ITSM Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 14.85 Billion |

| Market Size (2031) | USD 31.71 Billion |

| Growth Rate (2026 - 2031) | 16.38% CAGR |

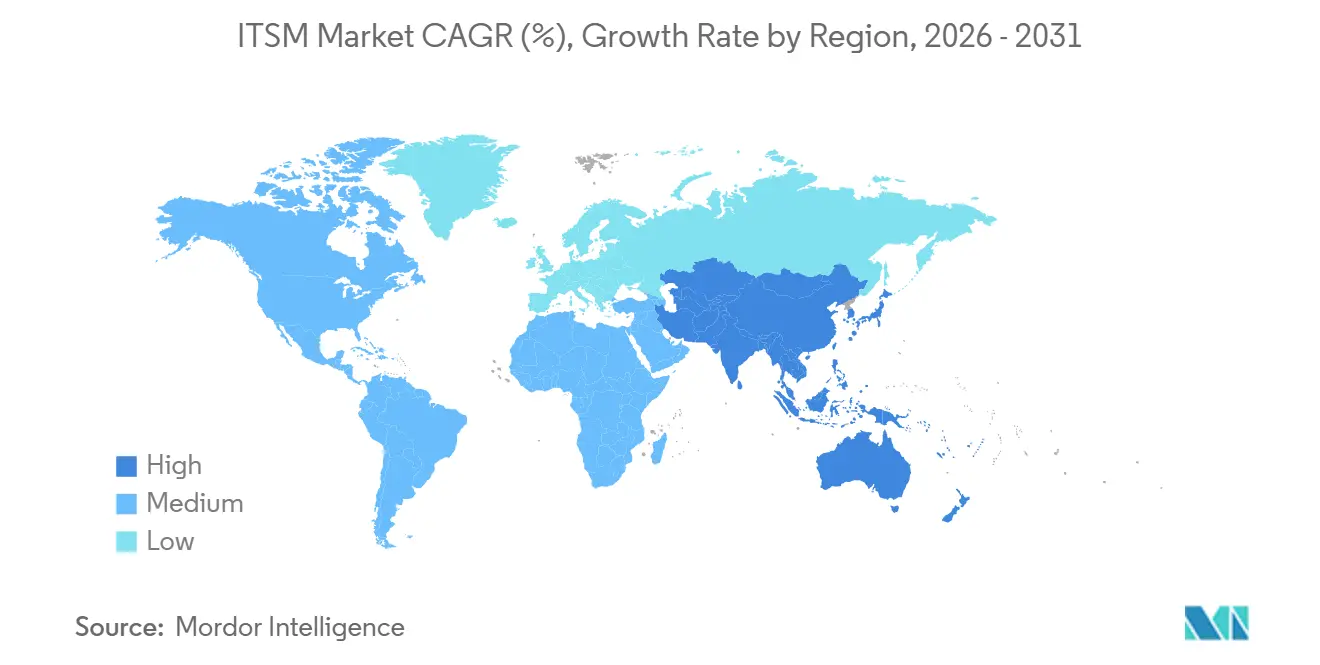

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

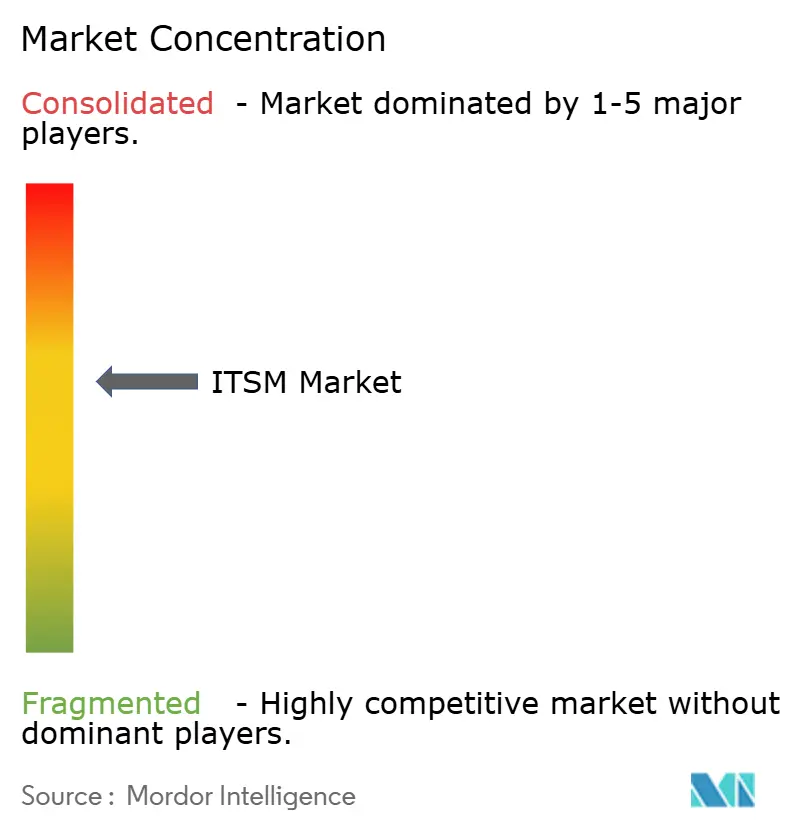

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

ITSM Market Analysis by Mordor Intelligence

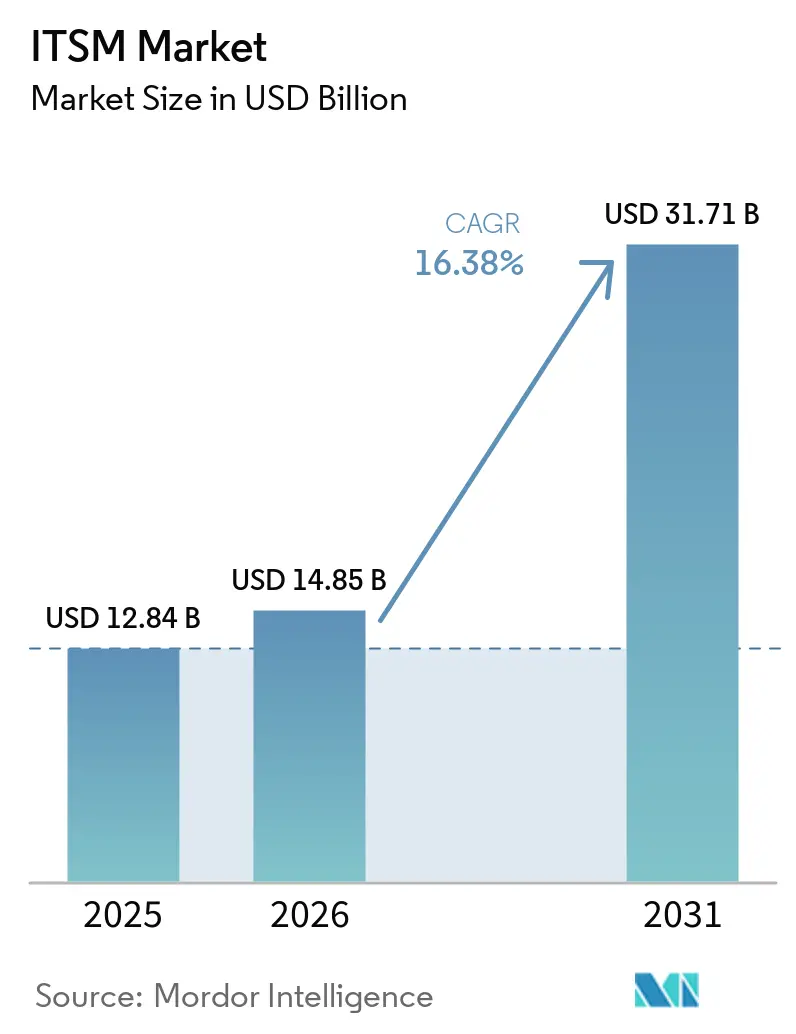

The IT service management market size is expected to increase from USD 12.84 billion in 2025 to USD 14.85 billion in 2026 and reach USD 31.71 billion by 2031, growing at a CAGR of 16.38% over 2026-2031. Growth is being shaped by steady enterprise movement away from on-premise service desk tools and toward cloud-native platforms that are updated more often and connected more tightly with modern infrastructure. Vendors are also building large language model and AIOps functions into core workflows, which is changing incident handling, service requests, knowledge delivery, and remediation across the IT service management market. The scope of the IT service management market is also moving beyond ticketing into financial oversight, sustainability reporting, and support for distributed edge operations, which broadens the role of service management inside day-to-day operations. This shift is making service management more central to business continuity, employee productivity, and digital service uptime, especially in organizations with hybrid infrastructure and rising compliance workloads. Competition in the IT service management market is therefore moving toward platform depth, integration breadth, and automation outcomes, while the largest opportunities remain in SME conversion, hybrid orchestration, and AI-enabled self-service.

Key Report Takeaways

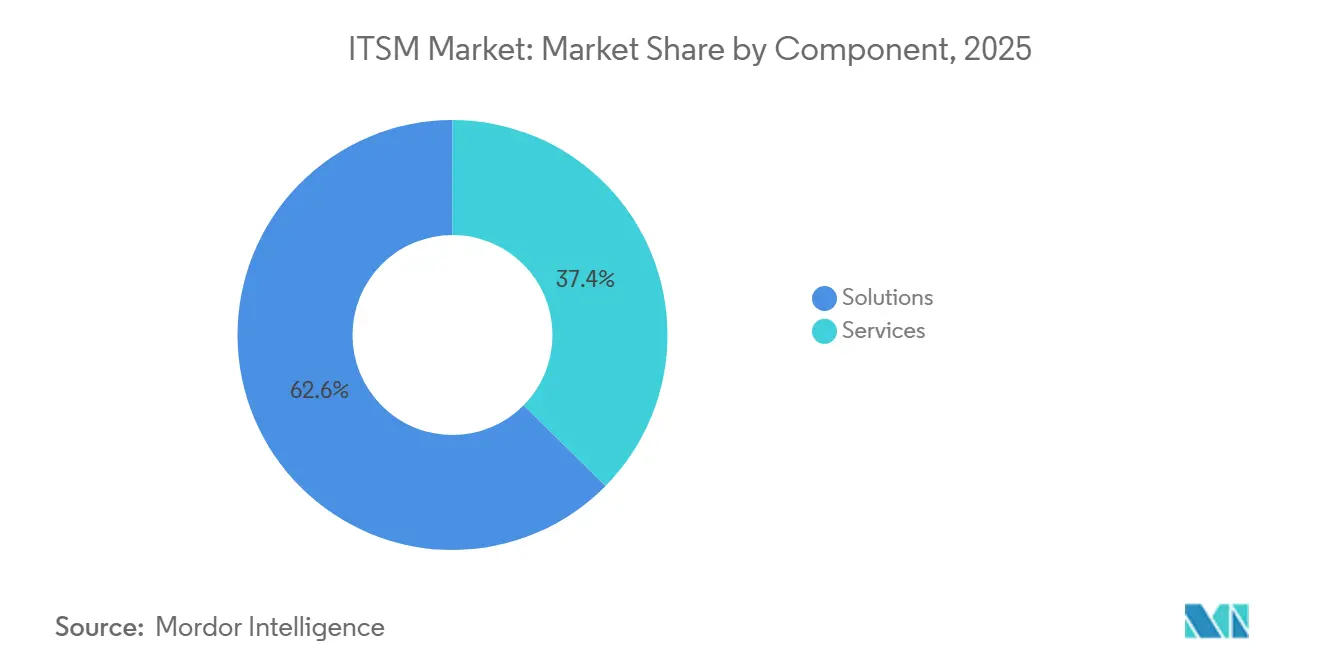

- By component, solutions held a 62.61% share of the ITSM market in 2025, while services are projected to expand at a 18.01% CAGR through 2031.

- By deployment, cloud held a 59.62% share of the ITSM market in 2025, and is projected to expand at a 18.21% CAGR through 2031.

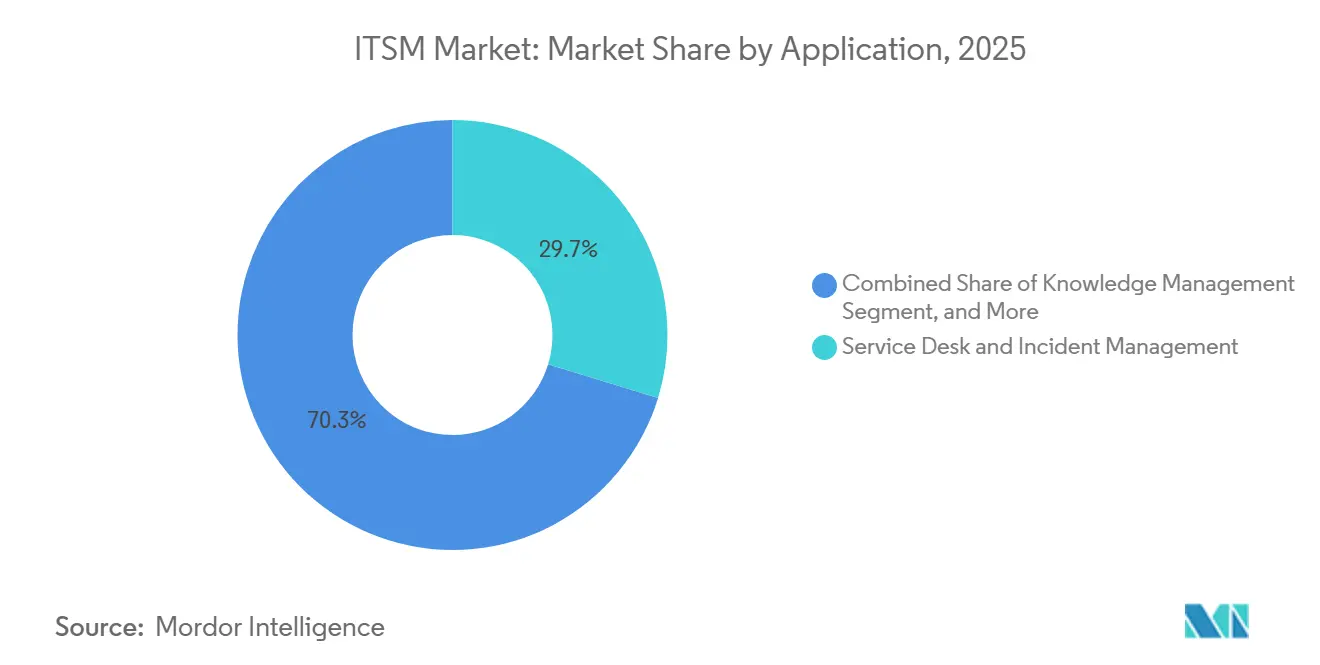

- By application, service desk and incident management led the ITSM market with a 29.73% share in 2025, while knowledge management is projected to expand at a 17.76% CAGR through 2031.

- By end-user industry, BFSI held 23.72% of the ITSM market share in 2025, while healthcare is projected to expand at a 17.86% CAGR through 2031.

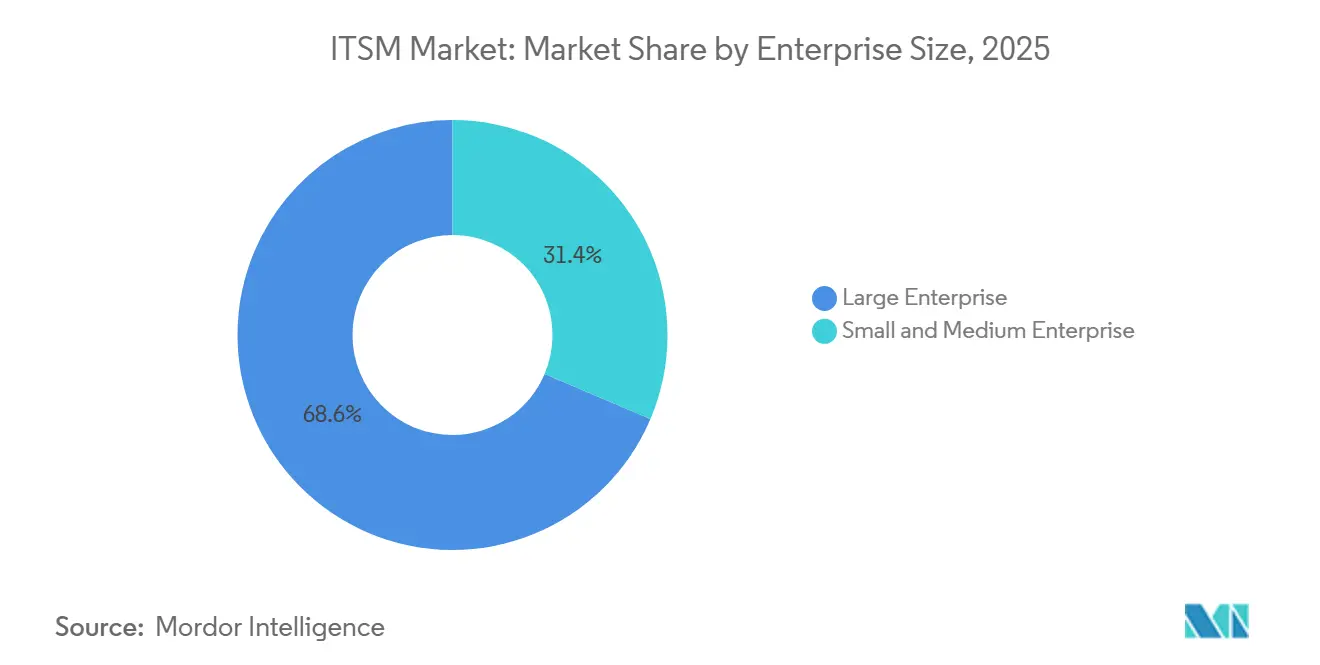

- By enterprise size, large enterprises held 68.62% of the ITSM market share in 2025, while SMEs are projected to expand at a 18.33% CAGR through 2031 in the IT service management market.

- By geography, North America held 38.02% share in 2025 of the ITSM market, while Asia-Pacific is projected to expand at a 19.90% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Market Trends and Insights

Drivers Impact Analysis of ITSM Market*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| AI-Driven Service Automation And AIOps Integration | +3.5% | Global | Short term (≤ 2 years) |

| Shift To Cloud-Native ITSM Platforms | +2.9% | North America and Europe, expanding to APAC | Medium term (2-4 years) |

| Unified Management For Hybrid And Multicloud Estates | +2.3% | North America, APAC core | Medium term (2-4 years) |

| Low-Code And No-Code Orchestration For Citizen ITSM | +1.7% | North America, Western Europe | Medium term (2-4 years) |

| FinOps And GreenOps Reporting Embedded In ITSM | +1.1% | North America and EU | Long term (≥ 4 years) |

| Edge Computing And 5G Operations Onboarding To ITSM | +0.6% | APAC, Middle East | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

AI-Driven Service Automation And AIops Integration

AI is moving from support assistance into direct workflow execution across the IT service management market. Vendors now position autonomous agents to resolve service desk cases, manage incidents, and support employee workflows with less manual intervention than earlier copilots allowed.[1]ServiceNow Newsroom Staff, “ServiceNow Brings Autonomous Workforce to Every Major Business Function,” ServiceNow Newsroom, servicenow.com Freshworks also expanded AI service delivery with Agent Studio, MCP Gateway, and xLA support, which shows that automation is becoming part of platform design rather than an optional feature layer. As these tools mature, the IT service management market is shifting from faster ticket handling toward more proactive detection, routing, and remediation, especially where incident data, workflows, and knowledge assets sit on the same platform. That makes platform consolidation more valuable because isolated AI tools do not carry the same workflow context or governance depth as integrated systems built for enterprise control.[2]IBM Newsroom Staff, “IBM and ServiceNow Expand Collaboration to Unlock Enterprise Data for AI at Scale,” IBM Newsroom, ibm.com

Shift To Cloud-Native ITSM Platforms

Cloud-native design remains a strong growth force in the IT service management market because it supports faster releases, easier scaling, and broader integration with collaboration, identity, and DevOps systems. Vendors can update SaaS environments more frequently than on-premise deployments, which keeps AI features, workflow templates, and compliance tools moving into production at a quicker pace. This difference matters because buyers increasingly compare platforms on how quickly useful functions arrive after purchase, not only on initial deployment choice. The cloud model also fits subscription spending patterns and reduces infrastructure management work for customers, which improves adoption across both large enterprises and smaller organizations. Even where regulated users retain some private infrastructure, the IT service management market continues to benefit because hybrid models still depend on cloud-led orchestration and service design.

Unified Management For Hybrid And Multicloud Estates

Large enterprises now run service environments across public cloud, private cloud, and on-premise systems, which raises the value of a single control layer in the IT service management market. Buyers want platforms that can absorb alerts, configuration items, and change events from several environments without creating separate process silos. IBM and ServiceNow expanded their collaboration in June 2026 to connect Red Hat Ansible, Instana, watsonx.data, and HashiCorp Terraform with ServiceNow workflows, which directly addresses issue detection and remediation across mixed estates. That kind of partnership shows that operational control is now built through deep integration with infrastructure tools rather than through a closed single-vendor stack. The IT service management market gains from this shift because hybrid complexity creates a steady need for orchestration, data unification, and automated operational handoffs.

Low-Code And No-Code Orchestration For Citizen ITSM

Low-code and no-code tools are widening the buyer base for the IT service management market by reducing reliance on specialist developers for routine workflow changes. Business teams can configure approval paths, portals, knowledge flows, and service forms with less delay, which makes ITSM programs easier to expand into adjacent functions. Ivanti added persona-based agentic AI and broader conversational capabilities to Neurons for ITSM in 2026, which reflects the push toward simpler configuration and faster automation setup.[3]Ivanti Staff, “Ivanti Enhances Autonomous Capabilities Across IT and Security Operations with AI-Driven Neurons Platform,” Ivanti, ivanti.com Freshworks also highlighted that 47% of IT tickets were submitted outside business hours, which supports demand for easy-to-configure autonomous service workflows that can run without overnight staffing growth. As a result, the IT service management market is becoming more accessible to organizations that want process automation without long development cycles or heavy scripting overhead.

Restraints Impact Analysis of ITSM Market*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Legacy Migration Complexity And High Switching Cost | -2.1% | Global, most acute in large enterprises, BFSI, and government | Medium term (2-4 years) |

| Shortage Of Skilled ITSM And ITOM Professionals | -1.6% | Global, most severe in APAC and emerging markets | Short term (≤ 2 years) |

| Emerging AI Governance And Data Residency Regulations | -1.0% | Europe, APAC | Medium term (2-4 years) |

| Rising Observability Data Costs Causing Tool Sprawl | -0.7% | Global, acute in mid-market enterprises | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Legacy Migration Complexity And High Switching Cost

Migration remains a real barrier in the IT service management market because large deployments often carry years of workflow customization, CMDB structure changes, and service history. That complexity raises the cost of vendor switching, especially in regulated environments where change approval, asset relationships, and audit records are tightly embedded in the platform. IBM and ServiceNow framed legacy modernization and AI-ready data as a joint enterprise problem in their 2026 collaboration update, which reflects how difficult older environments are to modernize without coordinated tooling and process work. BMC also continued CMDB and suite-level enhancements in its 2026 Helix releases, which underlines the operational weight that configuration data and platform structure still carry in enterprise service management. This keeps renewal decisions cautious across the IT service management market, because buyers must weigh feature gains against operational disruption, retraining, and data transition risk.

Shortage Of Skilled ITSM And ITOM Professionals

The talent gap continues to slow parts of the IT service management market, especially where organizations need both service management knowledge and modern automation skills. OTRS Group reported in June 2025 that 40% of SMBs cited talent shortages as a top-three constraint, 62% lacked adequate training and education to improve ITSM practices, and only 12% had a fully mature ITSM framework. This shortage lengthens rollout timelines, limits integration quality, and makes governance harder when organizations try to expand from ticketing into broader workflow automation. It also creates uneven adoption because better-resourced buyers can answer the problem with AI and managed services, while smaller teams still struggle with setup and day-to-day administration. The IT service management market therefore grows faster where platforms reduce admin effort, simplify configuration, and shorten the path from purchase to usable process automation.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

ITSM Market Segment Analysis

By Component:

Solutions Platform Dominance Shapes Revenue MixThe Solutions segment held 62.61% of the IT service management market share in 2025, which reflected the shift from project-heavy deployments toward recurring platform subscriptions. This lead shows that buyers increasingly value the software layer itself, rather than the consulting effort required to install it. In the IT service management market, cloud delivery has shortened deployment cycles and moved more spending toward licensing, workflow modules, and AI-enabled add-ons. Solutions are projected to show a significant CAGR through 2031, which keeps this segment at the center of value capture as vendors sell more automation, knowledge, and compliance functions. That growth also reflects the way customers now expect ongoing product improvement rather than long gaps between major upgrades.

Services are projected to expand at a 18.01% CAGR through 2031. The Services segment matters because large buyers continue to need implementation support, integration work, managed administration, and training to keep complex environments stable. Demand for these services rises when organizations migrate from legacy tools, extend workflows beyond IT, or bring hybrid infrastructure into a single operating model. In the IT service management industry, services also support customers that lack in-house process depth, especially when AI capabilities require careful governance and data cleanup before deployment. The service mix is changing as well, because managed services and fixed-scope migration packages reduce the perceived burden of modernization for mid-market buyers. Even so, the revenue balance in the IT service management market keeps moving toward solutions because recurring platform value is growing faster than one-time deployment work.

By Deployment:

Cloud Extends Lead, Hybrid Gains Ground In Regulated SectorsCloud deployment accounted for 59.62% share of the IT service management market size in 2025, which confirmed that SaaS has become the default choice for new platform buying. The cloud segment is projected to expand at a 18.21% CAGR through 2031, which keeps it ahead of other deployment models across the IT service management market. Buyers favor cloud because it reduces infrastructure overhead, supports elastic user growth, and allows vendors to deliver new capabilities without customer-led upgrade cycles. This matters more in 2026 because AI agents, observability links, and automation templates are changing fast, and customers want access to those updates as they are released. Cloud also fits subscription spending models, which has made enterprise-grade ITSM more reachable for organizations that once delayed adoption for budget reasons.

On-premise remains relevant in government, central banking, defense, and other settings where data location and security policy limit full SaaS use. These organizations still need service management, but they often buy it through tightly controlled infrastructure and longer release cycles. Hybrid models are therefore gaining ground because they let enterprises place high-volume service desk workflows in the cloud while retaining sensitive change and configuration data on private systems. This keeps the IT service management market balanced between innovation access and control requirements rather than forcing a full switch in every account. Over time, hybrid demand also supports vendors with strong orchestration and policy management, because mixed environments need stable process control across several technology layers.

By Application:

Service Desk Anchors Demand, Knowledge Management AcceleratesService Desk and Incident Management held the largest application share at 29.73% in 2025, which showed that core support operations still anchor platform buying in the IT service management market. Every organization with a formal IT function needs request logging, routing, escalation, and resolution tracking, which makes this the most common starting point for adoption. Its lead also reflects the fact that service desk processes generate the operational data that later supports automation, reporting, and broader service governance. Asset and Configuration Management, along with Change and Release Management, remain important because regulated and hybrid environments need strong visibility into systems, dependencies, and approved changes. These functions reinforce platform stickiness because once process data and approvals are embedded, customers are less likely to move quickly.

Knowledge Management is projected to expand at a 17.76% CAGR through 2031, making it the fastest-growing application area in the IT service management market. Growth here is tied to AI-generated articles, automated solution linking, and more capable self-service experiences that reduce pressure on frontline support teams. Knowledge assets are also becoming more important because they improve consistency between human agents and autonomous workflows. Service Request Management and other ITSM uses, including enterprise service management extensions into HR, finance, and facilities, are widening the practical scope of the platform. This means the IT service management market is no longer defined only by incident response, because the same workflow engine is now being used to manage a wider set of internal service interactions.

By End-User Industry:

BFSI Leads, Healthcare Captures Growth PremiumBFSI accounted for 23.72% of the market in 2025, which made it the largest end-user segment in the IT service management market. This position reflects the sector’s need for high uptime, strict change control, strong audit trails, and dependable support for complex digital service environments. Financial institutions depend on service continuity across customer channels, transaction platforms, and internal control systems, which makes governed IT operations essential. The segment also benefits from long-standing process maturity, because large banks and insurers are more likely to formalize service frameworks and invest in platform-wide governance. That combination supports steady platform demand even when deployment cycles are careful and migration decisions take longer.

Healthcare is projected to expand at a 17.86% CAGR through 2031, which makes it the fastest-growing end-user segment in the IT service management market. Growth comes from continued digitization of clinical workflows, broader use of connected devices, and rising need for compliance-ready support processes. Healthcare environments also place pressure on response speed, asset visibility, and change discipline because operational disruptions can affect care delivery as well as back-office performance. Manufacturing, government and public sector, IT and telecommunications, retail and e-commerce, travel and hospitality, and other end-user groups make up the rest of the addressable base. Across these verticals, the IT service management industry benefits most where service uptime, process accountability, and workflow standardization have direct operational consequences.

By Enterprise Size:

Large Enterprises Lead, SMEs Drive Adoption UpsideLarge enterprises held 68.62% of the market in 2025, which reflected the scale of their IT estates and the maturity of their governance requirements in the IT service management market. These organizations usually manage more users, more assets, and more layered approval structures, which supports larger platform contracts. They also pursue consolidation, replacing disconnected departmental tools with a common system for incidents, changes, assets, and knowledge. That approach makes enterprise buyers important to vendors because a single contract can cover several functions and business units. It also explains why platform breadth, integration depth, and global support remain critical competitive factors in the top tier.

SMEs are projected to expand at a 18.33% CAGR through 2031, making them the fastest-growing enterprise size segment in the IT service management market. Their growth reflects a simple economic change, because subscription delivery has lowered the entry barrier for organizations that previously relied on email, spreadsheets, or basic ticketing tools. OTRS Group reported in June 2025 that only 12% of SMBs had a fully mature ITSM framework and that 56% viewed modernization as a strategic opportunity, which points to a large conversion pool still open to vendors. Products aimed at this segment compete on fast setup, low admin effort, and predictable pricing, because those features matter more than deep customization for many smaller teams. This leaves SMEs as one of the clearest expansion spaces in the IT service management market, especially for vendors that can pair usability with credible automation.

Geography Analysis

North America and Europe ITSM Market

North America held 38.02% of the IT service management market size in 2025, which kept it in the leading regional position. The region benefits from high cloud maturity, established service management practices, and a concentrated presence of major vendors and large enterprise buyers. The United States remained the main revenue center because financial services, technology, and healthcare organizations continued to invest in governed digital operations across the IT service management market. Canada supported demand through public sector digitization and enterprise modernization, while Mexico benefited from nearshoring-related infrastructure expansion and a growing need for process control. Europe remained the second-largest regional market, supported by manufacturing, financial services, and telecommunications demand across mature enterprise environments.

APAC ITSM Market

Asia-Pacific is projected to expand at a 19.90% CAGR through 2031, which makes it the fastest-growing region in the IT service management market. India is a major driver because domestic cloud adoption, data localization requirements, and the scale of the outsourcing base continue to push investment in formal service management capabilities. China adds volume through large enterprise deployments in manufacturing and banking, where process consistency and operational oversight remain important. Japan also supports growth as organizations invest more in automation and structured IT operations to manage service quality across complex technology estates. Across Southeast Asia, greenfield adoption supports the IT service management market because many buyers move directly to cloud-first platforms instead of carrying long on-premise replacement cycles.

South America and MEA ITSM Market

South America remains smaller in value, but Brazil and Argentina continue to generate most regional demand through modernization work in financial services and government. These buyers often adopt formal service management as part of broader digitization programs, which supports steady but selective growth. The Middle East gains support from national digital transformation agendas in Saudi Arabia and the UAE, where public sector and telecom investments are expanding process-led service operations. Africa is still earlier in adoption, but South Africa, Nigeria, and Egypt present room for cloud-first growth because they can adopt current platforms without the same legacy burden seen in older enterprise environments.

Competitive Landscape

The competitive structure of the IT service management market is moderately concentrated in the enterprise tier, with ServiceNow holding the strongest overall platform position while several rivals remain credible across specific account types. ServiceNow continued to frame its platform around governed autonomous work in 2026, and the company highlighted the scale of its workflow footprint as it expanded AI-led operating capabilities. Its May 2026 rollout of Autonomous Workforce and its acquisition announcement around Armis showed a clear push to extend service management into broader operational and asset intelligence use cases. IBM’s June 2026 partnership expansion with ServiceNow added another layer to that strategy by linking infrastructure automation, observability, and enterprise data with service workflows. These moves raise switching costs because customers gain more value when ITSM is embedded in a wider operating stack instead of running as a stand-alone ticketing tool.

BMC, Atlassian, Salesforce, Ivanti, and other established vendors continue to compete through different product strengths rather than identical feature sets. BMC has focused on AI-augmented service management and ongoing CMDB refinement through its 2026 Helix releases, which helps it stay relevant with complex enterprise accounts that value process depth and configurability. Ivanti has pushed conversational and persona-based agentic capabilities in Neurons for ITSM, which supports buyers that want broader workflow accessibility and faster automation setup. Freshworks keeps applying pressure from the mid-market with transparent packaging, lower deployment friction, and AI-led service operations that fit organizations looking for faster time to value. This mix keeps the IT service management market competitive because buyers can choose between broad enterprise suites and simpler products that emphasize ease of use.

The mid-market remains more fragmented, with specialist and regional vendors competing on cost, local support, and narrower compliance needs. White space in the IT service management market remains strongest in SME adoption, healthcare workflow integration, and enterprise service management rollouts outside core IT teams. FinOps Foundation reported in 2026 that 98% of respondents were managing AI spend, which supports the broader pull toward connected platforms that can tie cost control, observability, and remediation into one operating flow. As that convergence continues, the IT service management market is likely to reward vendors that combine governance, automation, and integration depth without making deployment too heavy for smaller buyers.

ITSM Industry Leaders

ServiceNow, Inc.

IBM Corporation

BMC Software, Inc.

Atlassian Corporation Plc

Ivanti, Inc.

- *Disclaimer: Major Players sorted in no particular order

ITSM Market Companies Covered in this Report

- ServiceNow, Inc.

- IBM Corporation

- BMC Software, Inc.

- Atlassian Corporation Plc

- Ivanti, Inc.

- Freshworks Inc.

- ManageEngine, a division of Zoho Corporation Pvt. Ltd.

- Broadcom Inc.

- Open Text Corporation

- Micro Focus International plc

- ASG Technologies Group, Inc.

- SysAid Technologies Ltd.

- Cherwell Software, LLC

- TOPdesk B.V.

- Hornbill Service Management Ltd.

- SymphonyAI Summit

- EasyVista S.A.

- SolarWinds Corporation

- Atlassian Corporation Plc

- Axelos Limited

Recent Industry Developments in ITSM Market

- June 2026: IBM and ServiceNow announced an expanded multi-year collaboration combining IBM's Red Hat Ansible, IBM watsonx.data, Instana, and HashiCorp Terraform with the ServiceNow AI Platform to enable enterprise legacy modernization and autonomous IT operations across multi-vendor estates. Joint solutions were scheduled for availability in the second half of 2026, with the partnership targeting the AI-ready data problem and legacy application modernization gap at the largest enterprises globally.

- May 2026: Freshworks unveiled the Freddy AI Agent Studio within Freshservice at its annual Refresh conference, introducing the Model Context Protocol, MCP, Gateway for third-party AI context integration, Experience Level Agreements, xLAs, for AI-powered service delivery metrics, and a unified ServiceOps platform connecting ITSM, IT Asset Management, ITAM, and ITOM on a single shared data layer. Internal telemetry showed 47% of IT tickets were submitted outside business hours, directly justifying the autonomous after-hours resolution architecture.

- May 2026: ServiceNow launched the Autonomous Workforce at Knowledge 2026, unveiling AI specialists for IT service desk, CRM, employee service, and security and risk functions capable of autonomously resolving cases and managing incidents end to end. ServiceNow simultaneously introduced Otto, a new enterprise AI experience unifying conversational AI, autonomous workflows, and enterprise search, and announced the acquisition of Armis, an OT and IoT asset intelligence platform extending ITSM coverage into operational technology environments.

- January 2026: ServiceNow launched the Autonomous Workforce initiative, adding Moveworks to the ServiceNow AI Platform for conversational employee support and positioning the L1 IT Service Desk AI Specialist, handling password resets, software provisioning, and network troubleshooting autonomously using enterprise knowledge bases and historical incident data.

Global ITSM Market Report Scope

The IT Service Management Market is Segmented by Component (Solutions, Services), Deployment (Cloud, On-Premise, Hybrid), Application (Service Desk and Incident Management, Asset and Configuration Management, Change and Release Management, Service Request Management, Knowledge Management, Others), End-User Industry (BFSI, Manufacturing, Government and Public Sector, IT and Telecommunications, Retail and E-Commerce, Healthcare, Others), Enterprise Size (Large Enterprises, SME), and Geography (North America, South America, Europe, Asia-Pacific, Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Segmentation Overview

| Solutions |

| Services |

| Cloud |

| On-Premise |

| Hybrid |

| Service Desk and Incident Management |

| Asset and Configuration Management |

| Change and Release Management |

| Service Request Management |

| Knowledge Management |

| Other ITSM Applications |

| BFSI |

| Manufacturing |

| Government and Public Sector |

| IT and Telecommunications |

| Retail and E-Commerce |

| Healthcare |

| Travel and Hospitality |

| Other End-User Industries |

| Large Enterprises |

| Small and Mid-Size Enterprises (SME) |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Russia | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Southeast Asia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Egypt | ||

| Rest of Africa | ||

| By Component | Solutions | ||

| Services | |||

| By Deployment | Cloud | ||

| On-Premise | |||

| Hybrid | |||

| By Application | Service Desk and Incident Management | ||

| Asset and Configuration Management | |||

| Change and Release Management | |||

| Service Request Management | |||

| Knowledge Management | |||

| Other ITSM Applications | |||

| By End-User Industry | BFSI | ||

| Manufacturing | |||

| Government and Public Sector | |||

| IT and Telecommunications | |||

| Retail and E-Commerce | |||

| Healthcare | |||

| Travel and Hospitality | |||

| Other End-User Industries | |||

| By Enterprise Size | Large Enterprises | ||

| Small and Mid-Size Enterprises (SME) | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Russia | |||

| Spain | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Southeast Asia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Egypt | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the 2026 size of the IT service management market?

The IT service management market stands at USD 14.85 billion in 2026 and is forecast to reach USD 31.71 billion by 2031 at a 16.38% CAGR.

Which region leads global demand for IT service management?

North America led with 38.02% share in 2025, supported by strong cloud maturity, large enterprise buying, and a concentrated vendor presence.

Which region is growing the fastest through 2031?

Asia-Pacific is forecast to grow at a 19.90% CAGR through 2031, driven by cloud adoption, enterprise digitization, and expanding automation needs.

Which deployment model is most widely used?

Cloud led with 59.62% share in 2025 and is also the fastest-growing deployment model, reflecting buyer preference for faster updates and lower infrastructure burden.

Which end-user group creates the most demand?

BFSI held the largest end-user share at 23.72% in 2025 because regulated, always-on financial environments need strong operational governance and service continuity.

Page last updated on: