Dust Control Suppression Chemicals Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 5.48 Billion |

| Market Size (2031) | USD 6.79 Billion |

| Growth Rate (2026 - 2031) | 4.38% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Dust Control Suppression Chemicals Market Analysis by Mordor Intelligence

The Dust Control Suppression Chemicals Market size was valued at USD 5.25 billion in 2025 and estimated to grow from USD 5.48 billion in 2026 to reach USD 6.79 billion by 2031, at a CAGR of 4.38% during the forecast period (2026-2031). The growth trajectory reflects a deliberate shift away from water-only spraying toward chemical binders, which halve application frequency and reduce on-site water use. Demand is further buoyed by tightening PM2.5 and PM10 thresholds in North America, the European Union, and China, which are compelling operators to adopt formulations with verifiable capture efficacy. Meanwhile, IoT-enabled dosing systems are starting to optimize spray volumes in real time, trimming chemical waste by nearly one-fifth without compromising compliance. Over the next five years, price volatility for calcium- and magnesium-chloride feedstocks will remain a headline risk, yet the total cost-of-ownership advantage of binders over water-only protocols is expected to keep adoption on an upward slope, especially in arid mining basins.

Key Report Takeaways

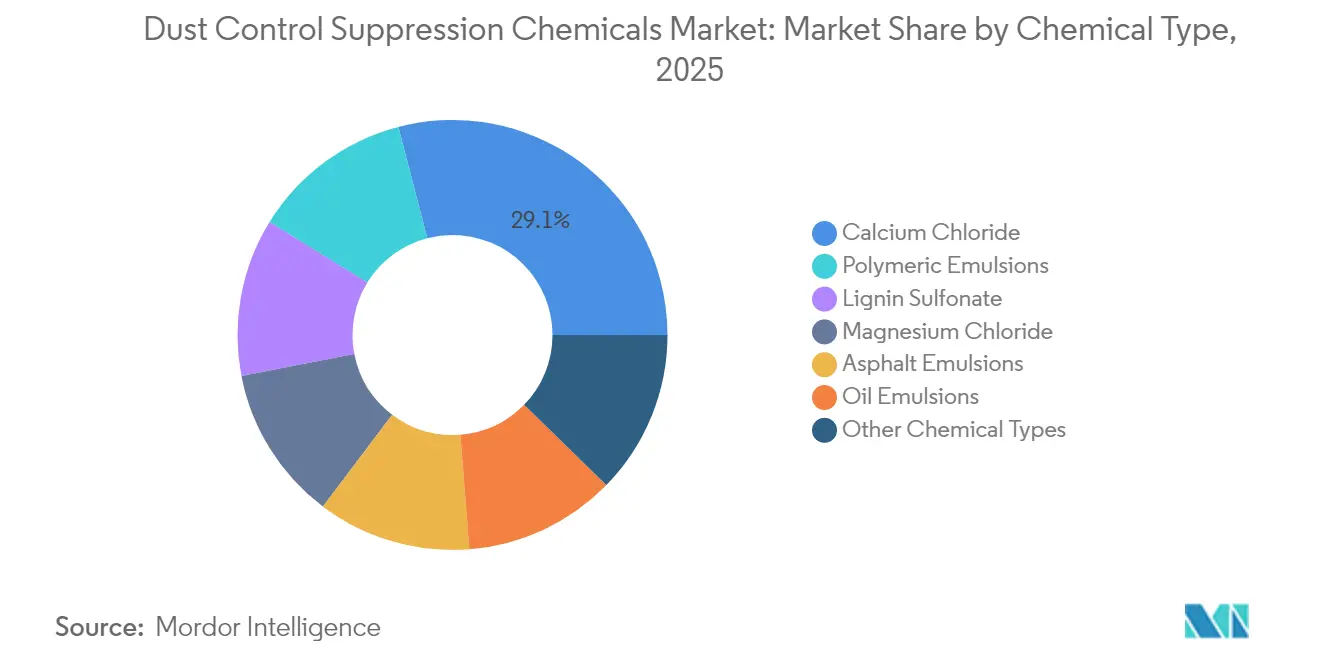

- By chemical type, calcium chloride led with 29.05% of 2025 revenue and is set to advance at a 4.78% CAGR through 2031.

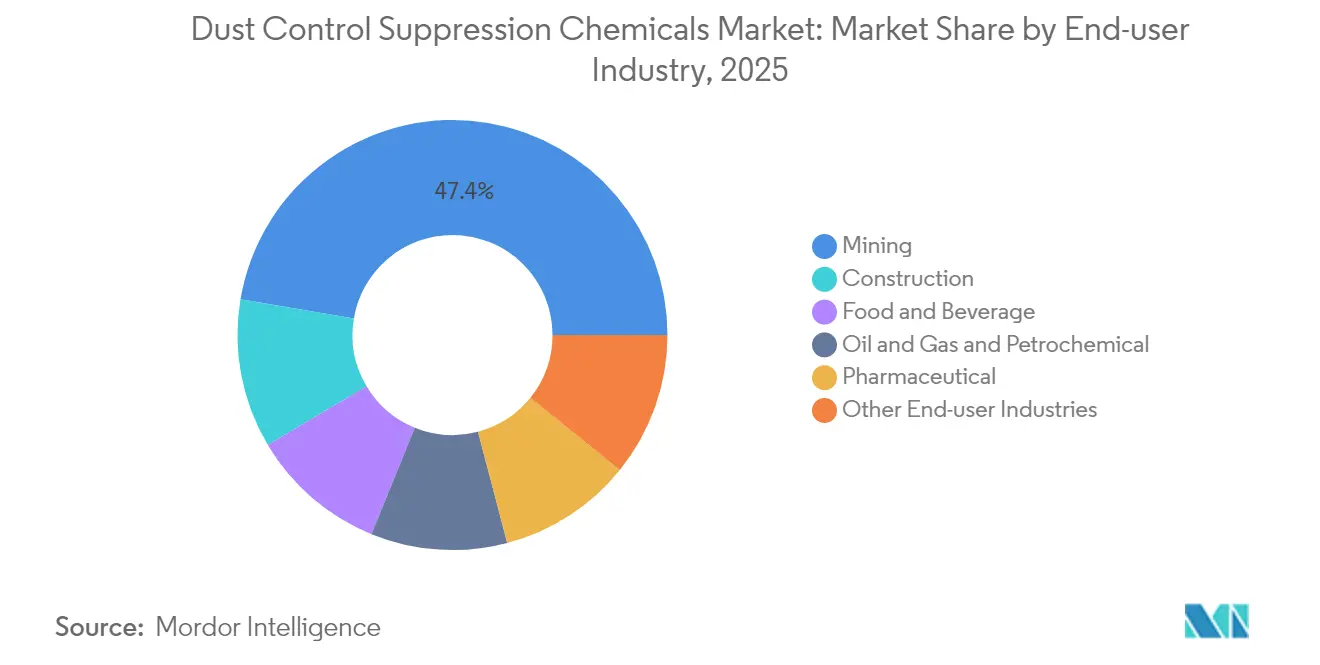

- By end-user industry, mining accounted for 47.35% of the 2025 value, while construction is forecast to expand at a 4.95% CAGR to 2031.

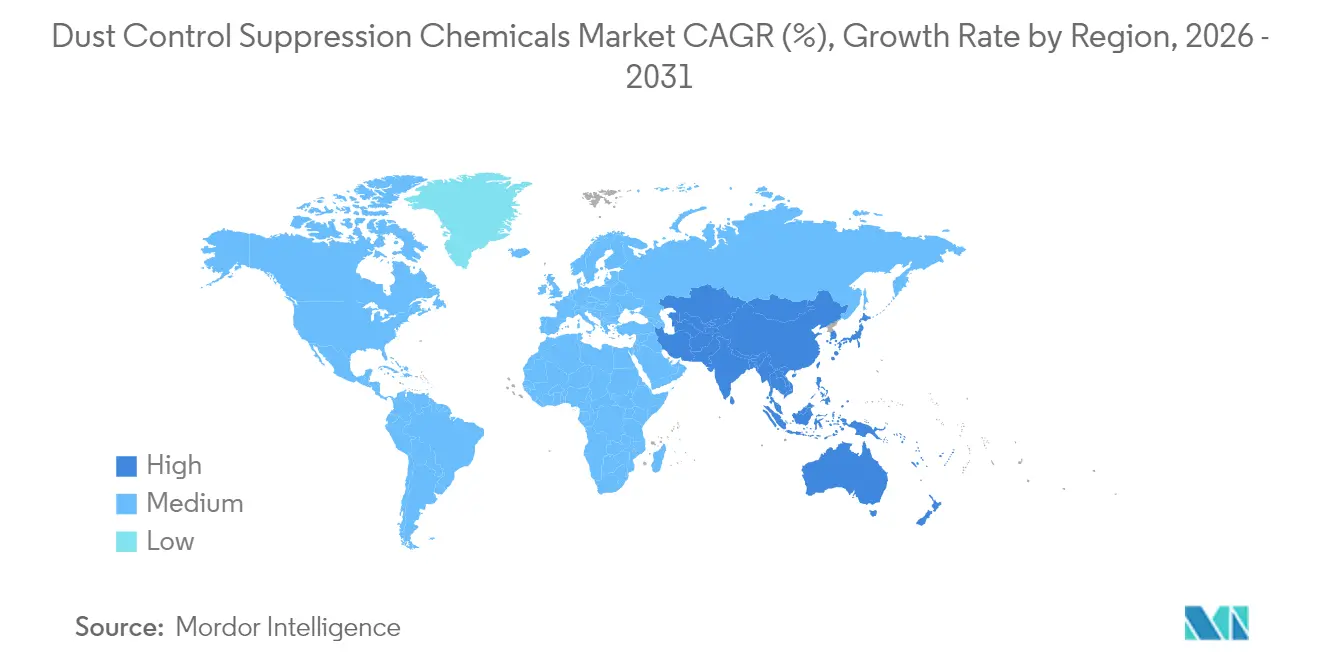

- By geography, Asia-Pacific commanded 47.10% of global revenue in 2025 and is projected to register a 4.62% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Dust Control Suppression Chemicals Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising infrastructure and mining activity | +1.3% | APAC core, spillover to Middle East | Medium term (2-4 years) |

| Stricter global PM10/PM2.5 emission standards | +1.1% | Global, early enforcement in North America and EU | Short term (≤ 2 years) |

| Shift from water-only spraying to binders | +0.9% | Worldwide, acute in water-scarce regions | Medium term (2-4 years) |

| Adoption of IoT-enabled dosing systems | +0.6% | North America, Australia, select APAC mines | Long term (≥ 4 years) |

| Carbon-credit revenue at mines | +0.4% | Global, concentrated in voluntary carbon markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Infrastructure and Mining Activity in Asia-Pacific

China, India, and Indonesia are ramping up their production of coal, nickel, and lignite. This surge in output is driving a consistent demand for road-dust suppressants, especially at pit faces, stockpiles, and along haul-road networks. India has approved new coal projects, aiming to increase capacity in the coming years. To secure state permits, these projects necessitate year-round dust mitigation[1]Ministry of Coal (India), “Coal Mining Projects and Production Targets,” coal.nic.in. Indonesia has inaugurated new nickel laterite mines, enforcing chemical suppression on access roads exceeding a certain length. Vietnam's ambitious North-South Expressway project mandates dust-control measures for earthworks situated near residential zones. Given this landscape, there's a pronounced preference for cost-effective calcium-chloride solutions on temporary haul roads, while permanent infrastructures gravitate towards lignin sulfonate and polymer emulsions.

Stricter Global PM10/PM2.5 Emission Standards

In February 2024, the U.S. Environmental Protection Agency updated the annual PM2.5 NAAQS. This move requires non-attainment zones in California, Arizona, and Utah to show measurable reductions by 2026. Meanwhile, the European Union's Directive 2024/2881 sets stricter limits, spurring faster polymer adoption in Germany and Poland[2]EUR-Lex, “Directive (EU) 2024/2881 on Ambient Air Quality and Cleaner Air for Europe,” eur-lex.europa.eu . In 2024, China broadened its county-level Blue-Sky audits, mandating large construction sites to provide real-time PM10 data. These regulations are steering buyers towards formulations certified by ISO 17025 test data, moving away from anecdotal field proofs alone.

Shift from Water-Only Spraying to Chemical Binders

In arid regions, rising water costs are disrupting established pricing models. In 2024, water charges at Pilbara mine sites made calcium chloride-based binders economically attractive. In Chile's Atacama Desert, blends of magnesium chloride have increased suppression intervals. This extension has significantly reduced haul-truck cycles and diesel consumption. Research published in peer-reviewed journals indicates that polymer-based suppressants can achieve a dust reduction. They do so using only a fraction of the water volume compared to standard spraying. This notable difference in performance is swaying procurement choices towards a focus on lifecycle economics.

Adoption of IoT-Enabled Smart Misting and Dosing Systems

Australian mines began fielding weather-linked dosing units in 2024. GRT’s Smart Dosing platform combines wind, humidity, and traffic inputs to modulate nozzle pressure, cutting chemical consumption while sustaining PM10 compliance. Pilbara pilots, linking sensor data to haul-truck density, achieve significant savings at each site. While a small portion of global mines currently utilize sensor-driven suppression, turnkey leasing models are easing adoption hurdles and yielding tangible benefits in terms of compliance.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Price volatility of chloride salts and lignin feedstock | -0.7% | Global, acute in North America for chlorides and lignin | Short term (≤2 years) |

| Corrosion concerns limiting chloride use on capital equipment | -0.5% | Europe, North America, select APAC infrastructure projects | Medium term (2-4 years) |

| Fragmented regulations slowing product standardisation | -0.4% | Global, acute in emerging markets (Southeast Asia, Africa, Latin America) | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Price Volatility of Chloride Salts and Lignin Feedstock

In 2024, spot prices for calcium chloride in North America fluctuated due to tightening brine output from the Great Salt Lake. Meanwhile, environmental quotas in China's Qinghai province capped magnesium chloride supplies in 2024, restricting export growth. A decline in North American kraft-pulp production led to reduced availability of lignin sulfonate, causing spot prices to surge. Formulators lacking long-term contracts faced margin compression, leading them to either absorb the costs or raise prices, which in turn delayed procurements for municipal road programs. Additionally, turnkey leasing models are not only lowering adoption barriers but also yielding a tangible compliance dividend.

Corrosion Concerns Limiting Chloride Use

European infrastructure projects are increasingly favoring polymer emulsions, as calcium and magnesium chlorides elevate maintenance costs on steel components over a decade. In a 2024 study from an Australian coal mine, haul-truck frame inspections occurred more frequently on chloride-treated roads compared to polymer-treated surfaces. While new corrosion-resistant coatings come with a higher price tag per truck, many smaller operators find this premium hard to accept.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Chemical Type: Chlorides Dominate, Polymers Gain Share

Calcium chloride captured 29.05% of the 2025 revenue and is forecasted to grow at 4.78% through 2031, maintaining its leadership position within the Dust Control Suppression Chemicals Market share. Magnesium chloride, though smaller, retains a foothold in cold-climate mines where performance is required below -15 °C. Lignin sulfonate appeals to buyers near sensitive watersheds because it binds fine particles without chloride leaching. Polymeric emulsions—mainly acrylate and vinyl acetate copolymers—are gaining traction as long-life infrastructure projects prioritize lifetime maintenance over unit price. Asphalt and oil emulsions fill niche roles, and bio-based formulations, although accounting for a small portion of the market value, are drawing research and development dollars as LEED-compliant alternatives.

Longer-term demand dynamics hinge on feedstock costs, corrosion considerations, and regulatory acceptance. Chloride solutions will maintain their edge in terms of cost per treated square meter, particularly where water scarcity is acute and equipment turnover is rapid. Polymers and lignin will continue to displace chlorides in Europe and selected Asian megaprojects where asset longevity and stormwater compliance are paramount.

By End-User Industry: Mining Leads, Construction Accelerates

Mining consumed 47.35% of 2025 demand as open-pit coal, iron-ore, and base-metal operations applied suppressants across haul-road networks exceeding 200 kilometers in some Australian and Brazilian sites. Construction will be the fastest-growing sector at a 4.95% CAGR, driven by India’s National Infrastructure Pipeline and Southeast Asian urbanization mandates.

Food and beverage plants use binders in grain-handling zones to mitigate combustible dust, while LNG and petrochemical operators prefer non-chloride chemistries during plant construction to avoid corrosion. Pharmaceutical facilities employ FDA-compliant polymers in cleanroom contexts. Ports, rail yards, and waste-management centers round out demand, their growth tied to stricter opacity rules at material-transfer points.

Geography Analysis

The Asia-Pacific region anchored 47.10% of the global value in 2025 and is projected to grow at 4.62% through 2031. Coal mine expansions in Indonesia, a massive infrastructure pipeline in India, and county-level Blue Sky audits in China largely fuel this growth. The market size for Dust Control Suppression Chemicals in the Asia-Pacific is anticipated to witness significant growth. With approvals from India’s Ministry of Coal and a significant push in nickel production in Indonesia, the region is enjoying a sustained boost. Furthermore, countries such as Vietnam and Malaysia are implementing dust-control regulations on new highways and airports, thereby expanding the market's reach.

North America captured a substantial portion of the 2024 market revenue. In response to the EPA’s stringent PM2.5 standards, mines and contractors in non-compliant areas are increasingly adopting chemical suppression alongside continuous monitoring. The primary consumers include projects centered around copper, lithium, and oil sands. Notably, IoT-integrated spray bars are becoming standard on new haul-truck fleets, reducing annual chemical demand without compromising compliance.

Europe, contributing significantly to the 2024 revenue, shows a distinct preference for polymer emulsions and lignin sulfonate. In Germany and the Nordic region, chloride-free solutions are mandated for highway and bridge upgrades to safeguard reinforced concrete from corrosion. While Poland and the Czech Republic favor cost-effective calcium chloride for mine haul roads, they're also adopting polymer blends to minimize maintenance costs. Additionally, Turkey’s initiative for earthquake recovery is accelerating the use of polymers in urban projects.

South America, along with the Middle East and Africa, jointly represented a notable share of the 2024 revenue. In Chile’s Atacama region, miners are utilizing high-concentration magnesium chloride to maximize application intervals amidst stringent water limitations. Brazil’s iron-ore industry is adapting to new PM10 standards near indigenous lands, integrating real-time sensors for compliance. Meanwhile, both Saudi Arabia and the UAE are incorporating dust-control stipulations in mining and construction permits, highlighting a regulatory alignment towards PM compliance in these emerging markets.

Competitive Landscape

The Dust Control Suppression Chemicals Market is moderately consolidated. Their advantages lie in vertical integration, ISO-accredited testing, and bundled technical services. Regional toll manufacturers in China and India are disrupting the calcium-chloride segment with price discounts, squeezing incumbent margins and prompting a strategic pivot toward value-added offerings such as real-time dosing analytics. White-space growth is emerging in bio-based suppressants derived from fenugreek gum and soy protein. Pilot deployments in Chinese coal mines have recorded reductions in PM10, but still face cost hurdles. Early adopters include high-visibility infrastructure programs seeking LEED points and mines pursuing voluntary carbon credits.

Dust Control Suppression Chemicals Industry Leaders

Borregaard AS

Cargill, Incorporated

Midwest Industrial Supply Inc.

Soilworks, LLC

Ecolab Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2024: Borregaard committed NOK 490 million to expand its Sarpsborg lignin-biopolymer capacity by up to 10% by 2027, with incremental output expected from late 2026. The investment specifically targets increasing capacity for lignin-based biopolymers, which are the key ingredient in their dust suppression product, Dustex.

- April 2024: Merichem Technologies acquired Chemical Products Industries, bolstering its sulfur-removal chemistry portfolio and widening its reach into industrial cleaning applications.

Global Dust Control Suppression Chemicals Market Report Scope

Dust control suppression chemicals work by binding dust particles together or making them heavier, preventing them from becoming airborne.

The dust control suppression chemicals market is segmented by chemical type, end-user industry, and geography. By chemical type, the market is segmented into lignin sulfonate, calcium chloride, magnesium chloride, asphalt emulsions, oil emulsions, polymeric emulsions, and other chemical types. By end-user industry, the market is segmented into mining, construction, food and beverage, oil, gas, and petrochemical, pharmaceutical, and other end-user industries. The report also covers the market sizes and forecasts for the dust control systems and suppression chemicals market in 28 countries across major regions. For each segment, market sizing and forecasting have been conducted based on revenue (USD).

| Lignin Sulfonate |

| Calcium Chloride |

| Magnesium Chloride |

| Asphalt Emulsions |

| Oil Emulsions |

| Polymeric Emulsions |

| Other Chemical Types |

| Mining |

| Construction |

| Food and Beverage |

| Oil and Gas and Petrochemical |

| Pharmaceutical |

| Other End-user Industries |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Indonesia | |

| Thailand | |

| Vietnam | |

| Malaysia | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Nordic Countries | |

| Turkey | |

| Russia | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| United Arab Emirates | |

| Qatar | |

| South Africa | |

| Nigeria | |

| Egypt | |

| Rest of Middle-East and Africa |

| By Chemical Type | Lignin Sulfonate | |

| Calcium Chloride | ||

| Magnesium Chloride | ||

| Asphalt Emulsions | ||

| Oil Emulsions | ||

| Polymeric Emulsions | ||

| Other Chemical Types | ||

| By End-user Industry | Mining | |

| Construction | ||

| Food and Beverage | ||

| Oil and Gas and Petrochemical | ||

| Pharmaceutical | ||

| Other End-user Industries | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| Indonesia | ||

| Thailand | ||

| Vietnam | ||

| Malaysia | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Nordic Countries | ||

| Turkey | ||

| Russia | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| Qatar | ||

| South Africa | ||

| Nigeria | ||

| Egypt | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

What is the current value of the Dust Control Suppression Chemicals Market?

The market is valued at USD 5.48 billion in 2026 and is projected to reach USD 6.79 billion by 2031.

How fast is Asia-Pacific demand expected to grow?

Asia-Pacific demand is forecast to rise at a 4.62% CAGR through 2031.

Which chemical type leads global revenue?

Calcium chloride leads with 29.05% of 2025 revenue.

Why are polymer emulsions gaining traction in Europe?

They avoid the corrosion issues linked to chloride salts and help meet the EU’s stricter PM2.5 limits.

What technology is trimming chemical waste at mine sites?

IoT-enabled dosing systems that adjust spray rates based on real-time weather and traffic data.

Page last updated on: