Technology, Media and Telecom

5th MayPricing Strategy for Semiconductor Components

3 Min Read

Ingestible Sensors Market Segmented by Component (Sensors, Wearable Patch / Data Recorder and More), Sensor Type (Temperature Sensor, Pressure Sensor and More). The Market Forecasts are Provided in Terms of Value (USD).

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

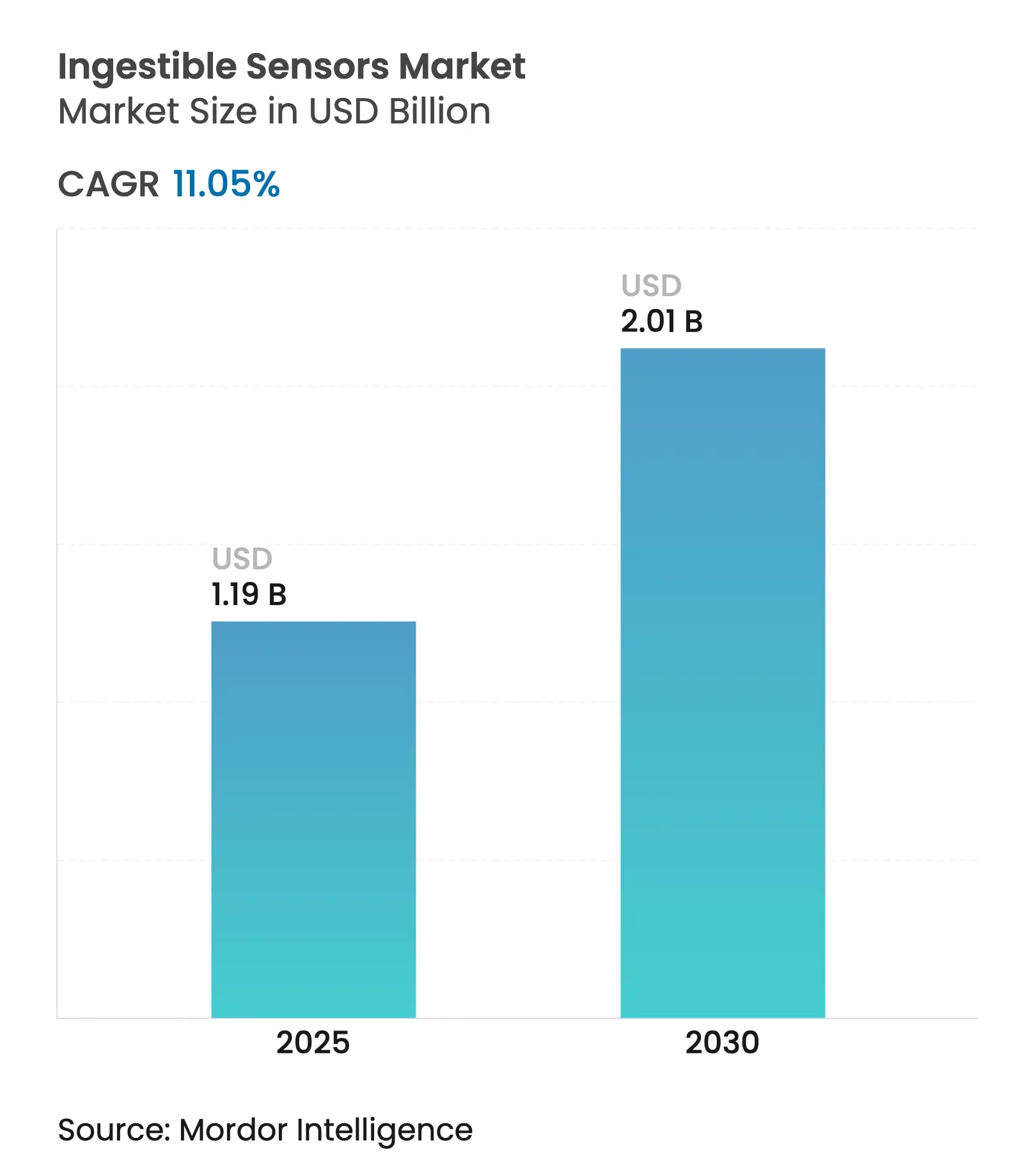

| Market Size (2025) | USD 1.19 Billion |

| Market Size (2030) | USD 2.01 Billion |

| Growth Rate (2025 - 2030) | 11.05 % CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order. Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

The ingestible sensors market size reached USD 1.19 billion in 2025 and is forecast to climb to USD 2.01 billion by 2030, reflecting an 11.05% CAGR. Strong momentum stems from advances in miniaturized electronics, expanded sensing modalities, and the healthcare sector’s pivot toward preventive, data-driven care. Integration of artificial intelligence with capsule-generated data is broadening real-time monitoring options for gastrointestinal disorders that once required invasive diagnostics. Regulatory clearances for digital pills are reducing market-entry barriers, while the spread of value-based reimbursement is pulling demand forward in North America and Europe. Venture funding for biosensing start-ups hit record levels in 2024, encouraging new entrants that target power efficiency and multi-parameter sensing. Nonetheless, battery capacity limits and heightened cybersecurity mandates are moderating the pace of product launches. [1] Imec, “Prototype of Ingestible Sensor Presented,” imec-int.com

Key Report Takeaways

Drivers Impact Analysis

| Driver | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Reimbursement Expansion for Digital Pills across OECD Reimbursement Expansion for Digital Pills across OECD | +2.1% | North America and Europe | Medium term (2-4 years) | % Impact on CAGR Forecast :+2.1% | Geographic Relevance :North America and Europe | Impact Timeline :Medium term (2-4 years) |

Pharma-led Push for Dose Adherence Platforms in North America Pharma-led Push for Dose Adherence Platforms in North America | +1.8% | North America | Short term (≤ 2 years) | |||

Miniaturised ASIC Advances Lowering Capsule Power Demand Miniaturised ASIC Advances Lowering Capsule Power Demand | +1.5% | Global | Medium term (2-4 years) | |||

CE-mark Surge for In-body Telemetry Modules in EU CE-mark Surge for In-body Telemetry Modules in EU | +1.3% | Europe | Short term (≤ 2 years) | |||

Large GI Disorder Patient Pools in APAC Driving Demand Large GI Disorder Patient Pools in APAC Driving Demand | +1.7% | Asia-Pacific | Medium term (2-4 years) | |||

Venture Investments in Biosensing Start-ups (2023-24 record high) Venture Investments in Biosensing Start-ups (2023-24 record high) | +1.2% | North America and Europe | Medium term (2-4 years) | |||

| Source: Mordor Intelligence | ||||||

Reimbursement Expansion for Digital Pills across OECD

Broader reimbursement in major OECD health systems is reinforcing predictable revenue streams for ingestible monitoring solutions. Payers link coverage to the long-term cost savings that accrue when chronic-disease patients adhere to therapy, prompting formularies to incorporate digital pills as standard options [ema.europa.eu]. Qualification of adherence sensors as valid biomarkers in European clinical trials further accelerates uptake. Hospitals now embed capsule-based adherence metrics in outcome-based contracts, anchoring demand that goes beyond early technology adopters. The resulting pull-through is expected to keep the ingestible sensors market on its double-digit growth path. [2]European Medicines Agency, “Qualification Opinion on Ingestible Sensor System for Medication Adherence,” ema.europa.eu

Pharma-led Push for Dose Adherence Platforms in North America

Pharmaceutical firms are embedding ingestible tags into legacy drugs to collect real-world evidence, defend pricing, and extend patent life. The FDA pathway opened by Abilify MyCite legitimized drug-device combinations, prompting others to invest heavily in similar programs. Digital ingestion data support differentiated labelling, which commands premium reimbursements and offsets the USD 100-300 billion annual burden of non-adherence. These industry moves solidify a commercial end-market that anchors early-stage sensor suppliers, sustaining the ingestible sensors market despite cyclical funding swings.

Miniaturized ASIC Advances Lowering Capsule Power Demand

Recent ASIC breakthroughs cut active-mode power draw, lengthening operational time without enlarging form factors. A University of California self-powered capsule using a glucose biofuel cell exemplifies how energy harvesting can replace conventional batteries. Lower power budgets also let engineers stack temperature, pH, pressure, and imaging modules in one shell, enhancing diagnostic depth. As energy density improves further, multi-day monitoring becomes realistic, widening the ingestible sensors market to indications that need continuous data streams.

CE-mark Surge for In-body Telemetry Modules in EU

Europe’s regulatory climate favours rapid approval of digital therapeutics that shrink hospital stays and enable remote care. The rise in CE-marked telemetry capsules shortens the gap between prototype and commercial roll-out, giving European clinicians early access to next-generation devices. Investors, noting smoother market entry, are channelling capital to regional start-ups, reinforcing Europe’s role as an innovation hub within the ingestible sensors market.

Restraints Impact Analysis

| Restraint | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

FDA Cyber-device Guidance Creating Data-Security Hurdles FDA Cyber-device Guidance Creating Data-Security Hurdles | -1.3% | North America | Short term (≤ 2 years) | % Impact on CAGR Forecast :-1.3% | Geographic Relevance :North America | Impact Timeline :Short term (≤ 2 years) |

Limited Capsule Battery Life Restricts Multi-Parameter Sensing Limited Capsule Battery Life Restricts Multi-Parameter Sensing | -1.6% | Global | Medium term (2-4 years) | |||

Mixed Clinical Evidence on Outcome Benefits for Payors Mixed Clinical Evidence on Outcome Benefits for Payors | -0.9% | Global | Medium term (2-4 years) | |||

High One-time Procedure Costs in Emerging Countries High One-time Procedure Costs in Emerging Countries | -0.8% | Asia-Pacific, Middle East and Africa | Long term (≥ 4 years) | |||

| Source: Mordor Intelligence | ||||||

FDA Cyber-device Guidance Creating Data-Security Hurdles

Stricter 2024 cybersecurity rules obligate ingestible sensors to embed multi-layer encryption and real-time threat monitoring across their entire ecosystem [irp.nih.gov]. Meeting these standards strains power budgets and prolongs verification cycles. Smaller innovators face longer design-freeze periods and higher certification costs, tilting competitive advantage toward established firms. While the measures improve patient data integrity, they can momentarily decelerate market arrivals, dampening near-term ingestible sensors market growth projections. [3]U.S. Food and Drug Administration, “Evaluation of Automatic Class III Designation (De Novo) for Proteus Personal Monitor,” accessdata.fda.gov

Limited Capsule Battery Life Restricts Multi-Parameter Sensing.

Constrained energy storage forces designers to trade-off between sampling frequency, imaging illumination, and transmission range. Image sensors, in particular, deplete charge quickly, usually limiting imaging capsules to less than 24 hours of operation [sciencedirect.com]. Emerging biofuel and energy-harvesting approaches are promising but not yet scaled for mass production. Until breakthroughs reach commercial maturity, the ingestible sensors market will continue to under-serve use cases that demand week-long data capture or high-resolution video streams.

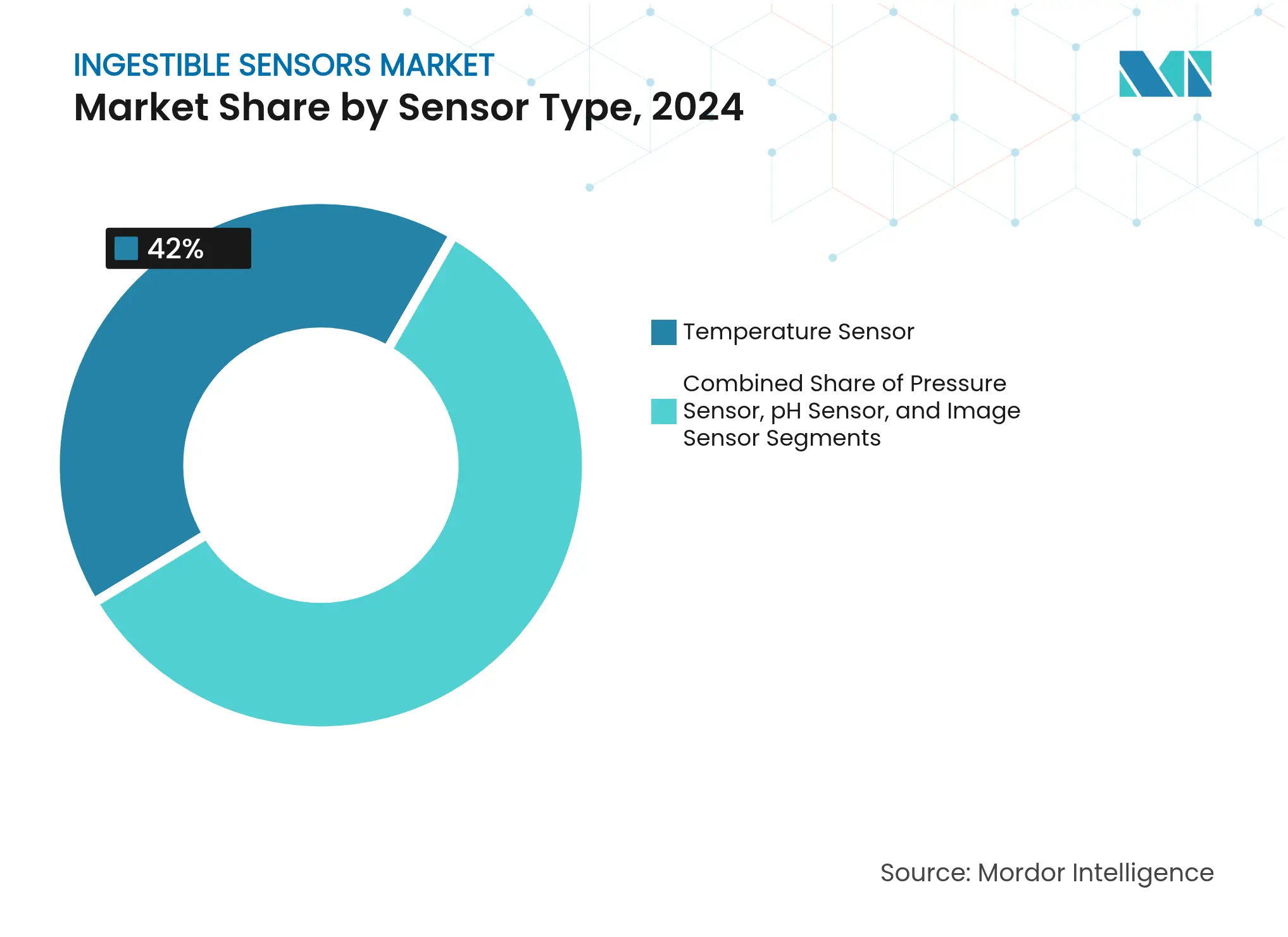

By Sensor Type: Temperature Monitoring Retains Primacy

Temperature sensors contributed 42% of the ingestible sensors market in 2024, a position earned through validated accuracy and low power demand [sciencedirect.com]. Sports medicine, military readiness, and perioperative care rely on these capsules to avert heat stress and monitor core temperature trends. The ingestible sensors market size for temperature devices is projected to expand steadily on the back of sports league protocols that mandate continuous thermal monitoring during training blocks. Imaging capsules, despite a smaller base, are set to grow fastest at 13.8% CAGR through 2030, benefitting from miniaturized optics and expanding reimbursement for capsule endoscopy.

Image-enabled devices elevate non-invasive detection of bleeding, polyps, and Crohn’s lesions, thus attracting gastroenterologists who seek to avoid sedation and endoscopic complications. Medtronic’s PillCam Genius SB demonstrates how AI-assisted image sorting can reduce physician reading time while capturing tens of thousands of mucosal pictures [news.medtronic.com]. Pressure and pH modules address motility disorders and acid reflux; recent prototypes such as PressureCap integrate multiple strain gauges without inflating capsule diameter [cell.com]. Cross-modality designs that embed all three sensor types may unlock premium pricing once battery innovations alleviate power constraints.

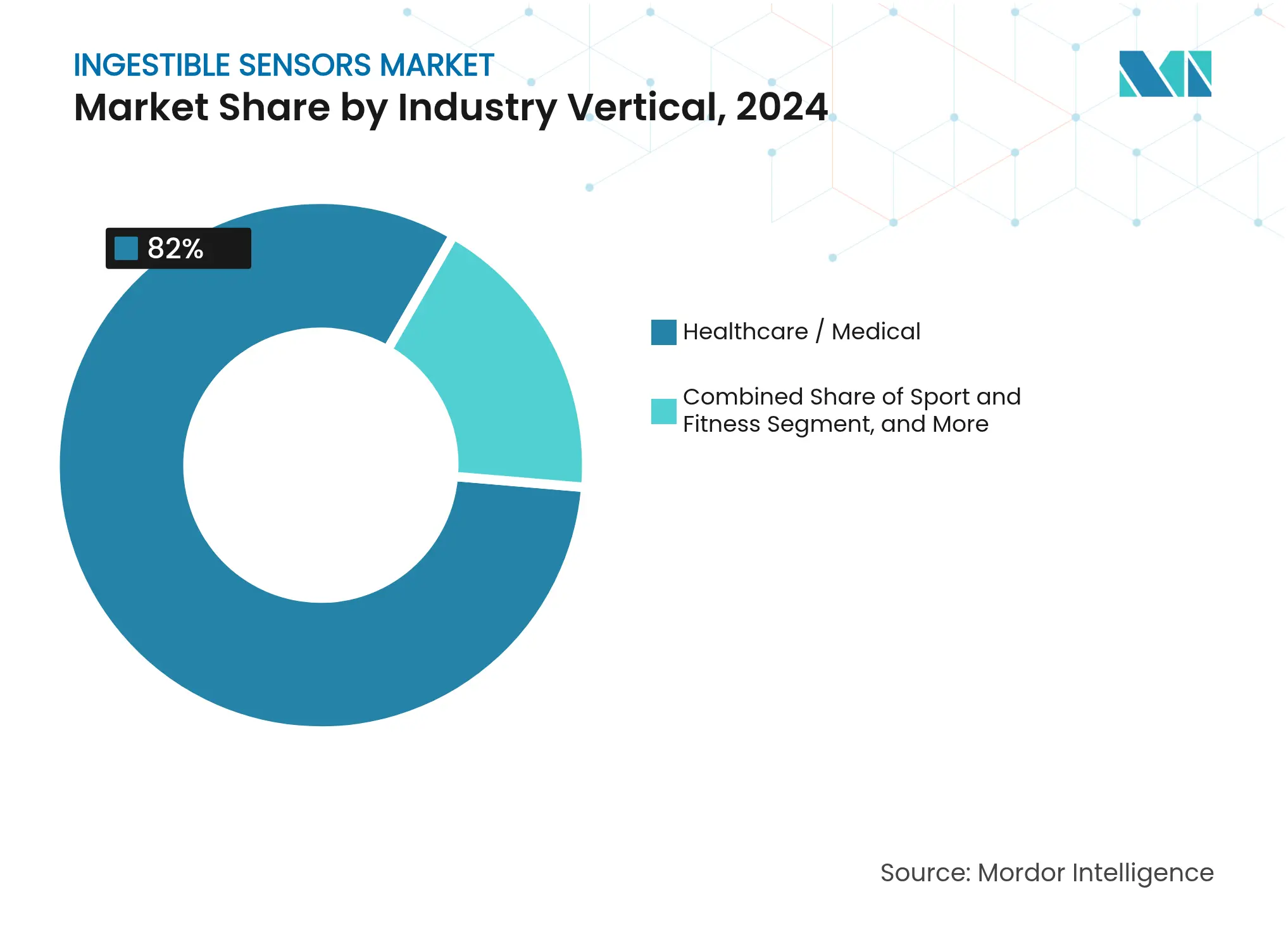

By Industry Vertical: Hospitals Dominate, Sports Accelerates

Healthcare facilities accounted for 86% of the ingestible sensors market revenue in 2024, using capsules for medication adherence audits, bleeding localization, and inflammatory bowel disease assessment. The ingestible sensors market size tied to hospital deployment is forecast to keep growing as clinical guidelines shift endoscopy volumes toward less invasive capsule pathways. Adherence modules, cleared by the FDA for antipsychotics and antivirals, show compliance rates approaching 99%, supporting payer adoption in value-based contracts.

Elite sports teams and military organizations, though a smaller slice, form the fastest-growing customer base at a 14.2% CAGR. Thermal capsules worn by endurance athletes during events like the Olympics safeguard participants from exertional heat stroke and optimize hydration regimens. Integration with wearable heart-rate straps and cloud analytics produces a holistic training dashboard, enticing high-performance coaching staffs. Over time, consumer fitness programs may adopt simplified versions, extending the ingestible sensors market beyond professional cohorts.

By Component: Sensor Hardware Still Leads but Software Gains Traction

Capsule sensors remain the value anchor of the ingestible sensors market, as each new generation delivers higher sensitivity and added modalities without significant cost inflation. Flexible pressure arrays and electrochemical gas sensors from university spinouts illustrate the rapid pace of core hardware innovation. Nonetheless, the software and analytics layer are capturing a rising revenue share because clinicians need decision-support insights rather than raw waveforms. Oracle’s collaboration to merge ingestible data with clinical-trial management suites shows how cloud algorithms can expand addressable use cases.

Analytics platforms employ machine learning to flag abnormal pH swings, micro-bleeds, or skipped doses in real time, thereby broadening the ingestible sensors market from episodic diagnostics to continuous care coordination. Meanwhile, wearable receiver patches evolve in parallel, offering Bluetooth LE connectivity and multi-day battery life to relay capsule telemetry securely to smartphones.

Recognized by Experts. Trusted by Leaders.

A trusted intelligence partner to global decision-makers across 90+ countries.

By End-user: Hospitals Hold the Lion’s Share, Home Healthcare Expands

Hospitals and ambulatory surgical centers accounted for the largest end-user share in 2024, owing to the procedural nature of capsule endoscopy and the need for immediate clinical interpretation. These institutions integrate ingestion events into electronic medical records, streamlining interdisciplinary workflows. Research institutes, though smaller, generate pivotal safety and efficacy data that propel regulatory filings.

Home healthcare constitutes the fastest-rising end-user segment as telehealth platforms normalize remote diagnostics. The ingestible sensors market benefits when patients can swallow a diagnostic capsule at home and upload data via a companion smartphone app, reducing clinic bottlenecks and travel burdens. Medtronic’s at-home PillCam kit showed that remote protocols maintain image quality while boosting patient satisfaction. Wider broadband access and secure cloud infrastructure will likely accelerate this shift, broadening market reach to underserved populations.

By Function: Monitoring Leads, Targeted Drug Delivery Emerges

Monitoring and adherence capsules still comprise the majority of functional deployments, driven by strong evidence that objective ingestion records improve therapeutic outcomes in HIV, tuberculosis, and hypertension management [sciencedirect.com]. The ingestible sensors market size for monitoring functions is projected to retain top billing through 2030 as payers embed adherence metrics in reimbursement formulas. Imaging capsules extend monitoring to structural pathologies, enabling clinicians to survey the entire small bowel without sedation.

Targeted drug-delivery capsules, although nascent, are attracting intense RandD interest. Magnetically actuated microneedle arrays that release biologics at predefined gut locations have shown promise in Crohn’s models. Closed loop designs that sense pH or redox markers and then trigger drug release could reshape therapy for ulcerative colitis, positioning the ingestible sensors market at the convergence of diagnostics and therapeutics.

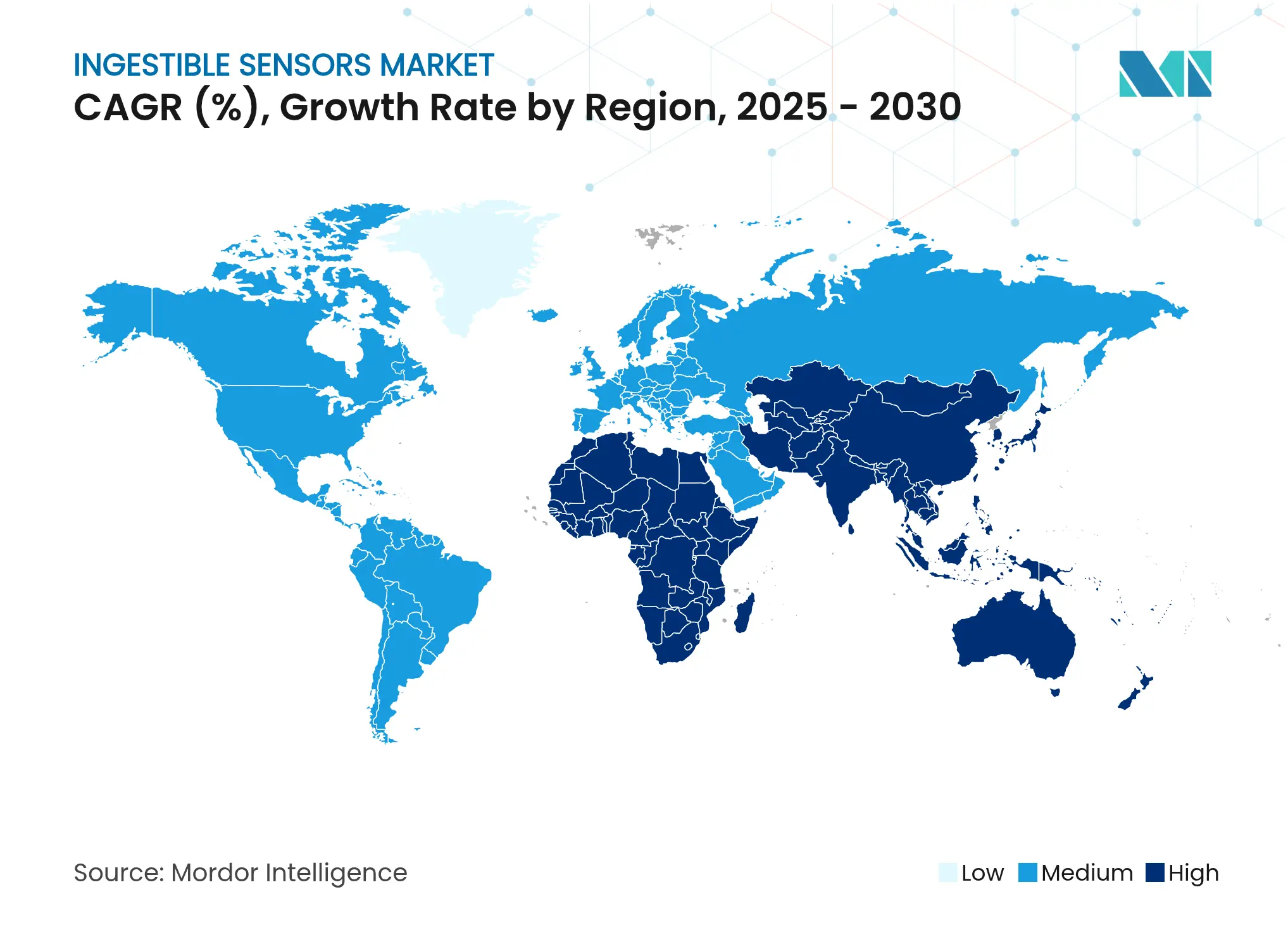

North America commanded 40% of ingestible sensors market revenue in 2024, underpinned by payer reimbursement for digital pills, strong venture funding, and a supportive FDA De Novo pathway [accessdata.fda.gov]. Hospital systems deploy adherence capsules to curb costly readmissions, while pharmaceutical companies leverage real-world ingestion data to negotiate formulary placements. Regional academic centers also run early-feasibility trials that validate next-generation sensing modalities.

Asia-Pacific is forecast to chart a 14.5% CAGR from 2025 to 2030, the fastest worldwide. Japan’s aging population and China’s large burden of gastrointestinal disorders create a sizable addressable base. Domestic manufacturers introduce cost-optimized capsules that align with regional purchasing power, while national digital-health strategies encourage remote monitoring adoption. Government insurance in markets such as South Korea has begun considering capsule endoscopy reimbursement, further stimulating demand.

Europe retains a notable share of the ingestible sensors market, leveraging its CE-mark system, which grants earlier access to innovative telemetry capsules. Public-sector programs emphasize preventive care, aligning with non-invasive diagnostics. Increased venture funding in Germany and the Nordics supports start-ups pursuing self-powered sensors and biodegradable housings. Meanwhile, Middle East and Africa and South America together represent a small but rising opportunity; private hospitals in the Gulf Cooperation Council and Brazil are early adopters, especially for capsule endoscopy in premium care packages.

Market Concentration

The ingestible sensors market is moderately consolidated. Medtronic maintains a leadership position through its PillCam family, backed by a global sales infrastructure and expansive clinical evidence base. Olympus and CapsoVision leverage optical expertise to compete in imaging, while Boston Scientific explores synergistic applications in gastrointestinal interventions. Established firms wield regulatory and manufacturing scale advantages, enabling them to navigate stringent cybersecurity mandates more readily than start-ups.

Data analytics capability has become a prime differentiation lever. Proprietary AI models that filter and classify thousands of capsule images per procedure help reduce physician reading time and identify lesions early. Companies are amassing wide patent portfolios that blend hardware, firmware, and software claims, creating high entry barriers. Over 500 patents tied to digital health capsules were filed by top players through 2024, indicating escalating intellectual-property intensity.

Partnerships between device makers and pharmaceutical firms are expanding. Otsuka’s investment in sensor-enabled antipsychotics illustrates how co-development can secure drug-device exclusivity that stretches market exclusivity timelines. University spinouts push the technology frontier on self-powered sensing and reversible anchoring mechanisms, while established companies focus on late-stage clinical validation and payer engagement. Over the forecast horizon, competition is expected to shift toward demonstrating verifiable outcome improvements and integration within broader remote-care ecosystems.

*Disclaimer: Major Players sorted in no particular order

1. INTRODUCTION

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET LANDSCAPE

5. MARKET SIZE AND GROWTH FORECASTS (VALUE)

6. COMPETITIVE LANDSCAPE

7. MARKET OPPORTUNITIES AND FUTURE OUTLOOK

Market Definitions and Key Coverage

Our study defines the ingestible sensors market as all swallowable, biocompatible electronic capsules that house micro-sensors, a power source, and short-range telemetry to capture variables such as temperature, pH, pressure, or images and transmit them to an external receiver for human diagnostic, adherence-monitoring, or therapy-trigger applications.

Scope exclusion: Animal-health devices and placebo capsules without electronics are kept outside this assessment.

Segmentation Overview

Detailed Research Methodology and Data Validation

Primary Research

We speak with gastroenterologists, biomedical engineers, elite-sport trainers, and supply managers across North America, Europe, and Asia Pacific. Their feedback on typical selling prices, procedure mix shifts, and regulatory timelines closes data gaps and fine-tunes assumptions surfaced during desk work.

Desk Research

Our team screens open datasets from CMS procedure files, Eurostat hospital activity logs, and Japan's MHLW white books, then layers UN Comtrade flows of sensor-grade chips to benchmark global supply. Journals indexed on PubMed outline capsule failure rates that affect replacement demand, while company splits from D&B Hoovers, Dow Jones Factiva, and 10-K filings ground revenue shares in reality. These examples illustrate, not exhaust, the secondary sources reviewed.

Market-Sizing & Forecasting

The model starts with a top-down reconstruction that marries annual capsule endoscopy counts, medication-non-adherence prevalence, and core-temperature monitoring usage. Supplier roll-ups of shipped units multiplied by blended ASPs validate totals. Key inputs include chronic GI disorder incidence, reimbursement tariffs, sensor cost curves, hospital device penetration, and regional approval tallies. A multivariate regression on these drivers projects 2025-2030 outcomes; bottom-up gaps are adjusted where export data diverge from modeled consumption.

Data Validation & Update Cycle

Mordor analysts run multi-step variance checks, flag outliers, and reconfirm anomalies with sources before sign-off. Models refresh each year, with interim updates if recalls, reimbursement changes, or major M&A events occur.

Why Mordor's Ingestible Sensors Baseline Inspires Confidence

Benchmark comparison

Published estimates differ because scopes, base years, and price assumptions vary.

By restricting coverage to medical-grade capsules and refreshing inputs every twelve months, Mordor trims such noise. Key gap drivers elsewhere include scope creep into veterinary pills, reliance on single-year ASPs, and omission of adherence-monitoring devices, all of which understate the market's true scale.

| Market Size | Anonymized source | Primary gap driver | ||

|---|---|---|---|---|

USD 1.19 B (2025) | Mordor Intelligence | - | Anonymized source:Mordor Intelligence | Primary gap driver:- |

USD 1.12 B (2025) | Global Consultancy A | Excludes sports-temperature capsules, constant ASPs | ||

USD 0.89 B (2023) | Industry Journal B | Older base year, leaves out adherence pills |

Pricing Strategy for Semiconductor Components

3 Min Read

Accelerating Additive Manufacturing Adoption in India

3 Min Read

Unlocking Saudi Arabia’s Regional Tourism Growth Potential

5 Min Read

When decisions matter, industry leaders turn to our analysts. Let’s talk.