Industrial Dust Collectors Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 9.67 Billion |

| Market Size (2031) | USD 12.29 Billion |

| Growth Rate (2026 - 2031) | 4.91% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Asia-Pacific |

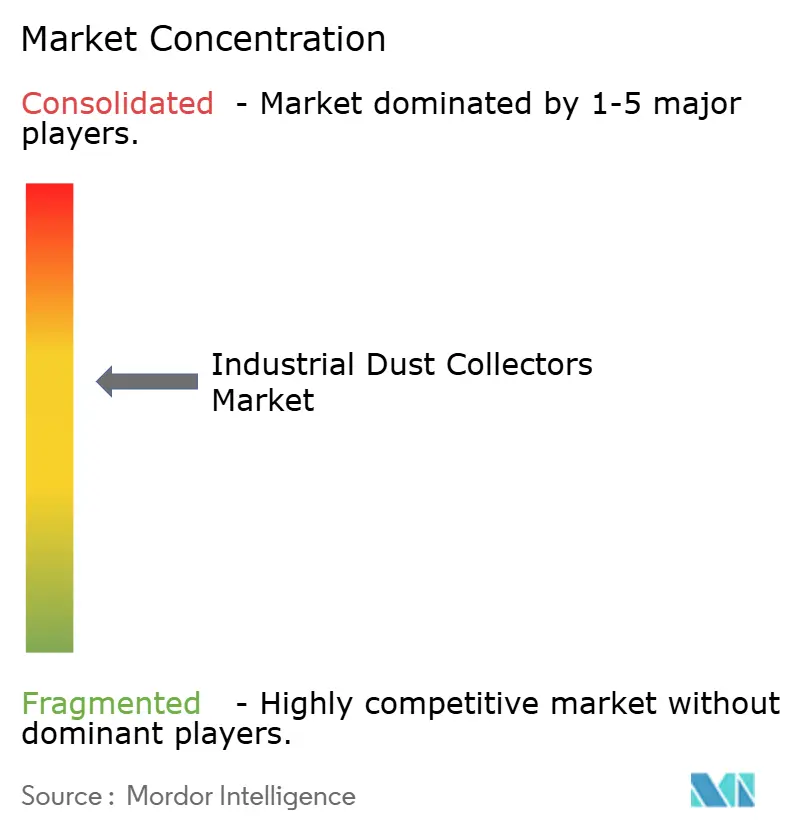

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Industrial Dust Collectors Market Analysis by Mordor Intelligence

The industrial dust collectors market size is projected to be USD 9.22 billion in 2025, USD 9.67 billion in 2026, and reach USD 12.29 billion by 2031, growing at a CAGR of 4.91% from 2026 to 2031. Capacity upgrades at lithium-ion battery and electric vehicle (EV) material plants are driving demand for explosion-proof cartridge and hybrid units. Retrofit programs at aging cement and steel mills in North America and Europe are extending equipment lifecycles by 15-20 years. Edge analytics platforms, which optimize pulse intervals, are reducing downtime costs by up to USD 18,000 per unit annually, supporting the adoption of continuous-pulse cleaning. Competitive intensity is increasing as full-line suppliers integrate Internet of Things (IoT) monitoring, aftermarket services, and filter-media replenishment into single contracts. Procurement cycles are diverging: greenfield gigafactories are prioritizing modular, skid-mounted systems with High-Efficiency Particulate Air (HEPA) H13 filtration, while brownfield heavy-industry assets are focusing on incremental retrofits to align with tight maintenance schedules.

Key Report Takeaways

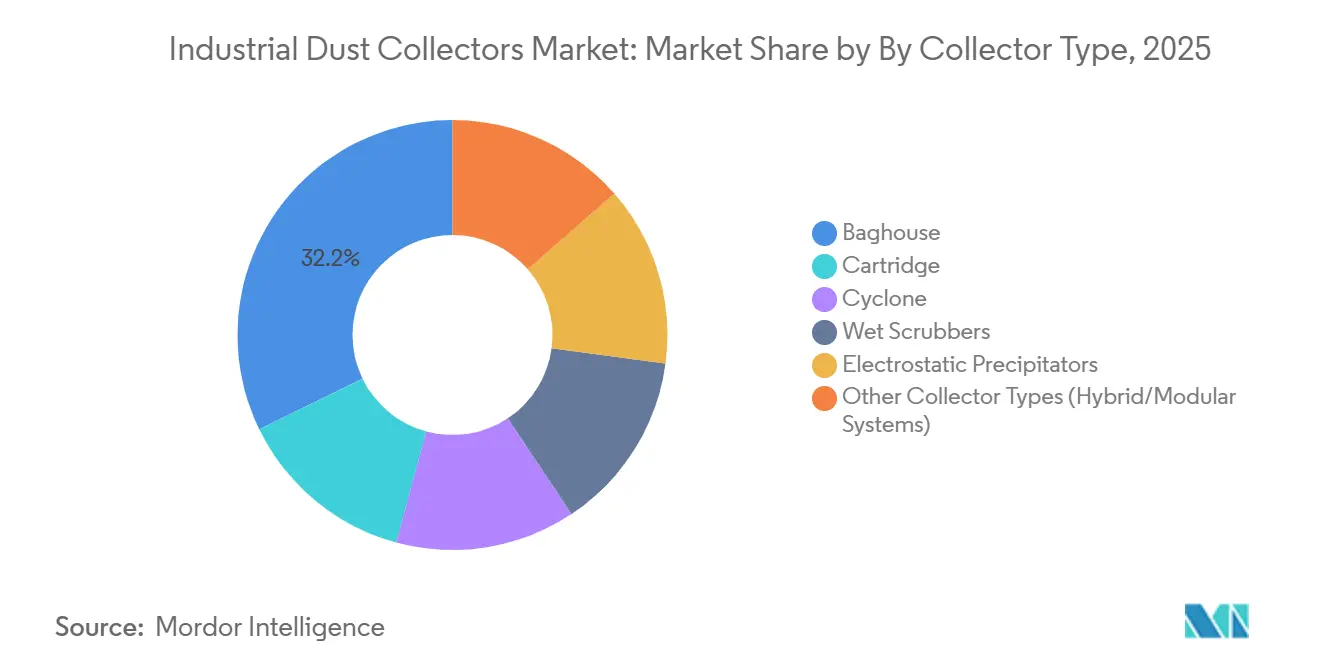

- By collector type, Baghouse accounted for 32.21% of the industrial dust collectors market share in 2025, and Other collector types are projected to register the fastest 5.58% CAGR through 2031.

- By filter-cleaning mechanism, Continuous-Pulse led with 52.23% of the industrial dust collectors market size in 2025, while the same segment is also expected to deliver the top 5.67% CAGR through 2031.

- By mobility, Stationary installations held 71.57% share of the industrial dust collectors market size in 2025, and Portables are expanding at a 5.82% CAGR to 2031.

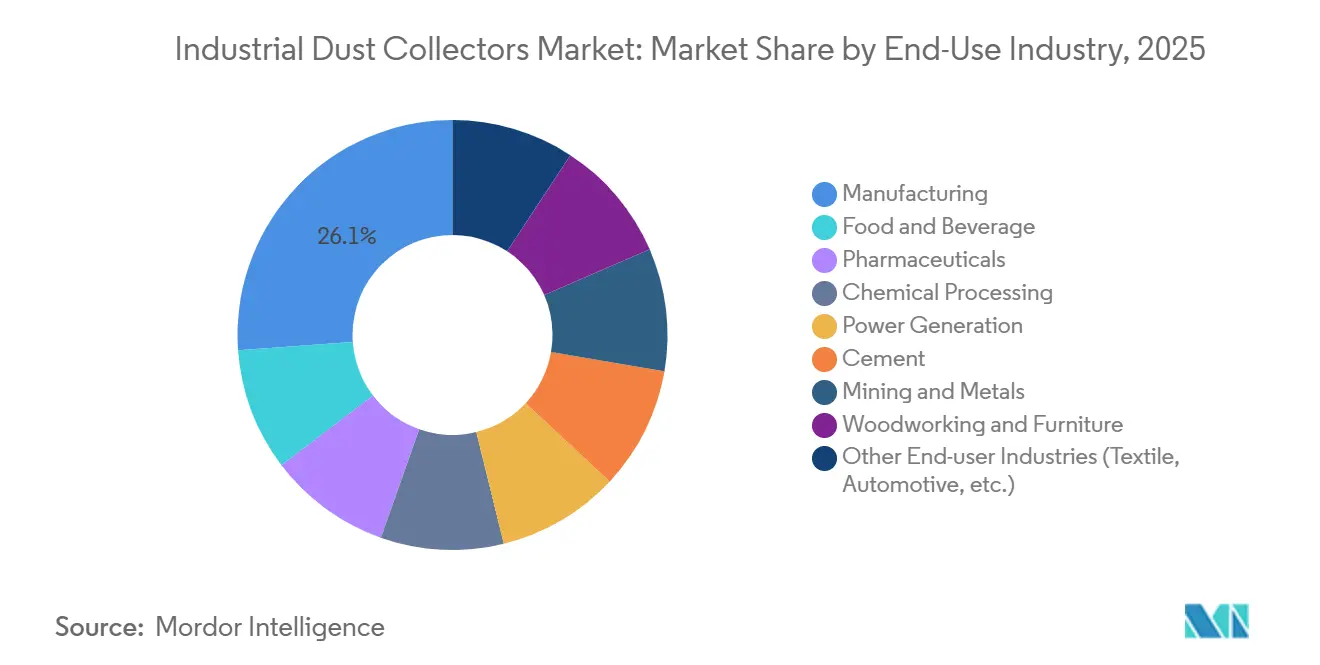

- By end-use industry, Manufacturing captured 26.11% of the industrial dust collectors market share in 2025; Other end-user industries are on track for the strongest 5.91% CAGR through 2031.

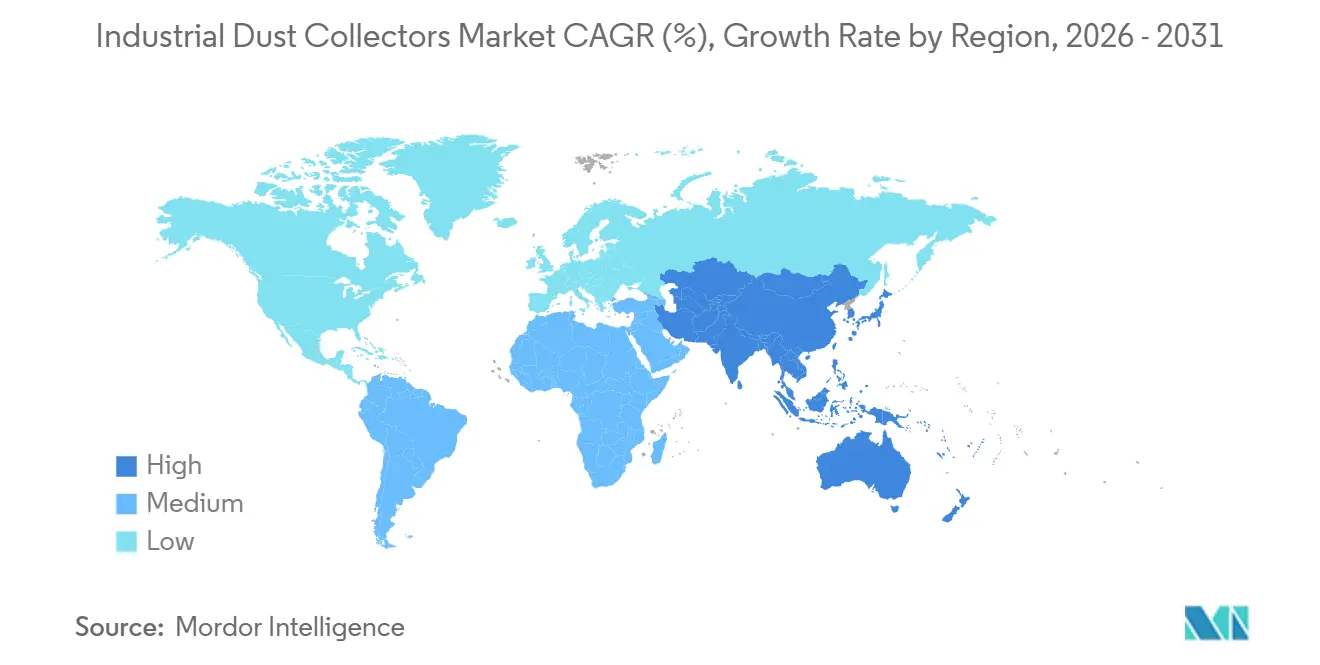

- By geography, Asia-Pacific dominated with 46.34% revenue share in 2025 and continues as the fastest region at a 5.54% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Industrial Dust Collectors Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid industrialization in the Asia-Pacific and Africa | +1.2% | APAC core, Sub-Saharan Africa | Medium term (2–4 years) |

| Expansion of dust-intensive battery and EV-material plants | +1.4% | North America, Europe, East Asia | Short term (≤ 2 years) |

| Retrofit demand from aging cement and steel assets | +0.9% | North America, Europe | Long term (≥ 4 years) |

| Carbon-neutral collector designs unlocking EU subsidies | +0.6% | EU-27, EFTA, Nordics | Medium term (2–4 years) |

| Edge-analytics-enabled predictive-maintenance savings | +0.8% | North America, Western Europe | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rapid Industrialization in Asia-Pacific and Africa

India has set a manufacturing output target of USD 1 trillion by 2030, with a projected growth rate of 12.5% CAGR. ASEAN factories are expected to grow by 5.4% in 2024 and 4.8% in 2025, driven by demand in cement, steel, and chemical sectors requiring high-capacity baghouse and electrostatic-precipitator systems.[1]Press Information Bureau, “India Manufacturing Target USD 1 Trillion by 2030,” pib.gov.in China's industrial output, estimated at USD 5.3 trillion in 2024, is sustaining retrofit projects across coal-fired power plants and non-ferrous smelters. In Vietnam, USD 36.6 billion in 2024 Foreign Direct Investment (FDI) directed toward electronics and automotive facilities is increasing demand for cleanroom-grade cartridge collectors. Sub-Saharan Africa's cement sector presents growth opportunities; however, infrastructure limitations currently restrict developments to tier-one projects supported by multilateral funding.

Expansion of Dust-Intensive Battery and EV-Material Plants

In 2024, a Quebec battery-material plant received a custom baghouse from Macrotek, designed with spark-detection interlocks[2]Macrotek Inc., “Battery-Plant Baghouse,” macrotek.com. Meanwhile, Donaldson's Torit PowerCore battery module achieves 99.99% efficiency on sub-micron particles, operating at a differential pressure of under 4 in.W.C. and reducing fan energy consumption by 20%. As Chilean lithium refineries expand towards U.S. gigafactories, there is a preference for modular, skid-mounted units that enable phased commissioning. Stringent fire-safety codes increase engineering costs but ensure compliance with safety standards for explosion-proof hybrids. The production of lithium-ion cathodes and anodes introduces combustible metal-dust hazards, requiring explosion-proof collectors equipped with High-Efficiency Particulate Air (HEPA) H13/H14 filtration and static-dissipative linings.

Retrofit Demand from Aging Cement and Steel Assets

In 2025, Tenaris allocated USD 85 million to replace legacy filters with a pulse-jet baghouse at its Pennsylvania mill. This upgrade reduced particulate emissions by 40% and extended maintenance intervals threefold. The U.S. EPA's 2024 revision of opacity limits has accelerated similar retrofits for mills built before 2000. Europe’s Industrial Emissions Directive mandates high-efficiency baghouses for kilns emitting over 50 mg/m³ of total dust, driving phased media upgrades instead of full unit replacements. Vendors are offering sensor-based kits, such as Emerson’s Dust Collector Monitoring, which extend filter life by one year and deliver annual savings of USD 18,000.

Carbon-Neutral Collector Designs Unlocking European Union Subsidies

In 2024, Filtrabit secured a EUR 4 million (USD 4.59 million) loan from the Finnish Climate Fund to commercialize a heat-recovery baghouse that reduces facility heating loads by 15%. In Germany, the Federal Office for Economic Affairs and Export Control (BAFA) reimburses up to 40% of capital costs for energy collectors that exceed baseline energy performance by 30%. Nordic cement plants have adopted ultrasonic cleaning technology, which eliminates the use of compressed air and generates annual savings of USD 5,000-8,000. Subsidy-driven demand increases have resulted in 12- to 16-week lead times for polytetrafluoroethylene (PTFE) filters and explosion-isolation valves, compressing supplier margins as buyers negotiate volume discounts.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Skilled-labor shortage for installation and service | -0.7% | North America, Western Europe | Medium term (2–4 years) |

| Slow adoption in micro-SME fabrication clusters | -0.5% | India, Indonesia, Vietnam, LATAM | Long term (≥ 4 years) |

| Dust-less power-tool integration reduces demand | -0.3% | North America, Europe, and emerging APAC | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Skilled-Labor Shortage for Installation and Service

Apprenticeships lasting 2 to 3 years are essential for tasks like high-voltage wiring, fabric tensioning, and classifying explosion hazards. A shortage of installers leads to project delays of 4 to 8 weeks, hindering aftermarket growth as operators defer media changes. In response, vendors offer factory-acceptance testing and pre-commissioning services, yet they take on performance risks, resulting in reduced profit margins.

Slow Adoption in Micro-SME Fabrication Clusters

Entry-level collectors, priced between USD 5,000 and 15,000, pose a significant challenge for cash-strapped workshops. Inconsistent enforcement, coupled with fines often falling below USD 1,000, undermines compliance efforts. While options like leasing, pay-per-use, and state-backed loans exist, they're still in their infancy, forcing SMEs to rely on self-funding. The absence of third-party certification muddies product differentiation, resulting in mis-specification and pushing market penetration back by 5-7 years.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Collector Type: Hybrid Systems Gain as Battery Plants Demand Explosion-Proof Modularity

Baghouse controlled 32.21% revenue in 2025, reflecting its dominance in cement, steel, and power generation. The industrial dust collectors market size for hybrid and modular platforms is projected to expand at 5.58% CAGR, capitalizing on battery gigafactory demand for skid-mounted, explosion-proof packages. Mitsubishi Power’s PTFE Hybrid Bag Filter marries electrostatic pre-charging with fabric media to achieve 99.9% efficiency while trimming pressure drop 25%. NFPA 660 harmonizes combustible-dust criteria, cutting engineering costs and accelerating permitting.

Hybrid adoption cannibalizes cyclone and wet-scrubber share in processes with fine or sticky dust. Vendors that can deliver rapid-install modules with integrated spark detection win bids at lithium processing, cathode precursor, and graphite-anode lines. Upstream in cement, fabric upgrades to PPS or P84 bags avert full replacement, sustaining aftermarket revenue even as new-build demand migrates to EV materials.

By Filter-Cleaning Mechanism: Continuous-Pulse Dominance Reflects IoT-Driven Optimization

Continuous-pulse systems captured 52.23% of 2025 revenue and will expand at 5.67% CAGR. Real-time differential-pressure sensors adjust pulse sequencing, slashing compressed-air use 30% and extending media life 25%. On-demand pulse solutions serve intermittent processes such as batch pharma blending, while sonic cleaning attracts Nordic cement plants with high power tariffs. AI-based predictive platforms underpin continuous-pulse dominance by monetizing data through SaaS.

IoT bundling differentiates offerings: vendors provide cyber-secure gateways, multi-protocol support, and cloud dashboards. As continuous-pulse becomes baseline, differentiation tilts to software sophistication and value-added service contracts. The industrial dust collectors market share for on-demand and sonic segments narrows but remains relevant in specialized duty cycles.

By Mobility: Portable Units Surge in Pharmaceutical and Welding Applications

In 2025, stationary units accounted for a 71.57% market share. However, portable units are projected to grow at a 5.82% compound annual growth rate (CAGR), driven by retrofits in pharmaceutical cleanrooms and the adoption of mobile welding fume extraction systems. Products such as 3M’s Xtract, RoboVent’s VentBoss, and Diversitech’s FRED offer airflow rates ranging from 200 to 1,800 cubic feet per minute (CFM), featuring high-efficiency particulate air (HEPA) H13 filtration and wireless differential pressure (DP) monitoring. Portable units are priced 20-30% higher than stationary units, but the elimination of fixed ductwork and the ability for rapid redeployment provide operational advantages.

Compliance with the U.S. Food and Drug Administration (FDA) Annex 1, which requires continuous particulate monitoring in Grade A/B rooms, is driving contract manufacturers to adopt movable units with integrated sensors. Weld-fume hoods with articulated arms and magnetic mounts can be positioned within 12 inches of the arc, capturing 95% of fumes without obstructing visibility. The expansion of semiconductor fabrication facilities and electric vehicle (EV) battery production lines in Japan and South Korea is increasing the demand for portable units, despite considerations related to energy efficiency.

By End-Use Industry: Textile and Automotive Aggregation Masks Diverse Growth Drivers

In 2025, manufacturing, including metal fabrication, machinery assembly, and electronics, contributed 26.11% of total revenue. The textiles, automotive, and specialty groups are projected to grow at a compound annual growth rate (CAGR) of 5.91%, driven by varying factors. For example, Bangladeshi mills are upgrading cyclones to comply with European Union (EU) fiber content regulations, while automotive module lines are implementing explosion-proof cartridge collectors to manage lithium and graphite dust.

Food processors are adopting stainless-steel sanitary designs with tool-free access to meet Hazard Analysis and Critical Control Points (HACCP) and Food Safety Modernization Act (FSMA) standards. Pharmaceutical facilities are ensuring compliance with International Organization for Standardization (ISO) 14644 cleanroom standards and using High-Efficiency Particulate Air (HEPA) H14 filters for final filtration. Chemical processors are utilizing polyphenylene sulfide (PPS) or polyimide (P84) bags to handle 260 °C streams and corrosive dusts. Woodworking operations, adhering to National Fire Protection Association (NFPA) 664 guidelines, are installing explosion-isolation valves for operations exceeding 1,000 pounds of dust per day. These varied application requirements diversify supplier portfolios while creating distinct technology opportunities.

Geography Analysis

In 2025, the Asia-Pacific region accounted for 46.34% of the revenue share, with a growth rate of 5.54% CAGR. China's enforcement of stack limits, ranging from 10 to 30 mg/m³, has driven baghouse retrofits in kilns and boilers. India's Clean Air Programme, targeting a 40% reduction in particulate matter (PM) by 2026, is increasing demand for collectors in industrial corridors. Vietnam's electronics FDI and Japan's battery-cell production expansions are driving the need for portable, HEPA-grade units. Additionally, cement expansion projects in the ASEAN region are supporting demand for high-capacity baghouses.

North America has strengthened its position, supported by the U.S. EPA's tightening of opacity regulations. Tenaris’s retrofit in Pennsylvania reflects a broader trend of mills established before 2000 upgrading to meet stricter NESHAP regulations. In Canada, mines are utilizing edge analytics to optimize pulse cleaning processes. Aerospace hubs in Mexico are adopting portable fume extractors following OSHA's 2024 reduction of hexavalent chromium permissible exposure limits (PELs). Skilled labor shortages are delaying installations but are also driving demand for turnkey contracting solutions.

Europe is leveraging EU carbon-neutral subsidies under the Industrial Emissions Directive, promoting ultrasonic and heat-recovery designs. Filtrabit’s loan in Finland highlights the role of grants in adoption. In Germany, BAFA supports high-efficiency units with 40% capital expenditure coverage. Nordic countries are favoring compressor-free sonic cleaning due to electricity price advantages. Russia faces challenges as sanctions limit access to advanced media, impacting performance improvements. In South America and the Middle East & Africa, growth opportunities are available in Brazil's bagasse sector, Saudi Arabia's petrochemicals, and South Africa's silica retrofits.

Competitive Landscape

The Industrial Dust Collectors market is moderately concentrated. The top five vendors controlled 35-40% revenue in 2025. Consolidation is accelerating. PARKER HANNIFIN CORP’s USD 9.25 billion Filtration Group deal in November 2025 adds baghouse and cartridge competencies and USD 220 million synergy potential. CECO Environmental’s USD 2.2 billion Thermon acquisition in February 2026 merges heat-tracing with environmental controls, targeting USD 40 million cost savings.

Mid-tier specialists such as Camfil and Nederman Holding AB lack scale for global aftermarket networks and therefore focus on ultra-high-temperature or nano-particle niches. Disruptors leverage SaaS: IAC’s Smart Plant sensors and Emerson’s Dust Collector Monitoring capture recurring revenue from data-driven maintenance. NFPA 660 harmonization lowers entry barriers for software-rich modular suppliers sourcing hardware from contract manufacturers. White-space lies in micro-SME clusters without financing, and in gigafactory explosion-proof hybrids.

Industrial Dust Collectors Industry Leaders

Donaldson Company, Inc.

Nederman Holding AB

Camfil

PARKER HANNIFIN CORP

CECO ENVIRONMENTAL

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: CECO ENVIRONMENTAL completed its USD 2.2 billion acquisition of Thermon Group, integrating heat-tracing technology to enhance its dust collectors portfolio and strengthen its industrial air quality management capabilities.

- November 2025: PARKER HANNIFIN CORP completed its USD 9.25 billion acquisition of Filtration Group, targeting USD 220 million in annual benefits, which could influence the dust collectors through advanced filtration technologies.

Global Industrial Dust Collectors Market Report Scope

Industrial dust collectors are air pollution control systems designed to enhance indoor air quality and ensure safety. They filter hazardous dust, fumes, and particulates from industrial processes. Using filters such as baghouses or cartridges, or separation technologies like cyclones, these systems capture airborne contaminants. This supports worker health, ensures compliance with environmental regulations, and improves machinery performance.

The Industrial Dust Collectors market is segmented by collector type, filter-cleaning mechanism, mobility, end-use industry, and geography. By collector type, the market is segmented into baghouse, cartridge, cyclone, wet scrubbers, electrostatic precipitators, and other collector types (hybrid/modular systems). By filter-cleaning mechanism type, the market is segmented into continuous-pulse, on-demand pulse, and sonic/ultrasonic. By mobility type, the market is segmented into stationary and Portable. By end-use industry type, the market is segmented into manufacturing, food and beverage, pharmaceuticals, chemical processing, power generation, cement, mining and metals, woodworking and furniture, and other end-user industries (textile, automotive, etc.). The report also covers the market size and forecasts for silver iodide in 17 countries across major regions. The market sizes and forecasts are provided in terms of value (USD).

| Baghouse |

| Cartridge |

| Cyclone |

| Wet Scrubbers |

| Electrostatic Precipitators |

| Other Collector Types (Hybrid/Modular Systems) |

| Continuous-Pulse |

| On-Demand Pulse |

| Sonic/Ultrasonic |

| Stationary |

| Portable |

| Manufacturing |

| Food and Beverage |

| Pharmaceuticals |

| Chemical Processing |

| Power Generation |

| Cement |

| Mining and Metals |

| Woodworking and Furniture |

| Other End-user Industries (Textile, Automotive, etc.) |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| NORDIC Countries | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle-East and Africa |

| By Collector Type | Baghouse | |

| Cartridge | ||

| Cyclone | ||

| Wet Scrubbers | ||

| Electrostatic Precipitators | ||

| Other Collector Types (Hybrid/Modular Systems) | ||

| By Filter-Cleaning Mechanism | Continuous-Pulse | |

| On-Demand Pulse | ||

| Sonic/Ultrasonic | ||

| By Mobility | Stationary | |

| Portable | ||

| By End-Use Industry | Manufacturing | |

| Food and Beverage | ||

| Pharmaceuticals | ||

| Chemical Processing | ||

| Power Generation | ||

| Cement | ||

| Mining and Metals | ||

| Woodworking and Furniture | ||

| Other End-user Industries (Textile, Automotive, etc.) | ||

| By Geography | Asia-Pacific | China |

| Japan | ||

| India | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| NORDIC Countries | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

How fast will Asia-Pacific spending on dust collectors grow?

Asia-Pacific revenue is projected to advance at a 5.54% CAGR between 2026 and 2031, supported by capacity additions in China, India, and ASEAN.

Which collector type is growing fastest?

Hybrid and modular systems are on track for a 5.58% CAGR through 2031 as battery gigafactories demand explosion-proof, skid-mounted equipment.

What drives the adoption of continuous-pulse cleaning?

Edge-analytics sensors cut compressed-air use 30% and extend filter life 25%, making continuous-pulse the default choice for new installations.

Why are portable units gaining popularity?

Pharmaceutical cleanrooms and welding stations favor portable collectors with HEPA H13 filters and wireless monitoring for rapid redeployment without ductwork.

What is the current market size of Industrial Dust Collectors Market?

The industrial dust collectors market size is projected to be USD 9.22 billion in 2025, USD 9.67 billion in 2026, and reach USD 12.29 billion by 2031, growing at a CAGR of 4.91% from 2026 to 2031.

Page last updated on: