Americas Microcontroller (MCU) Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

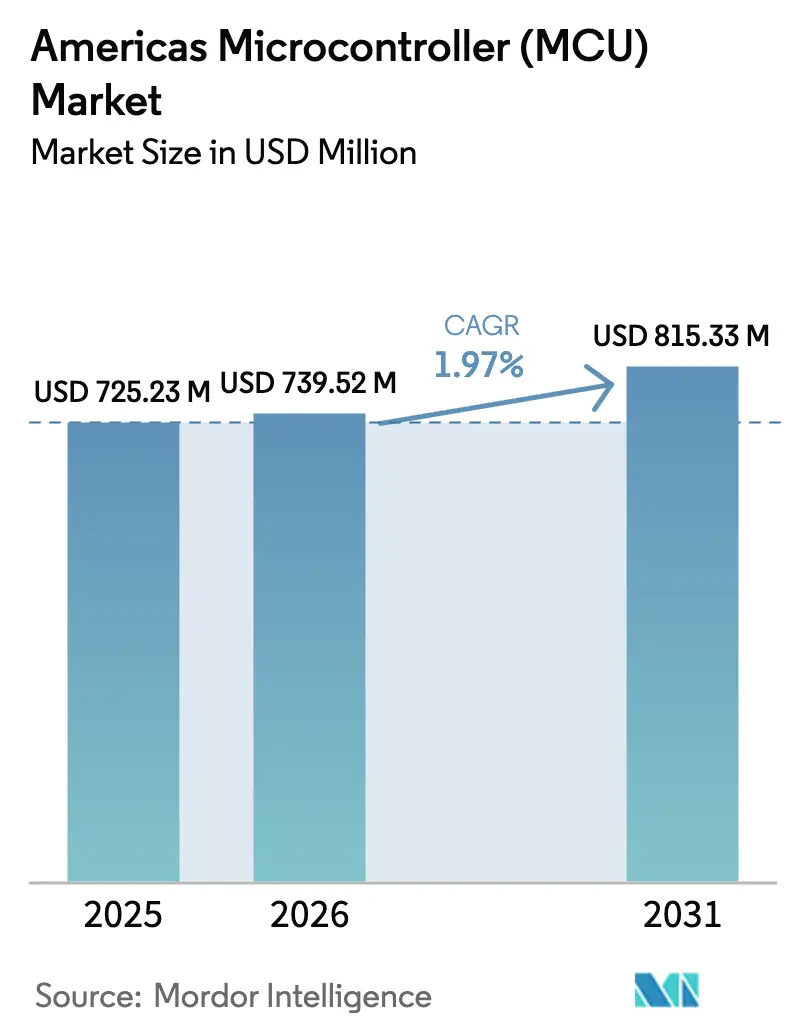

| Base Year Market Size (2025) | USD 725.23 Million |

| Market Size (2026) | USD 739.52 Million |

| Market Size (2031) | USD 815.33 Million |

| Growth Rate (2026 - 2031) | 1.97% CAGR |

| Market Concentration | Medium |

Major Players_Market.webp) *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Americas Microcontroller (MCU) Market Analysis by Mordor Intelligence

The Americas microcontroller market size is expected to grow from USD 725.23 million in 2025 to USD 739.52 million in 2026 and is forecast to reach USD 815.33 million by 2031 at 1.97% CAGR over 2026-2031. The measured growth reflects a transition from post-pandemic recovery to steady demand as automotive electrification mandates and IoT edge deployments multiply across factories, vehicles, smart homes, and wearables. Federal near-shoring incentives such as the USD 52 billion CHIPS and Science Act in the United States, alongside Brazil’s USD 186.6 billion Nova Indústria Brazil program, underpin fresh wafer-fab and design capacity that reduces exposure to Asian supply risk. Architecturally, the Americas microcontroller market is shifting toward higher-performance cores: 32-bit devices delivered 54.30% revenue in 2024, while 64-bit parts post the fastest 5.9% CAGR as software-defined vehicles and edge AI workloads require headroom. Demand from electric vehicles, FDA-cleared AI medical devices, and mandatory NIST IR 8425 cybersecurity standards reinforces unit volumes even as sub-28 nm capacity constraints linger.[1]National Institute of Standards and Technology, “NIST IR 8425: Recommended Criteria for Cyber-Security Labeling,” nist.gov

Key Report Takeaways

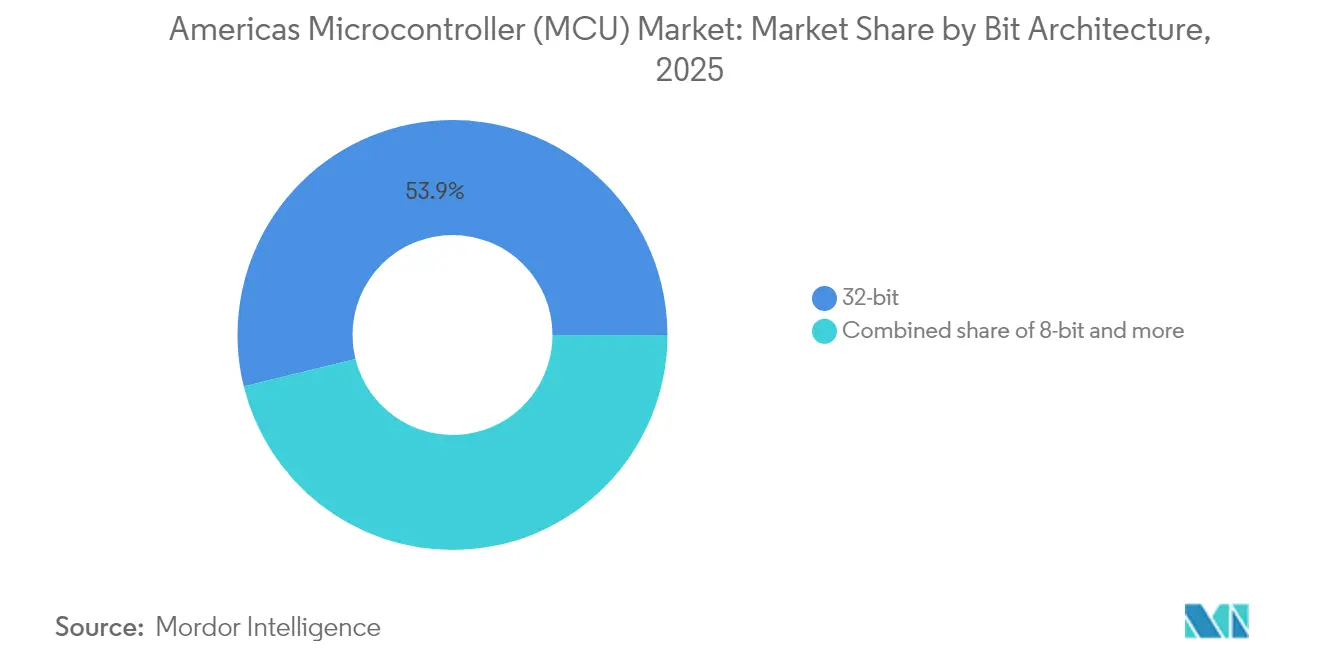

- By bit architecture, 32-bit devices led with 53.85% revenue share in 2025; 64-bit and above devices are projected to expand at a 5.54% CAGR through 2031.

- By end-user industry, the automotive sector held 29.25% of the Americas microcontroller market share in 2025, while healthcare and medical devices record the highest 5.78% CAGR to 2031.

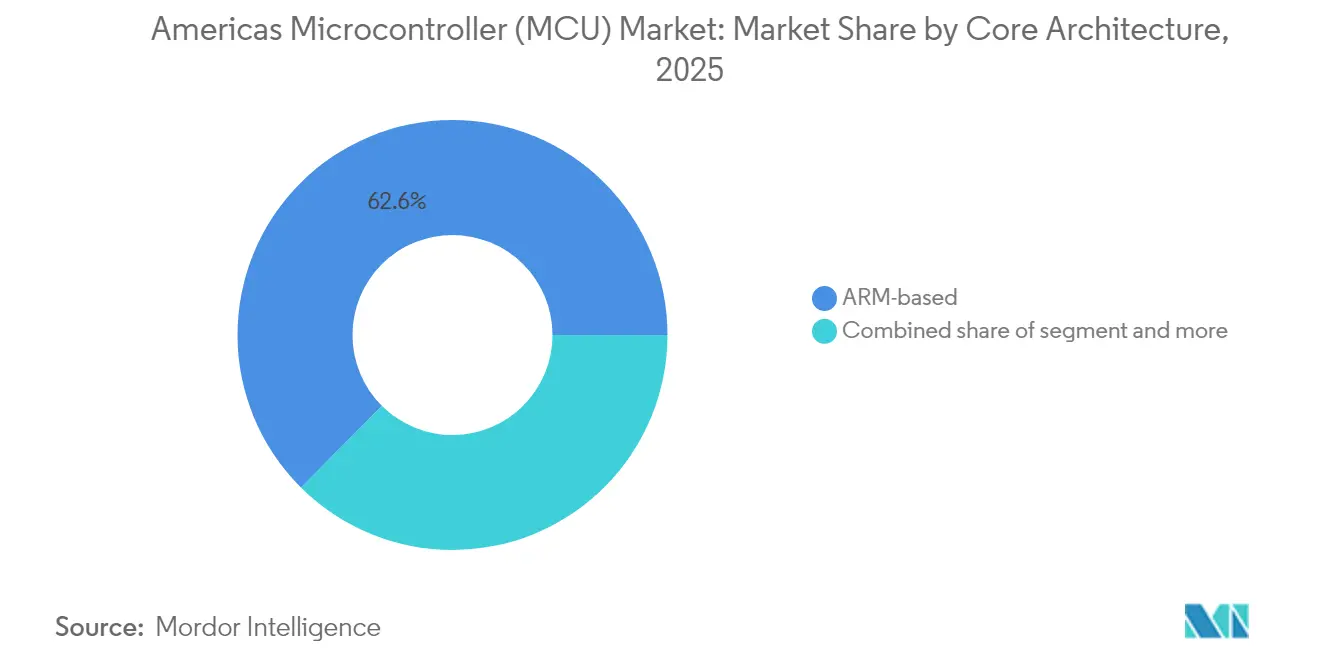

- By core architecture, ARM-based designs commanded 62.55% revenue in 2025; RISC-V designs post a 4.72% CAGR through 2031.

- By connectivity, non-wireless MCUs captured 71.10% of the Americas microcontroller market size in 2025, whereas wireless-enabled MCUs advance at a 6.44% CAGR to 2031.

- By geography, the United States accounted for 49.35% of 2025 revenue, while Brazil registers the fastest 6,720% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Americas Microcontroller (MCU) Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Automotive electrification push | 0.80% | North America and South America, with strongest impact in US and Brazil | Medium term (2-4 years) |

| Proliferation of IoT edge nodes | 0.60% | Global, with concentration in US industrial corridors and Brazilian smart cities | Short term (≤ 2 years) |

| Migration to 32-bit and ARM-based MCUs | 0.40% | Americas-wide, led by automotive and industrial applications | Medium term (2-4 years) |

| Government near-shoring incentives (CHIPS Act, Brazil PADIS) | 0.50% | US (25 states) and Brazil (Jalisco, São Paulo, Minas Gerais) | Long term (≥ 4 years) |

| Mandatory embedded-device cyber-security standards (U.S. NIST IR 8425) | 0.30% | US federal and state procurement, spillover to Canada and Mexico | Short term (≤ 2 years) |

| RISC-V cost disruption in entry-level SKUs | 0.20% | Americas-wide, strongest in cost-sensitive consumer and industrial segments | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Automotive Electrification Push

Electric vehicles embed three to five times more semiconductors than internal-combustion cars, and every traction inverter, battery-management board, or body-domain controller consumes at least one performance MCU. NXP unveiled its 16 nm S32K5 family in March 2025 with embedded MRAM and an 800 MHz Arm Cortex core to consolidate legacy ECUs and host real-time AI inference. Renesas’ RH850/C1M-Ax MCU coordinates dual traction inverters in hybrids, cutting board count and wiring weight. New greenhouse-gas limits in Canada and stricter US EPA rules accelerate electrified powertrain adoption, keeping the Americas microcontroller market closely tied to automotive design cycles. Infineon’s first automotive RISC-V MCU under the AURIX brand, launched in March 2025, signals a cost-driven alternative that still meets ASIL-D safety targets.[2]NXP Semiconductors, “S32K5 Arm Cortex-M MCU Family,” nxp.com

Proliferation of IoT Edge Nodes

Industrial and consumer devices are gaining local intelligence that shrinks latency and lowers cloud fees. IEEE data show the intelligent industrial edge segment leaped from USD 11.6 billion in 2019 to USD 30.8 billion by 2025, with software now 41% of spend. Renesas forecasts USD 10 billion for wireless connectivity MCUs by 2030 as ultra-low-power cores run secure neural networks at the edge. Arduino’s Nano Matter board, built on Silicon Labs’ MGM240S, executes gesture recognition locally and speaks the interoperable Matter protocol, easing smart-home rollouts. NXP’s 2025 wireless outlook likewise highlights on-chip machine-learning accelerators that shift inference workloads away from data centers.

Migration to 32-bit and ARM-based MCUs

Demand for higher compute density and in-field upgrade capability is phasing out 8-bit and 16-bit controllers. STMicroelectronics’ Stellar MCUs adopt 18 nm FD-SOI and store secure OTA update images while keeping ASIL-D safety. Industry estimates place RISC-V penetration at 15% of global MCUs in 2024, reflecting interest in royalty-free cores. Microchip’s move to 64-bit RISC-V parts balances ongoing Arm support and underlines the diversification aim of tier-one suppliers.

Government Near-shoring Incentives

The USD 52 billion CHIPS Act has already triggered more than USD 540 billion in private semiconductor commitments, pushing new fabs into Arizona, Texas, New York, and Ohio. Brazil’s PADIS incentives within the Nova Indústria Brazil plan add BRL 7 billion yearly to back design houses and specialty foundry upgrades; the Kutsari Project created the first National Semiconductor Design Center in February 2025. Texas alone hosts USD 61 billion of ongoing capacity projects, with Samsung and Texas Instruments leading builds.[3]U.S. Department of Commerce, “CHIPS and Science Act Drives Historic Investment,” commerce.gov

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Pricing commoditisation and margin squeeze | -0.40% | Americas-wide, particularly affecting high-volume consumer applications | Short term (≤ 2 years) |

| Persistent wafer-fab capacity bottlenecks below 28 nm | -0.30% | Global impact with Americas supply chain dependencies on Asian fabs | Medium term (2-4 years) |

| Software-complexity outpacing 8-/16-bit capabilities | -0.20% | North America industrial and automotive sectors, spillover to South America | Medium term (2-4 years) |

| IP-licensing and export-control compliance risks | -0.10% | US-Canada primarily, with regulatory spillover affecting Mexico and Brazil | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Pricing Commoditisation and Margin Squeeze

Volume segments such as wearables and entry-level smart-home sensors see ASP decline faster than input inflation. Microchip’s FY2025 net sales fell 42.3% despite healthy unit volumes, underscoring the knife-edge margin equation. RISC-V entrants with zero IP royalties intensify price competition, forcing established suppliers to differentiate through toolchains, reference designs, and long-term supply assurances.

Persistent Wafer-fab Capacity Bottlenecks Below 28 nm

Advanced high-performance MCUs increasingly need 22 nm or finer nodes, yet most regional fabs still run 40 nm and above. SEMI forecasts only 3% of CHIPS Act money earmarked for advanced packaging, a gap that constrains MCU throughput even as new wafer plants break ground. Legacy 28 nm lines remain critical for automotive safety MCUs that cannot redesign quickly, leaving the Americas microcontroller market exposed to Asia-centric supply shocks until local fabs complete in late 2027.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Bit Architecture: 64-bit Emergence Accelerates

In 2025 the 32-bit class accounted for 53.85% of revenue and anchored the Americas microcontroller market. Demand centers on automotive body, chassis, and power modules where memory protection, FOTA support, and deterministic real-time performance outweigh raw compute. The Americas microcontroller market size for 32-bit devices is projected to climb at 2.05% CAGR through 2031 as legacy 16-bit sockets upgrade.

The 64-bit and above band, while below 10% share today, owns the fastest 5.54% CAGR. AI-heavy driver-monitoring cameras, software-defined vehicle domain controllers, and industrial vision systems each require expanded address space and advanced vector engines. Microchip’s PIC64 High-Performance Spaceflight Computing line brings RISC-V vector units that run machine-learning inference in radiation-hardened environments, giving defense primes a domestic alternative to custom ASICs.

By End-user Industry: Healthcare Digitization Drives Growth

Automotive remained the largest of all end-user buckets with 29.25% revenue in 2025. OEM roadmaps for level 2+ driver assistance, battery state-of-health analytics, and zonal architectures keep MCU attach counts high. The segment is predicted to advance at 2.96% CAGR as electrified platforms shorten refresh cycles.

Healthcare and medical devices post the fastest 5.78% CAGR. Continuous-glucose monitors, portable ultrasound, and AI-supported diagnostic imagers rely on low-power secure MCUs that handle sensor fusion and run FDA-cleared algorithms. The Americas microcontroller market share for healthcare is small today but expands quickly because hardware must comply with cybersecurity controls and detailed audit logging regimes set by the FDA.

By Core Architecture: RISC-V Disruption Accelerates

ARM-based designs held 62.55% revenue in 2025; wide tool support and power efficiency prop them up across almost every vertical. The Americas microcontroller market size attached to ARM cores is forecast to grow modestly as existing customers extend platforms rather than switch.

RISC-V units however add 4.72% CAGR, helped by start-ups that design cost-optimized SKUs free from royalty overhead. Infineon’s March 2025 automotive RISC-V MCU series, initially sampled to European OEMs, will ship from a Texas 300 mm line in late 2026. Adoption is particularly rapid in cost-sensitive consumer devices and simple industrial IO blocks.

By Connectivity: Wireless Integration Surges

Non-wireless MCUs still supplied 71.10% of 2025 shipments, serving appliance controls, power-tool drivetrains, and safety-isolated industrial loops where wired buses dominate. Yet wireless-capable parts, growing 6.44% CAGR, pull ahead in terms of design wins as Thread, Wi-Fi 6, and ultra-wideband integrate onto a single package. Qualcomm and STMicroelectronics announced a reference platform that marries STM32 MCUs with Qualcomm AI wireless transceivers, trimming PCB area by 40% for next-gen smart-factory nodes.

Regulatory energy limits also spur low-sleep-current designs. Qorvo’s QPG6200L SoC consumes under 1 µA in deep sleep while maintaining tri-radio connectivity, enabling five-year battery life in door sensors.

Geography Analysis

The United States contributed 49.35% of 2025 revenue thanks to a USD 450 billion capex wave spanning 25 states. Texas claims the biggest slice after Samsung broke ground on a USD 17 billion Taylor fab and Texas Instruments expanded its Richardson campus. Canada fortifies back-end capacity: Ottawa granted USD 120 million to the Fabric network while IBM pledged USD 187 million for advanced packaging in Bromont, Quebec.

Brazil’s share is small today yet vaults on a 6,720% CAGR because PADIS tax incentives and the Kutsari Project create domestic chip design centers in São Paulo, Minas Gerais, and Pernambuco. Mexico leverages USMCA proximity, luring Foxconn and Nvidia to new AI server and superchip lines in Guadalajara. Secondary South American markets, including Argentina and Colombia, piggyback on MERCOSUR tariff breaks to import tooling and attract niche assembly houses.

Competitive Landscape

The Americas microcontroller market features moderate concentration. NXP Semiconductors, Texas Instruments, and Microchip Technology together command roughly 45% of regional revenue via broad portfolios that span 8-bit to 64-bit and integrate analog, connectivity, and security IP. NXP’s S32 CoreRide platform reduces software porting effort across vehicle zones and underpins long design-in cycles at OEMs. Texas Instruments differentiates through decades-long supply guarantees and fully characterized automotive temperature ranges. Microchip responds with MPLAB ecosystem updates, AI-assisted code generation, and a USD 880 million silicon-carbide capacity expansion in Colorado Springs.

Open-source ISA momentum stirs competition: Andes, Ventana, and SiFive license commercial RISC-V cores that allow tier-two MCU vendors to skip Arm royalties yet still ship certified development kits. Established players answer by widening security LSI, offering supply assurance contracts, and adding machine-learning accelerators. End users therefore choose between proven support networks and disruptive cost structures, balancing long-term availability against board spend.

White-space opportunities surround edge AI inference and medical wearable safety. Hardware-root-of-trust blocks meeting NIST IR 8425 and low-sleep-current radios propel premium ASPs in these niches despite overall commoditization pressures.

Americas Microcontroller (MCU) Industry Leaders

NXP Semiconductors N.V.

Texas Instruments Incorporated

Microchip Technology Inc.

STMicroelectronics N.V.

Renesas Electronics Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: NXP Semiconductors introduced the S32K5 16 nm automotive MCU with embedded MRAM to support unified software-defined vehicle architectures

- March 2025: Infineon Technologies launched the first automotive RISC-V MCU family under the AURIX brand, expanding open-architectural options.

- February 2025: Mexico inaugurated the Kutsari Project to establish a national semiconductor design center and regional hubs.

- January 2025: Microchip Technology announced USD 880 million expansion of Colorado Springs silicon carbide and silicon lines.

Americas Microcontroller (MCU) Market Report Scope

Microcontrollers are small integrated circuits specially programmed to control the particular function of an electronic system. The standard microcontroller comprises one chip's processor, memory, and input-output interface. A microcontroller is embedded into the system to maintain the specific parts of an apparatus. In a wide range of devices and systems, microcontrollers are used to carry out the task at hand; devices frequently use several microcontrollers that work together.

The Americas microcontroller (MCU) market is segmented by product (4 and 8-bit, 16-bit, and 32-bit), by application (aerospace and defense, consumer electronics and home appliances, automotive, industrial, healthcare, data processing and communication, and other applications), and by country (USA, Canada, and the rest of Americas).

The market sizes and forecasts are provided in terms of value in USD for all the above segments.

| 8-bit |

| 16-bit |

| 32-bit |

| 64-bit and Above |

| Automotive |

| Consumer Electronics |

| Industrial Automation |

| Communications and Networking |

| Healthcare and Medical Devices |

| Others |

| ARM-based |

| RISC-V-based |

| x86-based |

| Proprietary Cores |

| Wireless-enabled MCUs |

| Non-wireless MCUs |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Bit Architecture | 8-bit | |

| 16-bit | ||

| 32-bit | ||

| 64-bit and Above | ||

| By End-user Industry | Automotive | |

| Consumer Electronics | ||

| Industrial Automation | ||

| Communications and Networking | ||

| Healthcare and Medical Devices | ||

| Others | ||

| By Core Architecture | ARM-based | |

| RISC-V-based | ||

| x86-based | ||

| Proprietary Cores | ||

| By Connectivity | Wireless-enabled MCUs | |

| Non-wireless MCUs | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current size of the Americas microcontroller market?

The market is valued at USD 739.52 million in 2026 and is set to reach USD 815.33 million by 2031, growing at a 1.97% CAGR.

Which end-user industry generates the most revenue?

Automotive leads with 29.25% of 2025 revenue, helped by rising electric-vehicle and ADAS deployments.

Which segment is expanding fastest?

Healthcare and medical devices show the highest 5.78% CAGR through 2031, supported by FDA-cleared AI devices and stricter cybersecurity rules.

How dominant are ARM-based microcontrollers in the region?

ARM-based designs held 62.55% revenue share in 2025, although RISC-V parts are gaining on a 4.72% CAGR.

Why is Brazil’s growth rate so high?

Brazil benefits from the Nova Indústria Brasil incentives and the Kutsari Project, giving the country a forecast 6,720% CAGR to 2031.

What risks could slow market growth?

Price commoditisation in high-volume consumer lines and sub-28 nm wafer shortages could trim overall CAGR by 0.7 percentage points.

Page last updated on: