Infrared Detector Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

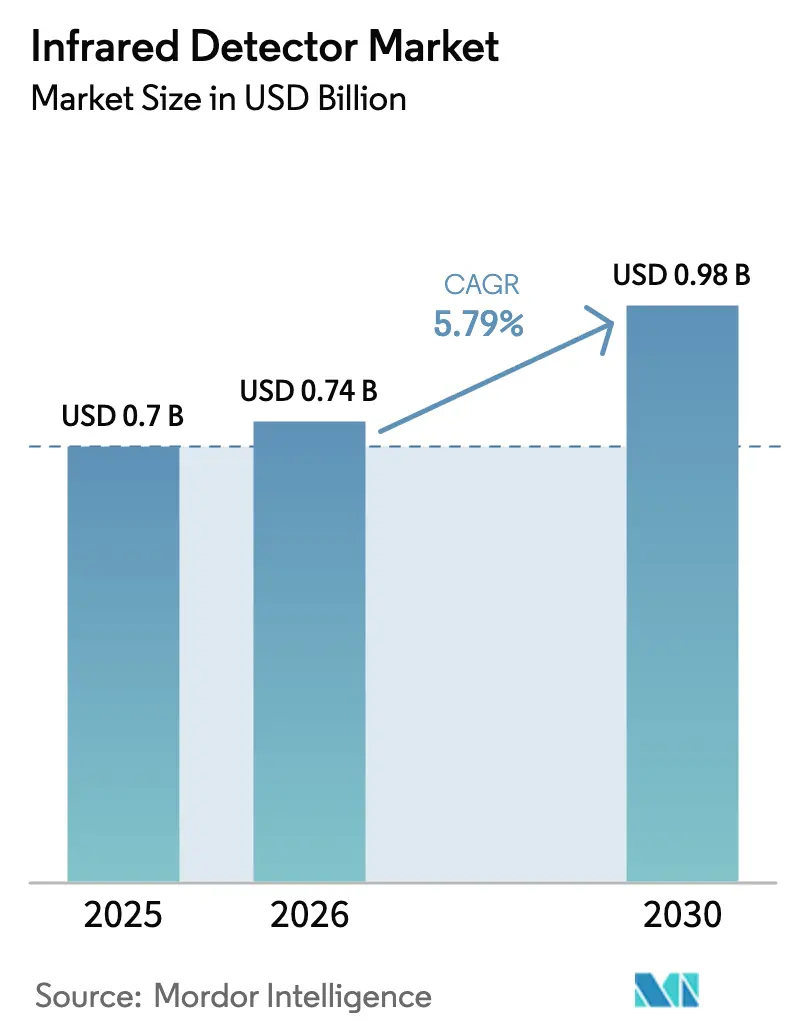

| Market Size (2026) | USD 0.74 Billion |

| Market Size (2030) | USD 0.98 Billion |

| Growth Rate (2026 - 2031) | 5.79% CAGR |

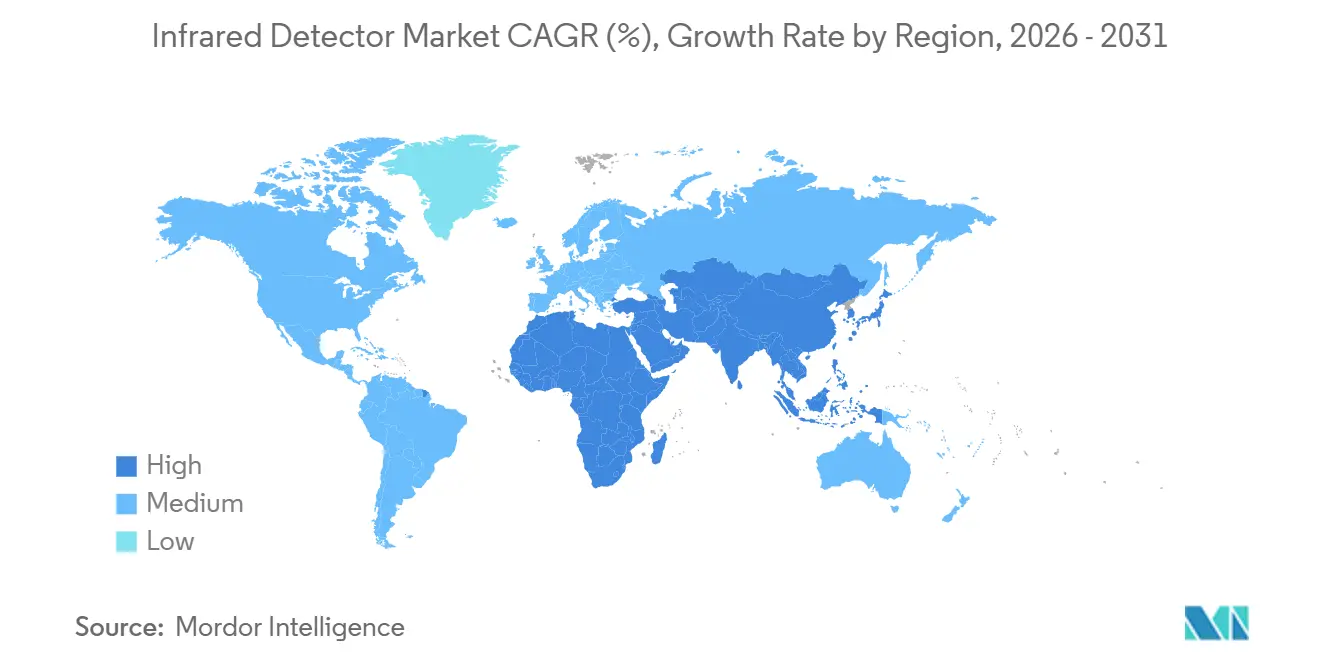

| Fastest Growing Market | Middle East |

| Largest Market | Asia Pacific |

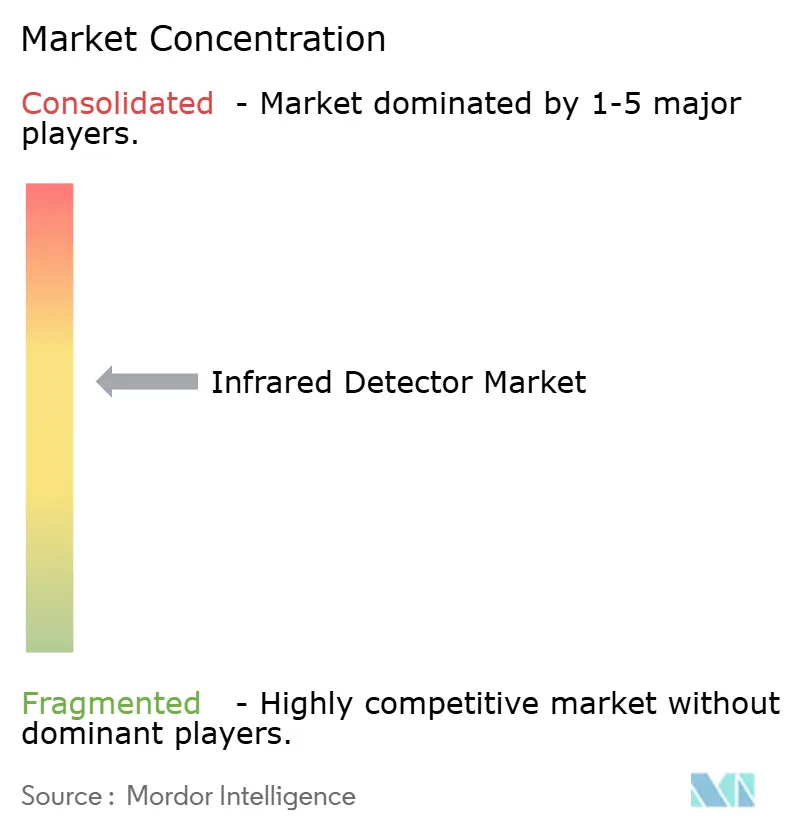

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Infrared Detector Market Analysis by Mordor Intelligence

The infrared detector market size is expected to increase from USD 0.70 billion in 2025 to USD 0.74 billion in 2026 and reach USD 0.98 billion by 2031, growing at a CAGR of 5.79% over 2026-2031. Heightened demand for solid-state LiDAR in electric vehicles, quarterly thermography audits mandated by the European Union, and hydrogen-leak monitoring rules across the Middle East are shifting revenue toward short-wave and mid-wave infrared focal-plane arrays. Uncooled microbolometers remain the workhorse of building automation and industrial maintenance, yet photo quantum designs based on indium-gallium-arsenide and mercury-cadmium-telluride are expanding in automotive and defense because they deliver faster frame rates and lower noise figures. Asia-Pacific retains volume leadership on the back of China’s LiDAR supply chain, while the Middle East presents the fastest regional upside as green-hydrogen complexes move from pilot to megawatt scale. Price pressure in passive pyroelectric sensors is accelerating migration to wafer-level-packaged microbolometers that integrate vacuum encapsulation, anti-reflection coatings, and readout circuitry in modules measuring under 10 millimeters on a side.

Key Report Takeaways

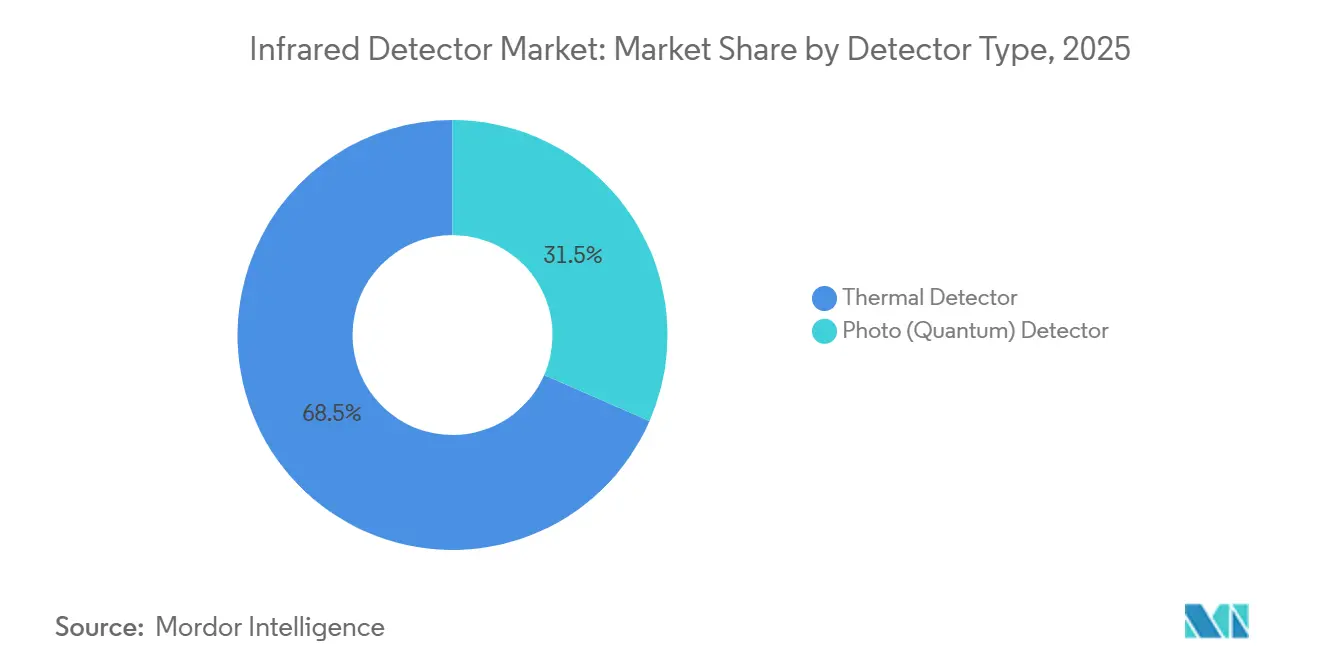

- By detector type, thermal detectors led with 68.46% of infrared detector market share in 2025, while photo quantum detectors are projected to expand at an 11.80% CAGR through 2031.

- By cooling technology, uncooled detectors accounted for 83.71% of the infrared detector market size in 2025; cooled detectors are advancing at a 10.90% CAGR over 2026-2031.

- By material, microbolometer films captured 64.27% share in 2025, whereas indium-gallium-arsenide arrays are forecast to rise at a 13.21% CAGR.

- By spectral range, long-wave infrared commanded 45.83% revenue share in 2025; short-wave infrared is on track for a 14.58% CAGR between 2026 and 2031.

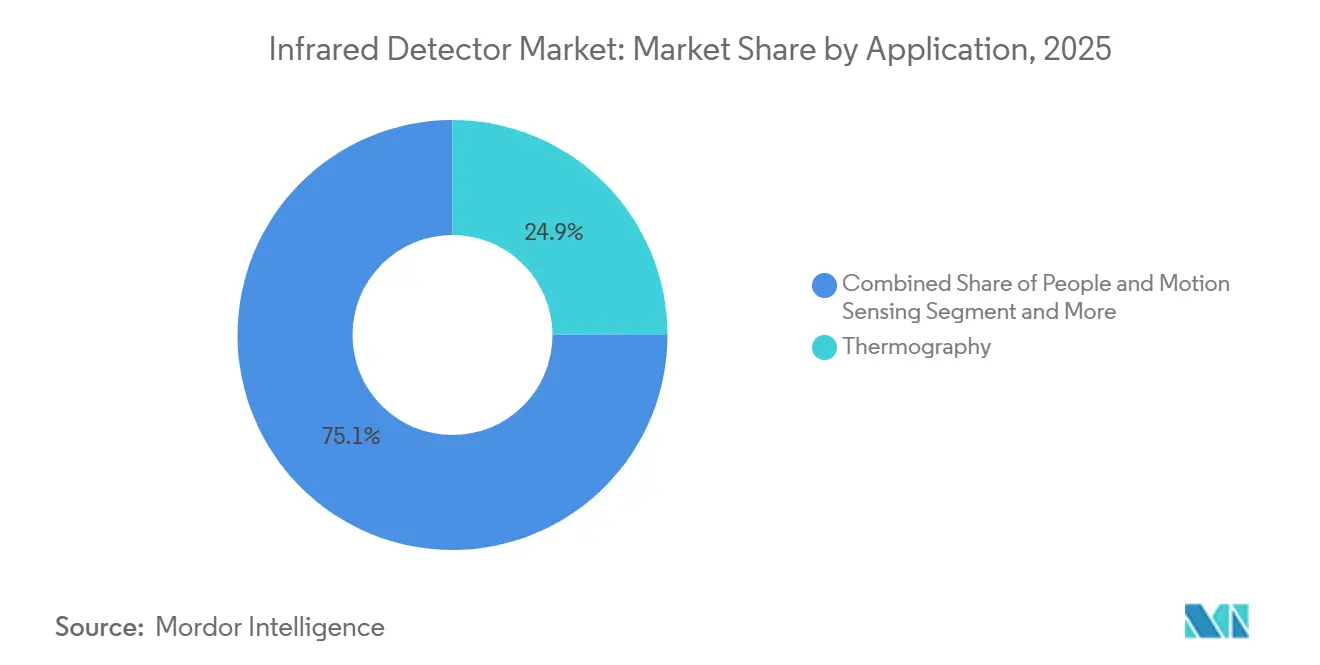

- By application, temperature measurement and thermography held 24.94% of 2025 demand, but automotive ADAS and LiDAR are set to post an 18.43% CAGR through 2031.

- By end-use industry, industrial manufacturing represented 31.03% of 2025 revenue, yet automotive is poised to grow at a 12.64% CAGR to 2031.

- By geography, Asia-Pacific held 40.15% of 2025 revenue; the Middle East is projected to record a 10.30% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Infrared Detector Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Miniaturization of Uncooled Micro-bolometer Arrays Empowering IoT Motion Sensors in Asia | +1.2% | Asia-Pacific core, spill-over to North America | Medium term (2-4 years) |

| Mandatory Predictive-Maintenance Thermography in EU Process Industries | +0.9% | Europe, secondary adoption in North America | Short term (≤ 2 years) |

| Surge in LiDAR-grade Near-IR Detectors for Autonomous and EV Platforms in China | +1.5% | China, expanding to Asia-Pacific and North America | Long term (≥ 4 years) |

| IR Gas-Leak Detection Mandates for Green-Hydrogen Plants across Middle East | +0.7% | Middle East, early pilots in Australia | Medium term (2-4 years) |

| Semiconductor Fab Inspection Demand for SWIR Cameras in Taiwan and South Korea | +0.6% | Taiwan and South Korea, secondary in Japan | Short term (≤ 2 years) |

| Border-Surveillance Modernization Programs in US and India | +0.5% | United States and India, limited Middle East adoption | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Miniaturization of Uncooled Micro-bolometer Arrays Empowering IoT Motion Sensors in Asia

Pixel pitches below 12 micrometers have allowed Japanese and South Korean suppliers to ship nearly 8 million focal-plane arrays for battery-powered IoT occupancy sensors in 2025, up 35% year on year.[1]IEEE, “Sub-10 µm Microbolometer Advancements,” ieeexplore.ieee.org Building-automation integrators adopted the smaller die to satisfy energy-efficiency codes that tie HVAC loads to verified room presence. Lens diameters shrank in parallel, allowing thermal modules to fit into light fixtures and wall switches that previously lacked space for 17-micrometer arrays. Manufacturing cost per square millimeter dropped about 40%, opening mid-tier smartphones to embedded thermal cameras. Passive operation avoids the eye-safety reviews associated with active near-infrared illumination, easing consumer-product certification under IEC 62471.

Mandatory Predictive-Maintenance Thermography in EU Process Industries

The Energy Efficiency Directive 2023/1791 obliges refiners, chemical plants, and steel mills to run quarterly thermography on motors, switchgear, and piping.[2]European Commission, “Energy Efficiency Directive 2023/1791,” ec.europa.eu Germany and France extended the scope in 2024 to medium-sized sites, tripling the addressable facility count to 12,000. Handheld and drone-mounted cameras with 0.05 °C resolution displaced contact probes in hazardous zones. U.K. and Dutch insurers now rebate between 5% and 10% of annual premiums when plants upload continuous thermal data to asset-management clouds. Camera vendors responded by bundling LTE modules and encrypted gateways, features that raise average selling price by roughly 20% versus offline units.

Surge in LiDAR-grade Near-IR Detectors for Autonomous and EV Platforms in China

China’s 2025 Level 3 vehicle guidelines require at least one solid-state or hybrid LiDAR per car.[3]MIIT, “Smart Vehicle Technical Guidelines 2025,” miit.gov.cn Frequency-modulated continuous-wave systems operating at 1,550 nanometers rely on indium-gallium-arsenide avalanche photodiodes offering fourfold range versus 905-nanometer pulsed silicon imagers. Domestic LiDAR makers shipped about 1.2 million units in 2025, sourcing detector wafers from Japanese and German epitaxy houses alongside local foundries. Operating above the silicon cut-off also meets IEC 60825-1 eye-safety Class 1 limits at higher optical power, extending highway detection to 300 meters. Brands such as BYD and NIO embedded the modules on production lines last year, accelerating volume demand for short-wave infrared arrays.

IR Gas-Leak Detection Mandates for Green-Hydrogen Plants across Middle East

Saudi Arabia and the United Arab Emirates published joint standards in 2024 that oblige continuous mid-wave infrared monitoring at electrolyzer sites above 10 megawatts. Cameras must sense hydrogen at 100 ppm from 100 meters, a metric achievable only with cooled mercury-cadmium-telluride or indium-antimonide detectors. NEOM’s 4-gigawatt complex alone will deploy roughly 250 fixed and portable cameras valued near USD 15 million. IRENA’s 2025 hydrogen-safety guide endorses infrared imaging as the primary leak countermeasure, reinforcing demand in Australia and Chile. Compliance with ISO 19880-8 extends detector sales into downstream fueling stations where portable imagers verify pipe integrity.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Export-control (ITAR-like) Limits on High-spec Cooled Detectors | -0.8% | Global, most acute in Asia-Pacific and Middle East | Long term (≥ 4 years) |

| Price Erosion in Passive PIR Components | -0.6% | Global, concentrated in consumer electronics segment | Short term (≤ 2 years) |

| Thermal Drift and Calibration Issues in Offshore Oil-and-Gas Deployment | -0.3% | North Sea, Gulf of Mexico, Southeast Asia offshore fields | Medium term (2-4 years) |

| Counterfeit Detector Channels in Emerging Markets | -0.2% | Africa, South Asia, parts of South America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Export-control (ITAR-like) Limits on High-spec Cooled Detectors

U.S. ITAR and EU dual-use lists classify cooled arrays above 640×480 resolution and below 20 mK noise as defense articles, adding up to 12 months for export licensing and legal fees over USD 100,000 per shipment. Asian and Middle Eastern buyers pivot to lower-spec microbolometers or seek domestically produced cooled detectors that skirt the threshold, trading performance for procurement speed. Western suppliers report 25% fewer international orders in 2025 compared with 2024 because of license denials. The restriction also fragments global R&D collaboration as cross-border technical-data exchanges now require government-approved agreements. Emerging superlattice materials aim to reset the regulatory floor, but widespread qualification remains at least four years away.

Price Erosion in Passive PIR Components

Average selling prices for discrete pyroelectric sensors fell about 15% in 2025 after Chinese capacity additions overshot demand from commercial-real-estate retrofits. Margin squeeze pushed incumbents such as Murata and Panasonic toward higher-value microbolometer modules that command two to three times the revenue per channel. OEMs consolidated supplier rosters, agreeing to long-term volume contracts that exchange scale for single-digit price cuts, locking out smaller vendors. Meanwhile, system value is migrating to cloud analytics and machine-learning models that reside off the sensor, making commoditized PIR elements even more interchangeable. The resulting race to the bottom limits R&D reinvestment in next-generation pyroelectric materials.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Detector Type: Quantum Arrays Gain in Automotive Sensing

Photo quantum arrays are projected to expand at an 11.80% CAGR, nearly double the overall infrared detector market, as automakers embed indium-gallium-arsenide avalanche photodiodes in highway-range LiDAR and mercury-cadmium-telluride in night-vision cameras. Thermal detectors, holding 68.46% of 2025 revenue, dominate cost-sensitive industrial and building-automation roles where passive operation and ambient-temperature tolerance outweigh the speed advantages of quantum devices. Because mature microbolometer supply chains can fabricate 640×480 arrays for under USD 50, the thermal camp anchors mass-market pricing. Yet the automotive pivot toward Level 3 autonomy raises per-vehicle detector content, nudging volume into the quantum camp and lifting average selling prices inside the infrared detector market.

Quantum growth depends on high-yield epitaxy of indium-gallium-arsenide and mercury-cadmium-telluride on lattice-matched substrates that remain scarce and expensive. Japan and Taiwan are scaling 200-millimeter epitaxial reactors to widen wafer diameters, which could cut die cost by as much as 30% once line yields exceed 60%. If those capacity ramps stay on track, the infrared detector market size attributed to quantum arrays for automotive and spectroscopy may reach USD 0.30 billion by 2031. Industrial thermography retains a stronghold for thermal detectors, but their share will slip below 60% as quantum adoption broadens into high-speed machine vision and hyperspectral biomedical imaging. The infrared detector industry thus faces a two-track future in which price-led thermal arrays coexist with performance-driven quantum devices.

By Cooling Technology: Uncooled Dominance Persists Amid Cooled Resurgence

Uncooled devices captured 83.71% of 2025 revenue as smartphone add-ons, driver-monitoring cameras, and drone gimbals require low-power, room-temperature operation. The segment’s cost advantage widened with wafer-level packaging that slashes assembly expense 40% and compresses module footprints below 10 millimeters. Cooled designs, however, are growing at a 10.90% CAGR because defense and long-range border-surveillance programs demand sub-20 millikelvin sensitivity. These programs procure high-price cooled cameras, often exceeding USD 20,000 each, and therefore punch above their unit volumes in dollar terms, enlarging the infrared detector market size for cryogenic systems.

Advances in pulse-tube and linear-drive Stirling coolers have extended the mean time between failures to 15,000 hours, easing maintenance burdens that once deterred commercial buyers. Scientific instruments and astronomy payloads are also adopting cooled focal-plane arrays for mid-wave spectroscopy, where thermal noise must be suppressed below detector shot noise. While cooled shipments remain a minority, their revenue share could top 22% by 2031 if export-control bottlenecks ease. The net result keeps uncooled architectures at volume leadership yet allows cooled niches to regain pricing leverage inside the broader infrared detector market.

By Material: InGaAs Surges on Semiconductor Inspection Demand

Microbolometers contributed 64.27% of 2025 revenue by leveraging silicon-compatible thin films that ride semiconductor economies of scale. Indium-gallium-arsenide is accelerating at a 13.21% CAGR on the strength of wafer inspection and 1,550-nanometer LiDAR that benefits from higher allowable laser power under IEC 60825-1. Mercury-cadmium-telluride prevails in dual-band military imagers thanks to tunable band-gap chemistry that spans 3-12 micrometers. Pyroelectric and thermopile volumes slide as occupancy sensing migrates to high-resolution microbolometers able to map people counts for smart-building analytics, a transition squeezing single-element component margins across the infrared detector industry.

Scaling indium-gallium-arsenide beyond four-inch wafers poses lattice-mismatch and defect challenges that drive substrate prices above USD 500 per piece. Collaborative programs between substrate vendors and equipment makers aim to push 150-millimeter diameters by 2028, a milestone that could lower die cost enough for consumer LiDAR. Mercury-cadmium-telluride faces environmental scrutiny under the EU RoHS Directive, spurring research into indium-arsenide/gallium-antimonide superlattices that promise equivalent performance without toxic mercury. The materials landscape therefore balances scalability, regulation, and application-specific performance as each segment looks to protect or grow its share of the infrared detector market.

By Spectral Range: SWIR Ascends on Dual-Use Momentum

Long-wave infrared commanded 45.83% of 2025 revenue because it pairs naturally with uncooled microbolometers in low-temperature thermography. Short-wave infrared is the fastest climber at a 14.58% CAGR, propelled by simultaneous gains in wafer inspection and automotive LiDAR that require penetration beyond the silicon absorption edge and eye-safe power budgets. Mid-wave infrared serves defense seekers and airborne surveillance, while near-infrared and far-infrared remain niche science and spectroscopy domains.

Volume pivots toward SWIR will redistribute material demand toward indium-gallium-arsenide and away from vanadium-oxide microbolometers. Still, the infrared detector market share for LWIR will stay above 35% by 2031 because predictive-maintenance and firefighting cameras rely on the 8-14 micrometer atmospheric window. Multi-spectral imagers blending visible, SWIR, and LWIR into a single package are gaining traction in precision agriculture, hinting at future devices that allocate pixel real estate dynamically according to application need. Such hybrid designs could further stretch the total infrared detector market size by opening performance tiers not served by single-band sensors.

By Application: Automotive ADAS and LiDAR Outpace Legacy Thermography

Thermography and temperature measurement produced 24.94% of 2025 demand, anchoring replacement cycles in process industries and utility asset management. Automotive ADAS and LiDAR, however, are forecast to post an 18.43% CAGR as Level 3 autonomy shifts from pilot to volume manufacturing, increasing detector content per vehicle from roughly USD 50 in 2025 to upward of USD 300 by 2031. People and motion sensing, industrial monitoring, and fire-and-gas detection still represent nearly 40% of shipments, but their growth lags mobility use cases that ride electric-vehicle scalability.

As autonomous functions proliferate, the infrared detector market size attached to automobiles could exceed USD 0.25 billion by 2031, narrowing the gap with industrial thermography. Spectroscopy and biomedical imaging remain constrained by high system costs, though hospital trials of hyperspectral endoscopes for oncology could unlock reimbursement pathways post-2027. Environmental monitoring via satellite and drones continues to draw on both SWIR and LWIR bands for wildfire detection and greenhouse-gas mapping. The breadth of emerging uses positions the infrared detector industry for diversified growth rather than singular dependence on any one domain.

By End-Use Industry: Automotive Sector Accelerates Past Industrial Base

Industrial manufacturing accounted for 31.03% of 2025 revenue, buoyed by decades of installed thermal camera bases in European petrochemical hubs. The automotive sector, expanding at a 12.64% CAGR, is on pace to eclipse industrial volume by late decade as LiDAR and driver-monitoring migrate from premium to mid-range vehicles. Aerospace and defense accounted for 20% of sales, driven by demand for cooled detectors for surveillance pods and missile seekers. Oil, gas, and energy users are layering infrared into hydrogen plants and LNG terminals, embedding continuous cameras where point sensors once sufficed.

Consumer electronics and smart infrastructure form a fragmented but fast-cycling demand pool where product lifetimes are measured in quarters, not years. Smartphone makers treat thermal imaging as a differentiator in flagship devices priced above USD 800, though attach rates remain in the single digits. Municipalities retrofit streetlights and traffic signals with micro-bolometer arrays to count pedestrians and optimize lighting schedules, turning cities into steady but modest buyers. The net shift tilts the infrared detector market toward mobility and infrastructure-as-a-service, underscoring why automotive growth shapes supplier roadmaps.

Geography Analysis

Asia-Pacific generated 40.15% of 2025 revenue, lifted by China’s 9 million electric-vehicle shipments and regional semiconductor inspection demand. The infrared detector market size for Asia-Pacific could exceed USD 0.40 billion by 2031 if LiDAR attach rates reach 30% on new cars. Japan anchors epitaxial wafer supply, while South Korea scales indium-gallium-arsenide fabs to support domestic memory foundries. Emerging Southeast Asian drone makers are adopting LWIR microbolometers for crop-health surveys, broadening application footprints across the bloc.

Europe contributed roughly 25% of 2025 sales on the back of thermography mandates in process plants and defense spending on cooled mid-wave systems. Replacement cycles every five to seven years generate predictable base-load demand, while tightened industrial-emissions rules add incremental unit sales. Leading detector houses in France and Germany leverage proximity to NATO prime contractors, enabling rapid customization for armored-vehicle sights and soldier-borne systems. Eastern Europe shows early adoption of building-automation sensors to satisfy updated EU energy codes, offering a diffuse but rising tail for uncooled volumes.

The Middle East, though less than 8% of 2025 revenue, is forecast at a 10.30% CAGR as Saudi and Emirati hydrogen projects translate policy into procurement. Each gigawatt of electrolyzer capacity pulls in about 500 mid-wave and LWIR cameras for leak detection, a density far above that in legacy oil-and-gas facilities. North America remains defense-heavy, with multi-year Army and Homeland Security programs ensuring steady orders for cooled arrays. South America and Africa together account for less than 10% of global sales because limited financing and political risk slow large-scale deployments, though Brazilian agriculture and South African mining provide targeted growth niches.

Regulatory Landscape

Export controls and public-sector procurement rules shape global trade in infrared detectors, especially for cooled, high-performance arrays used in defense and long-range surveillance. In the United States, thermal imaging cameras and related infrared sensing equipment are governed under the Export Administration Regulations (EAR), including Commerce Control List controls (for example, ECCN 6A003). Federal buyers also apply supply-chain restrictions such as NDAA Section 889 and FAR 52.204-25 for covered surveillance and communications equipment. Enforcement actions reinforce compliance risk for manufacturers and channel partners, and in February 2026 the US Department of Commerce, Bureau of Industry and Security (BIS) issued a final order resolving an administrative enforcement matter involving Teledyne FLIR LLC and affiliates tied to unlicensed thermal camera exports and de minimis rule miscalculations.

In Europe, regulation is broadening beyond safety and performance toward cybersecurity and privacy controls for connected infrared-enabled security systems. The EU Cyber Resilience Act (Regulation (EU) 2024/2847) establishes cybersecurity obligations for products with digital elements, with full application beginning December 11, 2027, affecting smart security cameras and connected sensing endpoints that integrate infrared modules. Separately, the European Data Protection Board (EDPB) updated guidance on video devices (April 2026 summary), reinforcing requirements such as DPIAs where surveillance involves large-scale monitoring of public areas, which affects how thermal and multi-sensor deployments are designed, configured, and documented. Standards activity is also tightening application-level requirements; ISO/FDIS 7240-33 reached the formal approval/FDIS registration stage on March 17, 2026 for thermal imaging fire detectors, supporting more consistent performance baselines in safety-oriented deployments.

Competitive Landscape

The top five suppliers, Teledyne FLIR, Lynred, Hamamatsu Photonics, Excelitas, and Leonardo DRS, accounted for about 45% of 2025 revenue, indicating moderate concentration in the infrared detector market. Their vertically integrated fabs, in-house readout-IC design, and proprietary cryocoolers create barriers for new entrants. Chinese challengers iRay Technology, Hikmicro, and Guide Sensmart undercut list prices by up to 30% in uncooled modules, capturing design wins in consumer thermal cameras and building-automation sensors. Western incumbents safeguard high-margin cooled arrays through defense contracting channels that require ITAR compliance and field-proven reliability records.

Technology roadmaps diverge along cost-versus-performance lines. Volume-oriented players invest in 200-millimeter wafer lines and automated pick-and-place assembly to shave cents per pixel, while military suppliers push type-II superlattice materials and single-photon avalanche diode arrays for next-generation seekers. Wafer-level packaging has become the universal upgrade path, compressing vacuum seals, getters, and optical coatings into a monolithic stack that reduces module height by 30%. Customers now ask for ISO 9001 and IATF 16949 process controls as prerequisites for automotive programs, raising compliance costs by roughly 15% but opening multi-million-unit addressable volumes.

Strategic activity intensified in 2025-2026. Teledyne FLIR earmarked USD 45 million to boost microbolometer capacity in California, while Lynred secured a EUR 30 million defense contract for cooled mid-wave arrays. Hamamatsu debuted a 640×512 indium gallium arsenide sensor targeting LiDAR, and iRay commissioned a new microbolometer fab in Wuhan. Excelitas added thermopile assets via acquisition, signaling consolidation among mid-tier suppliers. The competitive landscape therefore balances capacity expansion, material innovation, and merger-and-acquisition plays as firms defend or grow their slices of the infrared detector market.

Infrared Detector Industry Leaders

Honeywell International Inc.

Teledyne FLIR

Lynred (ULIS + Sofradir)

Hamamatsu Photonics

Excelitas Technologies

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Defense, border security, and counter-UAV programs are creating near-term whitespace for higher-resolution, performance-focused detectors and modules, particularly in MWIR and LWIR. Multiple suppliers are scaling product capability and capacity around this demand, with Lynred introducing DRACO MW SL (SXGA 1280x1024 MWIR, 7.5 um pixel pitch, T2SL-based) in June 2026 for land and counter-UAV applications, and Exosens announcing plans in May 2026 to double cooled IR camera production capacity during 2026 for long-range surveillance and counter-drone systems. On the demand side, large blanket procurements show volume pull for thermal imaging in unmanned and surveillance use cases, and in July 2026 Leonardo DRS announced a contract under a blanket purchase agreement to supply more than 50,000 Tenum Orbit thermal imaging cameras.

Industrial safety and compliance-driven monitoring is also shifting room for infrared detector attach-rate gains as operating practices move from periodic checks to continuous sensing, including thermography for asset health and infrared-based gas monitoring. The Middle East hydrogen buildout described in the report context, including joint Saudi-UAE standards for continuous monitoring at electrolyzer sites above 10 MW and ISO 19880-8 extending requirements downstream, aligns with opportunities for cooled MWIR cameras in fixed and portable configurations, while the EU Energy Efficiency Directive 2023/1791 anchors recurring thermography needs in process industries. At the technology level, active roadmaps for High Operating Temperature (HOT) detectors and room-temperature uncooled approaches, including T2SL and emerging materials research such as carbon nanotube and colloidal quantum dot concepts, point to product-space openings aimed at reducing SWaP-C while expanding performance tiers for automotive, drone, and industrial sensing.

Recent Industry Developments

- July 2026: Leonardo DRS announced a contract under a blanket purchase agreement to supply more than 50,000 Tenum Orbit thermal imaging cameras for high-volume unmanned and surveillance needs. The award highlights scaling demand for thermal imaging at fleet volumes rather than small specialty lots, which supports larger, more standardized detector and module supply programs.

- June 2026: Teledyne FLIR OEM released the Boson SX8, an ITAR-free, NDAA-compliant uncooled LWIR thermal camera module with SXGA resolution and an 8-micron pixel pitch. The module targets procurement-constrained defense and security deployments that prioritize compliant, domestically acceptable supply chains while pushing higher resolution into compact uncooled form factors.

- April 2024: Lynred secured a pre-development contract from the European Space Agency for the Sentinel-2 Next-Generation mission to design an advanced multispectral infrared detector, with a first prototype scheduled for 2026. The program underlines continued institutional investment in space-qualified infrared detection and sustains development pathways that can later transfer into high-reliability commercial and defense imaging designs.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the infrared detector market covers revenue generated from detector components that sense infrared radiation and convert it into an electrical signal, across common wavelength bands and cooling approaches, and then shipped into end-use applications worldwide.

Scope exclusions: We exclude complete infrared cameras and thermal imaging systems when detector value is not separable, along with downstream software and services.

Segmentation Overview

- By Detector Type

- Thermal Detector

- Photo (Quantum) Detector

- By Cooling Technology

- Uncooled Infrared Detector

- Cooled Infrared Detector

- By Material

- Microbolometer

- InGaAs (Indium Gallium Arsenide)

- MCT (Mercury Cadmium Telluride)

- Pyroelectric

- Thermopile

- By Spectral Range

- Near-Wave Infrared (NIR)

- Short-Wave Infrared (SWIR)

- Mid-Wave Infrared (MWIR)

- Long-Wave Infrared (LWIR)

- Far-Infrared (FIR)

- By Application

- People and Motion Sensing

- Temperature Measurement / Thermography

- Industrial Process Monitoring

- Spectroscopy and Biomedical Imaging

- Fire and Gas Detection

- Automotive ADAS and LiDAR

- Environmental and Agriculture Monitoring

- Other Applications (Building and HVAC Automation, Smart Homes, Military and Defense, etc.)

- By End-Use Industry

- Aerospace and Defense

- Industrial Manufacturing

- Automotive

- Oil, Gas and Energy

- Healthcare and Life Sciences

- Consumer Electronics

- Smart Infrastructure

- Others

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- New Zealand

- Rest of Asia-Pacific

- Middle East and Africa

- Middle East

- United Arab Emirates

- Saudi Arabia

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Nigeria

- Kenya

- Rest of Africa

- Middle East

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk work starts by building a clean fact base on where infrared detectors are used and what typically moves demand. We review public sources such as US Department of Defense budget documents, NASA and ESA technical publications, USGS and other government mineral statistics (for relevant compound supply context), and IEEE and similar peer-reviewed journals that discuss detector materials and performance trends.

Along with these, we also check company annual reports, investor presentations, trade association websites, and reputed press to map product lines and typical application pull. When needed, we use paid subscriptions for company financials and intelligence, patent databases, and import and export shipment-level databases to cross-check activity levels and price direction. This list is illustrative, and other public sources were also used for data collection, validation, and clarifying open questions.

Primary Interviews and Surveys

Primary work is used to pressure-test desk assumptions on adoption, pricing, and the split between cooled and uncooled demand. We speak with component suppliers, module integrators, OEM engineering teams, and procurement stakeholders across APAC, EMEA, and the Americas, so application-led signals (defense, industrial sensing, automotive, and security) are reflected in the final model.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 30% | CXOs: 12% | APAC: 44% |

| Mid tier: 54% | Functional/Unit leaders: 29% | EMEA: 33% |

| Smaller Players: 16% | Managers: 59% | Americas: 23% |

Market-Sizing & Forecasting

Sizing is built using top-down and bottom-up logic, where the demand pool is reconstructed from application adoption and procurement activity, and then validated using selective supplier and channel checks. In practice, we first estimate demand by end-use signals such as defense procurement cycles, industrial automation intensity, and safety and surveillance deployments, which are then translated into detector demand by the cooling mix and wavelength needs.

To keep the numbers grounded, a few practical inputs are tracked and updated each cycle, including cooled versus uncooled penetration by use case, typical average selling price ranges by material family (for example microbolometer, InGaAs, and MCT), shipment lead time trends that indicate backlog or digestion, and the share of demand tied to people and motion sensing versus measurement and inspection. Where bottom-up rollups are possible, we run sampled ASP times volume checks on a limited set of product classes to adjust totals when the implied unit economics do not line up.

Forecasting is done using scenario analysis supported by light multivariate regression, where key drivers such as defense spending direction, industrial production momentum, and automotive sensing adoption are varied within realistic ranges. When data gaps appear in smaller applications or newer spectral niches, we use proxies such as adjacent sensor adoption rates, then re-validate through follow-up calls before the results are finalized.

Data Validation & Update Cycle

Validation is handled through triangulation across independent signals, and then checked again through structured variance review before sign-off. Model outputs are compared with external indicators such as procurement timing, patenting activity direction, and reported product demand commentary, and outliers are flagged for rework.

Each major assumption is reviewed in more than one step, and respondents are re-contacted when pricing, cooling mix, or demand timing shifts materially. Reports are refreshed annually, and interim updates are triggered when material events occur, such as export rule changes, major program awards, or sudden supply constraints. Before delivery, we complete a fresh analyst pass so clients receive the latest updated view.

Mordor Intelligence's Infrared Detector Market Size Measured Against Other Published Estimates

Published market numbers for infrared detectors can look inconsistent, even when the topic label is the same, because the underlying counting rules are not always aligned. Differences usually come from what is counted as a detector sale, how mixed systems are handled, and which year is treated as the anchor for pricing and currency.

The table helps show where the spread is coming from. Under Mordor Intelligence's scope, the total stays focused on detector component revenues across wavelengths and cooling types, and it avoids folding in full camera systems or broader infrared sensing modules, which is a common reason some published totals land higher or lower.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 0.70 B (2025) | |

| Global Consultancy A | USD 0.62 B (2025) | Uses a tighter included-revenue definition that can undercount merchant detector value when detectors are bundled into modules, and it may apply more conservative ASP progression for cooled detectors in early forecast years. |

| Industry Research Group B | USD 0.57 B (2024) | Uses a different base year and can mix component and system-level revenue in selective applications, which makes year-to-year comparisons sensitive to currency timing and uneven refresh cadence. |

Looking across the three lines, most of the gap can be traced to scope boundaries around bundled modules and system-level revenues, plus differences in base year selection and pricing assumptions. With clearly defined inclusions, practical demand drivers, and repeated checks against observable market signals, we keep the estimate traceable and easy to reproduce with the same inputs.

Key Questions Answered in the Report

What is the forecast value of the infrared detector market in 2031?

The market is projected to reach USD 0.98 billion by 2031.

Which detector type is growing fastest through 2031?

Photo quantum arrays, particularly indium-gallium-arsenide and mercury-cadmium-telluride, are set to grow at 11.80% CAGR.

Why is short-wave infrared gaining traction in automotive applications?

1,550 nanometer SWIR enables higher eye-safe laser power for LiDAR, extending detection range to roughly 300 meters.

How do ITAR regulations influence global cooled detector sales?

Export licenses add up to 12 months and significant legal costs, steering some buyers toward uncooled or domestic alternatives.

Page last updated on: