Inertial Navigation System (INS) Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

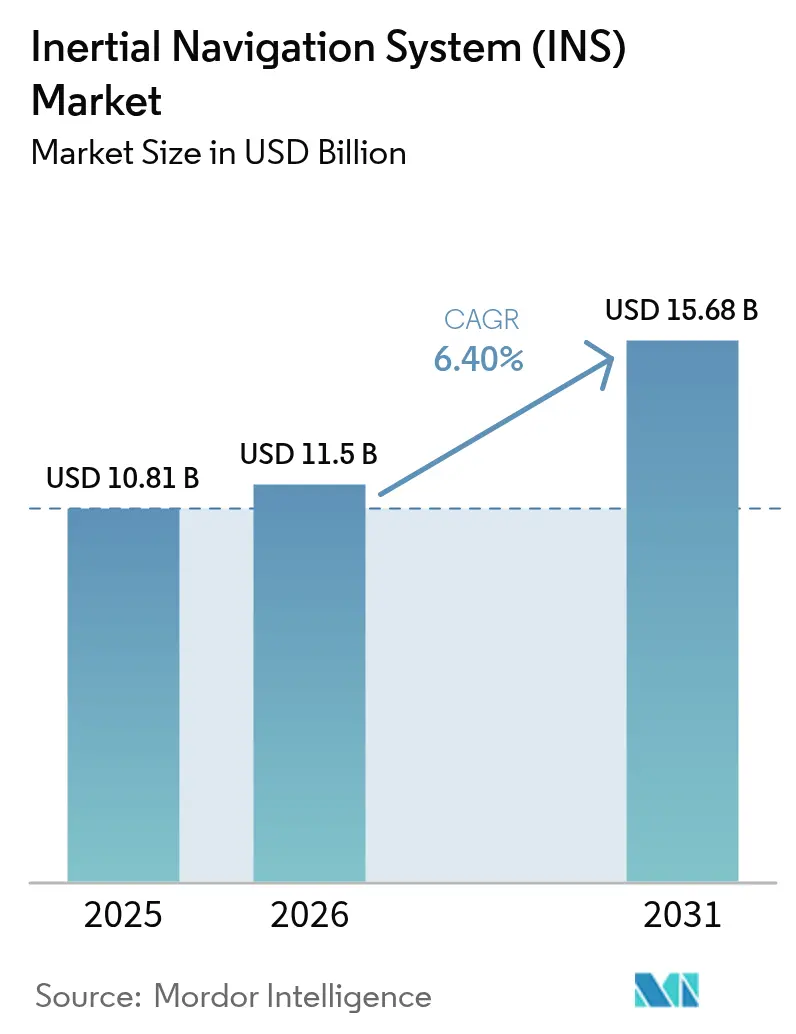

| Market Size (2026) | USD 11.5 Billion |

| Market Size (2031) | USD 15.68 Billion |

| Growth Rate (2026 - 2031) | 6.40% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Inertial Navigation System (INS) Market Analysis by Mordor Intelligence

The inertial navigation system market size was valued at USD 10.81 billion in 2025 and estimated to grow from USD 11.5 billion in 2026 to reach USD 15.68 billion by 2031, at a CAGR of 6.40% during the forecast period (2026-2031). Heightened defense allocations, including the U.S. Department of Defense’s USD 141 billion research budget that earmarks USD 1.5 billion for GPS-Enterprise initiatives, are anchoring demand for resilient navigation platforms. Breakthroughs such as the U.S. Naval Research Laboratory’s Continuous 3D-Cooled Atom Beam Interferometer are also addressing drift limitations that restrict performance in GPS-denied scenarios. [1]Atom interferometer charters Navy’s inertial navigation path. Phys.org, phys.org Strategic acquisitions—exemplified by Honeywell’s EUR 200 million (USD 226 million) purchase of Civitanavi Systems—are consolidating sensor know-how and extending global reach. [2]Honeywell to acquire Civitanavi Systems. Honeywell, honeywell.com Cost-efficient MEMS architectures broaden adoption beyond defense, while optical and quantum-based gyroscopes open premium niches. Commercial spaceflight, autonomous vehicles, and unmanned systems each offer a multiyear runway for scale as governments and enterprises prioritize resilient Positioning, Navigation, and Timing (PNT) solutions.

Key Report Takeaways

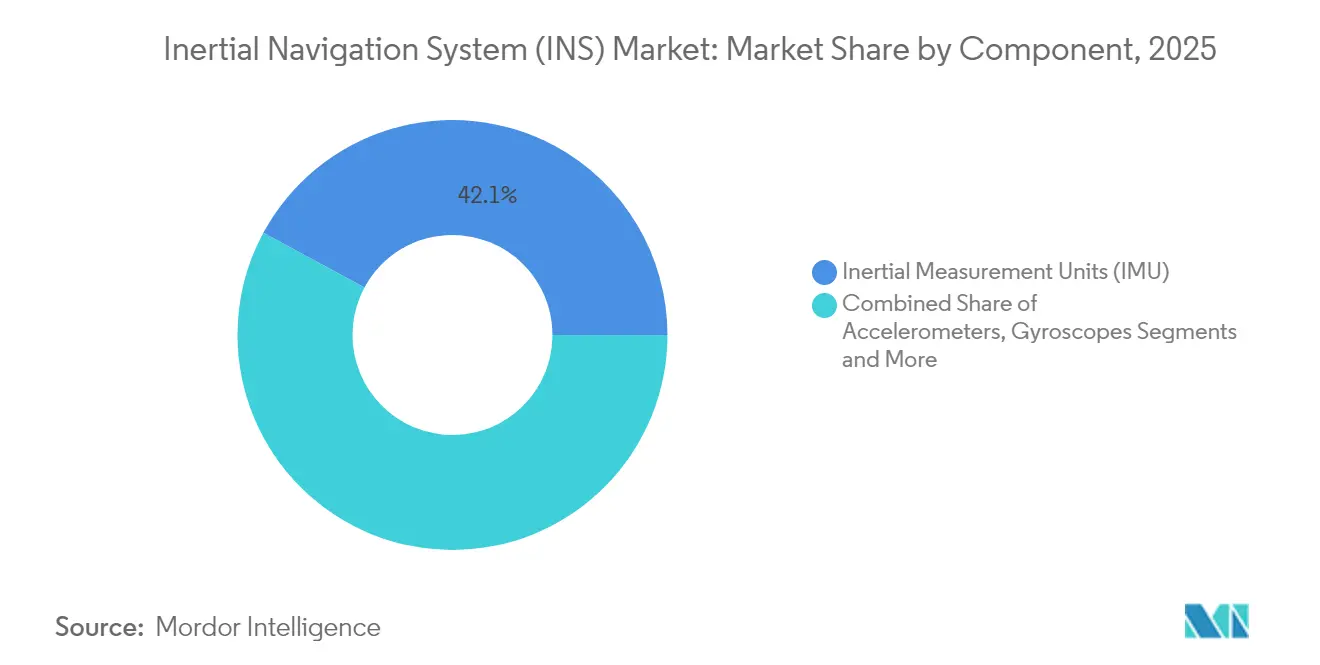

- By component, Inertial Measurement Units led with 42.12% inertial navigation system market share in 2025; the segment is forecast to expand at a 7.25% CAGR through 2031.

- By technology, MEMS devices captured 36.65% revenue share in 2025, and this portion of the inertial navigation system market is projected to grow at an 8.35% CAGR.

- By performance grade, navigation-grade products held 33.55% share of the inertial navigation system market size in 2025, whereas consumer-grade offerings are on track for an 8.45% CAGR to 2031.

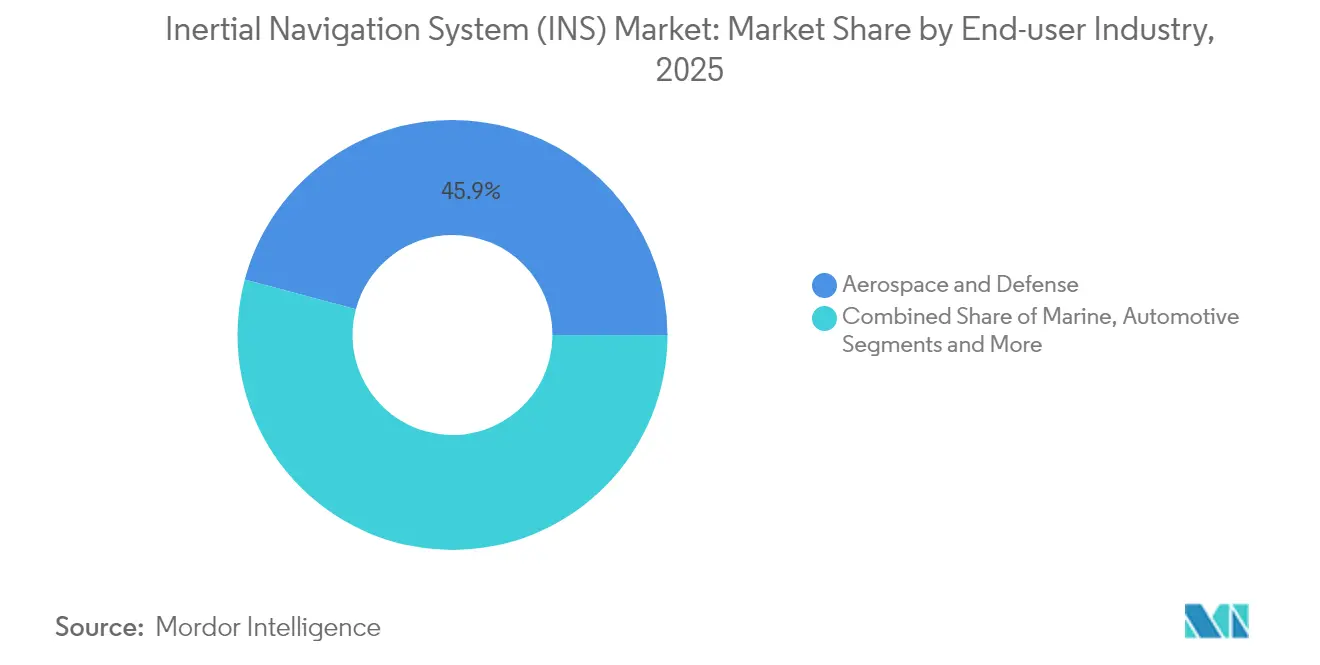

- By end-user industry, aerospace & defense dominated with 45.85% share in 2025; automotive applications represent the fastest-growing slice at an 8.05% CAGR.

- By platform, airborne systems accounted for 38.35% of the 2025 revenue pool, while space platforms exhibit a leading 7.7% CAGR outlook.

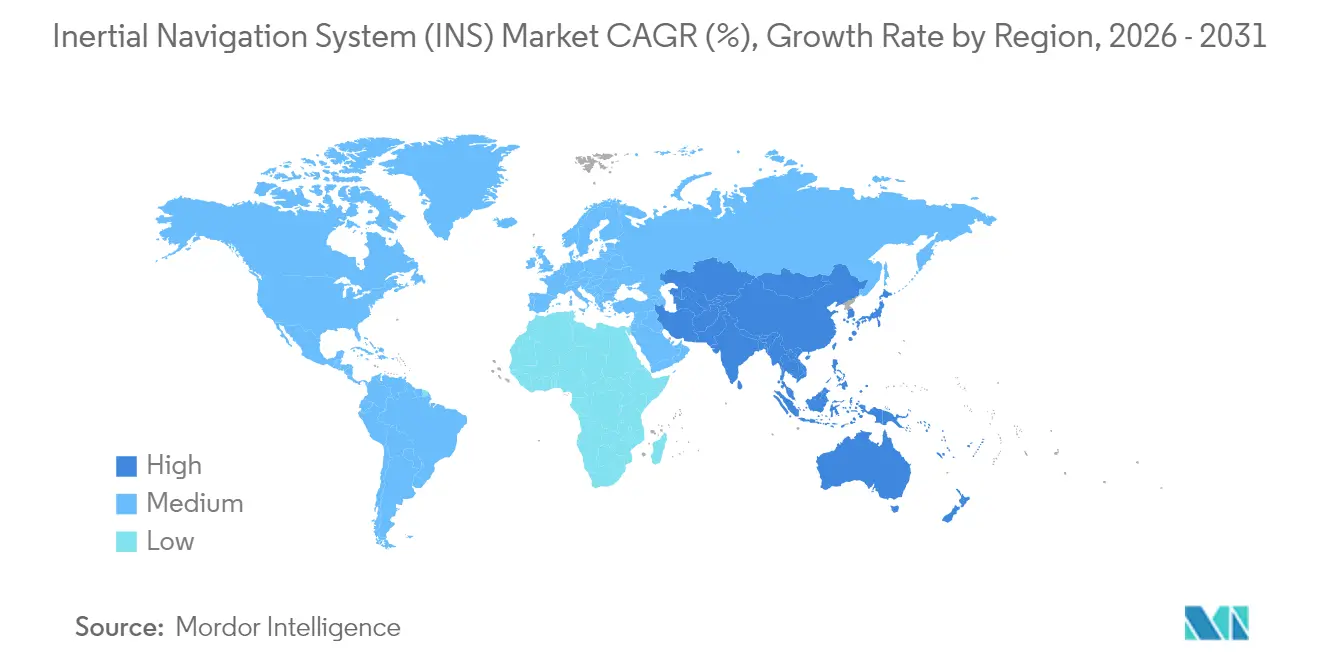

- By geography, North America commanded 31.10% of the 2025 total; Asia-Pacific is advancing at a 9.05% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Market Trends and Insights

Drivers Impact Analysis of Inertial Navigation System (INS) Market*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increased military and defense spending | 1.80% | Global, concentration in North America, Europe, APAC | Medium term (2-4 years) |

| Growing adoption in autonomous vehicles | 1.50% | Global, led by North America and APAC | Long term (≥ 4 years) |

| Rising demand from unmanned systems | 1.20% | Global, early adoption in North America and Europe | Medium term (2-4 years) |

| Miniaturized INS enabling precision-guided munitions | 0.90% | North America, Europe, select APAC markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Increased Military and Defense Spending

Defense modernization is funneling unprecedented capital toward the inertial navigation system market. The USD 141 billion U.S. RDT&E allocation dedicates USD 1.5 billion to GPS-Enterprise programs that integrate seamlessly with high-precision INS payloads. European contractors mirror this momentum; Thales recorded EUR 25.3 billion (USD 27.5 billion) in 2024 orders that included navigation equipment for land and naval platforms. Naval initiatives such as the AN/WSN-7 Ring Laser Gyro Navigator underscore a tactical pivot toward GPS-independent operations. NATO’s adoption of standardized Ships Inertial Navigation Systems highlights alliance-wide harmonization. Collectively these programs accelerate demand for navigation-grade sensors with radiation tolerance and electronic-warfare resilience.

Growing Adoption in Autonomous Vehicles

Vehicle OEMs view robust INS as a prerequisite for Level 4–5 autonomy, catalyzing a sizable slice of the inertial navigation system market. Loosely coupled 5G-IMU fusion schemes have demonstrated 14 cm accuracy for 95% of run-time, eclipsing legacy GPS-only methods. [3]Navigation-grade interferometric fiber optic gyroscope. arXiv, arxiv.org The sector’s 8.2% CAGR reflects adoption in mass-market models, not merely premium fleets. MEMS gyros fabricated with silicon-carbide achieve Q-factors of 4.6 million at 80 °C, sustaining bias instability below 0.5°·h⁻¹—an outcome well suited to high-temperature automotive cabins. Sensor fusion using Unscented Kalman Filters has cut RMS errors to under 5 m, bolstering lane-level guidance. As regulation converges on safety standards, tier-one suppliers embed dual-redundant IMUs, turning INS into a core design element rather than an optional add-on.

Rising Demand from Unmanned Systems (UAV, UGV, USV)

Autonomous drones, ground robots, and surface vessels frequently lose satellite coverage in subterranean or littoral theaters, elevating the need for tactical-grade INS solutions. Cooperative mining platforms illustrated by YuGong rely on INS fused with LiDAR and cameras to coordinate haul-truck movements in open-pit mines. Underground vehicles track light-band guidance and dead-reckon when GNSS lines up poorly. Micro-shell resonator gyroscopes trimmed to 0.32 mHz frequency mismatch achieve tactical-grade stability in volumes suitable for small UAVs. Maritime unmanned surface craft leverage hydro-acoustic stations and inertial sensors to rival Doppler velocity logs at lower operating cost. The convergence of AI path-planning with high-bandwidth inertial data underpins a long-term uplift for this driver.

Miniaturized INS Enabling Precision-Guided Munitions

Precision-strike doctrines amplify the value proposition of compact navigation-grade sensors. Cobweb-like disk resonator gyroscopes now deliver 20 dB noise reduction and ±130°/s input range without active trimming. At the systems level, the U.S. Navy’s SBIR calls for radiation-hardened oscillators to shore up missile survivability in nuclear or space environments. Fiber-optic gyros using air-core anti-resonant fibers register angular random walk of 0.0038 deg h⁻¹/², supporting long-duration mission envelopes. As cost curves bend downward, suppliers capable of packaging these advances into plug-and-play modules will enlarge their foothold in the inertial navigation system market.

Restraints Impact Analysis of Inertial Navigation System (INS) Market*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High cost of navigation-grade systems | -1.4% | Global, higher impact in emerging markets | Medium term (2-4 years) |

| Cumulative drift error versus GNSS | -0.8% | Global, affecting standalone INS applications | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Cost of Navigation-Grade Systems

Navigation-grade assemblies priced between USD 50,000 and USD 200,000 have historically restricted penetration in cost-sensitive domains. Although MEMS yields are improving, the three-fold price gap versus tactical-grade alternatives still discourages adoption in emerging economies. Chip-scale optical gyros developed by Anello Photonics claim 0.1% distance error over 100 km while compressing bill-of-materials cost. Parallel research shows low-cost microcontroller-based sensor-fusion achieving sub-meter accuracy underwater, proving that algorithmic enhancements can partially offset hardware pricing. Suppliers are adopting fab-lite models and licensing arrangements to lower per-unit calibration overhead, yet affordability remains a mid-term drag on inertial navigation system market expansion.

Cumulative Drift Error Versus GNSS

Even high-end gyros accrue bias over time, producing errors of one to two nautical miles per hour when left unaided. Atom interferometry promises to negate drift by locking phase measurements to fundamental atomic constants, as demonstrated by the Navy’s interferometer prototype. Laboratory results show that optimal IMU rotation profiles halve positional error during GNSS outages, but implementation adds mechanical complexity. Terrain-referenced or eLORAN backup layers are under evaluation to bound worst-case error growth. Until such multi-sensor stacks reach production maturity, drift concerns will continue to temper standalone INS deployments within the inertial navigation system market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Inertial Navigation System (INS) Market Segment Analysis

By Component:

IMUs Lead Integration TrendIMUs generated 42.12% of 2025 revenue, reinforcing their role as the foundational building block of the inertial navigation system market. Robust single-package integration of tri-axial accelerometers, gyroscopes, and optional magnetometers reduces wiring, weight, and calibration costs. This configuration is scaling into guided weapons, industrial bots, and consumer drones as unit economics improve. The segment is projected to post a 7.25% CAGR through 2031, fueled by wafer-level vacuum packaging and machine-learning-based error modeling that cut Allan variance by double-digit margins.

Autonomous warehouse and orchard robots illustrate emerging demand as GNSS reception degrades indoors or under dense foliage. A GRU-Transformer algorithm trimmed positional RMSE by 61.6% compared with traditional EKF, underscoring the multiplier effect of advanced filtering. Inventory robotics employ vision-aided IMUs to achieve 95.8% item detection on low shelves. These deployments reinforce IMUs’ trajectory toward ubiquity and affirm their expanding share within the inertial navigation system market.

By Technology:

MEMS Drives Cost ReductionMEMS devices owned 36.65% revenue in 2025, a testament to foundry scale and maturing lithography. Lower power draw and shock resilience position MEMS gyros as logical choices for smartphones and automotive ADAS. Forecasts place an 8.35% CAGR on MEMS shipments as fabs switch to 200-mm silicon-carbide and deploy high-aspect ratio etching to realize Q-factors above 4 million.

High-precision niches still rely on ring laser or fiber-optic gyros, yet optical-waveguide-on-silicon solutions are narrowing the performance gap. An optical gyro-on-chip reports centimeter-grade positional accuracy while occupying less than 1 cm² die area. Concurrently, ring laser researchers at INFN-Pisa improved fringe contrast stability, potentially extending MTBF for navigation-grade units. As these innovations commercialize, MEMS remains the fulcrum for volume growth in the inertial navigation system market.

By Performance Grade:

Navigation Grade Leads Premium SegmentNavigation-grade packages delivered 33.55% of 2025 revenue but command the highest average selling price in the inertial navigation system market. Bias stability below 0.01°/h and angle random walk under 0.001°/√h enable long-duration missions without external updates. Fiber-optic gyros employing air-core anti-resonant fibers achieved 0.0038 deg h⁻¹/² performance, confirming environmental robustness for strategic assets.

Consumer-grade products are registering an 8.45% CAGR as smartphone, wearables, and in-car infotainment join the buying pool. Improvements such as self-trimmed disk resonator gyros meeting tactical benchmarks at mass-market price points highlight the trickle-down effect of R&D. The inertial navigation system market size for consumer implementations is predicted to eclipse USD 2.29 billion by 2031, absorbing latent demand from augmented reality, gaming, and micro-mobility.

By End-user Industry:

Aerospace and Defense Maintains LeadershipAerospace and defense applications accounted for 45.85% of total 2025 revenue, underscoring the sector’s durable appetite for high-accuracy, radiation-hardened devices. Safran’s Geonix contract with the Finnish Defense Forces spotlights European investment in secure PNT.

Automotive lines remain the fastest-expanding, at 8.05% CAGR, driven by regulatory pressure for ADAS and consumer demand for convenience features. Forestry forwarders outfitted with GNSS/INS control reduced positional error to 0.4 m, proving economic viability for heavy-equipment OEMs. Energy, marine, and industrial robotics collectively populate the remainder of the inertial navigation system market, each exhibiting mid-single-digit growth tied to automation roadmaps.

By Platform:

Airborne Applications Drive InnovationAirborne integrations made up 38.35% of aggregate turnover in 2025, benefiting from commercial fleet renewal and military aircraft refresh cycles. Real-time kinematic solutions for CubeSat rendezvous operations have demonstrated centimeter-level relative accuracy, paving the way for autonomous orbital servicing missions.

Spacecraft represent the growth frontier, expanding at a 7.7% CAGR as launch cadences accelerate and constellation operators prioritize on-board PNT redundancy. The U.S. Department of Commerce’s license-exemption rule for exports to key allies eases transaction friction, encouraging suppliers to embed radiation-hardened INS in small-sat buses. Land and naval segments continue to diversify as unmanned ground and surface vehicles normalize INS usage patterns across defense and commercial fleets, rounding out the inertial navigation system market.

Geography Analysis

North America Inertial Navigation System (INS) Market

North America retained 31.10% of the inertial navigation system market in 2025, energized by a defense budget cycle that prioritizes resilient PNT. Northrop Grumman closed 2025 Q1 with USD 91.5 billion backlog, emphasizing long-term runway for avionics and missile navigation upgrades. Regulatory streamlining, such as the Export Administration Regulations amendment, trims roughly 90 annual license applications and accelerates space technology deliveries. Robust private-sector funding for autonomous-vehicle pilots and commercial launch providers sustains technology refresh rates, reinforcing the region’s leadership.

APAC Inertial Navigation System (INS) Market

Asia-Pacific is projected to post a 9.05% CAGR through 2031, steered by defense modernization, semiconductor fabrication scale, and rapid adoption of unmanned aerial vehicles. Japan and South Korea are raising capital spend on ADAS and micro-mobility, while India’s indigenous navigation constellation drives domestic INS integration in launch vehicles and missiles. Chinese smartphone OEMs continue to integrate dual-IMU set-ups to improve indoor positioning, helping pivot consumer perception toward premium navigation capabilities.

EMEA and South America Inertial Navigation System (INS) Market

Europe benefits from vertically integrated aerospace champions and concerted NATO programs. Honeywell’s purchase of Civitanavi bolsters the regional supply base for fiber-optic gyros. Thales noted a 49% upswing in orders from emerging markets, highlighting export attractiveness of European platforms thalesgroup.com. Energy exploration in the North Sea and Mediterranean demands subsea INS kits for pipeline inspection, offering incremental uplift. Smaller but steadily growing demand pockets in the Middle East, Africa, and South America stem from offshore drilling, mining, and border-security programs that all rely on GPS-independent navigation.

Regulatory Landscape

The inertial navigation system (INS) market is shaped by dual-use export controls and sector-specific safety and airworthiness frameworks. In the United Kingdom, The Export Control (Amendment) Regulations 2025 (SI 2025/532) updated Category 7 (Navigation and Avionics) technical notes, clarifying definitions that affect classification and licensing of INS systems and related components, with particular relevance for navigation-grade and military end uses.

On the civil side, European aviation and automotive rules are tightening integrity and assurance expectations for navigation functions. The EU framework for attestation of ATM/ANS equipment has been in force since September 2023 and provides structured compliance routes, such as certificates or declarations of design compliance, which influence the procurement of certified navigation and surveillance equipment into European air navigation services. In road transport, Commission Implementing Regulation (EU) 2026/481 (March 2026) amends automated driving system type-approval provisions. In June 2026, UN/WP.29 work on draft UN Regulation and a draft Global Technical Regulation for Automated Driving Systems will push manufacturers toward stronger safety-management, validation evidence, and post-deployment monitoring practices, increasing demands on sensor and navigation integrity for vehicles using INS as part of automated driving stacks.

Value Chain Analysis

The INS value chain begins with specialty inputs and subcomponents, moves through sensor fabrication and system integration, and then transitions to certification or qualification and platform-level installation. Upstream inputs include MEMS fabrication materials, high-purity fused silica and optical coatings for photonic components, and gases such as helium-neon for legacy laser-gyro architectures. Midstream participants span integrated aerospace and defense suppliers that produce or assemble navigation-grade systems (including Honeywell, Northrop Grumman, Safran, and Thales) and specialized providers that focus on tactical and industrial INS and GNSS-aided navigation modules (including KVH Industries, SBG Systems, and VectorNav Technologies).

Access to advanced semiconductor and precision manufacturing capacity is a key bottleneck, alongside compliance friction for cross-border transfers of high-grade gyro technology under ITAR/EAR-type controls. To protect availability of critical subassemblies, manufacturers have leaned on more vertical integration and dual-source strategies, including for fiber-optic coils and MEMS IMUs. Distribution and integration typically run through OEM avionics and vehicle electronics supply chains, where qualification and environmental testing, along with long lifecycle support such as spares, calibration, and updates, can be as decisive as upfront hardware cost.

Competitive Landscape

The inertial navigation system market remains moderately consolidated, with a cluster of diversified aerospace and defense primes accounting for the bulk of design wins. Honeywell’s acquisition of Civitanavi reflects a classic horizontal integration play that secures fiber-optic gyro IP and anchors European sales channels. Thales and Safran scale through large program captures, leveraging vertically integrated production to defend margin.

Emerging firms differentiate via optical-waveguide gyros and quantum sensors. Anello Photonics pursues a fab-less model that pairs photonic integrated circuits with CMOS control, promising to shave unit cost by double-digit percentages. One Silicon Chip Photonics aligns its roadmap toward centimeter-accurate navigation for commercial drones, an attractive adjacency as drone delivery pilots multiply.

Government research laboratories influence technology direction by derisking quantum and atom-interferometry techniques. The U.S. Naval Research Laboratory’s drift-free interferometer could upend performance benchmarks if transitioned out of the lab. Meanwhile, supply chain reshoring incentives in the United States and Europe encourage local MEMS gyro fabrication, insulating manufacturers from geopolitical risk. Competitive pressure therefore pivots on technological leapfrogging, time-to-qualification, and the ability to furnish full-stack PNT solutions under a single SLA.

Inertial Navigation System (INS) Industry Leaders

Northrop Grumman Corporation

MEMSIC Inc.

Honeywell International Inc.

Tersus GNSS Inc.

Inertial Labs Inc.

- *Disclaimer: Major Players sorted in no particular order

Inertial Navigation System (INS) Market Companies Covered in this Report

- Honeywell International Inc.

- Northrop Grumman Corp.

- Safran Electronics and Defense

- Thales Group

- Bosch Sensortec GmbH

- KVH Industries Inc.

- Trimble Inc.

- NovAtel Inc. (Hexagon)

- iXblue (Exail)

- VectorNav Technologies LLC

- MEMSIC Inc.

- Parker Hannifin – LORD MicroStrain

- Tersus GNSS Inc.

- Inertial Labs Inc.

- Oxford Technical Solutions Ltd.

- Inertial Sense LLC

- Aeron Systems Pvt. Ltd.

- STMicroelectronics NV

- Analog Devices Inc.

- Raytheon Technologies Corp.

Market Opportunities and Future Outlook

Defense demand is pulling INS toward resilient, GPS-contested operating concepts, creating openings for M-Code-capable embedded GPS/INS modernization, alternative navigation stacks, and higher-end inertial sensors that maintain performance through jamming and spoofing. A concrete indicator is DARPA's May 2026 Special Notice (DARPA-SN-26-88) for the PINPOINT program, which targets new approaches to address current MEMS inertial navigation performance limits and reinforces an R&D-to-procurement pipeline for higher-accuracy, lower-drift inertial solutions. Separately, the U.S. Air Force commitment of USD 49.7 million (July 2026) toward navigation alternatives highlights programmatic funding for architectures in which INS acts as a core continuity layer rather than a backup.

Commercial and government maritime autonomy is also creating a path for INS suppliers via modular integration platforms built around certified navigation cores. In May 2026, Anschuetz launched AUTONOMICS for autonomous naval navigation and mission execution based on its SYNAPSIS NX certified INS, pointing to demand for software-defined integration layers that can be deployed without replacing underlying certified inertial navigation hardware. EU-backed quantum sensor work, including the Horizon Europe Grand Challenge focused on quantum sensors for inertial navigation, expands opportunities for suppliers and labs working on cold-atom interferometry and other low-drift concepts, particularly when sovereignty and long-duration navigation without external updates drive procurement requirements.

Recent Industry Developments in Inertial Navigation System (INS) Market

- April 2026: Northrop Grumman delivered the first production unit of its LN-351 Embedded GPS/INS Modernization (EGI-M) solution, integrating M-Code capability and the INTEGRITY-178 tuMP real-time operating system. The milestone moves jam-resistant navigation from development into fieldable production deliveries and supports broader modernization cycles for resilient airborne PNT.

- March 2026: Honeywell introduced the HGuide i700 as a commercially available, no-license-required IMU aimed at unmanned air, land, and sea platforms. The NLR positioning reduces export and procurement friction for integrators and accelerates deployment of INS-based navigation continuity in robotics and unmanned systems.

- June 2025: Honeywell launched the HG3900 next-generation silicon IMU, targeting higher-performance MEMS inertial sensing for aerospace and defense applications. By pushing silicon IMU capability upward, the release supports a broader shift toward smaller, lighter inertial subsystems that can be adopted across more platforms and integration form factors.

Inertial Navigation System (INS) Market Report Scope and Research Methodology

Market Definition and Coverage

The inertial navigation system market covers revenue from complete INS units that use gyroscopes and accelerometers (with onboard processing) to calculate position, velocity, and attitude without needing an external signal.

Scope exclusions: we exclude stand-alone motion sensors sold without embedded navigation computation, and software-only sensor-fusion toolkits.

Segments Covered in This Report

- By Component

- Accelerometers

- Gyroscopes

- Magnetometers

- Inertial Measurement Units (IMU)

- Others

- By Technology

- Mechanical Gyro

- Ring Laser Gyro (RLG)

- Fiber-Optic Gyro (FOG)

- Micro-Electro-Mechanical Systems (MEMS)

- Hemispherical Resonator Gyro (HRG)

- Others

- By Performance Grade

- Navigation Grade

- Tactical Grade

- Industrial Grade

- Automotive Grade

- Consumer Grade

- By End-user Industry

- Aerospace and Defense

- Marine

- Automotive

- Industrial and Manufacturing

- Oil and Gas and Energy

- Agriculture, Mining and Construction

- Others

- By Platform

- Airborne

- Land

- Naval

- Space

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Russia

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- ASEAN

- Rest of APAC

- Middle East and Africa

- Saudi Arabia

- United Arab Emirates

- Turkey

- South Africa

- Rest of MEA

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk work started with a clear map of where INS demand shows up and how it is typically purchased across airborne, land, naval, and space platforms. To anchor this, we used public defense budget documents, procurement and contract award notices, civil aviation and space launch statistics, and safety or performance standards that describe navigation and inertial sensing requirements.

To ground the model inputs, we also reviewed government trade data for relevant electronics and aerospace categories, industry association publications for avionics and marine equipment, and peer-reviewed engineering journals on gyro and accelerometer technology shifts. Company annual reports, investor presentations, and reputable press were used to track shipment momentum, mix changes by grade (navigation, tactical, industrial), and pricing direction. In a few cases, we used a paid subscription for company financials and a patent database to confirm corporate exposure and stated innovation priorities. The sources listed here are illustrative only, and we checked many other public materials to collect, validate, and clarify data points.

Primary Interviews and Surveys

Primary calls and surveys were used to confirm what is actually being bought as an INS (versus an IMU), where integration happens, and how pricing differs by platform and performance grade. We spoke with system integrators, component specialists, OEM-facing distributors, and end-user side experts, then used that feedback to tighten assumptions that could not be fully validated from public documents. Because demand is global, we cross-checked inputs across the main buying regions so the final totals would not be driven too heavily by a single procurement cycle or one platform trend.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 35% | CXOs: 17% | APAC: 52% |

| Mid tier: 48% | Functional/Unit leaders: 39% | EMEA: 30% |

| Smaller Players: 17% | Managers: 44% | Americas: 18% |

Market-Sizing & Forecasting

Sizing used a top-down build where platform activity and procurement signals were translated into an INS demand pool, then converted into value using grade-level pricing ranges. Aircraft deliveries and retrofit intensity, naval vessel build and upgrade cycles, missile and guided system procurement, and space launch cadence were treated as demand indicators, then adjusted for typical INS fit-rate and replacement patterns.

We cross-checked those totals with selective bottom-up approximations, such as sampled unit volumes multiplied by average selling price by grade, plus channel checks on mix shifts between MEMS-based systems and higher performance gyro technologies. When the bottom-up view had gaps, for example limited visibility on smaller program buys, we bridged the missing portion using ratios observed in primary interviews, then stress-tested the results against public contract timing.

For forecasting, scenario analysis was used to reflect program timing risk, regional defense allocation changes, and adoption pace in industrial and marine navigation. Assumptions on ASP movement were kept explicit, with mix-driven changes higher than inflation-driven changes, and they were reviewed with experts to avoid overstating premium-grade migration.

Data Validation & Update Cycle

Outputs were validated through multiple checks so the story matched real-world signals. Model results were compared against independent indicators such as platform delivery counts, procurement announcements, and technology mix commentary, and then large variances were traced back to the specific assumption that caused them.

Before sign-off, the work goes through step-by-step analyst review where calculations, unit logic, and currency conversions are rechecked. If a critical input looks off, we do targeted re-contacts. Reports are refreshed annually, and material events such as major program awards or export restrictions trigger interim adjustments. Right before delivery, a final pass is done to ensure the latest public updates are reflected in both the numbers and the narrative.

Mordor Intelligence's Inertial Navigation System Market Size Measured Against Other Published Estimates

Published INS market values often do not align because each publisher draws the line differently on what counts as an INS sale, and because platform and grade mix can change value quickly even when unit demand is steady. Differences also come from how pricing is treated across navigation-grade, tactical-grade, and industrial-grade systems, and from whether an estimate is anchored to procurement timing or to broader electronics demand.

The main gap comes from whether stand-alone inertial sensors and software-only navigation stacks are counted as INS, where Mordor Intelligence counts only complete INS units with onboard navigation computation. This scope keeps the 2025 total tied to platform-level demand signals and grade-level ASP checks.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 10.81 B (2025) | |

| Industry Research Publisher A | USD 12.10 B (2024) | Uses an earlier base year and appears to use broader buckets (including services and some adjacent solution categories), which can lift totals when integration and support revenue are blended into product value. |

| Global Research Publisher B | USD 13.65 B (2025) | Tends to apply a wider platform and end-user lens with a faster ASP and mix progression, which can raise the 2025 value if more commercial and premium-grade content is assumed within the counted scope. |

The spread in the table is mainly explained by scope choices and pricing logic rather than a disagreement on where demand is coming from. By keeping the counted item consistent (complete INS units) and then checking it against platform activity and grade mix, the estimate stays traceable to inputs that can be revisited as programs, volumes, and pricing move year to year.

Key Questions Answered in the Report

What is the current size of the inertial navigation system market?

The market is valued at USD 11.5 billion in 2026 and is forecast to reach USD 15.68 billion by 2031.

Which component segment leads revenue?

Inertial Measurement Units account for 42.12% of 2025 revenue and are poised for a 7.25% CAGR.

Why are MEMS gyroscopes gaining share?

MEMS devices deliver lower cost, reduced power draw, and shock resistance, enabling adoption in consumer, automotive, and industrial products.

Which industry vertical is expanding fastest?

Automotive applications show an 8.05% CAGR as OEMs incorporate INS into autonomous and ADAS platforms.

How does increasing defense spending influence demand?

Elevated military budgets worldwide boost procurement of navigation-grade systems that can operate without GPS, driving a +1.8% impact on forecast CAGR.

What technology trends could reshape competitive dynamics?

Photonic integrated gyroscopes and quantum-based interferometers promise centimeter-level accuracy at smaller size and lower power, challenging legacy ring laser and fiber-optic solutions.

Page last updated on: