Industrial Drums Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 15.41 Billion |

| Market Size (2031) | USD 20.06 Billion |

| Growth Rate (2026 - 2031) | 5.42% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

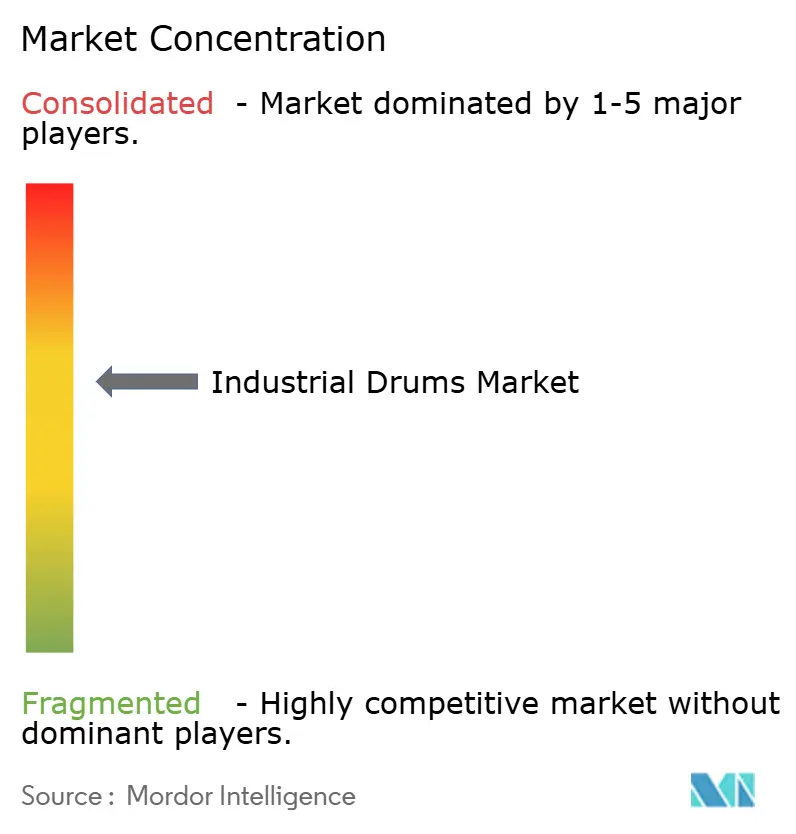

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Industrial Drums Market Analysis by Mordor Intelligence

The industrial drums market size is expected to grow from USD 14.62 billion in 2025 to USD 15.41 billion in 2026 and is forecast to reach USD 20.06 billion by 2031 at 5.42% CAGR over 2026-2031. Steady chemical output, rising petrochemical investments, and widening food‐grade export flows anchor demand. Regulatory momentum toward reusable packaging, demonstrated by Cummins’ RFID‐enabled returnable program, reinforces the shift away from single-use bulk bags. Composite drums win share as weight-sensitive shippers pursue corrosion-resistant options, while RFID adoption spreads across hazardous-materials fleets to improve traceability. Asia-Pacific drives volume on the back of China’s cracker additions and India’s 12% annual chemical growth target through 2030, whereas North America and Europe prioritize premium, compliance-led formats. Consolidation such as Berry Global’s 2025 merger with Amcor adds scale advantages that squeeze smaller rivals. [1]Berry Global, “Press Release on Amcor Merger Completion,” berryglobal.com

Key Report Takeaways

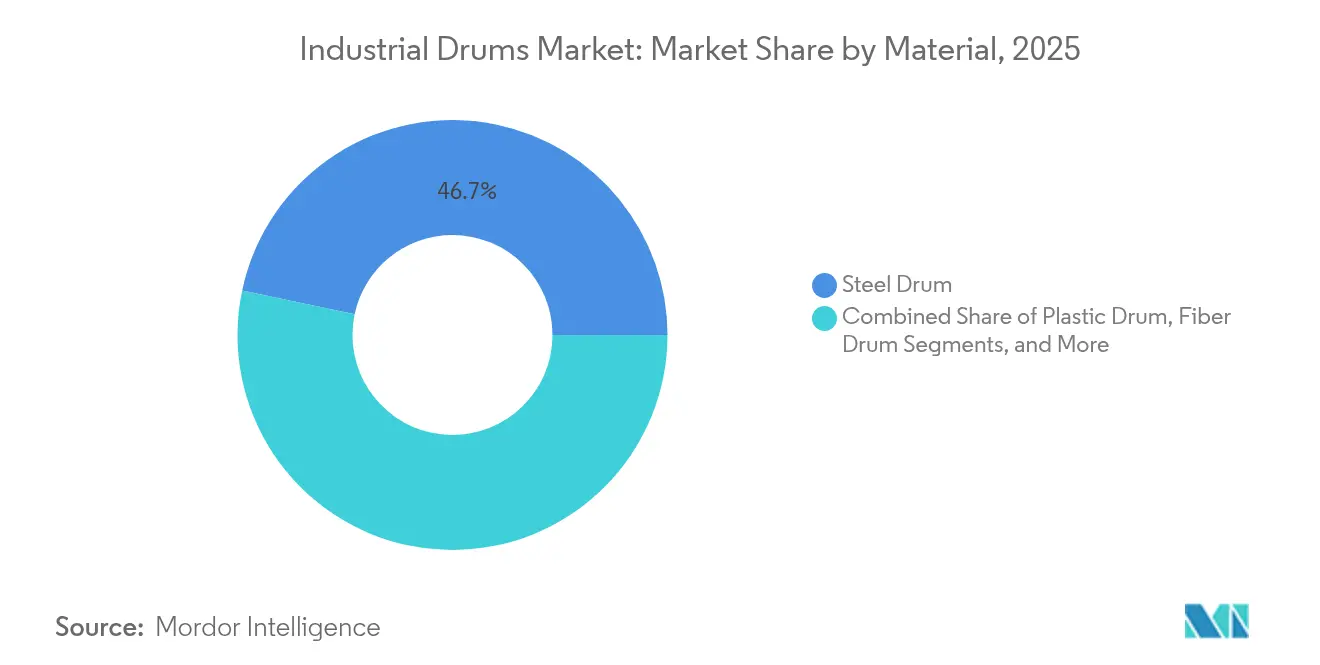

- By material, steel accounted for 46.68% of the industrial drums market share in 2025, while composite drums recorded the fastest 7.21% CAGR to 2031.

- By capacity, the 60 - 100 gallon range held 35.21% of the industrial drums market size in 2025, while above-100-gallon formats hold the fastest 6.08% CAGR to 2031.

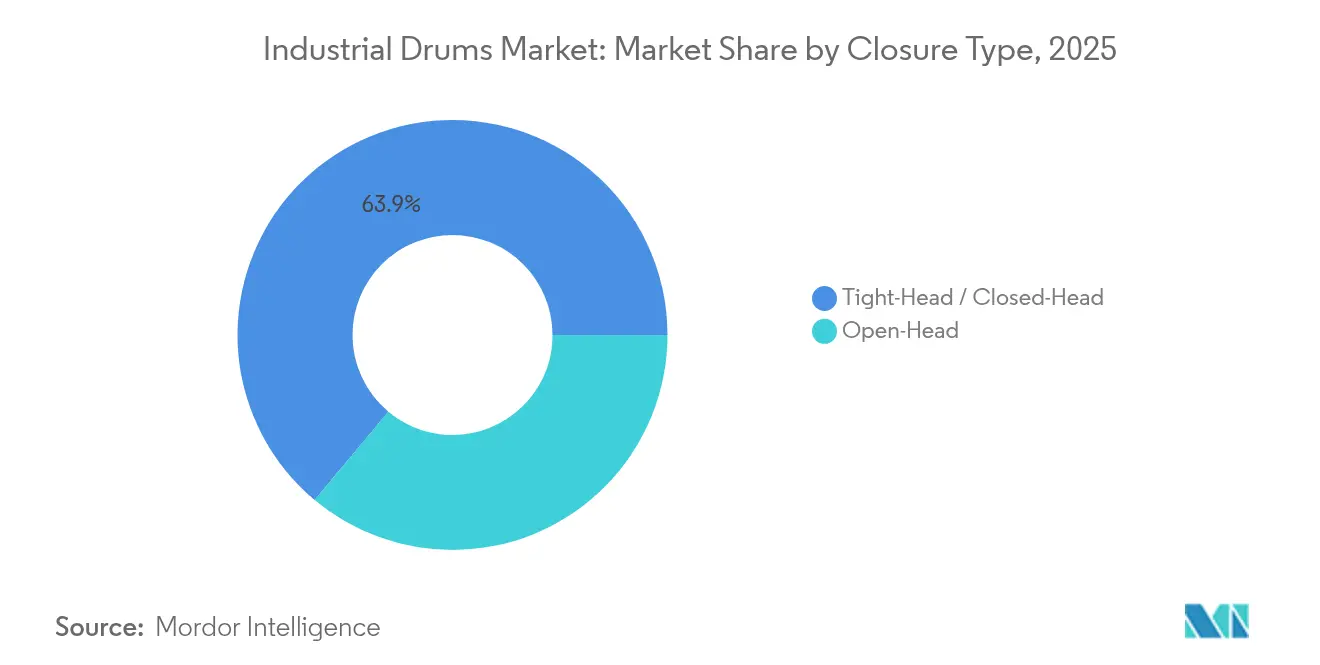

- By closure type, tight-head designs led with 63.92% revenue share in 2025, and Open-Head designs hold the fastest 6.47% CAGR to 2031.

- By end-user, chemicals and fertilizers retained 32.11% share of the industrial drums market size in 2025, while pharmaceuticals recorded the fastest 6.85% CAGR to 2031.

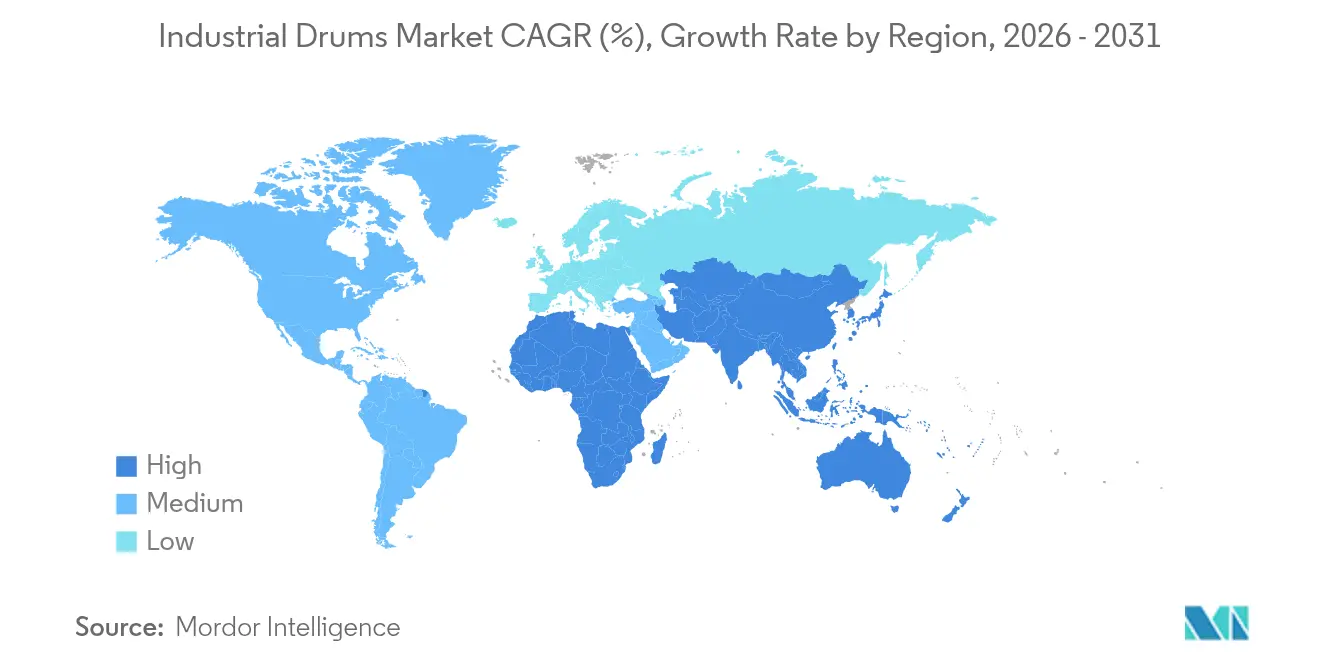

- By geography, Asia-Pacific captured 39.55% of the industrial drums market share in 2025 and is projected to expand at a 7.65% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Industrial Drums Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growth in chemical and petrochemical output | +1.2% | Global with Asia-Pacific leadership | Medium term (2-4 years) |

| Expansion of food-grade export logistics | +0.8% | North America and Europe spreading to Asia | Long term (≥ 4 years) |

| Strengthening supply-chain resiliency needs | +0.9% | Global with North America focus | Short term (≤ 2 years) |

| Regulatory phase-out of single-use bulk bags | +0.7% | Europe core, ripple to North America | Medium term (2-4 years) |

| Circular-economy leasing and reconditioning | +0.5% | Europe and North America, pilots in Asia | Long term (≥ 4 years) |

| RFID-enabled drum tracking for haz-mat compliance | +0.4% | Global, led by North America | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Growth in Chemical and Petrochemical Output

Robust specialty-chemical builds in China, cracker expansions in the Middle East, and mergers among Japanese majors collectively increase drum throughput requirements. The American Chemistry Council notes sustained resilience in U.S. chemical production despite logistics bottlenecks, while India is targeting 12% compound growth, which keeps drum demand firmly on an upward path. Larger integrated complexes process greater batch sizes, pushing shippers toward 100-plus gallon formats and composite linings that withstand aggressive intermediates. SysKem Chemie ships Class 8 caprylic acid exclusively in coated drums that meet United Nations test codes, illustrating the higher specification trend.

Expansion of Food-Grade Export Logistics

Diversification of ingredient sourcing has lengthened supply chains for sweeteners, plant proteins, and fruit concentrates. CDF Corporation launched USDA-compliant liners in February 2025, showing suppliers’ response to stricter contamination thresholds. Harmonized documentation under the Codex Alimentarius enables multi-regional certification, supporting scale economies for manufacturers producing food-grade drums in bulk. Premium organic exporters have begun to pay price differentials for drums embedded with tamper-evident seals and QR-code lineage data, enhancing provenance claims in destination markets.

Strengthening Supply-Chain Resiliency Needs

After the 2024 congestion cycle, buyers now insist on local drum stocks and dual sourcing. Cummins’ RFID deployment cut replacement purchases by 18% in its first year and signaled a wider move toward viewing drums as capital assets rather than disposable consumables. Tag providers such as HID Global supply chemically durable UHF labels that feed live geolocation to ERP dashboards. [2]HID Global, “Container Tracking Solutions,” hidglobal.com Locking in multi-year steel contracts has become a defensive tactic, given MEPS International’s USD 900 per-ton projection for April 2025 and the tariff uncertainty outlined in Ryerson’s metals outlook.

Regulatory Phase-Out of Single-Use Bulk Bags

The incoming EU Packaging and Packaging Waste Regulation mandates minimum reuse rates, causing some agrochemical exporters to replace poly-woven FIBCs with reconditioned tight-head drums. U.S. DOT code 1A1 for non-removable-head steel units remains the global benchmark for hazardous liquids. [3]Pipeline and Hazardous Materials Safety Administration, “§ 178.502 Identification Codes for Packagings,” ecfr.gov North Coast Container conducts annual drop and hydrostatic tests that most start-ups find cost-prohibitive, further cementing incumbents’ positions. Early adopters in California align drums with Proposition 65 and PFAS restrictions, signaling deeper integration of chemical and packaging compliance regimes.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Raw-material price volatility | -0.8% | Global with pronounced North America impact | Short term (≤ 2 years) |

| Environmental compliance cost for disposal | -0.5% | Europe and North America, expanding to Asia | Medium term (2-4 years) |

| Cannibalization by IBCs and flexitanks | -0.6% | Global, centered on bulk-liquid segments | Medium term (2-4 years) |

| On-site micro-blending cutting drum demand | -0.4% | North America and Europe clusters | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Raw-Material Price Volatility

Steel and resin swings squeeze margins as drum makers struggle to synchronize contracts with customer price lists. Ryerson’s 2025 forecast flags potential anti-dumping duties on Asian hot-rolled coil, adding another layer of unpredictability. Balmer Lawrie is piloting 0.5 mm-wall drums that allow 80 units per TEU, four more than traditional gauges, to offset rising coil costs; at INR 23.39 billion (USD 280.8 million) 2024 sales, the savings are material.

Cannibalization by IBCs and Flexitanks

Single-use flexitanks priced at USD 170 with 24,000 L capacity reduce per-liter freight by up to 35%, tempting edible-oil shippers to switch. Meanwhile, composite IBC producers integrate pallet bases and tracking chips, lowering warehouse labor. Nevertheless, drums retain strongholds in UN-regulated corrosive and flammable classes where multilayer liners or reinforced hoops are mandatory.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material: Steel Dominance Adjusts to Composite Uptake

Steel captured the lion’s share at 46.68% because refinery and agrochemical players favor its mechanical strength and straightforward reconditioning loops. At the same time, composite drums are on a 7.21% trajectory as buyers weigh freight savings against initial premiums. Recent audits at Indian ports show that lightweight steel accounted for 37% of outbound haz-chem shipments, underscoring cost reductions from thinner gauges. The industrial drums market benefits from global scrap incentives that make low-alloy steel a closed-loop asset, whereas virgin HDPE resin tracks propylene prices more closely.

Plastic and fiber variants address niche solute compatibility or weight constraints. Although fiber units lack UN credentials for liquids, they now incorporate moisture-resistant liners that extend shelf life for dry food powders. Composite models combine polymer barriers with steel ribs, targeting formulators of moisture-sensitive adhesive ingredients. Their rise illustrates how the industrial drums market evolves through hybridization rather than a binary material switch.

By Capacity: Mid-Range Preference Shifts toward High-Volume SKUs

Sixty-to-one-hundred-gallon drums align with forklift clearance and remain the workhorse at 35.21% share. However, fully automated chemical clusters prefer 110-gallon drums that support fewer lifts per ton processed. Through 2031, above-100-gallon formats hold the fastest 6.08% expansion rate. Camco Chemical’s USD 3 million line allows dual fill heads for 30 and 110 gallon SKUs, underlining buyers’ preference for multi-volume flexibility. The industrial drums market size for capacities beyond 100 gallons is projected to touch USD 4.55 billion by 2031, reflecting wider adoption of palletless robotic handling cells.

Smaller drums serve specialty flavors, pharma actives, and lab reagents where lot segregation trumps bulk economics. Yet their share erodes as tank-to-fill micro-blending units shrink on-site intermediate inventories. Overall, capacity choice mirrors a trade-off between ergonomic safety, freight utilization, and regulatory caps on allowable mass per package in airborne routes.

By Closure Type: Tight-Head Security versus Open-Head Flexibility

Tight-heads, or closed-heads, generated nearly two-thirds of 2025 sales because their welded tops prevent seepage of flammables in transit. They dominate ISO-tank feeder legs and refinery loop returns. Open-heads, expanding at 6.47%, cater to viscous pastes and dry blends that require full-aperture filling. Pharmaceutical auditors insist on removable lids to validate swab cleanliness between batches, intensifying demand in contract drug manufacturing.

The industrial drums market is witnessing hybrid lug-ring designs that aim to marry tamper evidence with removable access, yet regulatory listing under DOT code 1A2 still involves months of stack, drop, and hydrostatic testing, a hurdle few new entrants overcome.

By End-User: Chemical Leadership Elevated by Pharma Momentum

Chemicals and fertilizers command 32.11% owing to massive commodity volumes. Specialty makers layer in antistatic linings to comply with IEC 60079 zones, illustrating customization depth. Pharmaceutical growth at 6.85% stems from FDA cleaning validation letters that push contract fillers toward UN-certified, easily sanitized drums. The industrial drums industry captures premium margins here because documentation and extractables analysis raise barriers to cheaper substitutes.

Food and beverage shippers demand FDA - compliant resins and traceable lot coding, while paints and coatings specify solvent-resistant phenolic linings. Lubricant packers continue to rely on open-head steel for grease and tight-head plastic for DEF fluids, underscoring how the industrial drums market segments by chemical compatibility and viscosity profile rather than simple end-use labels.

Geography Analysis

Asia-Pacific contributed 39.55% revenue in 2025, propelled by Chinese cracker projects and India’s chemicals roadmap. Balmer Lawrie leveraged eight plants to secure national contracts for agrochemical exporters and logged INR 23.39 billion (USD 280.8 million) turnover. Regional governments offer land rebates for packaging clusters adjacent to refinery corridors, shortening delivery lead times and reducing dent damage.

North America benefits from shale-based feedstock and maintains stringent DOT oversight that drives demand for high-specification steel drums. Cummins’ returnable system illustrates how U.S. OEMs internalize packaging for circularity gains. Europe emphasizes circular economy compliance under the Packaging and Packaging Waste Regulation and has seen pilot leasing pools triple since 2023, mostly for food and personal-care ingredients. South America and the Middle East and Africa remain smaller but high-growth nodes. Brazilian biodiesel exporters pivot to composite drums to mitigate soy-oil oxidation, whereas Gulf petrochemical hubs procure thick-gauge steel variants to withstand extreme ambient temperatures. Cross-regional freight arbitrage also stimulates backhaul drum reconditioning networks, reinforcing global linkages within the industrial drums market.

Competitive Landscape

Competition is moderate, with regional strongholds. The top five producers control roughly 42% of global sales, giving the market a concentration score of 6. Balmer Lawrie dominates Indian demand through end-to-end offerings, from steel rolling to in-house epoxy lining. Mauser and Greif leverage global footprints to service multinationals under single-invoice models. Berry Global’s April 2025 Amcor integration unlocks USD 650 million in synergistic savings, directly impacting bid pricing.

Technology is the new battleground. HID Global partners with drum fabricators to embed NFC tags during hoop welding, a shift that differentiates commodity steel shells via data services. Mid-tier firms invest in robotically welded chimes to reduce labor spend, while start-ups explore bio-based resins to meet emerging PFAS and VOC curbs. Flexitank suppliers such as Shandong Blue Whale blur category lines by courting bulk edible-oil traffic formerly handled by drum fleets.

Service models mature alongside hardware. Reconditioners bundle cleaning, relining, and end-of-life shredding to satisfy ISO 14001 audits. Subscription-based leasing, now 9% of North American steel-drum circulation, offers predictable OPEX versus CAPEX, resonating with CFOs chasing asset-light balance sheets. Such moves underscore how the industrial drums market continues to expand beyond mere container fabrication into lifecycle management ecosystems.

Industrial Drums Industry Leaders

Greif, Inc.

Mauser Packaging Solutions Holding Company

SCHUTZ GmbH & Co. KGaA

Time Technoplast Ltd.

Balmer Lawrie & Co. Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: University of Oxford unveiled PFAS destruction chemistry with fluoride recovery, relevant to drum waste streams.

- February 2025: CDF Corporation introduced FDA-compliant drum liners for beverages.

- January 2025: Lubrizol enhanced dispersant capacity in North America to meet lubricant additive demand.

- January 2025: GEWA Music secured Gretsch Drums manufacturing rights, assuming the South Carolina plant.

Global Industrial Drums Market Report Scope

Industrial drums are primarily used to store and transport materials for the delivery of mass freight. Based on the different materials, industrial drums are often separated into three main categories: steel drums, plastic drums, and fiber drums. The study tracks revenue accrued from the sales of the drums offered by various vendors operating in the market with manufacturing capability. The study does not consider service providers that offer third-party supplier services.

The global industrial drums market is segmented by product type (steel drum, plastic drum, fiber drum), end-user industry (food and beverages, chemicals and fertilizers, pharmaceuticals, petroleum and lubricants, other end-user industries), and geography (North America [United States, Canada], Europe [United Kingdom, Germany, France, Italy, Rest of Europe], Asia-Pacific [China, India, Japan, Australia and New Zealand, Rest of Asia-Pacific], Latin America [Brazil, Mexico, Rest of Latin America], Middle East and Africa [United Arab Emirates, Saudi Arabia, South Africa, Egypt, Rest of Middle East and Africa]). The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

| Steel Drum |

| Plastic Drum |

| Fiber Drum |

| Composite/Hybrid Drum |

| Up to 30 Gallons |

| 30 – 60 Gallons |

| 60 – 100 Gallons |

| Above 100 Gallons |

| Tight-Head / Closed-Head |

| Open-Head |

| Chemicals and Fertilizers |

| Petroleum and Lubricants |

| Food and Beverage |

| Pharmaceuticals |

| Paints, Coatings and Adhesives |

| Building and Construction |

| Other End-user Industries |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Kenya | ||

| Rest of Africa | ||

| By Material | Steel Drum | ||

| Plastic Drum | |||

| Fiber Drum | |||

| Composite/Hybrid Drum | |||

| By Capacity | Up to 30 Gallons | ||

| 30 – 60 Gallons | |||

| 60 – 100 Gallons | |||

| Above 100 Gallons | |||

| By Closure Type | Tight-Head / Closed-Head | ||

| Open-Head | |||

| By End-user Industry | Chemicals and Fertilizers | ||

| Petroleum and Lubricants | |||

| Food and Beverage | |||

| Pharmaceuticals | |||

| Paints, Coatings and Adhesives | |||

| Building and Construction | |||

| Other End-user Industries | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Chile | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Kenya | |||

| Rest of Africa | |||

Key Questions Answered in the Report

How large is the industrial drums market today?

The industrial drums market size reached USD 15.41 billion in 2026 and is projected to climb to USD 20.06 billion by 2031 at a 5.42% CAGR.

Which region generates the highest demand for drums?

Asia-Pacific leads with 39.55% revenue owing to rapid chemical capacity additions and expanding export hubs.

What material type dominates global drum sales?

Steel remains dominant at 46.68% share because of its strength, recyclability, and regulatory familiarity.

Why are composite drums gaining popularity?

Composite and hybrid drums offer lighter weight and corrosion resistance, translating into freight savings and longer service life.

How are regulations affecting drum design?

EU and U.S. rules favor reusable packaging and mandate UN certification testing, steering buyers toward durable, track-and-trace steel and composite formats.

Are flexitanks threatening drum demand?

Flexitanks and IBCs gain traction in specific bulk-liquid lanes, yet drums maintain an edge for hazardous materials and closed-loop reconditioning models.

Page last updated on: