Inflammatory Bowel Therapeutics Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

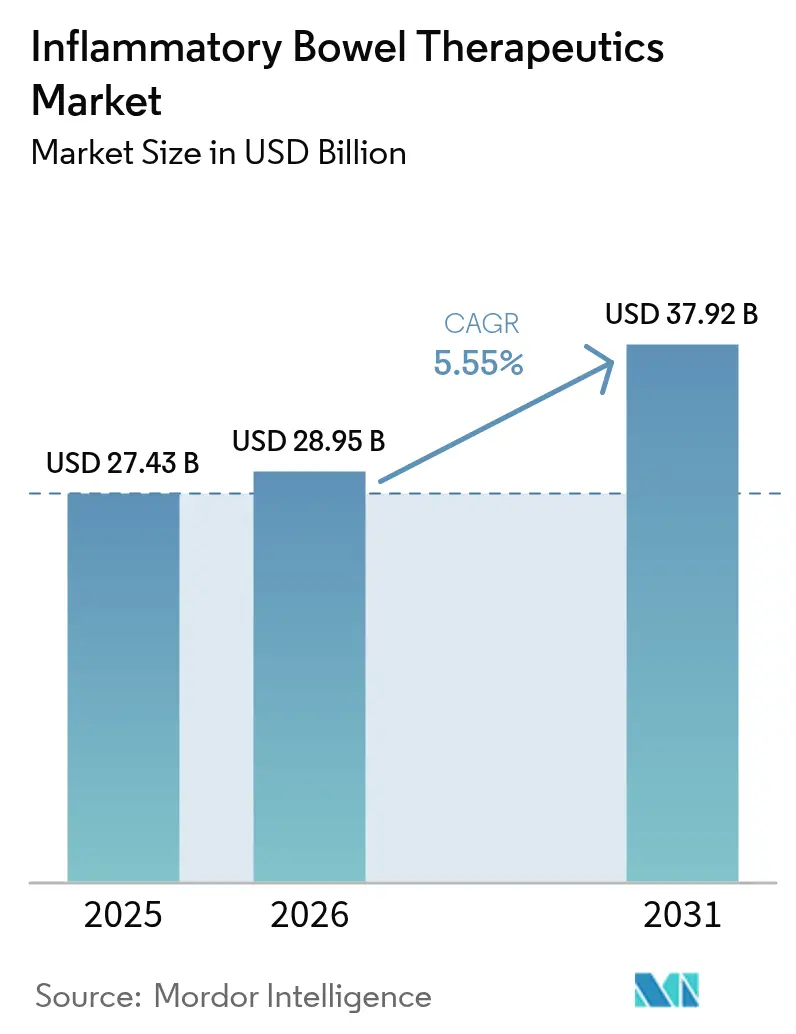

| Market Size (2026) | USD 28.95 Billion |

| Market Size (2031) | USD 37.92 Billion |

| Growth Rate (2026 - 2031) | 5.55% CAGR |

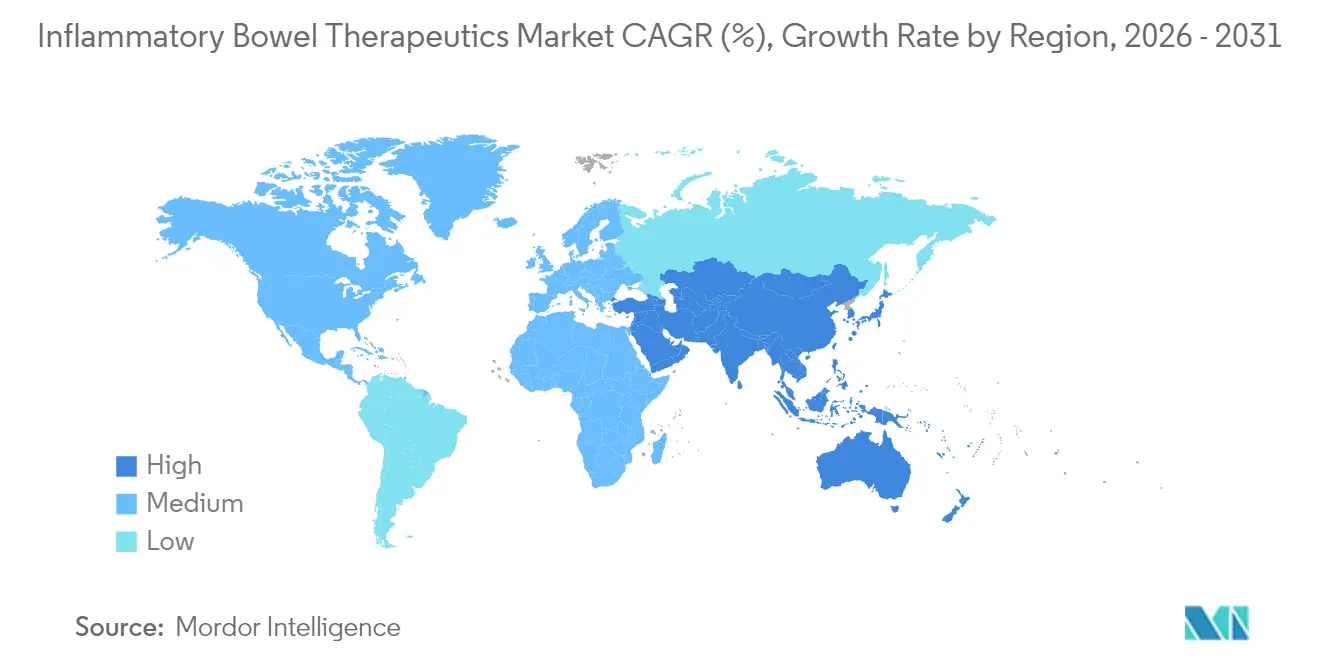

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Inflammatory Bowel Therapeutics Market Analysis by Mordor Intelligence

The inflammatory bowel therapeutics market size is expected to grow from USD 27.43 billion in 2025 to USD 28.95 billion in 2026 and is forecast to reach USD 37.92 billion by 2031 at 5.55% CAGR over 2026-2031. The inflammatory bowel therapeutics market is benefiting from a late-stage pipeline rich in anti-IL-23 and TL1A agents, the rapid commercial uptake of oral JAK inhibitors, and a decisive swing toward biosimilars that is widening patient access in insured as well as cost-sensitive regions. Physician adherence to treat-to-target guidelines that call for early biologic use and endoscopic remission as the primary endpoint is accelerating product adoption, while supply-chain investments are gradually easing manufacturing bottlenecks for complex biologics. AbbVie’s pivot from Humira to Skyrizi and Rinvoq underscores a broader industry transition away from TNF-alpha dominance and toward precision immunology, small-molecule convenience, and portfolio diversification.

The market’s momentum is reinforced by strong performance of ulcerative colitis drugs, continued double-digit growth in oral formulations, and a rising share of digital adherence solutions that improve real-world outcomes. Crohn’s disease therapies are expanding faster than the overall market, contract development and manufacturing organizations (CDMOs) are adding new capacity, and payer demands for value-based contracting are forcing manufacturers to combine innovation with disciplined pricing strategies. North America remains the largest revenue contributor, but Asia-Pacific is the fastest-growing region as regulators harmonize biosimilar pathways and governments invest in specialty care infrastructure. Collectively, these dynamics point to a resilient outlook for the inflammatory bowel therapeutics market.

Key Report Takeaways

- By disease, ulcerative colitis led with 51.68% of inflammatory bowel therapeutics market share in 2025, while Crohn’s disease is poised to expand at an 8.32% CAGR to 2031.

- By drug class, TNF inhibitors retained 35.95% share of the inflammatory bowel therapeutics market size in 2025 and JAK inhibitors are advancing at a 6.85% CAGR through 2031.

- By route of administration, parenteral products accounted for 75.62% of the inflammatory bowel therapeutics market size in 2025; oral therapies are growing at an 8.08% CAGR to 2031.

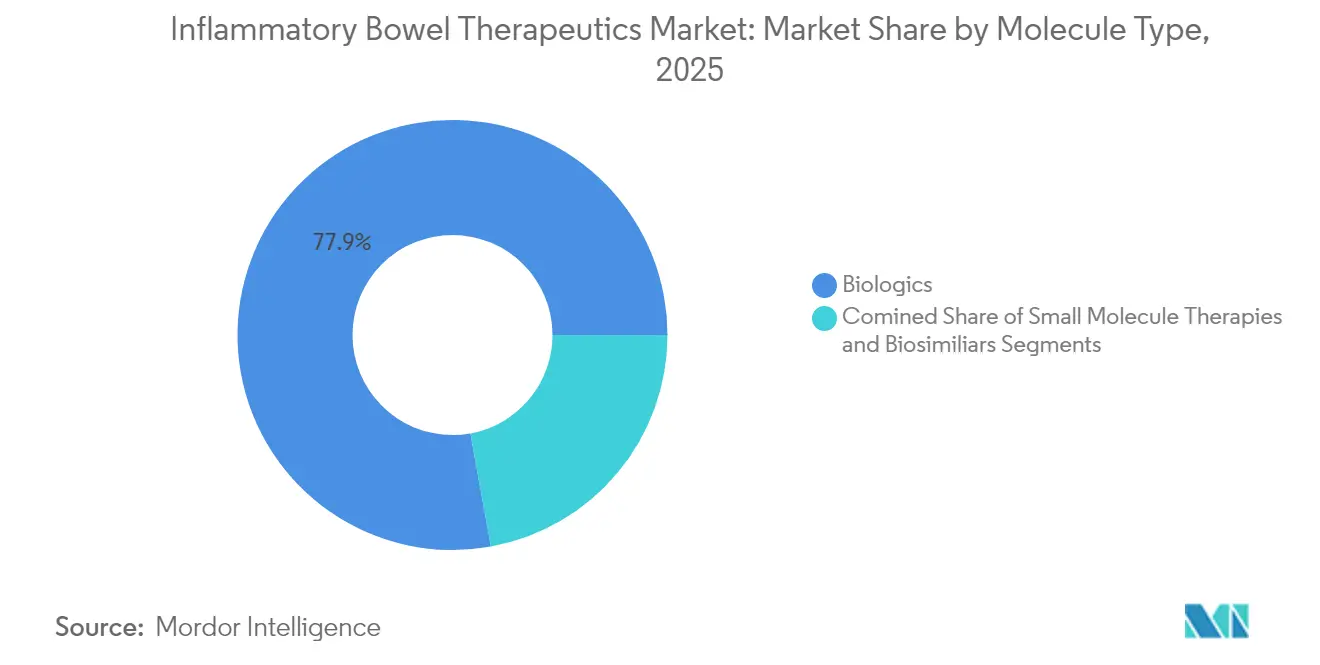

- By molecule type, biologics commanded 77.86% of revenue in 2025 while small-molecule therapies are forecast to rise at a 9.29% CAGR between 2026 and 2031.

- By distribution channel, hospital pharmacies controlled 47.31% of global sales in 2025, whereas online pharmacies are on course for a 9.17% CAGR amid direct-to-patient fulfillment gains.

- By geography, North America held 35.84% of the inflammatory bowel therapeutics market share in 2025 and Asia-Pacific is projected to post the highest 8.21% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Inflammatory Bowel Therapeutics Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Intensifying Late-Stage Pipeline For Anti-IL-23 & TL1A Agents | +0.7% | Global, with early gains in North America & EU | Medium term (2-4 years) |

| Rapid Uptake Of Oral JAK Inhibitors In Moderate-To-Severe UC & CD | +1.2% | North America & EU core, spill-over to APAC | Short term (≤ 2 years) |

| Expansion Of Treat-To-Target Guidelines Boosting Early Biologic Use | +0.9% | Global, with advanced implementation in North America | Medium term (2-4 years) |

| Mainstream Biosimilar Penetration Driving Patient Access | +0.8% | EU leading, North America accelerating, APAC emerging | Long term (≥ 4 years) |

| Rise Of Digital Adherence Solutions Improving Real-World Outcomes | +0.6% | North America & EU, expanding to APAC | Medium term (2-4 years) |

| Investment In Microbiome-Based Adjunct Therapies | +0.4% | Global research hubs, commercial focus in North America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Intensifying Late-Stage Pipeline for Anti-IL-23 & TL1A

Anti-IL-23 drugs are displacing legacy TNF blockers as Phase 3 data confirm superior endoscopic remission rates; risankizumab achieved 31.8% at week 48 versus ustekinumab’s 16.2% in a head-to-head trial. The European regulator issued a positive opinion for risankizumab in ulcerative colitis, setting the stage for a continent-wide launch. Eli Lilly’s mirikizumab is in late-stage testing alongside tirzepatide to address obesity comorbidities, underscoring the market’s move toward multi-disease management. TL1A inhibitors are moving through proof-of-concept studies as drug makers strive for intestine-specific anti-inflammatory action without systemic immune suppression. These combined efforts are set to reshape treatment algorithms and reallocate revenue streams within the inflammatory bowel disease (IBD) therapeutics market.

Rapid Uptake of Oral JAK Inhibitors in Moderate-to-Severe UC & CD

Oral JAK inhibitors have broken the injection barrier that discouraged some patients from initiating biologic therapy. Tofacitinib and upadacitinib deliver efficacy comparable to infusion-based biologics, while copay savings programs cut out-of-pocket costs for eligible patients. The United States FDA has refined the REMS program to balance vigilance with prescriber convenience, and real-world data are clarifying cardiovascular and malignancy risk profiles in IBD populations. Pediatric trials of etrasimod in adolescents signal that the addressable pool will grow as age restrictions fall. This convergence of clinical data, patient demand, and payer support is translating into a materially higher growth contribution from oral therapies to the inflammatory bowel disease (IBD) therapeutics market.

Expansion of Treat-to-Target Guidelines Boosting Early Biologic Use

The STRIDE-II framework positions endoscopic remission as the primary outcome, prompting clinicians to escalate therapy faster and favor biologics earlier in the disease course.[1]Noor et al., “A Biomarker-Stratified Comparison of Top-Down vs Accelerated Step-Up Treatment Strategies for Patients with Newly Diagnosed Crohn’s Disease (PROFILE),” The Lancet, thelancet.com Biomarker-driven dosing tools such as the REMODEL-CD algorithm are demonstrating fewer treatment failures and longer drug persistence in pediatric patients.[2] Phillip Paul Minar, “Precise Infliximab Exposure and Pharmacodynamic Control to Achieve Deep Remission in Paediatric Crohn’s Disease (REMODEL-CD): Study Protocol for a Multicentre, Open-Label, Pragmatic Clinical Trial in the USA,” BMJ Open, bmjopen.bmj.com Updated American Gastroenterological Association recommendations de-emphasize adalimumab as first-line therapy in complex Crohn’s disease, redirecting demand toward IL-23 and JAK inhibitors. As adoption widens, early biologic starts increase revenue per patient and lift long-run adherence, fortifying the revenue outlook for the inflammatory bowel disease (IBD) therapeutics market.

Mainstream Biosimilar Penetration Driving Patient Access

Adalimumab biosimilars reached an 18% prescription share by mid-2024 after key formulary switches by large US pharmacy benefit managers. Sandoz’s Hyrimoz now captures most biosimilar scripts under the CVS Cordavis label, showing how PBM policies can override lingering prescriber hesitancy. Payer incentives are estimated to save national health systems up to USD 6 billion, though PBMs must offset lost rebate income. Gastroenterologists are embracing switching faster than dermatologists, and AbbVie has responded by cutting Humira list prices by up to 86% while channeling investment into Skyrizi and Rinvoq. As competitive pricing reshapes formularies, the inflammatory bowel disease therapeutics market gains new demand from previously untreated or under-treated patients.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent REMS & Boxed Warnings For JAK Class | -0.8% | North America leading, EU following, APAC adapting | Short term (≤ 2 years) |

| High Biologic Pricing Pressure From Payers & HTA Bodies | -0.5% | Global, with intense scrutiny in EU & emerging markets | Medium term (2-4 years) |

| Manufacturing Capacity Bottlenecks For Complex Biologics | -0.4% | Global supply chains, acute in North America & EU | Long term (≥ 4 years) |

| Patient Reluctance Toward Long-Term Immunosuppression | -0.3% | Global, with cultural variations across regions | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Stringent REMS & Boxed Warnings for JAK Class

Uptake of JAK inhibitors faces regulatory friction as prescribers must counsel patients on cardiovascular, malignancy, and thrombosis risks under the FDA’s REMS program. The boxed warnings are particularly restrictive for elderly or comorbid populations, slowing first-line adoption in these cohorts. Although accumulating real-world data may soften these constraints over time, the near-term drag favors IL-23 agents and gut-selective mechanisms, trimming potential growth for the inflammatory bowel disease therapeutics market.

High Biologic Pricing Pressure From Payers & HTA Bodies

Cost-effectiveness agencies such as Germany’s IQWiG and England’s NICE have tightened incremental benefit thresholds, forcing originator companies to offer larger rebates or face exclusion from formularies. A study in Iran pegged average annual biologic costs at USD 2,316.90 per patient, with direct medical costs accounting for nearly half of the economic burden.[3]Hassan Karami, Amin Ghanbarnejad, Mitra Nowrouzpour, Ali Mouseli, Reihaneh Taheri Kondar, Maryam Shirvani Shiri, and Farbod Ebadi Fard Azar, “Cost-of-Illness Analysis of Ulcerative Colitis Patients Treated with Biological Therapy: A Prospective Observational Study in Iran,” BMC Health Services Research, bmchealthservres.biomedcentral.com Copay accumulator and maximizer programs further complicate patient affordability until state-level legislation intervenes. These developments cap price expansion potential and narrow gross margins in the inflammatory bowel disease therapeutics market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Disease: Crohn’s Disease Drives Future Growth

Revenue from Crohn’s disease is projected to climb at an 8.32% CAGR to 2031, overtaking overall market pace despite ulcerative colitis’ 51.68% revenue dominance in 2025. The crohn’s-specific inflammatory bowel disease therapeutics market size for pediatric patients is enlarging as pharmacokinetic studies in children as young as two demonstrate safe dosing of risankizumab. Combination regimens that pair an anti-integrin with a JAK inhibitor have yielded superior endoscopic healing in refractory cases, further lifting average treatment spend.

Persistent mucosal damage and higher surgical rates push clinicians to adopt early biologic intervention in Crohn’s disease, and insurers are gradually approving top-down protocols. The disease’s heterogeneity raises per-patient monitoring costs, but also creates headroom for premium-priced precision therapies. Ulcerative colitis, by contrast, benefits from a clearer disease course and an expanding lineup of effective oral agents, including newly approved mirikizumab. Treatment personalization, spanning dual biologic approaches as well as comorbidity management, is set to raise lifetime revenue per Crohn’s patient within the inflammatory bowel disease therapeutics market.

By Drug Class: JAK Inhibitors Challenge TNF Dominance

TNF inhibitors held a 35.95% inflammatory bowel disease therapeutics market share in 2025 even as biosimilar erosion intensified. Skyrizi and Rinvoq revenues leapt to USD 17.689 billion in 2024, exemplifying how carefully sequenced portfolio hand-offs can cushion the erosion of legacy assets. JAK inhibitors, growing at a 6.85% CAGR, marry oral convenience with increasingly favorable safety packages and are progressively tested in younger cohorts.

Interleukin inhibitors, particularly IL-23 agents, are positioned for step-change adoption once broad reimbursement starts in Europe and Japan. Anti-integrins continue to serve patients who prefer gut-selective targeting, and research into TL1A antagonists is adding another mechanism to the therapeutic mix. Meanwhile, PHD inhibitors such as ISM5411 are carving out a future niche as gut-restricted small molecules, indicating that mechanistic diversification will remain central to competitiveness within the inflammatory bowel disease therapeutics market.

By Route of Administration: Oral Therapies Gain Momentum

Parenteral delivery commanded 75.62% of 2025 spending because most biologics remain injectable, yet oral products are the fastest-growing segment at 8.08% CAGR to 2031. The shift is propelled by busy lifestyles, needle-phobia, and remote prescription refills, prompting companies to prioritize small-molecule pipelines and even explore oral biologic formats.

Subcutaneous self-injection is narrowing the convenience gap, but a pronounced preference for pill-based regimens persists, especially in moderate ulcerative colitis where rapid symptom relief is crucial. Pediatric and adolescent communities favor oral dosing to avoid school-day clinic visits. As REMS requirements are clarified and long-term safety data accumulate, the oral drug class is expected to win an elevated role in first-line therapy decisions within the inflammatory bowel disease therapeutics market.

By Molecule Type: Small Molecules Challenge Biologic Supremacy

Biologics represented 77.86% of 2025 revenue on the strength of mature TNF and emerging IL-23 franchises. Even so, small-molecule therapies are slated for a 9.29% CAGR, the highest across all segmentation types. Small molecules eliminate cold-chain logistics and carry lower production costs, enabling competitive pricing and easier distribution through retail and digital channels.

Pfizer’s comprehensive affordability solutions for tofacitinib and etrasimod underscore how support services can neutralize payer hurdles. Biosimilar competition will extract value from legacy biologics, but next-generation constructs such as bispecific antibodies and orally delivered proteins may defend biologics’ revenue base. AI-guided discovery platforms are accelerating candidate generation, promising a robust stream of differentiated small molecules that will diversify the inflammatory bowel disease therapeutics market.

By Distribution Channel: Digital Transformation Accelerates

Hospital pharmacies commanded 47.31% of global sales in 2025 owing to their role in infusion services and multidisciplinary care coordination. Yet online pharmacies are expanding at 9.17% CAGR as direct-to-patient shipping, telehealth follow-ups, and auto-refill programs proliferate. Specialty pharmacy hubs offer cold-chain warehousing and virtual nursing check-ins, thereby merging clinical oversight with e-commerce convenience.

Retail outlets remain relevant for maintenance or step-down therapy, but newer reimbursement models favor digital channels that can integrate copay assistance and adherence monitoring. Insurers are increasingly comfortable reimbursing telepharmacy services, reducing friction for patients in rural areas. This multi-channel approach is redefining how stakeholders capture value across the inflammatory bowel disease therapeutics market.

Geography Analysis

North America controlled 35.84% of global revenue in 2025 on the back of advanced health-care infrastructure, strong insurance coverage, and rapid product launches through the FDA’s breakthrough designation pathway. Uptake of Skyrizi and Rinvoq, which booked USD 17.689 billion in combined sales, demonstrates how quickly prescribers migrate to new mechanisms when supported by robust real-world evidence. Copay assistance remains essential, yet 29 states still allow accumulator programs that can blunt the benefit of manufacturer coupons, prompting ongoing patient-advocacy efforts.

Europe ranks second by value but leads the world in biosimilar adoption, creating a price-competitive environment that compresses margins yet expands patient reach. The EMA’s positive CHMP opinion for risankizumab in ulcerative colitis is expected to accelerate IL-23 growth, whereas HTA bodies continue to challenge incremental innovation premiums, directing companies toward outcomes-based contracts. Post-marketing safety registries are especially developed, informing global regulatory revisions and underpinning payer negotiations.

Asia-Pacific is forecast for the highest regional CAGR at 8.21% through 2031, propelled by regulatory harmonization and public-sector investment in specialty care. Japan’s biotechnology revitalization strategy includes funding for local startups and expedited review pathways, while China’s retrospective study of ustekinumab reports 75% remission rates in pediatric Crohn’s disease cohorts. India is emerging as a CDMO alternative under the US Biosecure Act, appealing to multinationals wary of supply-chain concentration in China. These developments collectively add depth and resilience to the inflammatory bowel disease therapeutics market across Asia-Pacific.

Middle East and Africa, though smaller in absolute terms, deliver long-run upside thanks to young demographics and improving specialty-care access. GCC governments are building IBD centers of excellence and partnering with multinational firms for local fill-and-finish operations. South Africa’s clinical-trial capacity is drawing early-phase studies, giving the region first-hand exposure to cutting-edge therapies that could shorten launch timelines.

South America delivers steady gains as Brazil and Argentina refine their regulatory frameworks and court foreign investment. Economic volatility still pressures biologic pricing, but phased reimbursement programs and local production partnerships are increasing availability. Clinical-trial participation continues to serve as an entry strategy for companies targeting Latin America, offering compassionate-use channels for severe cases while building prescriber familiarity.

Competitive Landscape

The inflammatory bowel disease therapeutics market is moderately concentrated, with the top five companies still accounting for a majority of sales, yet competitive intensity is rising as biosimilars and novel mechanisms gain ground. AbbVie’s shift toward IL-23 and JAK franchises shows how legacy leaders can defend share after loss of exclusivity, while Johnson & Johnson is exploring dual biologic strategies that combine Stelara with vedolizumab to serve refractory patients.

Start-ups harnessing artificial intelligence are compressing research timelines; Insilico Medicine took only 18 months to bring ISM5411 from concept to Phase 1 completion, illustrating the disruptive potential of AI-first platforms. CDMOs are critical enablers, and capacity restraints make long-term supply agreements a competitive differentiator. Manufacturers are also enhancing patient-support ecosystems; AbbVie’s Skyrizi Complete bundles reimbursement counseling, nurse coaching, and digital adherence monitoring to lock in persistence.

Hybrid commercialization models that pair digital health solutions with pharmacotherapy are gaining traction. Seres Therapeutics and Takeda are piloting microbiome-plus-biologic bundles, offering a more holistic approach to disease control. Payers, meanwhile, are scrutinizing real-world effectiveness to inform risk-share contracts, pushing drug makers to invest in post-marketing registries and outcome-tracking platforms. Together, these trends underscore a market where innovation extends beyond the molecule into manufacturing, service delivery, and data analytics.

Inflammatory Bowel Therapeutics Industry Leaders

Bristol-Myers Squibb Company

AbbVie Inc.

Bausch Health

Johnson & Johnson

Takeda Pharmaceutical

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Insilico Medicine reported positive Phase 1 data for ISM5411, an AI-designed gut-restricted PHD inhibitor, clearing the way for Phase 2 proof-of-concept trials in ulcerative colitis later in 2025.

- January 2025: Eli Lilly secured FDA approval for Omvoh (mirikizumab-mrkz) in adults with moderately to severely active Crohn’s disease, adding a second IBD indication after its 2023 ulcerative colitis approval.

- June 2024: The FDA approved Skyrizi (risankizumab-rzaa) for moderately to severely active ulcerative colitis, making it the first IL-23 specific inhibitor authorized for both major forms of IBD.

Global Inflammatory Bowel Therapeutics Market Report Scope

As per the scope of the report, inflammatory bowel disease (IBD) is characterized by chronic inflammation of the gastrointestinal (GI) tract. The two classifications of IBD are Crohn’s disease and ulcerative colitis. Prolonged inflammation can cause damage to the GI tract. The Inflammatory Bowel Disease (IBD) therapeutics market is segmented by disease type (Crohn’s disease and ulcerative colitis), drug class (TNF inhibitors, JAK inhibitors, IL Inhibitors, Anti-integrins, Aminosalicylates, Corticosteroids, and other drug classes), route of administration (oral and parenteral), end user (hospital pharmacies, online pharmacies, and retail pharmacies), and geography (North America, Europe, Asia-Pacific, Middle East and Africa, and South America). The market report also covers the estimated market sizes and trends of 17 countries across major regions globally.

The report offers values in USD for the above segments.

| Crohn’s Disease |

| Ulcerative Colitis |

| TNF Inhibitors |

| JAK Inhibitors |

| IL Inhibitors |

| Anti-integrins |

| Aminosalicylates |

| Corticosteroids |

| Other Classes |

| Biologics |

| Small-Molecule Therapies |

| Biosimilars |

| Parenteral |

| Oral |

| Hospital Pharmacies |

| Retail Pharmacies |

| Online Pharmacies |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Disease | Crohn’s Disease | |

| Ulcerative Colitis | ||

| By Drug Class | TNF Inhibitors | |

| JAK Inhibitors | ||

| IL Inhibitors | ||

| Anti-integrins | ||

| Aminosalicylates | ||

| Corticosteroids | ||

| Other Classes | ||

| By Molecule Type | Biologics | |

| Small-Molecule Therapies | ||

| Biosimilars | ||

| By Route of Administration | Parenteral | |

| Oral | ||

| By Distribution Channel | Hospital Pharmacies | |

| Retail Pharmacies | ||

| Online Pharmacies | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current size of the inflammatory bowel disease therapeutics market?

The inflammatory bowel disease therapeutics market size reached USD 28.95 billion in 2026 and is projected to hit USD 37.92 billion by 2031, growing at a 5.55% CAGR.

Which therapeutic area is expanding the fastest within this market?

Crohn’s disease drugs are expected to grow at an 8.32% CAGR to 2031, outpacing ulcerative colitis therapies.

How quickly are oral JAK inhibitors gaining share?

The JAK inhibitor segment is forecast to rise at 6.85% CAGR, supported by oral convenience and maturing safety data.

Why is Asia-Pacific the most attractive growth region?

Regulatory harmonization, rising disease awareness, and expanding biosimilar access underpin an 8.21% CAGR for Asia-Pacific through 2031.

What is driving biosimilar penetration?

Aggressive payer formulary changes and potential healthcare savings estimated at up to USD 6 billion are accelerating adalimumab biosimilar uptake.

How are digital pharmacies influencing distribution?

Online pharmacies are growing at 9.17% CAGR thanks to direct-to-patient shipping, automated refills, and integrated copay support programs.

Page last updated on: