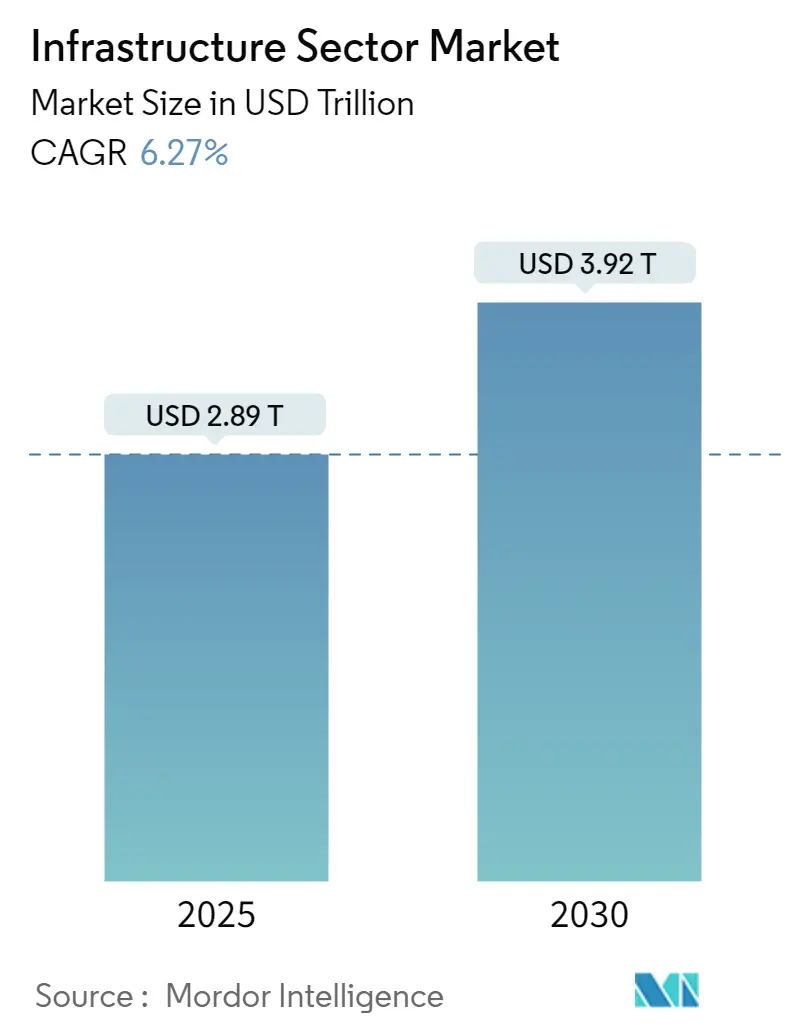

Infrastructure Construction Market Size

Market Overview

| Study Period | 2020 - 2030 |

| Market Size (2025) | USD 2.89 Trillion |

| Market Size (2030) | USD 3.92 Trillion |

| Growth Rate (2025 - 2030) | 6.27% CAGR |

| Fastest Growing Market | North America |

| Largest Market | Asia-Pacific |

| Market Concentration | Low |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Infrastructure Construction Market Analysis

The Infrastructure Sector Market size is estimated at USD 2.89 trillion in 2025, and is expected to reach USD 3.92 trillion by 2030, at a CAGR of 6.27% during the forecast period (2025-2030).

The infrastructure industry is witnessing a fundamental shift toward sustainable infrastructure development and environmental consciousness, driven by increasing global climate commitments. Over 30 regions and 700 cities worldwide have joined the United Nations' Race to Zero campaign, demonstrating a strong commitment to reducing carbon emissions to zero by 2050. This transition is particularly crucial as infrastructure construction and operations account for approximately 70% of all carbon emissions, primarily through energy and transport sectors and the production of materials like cement and steel. The industry is responding through increased adoption of cleaner infrastructure technology in public infrastructure projects and a growing focus on renewable energy integration.

Technology adoption is revolutionizing infrastructure development, with artificial intelligence, robotics, and drone technology emerging as key enablers of operational efficiency. The industry is experiencing accelerated digitalization, particularly in preventative maintenance, inspections, and repair assessments. Cloud-based technologies and digital infrastructure have become essential components, driving demand for robust data transmission and storage assets, including fiber networks, edge data centers, and telecommunication towers. This digital transformation is fundamentally changing how infrastructure assets are designed, built, and maintained.

Investment patterns in infrastructure are evolving, with sovereign wealth funds and public pensions playing an increasingly significant role. In 2021, these institutions directly invested USD 36.4 billion in infrastructure projects, marking a substantial increase in private sector participation. Notable developments include Saudi Arabia's launch of a USD 53 billion national infrastructure fund in October 2021, advised by BlackRock, targeting critical sectors such as water, transportation, energy, and health over the next decade. This trend reflects a growing recognition of infrastructure investment as a stable, long-term investment opportunity.

The modernization of existing infrastructure while developing new sustainable infrastructure assets has become a critical focus area for governments and private investors alike. In the Middle East and North Africa (MENA) region alone, experts estimate that spending of at least 8.2% of GDP will be needed to meet infrastructure goals by 2030. This modernization drive encompasses various sectors, from traditional transportation and energy infrastructure to advanced digital infrastructure networks and smart city initiatives. The industry is witnessing a shift toward more resilient and adaptable infrastructure designs that can accommodate future technological advancements and changing environmental conditions.

Infrastructure Construction Market Trends

Rising Infrastructure Development and Government Initiatives

Governments worldwide are implementing ambitious infrastructure development programs to boost economic growth and enhance connectivity. The scale of infrastructure investment required globally is massive, with estimates indicating that more than USD 2 trillion worth of investments in transportation infrastructure alone will be needed annually until 2040 to fuel economic development. This unprecedented level of investment is being channeled through various government initiatives and development programs designed to modernize existing infrastructure and create new assets. For instance, the Indian government has expanded its National Infrastructure Pipeline (NIP) to include 7,400 projects, focusing on critical sectors such as roads, housing, urban development, railroads, and renewable energy.

The commitment to infrastructure development is evident in the substantial budgetary allocations by various governments. The Philippines government has demonstrated this through a significant infrastructure push, allocating USD 6.5 billion specifically for bridge construction, flood management, asset preservation, and transportation network development. Additionally, a separate allocation of USD 1.3 billion has been dedicated to rail transportation, land public transportation, and maritime infrastructure development. These initiatives reflect the growing recognition among policymakers that robust public infrastructure is fundamental to achieving sustainable economic growth and improving the quality of life for citizens.

Rapid Urbanization and Economic Growth

The accelerating pace of urbanization across the globe has emerged as a significant driver for urban infrastructure development, particularly in emerging economies. This demographic shift is creating unprecedented demand for new and improved infrastructure facilities, from transportation networks to utility systems. The impact is particularly visible in the aviation sector, where countries are rapidly expanding their airport infrastructure to meet growing urban mobility needs. For example, China has demonstrated remarkable progress in airport infrastructure development, increasing its number of certified transport airports to 241, with 114 airport construction projects either initiated or continued during recent years.

The economic implications of urbanization are compelling governments and private sector entities to invest in infrastructure development. This is evidenced by initiatives such as the Federal Aviation Administration's (FAA) allocation of more than USD 479 million for airport infrastructure improvements across 123 projects in the United States. The focus extends beyond aviation to include comprehensive urban infrastructure development, encompassing public transportation systems, smart city initiatives, and sustainable urban planning projects. These investments are crucial for maintaining economic competitiveness and ensuring the efficient movement of goods and people in increasingly densified urban environments.

Growing Foreign Direct Investment and Private Sector Participation

The infrastructure sector is witnessing increased participation from foreign investors and private sector entities, driven by favorable government policies and improved investment frameworks. Countries across Asia-Pacific have maintained steady foreign direct investment (FDI) inflows, particularly in infrastructure development projects, despite global economic uncertainties. This trend is supported by government initiatives to streamline bureaucratic processes, simplify land acquisition procedures, and enhance transparency in project implementation, making infrastructure investments more attractive to international investors.

The evolution of infrastructure financing models has played a crucial role in attracting private infrastructure sector participation. Governments are increasingly adopting public-private partnership (PPP) models and creating specialized infrastructure investment vehicles to facilitate private sector engagement. This is complemented by efforts to reduce implementation delays and bureaucratic hurdles, which have historically been major deterrents to private investment in infrastructure projects. The focus on creating transparent and efficient project execution frameworks has helped build investor confidence and enabled the mobilization of significant private capital for infrastructure development. These developments are particularly significant in emerging economies where public resources alone are insufficient to meet the growing infrastructure needs.

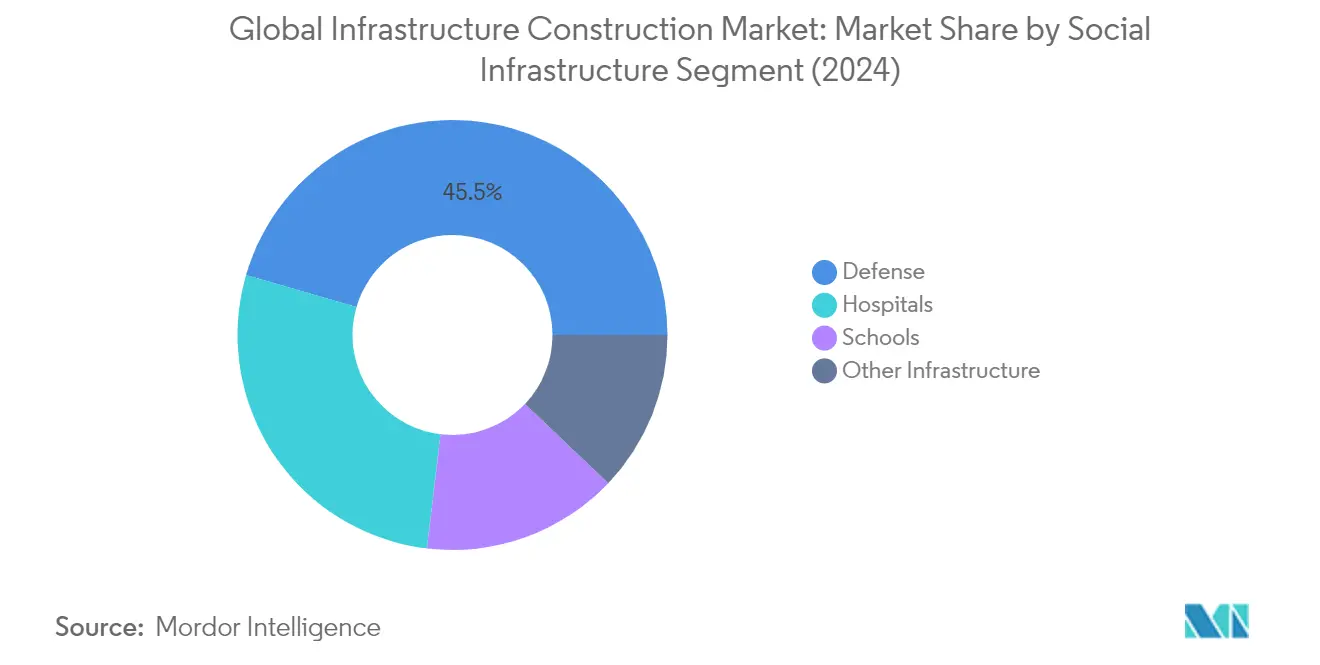

Segment Analysis: Social Infrastructure

Defense Segment in Global Infrastructure Construction Market

The defense segment has emerged as the dominant force in the global infrastructure construction market, commanding approximately 46% market share in 2024, with revenues reaching USD 222.1 billion. This segment's prominence is driven by increasing global security concerns and the modernization of military infrastructure across major economies. The defense infrastructure sector encompasses critical facilities including military bases, training facilities, command centers, and specialized defense research establishments. Governments worldwide are investing heavily in upgrading existing defense infrastructure and developing new facilities to meet evolving security challenges and technological requirements. The segment also demonstrates robust growth potential, with significant investments being channeled into smart military installations, cybersecurity infrastructure, and advanced defense research facilities.

Hospitals Segment in Global Infrastructure Construction Market

The hospitals segment represents a vital component of social infrastructure development, accounting for approximately 28% of the market in 2024. This sector encompasses the construction and renovation of healthcare facilities, including general hospitals, specialized medical centers, and emergency care units. The segment's growth is primarily driven by the increasing healthcare needs of aging populations, advancements in medical technology requiring modern facilities, and the ongoing focus on strengthening healthcare infrastructure post-pandemic. Healthcare facilities are increasingly being designed with future-ready capabilities, incorporating features like modular construction, infection control measures, and smart hospital technologies. The segment continues to attract substantial public and private investments, particularly in developing regions where healthcare infrastructure gaps need to be addressed.

Remaining Segments in Social Infrastructure

The social infrastructure market is further segmented into schools and other infrastructure components, which together play a crucial role in community development. The schools segment focuses on educational infrastructure, including primary and secondary schools, universities, and vocational training centers, emphasizing modern learning environments and digital integration. The other infrastructure category encompasses various social amenities such as community centers, recreational facilities, and public service buildings. These segments are experiencing significant transformation with the integration of sustainable building practices, digital technologies, and flexible space utilization concepts, reflecting changing social needs and environmental considerations.

Segment Analysis: Transportation Infrastructure

Airports Segment in Transportation Infrastructure Market

The airports segment has emerged as the dominant force in the global transportation infrastructure market, commanding approximately 39% market share in 2024, with a value of around USD 349.3 billion. This significant market position is driven by the increasing need for airport modernization and expansion projects worldwide to accommodate growing air traffic demands. Major economies are investing heavily in upgrading their aviation infrastructure, including terminal expansions, runway improvements, and smart airport technologies. The segment's growth is particularly strong in the Asia-Pacific region, where rapid urbanization and rising middle-class populations are driving demand for air travel infrastructure.

Ports Segment in Transportation Infrastructure Market

The ports segment is demonstrating remarkable growth potential in the transportation infrastructure market, with an expected growth rate of approximately 8% during the forecast period 2024-2029. This accelerated growth is driven by increasing maritime trade volumes, the need for port modernization, and the integration of smart technologies in port operations. Investments in automated container terminals, digital port management systems, and sustainable port infrastructure are becoming increasingly prevalent. The segment is also benefiting from various government initiatives worldwide to enhance port capacity and efficiency, particularly in emerging economies where maritime trade plays a crucial role in economic development.

Remaining Segments in Transportation Infrastructure

The transportation infrastructure market encompasses several other vital segments including railways, roadways, and waterways, each playing a crucial role in the global transportation network. The railways segment continues to be a cornerstone of public transportation infrastructure, with significant investments in high-speed rail networks and urban transit systems. The roadways segment remains fundamental to ground transportation, focusing on sustainable and smart highway systems. The waterways segment, while smaller in market share, is essential for inland water transportation and continues to see modernization efforts for more efficient cargo movement and reduced environmental impact.

Segment Analysis: Extraction Infrastructure

Oil and Gas Segment in Global Infrastructure Construction Market

The Oil and Gas segment continues to dominate the global infrastructure construction market's extraction infrastructure sector, commanding approximately 63% of the market share in 2024. This segment's prominence is driven by massive investments in upstream, midstream, and downstream infrastructure development across major oil and gas producing regions. The segment's robust performance is supported by increasing global energy demand, ongoing modernization of existing infrastructure, and the development of new extraction facilities. Key developments include the expansion of LNG terminals, construction of new pipeline networks, and upgrading of processing facilities to meet stringent environmental standards. The segment is experiencing the fastest growth in the extraction infrastructure sector, with significant investments being made in sustainable extraction technologies and infrastructure that supports both conventional and unconventional oil and gas resources. The growth is particularly notable in regions focusing on energy security and diversification of supply chains, with substantial projects underway in North America, the Middle East, and Asia-Pacific regions.

Remaining Segments in Extraction Infrastructure

The Other Extraction segment, which encompasses minerals, metals, and coal infrastructure, plays a vital role in supporting global industrial development and the transition to clean energy technologies. This segment is experiencing significant transformation driven by the growing demand for critical minerals essential for renewable energy technologies and electric vehicle batteries. The infrastructure development in this segment includes the construction of new mining facilities, processing plants, and transportation networks. The segment is particularly active in regions with rich mineral deposits, with major projects focused on modernizing existing facilities and developing new extraction capabilities. The increasing focus on sustainable mining practices has led to investments in advanced processing facilities and infrastructure that minimize environmental impact while maximizing resource recovery efficiency. Additionally, the segment is seeing substantial investments in digital infrastructure and automation technologies to improve operational efficiency and safety in mining operations.

Segment Analysis: Utilities Infrastructure

Power Generation Segment in Global Utilities Infrastructure Market

The Power Generation segment continues to dominate the global utilities infrastructure market, commanding approximately 56% market share in 2024 with revenues of USD 365.1 billion. This substantial market position is driven by increasing global energy demands, rapid urbanization, and the ongoing transition towards cleaner energy sources. The segment encompasses various power generation technologies including conventional thermal power plants, nuclear facilities, and an expanding portfolio of renewable energy installations. Major infrastructure developments in emerging economies, particularly in Asia-Pacific, combined with modernization efforts in developed markets, are sustaining the segment's dominant position. The focus on grid reliability and energy security concerns has led to significant investments in upgrading and expanding power generation capabilities worldwide.

Water Segment in Global Utilities Infrastructure Market

The Water segment is emerging as the fastest-growing sector in the utilities infrastructure market, projected to expand at approximately 9% during 2024-2029. This remarkable growth is driven by increasing water scarcity concerns, rapid urbanization, and the pressing need for sustainable water management solutions. Governments worldwide are prioritizing investments in water infrastructure modernization, including advanced treatment facilities, smart metering systems, and efficient distribution networks. The segment is witnessing substantial technological advancements in areas such as desalination, water recycling, and smart water management systems. Growing environmental regulations and the need for resilient water infrastructure in the face of climate change are further accelerating investments in this sector.

Remaining Segments in Utilities Infrastructure Market

The utilities infrastructure market encompasses several other vital segments including Electricity Transmission & Distribution, Gas infrastructure, and telecommunications infrastructure. The Electricity T&D segment plays a crucial role in modernizing power grids and enabling the integration of renewable energy sources. The Gas infrastructure segment continues to evolve with the transition towards cleaner fuel alternatives and the development of natural gas networks. The telecommunications infrastructure segment is experiencing significant transformation driven by the rollout of 5G networks, fiber-optic network infrastructure, and digital connectivity initiatives. These segments collectively contribute to the comprehensive development of utility infrastructure, supporting economic growth and technological advancement across regions.

Segment Analysis: Manufacturing Infrastructure

Industrial Parks and Clusters Segment in Manufacturing Infrastructure Market

Industrial Parks and Clusters emerged as both the dominant and fastest-growing segment in the global manufacturing infrastructure market. In 2024, this segment accounts for approximately 31% of the total manufacturing infrastructure market share, driven by rapid urbanization and the increasing demand for integrated industrial facilities. The segment's growth is propelled by China's large-scale expansion of industrial parks, which has resulted in extensive planning, development, and functional transformation initiatives. Governments worldwide are increasingly focusing on developing specialized industrial zones to promote economic growth and attract foreign investments. These industrial parks are being designed with advanced infrastructure, including smart technologies, sustainable practices, and efficient logistics networks. The development of these parks has also been boosted by various government initiatives and policies aimed at creating manufacturing hubs and promoting industrial clustering for enhanced productivity and economic efficiency.

Petroleum Refining Segment in Manufacturing Infrastructure Market

The Petroleum Refining segment has emerged as another significant growth driver in the manufacturing infrastructure market. This segment's expansion is driven by increasing investments in refinery modernization projects and the growing demand for refined petroleum products across developing economies. The sector is witnessing substantial technological advancements, particularly in automation and process optimization, which are enhancing operational efficiency and reducing environmental impact. Refineries are increasingly incorporating digital technologies and advanced control systems to improve production capabilities and meet stringent environmental regulations. The segment is also seeing significant investments in upgrading existing facilities to handle different grades of crude oil and produce higher-quality fuels that meet evolving environmental standards.

Remaining Segments in Manufacturing Infrastructure

The manufacturing infrastructure market encompasses several other vital segments including Metal and Ore Production, Chemical Manufacturing, and other specialized manufacturing facilities. The Metal and Ore Production segment continues to play a crucial role in supporting global industrialization and construction activities, with significant developments in sustainable production methods and advanced processing technologies. The Chemical Manufacturing segment is experiencing transformation through digitalization and automation initiatives, while focusing on sustainable production practices and green chemistry principles. These segments collectively contribute to the overall manufacturing ecosystem by providing essential materials and products for various industries, while continuously adapting to new technological advances and environmental requirements.

Infrastructure Sector Market Geography Segment Analysis

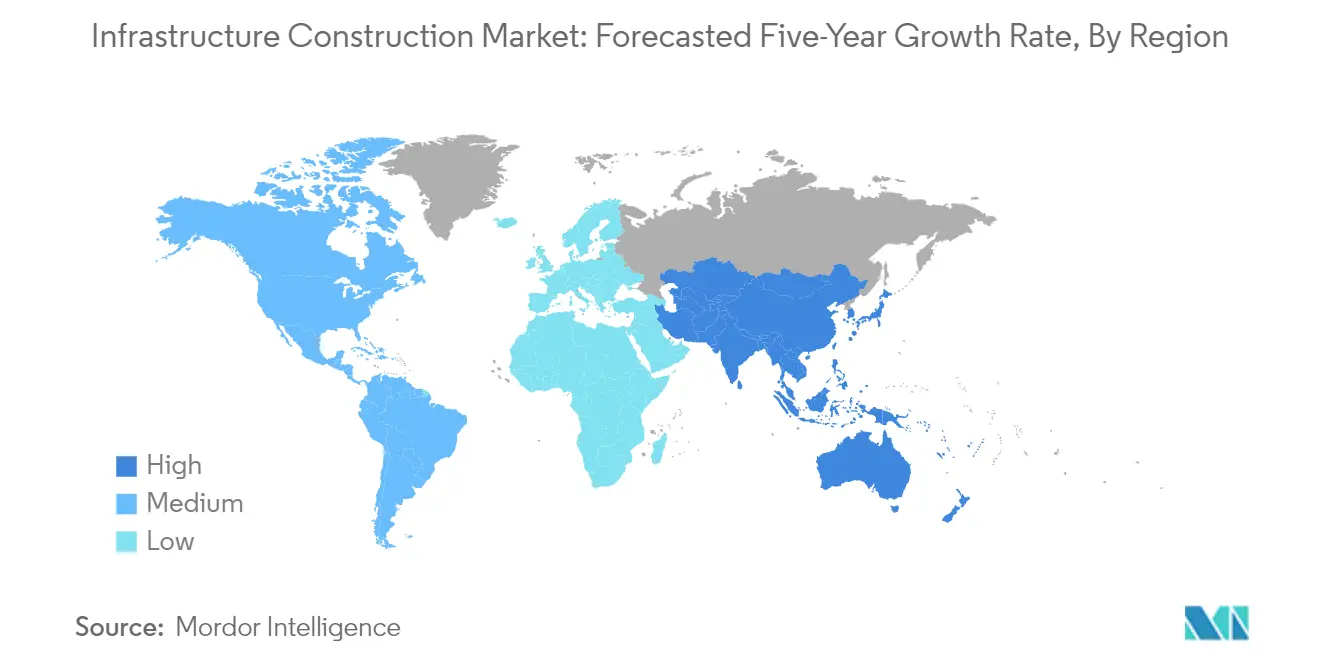

Infrastructure Construction Market in North America

The North American infrastructure construction market continues to demonstrate robust development, accounting for approximately 12% of the global market value in 2024. The region's infrastructure market is primarily driven by ambitious federal infrastructure initiatives and modernization programs across the United States and Canada. The market benefits from strong institutional frameworks, technological advancement in construction methodologies, and an increasing focus on sustainable infrastructure development. Private sector participation through public-private partnerships has become increasingly prevalent, particularly in transportation infrastructure and energy infrastructure projects. The region's emphasis on upgrading aging infrastructure, implementing smart city solutions, and developing renewable energy infrastructure continues to create substantial market opportunities. Additionally, the integration of digital technologies, including Building Information Modeling (BIM) and AI-driven construction management systems, is reshaping project execution and efficiency in the region. The market also shows strong momentum in developing resilient infrastructure to address climate change challenges and natural disasters.

Infrastructure Construction Market in Europe

The European infrastructure construction market has demonstrated steady progression, recording approximately 4% growth annually from 2019 to 2024. The market's evolution is characterized by significant investments in sustainable infrastructure and digital transformation initiatives across the continent. The European Union's commitment to green infrastructure development and carbon neutrality goals continues to shape the market landscape. The region's focus extends beyond traditional infrastructure to encompass smart city developments, renewable energy installations, and advanced transportation networks. Cross-border infrastructure projects remain a key feature of the market, promoting regional connectivity and economic integration. The market demonstrates particular strength in implementing innovative construction technologies and sustainable building practices. European countries are increasingly prioritizing infrastructure resilience and adaptation to climate change, while also focusing on urban regeneration and social infrastructure development. The region's mature regulatory framework and strong emphasis on environmental standards continue to influence project design and execution methodologies.

Infrastructure Construction Market in Asia-Pacific

The Asia-Pacific infrastructure construction market maintains its position as the global growth engine, with projections indicating approximately 6% annual growth from 2024 to 2029. The region's infrastructure development is characterized by rapid urbanization, increasing industrial capacity, and ambitious national development programs. Massive investments in transportation infrastructure, including high-speed rail networks and smart city projects, continue to drive market expansion. The region's commitment to economic corridor development and cross-border connectivity initiatives creates substantial opportunities for infrastructure development. Digital infrastructure and smart city solutions are increasingly becoming integral components of infrastructure projects across the region. The market benefits from strong government support, increasing private sector participation, and growing international investment interest. Environmental sustainability and climate resilience are becoming more prominent considerations in infrastructure planning and execution. The region's focus on technological innovation and modern construction methodologies is transforming project delivery approaches and operational efficiency.

Infrastructure Construction Market in Latin America

The Latin American infrastructure construction market exhibits significant potential for growth, driven by increasing urbanization and economic development needs across the region. The market is characterized by a strong focus on improving transportation infrastructure networks, energy infrastructure, and urban development projects. Countries across the region are implementing reforms to attract private investment and international partnerships in infrastructure development. The market shows particular dynamism in renewable energy infrastructure and digital infrastructure projects. Social infrastructure development, including healthcare and education facilities, remains a key priority across the region. The adoption of modern construction technologies and sustainable building practices is gradually increasing, improving project efficiency and environmental performance. The region's infrastructure development strategies increasingly emphasize climate resilience and sustainable urban development, reflecting growing environmental awareness and changing social needs.

Infrastructure Construction Market in Middle East & Africa

The Middle East and African infrastructure construction market continues to evolve, driven by ambitious national development plans and increasing urbanization across both regions. The market demonstrates strong potential in renewable energy infrastructure, transportation infrastructure networks, and urban development projects. Government initiatives to diversify economies and reduce dependence on traditional sectors are creating new opportunities in infrastructure development. The region shows increasing adoption of sustainable infrastructure practices and smart infrastructure solutions. Private sector participation is growing, supported by improving regulatory frameworks and investment incentives. Digital transformation in infrastructure planning and execution is gaining momentum across the region. The market particularly benefits from increasing regional cooperation and cross-border infrastructure initiatives. Social infrastructure development, including healthcare and education facilities, remains a key focus area, reflecting the region's young and growing population.

Infrastructure Construction Industry Overview

Top Companies in Infrastructure Construction Market

The global infrastructure construction market features prominent players like ACS Group, VINCI, China State Construction Engineering, Skanska AB, Larsen & Toubro, and Kajima Corporation leading the industry. These companies are increasingly focusing on technological innovation, particularly in areas like Building Information Modeling (BIM), drone-based site monitoring, and digital twin technologies to enhance project efficiency and reduce costs. Strategic partnerships with technology providers and startups are becoming commonplace as companies aim to modernize their operations and improve project delivery capabilities. Companies are also expanding their geographical presence through joint ventures and local partnerships, especially in emerging markets across Asia and Africa. The industry is witnessing a significant shift towards sustainable infrastructure development, with major players investing in green building technologies and renewable energy projects. Operational agility has become crucial, with companies adopting modular construction techniques and prefabrication methods to accelerate project completion times while maintaining quality standards.

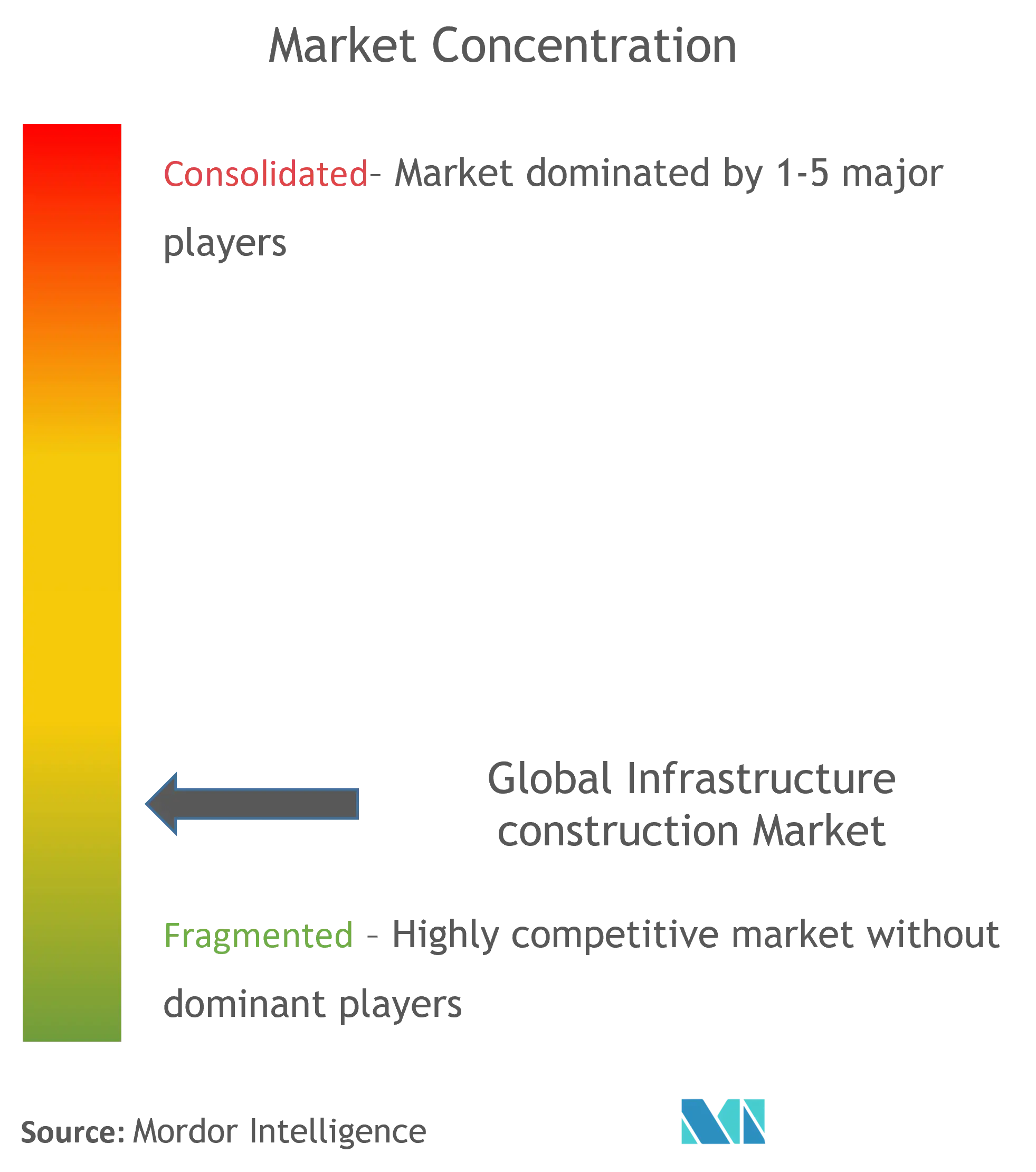

Market Dominated by Diversified Global Players

The infrastructure market exhibits a fragmented competitive landscape with a mix of global conglomerates and regional specialists operating across different geographical regions. Large multinational corporations, particularly from China, Europe, and the United States, dominate the global market through their extensive resource capabilities, technological expertise, and ability to handle complex mega-projects. These companies typically operate across multiple segments including transportation infrastructure, energy facilities, and urban development projects. The market also features numerous regional players who maintain strong positions in their local markets through a deep understanding of local regulations, established relationships with government bodies, and specialized expertise in specific infrastructure segments.

The industry is experiencing ongoing consolidation through strategic mergers and acquisitions, as larger players seek to expand their capabilities and geographical reach. Companies are increasingly forming consortiums and joint ventures to manage risk and pool resources for large-scale infrastructure projects. This trend is particularly evident in emerging markets where local expertise is combined with international technical capabilities and funding resources. The market also sees significant vertical integration as companies expand their service offerings to include design, construction, operation, and maintenance capabilities, creating more comprehensive infrastructure services.

Innovation and Sustainability Drive Future Success

Success in the infrastructure industry increasingly depends on companies' ability to integrate technological innovation while maintaining cost competitiveness. Market leaders are investing heavily in digital transformation, including artificial intelligence for project planning, IoT for asset monitoring, and advanced analytics for risk management. Companies that can effectively combine traditional construction expertise with modern technological capabilities are better positioned to secure large-scale projects. The ability to deliver sustainable infrastructure solutions has become a critical differentiator, with clients increasingly demanding green building certifications and environmental impact considerations in project execution.

For new entrants and growing players, success lies in developing specialized expertise in high-growth segments like renewable energy infrastructure or smart city projects. Building strong relationships with government bodies and financial institutions remains crucial given the public-private partnership nature of many infrastructure projects. Companies must also focus on developing robust supply chain networks and maintaining financial stability to handle project delays and regulatory changes. The increasing emphasis on lifecycle cost management and post-construction maintenance services presents opportunities for companies to develop recurring revenue streams beyond traditional construction activities. Risk management capabilities, particularly in handling environmental regulations and social impact assessments, have become essential for long-term success in the market.

Infrastructure Construction Market Leaders

-

ACS Group

-

VINCI

-

China State Construction Engineering Corporation Ltd (CSCEC)

-

Skanska

-

Larsen & Toubro

- *Disclaimer: Major Players sorted in no particular order

Infrastructure Construction Market News

- March 2023: HOCHTIEF and infrastructure investor Palladio Partners partnered to build and operate a sustainable data center in Heiligenhaus (North Rhine-Westphalia). They signed a contract for the new type of high-tech YEXIO facility in the Innovation Park of the university town.

- October 2022: China Communications Construction Company Limited and PipeChina, known formally as China Oil and Gas Pipeline Network, held a signing ceremony for a strategic framework cooperation agreement in Beijing.

- January 2022: VINCI awarded a contract for the Takitimu North Link road in Southeast Auckland, New Zealand. HEB Construction, a VINCI Construction subsidiary based in New Zealand, would be responsible for the design and construction of the Takitimu North Link as per a joint venture with Fulton Hogan. This project is expected to support urban development in the region by improving accessibility. It will also relieve neighboring towns from heavy freight traffic, thereby enhancing safety.

Infrastructure Construction Industry Segmentation

Infrastructure construction is a proposed plan to build, maintain, and upkeep infrastructural facilities, systems, and services. Building new roads, constructing new power plants, maintaining sewage systems, and providing drinking water to the public are all examples of infrastructure construction.

The study is a comprehensive background analysis of the infrastructure construction market, covering the current market trends, restraints, technological updates, and detailed information on various segments and the competitive landscape of the industry. The impact of COVID-19 has also been incorporated and considered during the study.

The Global Infrastructure Construction Market is segmented by Type (Social Infrastructure (Schools, Hospitals, Defense, Other Infrastructure), Transportation Infrastructure (Railways, Roadways, Airports, Ports, Waterways), Extraction Infrastructure (Oil and Gas, Other Extraction (Minerals, Metals, and Coal), Utilities Infrastructure (Power Generation, Electricity Transmission & Distribution, Water, Gas, Telecoms), Manufacturing Infrastructure (Metal and Ore Production, Petroleum Refining, Chemical Manufacturing, Industrial Parks and Clusters, and Other Infrastructure)) and by Geography (North America, Europe, Asia-Pacific, Latin America, Middle East, and Africa). The report offers market size and forecasts for the Global Infrastructure Construction Market in value (USD) for all the above segments.

| By Type | Social Infrastructure | Schools | |

| Hospitals | |||

| Defense | |||

| Other Infrastructure | |||

| Transportation Infrastructure | Railways | ||

| Roadways | |||

| Airports | |||

| Ports | |||

| Waterways | |||

| Extraction Infrastructure | Oil and Gas | ||

| Other Extraction (Minerals, Metals, and Coal) | |||

| Utilities Infrastructure | Power Generation | ||

| Electricity Transmission & Distribution | |||

| Water | |||

| Gas | |||

| Telecoms | |||

| Manufacturing Infrastructure | Metal and Ore Production | ||

| Petroleum Refining | |||

| Chemical Manufacturing | |||

| Industrial Parks and Clusters | |||

| Other Infrastructure | |||

| By Geography | North America | ||

| Europe | |||

| Asia-Pacific | |||

| Latin America | |||

| Middle East & Africa | |||

| Social Infrastructure | Schools |

| Hospitals | |

| Defense | |

| Other Infrastructure | |

| Transportation Infrastructure | Railways |

| Roadways | |

| Airports | |

| Ports | |

| Waterways | |

| Extraction Infrastructure | Oil and Gas |

| Other Extraction (Minerals, Metals, and Coal) | |

| Utilities Infrastructure | Power Generation |

| Electricity Transmission & Distribution | |

| Water | |

| Gas | |

| Telecoms | |

| Manufacturing Infrastructure | Metal and Ore Production |

| Petroleum Refining | |

| Chemical Manufacturing | |

| Industrial Parks and Clusters | |

| Other Infrastructure |

| North America |

| Europe |

| Asia-Pacific |

| Latin America |

| Middle East & Africa |

Infrastructure Construction Market Research FAQs

How big is the Infrastructure Sector Market?

The Infrastructure Sector Market size is expected to reach USD 2.89 trillion in 2025 and grow at a CAGR of 6.27% to reach USD 3.92 trillion by 2030.

What is the current Infrastructure Sector Market size?

In 2025, the Infrastructure Sector Market size is expected to reach USD 2.89 trillion.

Who are the key players in Infrastructure Sector Market?

ACS Group, VINCI, China State Construction Engineering Corporation Ltd (CSCEC), Skanska and Larsen & Toubro are the major companies operating in the Infrastructure Sector Market.

Which is the fastest growing region in Infrastructure Sector Market?

North America is estimated to grow at the highest CAGR over the forecast period (2025-2030).

Which region has the biggest share in Infrastructure Sector Market?

In 2025, the Asia-Pacific accounts for the largest market share in Infrastructure Sector Market.

What years does this Infrastructure Sector Market cover, and what was the market size in 2024?

In 2024, the Infrastructure Sector Market size was estimated at USD 2.71 trillion. The report covers the Infrastructure Sector Market historical market size for years: 2020, 2021, 2022, 2023 and 2024. The report also forecasts the Infrastructure Sector Market size for years: 2025, 2026, 2027, 2028, 2029 and 2030.

Page last updated on: June 16, 2024