Communication Logic Integrated Circuits Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

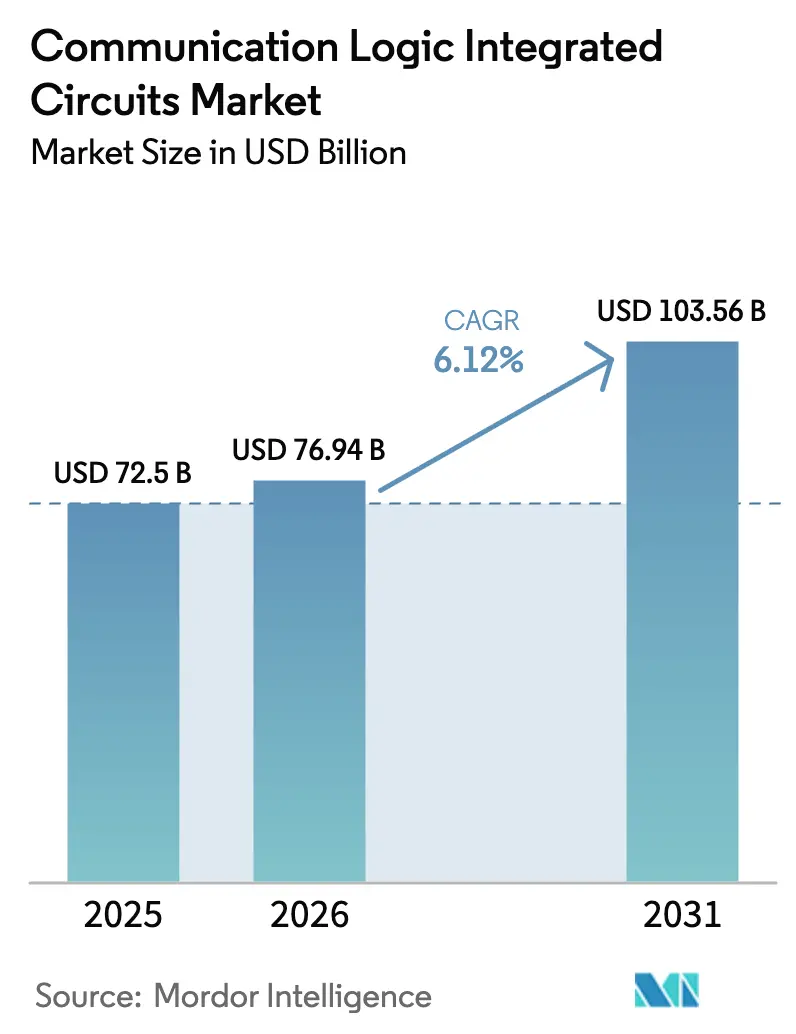

| Market Size (2026) | USD 76.94 Billion |

| Market Size (2031) | USD 103.56 Billion |

| Growth Rate (2026 - 2031) | 6.12% CAGR |

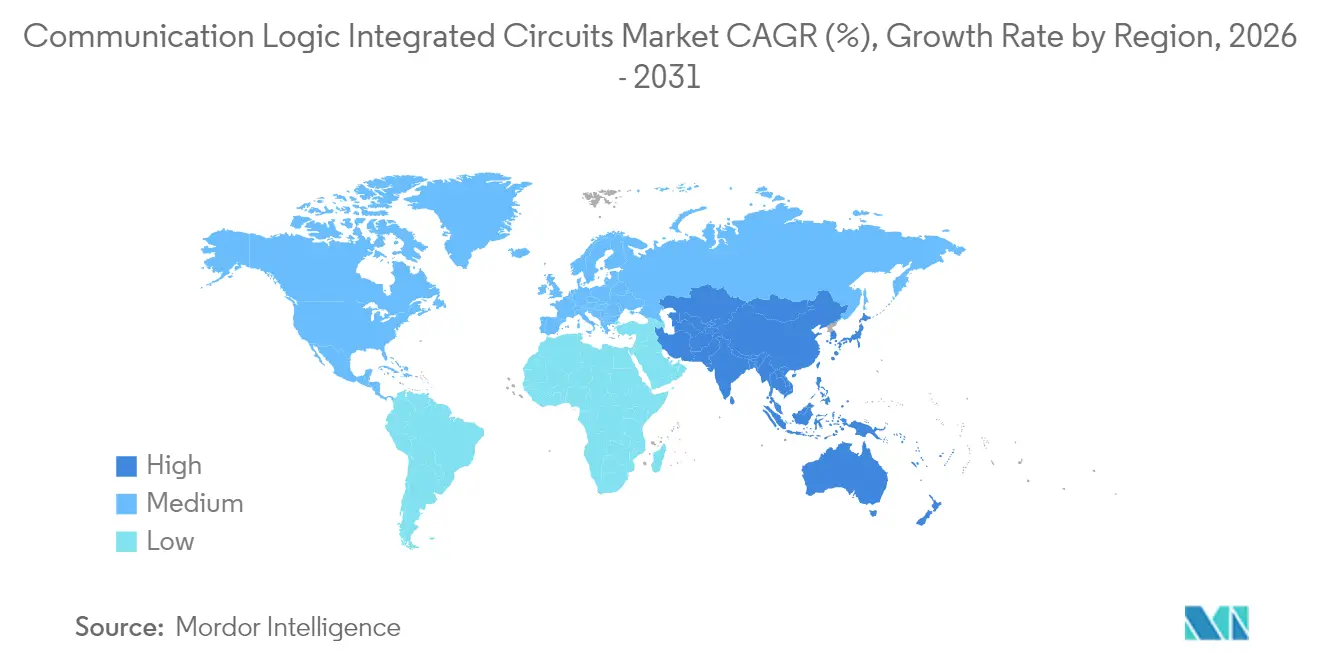

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

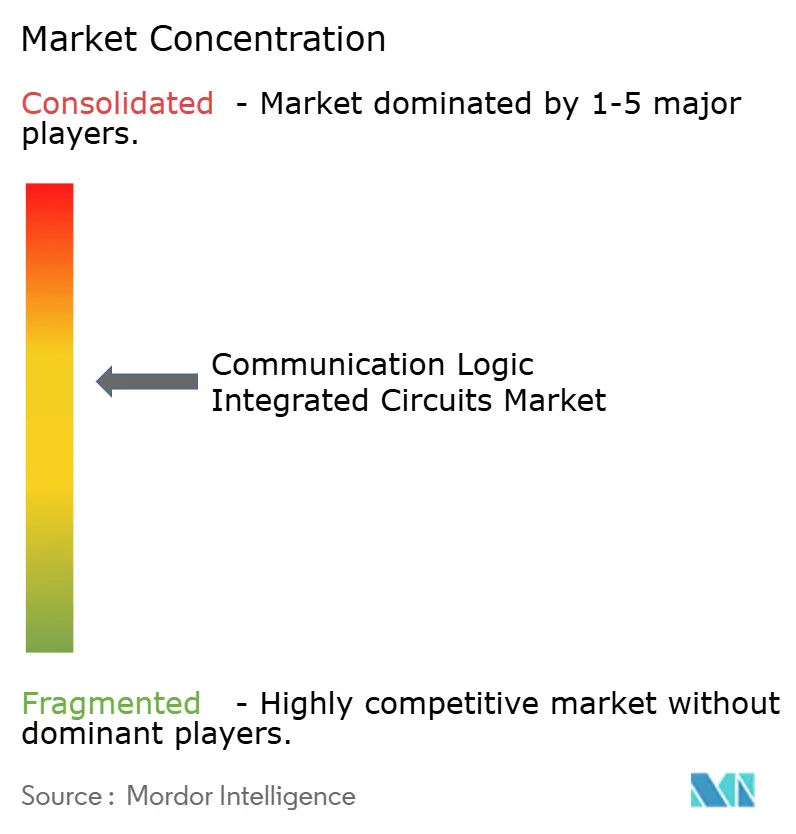

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Communication Logic Integrated Circuits Market Analysis by Mordor Intelligence

The Communication Logic Integrated Circuits market size is expected to grow from USD 72.5 billion in 2025 to USD 76.94 billion in 2026 and is forecast to reach USD 103.56 billion by 2031 at 6.12% CAGR over 2026-2031. This expansion is closely tied to the rapid rollout of sovereign AI infrastructure, the shift toward edge-centric computing topologies, and the widening adoption of 5G front-end modules that require purpose-built communication logic. Additional momentum comes from automotive zonal architectures that redistribute vehicle data flows, and from battery-constrained IoT nodes that integrate low-latency AI coprocessors. Major vendors are moving design resources from legacy connectivity chips toward highly integrated controllers that merge signal processing, power management, and AI acceleration in a single device, ensuring that the Communication Logic Integrated Circuits market retains a pivotal role in next-generation electronics. Heightened capital spending under the US CHIPS Act and EU Chips Act has also begun to rebalance global supply chains, reinforcing North American and European manufacturing depth while preserving the long-standing foundry leadership of Taiwan and South Korea.

Key Report Takeaways

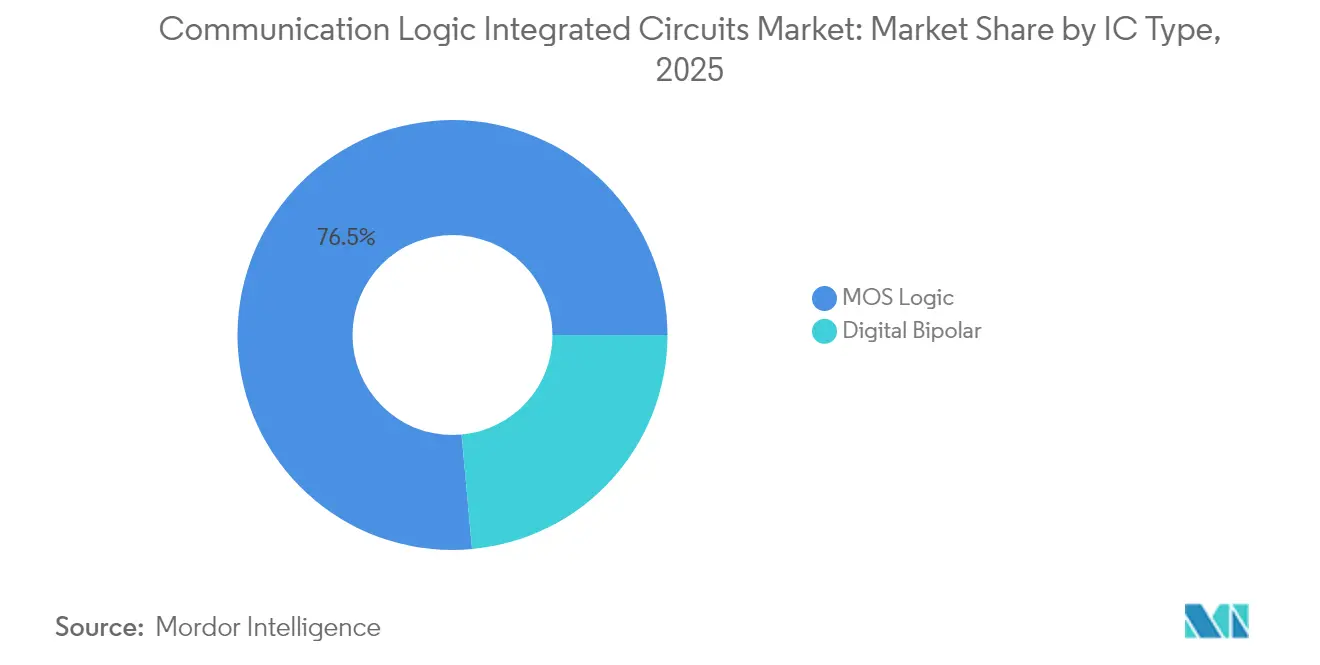

- By IC type, MOS Logic held 76.45% of the Communication Logic Integrated Circuits market share in 2025; MOS Special-Purpose devices are expected to expand at a 8.68% CAGR through 2031.

- By process node, the 16-14 nm class led with 31.95% share in 2025, whereas ≤5 nm devices are forecast to rise at a 14.72% CAGR.

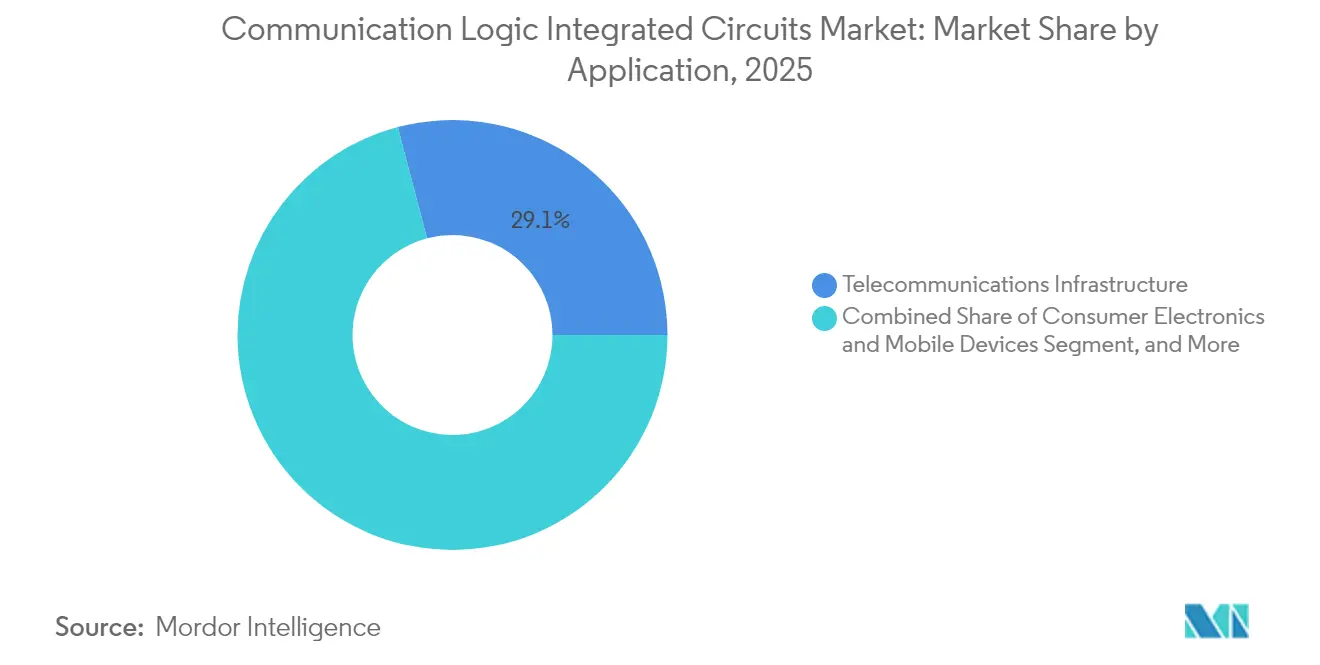

- By application, telecommunications infrastructure captured 29.10% revenue share in 2025, while automotive electronics is projected to grow at 12.15% CAGR to 2031.

- By wafer size, 300 mm fabrication accounted for 67.85% of the Communication Logic Integrated Circuits market size in 2025 and is advancing at a 8.92% CAGR.

- By geography, Asia-Pacific commanded a 41.75% share in 2025; the region is on track for an 10.58% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Communication Logic Integrated Circuits Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surging 5G RF-Frontend Design Wins among Asian IDMs | +1.2% | Asia-Pacific core, spill-over to North America | Medium term (2-4 years) |

| Demand Spike for Low-Power Edge AI Coprocessors in Battery-Powered IoT Nodes | +0.9% | Global, with concentration in North America and EU | Short term (≤ 2 years) |

| Migration of Enterprise Workloads to Cloud Data Centers Driving High-Speed SerDes Demand | +0.8% | North America and EU primary, APAC secondary | Medium term (2-4 years) |

| Automotive Zonal E/E Architectures Boosting High-Bandwidth In-Vehicle Networking ICs | +1.1% | Global, led by Germany, the US, and China, are automotive hubs | Long term (≥ 4 years) |

| Open-RAN Disaggregation Creating New Volume for Programmable Logic Devices | +0.7% | North America and EU early adoption, APAC scale deployment | Medium term (2-4 years) |

| U.S. CHIPS and EU Chips Acts Catalyzing Advanced Logic Capacity Investments | +0.6% | North America and EU domestic, indirect global impact | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Surging 5G RF-Frontend Design Wins among Asian IDMs

Strong 5G base-station deployments in South Korea, Taiwan, and mainland China encouraged Asian integrated device manufacturers to lock in beam-forming and antenna-tuning sockets once dominated by Western suppliers.[1]Ko Dong-hwan, “Korea Unveils Plan to Build $471 Bil. Mega Chip Cluster in Gyeonggi Province,” The Korea Times, koreatimes.co.kr MediaTek broadened its RF portfolio while partnering with regional foundries for mid-range nodes that trade peak efficiency for sizable cost savings. These design wins reduced supplier concentration in the Communication Logic Integrated Circuits market and shifted procurement decisions toward firms located near contract manufacturers, lowering logistics overhead and shortening design-to-production cycles. Network operators favored this proximity to speed iterative hardware revisions and maintain bill-of-materials discipline. As 5G densification pivots from flagship urban zones to suburban coverage, local IDMs are poised to retain volume leadership, reflecting a structural change in competitive dynamics.

Demand Spike for Low-Power Edge AI Coprocessors in Battery-Powered IoT Nodes

The influx of battery-operated sensors in industrial and consumer environments raised the priority of ultra-low-power communication logic able to handle AI inference tasks without compromising runtimes. Syntiant’s 2024 acquisition of Knowles Consumer MEMS underscored how commercial success now depends on co-optimizing RF interfaces with neural inference engines, allowing wake-on-AI triggers that keep radios dormant until events of interest occur. Device makers that once adopted off-the-shelf Bluetooth or Wi-Fi controllers now request application-specific designs that embed adaptive duty-cycling and integrated voice activity detection, forcing IC suppliers to rethink standard product roadmaps. The resulting product wave strengthens the Communication Logic Integrated Circuits market as a cornerstone of pervasive intelligence deployments.

Migration of Enterprise Workloads to Cloud Data Centers Driving High-Speed SerDes Demand

Enterprise cloud migration re-shaped intra-data-center traffic patterns as AI training jobs generated bursty, latency-sensitive east-west flows that stressed conventional connectivity silicon. Marvell and Broadcom each released 224 Gbps SerDes lanes and PCIe Gen 6 fabrics, enabling rack-scale GPU clusters to communicate at multi-terabit throughputs. Hyperscale operators prioritized bandwidth per watt ahead of absolute efficiency, reversing a decade of energy-focused optimization. Custom cloud ASIC teams pushed vendors for long-reach retimer solutions that maintain signal integrity across larger server pools, translating into robust order backlogs for the Communication Logic Integrated Circuits market. The trend will intensify as memory disaggregation based on Compute Express Link becomes mainstream.

Automotive Zonal E/E Architectures Boosting High-Bandwidth In-Vehicle Networking ICs

OEM migrations from distributed electronic control units toward zonal domains amplified Ethernet backbone traffic inside vehicles. NXP expanded its S32 networking portfolio while Infineon embedded communication subsystems into RISC-V microcontrollers, reflecting OEM demand for deterministic latency across mixed-criticality traffic. High-speed backbones must coexist with time-sensitive networking extensions to guarantee safety functions alongside infotainment streams, elevating design complexity and value-add for communication logic suppliers. Certification cycles remain stringent, yet premium models now set the blueprint for mass-segment adoption, ensuring that automotive volumes will surpass traditional infrastructure consumption for several key device classes before 2030. This inflection secures another long-term growth pillar for the Communication Logic Integrated Circuits market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Escalating Mask-Set Costs Beyond 5 nm Nodes | -0.8% | Global, concentrated in advanced foundry locations | Short term (≤ 2 years) |

| IP Export Controls Curtailing Leading-Edge Logic Supply to China | -0.5% | Global supply chain, China demand impact | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Escalating Mask-Set Costs Beyond 5 nm Nodes

Mask-set pricing rose sharply once production crossed below the 5 nm threshold, where extreme ultraviolet lithography demands complex pellicle stacks and higher defect control. At 2 nm, a single mask set averaged USD 30,000, and at 1.4 nm, pricing climbed to USD 45,000, stretching capital budgets for mid-tier vendors that specialize in low-volume, application-specific communication ICs. Each design iteration often requires mask respins, compounding the investment hurdle and pushing smaller firms toward mature process nodes, even when next-generation energy performance is needed. This divergence slows innovation cadence within the Communication Logic Integrated Circuits market and concentrates high-margin volumes among the handful of foundries able to fund process migrations.

IP Export Controls Curtailing Leading-Edge Logic Supply to China

Expanded US and allied export restrictions on advanced logic process nodes constrained Chinese access to high-performance communication ICs. Global vendors now pursue parallel product lines—one compliant with leading-edge guidelines for unrestricted markets, and another based on mature geometries suitable for export. Compliance costs and duplicated engineering workloads divert resources away from core R&D, modestly suppressing aggregate output value. Domestic Chinese firms accelerated indigenous 14 nm and planned 7 nm development, but yield challenges and tool shortages mean that performance lags are likely for several years, generating a fragmented demand landscape that the Communication Logic Integrated Circuits market must navigate.[2]Center for Strategic and International Studies Staff, “Understanding U.S. Allies’ Current Legal Authority to Implement AI and Semiconductor Export Controls,” CSIS, csis.org

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By IC Type: MOS Logic Dominance Faces Special-Purpose Disruption

The 2025 baseline showed MOS Logic devices holding 76.45% share of the Communication Logic Integrated Circuits market, confirming their role as the universal platform for telecom baseband cards, broadband gateways, and hyperscale switch silicon. MOS gate arrays and standard-cell architectures reduced non-recurring engineering charges, letting OEMs target annual refresh cycles without incurring the expense of full custom designs. At the same time, MOS drivers/controllers retained critical sockets between digital logic and wideband RF front-ends, safeguarding legacy revenue streams for incumbent suppliers. Digital bipolar devices preserved a small niche in millimeter-wave back-haul where linearity and dynamic range surpass MOS alternatives.

Special-purpose MOS variants have begun to redefine value capture. They expanded at a 8.68% CAGR through 2031, propelled by edge analytics gateways, advanced driver-assistance systems, and zonal domain controllers that call for deterministic traffic shaping. Vendors carved out programmable logic blocks around proprietary accelerators, creating performance headroom without the silicon area penalties of monolithic SoCs. Automotive original equipment manufacturers have already integrated such tailored controllers to merge safety-critical CAN traffic, infotainment video, and sensor fusion feeds on a common backbone. As more software-defined workloads migrate to end points, this application momentum will continue to tilt the Communication Logic Integrated Circuits market toward flexible yet task-optimized devices.

By Process Node: Advanced Nodes Drive Performance Migration

The mid-range 16-14 nm class retained 31.95% share in 2025, balancing die cost, power consumption, and accessory intellectual-property availability. These nodes remain popular for carrier access equipment, small-cell radios, and enterprise Wi-Fi chips. The Communication Logic Integrated Circuits market size attributed to this node family is forecast to hold steady until 2027 before tapering as more designs shift downward in geometry.

In contrast, ≤5 nm fabrication is projected to surge at a 14.72% CAGR, reflecting AI inference functions that demand dense arithmetic throughput within power-limited form factors. Prototype 3 nm SerDes exceeding 224 Gbps already validated performance headroom for cloud optical links, and mobile system-on-chips scheduled for 2026, incorporate similar communication subsystems. Although escalating wafer and mask fees remain a hurdle, large consumer smartphone and hyperscale procurement volumes help amortize capital costs across tens of millions of dies, ensuring that cutting-edge process capacity remains fully booked. Consequently, the Communication Logic Integrated Circuits market will feature a dual-track roadmap in which advanced nodes address performance-driven tiers while mature geometries serve cost-sensitive mass deployments.

By Application: Automotive Electronics Accelerates Past Traditional Leaders

Telecommunications infrastructure dominated revenue with a 29.10% Communication Logic Integrated Circuits market share in 2025, benefiting from 5G macro-cell densification, fiber access rollouts, and continued DOCSIS upgrades. Yet automotive electronics registered the swiftest trajectory at 12.15% CAGR, as zonal architectures consolidated control units and shifted gigabit traffic to vehicle backbones. During model-year 2025 launches, premium marques adopted multigigabit PHYs to feed Level 3 driver-assistance processors, illustrating how robust networking now underpins differentiation in software-defined vehicles.

Cloud data centers secured their growth path as enterprise AI workloads multiplied. Hyperscale operators deployed retimer-rich switch-ASIC boards that required advanced SerDes channels and clock-data-recovery logic. Consumer devices, once the principal volume anchor, now evolve at a measured pace given lengthening replacement cycles, but still inject consistent baseline demand for Bluetooth, Wi-Fi, and ultra-wideband co-processors. Across these verticals, the Communication Logic Integrated Circuits market size for automotive content is on track to surpass traditional telecom by 2029 under base-case penetration forecasts.

By Wafer Size: 300 mm Fabrication Drives Cost Leadership

Large-diameter 300 mm wafers supplied 67.85% of 2025 unit volume and are increasing at a 8.92% CAGR, reflecting lower cost per die for highly metalized, routing-intensive communication SoCs. Foundries expanded 300 mm output in Arizona, Kumamoto, and Hsinchu to accommodate high-density reticle designs that cannot break even on 200 mm lines. These economics granted leading vendors a durable manufacturing cost advantage, consolidating mid-tier competitors that lack the capital base to reserve advanced line-time.

Two-hundred-millimeter fabrication maintains relevance for analog-heavy or ruggedized parts where legacy equipment and shorter cycle times outweigh raw die-count efficiency. Wafer diameters ≤150 mm persist in aerospace, defense, and medical subsegments where heritage qualification and radiation tolerance enforce older toolsets. Nonetheless, R&D budgets skew decisively toward 300 mm; by 2030, almost every new tape-out targeting volume manufacturing is expected to leverage the format. This scale effect reinforces the Communication Logic Integrated Circuits market trend toward fewer but larger fabs capable of shipping multimillion-unit quarterly volumes.

Geography Analysis

Asia-Pacific captured 41.75% of the Communication Logic Integrated Circuits market revenue in 2025 and is pacing toward an 10.58% CAGR through 2031. South Korea launched a USD 471 billion cluster in Gyeonggi Province that will host 16 new fabs from Samsung and SK Hynix, fortifying regional supply depth and generating significant foundry demand for RF front-end and SerDes controllers. Japan simultaneously revived domestic capability through partnerships with TSMC and Rapidus, positioning the archipelago as an auxiliary hub for advanced communication logic. Mainland China’s trajectory became more complex under export controls, prompting accelerated domestic node investment and creating parallel ecosystems that global vendors must reconcile while pursuing long-term growth.

North America benefited from USD 39 billion in CHIPS Act incentives that drew major expansions by Intel, TSMC, and SkyWater. These projects targeted secure supply for data-center interconnect ASICs and automotive Ethernet controllers demanded by US-based customers. Canada leveraged photonics research institutes to nurture start-ups focused on coherent optics, while Mexico gained test-and-assembly work due to near-shoring strategies in consumer device-grade Wi-Fi and Bluetooth modules. Collectively, these moves strengthened continental resilience, trimming logistic risks that came into focus during earlier supply shortages.

Europe advanced its goal of a 20% global share by 2030 through the EUR 43 billion EU Chips Act. Germany prioritized automotive processors that merge zonal networking with functional safety requirements, and France invested in 300 mm pilot lines for low-power edge AI connectivity SoCs. Nordic states applied device expertise to renewable microgrid communicators, making specialized gateway logic a rising niche. Post-Brexit trade negotiated carve-outs for UK-based design houses that license digital front-ends to European foundries, keeping intellectual property flows active despite new customs layers.

Competitive Landscape

Established companies such as Intel, Texas Instruments, and Analog Devices relied on vertically integrated portfolios to deliver combined power, clock, and communication solutions. Their dominance rests on multi-decade customer relationships and process co-optimization across adjacent analog blocks. Nonetheless, pure-play AI chipmakers began inserting custom DSP blocks that absorb classical serializer-deserializer functions, shifting some demand away from traditional suppliers. Qualcomm protected its leadership in multi-radio coordination through a growing patent estate that covers low-latency scheduling across Wi-Fi, cellular, and Bluetooth bands.[4]Qualcomm Technologies Patent, “Managing Signals on Multiple Wireless Links,” Nweon, nweon.com

Strategic focus migrated toward application-specific differentiation rather than generic speed or channel counts. Vendors allocated R&D dollars to automotive AEC-Q100 compliance, sub-milliwatt sensor companion chips, and coherent optics modules, each niche requiring expertise that off-the-shelf intellectual-property catalogs cannot meet. Parallel design tracks for restricted and unrestricted markets, mandated by export regimes, altered cost structures, and rewarded players able to amortize duplicated work over broad customer bases. Meanwhile, open-interface initiatives such as Open-RAN and Compute Express Link reduced lock-in, pressuring incumbents to release more interoperable firmware.

Mergers and acquisitions remained central to capability acceleration. AMD’s 2025 purchase of silicon-photonics specialist Enosemi brought integrated optical interfaces directly onto compute die, a feature critical for next-generation GPU clusters. Nokia’s earlier move to absorb Infinera aligned optical transport know-how with mobile-core silicon, foreshadowing tighter horizontal bundling in operator hardware. These transactions signal that future leadership in the Communication Logic Integrated Circuits market will hinge on end-to-end system knowledge rather than discrete component efficiency alone.

Communication Logic Integrated Circuits Industry Leaders

STMicroelectronics N.V.

Analog Devices Inc.

Broadcom Inc.

Intel Corporation

NXP Semiconductors N.V.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: AMD acquired Enosemi to enhance optical-interconnect bandwidth for AI data centers.

- March 2025: TSMC announced a NT$1.5 trillion (USD 45.2 billion) expansion for 2 nm production capacity in Kaohsiung.

- February 2025: SkyWater Technology bought Infineon’s Austin fab, broadening US-based communication IC output.

- January 2025: Nokia completed its USD 2.3 billion purchase of Infinera, integrating optical networking IP with mobile infrastructure silicon.

Global Communication Logic Integrated Circuits Market Report Scope

Logic integrated circuits (ICs) are specialized semiconductor devices that perform logical operations on digital signals. These operations include fundamental functions such as AND, OR, and NOT, which are the building blocks of digital circuits.

For market estimation, the revenue generated from sales of various types of communication logic integrated circuits, such as digital bipolar and MOS logic, across a diverse range of geographic regions worldwide is tracked. Market trends are evaluated by analyzing product innovation, diversification, and expansion investments. Enhancements in energy efficiency, artificial intelligence, miniaturization, machine learning, 5G, data centers, etc., are also crucial in determining the growth of the studied market.

The communication logic integrated circuits market is segmented by IC type (digital bipolar and MOS logic [MOS general purpose, MOS gate arrays, MOS drivers/controllers, MOS standard cells, and MOS special purpose]) and geography (the United States, Europe, Japan, China, Korea, Taiwan, and Rest of the World). The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

| Digital Bipolar | |

| MOS Logic | MOS General Purpose |

| MOS Gate Arrays | |

| MOS Drivers / Controllers | |

| MOS Standard Cells | |

| MOS Special Purpose |

| ≥90 nm |

| 65 – 40 nm |

| 32 – 22 nm |

| 16 – 14 nm |

| 10 – 7 nm |

| ≤5 nm |

| ≤150 mm |

| 200 mm |

| 300 mm |

| Telecommunications Infrastructure |

| Consumer Electronics and Mobile Devices |

| Data Centers and Cloud Computing |

| Automotive Electronics |

| Industrial and IoT |

| Aerospace and Defense |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| France | ||

| United Kingdom | ||

| Nordics | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Taiwan | ||

| South Korea | ||

| Japan | ||

| India | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Mexico | ||

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Rest of Africa | ||

| By IC Type | Digital Bipolar | ||

| MOS Logic | MOS General Purpose | ||

| MOS Gate Arrays | |||

| MOS Drivers / Controllers | |||

| MOS Standard Cells | |||

| MOS Special Purpose | |||

| By Process Node | ≥90 nm | ||

| 65 – 40 nm | |||

| 32 – 22 nm | |||

| 16 – 14 nm | |||

| 10 – 7 nm | |||

| ≤5 nm | |||

| By Wafer Size | ≤150 mm | ||

| 200 mm | |||

| 300 mm | |||

| By Application | Telecommunications Infrastructure | ||

| Consumer Electronics and Mobile Devices | |||

| Data Centers and Cloud Computing | |||

| Automotive Electronics | |||

| Industrial and IoT | |||

| Aerospace and Defense | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | Germany | ||

| France | |||

| United Kingdom | |||

| Nordics | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Taiwan | |||

| South Korea | |||

| Japan | |||

| India | |||

| Rest of Asia-Pacific | |||

| South America | Brazil | ||

| Mexico | |||

| Argentina | |||

| Rest of South America | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current size of the Communication Logic Integrated Circuits market?

The market is valued at USD 76.94 billion in 2026 and is projected to reach USD 103.56 billion by 2031.

Which application segment is growing fastest?

Automotive electronics is forecast to advance at 12.15% CAGR, driven by zonal vehicle networks and software-defined features.

Why are ≤5 nm nodes becoming important for communication logic?

They offer higher transistor density that supports AI inference and multi-terabit SerDes while meeting stringent power envelopes.

How do mask-set costs affect smaller IC vendors?

Sub-5 nm mask sets can exceed USD 30,000, raising project budgets and limiting advanced node access for firms with niche volumes.

What impact do export controls have on market dynamics?

Restrictions require separate product lines for China and non-China markets, increasing engineering overhead and altering supply chain strategy.

Which region contributes most to market revenue today?

Asia-Pacific leads with 41.75% share, bolstered by large-scale investments in South Korea, Japan, and Taiwan.

Page last updated on: