Insulated Packaging Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

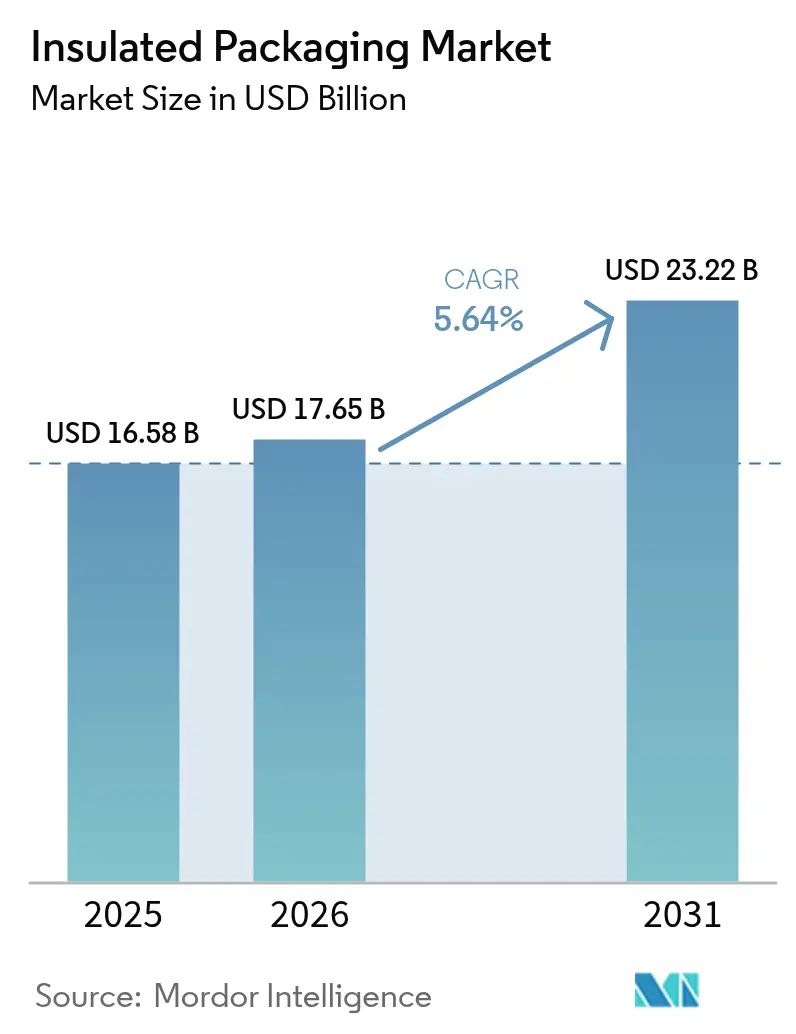

| Market Size (2026) | USD 17.65 Billion |

| Market Size (2031) | USD 23.22 Billion |

| Growth Rate (2026 - 2031) | 5.64% CAGR |

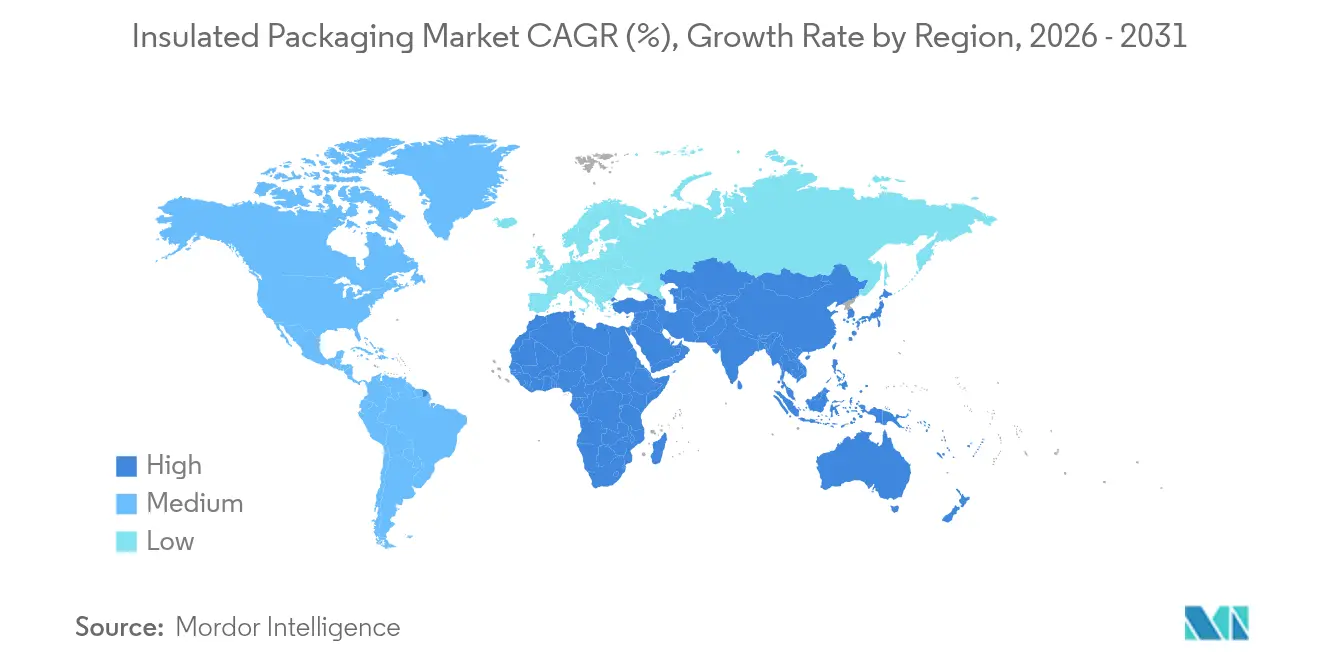

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Insulated Packaging Market Analysis by Mordor Intelligence

The Insulated Packaging Market size is expected to grow from USD 16.58 billion in 2025 to USD 17.65 billion in 2026 and is forecast to reach USD 23.22 billion by 2031 at 5.64% CAGR over 2026-2031.

Robust e-commerce penetration in temperature-sensitive categories, rising biologics output, and food-delivery adoption are reshaping cost models toward total-landed-cost optimization that factors spoilage, reverse logistics, and carbon intensity. Converter margins tightened in 2024-2025 as polystyrene spot prices moved 18-22% quarter-to-quarter, spurring trials of bio-based aerogels and phase-change materials that limit exposure to petrochemical feedstocks. Sustainability mandates are equally catalytic: the European Union’s recyclable-by-2030 rule is driving fiber-based formats, while U.S. regulators emphasize data-logged stability in pharmaceutical shipments. Competitive intensity is moderate, yet vertical integration around PCM formulation and IoT sensing continues to unlock pricing power.

Key Report Takeaways

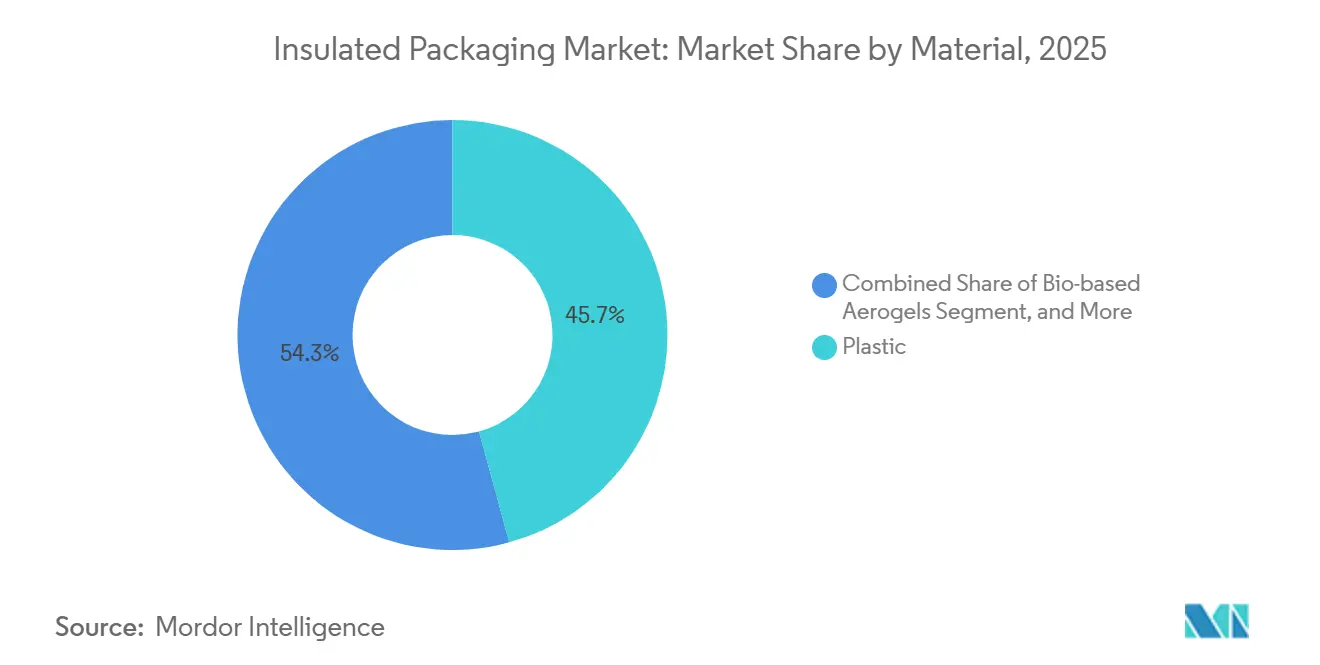

- By material, plastic retained 45.74 of % insulated packaging market share in 2025, whereas bio-based aerogels are poised for the fastest 6.89% CAGR through 2031.

- By product type, boxes and containers accounted for 38.31% of revenue in 2025, while pallet shippers are forecast to advance at a 6.44% CAGR through 2031.

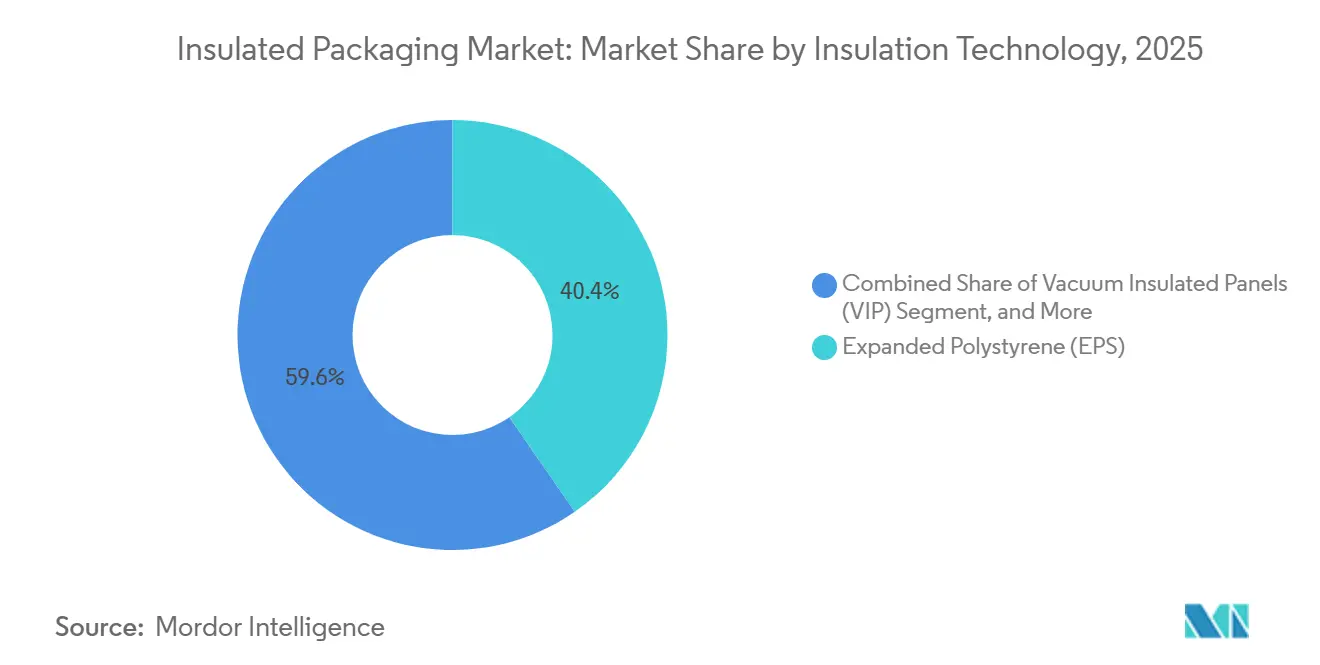

- By insulation technology, expanded polystyrene led with 40.37% of the insulated packaging market size in 2025, yet vacuum insulated panels register the highest 6.39% CAGR outlook.

- By end-user, food and beverage dominated with 48.43% share in 2025, whereas pharmaceutical and biotechnology applications will expand at a 6.71% CAGR during 2026-2031.

- By geography, North America commanded 31.63% of the value in 2025, while the Asia-Pacific is projected to register the fastest 6.59% CAGR on the back of chemical and biosimilar exports.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Insulated Packaging Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing E-Commerce Driven Demand for Thermal-Efficient Shippers | +1.8% | Global, Especially North America and Europe | Medium Term (2–4 Years) |

| Rising Global Cold-Chain Investments in Biologics and Meal-Kits | +1.5% | North America, Europe, Asia-Pacific | Long Term (≥4 Years) |

| Rapid Adoption of PCM and VIP Technologies for Last-Mile Delivery | +1.2% | Urban North America, Europe, Asia-Pacific | Short Term (≤2 Years) |

| Sustainability Mandates Accelerating Shift to Fiber-Based Insulators | +1.0% | Europe, North America, Spillover Asia-Pacific | Medium Term (2–4 Years) |

| Expansion of Grocery Q-Commerce Networks | +0.8% | Urban Asia-Pacific, North America Metros | Short Term (≤2 Years) |

| Temperature-Sensitive Specialty Chemical Exports from Asia-Pacific | +0.6% | Asia-Pacific Core, Export Lanes to Middle East and Africa | Long Term (≥4 Years) |

| Source: Mordor Intelligence | |||

Growing E-Commerce Driven Demand For Thermal-Efficient Shippers

Direct-to-consumer grocery, frozen meals, and nutritional supplements now require packaging that safeguards product integrity for up to four hours after doorstep delivery, a standard once limited to pharmaceutical logistics. Meal-kit platforms mandate slim, high-R-value formats to stay under parcel dimensional-weight limits, an advantage delivered by vacuum-insulated panels that achieve R-30 in a 20 mm profile.[1]Pelican BioThermal, “CoolPall Flex Specifications,” pelicanbiothermal.com The fragmentation of order volumes, each household receives its own insulated unit- has ultimately expanded total demand despite thinner packaging walls per unit. Cross-border e-commerce introduces time-on-route uncertainty, prompting wider PCM adoption to cushion temperature spikes in the absence of dry-ice regulations.[2]International Safe Transit Association, “Thermal Packaging Testing Standards,” ista.org

Rising Global Cold-Chain Investments In Biologics And Meal-Kits

Capacity expansions in monoclonal antibodies, mRNA vaccines, and cell therapies have outpaced the availability of validated shipping assets. International Safe Transit Association (ISTA)- certified solutions that guarantee ±2 °C stability across seasonal profiles are now table stakes for pharmaceutical sponsors. Cold Chain Technologies responded with a 1,600 L pallet shipper introduced in 2025, enabling dose consolidation and 30-40% lower packaging cost per vial. Parallel growth in premium meal kits reinforces volume for high-performance formats, allowing converters to amortize R&D across both end markets.

Rapid Adoption Of PCM And VIP Technologies For Last-Mile Delivery

Urban same-day delivery compresses transit windows to 4-6 hours, incentivizing light, compact systems. Phase-change materials harness latent heat to stabilize contents while cutting gel-pack weight. Falling VIP prices, down 15-20% annually as scale ramps, move panels beyond pharma into gourmet coffee and seafood. Reinforced shells and edge protectors mitigate puncture risk in automated sortation lines, expanding addressable use cases. The technology's Achilles heel, puncture vulnerability, is being addressed through laminated outer shells and edge-protection designs that withstand the rigors of parcel sortation. Converters that master PCM formulation and VIP lamination will capture margin premiums, while those relying solely on commodity foam face commoditization as customers demand performance differentiation.

Sustainability Mandates Accelerating Shift To Fiber-Based Insulators

European recyclability requirements, effective 2030, categorically disadvantage multi-material foams. Tetra Pak invested EUR 60 million (USD 67.8 million) in Sweden to pilot paper-based barriers that rival 48-hour cold-chain performance. Huhtamaki’s USD 100 million molded-fiber complex in Indiana supplies curbside-recyclable shippers with PCM pockets, meeting retailer pledges to remove expanded polystyrene from e-grocery deliveries. Early adopters secure price premiums in organic and specialty pharma niches where consumers reward visibly sustainable packaging. Brand owners face a strategic choice: absorb 10-15% higher packaging costs to meet sustainability commitments, or risk reputational damage and potential regulatory penalties.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile Polymer Prices Squeezing Converter Margins | -0.9% | Global, Acute Asia-Pacific and North America | Short Term (≤2 Years) |

| Limited Curb-Side Recyclability of Multi-Layer Pouches | -0.6% | Europe, North America, Rising Asia-Pacific | Medium Term (2–4 Years) |

| Inconsistent Thermal-Test Standards Inflating Certification Costs | -0.5% | Global Pharmaceutical and Food Export Corridors | Medium Term (2–4 Years) |

| High Capex Requirements for Scaling Bio-Based Aerogel Production | -0.4% | Europe and North America Pilot Facilities | Long Term (≥4 Years) |

| Source: Mordor Intelligence | |||

Volatile Polymer Prices Squeezing Converter Margins

Polystyrene feedstock traded between USD 1,200 and USD 1,550 per t during 2024-2025, as crude price swings and cracker outages disrupted supply.[3]Plastics News, “Polystyrene Price Volatility and Market Trends,” plasticsnews.com Converters on 60-day price locks absorbed margin pain when customers resisted mid-contract hikes. Larger players balanced volatility through hedging and mixed-material portfolios, while smaller firms became acquisition targets for scale operators seeking distressed assets. The dynamic favors vertically integrated producers that control resin formulation or have diversified material portfolios spanning foam, fiber, and bio-based substrates. Polymer price risk also accelerates R&D into non-petrochemical alternatives; bio-based aerogels derived from agricultural waste or algae decouple insulation economics from oil markets, though current production volumes remain subscale and unit costs exceed conventional foam by 2-3 times.

Limited Curb-Side Recyclability Of Multi-Layer Pouches

High-performance foil-polyethylene laminates cannot be separated in municipal facilities, triggering extended producer responsibility fees in markets such as Germany and California.[4]European Commission, “Packaging and Packaging Waste Regulation,” ec.europa.eu Brand owners are now piloting mono-material polyethylene or fiber formats despite slight thermal compromises. A paper-based grocery bag launched in 2025 caters to two-hour q-commerce windows and costs 20% less than rigid foam, illustrating rapid substitution potential. The transition creates a two-tier market: premium pharmaceutical shipments that prioritize performance and accept landfill disposal, versus mass-market food applications that prioritize recyclability and accept shorter thermal windows.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material: Bio-Based Substrates Challenge Plastic Incumbency

Plastic foams captured 45.74 of % insulated packaging market share in 2025, anchored by mature EPS and polyurethane supply chains that deliver a predictable cost-performance equation. However, bio-based aerogels are set to rise fastest at a 6.89% CAGR, encouraged by extended producer responsibility fees that penalize fossil-derived inputs. Converters view mycelium composites, grown from agricultural waste into rigid panels within 10 days, as a route to curbside-recyclable insulation with competitive R-value. Paper and wood-fiber formats, while recyclable, need barrier coatings to resist ambient moisture, a gap Tetra Pak targets with its barrier-coated fiber slated for 2027 rollout. Glass micro-spheres and metal foils fill niche, high-value reusable pharma shippers that amortize weight penalties across 20-plus cycles.

Weight-based freight surcharges, meanwhile, steer commodity food brands toward lightweight plastic even as sustainability agendas loom. Aerogel-infused textiles are in early commercialization, reserved for cell-therapy payloads where packaging costs are immaterial relative to cargo value. The insulated packaging market for premium biologics, therefore, gravitates toward advanced composites, while mass grocery volumes will likely remain with EPS until regulatory or raw-material shocks force a migration. Dual sourcing across foam and fiber now features in large brand tenders, signaling that supply-chain resilience matters as much as unit price.

By Product Type: Pallet Shippers Gain as Pharma Consolidates

Boxes and containers accounted for 38.31% of the insulated packaging market size in 2025, thanks to their versatility across meal kits, seafood, and specialty supplements. Still, pallet shippers are projected to post the fastest 6.44% CAGR, as pharmaceutical manufacturers consolidate pallets to cut per-dose packaging waste by up to 40%. A single 1,600 L VIP-lined pallet can replace 40 parcel boxes, trimming labor at fill sites and simplifying reverse logistics. Pouches and bags, once favored for lightweight efficiency, now face recyclability headwinds that threaten share in Europe and parts of North America where EPR fees penalize multi-layer laminates.

Wraps and liners remain essential as secondary insulation, lining both boxes and pallets to guard against condensation and puncture in multi-modal freight. Retail meal-kit operators also layer thin reflective wraps around refrigerated protein packs to extend shelf life during consumer handling. Growth in grocery quick-commerce reinforces demand for collapsible liners that fit micro-fulfillment footprints. Overall, product-mix evolution underscores a broader trend: as cold-chain networks mature, economies of scale increasingly favor bulk pallet formats in pharma, whereas the food sector balances convenience with recyclability.

By Insulation Technology: VIP Adoption Accelerates in Urban Corridors

Expanded polystyrene led with 40.37% insulated packaging market share in 2025, benefiting from decades of cost optimization and global extrusion capacity. Yet vacuum-insulated panels are set for a 6.39% CAGR because same-day delivery models prize the space savings of R-30 insulation within a 20 mm wall, helping shippers avoid parcel dimensional surcharges that can exceed USD 5 per box. Phase-change material systems grow alongside pharma payloads that mandate ±2 °C stability over 96 hours, eliminating dry-ice regulatory hassles. Reflective foil laminates occupy the value tier for grocery delivery, providing R-5 in two-hour windows at the lowest material cost.

Cost curves are narrowing: VIP panel prices fell 15-20% annually during 2024-2025 as automated lamination lines scaled, feeding adoption beyond high-value biologics into premium seafood and artisanal dessert sectors. PCM suppliers innovate bio-based esters that melt at 0-4 °C, aligning with refrigerated grocery standards while avoiding hazardous classification. Foil-air structures remain relevant in low-budget markets lacking strict validation, reinforcing a stratified technology stack in which performance, regulatory burden, and freight economics dictate material choice.

By End-User Industry: Pharma Growth Outpaces Food Volume

Food and beverage held 48.43% of insulated packaging market share in 2025, bolstered by grocery e-commerce penetration above 15% in key cities and sustained demand for fresh-produce exports. Pharmaceuticals and biotechnology, however, will expand fastest at a 6.71% CAGR, thanks to mRNA vaccine infrastructure now repurposed for biosimilars and gene therapies that require 2-8 °C control. The FDA’s 21 CFR Part 11 rule elevates packaging from a passive box to a data-logging asset, pushing converters to embed IoT sensors that verify temperature integrity from plant to patient. Beauty and personal care brands are embracing the cold chain with live probiotic serums and heat-sensitive retinols, favoring packaging that balances aesthetics with function.

Industrial chemicals add pockets of growth, particularly Asia-Pacific exports of catalysts and specialty polymers that degrade above 25 °C during maritime transit. Converter gross margins skew higher in pharma than food, incentivizing capacity prioritization toward validated shippers even as meal-kit volumes dominate tonnage. Cross-selling opportunities arise as material platforms originally tuned for vaccines migrate into premium seafood or craft-beer markets seeking longer shelf life. Consequently, diversified converters hedge cycle risk by straddling regulated and consumer segments while maintaining shared manufacturing assets for scale efficiency.

Geography Analysis

North America accounted for 31.63% of global value in 2025 on the back of mature e-commerce, high biologics spend, and grocery delivery exceeding 15% of food retail in major cities. The region continues to prioritize data-logged pharmaceutical compliance, positioning IoT-enabled packaging as a competitive necessity.

Asia-Pacific is forecast to expand at a 6.59% CAGR, the fastest among all geographies. Chinese specialty-chemical exporters and Indian vaccine producers are scaling up insulated packaging procurement to navigate 30-40 °C port-dwell temperatures on routes to the Middle East and Africa. Southeast Asian grocery platforms are also investing in cold warehouses and last-mile networks, thereby increasing the penetration of higher-value shippers that guarantee 4-hour freshness windows.

Europe emphasizes recyclability over performance, accelerating the conversion to fiber and mono-material polyethylene to meet EC 2030 mandates. South America lags in infrastructure, constraining adoption to low-cost foams, while the Middle East is building pharma corridors that require premium, validated shippers. Africa remains price-sensitive, absorbing recycled EPS for seafood exports but gradually onboarding cost-efficient VIP-foil hybrids as airport cold rooms come online.

Competitive Landscape

The top five suppliers, Amcor, Sealed Air, Sonoco, WestRock, and Mondi- collectively hold roughly 35-40% global revenue, underscoring moderate concentration. Strategic moves increasingly revolve around vertical integration; converters acquire PCM formulators or partner with sensor firms to bundle data services with each box. Huhtamaki’s USD 100 million fiber complex in Indiana exemplifies the pivot toward curbside-recyclable substrates for e-grocery contracts.

Material innovation is a battleground: Ecovative Design scales mycelium composites, while Tetra Pak and Huhtamaki race to commercialize aerogel-lined paperboard that rivals 48-hour performance. Patent filings cluster around VIP edge-sealing, PCM micro-encapsulation, and fiber moisture-barrier chemistries. Players that secure IP can license technology or establish price moats.

Consolidation continues at the regional tier, illustrated by Sealed Air’s 2024 acquisition of a Southeast Asian converter that bolstered local footprint without heavy capex. Commodity foam leaders exploit scale, yet premium niches fragment among specialists offering sustainability, regulatory expertise, or IoT integration, creating dual-speed competition within the insulated packaging market.

Insulated Packaging Industry Leaders

Sonoco Products Company

International Paper Company

Cryopak Industries Inc.

Amcor PLC

Smurfit WestRock plc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Tetra Pak allocated EUR 60 million (USD 67.8 million) for a Swedish pilot plant producing paper-based barriers achieving 48-hour thermal duration.

- February 2025: Insulated Products Corporation launched a paper grocery bag engineered for two-hour q-commerce fulfillment.

- February 2025: Cold Chain Technologies debuted the 1,600 L CCT Tower Elite pallet shipper with integrated VIP panels.

- May 2025: Tetra Pak UK invested GBP 1.4 million (USD 1.82 million) in a recycling line to recover fiber from used insulated cartons.

Global Insulated Packaging Market Report Scope

The Insulated Packaging Market Report is Segmented by Material (Plastic, Paper and Wood-fiber, Glass, Metal Foils, Bio-based Aerogels, Other Material Types), Product Type (Pouches and Bags, Boxes and Containers, Pallet Shippers, Wraps and Liners), Insulation Technology (Expanded Polystyrene, Vacuum Insulated Panels, Phase-Change Material Systems, Reflective Foil Laminate), End-user Industry (Food and Beverage, Pharmaceutical and Biotechnology, Industrial Chemicals, Beauty and Personal Care, Other End-user Industries), and Geography (North America, South America, Europe, Asia-Pacific, Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Plastic |

| Paper and Wood-fiber |

| Glass |

| Metal Foils |

| Bio-based Aerogels |

| Other Material Types |

| Pouches and Bags |

| Boxes and Containers |

| Pallet Shippers |

| Wraps and Liners |

| Expanded Polystyrene (EPS) |

| Vacuum Insulated Panels (VIP) |

| Phase-Change Material (PCM) Systems |

| Reflective Foil Laminate |

| Food and Beverage |

| Pharmaceutical and Biotechnology |

| Industrial Chemicals |

| Beauty and Personal Care |

| Other End-user Industries |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Spain | |

| Italy | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Kenya | |

| Rest of Africa |

| By Material | Plastic | |

| Paper and Wood-fiber | ||

| Glass | ||

| Metal Foils | ||

| Bio-based Aerogels | ||

| Other Material Types | ||

| By Product Type | Pouches and Bags | |

| Boxes and Containers | ||

| Pallet Shippers | ||

| Wraps and Liners | ||

| By Insulation Technology | Expanded Polystyrene (EPS) | |

| Vacuum Insulated Panels (VIP) | ||

| Phase-Change Material (PCM) Systems | ||

| Reflective Foil Laminate | ||

| By End-user Industry | Food and Beverage | |

| Pharmaceutical and Biotechnology | ||

| Industrial Chemicals | ||

| Beauty and Personal Care | ||

| Other End-user Industries | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Spain | ||

| Italy | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Kenya | ||

| Rest of Africa | ||

Key Questions Answered in the Report

How large will global insulated packaging demand be by 2031?

The insulated packaging market size is forecast to reach USD 23.22 billion by 2031, guided by a 5.64% CAGR from 2026.

Which material will grow fastest in insulated formats?

Bio-based aerogels are projected for the quickest 6.89% CAGR as converters seek recyclability and reduced oil dependency.

Why are pallet shippers gaining traction in cold-chain logistics?

Pharmaceutical manufacturers consolidate bulk biologics into VIP-lined pallet shippers to lower per-dose packaging cost by up to 40%.

What drives vacuum insulated panel adoption in grocery delivery?

VIPs trim wall thickness, helping e-commerce players avoid parcel dimensional surcharges that can add USD 5 per shipment.

Where is regional growth strongest through 2031?

Asia-Pacific leads with a 6.59% CAGR on the back of chemical and biosimilar exports and expanding cold-chain infrastructure.

How concentrated is competition among packaging suppliers?

The top five firms hold 35-40% of revenues, indicating moderate concentration that still permits new entrants with material innovations.

Page last updated on: