United States Industrial Gas Regulator Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

| Market Size (2025) | USD 3.11 Billion |

| Market Size (2030) | USD 3.71 Billion |

| Growth Rate (2025 - 2030) | 3.64% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United States Industrial Gas Regulator Market Analysis by Mordor Intelligence

The United States industrial gas regulator market size is estimated at USD 3.11 billion in 2025 and is projected to reach USD 3.71 billion by 2030, growing at a 3.64% CAGR from 2025 to 2030. Healthy demand from semiconductor fabs, hydrogen fueling stations, and chemical processing plants sustains growth despite the market’s mature profile. Procurement priorities now favor regulators that fuse traditional mechanical reliability with digital pressure-sensor modules, enabling closer compliance monitoring and predictive maintenance. Suppliers capable of guaranteeing ultra-high-purity performance for reactive and specialty gases gain an edge as chipmakers and green hydrogen integrators expand their capacity. Material cost volatility for nickel and copper complicates pricing strategies, yet retrofit programs in aging Midwest complexes help maintain steady baseline order flows.

Key Report Takeaways

- By gas type, reactive gases led with 38.12% of the United States industrial gas regulator market share in 2024, while specialty and calibration blends are projected to post a 3.51% CAGR through 2030.

- By material, brass retained a 42.67% share of the United States industrial gas regulator market in 2024, whereas high-purity alloys are projected to grow at a 4.12% CAGR by 2030.

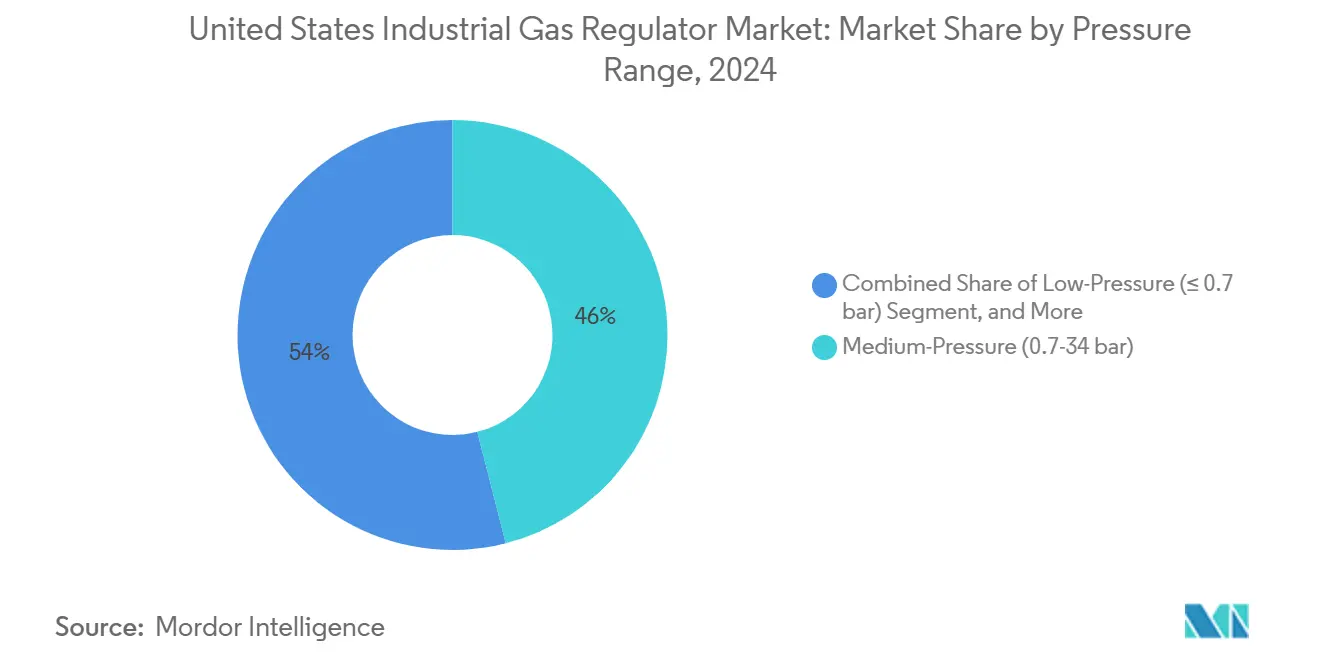

- By pressure range, medium-pressure regulators captured 46.01% share of the United States industrial gas regulator market size in 2024, and high-pressure units are expected to expand at a 4.81% CAGR to 2030.

- By end-use industry, the chemicals and petrochemicals segment held 27.43% of the United States industrial gas regulator market share in 2024; energy transition applications are set to log the fastest 5.08% CAGR through 2030.

Worldwide, activity is shaped by contributions from multiple countries and regions, with United states representing one among them. The global report on industrial gas regulator market by Mordor Intelligence reflects how these countries and regional layers combine into a single system.

United States Industrial Gas Regulator Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accelerating expansion of U.S. specialty gas blending facilities | +0.8% | Texas Gulf Coast, Pennsylvania | Medium term (2-4 years) |

| Surging demand for high-purity regulators in semiconductor fabs | +0.9% | Arizona, Oregon, New York, Ohio | Short term (≤ 2 years) |

| Rapid uptake of hydrogen fueling stations across California and Texas | +0.6% | California, Texas, Pacific Northwest | Long term (≥ 4 years) |

| Tightening OSHA and EPA safety compliance for toxic gas handling | +0.7% | National | Short term (≤ 2 years) |

| Growing retrofit activity in aging Midwest chemicals plants | +0.5% | Ohio, Indiana, Illinois | Medium term (2-4 years) |

| Under-the-radar integration of digital pressure sensors in legacy brass regulators | +0.4% | National | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Accelerating Expansion of U.S. Specialty Gas Blending Facilities

Multiple new specialty gas plants are coming online, including Air Liquide’s USD 850 million Boise project timed to support Micron’s memory-chip line. Each plant requires ultra-high-purity pressure control with contamination thresholds below 1 ppb, thereby increasing demand for precision-machined regulators with sub-micron surface finishes. Localized production nodes reduce lead times, allowing regulators with domestic machining capacity to enjoy logistical savings. Merck’s USD 1 billion build-out in Pennsylvania signals continued geographic clustering near semiconductor corridors. Procurement specifications increasingly bundle digital leak-detection modules to meet customer uptime targets, pushing average selling prices upward.

Surging Demand for High-Purity Regulators in Semiconductor Fabs

Intel’s USD 20 billion Ohio fab and TSMC’s Arizona site both list Hastelloy or Monel regulators with leak rates below 1 × 10⁻⁹ sccs as the baseline. Swagelok documentation indicates that chip fabs require ±0.1% pressure stability from -40 °C to +150 °C, driving the adoption of orbital-welded assemblies with electropolished wetted paths. These stringent criteria limit the qualified supplier pool and enable margin premiums that counterbalance metal-cost swings. Volume ramps scheduled for 2026-2027 maintain high visibility for regulator orders tied to line-tool installations.

Rapid Uptake of Hydrogen Fueling Stations Across California and Texas

California’s SB 1418 and SB 1420 now mandate greater station density, and ARCHES hub funding brings USD 1.2 billion to accelerate deployment. Typical 700-bar forecourt dispensers require dual-stage regulators with hydrogen-embrittlement-resistant alloys. Parallel activity in Texas focuses on industrial hydrogen clusters near petrochemical complexes, linking dispensing networks with pipeline hubs. Federal decarbonization grants covering hydrogen-ready iron plants extend regulator demand into heavy-industry process lines.

Tightening OSHA and EPA Safety Compliance for Toxic Gas Handling

HazCom and RMP revisions sharpen scrutiny on chlorine, ammonia, and sulfur hexafluoride systems. Upgrades often replace legacy spring-loaded relief valves with smart regulators that pair integrated burst disks with IoT sensors, feeding plant DCS dashboards. Documentation packages that include finite element analyses and SIL-rated safety loops are increasingly making or breaking bid awards, elevating suppliers that maintain in-house engineering staff certified to ASME codes.[1]U.S. Department of Energy, “Industrial Decarbonization Funding Opportunity,” energy.gov

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatility in nickel and copper prices impacting stainless and brass regulators | -0.6% | Global, North America manufacturing | Short term (≤ 2 years) |

| Lengthy certification cycles for regulators in nuclear-grade applications | -0.3% | Nuclear facility regions | Long term (≥ 4 years) |

| Under-the-radar talent shortage of ASME-certified regulator welders | -0.4% | National | Medium term (2-4 years) |

| Supply chain disruption from specialty alloy castings imported from Europe | -0.5% | National | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Volatility in Nickel and Copper Prices Impacting Stainless and Brass Regulators

Nickel swung 40% during 2024, while copper traded above USD 8,000 per t, compressing margins for stainless and brass assemblies. OEMs holding multi-year framework contracts face lagged pass-through levers, and bid validity windows have shrunk to thirty days. Material hedging only partly offsets exposure because small-batch exotic-alloy orders lack futures contracts. Consequently, some manufacturers resize flow paths or adopt duplex stainless steel blends to reduce total nickel, but any redesign triggers requalification that can last a year.

Lengthy Certification Cycles for Regulators in Nuclear-Grade Applications

NRC Type Test programs stretch 18-36 months and require destructive helium-leak trials plus seismic shake-table runs. The GAO identified a 57-person staffing gap in the NRC’s advanced-reactor office, which prolonged review intervals. Suppliers must carry inventory against uncertain approval dates, tying up working capital. Yet vendors that secure certification become entrenched for decades because nuclear facilities rarely rebid critical components.[2]U.S. Government Accountability Office, “NRC Licensing Workforce Report,” gao.gov

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Gas Type: Reactive Gases Drive Core Demand

Reactive gases accounted for 38.12% of the United States industrial gas regulator market share in 2024, reflecting the large volume of oxygen and hydrogen throughput in the chemicals, metal processing, and emerging green-hydrogen loops. Reactors, reformers, and blast furnaces rely on consistent medium-pressure oxygen feeds, making robust brass or stainless regulators a baseline necessity. Hydrogen’s growing role in ammonia and direct-reduced iron plants lifts demand for high-pressure units with hydrogen-embrittlement-resistant alloys. Specialty and calibration blends are expected to register a 3.51% CAGR by 2030, propelled by semiconductor etch and deposition steps that need contaminant levels below 1 ppb. These blends typically move in small-batch cylinders, prompting orders for compact diaphragm regulators equipped with electropolished wetted parts and precision needle valves.

Inert gases, such as nitrogen and argon, provide blanket atmospheres for food, pharmaceutical, and metal fabrication lines; growth remains steady but unspectacular. Corrosive and toxic gases, including chlorine and sulfur hexafluoride, represent niche yet high-margin opportunities because they mandate fluoropolymer seals and remote isolation features. Suppliers that maintain cross-certifications for oxygen-service cleaning plus toxic-gas safety relief earn preferred-vendor status. Hydrogen’s rise under federal decarbonization grants further widens the installed base of regulators rated above 350 bar, offsetting slower growth in traditional petrochemical oxygen duty cycles.[3]U.S. Department of Energy, “Clean Hydrogen Strategy,” energy.gov

By Material: Brass Dominance Faces High-Purity Challenge

Brass retained 42.67% of the United States industrial gas regulator market share in 2024, thanks to its cost-efficiency and adequate corrosion resistance for compressed air, nitrogen, and low-grade hydrogen service. Standard bar-stock machining and chrome-plating lines are mature, keeping unit costs low. Stainless steel commands higher ASPs and mitigates mild corrosives, making it the workhorse for pharmaceutical nitrogen, beverage CO₂, and many petrochemical oxygen circuits. Exotic alloys are projected to post a 4.12% CAGR through 2030, driven by semiconductor fabs and advanced reactors that require Monel, Hastelloy, or Inconel bodies for ultra-high-purity or high-temperature helium applications. High-purity alloy orders typically include particle-count certificates and helium-leak tests below 1×10⁻⁹ sccs, enhancing the value per unit.

Nickel volatility pressures stainless margins, while copper price swings hit brass. Some OEMs trial duplex stainless or nickel-free steels, but re-qualification adds time. Concurrently, digital sensor retrofits into brass units provide a low-CapEx modernization path, delaying full stainless or alloy-body replacements in cash-constrained plants. European alloy-casting bottlenecks continue to pose a supply risk, prompting buyers to diversify their foundry sources. Vendors that align material choices with total cost-of-ownership analytics win bids where end users quantify lifecycle savings.

By Pressure Range: Medium-Pressure Applications Dominate

Medium-pressure regulators, operating between 0.7 and 34 bar, captured a 46.01% share of the United States industrial gas regulator market size in 2024. Chemical reactors, refinery purge systems, and HVAC controls typically fall in this band, supporting stable order frequency. Low-pressure devices operating under 0.7 bar serve labs and precision metrology; demand remains niche yet profitable due to stringent repeatability specifications. High-pressure regulators above 34 bar are projected to grow at a 4.81% CAGR through 2030, driven by 700-bar hydrogen dispensation, carbon capture pilots, and helium-loop advanced reactors.

High-pressure designs must hold ±0.1% set-point across wide thermal swings, necessitating precision-ground stems and layered diaphragm packs. Hydrogen embrittlement risks necessitate the use of Monel or special-annealed stainless steel. The cost per unit exceeds that of medium-pressure models by factors of three to six, thereby bolstering revenue despite lower volumes. OEMs that streamline component modularity across pressure classes simplify MRO stocking for distributors, aiding market penetration.

By End-Use Industry: Chemicals Lead, Energy Transition Accelerates

Chemicals and petrochemicals accounted for a 27.43% share of the United States industrial gas regulator market size in 2024, driven by steady demand for oxygen, nitrogen, and hydrogen across cracking, reforming, and polymerization trains. Refurbishment cycles for 1960-1980-vintage Midwest complexes add retrofit tonnage for smart regulator replacements. Energy transition applications are primed for a 5.08% CAGR through 2030 as green-hydrogen hubs, fuel-cell rollout, and hydrogen-ready direct-reduced iron lines multiply.

Oil and gas maintain a sizable installed base in upstream gas lift, midstream compression, and downstream refining; however, growth plateaus due to flat rig counts and decarbonization policies. Semiconductor, life sciences, and food and beverage segments create valuable, high-purity niches. Nuclear advanced-reactor demonstrations, though small in unit volume, yield high average selling prices due to stringent testing. Vendors successful across multiple verticals diversify revenue, limit cyclic exposure, and achieve economies of scale in component sourcing.

Geography Analysis

California anchors hydrogen infrastructure growth through state mandates and ARCHES federal funding, accelerating orders for 700-bar regulators outfitted with embrittlement-resistant trims. Dozens of forecourt stations now specify dual-stage regulators, and heavy-duty fleet depots underpin multi-year demand visibility. Texas mirrors momentum in industrial hydrogen, leveraging Gulf Coast petrochemical assets and port export plans. Suppliers with Houston warehousing achieve faster site-commissioning support, a decisive bid factor for EPCs.

The Midwest industrial belt, notably Ohio, Indiana, and Illinois, drives the volume of retrofits. Northern Indiana Public Service Company’s 2024 resource plan outlines 2,600 MW of new combined-cycle capacity, each block outfitted with hundreds of nitrogen blanketing and instrument-air regulators. Skilled manufacturing labor pools persist, though ASME welder shortages extend project timelines. Local OEMs leverage these strengths to offset material cost headwinds through lean cellular assembly.

Pennsylvania emerges as a specialty-gas epicenter after Merck’s USD 1 billion plant announcement. The Northeast corridor maintains pharmaceutical-grade demand for stainless and alloy regulators, while Arizona and Oregon enjoy semiconductor expansion from Intel and TSMC. Wyoming and Washington house advanced reactor pilots, introducing high-pressure helium duty cycles that few suppliers can meet. Regional diversification spreads risk and supports fulfillment network optimization.

Competitive Landscape

Moderate consolidation defines the United States industrial gas regulator market. Parker Hannifin’s Flow and Process Control division posted USD 4.67 billion in trailing-twelve-month sales, enabling platform investments in hydrogen-compatible trims and digital monitoring bundles. Emerson’s Final Control group follows, integrating regulators with its valve, actuator, and AspenTech optimization software stack.[4]Emerson Electric Co., “Final Control Segment Highlights,” emerson.com Swagelok leverages channel exclusivity and application engineering to protect its share in ultra-high-purity niches.

Technical performance and compliance support, rather than price, increasingly influence procurements. Vendors invest in IoT-ready sensor blocks, electropolished interiors, and low-outgassing seat materials. Honeywell’s 2024 LNG-process acquisition signals cross-pollination between cryogenic handling and regulator design. Dover’s cryogenic buys reveal similar strategic scope expansions. Mid-sized specialists differentiate themselves via rapid prototype cycles and custom alloy machining, but face scaling limits due to welder shortages. Workforce development programs become competitive moats.

Certification hurdles in nuclear and semiconductor fabs erect high entry barriers. Once approved, regulators remain embedded for decades, locking in aftermarket spares revenue. Digital retrofit kits threaten displacement of incumbent analog units, sparking alliances between sensor firms and mechanical OEMs. Market leaders hold strong MRO networks that guarantee next-day spares, crucial for fab uptime and refinery turnarounds. Overall contestability remains moderate with room for consolidation in adjacent sensing and data-analytics niches.

United States Industrial Gas Regulator Industry Leaders

Airgas Inc. (an Air Liquide company)

Emerson Electric Co.

Parker Hannifin Corporation

Swagelok Company

The Harris Products Group, a Lincoln Electric Company

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: Emerson advanced its USD 670 million AspenTech merger to deliver integrated optimization and control suites that incorporate regulatory systems.

- August 2025: The Department of Energy allocated new industrial decarbonization funds for hydrogen-ready manufacturing, triggering regulatory orders for direct-reduced iron and chemical lines.

- July 2025: Intel’s Ohio fab crossed procurement milestones, awarding USD 50 million in ultra-high-purity regulator contracts for sub-ppb chip processes.

- June 2025: California awarded bulk regulator supply deals to equip new 700-bar hydrogen stations under the ARCHES hub funding.

United States Industrial Gas Regulator Market Report Scope

| Inert (N₂, Ar) |

| Reactive (O₂, H₂) |

| Corrosive / Toxic (Cl₂, NH₃, HCl, SF₆) |

| Specialty and Calibration Blends |

| Brass |

| Stainless Steel |

| High-Purity Alloys (Monel, Hastelloy) |

| Low-Pressure (≤ 0.7 bar) |

| Medium-Pressure (0.7-34 bar) |

| High-Pressure (≥ 34 bar) |

| Oil and Gas |

| Chemicals and Petrochemicals |

| Metals and Mining |

| Healthcare and Life-Sciences |

| Food and Beverage |

| Electronics and Semiconductor |

| Energy Transition (Green-Hydrogen, Fuel-Cells) |

| By Gas Type | Inert (N₂, Ar) |

| Reactive (O₂, H₂) | |

| Corrosive / Toxic (Cl₂, NH₃, HCl, SF₆) | |

| Specialty and Calibration Blends | |

| By Material | Brass |

| Stainless Steel | |

| High-Purity Alloys (Monel, Hastelloy) | |

| By Pressure Range | Low-Pressure (≤ 0.7 bar) |

| Medium-Pressure (0.7-34 bar) | |

| High-Pressure (≥ 34 bar) | |

| By End-Use Industry | Oil and Gas |

| Chemicals and Petrochemicals | |

| Metals and Mining | |

| Healthcare and Life-Sciences | |

| Food and Beverage | |

| Electronics and Semiconductor | |

| Energy Transition (Green-Hydrogen, Fuel-Cells) |

Key Questions Answered in the Report

How large is current demand for industrial gas regulators in the United States?

The United States industrial gas regulator market size is USD 3.11 billion in 2025 with a projected value of USD 3.71 billion by 2030 at a 3.64% CAGR.

Which gas type drives the highest regulator sales?

Reactive gases such as oxygen and hydrogen lead with 38.12% market share owing to heavy use in chemicals, metals, and emerging hydrogen applications.

What material category is growing fastest?

High-purity alloys including Hastelloy and Monel are forecast to grow at 4.12% CAGR due to semiconductor and nuclear demand.

Why are high-pressure regulators gaining traction?

Deployment of 700-bar hydrogen fueling stations and advanced reactor projects pushes high-pressure regulator growth at 4.81% CAGR through 2030.

Which end-use sector shows the strongest growth outlook?

Energy transition projects encompassing green-hydrogen and fuel-cell integration are set to post a 5.08% CAGR, outpacing other industries through 2030.

What is a key supply-chain challenge facing manufacturers?

Volatile nickel and copper prices tighten margins for stainless and brass regulators, prompting design optimization and material substitution efforts.

Page last updated on: