bundled analyzer-plus-service contracts that elevate regional spend.

Europe remains large and compliance-driven, with Germany, Poland, Spain, and Italy accounting for most installations. Tightened EU-ETS rules and Industrial Emissions Directive standards encourage analyzer replacements that deliver ±2% accuracy. North America sees retrofit momentum as United States tax credits reward verified emission cuts, and Canada’s Output-Based Pricing System expands to more provinces. South America adds selective demand in Brazil, Argentina, and Mexico as state-level air agencies adopt continuous monitoring, while Africa concentrates activity in South Africa, Nigeria, and Egypt where multinational plants align with export-market environmental norms. Collectively, these dynamics ensure global diversity in the emission monitoring systems market.

Mordor Intelligence provides coverage of the emission monitoring systems market across other key regional markets, including North America, each with their regulatory frameworks and demand patterns.

Regulatory Landscape

Emission monitoring system demand is anchored by tighter, more digitized compliance regimes across major jurisdictions. In the European Union, the revised Industrial Emissions Directive (IED 2.0) entered into force in August 2024, and Regulation (EU) 2024/1244 established reporting of environmental data from industrial installations through an Industrial Emissions Portal. This shifts compliance toward standardized electronic reporting and installation-level data traceability, with the Commission setting a January 2026 deadline to draw up the first set of reporting guidelines under the regulation.

In the United States, US EPA rulemaking and reporting standardization continue to reinforce CEMS as the default compliance tool for regulated units. During 2026, the EPA issued amendments and technical guidance that affect how facilities demonstrate compliance and submit performance data, including March 2026 reporting instructions for 2026Q1 under the Mercury and Air Toxics Standards (MATS) data submission module and January 2026 amendments confirming that NOx CEMS installed and certified under 40 CFR Part 75 are acceptable for monitoring NOx emissions from stationary combustion turbines. April 2026 technical amendments to NSPS/Emission Guidelines for the crude oil and natural gas source category also updated discrete continuous monitoring provisions, including vent gas net heating value monitoring.

Value Chain Analysis

The value chain spans core measurement components, system integration, and compliance services. Upstream suppliers provide gas analyzers and photonics modules (NDIR, chemiluminescence, UV, TDLS), sampling and conditioning hardware for extractive systems, flow and opacity monitors, and data acquisition systems (DAS) with plant-network interfaces (for example, OPC UA/Ethernet) that connect stack data to plant historians and compliance reporting tools. Midstream integrators and OEMs assemble certified CEMS/PEMS packages, engineer installation and tie-ins to DCS/DAQ environments, and validate performance to jurisdictional standards, including EN 14181/EN 15267 workflows in Europe and Part 75-aligned configurations in the United States.

Downstream value is increasingly captured in services and software that keep systems audit-ready, including commissioning, calibration gases and routines, relative accuracy testing with accredited technicians, and managed reporting that aligns with regulator portals and templates. The compliance push toward electronic reporting reinforces recurring activities such as data validation, QA/QC documentation, and performance test submittals. With 2026 updates to US EPA reporting instructions for CEMS performance evaluations and the EU move toward Industrial Emissions Portal reporting for the 2026 reporting year, integrator-led data formatting, cybersecurity hardening, and remote diagnostics are drawing more attention, especially as certified technician availability remains constrained.

Competitive Landscape

The market shows moderate concentration. Five global conglomerates ABB, Siemens, Emerson, Thermo Fisher Scientific, and AMETEK held roughly 45% of 2025 revenue, leveraging wide product portfolios, multi-jurisdictional certifications, and service annuities from long-lived installations. Niche players such as HORIBA, SICK, Teledyne, ENVEA, and Opsis secure share in high-precision or niche segments, including pharmaceuticals, semiconductors, and marine applications, where detection limits and response times exceed general-purpose specifications. New entrants from data science and photonics concentrate on predictive software and in-situ lasers, respectively, eroding incumbent hold on emerging growth niches.

Strategic moves emphasize vertical integration and digital-service bundling. Emerson invested in predictive-model software in 2024 to complement its DeltaV control system, aiming to serve cost-sensitive Eastern European utilities through hybrid architectures. Siemens embeds analyzer interfaces into SIMATIC control platforms to automate EU-ETS reporting, enhancing stickiness for heavy industries. ENVEA and Opsis undercut extractive incumbents by offering modular in-situ laser systems priced 20%-30% lower, resonating with municipal utilities. Certification remains a moat; ISO 12039, EN 15267, and United States Performance Specification standards require costly tests that favor firms with in-house labs.[4] International Organization for Standardization, “ISO 12039:2019,” iso.org

Geographic expansion also shapes competition. HORIBA opened a Jakarta service hub in 2025 to support Southeast Asian customers, cutting turnaround time from four weeks to one. Teledyne introduced an IMO-certified ship-board analyzer with satellite telemetry, capturing early maritime retrofits. ABB secured a USD 52 million refinery order in the Middle East to retrofit 18 heaters and flares, signaling oil and gas modernization momentum. Vendors that pair hardware with cloud analytics and certified services position to capture recurring revenue as the emission monitoring systems market pivots toward outcome-based contracts.

Emission Monitoring Systems Industry Leaders

ABB Ltd.

Siemens AG

Emerson Electric Co.

General Electric Company

AMETEK Inc.

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Replacement and retrofit cycles are a key opportunity, driven by stricter low-range measurement needs and digital reporting requirements. EU IED 2.0 enforcement and the move toward standardized electronic reporting via the Industrial Emissions Portal under Regulation (EU) 2024/1244 create whitespace for vendors that pair low-range analyzers with automated QA/QC, audit trails, and reporting templates aligned to installation-level permits and portal data fields. ABB’s product activity points to the direction of competition, with ABB launching the ACF5000 LCS in May 2026 as a low-range CEMS aligned to tighter European requirements for upgrades where legacy systems struggle with single-digit ppm measurement and drift control.

A second opportunity centers on hybrid architectures that combine installed CEMS with predictive models and ongoing services to reduce total compliance cost while maintaining verification rigor. Yokogawa signed a global agency agreement with CMC Solutions in February 2026 to market and service predictive emission monitoring systems (PEMS) for industrial customers, reflecting channel expansion around software-led monitoring and managed lifecycle support. Adjacent compliance investments in power and industrial upgrades also pull monitoring into bundled projects, as seen in Fuel Techs April 2026 awards of approximately USD 10 million that included SCR integration for municipal utility gas turbines, where emissions monitoring and reporting are typically engineered alongside control upgrades to demonstrate performance and sustain permit compliance.

Recent Industry Developments

- June 2026: Siemens Energy agreed to acquire Camlin Group, adding grid monitoring and asset digitalization capabilities that strengthen its broader monitoring and analytics footprint around energy infrastructure. The agreement supports tighter integration of operational data and diagnostics that large industrial customers increasingly link to emissions compliance reporting and reliability targets.

- May 2026: ABB launched the ACF5000 LCS, a low-range continuous emission monitoring system designed for tighter industrial emissions compliance use cases. The launch targets retrofit and new-build projects that require improved low-concentration measurement performance and streamlined reporting workflows under evolving European requirements.

- October 2025: AMETEK acquired a United States predictive-emission software firm for USD 120 million and integrated the capability into its Process Instruments division. The acquisition expands AMETEK's ability to sell hybrid CEMS-PEMS packages and capture recurring revenue from cloud analytics, model maintenance, and compliance reporting services.

Research Methodology Framework and Report Scope

Market Definition and Coverage

The market is defined as revenues from fixed-site emission monitoring systems used at industrial point sources to measure and report stack emissions for regulatory compliance. It includes continuous and predictive monitoring setups, along with the related hardware, software, and support services needed to keep systems operating.

Scope exclusions: Portable handheld emission testers and satellite-based ambient sensing are excluded from this market sizing.

Segmentation Overview

- By System Type

- Continuous Emission Monitoring Systems (CEMS)

- Predictive Emission Monitoring Systems (PEMS)

- By Component

- Hardware

- Gas Analyzers

- Flow and Opacity Monitors

- Data Acquisition Systems (DAS)

- Software

- Stand-Alone

- Cloud-Hosted

- Services

- Installation and Deployment

- Calibration and Certification

- Support and Maintenance

- Hardware

- By Monitoring Technology

- Extractive

- Hot-Wet

- Cold-Dry

- Dilution

- In-Situ

- Tunable Diode Laser Spectroscopy (TDLS)

- Extractive

- By End-User Industry

- Power Generation

- Coal-Fired

- Combined-Cycle Gas Turbines

- Oil and Gas

- Upstream

- Midstream

- Downstream and Refineries

- Metals and Mining

- Chemicals and Petrochemicals

- Pharmaceuticals

- Cement and Aggregates

- Pulp and Paper

- Waste-to-Energy and Incineration

- Maritime (Ship-Board)

- Power Generation

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- United Kingdom

- Germany

- France

- Italy

- Spain

- Russia

- Rest of Europe

- Asia Pacific

- China

- India

- Japan

- South Korea

- Australia

- Southeast Asia

- Rest of Asia Pacific

- Middle East

- United Arab Emirates

- Saudi Arabia

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Nigeria

- Egypt

- Rest of Africa

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk work starts with building the compliance and demand picture for stationary sources that typically require monitoring, then mapping what is usually installed at sites like boilers, kilns, furnaces, reactors, and flares. We used public references such as US EPA air programs and compliance guidance, the European Environment Agency and EU industrial emissions resources, United Nations and World Bank industrial activity indicators, and trade data sources such as UN Comtrade for relevant equipment flows.

To keep the model grounded in real supply and pricing signals, we also reviewed annual reports, investor presentations, and product documentation from system and component suppliers, plus technical papers and standards where they are publicly accessible. Select paid subscriptions were used only for company financials and intelligence, news and financials tracking, and patent databases to confirm product focus and update timing. These examples are not exhaustive, and other public sources were also reviewed to support data collection, validation, and clarification.

Primary Interviews and Surveys

Primary work focused on speaking with people who buy, specify, install, and maintain emission monitoring systems across major regions, and then pressure-testing the desk assumptions that could move market totals. We covered a mix of equipment suppliers, service providers, EPC and integration participants, and end-user compliance teams to validate adoption timing, typical system configurations, and how service revenues attach after installation.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 28% | CXOs: 13% | APAC: 37% |

| Mid tier: 52% | Functional/Unit leaders: 36% | EMEA: 36% |

| Smaller Players: 20% | Managers: 51% | Americas: 27% |

Market-Sizing & Forecasting

Sizing is built using a top-down approach where emissions compliance intensity and industrial activity are used to reconstruct the addressable installed base of monitored point sources by region, then translated into annual spending. The model is cross-checked using selective bottom-up approximations, such as sampled system pricing by configuration, channel checks on typical service bundles, and supplier revenue splits where disclosures allow.

Key inputs used in the model include the mix of CEMS versus PEMS deployments, replacement and calibration cycles, the share of regulated facilities by industry, typical pollutant parameter coverage (for example SO2, NOx, CO, CO2, O2, flow, and opacity), and the attachment rate of software and ongoing services to each installed system. Where site counts or replacement timing are uncertain, gaps are handled through ranges agreed with interview feedback, then narrowed by checking against import patterns and supplier commentary on backlog and compliance-driven demand.

For forecasting, scenario analysis is used, with a base case anchored to expected enforcement strength and industrial output by region, then adjusted using expert views on capex timing and service renewal behavior. Assumptions such as ASP progression and service mix are updated when multiple interviewees indicate sustained pricing pressure or a shift toward software-led monitoring and reporting.

Data Validation & Update Cycle

Validation is done through triangulation checks that compare the modeled totals against independent signals, such as regulated facility counts, technology mix trends, and supplier-reported business momentum. Outliers are investigated, and if a large variance appears in a region or end-use, follow-up outreach is triggered to recheck the input assumption that likely caused the swing.

Before sign-off, the full model goes through multi-step internal review where calculations, unit consistency, and currency conversion timing are verified, followed by a final reasonableness pass against recent market events. Reports are refreshed annually, and interim updates are made when material regulation changes, major industrial disruptions, or visible price moves are observed. Right before delivery, we do a last update sweep so clients receive the latest view that matches the current information set.

Mordor Intelligence's Emission Monitoring Systems Market Sizing Compared With Other Published Estimates

Published market sizes for emission monitoring systems can look far apart, even when the topic name is similar, because each study makes its own calls on what to include, which year is treated as the base, and how quickly pricing and adoption are assumed to change. Differences also show up when one estimate blends adjacent monitoring categories or counts non-stationary use cases that are not tied to regulated point sources.

The main gap comes from whether portable testers and broader ambient sensing are counted. Mordor Intelligence treats the market as fixed-site CEMS and PEMS spending tied to stack compliance, with handheld and satellite sensing excluded from the revenue pool. Other gaps often come from how service revenues are attached, whether software is counted as part of the system value, and how currency conversion timing and ASP updates are handled across regions.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 3.48 B (2025) | |

| Global Consultancy A | USD 3.50 B (2023) | Uses an earlier base year and may treat a wider set of monitoring and reporting capabilities as in-scope, which can shift totals when software and remote monitoring value is counted differently across regions. |

| Industry Publisher B | USD 6.70 B (2024) | Appears to apply a broader definition of emission monitoring as an equipment and sensor network, which can pull in adjacent categories and inflate the spend pool versus a strict fixed-site stack compliance scope. |

The spread across the three figures is mostly explained by scope and timing choices rather than arithmetic errors. When the market is kept tied to regulated stationary sources, and when system value is separated cleanly from nearby monitoring categories, the resulting size is easier to trace back to clear demand drivers and to update in a repeatable way.

Key Questions Answered in the Report

How large is the emission monitoring systems market in 2026?

The market stands at USD 3.71 billion in 2026 and is projected to reach USD 5.12 billion by 2031.

Which region grows fastest through 2031?

The Middle East posts the quickest 8.19% CAGR, driven by refinery and petrochemical modernization mandates.

What technology segment is expanding most rapidly?

In-situ tunable diode laser spectroscopy is advancing at about 8.19% a year due to lower lifecycle cost in high-moisture environments.

Why are predictive emission monitoring systems gaining traction?

They reduce hardware capital by up to 50%, cut installation time from 12 weeks to 4 weeks, and now meet accuracy thresholds under evolving regulations.

What is the biggest restraint facing new installations in Europe?

A shortage of TÜV and MCERTS-certified technicians has doubled commissioning lead times to roughly 18 weeks.

Page last updated on: