Market Overview

| Study Period | 2022 - 2030 |

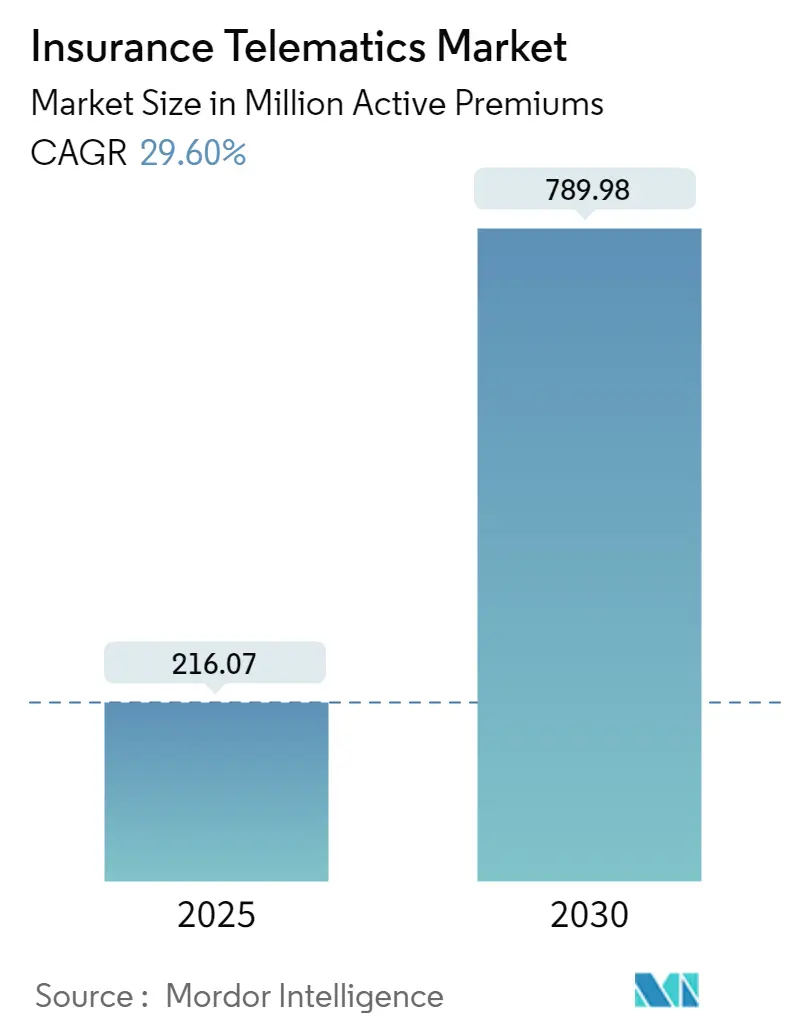

| Market Volume (2025) | 216.07 Million active premiums |

| Market Volume (2030) | 789.98 Million active premiums |

| Growth Rate (2025 - 2030) | 29.60% CAGR |

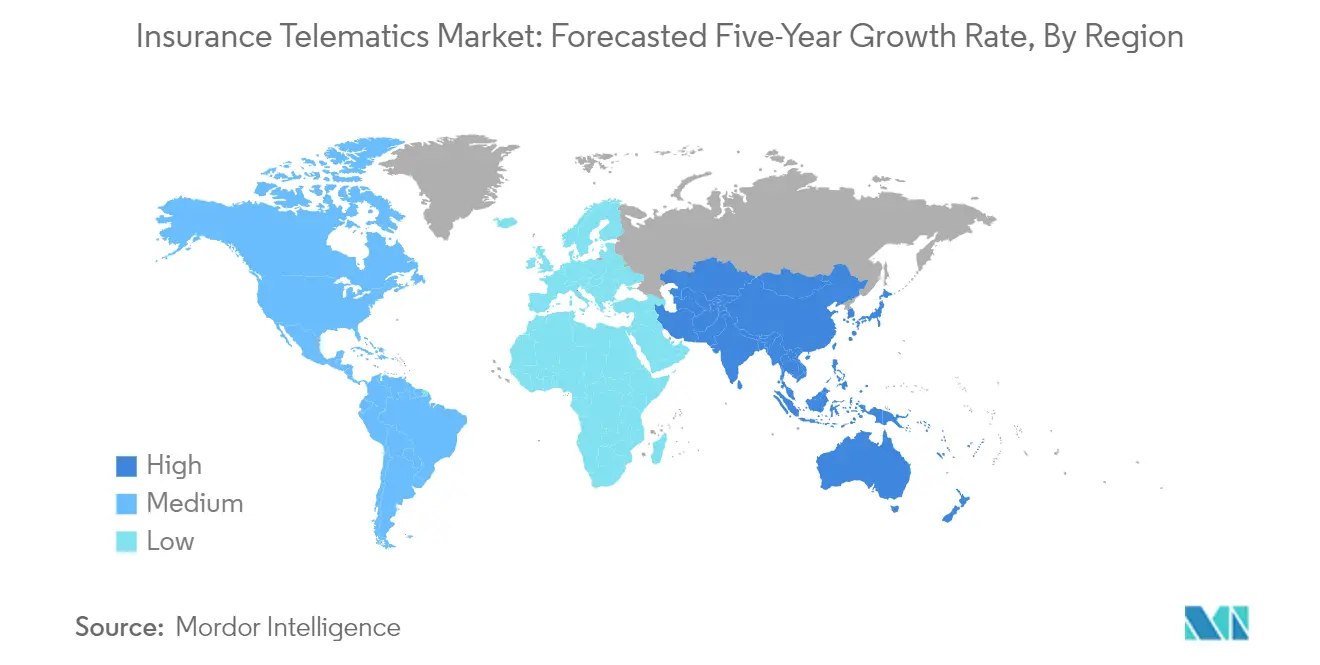

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

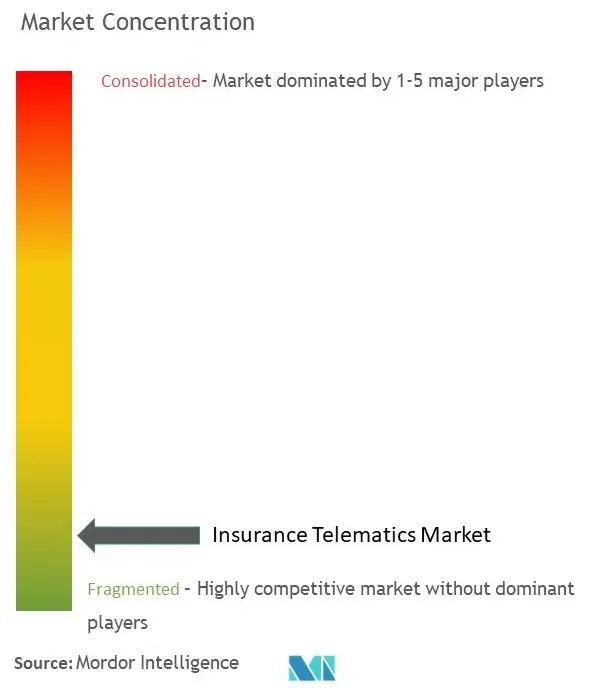

| Market Concentration | Low |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Insurance Telematics Market Analysis

The Insurance Telematics Market size is estimated at 216.07 million active premiums in 2025, and is expected to reach 789.98 million active premiums by 2030, at a CAGR of 29.6% during the forecast period (2025-2030).

The insurance telematics industry is experiencing significant transformation driven by evolving road safety concerns and changing mobility patterns. In the European Union, approximately 20,400 people were killed in road crashes in 2023, with a marginal 1% decline from 2022. The fatality distribution reveals that car drivers and passengers account for 45% of casualties, while pedestrians, two-wheeler users, and cyclists represent 18%, 19%, and 10% respectively. These statistics have prompted insurers to implement more sophisticated risk assessment mechanisms through telematics solutions, focusing on preventive measures and real-time monitoring capabilities.

The rapid electrification of the automotive sector is reshaping the insurance telematics landscape, with electric vehicle adoption creating new opportunities for advanced monitoring systems. According to the IEA report, electric vehicle sales reached unprecedented levels in 2023, with China leading at 8 million units, followed by Europe at 3.4 million, and the United States at 1.6 million units. This shift towards electric vehicles has necessitated the development of specialized vehicle telematics solutions that can effectively monitor and assess the unique risk factors associated with electric powertrains and charging patterns.

The integration of artificial intelligence and IoT technologies is revolutionizing how insurers collect and analyze driving data. Insurance companies are increasingly moving away from traditional OBD-II port devices toward sophisticated smartphone-based solutions that leverage advanced sensors and machine learning algorithms. This technological evolution has enabled more accurate risk assessment capabilities while significantly reducing hardware deployment costs and improving user accessibility. The industry is witnessing a notable shift toward mobile-first solutions that provide real-time feedback and personalized coaching to drivers.

Regulatory frameworks and data privacy considerations continue to shape the market landscape, particularly in developed regions. The European Union's mandate requiring telematics devices in all new vehicles by 2024 represents a significant regulatory push toward widespread adoption. Insurance providers are adapting their solutions to comply with stringent data protection regulations while maintaining the effectiveness of their risk assessment capabilities. This regulatory environment has fostered innovation in secure data transmission protocols and transparent data usage policies, building consumer trust in digital insurance products.

Insurance Telematics Market Trends

Increasing Adoption of Usage-Based Insurance by Insurance Companies

Usage-based insurance (UBI) is experiencing unprecedented growth as insurance providers seek to offer more personalized and data-driven coverage options. The traditional one-size-fits-all approach to auto insurance is being replaced by sophisticated telematics-based programs that analyze actual driving behavior and usage patterns. According to insurance industry data, the average value of private passenger automobile comprehensive insurance claims for physical damage in the United States increased to USD 2,738 in 2022, pushing insurers to adopt more precise risk assessment methods through telematics.

Recent market developments demonstrate the accelerating adoption of UBI solutions. In September 2023, OCTO launched the Digital Driver 'Try Before You Buy' solution, allowing insurance companies to define customer pricing more accurately through transparent relationships based on actual driving behavior data. Similarly, in December 2023, The Green Insurer introduced a new car insurance product that rewards customers for driving responsibly by computing their carbon footprint through driving data analysis. These innovations highlight how insurance companies are leveraging telematics not only for risk assessment but also for promoting sustainable driving practices and customer engagement.

Understand The Key Trends Shaping This Market

Download PDF

Increase in Innovation in the Automotive Industry Drive the Market Growth

The automotive industry is undergoing rapid technological transformation, with connected car technologies and autonomous driving capabilities leading the innovation wave. According to Intel's projections, autonomous vehicles are expected to account for approximately 12% of car registrations by 2030, creating new opportunities for insurance telematics integration. The industry is witnessing significant investments in advanced driver assistance systems (ADAS), vehicle-to-everything (V2X) communication, and embedded telematics solutions that enable more comprehensive risk assessment and real-time monitoring capabilities.

Recent developments underscore the industry's commitment to innovation. In February 2024, Harman introduced the Harman Ready Connect 5G Telematics Control Unit (TCU), leveraging connected car technologies and Qualcomm's Snapdragon Digital Chassis to expand connectivity boundaries. Additionally, in December 2023, HCLTech and Roadzen announced a collaboration to harness AI and data engineering for delivering benefits to both auto insurance carriers and their customers. These innovations are transforming how insurers assess risk, price policies, and interact with policyholders, while simultaneously improving vehicle safety and operational efficiency through advanced automotive telematics solutions.

Segment Analysis: By Usage Type

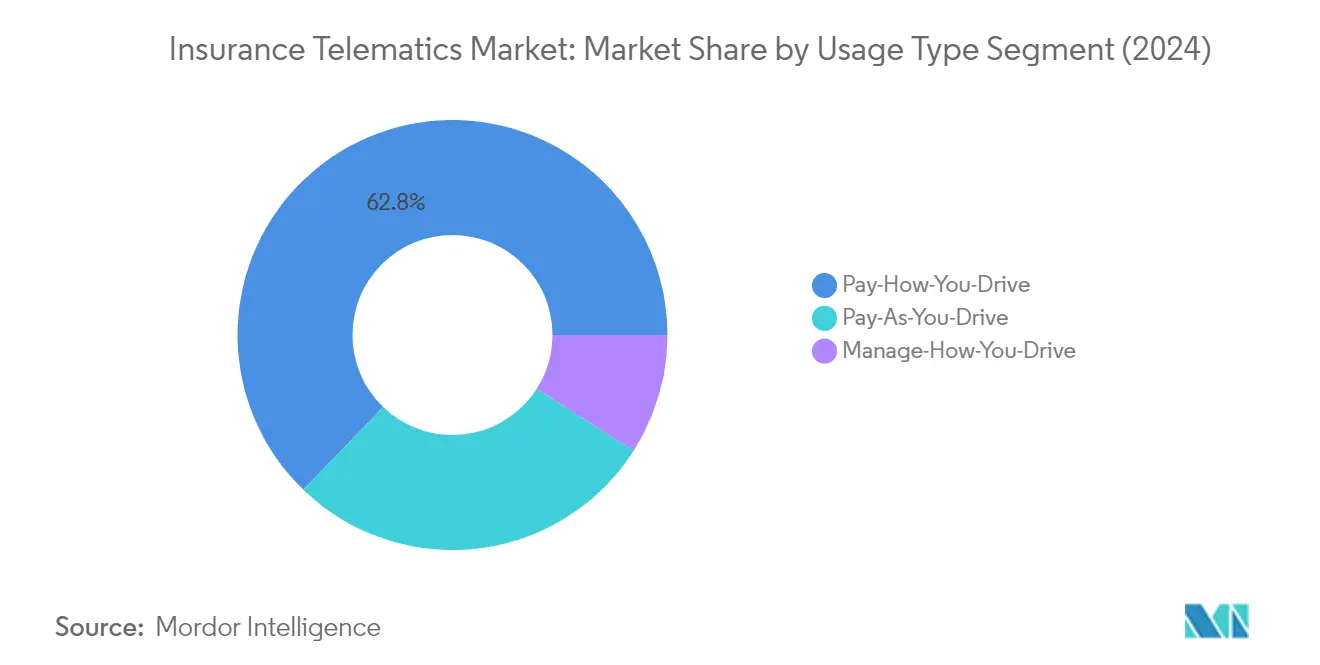

Pay-How-You-Drive Segment in Insurance Telematics Market

The Pay-How-You-Drive (PHYD) segment dominates the usage-based insurance market, commanding approximately 63% market share in 2024, while also emerging as the fastest-growing segment with a projected growth rate of around 30% from 2024 to 2029. This segment's prominence is driven by its innovative approach, where driving skills are considered the primary factor in setting premiums. Insurance providers are increasingly adopting PHYD insurance models as they offer more accurate risk assessment by monitoring various parameters such as speed, braking patterns, sudden stops, acceleration, and concentration levels through telematics tracking devices. The segment's growth is further bolstered by the integration of advanced technologies like AI and machine learning for more precise driver behavior analysis. Major insurance companies are actively expanding their PHYD insurance offerings, with many introducing sophisticated mobile applications and connected car solutions to provide real-time driving feedback and personalized premium adjustments based on driving behavior.

Remaining Segments in Usage-Based Insurance Telematics Market

The Pay-As-You-Drive (PAYD) and Manage-How-You-Drive (MHYD) segments represent significant components of the telematics usage-based insurance market, each offering unique value propositions to consumers. The PAYD insurance segment focuses on distance-based premium calculations, making it particularly attractive to low-mileage drivers and those seeking more flexible insurance options. This approach has gained traction with the rise of remote work and changing driving patterns. Meanwhile, the MHYD segment extends beyond basic tracking to provide comprehensive driver coaching and behavioral improvement tools, incorporating real-time alerts and personalized suggestions to ensure safety. Both segments are witnessing increased adoption as insurance providers expand their telematics insurance policies portfolios to meet diverse customer needs and preferences in the evolving automotive insurance landscape.

Insurance Telematics Market Geography Segment Analysis

Insurance Telematics Market in North America

North America continues to lead the global telematics insurance market, commanding approximately 49% of the total market share in 2024. The region's dominance is primarily driven by the substantial presence of automotive OEMs, high levels of technology awareness among car buyers, and widespread adoption of 4G/5G networks. The United States, in particular, demonstrates strong market potential due to consumers' increasing preference for usage-based insurance (UBI) snapshot programs over traditional motor insurance policies. The region's growth is further supported by continuous product launches from several insurance telematics companies, which have elevated market competition and innovation. The decreasing cost of development and technology, evolving consumer behavior, and stringent government regulations are additional factors propelling market growth. The introduction of insurance telematics solutions has brought numerous advantages for both insurers and consumers, with insurers benefiting from reduced claim-handling expenses and consumers gaining from promoted safe driving practices that help mitigate accident severity and frequency.

Insurance Telematics Market in Europe

Europe has emerged as a significant market for telematics motor insurance, experiencing approximately 28% growth from 2019 to 2024. The region's market is characterized by strong regulatory support, particularly in the European Union, where government mandates require the installation of telematic devices on all new vehicles. The market's expansion is driven by continuous innovations to meet consumers' evolving requirements and the growing adoption of advanced driver assistance systems (ADAS). The region has witnessed significant developments in telematics technology, particularly in countries like Italy, where the government actively supports market growth through legislation. The presence of major automotive manufacturers and their increasing focus on connected vehicle technologies has further strengthened the market. European insurtech companies are actively collaborating to bring new options and insurance schemes to customers, encouraging a smoother transition from traditional methods of buying vehicle insurance to detailed telematics alternatives.

Insurance Telematics Market in Asia-Pacific

The Asia-Pacific telematics insurance market is poised for remarkable expansion, with a projected growth rate of approximately 37% during 2024-2029. The region's market is driven by increasing vehicle ownership, strong regulatory support, and rapid technological advancement. The connected vehicle ecosystem, particularly in countries like India, has received a significant boost through government safety initiatives and amendments to automotive industry standards. The market is witnessing substantial developments in mobile telematics and smartphone-centered solutions, allowing for real-time tracking and analysis of driving behavior. The region's automotive sector is experiencing rapid transformation with the increasing adoption of electric vehicles and connected car technologies. Major players in the market are expanding their presence through strategic partnerships and innovative solution offerings, while governments are implementing supportive policies to promote the adoption of connected car insurance solutions.

Insurance Telematics Market in Rest of the World

The Rest of the World region, encompassing Latin America, the Middle East, and Africa, represents an emerging market for insurance telematics with significant growth potential. Latin America has emerged as one of the significant adopters in the market, driven by growing investments in the automotive sector and the increasing presence of key telematics solution providers. The region is witnessing substantial developments in digital mobility solutions and connected vehicle services. The Middle East, particularly the UAE, is showing promising growth potential with the increasing deployment of 5G technology and supportive government initiatives for autonomous vehicles. The market is further strengthened by various manufacturers establishing their facilities in the region and the growing adoption of advanced telematics solutions in both personal and commercial vehicles. The implementation of new legislation supporting autonomous vehicles and smart mobility initiatives is expected to create additional opportunities for market growth.

Get Analysis on Important Geographic Markets

Download PDF

Insurance Telematics Market Overview

Top Companies in Insurance Telematics Market

The insurance telematics market features prominent players like GEICO, AXA SA, Octo Telematics, Cambridge Mobile Telematics, and Allstate Insurance leading innovation and market development. Companies are increasingly focusing on developing advanced smartphone-based insurance telematics solutions that leverage artificial intelligence and machine learning capabilities to provide more accurate risk assessment and personalized pricing models. Strategic partnerships between telematics insurance companies and automotive manufacturers have become a key trend, enabling seamless integration of telematics solutions into vehicles. Market leaders are investing heavily in research and development to enhance their technological capabilities, particularly in areas such as crash detection, driver behavior analysis, and real-time monitoring systems. The industry is witnessing a shift towards cloud-based platforms and mobile-first solutions, with companies expanding their service offerings to include features like emergency response systems, preventive maintenance alerts, and comprehensive fleet management solutions.

Dynamic Market Structure Drives Industry Evolution

The telematics insurance industry exhibits a mix of global insurance conglomerates and specialized telematics technology providers, creating a complex competitive landscape. Large insurance companies leverage their established customer base and financial resources to develop proprietary insurance telematics solutions, while specialized providers focus on developing cutting-edge technology platforms that can be integrated into existing insurance products. The market is experiencing increasing consolidation through strategic acquisitions and partnerships, as companies seek to combine insurance expertise with technological capabilities. Traditional insurance providers are actively acquiring or partnering with technology startups to enhance their digital capabilities and expand their telematics offerings.

The competitive dynamics are further shaped by regional market leaders who maintain strong positions in their respective territories through a deep understanding of local regulatory requirements and customer preferences. Market consolidation is particularly evident in mature markets where larger players are absorbing smaller, innovative companies to expand their technological capabilities and market reach. The industry is witnessing a trend of cross-border partnerships and joint ventures, especially between established insurance providers and emerging technology companies, aimed at creating comprehensive telematics solutions that can be deployed across multiple markets.

Innovation and Adaptability Drive Market Success

Success in the telematics insurance industry increasingly depends on companies' ability to develop user-friendly, comprehensive solutions that seamlessly integrate with existing vehicle systems and provide tangible benefits to both insurers and end-users. Incumbent players are focusing on expanding their technological capabilities through internal development and strategic partnerships, while also maintaining strong relationships with automotive manufacturers to ensure native integration of their solutions. Market leaders are investing in insurance analytics capabilities and artificial intelligence to enhance their risk assessment models and provide more personalized insurance products. Companies are also emphasizing customer education and engagement to drive adoption of telematics-based auto insurance products.

For new entrants and challenger companies, success lies in identifying and exploiting specific market niches or technological advantages that differentiate them from established players. The market presents moderate barriers to entry due to the need for significant technological expertise and regulatory compliance capabilities. Regulatory requirements regarding data privacy and security continue to evolve, requiring companies to maintain robust compliance frameworks and adapt their solutions accordingly. The concentration of end-users varies by region and market segment, with commercial fleet operators representing a particularly attractive target market due to their higher adoption rates and specific needs for comprehensive telematics solutions. The risk of substitution remains relatively low due to the increasing integration of telematics into core insurance products and the growing emphasis on data-driven risk assessment.

Insurance Telematics Market Leaders

-

GEICO (Berkshire Hathaway Inc.)

-

UnipolTech SpA (UNIPOL GRUPPO SpA)

-

Octo Telematics SpA

-

DriveQuant

-

Imertik Global Inc

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Insurance Telematics Market News

- In January 2024, Targa Telematics SPA announced the acquisition of Earnix’s telematics business to expand insurance digitization. Through this acquisition, Targa assumes ownership of Drive-it, which has a solution to develop a behavioral analysis of drivers, leveraging machine learning and Artificial Intelligence technologies.

- In December 2023, MiX Telematics and Powerfleet to Present at the Raymond James TMT and MiX Telematics and Powerfleet announced a business combination, which was expected to create one of the most extensive mobile asset Internet of Things (IoT) Software-as-a-Service (SaaS) providers in the world.

Insurance Telematics Market Industry Segmentation

The market for insurance telematics was analyzed considering the total number of active premiums filed by the various insurance providers operating worldwide.

The insurance telematics market is segmented by usage type (pay-as-you-drive, pay-how-drive, manage-how-you-drive) and geography (North America, Europe, Asia-Pacific, Rest of the World). The market sizes and forecasts are provided in terms of the number of active premiums for all the above segments.

| By Usage Type | Pay-as-you-drive |

| Pay-how-you-drive | |

| Manage-how-you-drive | |

| By Geography*** | North America |

| Europe | |

| Asia | |

| Australia and New Zealand | |

| Latin America | |

| Middle East and Africa |

By Usage Type

| Pay-as-you-drive |

| Pay-how-you-drive |

| Manage-how-you-drive |

By Geography***

| North America |

| Europe |

| Asia |

| Australia and New Zealand |

| Latin America |

| Middle East and Africa |

Need A Different Region or Segment?

Customize Now

Insurance Telematics Market Research FAQs

How big is the Insurance Telematics Market?

The Insurance Telematics Market size is expected to reach 216.07 million active premiums in 2025 and grow at a CAGR of 29.60% to reach 789.98 million active premiums by 2030.

What is the current Insurance Telematics Market size?

In 2025, the Insurance Telematics Market size is expected to reach 216.07 million active premiums.

Who are the key players in Insurance Telematics Market?

GEICO (Berkshire Hathaway Inc.), UnipolTech SpA (UNIPOL GRUPPO SpA), Octo Telematics SpA, DriveQuant and Imertik Global Inc are the major companies operating in the Insurance Telematics Market.

Which is the fastest growing region in Insurance Telematics Market?

Asia Pacific is estimated to grow at the highest CAGR over the forecast period (2025-2030).

Which region has the biggest share in Insurance Telematics Market?

In 2025, the North America accounts for the largest market share in Insurance Telematics Market.

What years does this Insurance Telematics Market cover, and what was the market size in 2024?

In 2024, the Insurance Telematics Market size was estimated at 152.11 million active premiums. The report covers the Insurance Telematics Market historical market size for years: 2022, 2023 and 2024. The report also forecasts the Insurance Telematics Market size for years: 2025, 2026, 2027, 2028, 2029 and 2030.

Page last updated on: December 24, 2024