Global Colorectal Cancer Therapeutics Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

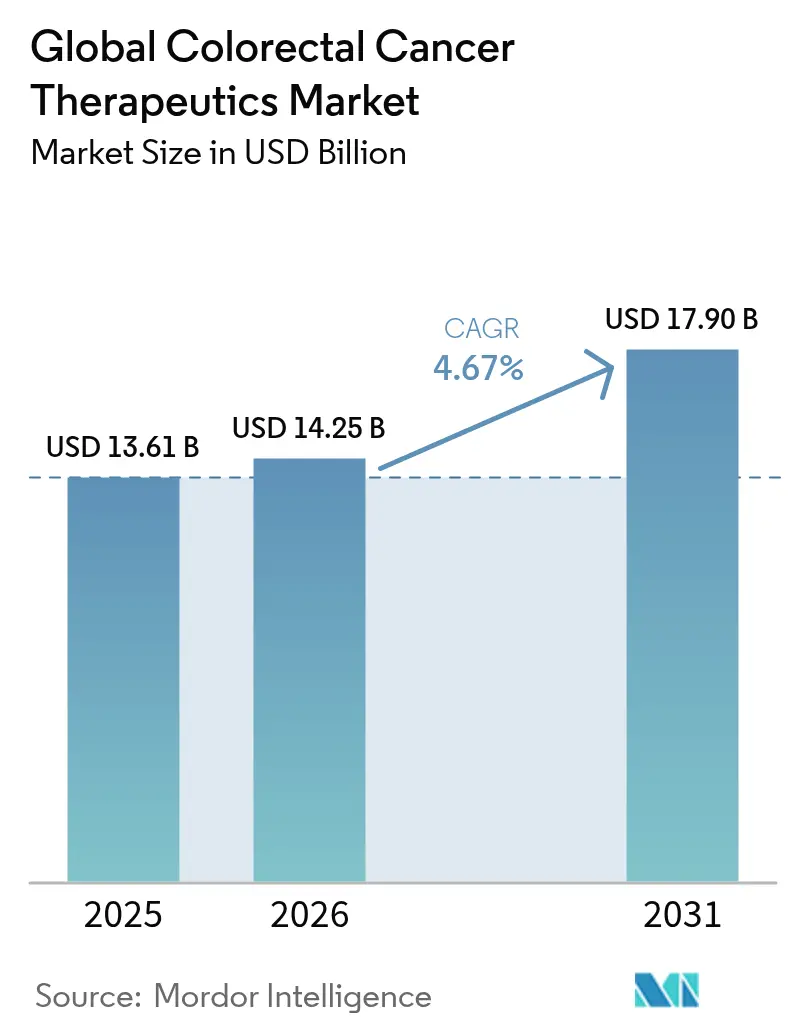

| Market Size (2026) | USD 14.25 Billion |

| Market Size (2031) | USD 17.9 Billion |

| Growth Rate (2026 - 2031) | 4.67% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

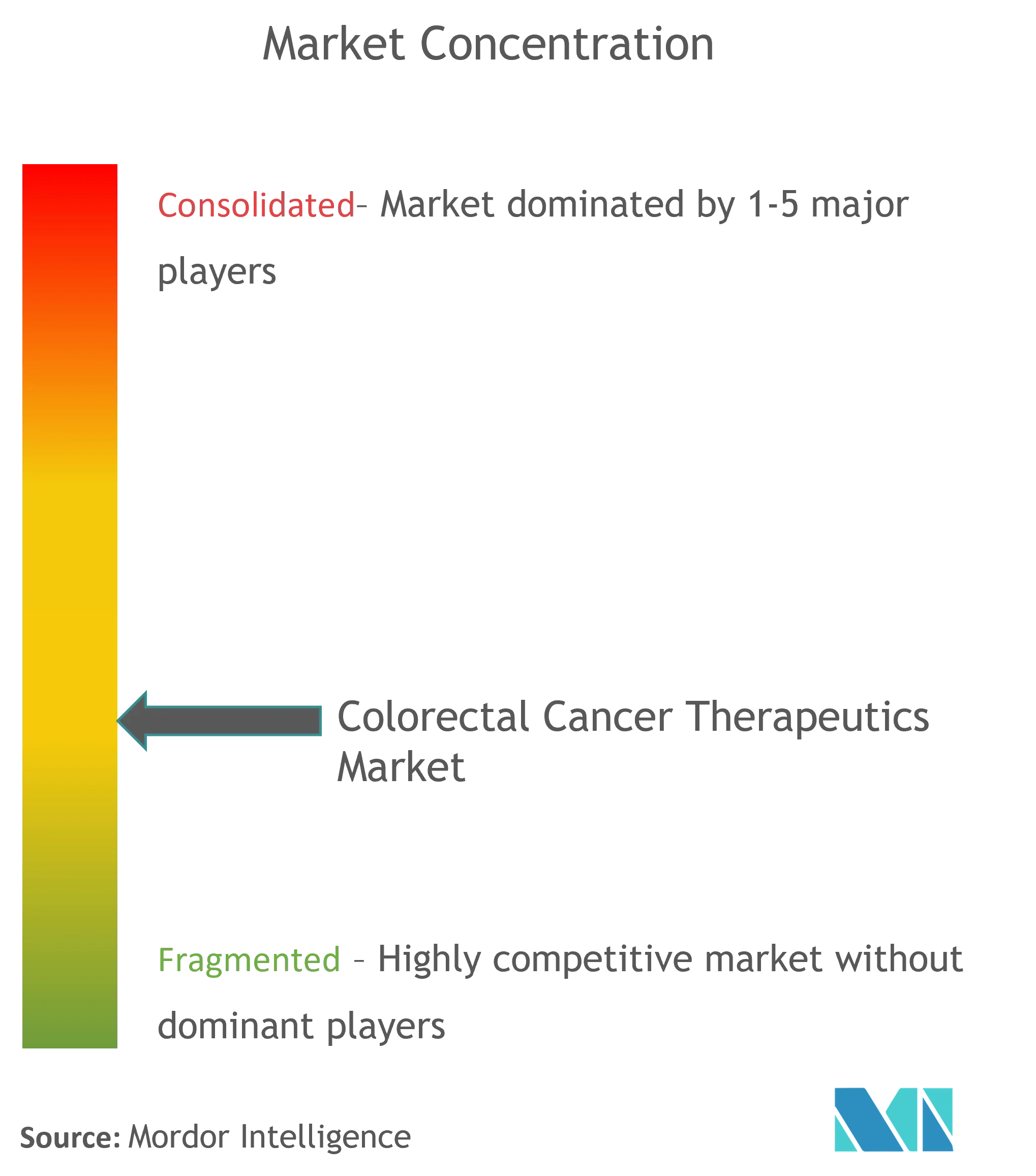

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Global Colorectal Cancer Therapeutics Market Analysis by Mordor Intelligence

The colorectal cancer therapeutics market size is expected to grow from USD 13.61 billion in 2025 to USD 14.25 billion in 2026 and is forecast to reach USD 17.9 billion by 2031 at 4.67% CAGR over 2026-2031. Precision-medicine adoption, particularly companion-diagnostic-linked immunotherapies, is the primary engine of expansion within the colorectal cancer therapeutics market. Consolidated reimbursement pathways for biomarker-guided regimens and landmark regulatory approvals, such as dostarlimab in mismatch repair-deficient (dMMR) rectal cancer, are accelerating the pace at which new protocols replace conventional chemotherapy. Sustained oncology drug shortages for platinum backbones have inflated treatment costs, reinforcing payers’ willingness to shift toward more targeted options that promise lower overall resource utilization. Regionally, North America remains the largest contributor, while Asia Pacific delivers the fastest incremental demand as early-detection and screening programs expand.

Key Report Takeaways

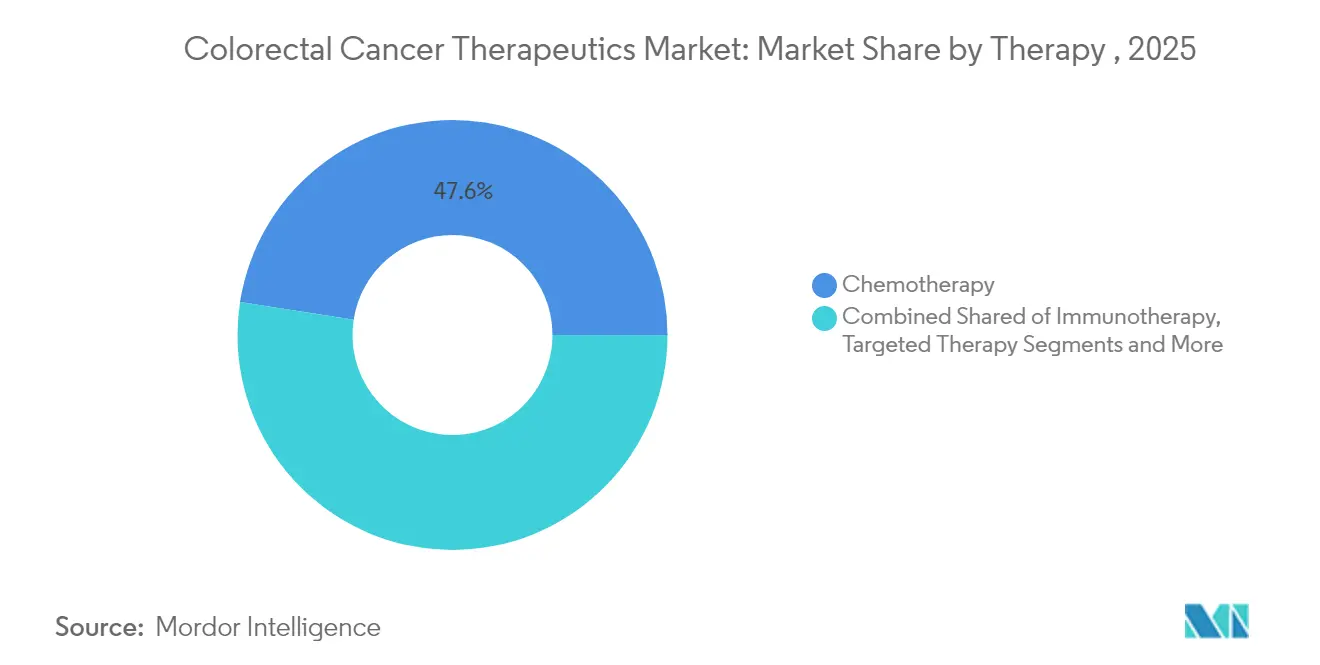

- By therapy, chemotherapy held 47.55% colorectal cancer therapeutics market share in 2025, whereas immunotherapy is projected to advance at a 14.21% CAGR through 2031.

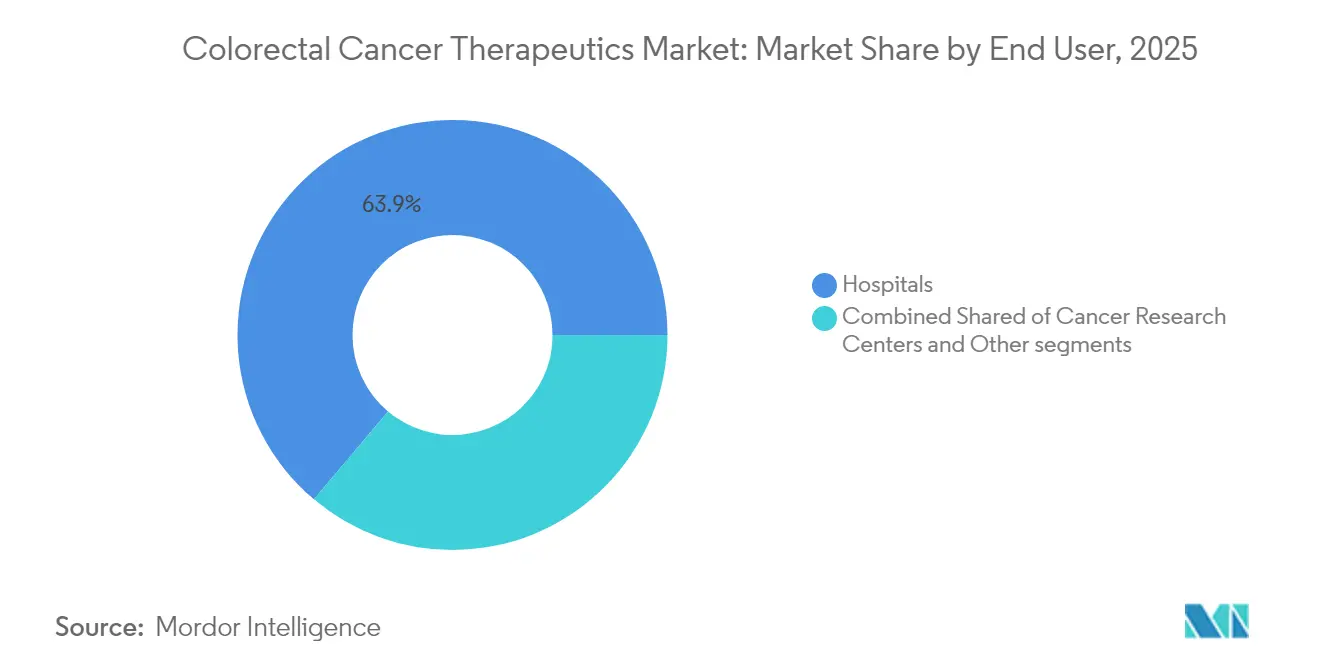

- By end user, hospitals commanded 63.85% revenue share of the colorectal cancer therapeutics market size in 2025; cancer research centers post the quickest growth at 9.78% CAGR through 2031.

- By geography, North America captured 42.35% colorectal cancer therapeutics market share in 2025, while Asia Pacific is poised to expand at a 9.46% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Colorectal Cancer Therapeutics Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Incidence & Prevalence Of Colorectal Cancer | 1.20% | Global, with highest impact in Asia Pacific and emerging markets | Long term (≥ 4 years) |

| Breakthroughs In Targeted & Immune-Oncology Modalities | 1.80% | North America & EU leading, expanding to Asia Pacific | Medium term (2-4 years) |

| Expanded Reimbursement For Biomarker-Guided Therapies | 0.90% | North America & EU core, gradual expansion globally | Medium term (2-4 years) |

| Microbiome-Modulating Adjuvants Boosting Drug Response | 0.40% | North America & EU research centers, early commercial adoption | Long term (≥ 4 years) |

| AI-Enabled Early Detection Accelerating Therapy Starts | 0.60% | Global, with faster adoption in developed markets | Short term (≤ 2 years) |

| Biosimilar MAbs Price-Led Adoption In Emerging Markets | 0.30% | Asia Pacific, Latin America, Middle East & Africa | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Incidence & Prevalence of Colorectal Cancer

Global incidence is projected to climb nearly 10% in men and 12% in women by 2040, while mortality could rise more than 25%. Asia already reports the highest age-standardized rate at 23.88 per 100,000 population, positioning the region as a vital future revenue pool.[1]American College of Gastroenterology, “Colorectal Cancer Facts & Figures,” gi.org Growth in the colorectal cancer therapeutics market aligns with government-led screening expansion, yet sizable populations remain unscreened, sustaining late-stage diagnoses and drug demand. Persistent lifestyle risk factors and aging demographics reinforce long-haul therapy volumes, anchoring the colorectal cancer therapeutics market to a durable patient base.

Breakthroughs in Targeted & Immune-Oncology Modalities

Nivolumab plus ipilimumab delivered 72% 24-month progression-free survival in dMMR metastatic disease versus 14% for chemotherapy. Dostarlimab monotherapy achieved a 100% clinical complete response in locally advanced dMMR rectal cancer, eliminating surgery for every treated patient in a pivotal trial. KRAS G12C regimens such as adagrasib plus cetuximab showed a 34% overall response in refractory settings.[2]U.S. Food & Drug Administration, “FDA Grants Accelerated Approval to Adagrasib and Cetuximab,” fda.gov These data are resetting treatment algorithms and maintaining premium pricing latitude, intensifying innovation cycles inside the colorectal cancer therapeutics market.

Expanded Reimbursement for Biomarker-Guided Therapies

CMS coverage of CT colonography from January 2025 and FDA-approved blood-based screening tests enlarge the eligible diagnostic funnel, driving earlier therapeutic intervention. EMA endorsement of fruquintinib with a 7.4-month survival benefit for heavily pre-treated patients further widens the therapeutic arsenal. As reference biologic prices fall by more than 30% once biosimilars enter, cost savings recycle into broader access for novel agents, a dynamic pivotal to the colorectal cancer therapeutics market.

Microbiome-Modulating Adjuvants Boosting Drug Response

Randomized studies show agents like PHY-906 can enhance irinotecan tolerance while reducing gastrointestinal toxicity, supporting the adoption of combination therapy. Companion microbiome diagnostics are emerging to triangulate responders, an avenue likely to spawn new corporate partnerships that grow the colorectal cancer therapeutics market over the long term.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Cost of Novel Biologics & IO Combinations | -1.10% | Global, with the highest impact on emerging markets and price-sensitive healthcare systems | Medium term (2-4 years) |

| Severe Toxicity & QoL Trade-Offs Limiting Compliance | -0.80% | Global, particularly affecting elderly populations and centers with limited supportive care infrastructure | Short term (≤ 2 years) |

| Narrow MSI-H Pool Curbing Checkpoint-Inhibitor Adoption | -0.60% | Global, with proportionally higher impact in regions with limited biomarker testing capabilities | Medium term (2-4 years) |

| API Supply-Chain Fragility for Key Chemo Agents | -0.40% | Global, with acute impact in regions dependent on single-source manufacturing | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Cost of Novel Biologics & IO Combinations

Checkpoint regimens frequently exceed USD 100,000 annually, straining payer budgets in price-sensitive systems. Immune-mediated colitis affects up to 8.6% of treated patients, adding unplanned supportive-care outlays. Value-based contracting is gaining traction to align payment with outcomes, a trend that may temper near-term revenue growth for the colorectal cancer therapeutics market.

Severe Toxicity & QoL Trade-Offs Limiting Compliance

Immune-enterocolitis risk is highest with CTLA-4 inhibitors, pressing providers to invest in specialist management frameworks. Elderly individuals with comorbidities face higher discontinuation rates, muting utilization in a demographic that forms a growing share of the colorectal cancer therapeutics market patient pool.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Therapy: Immunotherapy Disrupts Traditional Paradigms

Chemotherapy sustained a 47.55% colorectal cancer therapeutics market share in 2025, yet immunotherapy is set to capture outsized incremental value through a 14.21% CAGR to 2031. Dostarlimab’s 100% response in dMMR rectal cancer is emblematic of evidence rewriting practice guidelines. Targeted inhibitors such as sotorasib and adagrasib are broadening applicability beyond MSI-H tumors, translating biomarker discovery directly into revenue. The colorectal cancer therapeutics market size for immunotherapy is forecast to more than double by 2031 as combination protocols earn first-line status in biomarker-defined cohorts.

Pipeline breadth is now anchored in cell-based modalities and bispecific antibodies. GCC19CART recorded 40% objective responses in heavily pre-treated metastatic cases, illustrating how cellular immunotherapies could lift survival in microsatellite-stable disease. As assays for circulating tumor DNA sharpen minimal-residual-disease detection, adaptive dosing models will extend treatment duration, sustaining spending inside the colorectal cancer therapeutics market.

By End User: Research Centers Drive Innovation Adoption

Hospitals retained 63.85% of the 2025 revenue share, largely due to integrated surgery, radiation, and systemic care capacity. Nonetheless, clinical research institutions are expanding at a 9.78% CAGR, leveraging investigational access to new immuno-oncology regimens. The colorectal cancer therapeutics market size attached to research centers is projected to surpass USD 4.22 billion by 2031 as global trial networks proliferate.

Drug shortages have prompted 43% of cancer centers to alter enrolment protocols, underscoring operational bottlenecks that shape drug-utilization timelines. Adoption of tele-oncology follow-up and outpatient infusion suits further reallocates volumes from tertiary hospitals to distributed settings, adding competitive tension among provider types inside the colorectal cancer therapeutics market.

Geography Analysis

North America accounted for 42.35% of 2025 revenue, supported by CMS coverage of advanced screenings and rapid FDA approvals that compress time from lab to clinic. Regional payers champion biomarker testing, embedding precision therapy into standard of care and reinforcing North American leadership within the colorectal cancer therapeutics market. Academic centers’ dense trial portfolios catalyze first-in-class uptake, turning the region into a launchpad for global rollouts.

Asia Pacific is the fastest-growing territory with a 9.46% CAGR. Rising incidence, urbanization-linked risk factors, and stepwise healthcare investment fuel volume expansion. China’s updated colorectal guidelines mirror Western precision-medicine standards, an alignment expected to unlock multi-billion-dollar potential in the colorectal cancer therapeutics market. Yet screening penetration remains low; Thailand reports that 58.8% of eligible adults have never undergone a screening test, representing untapped demand for both diagnostics and therapies.

Europe delivers steady growth underpinned by EMA approvals; 28 oncology products gained clearance in 2024, including fruquintinib’s progression-free survival advantage in refractory disease. Cost-containment frameworks encour-age biosimilar adoption, redistributing budgets toward high-innovation regimens. Meanwhile, Middle East & Africa and South America build capacity through public-private partnerships that prioritize biosimilars and essential medicines, gradually enlarging their presence in the colorectal cancer therapeutics market.

Competitive Landscape

The colorectal cancer therapeutics market displays moderate fragmentation. Five leading companies, led by Roche, Pfizer, and Bristol Myers Squibb, collectively control significant market share. Their positions are reinforced through portfolio breadth across both chemo backbones and immunotherapy flagships. Biosimilar erosion pressures chemotherapy revenues, but manufacturers recoup via licensed combination packages and companion diagnostics.

Strategic alliances concentrate on codeveloping biomarker assays; Amgen and Guardant Health, for example, advance KRAS G12C testing synchronized with sotorasib rollouts. White-space ambitions focus on microsatellite-stable disease where CAR-T constructs, bispecific antibodies, and oncolytic viruses are vying for first-mover advantage. Rapid artificial-intelligence integration into image-analysis pipelines is becoming a differentiator, shortening trial timelines and improving responder selection, thereby sharpening competitiveness throughout the colorectal cancer therapeutics market.

Mergers remain targeted rather than transformational. Transactions emphasize platform synergies—drug-antibody conjugate capabilities or microbiome diagnostics—over scale buying. In-licensing of mid-phase assets allows big pharma to hedge pipeline risk while niche biotechs monetize validated mechanistic innovations, keeping deal flow buoyant in the colorectal cancer therapeutics industry.

Global Colorectal Cancer Therapeutics Industry Leaders

Bristol-Myers Squibb Company

Pfizer Inc

F. Hoffmann-La Roche Ltd

Bayer AG

Eli Lilly and Company

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Roche's Tecentriq significantly reduced recurrence and death rates in certain colon cancer patients, strengthening its role in the adjuvant immunotherapy market and opening possibilities for broader treatment approvals.

- May 2025: Merck KGaA's antibody-drug conjugate demonstrated safety in colorectal cancer trials at ASCO25, advancing targeted therapies for solid tumors and suggesting expanded ADC applications in gastrointestinal cancers.

- May 2025: Pfizer's Braftovi combination therapy reduced disease progression by 47% for metastatic colorectal cancer patients at ASCO25, highlighting its potential as a new standard of care for BRAF V600E-mutant patients.

- April 2025: City of Hope announced FDA approval for the sotorasib and panitumumab combination, which achieved over 30% tumor shrinkage in KRAS G12C metastatic colorectal cancer, compared to 1.9% with standard care, establishing a new treatment paradigm for chemorefractory patients.

- February 2025: Pfizer's Braftovi received accelerated FDA approval based on the BREAKWATER trial results, which showed a 61% objective response rate compared to 40% for standard chemotherapy in BRAF V600E-mutant metastatic colorectal cancer.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the colorectal cancer therapeutics market as the worldwide revenue generated from prescription drugs administered to treat malignancies arising in the colon or rectum, whether used as monotherapy or in approved combination regimens. Treatments span cytotoxic chemotherapy, targeted small molecules, monoclonal antibodies, checkpoint inhibitors, and approved biosimilars, measured at ex-manufacturer prices net of typical rebates.

Scope exclusion: supportive care agents that do not deliver an antitumor effect, surgical devices, screening tests, and investigational molecules not yet approved are outside our frame.

Segmentation Overview

- By Therapy

- Immunotherapy

- Chemotherapy

- Targeted Therapy

- Combination Therapy

- By End User

- Hospitals and Clinics

- Cancer Research Centers

- Others

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia Pacific

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Detailed Research Methodology and Data Validation

Primary Research

We interviewed medical oncologists, hospital pharmacists, and reimbursement advisors in North America, Europe, and Asia Pacific, then surveyed procurement heads at cancer centers to test dosing mix, average selling price erosion, and time to switch when newer immunotherapies enter. Their frontline insights helped us validate desk findings, close regional gaps, and fine-tune scenario weights.

Desk Research

We began with peer-reviewed epidemiology from sources such as GLOBOCAN, WHO Cancer Mortality Database, and CDC WONDER, which let us size incident and prevalent patient pools across 17 countries. Trade bodies like IQVIA Institute, PhRMA, and the European Cancer Organisation provided annual sales audits, pipeline snapshots, and therapy adoption curves. Regulatory portals, for instance, FDA's Drug@FDA and EMA's EPAR, supplied launch dates and labeled indications that steer uptake assumptions. Company 10-Ks and quarterly filings helped our team align list prices and dosage schedules. Paid datasets, notably Dow Jones Factiva for deal news and D&B Hoovers for company financials, grounded cost benchmarks. This list is illustrative; many other open and subscription sources informed our desk work.

Second, we reviewed country-specific reimbursement guidelines, tender results, and patent registries to catch cliff events and price caps that shape forecast ranges. These materials, gathered continuously, form the factual backbone that Mordor analysts lean on before engaging the market.

Market-Sizing & Forecasting

A top-down patient flow model converts stage-specific incidence into treated volumes, applies line-of-therapy penetration rates, and multiplies by weighted course prices. Supplier roll-ups and sampled average selling price times volume serve as a bottom-up check, with variances reconciled. Key inputs include age-adjusted incidence growth, biomarker test penetration, launch cadence of first-in-class drugs, generic entry timing, reimbursement turnaround, and median duration on therapy. Multivariate regression, supported by expert consensus on policy outlook and pipeline success probability, projects each driver to 2030 and produces the 4.73 percent CAGR that Mordor Intelligence publishes. Gaps in bottom-up data, mainly from markets with opaque tender pricing, are bridged with regional analogs approved during analyst review.

Data Validation & Update Cycle

Outputs pass two rounds of anomaly review, cross-checks with independent sales audits, and peer review within our life sciences team. Reports refresh every twelve months, and we reopen models sooner when a material event, such as a new checkpoint inhibitor approval or a pricing reform, hits.

Why Our Colorectal Cancer Therapeutics Baseline Commands Reliability

Published figures often differ because research houses choose distinct drug baskets, vary discount assumptions, and refresh data on different calendars. Our disciplined scope, yearly update rhythm, and dual validation steps give decision makers a dependable anchor.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 13.61 B | Mordor Intelligence | - |

| USD 13.37 B | Global Consultancy A | counts diagnostics revenue and applies flat price growth |

| USD 13.86 B | Research Publisher B | models aggressive immunotherapy uptake without adjusting for reimbursement delays |

| USD 9.38 B | Industry Analytics C | excludes targeted biosimilars and applies Asian data only to developed economies |

The comparison shows that variations stem from scope stretch or narrow definitions rather than fundamental market uncertainty. By aligning variables with real treatment practice and validating every step, Mordor Intelligence delivers a balanced, transparent baseline clients can rely on.

Key Questions Answered in the Report

What is the current size of the colorectal cancer therapeutics market?

The colorectal cancer therapeutics market size reached USD 14.25 billion in 2026 and is projected to hit USD 17.9 billion by 2031

Which therapy segment is expanding the fastest?

Immunotherapy leads growth with a forecast 14.21% CAGR through 2031, driven by strong clinical efficacy in biomarker-selected patients

Which region contributes the most revenue?

North America accounted for 42.35% of global revenue in 2025, supported by advanced reimbursement and rapid regulatory approvals.

Why are biomarker tests critical for market growth?

Biomarker assays enable precision prescribing, qualify patients for high-value immunotherapies, and unlock broader reimbursement coverage.

How are supply-chain issues affecting treatment choices?

Shortages of platinum chemotherapy agents raise costs and prompt payers to consider targeted regimens that reduce inpatient resource burden.

Page last updated on: