Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 941 Billion |

| Market Size (2026) | USD 0.99 Billion |

| Market Size (2031) | USD 1.26 Billion |

| Growth Rate (2026 - 2031) | 4.98% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Bangladesh Candy Market Analysis by Mordor Intelligence

Bangladesh candy market size in 2026 is estimated at USD 987.9 million, growing from 2025 value of USD 941 million with 2031 projections showing USD 1.26 billion, growing at 4.98% CAGR over 2026-2031. In FY 2023-24, buoyed by a 5.82% GDP growth and a per-capita income of USD 2,675, consumers have ramped up spending on discretionary items, particularly confectionery[1]Source: Bangladesh Bureau of Statistics," Bangladesh Economic Review 2024, " mof.portal.gov.bd. With 45% of the population under 24, the youthful demographic fuels a steady demand for affordable treats, as younger consumers tend to prioritize indulgent and accessible products. This demographic advantage not only supports baseline demand but also encourages manufacturers to target this segment with innovative marketing strategies and product offerings. Concurrently, innovations in products, such as new flavors, healthier alternatives, and premium options, alongside the modernization of retail infrastructure and the rapid adoption of digital commerce platforms, are propelling the candy market forward.

Key Report Takeaways

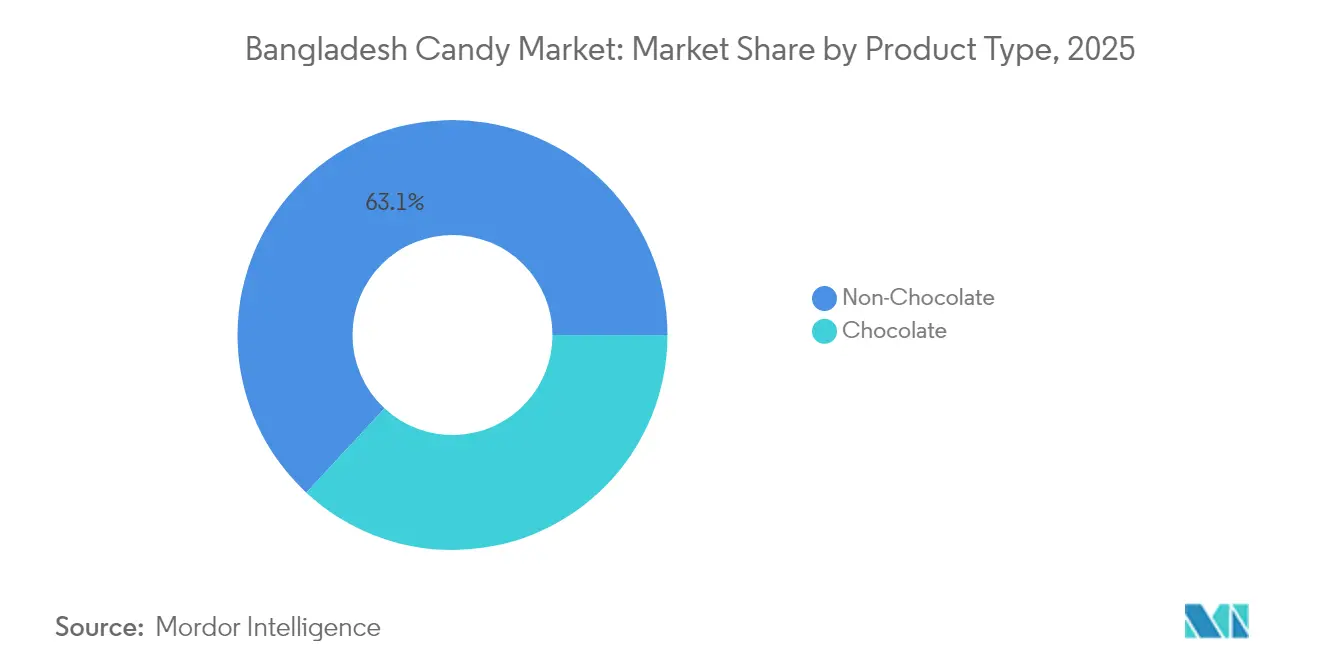

- By product type, non-chocolate lines held 63.10% of the candy market share in 2025, while chocolate is forecast to deliver the fastest 5.06% CAGR from 2026-2031.

- By ingredient, sugar-based formulations commanded 82.00% of the candy market size in 2025, yet sugar-free and low-calorie offerings are set to expand at a 7.28% CAGR during 2026-2031.

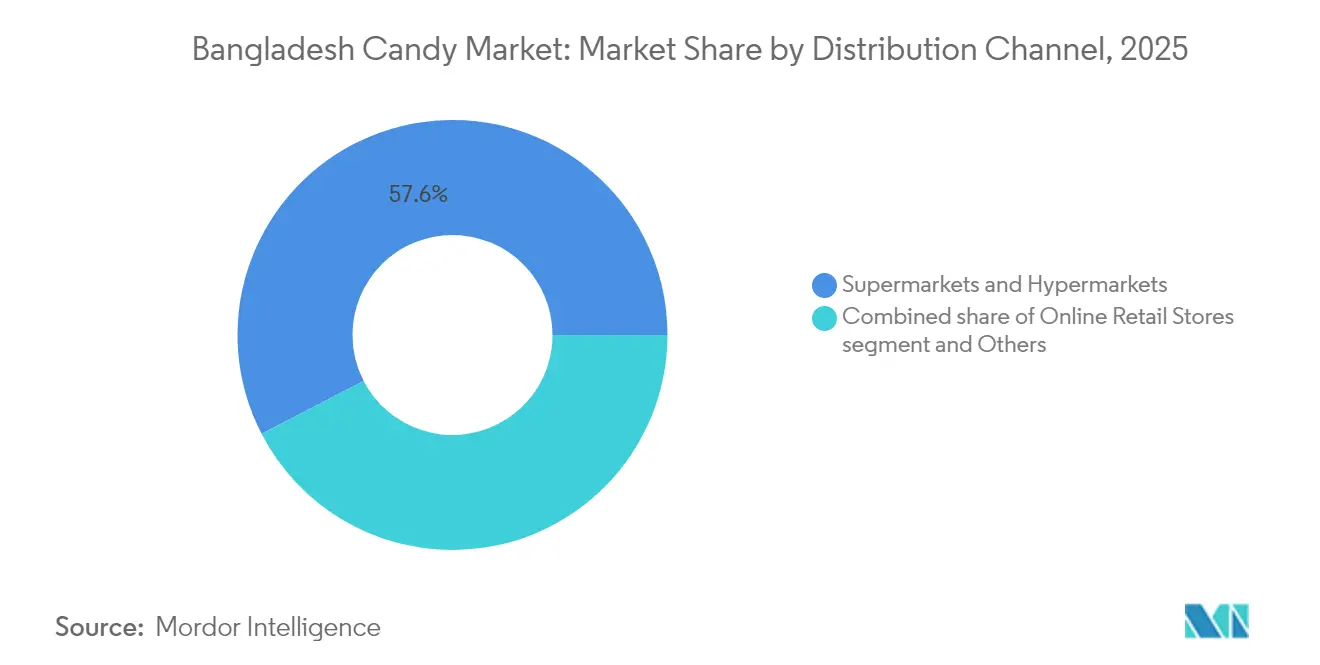

- By distribution channel, supermarkets and hypermarkets captured 57.60% revenue share of the candy market in 2025, whereas online retail is predicted to advance at a 5.34% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Bangladesh Candy Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising urban middle-class demand for affordable indulgence | +1.2% | National, concentrated in Dhaka, Chittagong, Sylhet | Medium term (2-4 years) |

| Expansion of modern retail chains and e-commerce | +0.8% | Urban centers with spillover to semi-urban areas | Long term (≥ 4 years) |

| Seasonal/festival-centric consumption spikes | +0.7% | National, with peaks in major cities during Eid, Durga Puja | Short term (≤ 2 years) |

| Product innovation with localized flavors and portion packs | +0.5% | National, with early adoption in metropolitan areas | Medium term (2-4 years) |

| Growth of sugar-free and functional candies | +0.4% | Urban areas with health-conscious demographics | Long term (≥ 4 years) |

| Duty-free raw-sugar import policy for exporters | +0.3% | National, benefiting export-oriented manufacturers | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising urban middle-class demand for affordable indulgence

By 2025, Bangladesh is poised to welcome 34 million middle-class consumers, solidifying a robust foundation for its candy market. Candy, often seen as a "small-ticket luxury," offers aspirational households a guilt-free indulgence, allowing them to experience premium experiences without significant financial strain. Research indicates that taste is the primary driver for 80.1% of confectionery purchases, with female shoppers playing a pivotal role in brand selection due to their influence on household buying decisions[2]Source: Journal of Bangladesh Agricultural University," Ice cream consumption in a selected area of Bangladesh: Effect of demographic, psychometric and product factors", www.ejmanager.com . Additionally, the growing middle-class population is expected to drive demand for affordable yet high-quality products, further boosting the candy market. While a significant 95.4% of university students indulge in sugar-sweetened beverages, a notable 94.5% are leaning towards healthier alternatives, hinting at a market ready for portion-controlled treats that align with evolving health-conscious preferences. These intertwined trends suggest a surge in demand, particularly for SKUs priced under USD 0.10, provided they're packaged to exude quality and appeal to value-conscious consumers. The combination of affordability, taste, and health-conscious options is likely to shape the market dynamics in the coming years.

Expansion of modern retail chains and e-commerce

Organized retail, a USD 18 billion industry expanding at an annual rate of 7.5%, is revolutionizing confectionery access for shoppers. Supermarkets, spearheaded by Shwapno's ambitious leap from 300 to 3,000 outlets, are enhancing shelf visibility, standardizing merchandising, and ensuring inventory reliability. This expansion not only increases consumer access to a wider variety of confectionery products but also fosters a more consistent shopping experience. In parallel, online platforms like Chaldal ramped up daily deliveries from 2,500 to 12,000 orders during the pandemic, underscoring the power of digital scalability and the growing preference for e-commerce. Urban youth's widespread adoption of mobile financial services is streamlining repeat confectionery purchases by reducing transactional barriers and improving convenience. Meanwhile, manufacturers benefit from real-time feedback on SKU adjustments through click-stream data, enabling them to respond swiftly to changing consumer preferences and market demands.

Seasonal/festival-centric consumption spikes

During Eid, Durga Puja, and wedding seasons, candy sales experience predictable peaks and troughs. Research highlights that festival calendars can triple unit sales for products like rasogolla, driven by increased consumer demand for gifting and celebratory consumption[3]Source: Asian Journal of Medical and Biological Research," Uses of milk in sweetmeat shops and consumer preferences to milk products at Mymensingh municipality in Bangladesh", www.banglajol.info . To tap into the gifting budgets, producers preload inventories and introduce festival-exclusive flavors or themed packaging, which appeal to cultural and festive sentiments. Additionally, producers often invest in marketing campaigns tailored to these occasions to further boost sales and brand visibility. However, these sales spikes also lead to challenges like factory overtime, packaging shortages, and trucking congestion. To address these issues, producers rely on advanced demand-forecast algorithms to optimize resource allocation, streamline production schedules, and ensure the timely delivery of products during high-demand periods. Furthermore, some companies collaborate with logistics partners to mitigate transportation bottlenecks and maintain supply chain efficiency during these critical seasons.

Product innovation with localized flavors and portion packs

Khondol Sweet's quest for Geographical Indication status underscores the commercial promise of safeguarding regional recipes, as it helps protect the unique identity and heritage of these products while enhancing their market value. The corporate sweetmeat industry, boasting an annual valuation of Tk 20,000 crore, showcases the potential when traditional recipes are paired with contemporary packaging, which appeals to modern consumer preferences. By introducing portion-controlled SKUs, the reach has expanded significantly; ENA Food & Beverage has customized pack sizes to fit micro-merchant budgets, successfully scaling to over 10,000 retail nodes. This approach not only increases accessibility but also caters to diverse consumer segments, including those in rural and urban areas. Additionally, the strategy of blending heritage recipes with modern branding ensures a competitive edge in a market where consumer expectations are rapidly evolving. The key to success lies in harmonizing authenticity, affordability, and convenience, ensuring that heritage products remain relevant in a competitive market.

Restraints Impact Analysis*

| Restraint | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile global sugar and cocoa prices | -0.9% | National, affecting all manufacturers | Short term (≤ 2 years) |

| Lack of cold-chain for summer chocolate distribution | -0.6% | National, more severe in rural areas | Medium term (2-4 years) |

| Rising health awareness toward sugar reduction | -0.5% | Urban areas with educated demographics | Long term (≥ 4 years) |

| Informal/unbranded sector price under-cutting | -0.4% | Rural and semi-urban markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Volatile global sugar and cocoa prices

In 2024, domestic sugar prices in Bangladesh ranged between Tk 105-120/kg, surpassing government-set caps and squeezing manufacturer margins. This price surge has placed significant pressure on both producers and consumers, highlighting inefficiencies in the supply chain and the impact of global market dynamics. While a proposed reduction in the refined-sugar duty to Tk 4,000/tonne aims to provide some relief, Bangladesh continues to rely on imports for the majority of its 2 million-tonne annual sugar requirement, leaving the market vulnerable to external shocks. Global commodity fluctuations, intensified by tariff-rate decisions from the U.S., introduce uncertainties that ripple down to wholesale candy prices, further complicating the situation. Larger firms mitigate risks through futures markets, leveraging their financial capacity to hedge against price volatility. In contrast, smaller players frequently bear the brunt of rising costs, often absorbing these expenses or resorting to shrinking pack sizes to maintain affordability for consumers.

Lack of cold-chain for summer chocolate distribution

When temperatures soar past 35 °C, transporting chocolate in unrefrigerated trucks becomes a significant challenge, jeopardizing its shelf life and diminishing the consumer experience. In response, Golden Harvest and IFC have launched a cold-chain joint venture in Bangladesh, backed by a USD 22 million investment. This initiative marks the country's first systematic approach to addressing the issue of temperature-sensitive logistics. However, the current capacity of this cold-chain infrastructure still falls short of meeting the rapidly growing demand. As the country continues to grapple with the need for nationwide refrigerated logistics, manufacturers are adapting their strategies. They are focusing on promoting chocolate sales during the cooler months when the risk of heat damage is lower or limiting their product offerings to SKUs specifically designed to withstand higher temperatures.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Non-Chocolate Dominance Amid Chocolate Acceleration

In 2025, non-chocolate varieties dominated the candy market, accounting for 63.10% of the market share. This stronghold not only bolstered overall revenues but also ensured the availability of economy-tier options. Spanning a diverse range of tastes, from toffees to mints, this segment seamlessly aligns with local festivities and caters to the purchasing power of lower-income groups. Manufacturers have adeptly leveraged domestic raw material sources and the segment's minimal refrigeration requirements, ensuring a stable year-round supply. Furthermore, strategic cross-promotions with refreshment drinks and the use of sachet packaging have amplified their presence in roadside kiosks, making them more accessible to the everyday consumer.

On the other hand, the chocolate segment is on an upward trajectory, boasting a 5.06% CAGR outlook. This growth signals a burgeoning momentum in the premium tier, hinting at potential shifts in future candy market size allocations. Urban millennials, influenced by social media and global confectionery trends, are increasingly drawn to impulse bars and curated gift assortments. In response to this trend, investments are pouring into advanced automated enrobing lines and cocoa-butter substitutes tailored for tropical climates. Yet, despite this momentum, summer sales face challenges without a robust cold-chain system, limiting the segment's full-year revenue potential.

By Ingredient Type: Sugar-Based Foundation with Health-Conscious Evolution

In 2025, sugar-based products commanded a dominant 82.00% share of the candy market, underscoring both established taste preferences and economic considerations. Strong ties with local sugar refiners and traditional sweetmeat artisans further cement this dominance. Brands consistently innovate, introducing new fruit flavors, stripes, and dual-color centers to maintain high engagement across diverse social groups. This segment benefits from its affordability, wide availability, and cultural significance, making it a staple choice for consumers across various demographics. Additionally, the long-standing presence of sugar-based candies in the market has fostered brand loyalty, further reinforcing their market position.

While starting from a modest base, sugar-free and low-calorie products are on the rise, boasting a 7.28% CAGR and prompting shifts in ingredient sourcing strategies. The inclusion of both artificial and natural sweeteners is broadening supplier portfolios, complicating quality control processes. These products cater to the growing health-conscious consumer base, addressing concerns about sugar intake and lifestyle diseases. Marketing strategies prominently feature endorsements from medical professionals and emphasize portion control, particularly in displays near pharmacies, to appeal to this segment of health-focused buyers. Furthermore, the increasing availability of these products in mainstream retail channels, alongside targeted advertising campaigns, is driving their adoption among a wider audience.

By Distribution Channel: Modern Retail Leadership with Digital Acceleration

In 2025, supermarkets and hypermarkets accounted for 57.60% of total turnover, leveraging organized displays and category management to drive unit sales. These retail formats provide a structured shopping experience, enabling consumers to easily navigate through various product categories. Promotions like buy-one-get-one offers and loyalty-card incentives boost basket sizes, encouraging repeat purchases and customer retention. Additionally, on-shelf data analytics play a critical role in guiding SKU rationalization, ensuring optimal product assortment and inventory management. These strategies collectively enhance operational efficiency and contribute to sustained revenue growth in this segment.

Online retail, projected to grow at a 5.34% CAGR, serves as the agile arm of the candy market. E-commerce platforms capitalize on consumer trends by offering timed flash sales, such as those on Ramadan evenings or with Durga Puja gift boxes, which drive significant volume spikes. Despite 90% of orders still relying on cash-on-delivery, the rising adoption of mobile wallets indicates a gradual shift towards smoother and more efficient fulfillment cycles. Furthermore, partnerships with micro-hubs are expanding rural last-mile coverage, enabling branded confectionery to penetrate villages that previously only accessed unbranded sweets. This development not only broadens market reach but also enhances brand visibility in underserved regions, creating new growth opportunities for the candy market.

Geography Analysis

In Bangladesh, the candy market is predominantly driven by Dhaka, Chittagong, and Sylhet. These cities, boasting higher incomes and a dense network of modern retail, are home to trend-setting consumers who significantly influence market dynamics. As a result, manufacturers are increasingly directing their billboard and social media campaigns towards these urban centers, where both purchase frequency and average selling prices are at their peak. These cities also serve as testing grounds for innovations, with cold-chain pilots being introduced here before a broader rollout to other regions.

Meanwhile, in the northern districts, there's a pronounced loyalty to traditional sweetmeats. This allegiance not only boosts the volume of sugar-based hard candies but also ensures these candies resonate with local flavors, catering to the cultural preferences of the population. Recent upgrades to the road network have cut delivery times for semi-urban clusters, allowing local marts to rotate their stock more frequently. However, these consumers remain highly price-sensitive, gravitating towards sachet SKUs priced below Tk 5, which cater to their affordability while maintaining product accessibility.

On the western and coastal fronts, there's a noticeable trend of early adoption of chocolate snacks. This shift is largely attributed to trade routes linked to ports, which have familiarized residents with imported brands and diversified their preferences. Furthermore, e-commerce platforms are bridging brand-awareness gaps, allowing coastal households to experience the same online selections as those in Dhaka. These regions are also emerging as strategic hubs for export activities, leveraging the Chittagong seaport to facilitate cross-border confectionery shipments and expand the market reach of local manufacturers.

Regulatory Landscape

Candy manufacturing, import, and sale in Bangladesh fall under the Bangladesh Food Safety Act, 2013, administered by the Bangladesh Food Safety Authority (BFSA), which frames national food safety standards and enforcement. For packaged confectionery in trade, the Bangladesh Standards and Testing Institution (BSTI) serves as a central compliance gatekeeper through mandatory standards and testing, while imported confectionery items (such as lozenges) require BSTI conformity certification under the Import Policy Order framework to access the legal market.

Standards activity has been active around core candy categories, with BSTI circulating draft revisions during 2026 for key confectionery standards, including BDS 490 (Hard Candy, fourth revision) and BDS 1498 (Chewing Gum, second revision). Bangladesh also used the WTO SPS channel in 2026 to notify a draft BDS 490 specification for hard candy, reinforcing hygienic requirements alongside packaging and marking rules, and tightening the focus on additive guidance and safety parameters (including heavy metals and microbiology) that manufacturers and importers need to embed into QA/QC and labeling processes.

Competitive Landscape

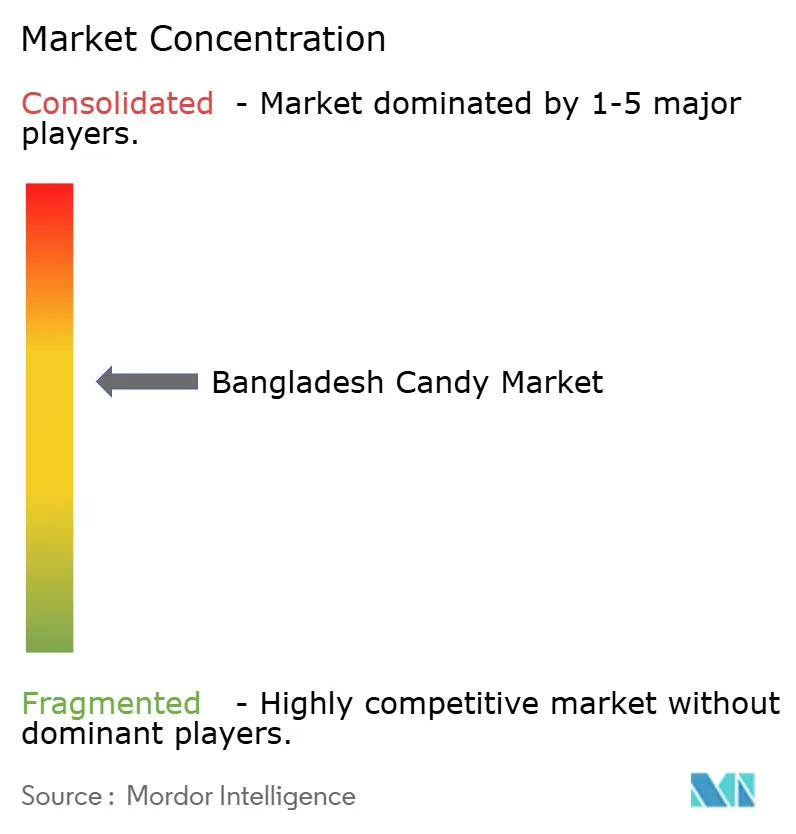

Bangladesh's candy market, with a moderate fragmentation score of 6 on the market-concentration scale, indicates potential for strategic mergers without hindering innovation. Local powerhouses like PRAN-RFL, Olympic Industries, and ACI Foods compete alongside global titans such as Nestlé, Mars Wrigley, and Perfetti Van Melle. While domestic players capitalize on extensive distribution networks, particularly in rural areas where accessibility is key, multinationals focus on premium positioning, leveraging their global expertise and robust research and development capabilities to introduce innovative products tailored to evolving consumer preferences.

Significant capital investments reflect a bullish outlook and long-term confidence in the market's growth potential. PRAN-RFL has allocated USD 22.5 million for new confectionery lines spread across 18 industrial parks, aiming at both urban markets and exports to strengthen its footprint domestically and internationally. Meanwhile, Akij Group's Tk 1,200 crore bakery initiative, launching the Bakeman's brand, heightens competition between biscuits and candies, signaling a strategic move to capture a larger share of the snack market. Foreign direct investments are also on the rise, highlighted by Coca-Cola İçecek's USD 130 million purchase of local bottling assets, which bolsters the potential for beverage and snack pairings, creating opportunities for cross-category synergies.

Digital tools are reshaping the supply chain landscape, driving efficiency and competitiveness. For instance, PriyoShop's platform connects corner shops with wholesalers, enabling dynamic pricing and swift 48-hour restocking, which is crucial for maintaining inventory in high-demand periods. Brands are leveraging predictive data to time their re-orders, ensuring optimal stock during festive surges and minimizing stockouts. In a market increasingly attuned to health and sustainability, features like recyclable wrappers, reduced sugar claims, and eco-friendly packaging are becoming key differentiators, helping brands align with the preferences of a health-conscious and environmentally aware consumer base.

Bangladesh Candy Industry Leaders

-

Perfetti Van Melle

-

Olympic Industries Limited

-

ACI Foods Limited

-

PRAN Rfl Group

-

Nestlé S.A.

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

A practical opportunity is capacity and capability upgrading that can reduce cost-to-serve and broaden the addressable range of formats, particularly for chocolate and gums that face heat and handling constraints. Olympic Industries actions in 2025-2026 illustrate this pathway. The company announced machinery imports to lift chocolate output capacity (3,300 tonnes annually), and it later secured expansion headroom through a board-approved land purchase adjacent to its Narayanganj factory (Tk 26.22 crore, 489.89 decimals). Alongside production scale, there is further room for cold-chain and temperature-resilient distribution to support broader year-round penetration of chocolate SKUs, building on the existing cold-chain joint venture in Bangladesh backed by a USD 22 million investment by Golden Harvest and IFC.

A second opportunity centers on export-enablement and compliance-led product modernization, where investments in hygiene controls, testing, and process automation help branded players differentiate versus the informal sector. Bangladesh Agricultural Development Corporation (BADC) inaugurated the country’s first Vapour Heat Treatment plant (Gabtoli, Dhaka, July 2026) to help exports meet phytosanitary expectations, indicating infrastructure build-out that can support wider processed-food export programs and upstream quality improvements. With BSTI advancing draft revisions in 2026 for hard candy and chewing gum standards (BDS 490 and BDS 1498), manufacturers can develop compliant sugar-free/low-calorie and functional lines with clearer labeling and safety assurance. These efforts can also be tested and rolled out faster through modern retail and e-commerce platforms (including Shwapno expansion and delivery scaling) across Dhaka, Chittagong, and Sylhet, and into semi-urban corridors.

Recent Industry Developments

- April 2026: Olympic Industries approved the purchase of 489.89 decimals of land adjacent to its Narayanganj factory for Tk 26.22 crore to support future expansion. The additional footprint strengthens the company’s ability to add new confectionery and snack lines and helps protect supply continuity during seasonal demand spikes.

- September 2025: Olympic Industries signed a Tk 50 crore loan agreement under the JICA-funded Food Value Chain Improvement Project to modernize and expand its Narayanganj plants. The financing supports plant upgrades that can raise throughput and improve process control, which is increasingly important as compliance expectations tighten for packaged confectionery.

- February 2024: Golden Harvest and IFC advanced a cold-chain joint venture in Bangladesh backed by a USD 22 million investment to build systematic refrigerated logistics. Expanded cold-chain capacity improves the feasibility of distributing heat-sensitive chocolate candies across warmer months and beyond the largest urban centers.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this report, the Bangladesh candy market is defined as the value of candy products sold for consumption within Bangladesh across retail and other trade channels, measured in USD for a consistent year-on-year view.

Scope exclusions: It excludes home-made or informal unregistered sales, and it also excludes adjacent snack categories such as biscuits, bakery confectionery, and ice cream.

Segmentation Overview

-

Product Type

- Chocolate Candy

-

Non-Chocolate Candy

- Hard Boiled Candies

- Pastilles, Gums, Jellies and Chews

- Others

-

By Ingredient Type

- Sugar-based

- Sugar-free/Low-calorie

-

By Distribution Channel

- Supermarkets/Hypermarkets

- Convenience Stores

- Online Retail Stores

- Other Distribution Channels

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to set the base structure of the model and to anchor assumptions that can be checked in public data. We referred to sources such as Bangladesh Bank and government statistical releases for macro indicators, customs or trade statistics for sweets and sugar confectionery flows, and FAO and other agriculture datasets to understand sugar and related input availability.

To keep the market view grounded, we also reviewed company annual reports and investor presentations where available, brand and distributor announcements in reputed press, and information published by local chambers or food industry associations. Alongside this, paid subscription sources for company financials and intelligence, and a separate paid patent database were used selectively to track product activity and cross-check scale where disclosures were limited. These sources are illustrative only, and many other public references were used for data collection, validation, and clarification during analysis.

Primary Interviews and Surveys

Primary work was carried out through expert interviews and structured surveys with manufacturers, importers and distributors, modern trade and traditional retail participants, and packaging and ingredient-linked stakeholders. The discussions covered Bangladesh-wide demand patterns, channel mix shifts, and price movements, so assumptions from desk research could be corrected and then triangulated across multiple viewpoints.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 26% | CXOs: 19% | APAC: 39% |

| Mid tier: 55% | Functional/Unit leaders: 34% | EMEA: 35% |

| Smaller Players: 19% | Managers: 47% | Americas: 26% |

Market-Sizing & Forecasting

Market sizing starts with a top-down build where the demand pool is reconstructed using Bangladesh consumer spend direction, confectionery and sugar-linked indicators, and the observed shift in channel availability, and then these totals are mapped to candy's addressable share. To make sure the result is not purely assumption-driven, we corroborated totals using selective bottom-up checks such as sampled brand and channel price points (ASP) multiplied by estimated sales throughput, plus distributor and retailer validation on typical sell-out ranges.

Key inputs used in the model include urbanization and income trends, population age mix that influences impulse buying, imported product availability in modern trade, online retail participation, and observed price pack architecture changes that affect realized ASP in local currency. Forecasting was done with scenario-based modeling supported by simple regression checks on the strongest drivers, and then adjusted using primary feedback on expected pricing, promotion intensity, and channel expansion. Where direct bottom-up visibility was weak, the gaps were handled by applying conservative conversion ratios that were re-tested through follow-up calls until the assumptions stayed stable.

Data Validation & Update Cycle

Validation is handled through a step-by-step triangulation process where the modeled market value is compared with independent signals such as category price movements, channel expansion cues, and trade flow direction, which helps flag unusual jumps early. If variances show up, the assumptions are unpacked and re-checked, and respondents are re-contacted when a mismatch is large or when one input is driving the model too strongly.

Before sign-off, the work is reviewed by another analyst who checks year alignment, unit consistency, and whether the logic matches the stated scope. The report is refreshed annually, and interim updates are made when material events occur, such as sudden currency shifts or tax and duty changes that can move retail pricing quickly. Right before delivery, we do a fresh review pass so clients receive the most current view available at that time.

Mordor Intelligence's Bangladesh Candy Market Estimate Compared With Other Published Estimates

Published market sizes for Bangladesh candy can differ even when they appear to cover the same category. The spread usually comes from how each study sets the year, currency handling, price logic, and how often the numbers are refreshed after major market changes.

In candy, small choices can move the total, such as whether prices are modeled at retail or ex-factory, how promotional pricing is normalized, and if a USD figure is converted using an annual average rate or a point-in-time rate. Refresh cadence also matters because quick changes in imported assortment, online sales share, and pack-size inflation can make an older ASP curve look too low or too high.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 0.94 B (2025) | |

| Industry Publisher A | USD 0.78 B (2025) | Often relies on broader confectionery proxies and a slower refresh cycle, which can understate recent retail price-pack shifts and the USD conversion effect during volatile periods. |

| Research Portal B | USD 0.74 B (2024) | Uses an earlier base year and may carry forward ASP growth with a simpler trend line, which can miss step-changes from duty, freight, and imported mix changes that impact realized prices. |

The table shows that timing and price handling explain most of the difference, more than any single demand factor. By re-checking ASP movements in local currency and then applying consistent USD timing during each annual refresh, Mordor Intelligence keeps the estimate closer to what trade participants report as current sell-in and sell-out reality. With a clear scope and repeatable steps, the result is easier to reconcile when new information becomes available.

Key Questions Answered in the Report

How large is Bangladesh’s candy market in 2026?

The candy market size stands at USD 987.9 million in 2026 and is forecast to reach USD 1.26 billion by 2031.

Which product segment leads sales?

Non-chocolate formats dominate with 63.10% share in 2025, reflecting deep cultural affinity and affordability.

What is the fastest-growing distribution channel for confectionery?

Online retail is expanding at a 5.34% CAGR as digital platforms extend delivery into semi-urban and rural districts.

Why are sugar-free candies gaining traction?

Rising diabetes prevalence and health awareness have lifted sugar-free and low-calorie product CAGR to 7.28%.

Page last updated on: