Industrial Cooking Fire Protection Systems Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

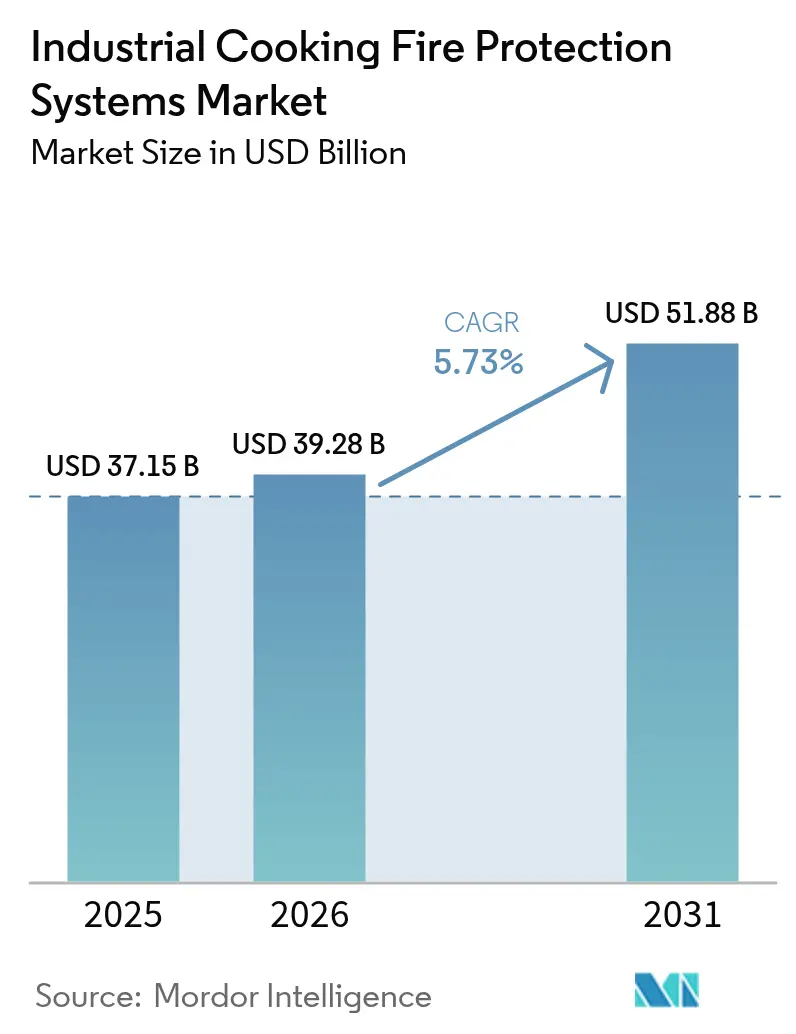

| Market Size (2026) | USD 39.28 Billion |

| Market Size (2031) | USD 51.88 Billion |

| Growth Rate (2026 - 2031) | 5.73% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Industrial Cooking Fire Protection Systems Market Analysis by Mordor Intelligence

The industrial cooking fire protection systems market size was valued at USD 37.15 billion in 2025 and estimated to grow from USD 39.28 billion in 2026 to reach USD 51.88 billion by 2031, at a CAGR of 5.73% during the forecast period (2026-2031). This expansion is rooted in the strict enforcement of NFPA 96 and UL 300, rapid roll-outs of quick-service restaurants (QSRs) and hotel kitchens, and a wave of smart detection–suppression innovations.[1]Washington State Register, “Effective Date of Rule: Immediately upon filing,” lawfilesext.leg.wa.govElevated grease-fire risks in high-temperature plant-oil frying, paired with growing insurance incentives for compliant retrofits, are compelling both new builds and legacy operations to upgrade. Wet-chemical agents continue to dominate because of proven grease-fire effectiveness, yet water-mist technologies are gaining momentum as regulators phase out PFAS-based foam.[2]Gaylord Ventilation, “Gaylord Dual Tech Nozzle Update – AFFF & PFAS,” gaylordventilation.comNorth America, backed by extensive QSR footprints and an entrenched service network, retains market leadership, while Asia-Pacific delivers the fastest growth on the back of rapid urbanization and restaurant proliferation. Suppliers that integrate IoT sensors, predictive analytics and cloud dashboards are securing premium margins by shifting value from simple compliance to operational uptime and data-driven safety.

Key Report Takeaways

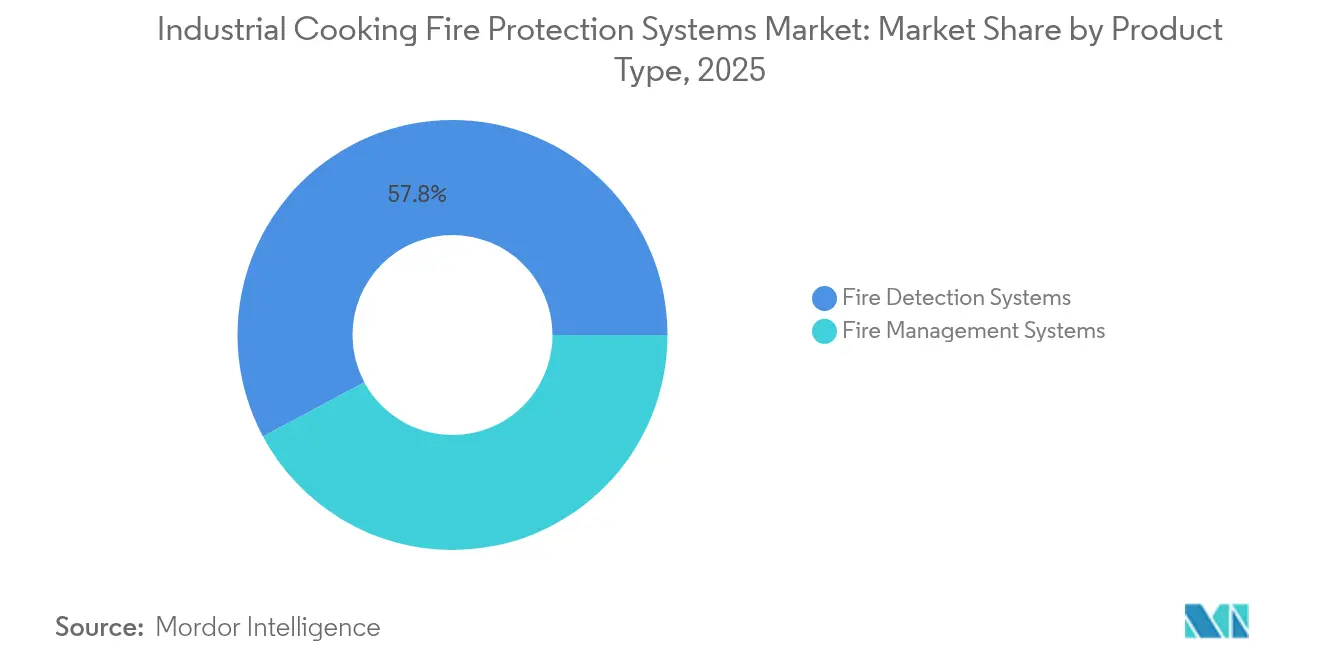

- By product type, fire detection systems led with 57.82% revenue share in 2025, whereas fire management systems are projected to post the fastest 6.05% CAGR to 2031.

- By suppression agent, wet-chemical solutions captured 61.12% of industrial cooking fire protection systems market share in 2025; water-mist systems are forecast to grow at 6.95% CAGR through 2031.

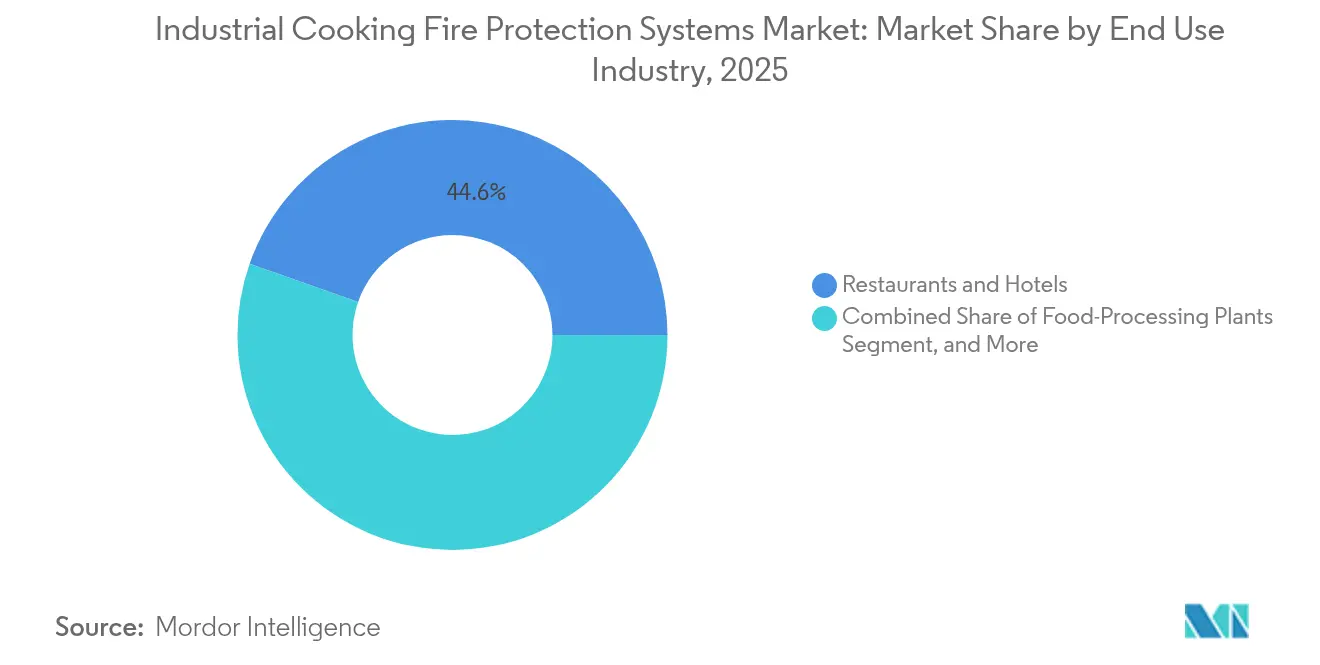

- By end-use industry, restaurants and hotels commanded 44.63% share of the industrial cooking fire protection systems market size in 2025, while food-processing plants register the highest 6.46% CAGR to 2031.

- By connectivity, wired platforms held 69.85% share in 2025, whereas wireless/cloud-connected systems are increasing at an 7.9% CAGR on stronger IoT adoption.

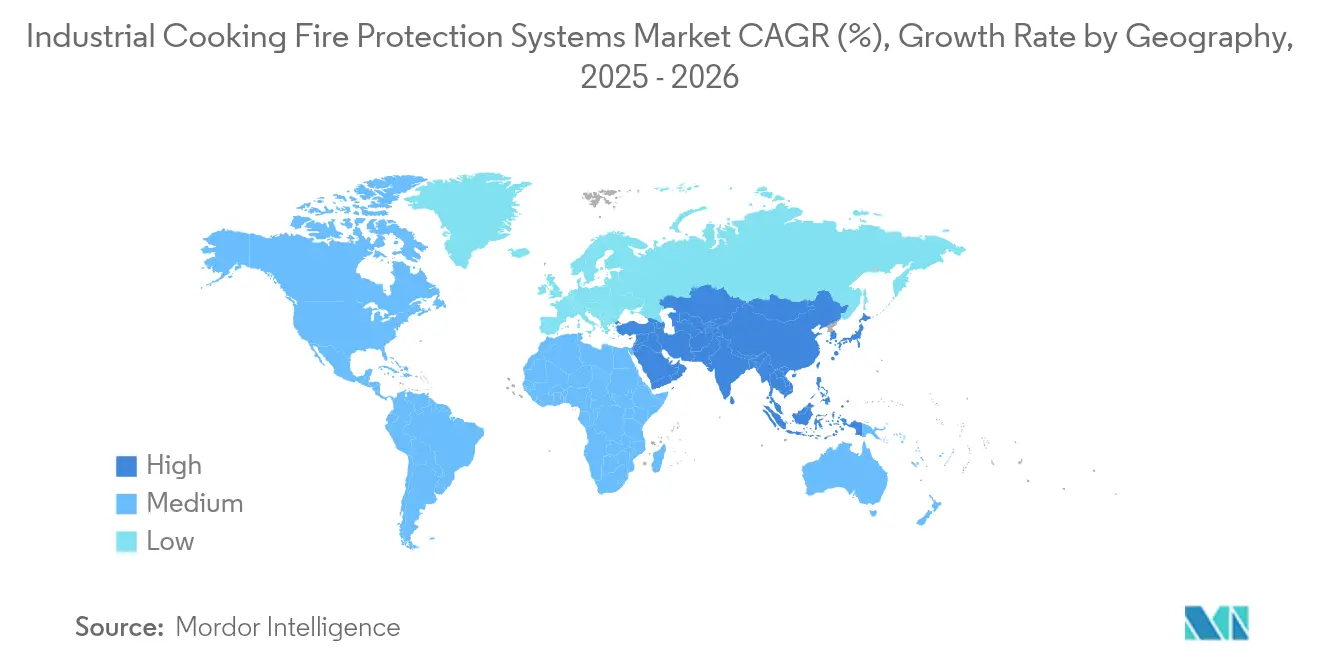

- By geography, North America dominated with 32.78% share in 2025; Asia-Pacific is advancing at 6.18% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Industrial Cooking Fire Protection Systems Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent global kitchen-safety mandates | +1.2% | Global; most stringent in North America & EU | Medium term (2-4 years) |

| Accelerated hotel and QSR build-outs | +0.8% | Asia-Pacific core; MEA spill-over | Short term (≤ 2 years) |

| Smart, IoT-enabled platforms | +1.1% | North America & EU early adopters; Asia-Pacific catching up | Long term (≥ 4 years) |

| Insurance premium rebates | +0.9% | Global with regional variation | Medium term (2-4 years) |

| ESG push for PFAS-free agents | +0.7% | EU leads; North America & Asia-Pacific scale | Long term (≥ 4 years) |

| Rising fire risk from high-temperature plant-oil frying | +0.6% | Global; concentrated in QSR & food processing | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Stringent Global Kitchen-Safety Mandates (NFPA 96, UL 300)

Reinforced enforcement of NFPA 96 duct and hood provisions and UL 300 performance tests has shifted upgrades from optional to compulsory. The International Fire Code’s Section 904.13 prescribes automatic extinguishing equipment for cooking operations, prompting full retrofits of aging grease-fire systems, particularly those predating 1998 UL 300 certification.[3]International Code Council, “904.13 Commercial cooking systems,” codes.iccsafe.orgCompliance is no longer limited to brick-and-mortar kitchens; food trucks, catering trailers and university cafeterias are now within jurisdiction, creating thousands of incremental installations. Local authorities in Washington State now require NICET-qualified technicians, raising professional barriers and ensuring correct commissioning. Insurance carriers tie policy renewals to evidence of UL-300 records, generating recurring service revenue. Combined, these factors underpin a structural uptick in demand for certified detection and suppression gear across every region.

Accelerated Hotel and QSR Build-Outs

Yum China’s operation of 12,947 restaurant units exemplifies the new-build surge that is reshaping the industrial cooking fire protection systems market.[4]Yum China Holdings, “Annual Report,” sec.gov Hotel chains recovering from pandemic lows are simultaneously renovating back-of-house kitchens, embedding fire suppression at design phase rather than as retrofit. Asia-Pacific sites often open in clusters, creating procurement waves that strain supply of UL-300-listed nozzles and valves. Global QSR brands pursue template kitchens with identical protection technologies, so a supplier that wins one master franchise can attain hundreds of repeat units. This consolidation steers deal flow toward scale-capable OEMs, marginalizing smaller regional players and accelerating the shift toward global standards.

Smart, IoT-Enabled Detection and Suppression Platforms

Artificial-intelligence algorithms paired with multi-sensor arrays raise grease-fire detection accuracy beyond 95%, cutting incident response time 72% relative to legacy thermal sensors. Connected panels stream temperature, vapor and particulate data into building-management dashboards, letting facility managers adjust airflow, reduce energy draw and pre-empt flashover. Honeywell’s AI-enabled detectors minimize nuisance trips while pushing firmware patches over the air, addressing a chronic pain-point for QSR operators. Wireless cloud linkage also furnishes proof-of-maintenance logs that insurers increasingly demand. Consequently, smart systems command 15-20% higher ASPs yet still deliver payback through downtime avoidance and insurance discounts, bolstering premium segment revenue.

Insurance Premium Rebates for Compliant Retrofits

Underwriters are refining actuarial models to recognize loss-prevention gains from modern suppression systems. Restaurants presenting documented UL-300 compliance now claim premium reductions of 5–12%, and additional credits for kitchens monitored via IoT dashboards. The savings multiply across large QSR fleets, further justifying capital spend on upgrades. Insurers are piloting tiered pricing that rewards predictive maintenance data feeds, nudging operators toward cloud-connected solutions. This financial lever transforms safety investment from cost center to profit enabler, accelerating replacement cycles in both mature and emerging markets.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High CAPEX for upgrading legacy hoods & ducts | -0.4% | Global; most acute in North America & EU | Medium term (2-4 years) |

| False-alarm downtime & nuisance discharges | -0.2% | Global; high-volume kitchens most affected | Short term (≤ 2 years) |

| PFAS phase-out disrupting agent supply | -0.3% | EU lead; North America following | Long term (≥ 4 years) |

| Shortage of UL 300-certified installers | -0.3% | North America & EU expanding to Asia-Pacific | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High CAPEX for Upgrading Legacy Hoods and Ducts

Replacing older ventilation runs to fit modern nozzle footprints can top USD 100,000 per site, a figure that excludes structural reinforcing and electrical re-routing. Many small operators defer projects, stretching compliance grace periods and stalling some retrofit opportunities. Historic inner-city properties present layout conflicts that raise installation hours and crane rental costs. These budget pressures slow conversion of entrenched yet obsolete systems in mature markets, dampening upside despite regulatory push.

False-Alarm Downtime and Nuisance Discharges

Every unintended suppression release forces full clean-down, food disposal and hours-long closure, costing high-volume QSRs thousands in lost sales. The balance between sensitivity and resilience remains delicate; aerosolized cooking vapors can still trigger cheaper photo-electric detectors. Past nuisance incidents have made some franchisees hesitant to adopt more advanced sensors, fearing reputational damage and food waste. Vendors must therefore demonstrate concrete reductions in false-alarm rates to overcome lingering skepticism.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Detection Systems Retain Lead as Suppression Accelerates

Detection systems generated the largest slice of the industrial cooking fire protection systems market at 57.82% in 2025, cementing their role as the foundational layer of kitchen safety. Integrating thermal, optical and air-sampling sensors curtails latency while reducing spray activations, maintaining uptime for foodservice operators. Simultaneously, suppression platforms are set to log a 6.05% CAGR through 2031 as regulators insist on active agent discharge and full-hood coverage. An increasingly popular integrated design folds both detection and nozzle arrays into a single control panel, curbing maintenance visits and yielding unified compliance documentation. Johnson Controls’ Ansul R-102-newly EN 17446-certified-embodies this approach, securing additional European tender win.

The convergence trend is reshaping buyer expectations: operators now benchmark quotes on life-cycle support, firmware updates and data analytics rather than equipment alone. This pull is nudging OEM roadmaps toward modular architectures that accommodate smart sensors, alternative agents and cloud APIs. As integrated kits permeate small-format kitchens and ghost kitchens, detection-only replacements will increasingly taper, pivoting revenue growth to next-generation hybrid offerings

By Suppression Agent: Water-Mist Disrupts Wet-Chemical Dominance

Wet-chemical formulas still account for 61.12% of the industrial cooking fire protection systems market share due to long-standing UL 300 testing success against vegetable-oil fires. Yet water-mist technologies are climbing at a projected 6.95% CAGR as operators seek fluorine-free solutions amid PFAS restrictions. High-pressure atomization creates micro-droplets that cool flames, displace oxygen and limit thermal radiation, delivering rapid knock-down with minimal residue. Siemens deepened its water-mist capabilities via the Danfoss Fire Safety acquisition, ensuring a PFAS-free roadmap for multinational clients.

Dry-chemical and inert-gas agents keep niche appeal where sensitive electronics or enclosed machinery demand zero water exposure. However, PH-neutral water-mist additives are narrowing performance gaps, making them viable for mixed-hazard kitchens. As environmental framing shifts procurement criteria, agent selection now extends beyond suppression metrics to sustainability audit points, reinforcing the momentum behind water-mist roll-outs.

By End-Use Industry: Food Processing Surges Past Traditional Restaurant Core

Restaurants and hotels contributed 44.63% to 2025 revenue, mirroring the historical focus of commercial safety codes. Large chains continue multi-site retrofits, but incremental restaurant growth alone will not sustain double-digit volume gains. Instead, industrial food-processing plants are set to pace the field with a 6.46% CAGR through 2031 as automation pushes fryers and ovens to 24-hour cycles and higher flash-point oils. These environments demand extended-coverage agent flows and high-capacity cylinder banks, spurring bespoke engineering contracts.

Institutional kitchens-spanning hospitals, universities and correctional facilities-add steady baseline demand, driven by stringent duty-of-care liabilities. Meanwhile, cloud-kitchen aggregators adopt space-efficient hood packages and centralized fire panels that link multiple tenant kiosks, carving out a fast-growing sub-segment. As a result, suppliers adept at scaling from single-line restaurants to 5,000 l/h industrial fryers will capture outsized wallet share.

By Connectivity: Wireless Platforms Challenge Wired Dominance

Hard-wired architectures kept 69.85% share in 2025 by virtue of decades-proven reliability and lower upfront costs. However, wireless and cloud-connected variants are tracking the highest 7.9% CAGR. Battery-backed mesh sensors slash installation downtime, especially in retrofit scenarios where cutting walls or ceilings is prohibitive. Continuous diagnostics flow to mobile dashboards, empowering managers to pre-empt pressurization loss or nozzle obstruction. Cloud APIs also allow insurers to verify inspection logs automatically, unlocking premium discounts.

Durability improvements—five-year sealed lithium packs and robust 868/915 MHz protocols—have erased historical objections around power and interference. Consequently, franchisees planning multi-unit roll-outs now weigh wireless first, even in new builds, to future-proof sites for data integrations spanning HVAC, refrigeration and energy analytics. This shift signals a long-term migration in value from copper cabling to software subscriptions bundled with hardware.

Geography Analysis

North America led the industrial cooking fire protection systems market with 32.78% share in 2025 on the back of mature codes, rigorous inspection regimes and dense QSR networks. United States outlets rely on extensive distributor coverage for quarterly maintenance, while Canada pilots PFAS-free pilots that presage continent-wide transitions. Growth to 2031 hinges on replacing legacy wet-chemical skids with IoT-ready, fluorine-free platforms and on integrating hood protection into broader smart-building suites.

Asia-Pacific is on track for the fastest 6.18% CAGR, powered by the unrelenting rollout of branded QSR chains and upscale hotels in Tier 2 and Tier 3 cities across China and India. National building-code tightening and insurers’ insistence on UL-300 equivalence push operators toward certified hardware. Japan’s reliance on performance-based design stimulates demand for compact water-mist systems compatible with narrow kitchen footprints, boosting penetration of high-pressure solutions.

Europe shows steady, regulation-driven expansion. Early adoption of PFAS bans accelerates agent reformulations, positioning European OEMs as trailblazers in sustainable suppression chemistry. Germany’s export-oriented food machinery plants and the United Kingdom’s bustling takeaway sector both require hybrid detection-suppression packages to counter elevated fry-oil flash points. Southern Europe’s tourism rebound revives hotel retrofits, presenting catch-up potential for fire-safety modernization.

Competitive Landscape

The industrial cooking fire protection systems market is moderately fragmented but tilting toward consolidation as large conglomerates acquire specialist technologies. Johnson Controls leverages its Tyco/Ansul brand depth to offer fully integrated detection, suppression and service bundles, anchoring multi-year framework deals with global QSR chains. Honeywell embeds kitchen modules inside its broader building-management ecosystem, crossing over cybersecurity, HVAC and occupant-safety data to offer holistic operational views.

Siemens’ USD 1.2 billion Danfoss Fire Safety takeover in December 2024 exemplifies the race for green suppression IP and enhances its Smart Infrastructure playbook Siemens. Private-equity-backed roll-ups-such as RapidFire Safety’s 2025 acquisition of Christopherson Fire Protection-aggregate regional installers into national platforms able to meet NICET staffing directives and tighter service-level agreements. Competitive differentiation is now less about nozzle metallurgy and more about API openness, analytics dashboards and zero-PFAS credentials.

Pricing power remains with vendors who bundle annual inspection and cloud monitoring, locking clients into multiyear service annuities. Smaller regional manufacturers still win on cost in emerging markets but face mounting certification hurdles and customer preference for suppliers that can furnish proof-of-performance data across continents.

Industrial Cooking Fire Protection Systems Industry Leaders

Ansul Incorporated

API Group Inc.

Emerson Electric Company

Johnson Controls International plc

Gentex Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: FireRite became an authorized distributor of Ansul kitchen suppression solutions, broadening UL-300 product availability in the United Kingdom.

- January 2025: Washington State adopted emergency rules mandating UL 300-compliant automatic extinguishing systems and NICET-certified technicians for commercial kitchens .

- May 2025: RapidFire Safety & Security acquired Christopherson Fire Protection, expanding service coverage across Southern California.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the industrial cooking fire protection systems market as all fixed-installation solutions, detection panels, flame, smoke, heat sensors, hoods, and agent-based suppression units, purpose-built for commercial kitchens and food-processing lines, delivered either as new builds or retrofits and linked to local exhaust systems to meet codes such as NFPA 96.

Scope exclusion: portable extinguishers sold through retail hardware or e-commerce channels are outside this assessment.

Segmentation Overview

- By Product Type

- Fire Detection Systems

- Flame Detectors

- Smoke Detectors

- Heat Detectors

- Fire Management/Suppression Systems

- Wet Chemical Systems

- Dry Chemical Systems

- Water-Mist Systems

- Foam Systems

- Fire Detection Systems

- By Suppression Agent

- Wet Chemical

- Dry Chemical

- Water-Mist

- Inert Gas/CO?

- By End-Use Industry

- Restaurants and Hotels

- Food-Processing Plants

- Institutional Kitchens (Hospitals, Schools, Prisons)

- Catering and Cloud-Kitchen Facilities

- By Connectivity

- Wired Systems

- Wireless/Cloud-Connected Systems

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Russia

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- Rest of Asia-Pacific

- Middle East and Africa

- GCC

- Turkey

- South Africa

- Rest of Middle East and Africa

- North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed kitchen-design engineers, insurance underwriters, code inspectors, and procurement heads across North America, Europe, Asia-Pacific, and the Gulf, which allowed us to validate incident frequencies, average upgrade budgets, and emerging demand for PFAS-free water-mist lines that secondary data alone could not quantify.

Desk Research

Analysts began with freely accessible tier-1 statistics such as US Fire Administration incident tables, UL 300 certification lists, Eurostat building permits tagged to hospitality use, and customs flow records for wet-chemical cartridges. Industry association white papers from NFPA and the Global Foodservice Equipment Council added incident rates and retrofit cycles, while company 10-Ks and IPO filings helped cross-check average selling prices. Paid libraries that we subscribe to, including D&B Hoovers for revenue splits and Dow Jones Factiva for deal tracking, supplied further input. The sources mentioned remain illustrative; many other references were consulted for corroboration and clarification.

Market-Sizing & Forecasting

A top-down construct aligns reported commercial kitchen counts with region-specific adoption rates of compliant hoods and agents, followed by bottom-up checks using sampled ASP × volume from fifteen representative suppliers. Key variables in our model include: (1) yearly net additions of quick-service restaurant outlets, (2) enforcement intensity of NFPA 96 or local analogs, (3) penetration share of wet-chemical cartridges versus water-mist, (4) average retrofit capex per hood, and (5) shift toward IoT-enabled detectors. Multivariate regression, supported by scenario analysis for regulation tightening, projects demand to 2030; missing granular shipment splits are bridged through supplier roll-ups adjusted with import data.

Data Validation & Update Cycle

Outputs undergo variance checks against independent incident ratios and insurer loss data, and then pass a two-step analyst review before sign-off. The dataset refreshes each year, with interim revisions triggered by material code amendments or technology breakthroughs.

Why Mordor's Industrial Cooking Fire Protection Systems Baseline Ensures Reliability

Published estimates often differ because firms pick unequal scopes, base years, and currency conversions, and because some count general fire systems installed in factories, while others, like us, isolate kitchen-specific assemblies.

Key gap drivers include inclusion of residential units, inconsistent ASP inflation assumptions, and one-time COVID rebate adjustments that certain studies embed. Mordor Intelligence limits scope to commercial and industrial kitchens, applies uniform 2024 exchange averages, and refreshes inputs annually; therefore, our 2025 baseline reflects the latest code adoptions and supplier price moves.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 37.15 B (2025) | Mordor Intelligence | - |

| USD 38.03 B (2023) | Global Consultancy A | Includes residential range-hood systems and mixes 2023 FX rates with 2024 volumes |

| USD 34.30 B (2021) | Industry Analytics Firm B | Back-casted to 2021 and rolls hotel sprinklers into kitchen totals, leading to overlap |

| USD 35.56 B (2020) | Trade Journal C | Uses incident cost extrapolation without ASP validation and no retrofit segmentation |

In summary, the disciplined scope selection, variable tracking, and annual refresh cadence adopted by Mordor Intelligence give decision-makers a balanced, transparent baseline that can be traced to verifiable kitchen counts and repeatable modelling steps.

Key Questions Answered in the Report

What is the current size of the industrial cooking fire protection systems market?

The market reached USD 37.15 billion in 2025 and is projected to hit USD 51.88 billion by 2031 on a 5.73% CAGR.

Which product type holds the largest share?

Fire detection systems remain the largest segment, accounting for 57.82% of 2025 revenue.

Why are water-mist systems growing faster than wet-chemical agents?

Regulators are phasing out PFAS in foams, and water-mist delivers comparable suppression with superior environmental credentials, driving a 6.95% CAGR.

Which region is expanding the quickest?

Asia-Pacific is the fastest-growing region at 6.18% CAGR as urbanization fuels new restaurant and hotel kitchens.

How are IoT solutions changing kitchen fire protection?

Cloud-connected sensors provide real-time diagnostics and maintenance alerts, cutting false-alarm downtime and qualifying operators for insurance rebates.

What impact do NFPA 96 and UL 300 mandates have on market demand?

Strict enforcement forces retrofits and new installations, adding roughly 1.2% to the forecast CAGR and expanding recurring service revenue.

Page last updated on: