Fire Suppression Systems Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

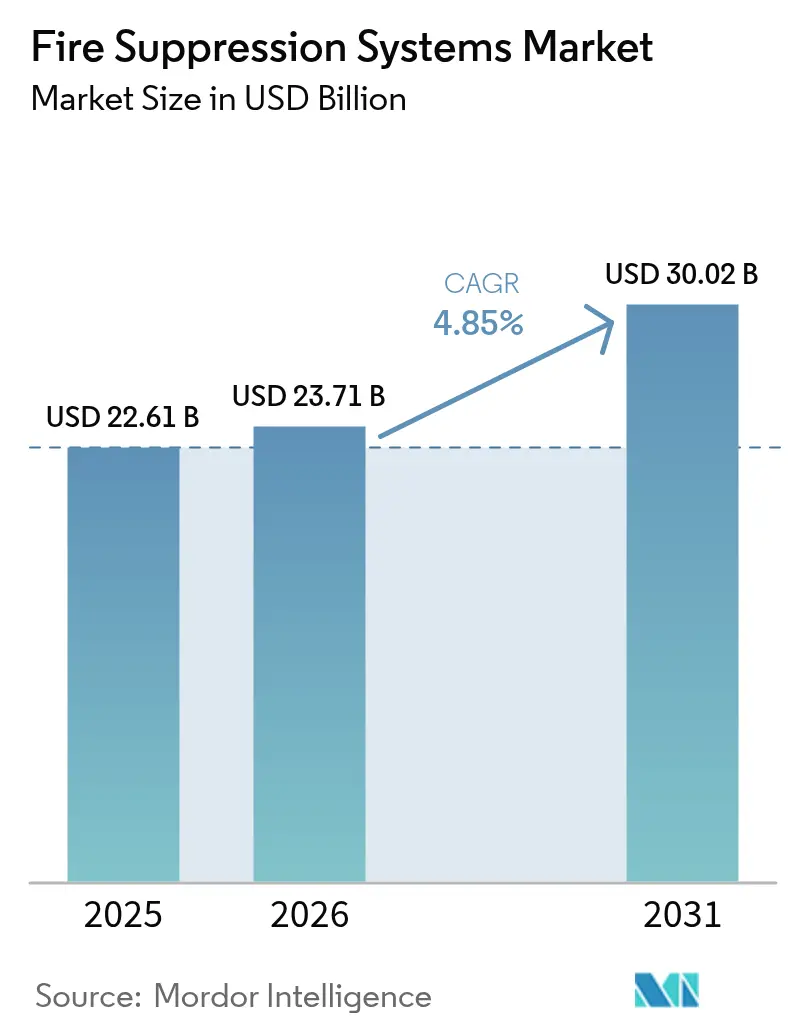

| Market Size (2026) | USD 23.71 Billion |

| Market Size (2031) | USD 30.02 Billion |

| Growth Rate (2026 - 2031) | 4.85% CAGR |

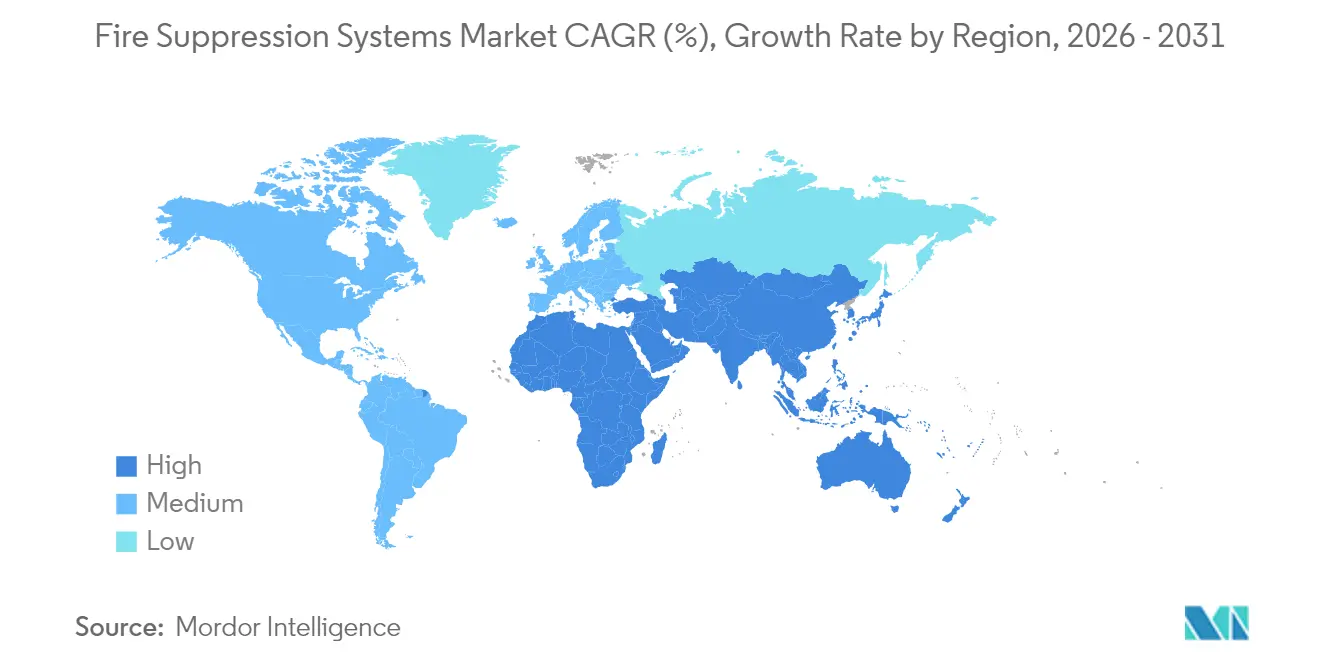

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Fire Suppression Systems Market Analysis by Mordor Intelligence

The fire suppression systems market size was valued at USD 22.61 billion in 2025 and estimated to grow from USD 23.71 billion in 2026 to reach USD 30.02 billion by 2031, at a CAGR of 4.85% during the forecast period (2026-2031). Heightened regulatory scrutiny, the migration toward environmentally benign clean agents, and sustained infrastructure spending in data centers, energy, and high-rise construction collectively underpin the growth path of the fire suppression systems market. Water-based sprinklers retain cost leadership, yet clean-agent platforms are scaling quickly on halon-replacement demand. Asia-Pacific, propelled by hyperscale data center buildouts and factory additions, already contributes the largest regional revenue slice. Meanwhile, portfolio optimization by leading OEMs and integrators signals a maturing but still consolidating competitive arena.

Key Report Takeaways

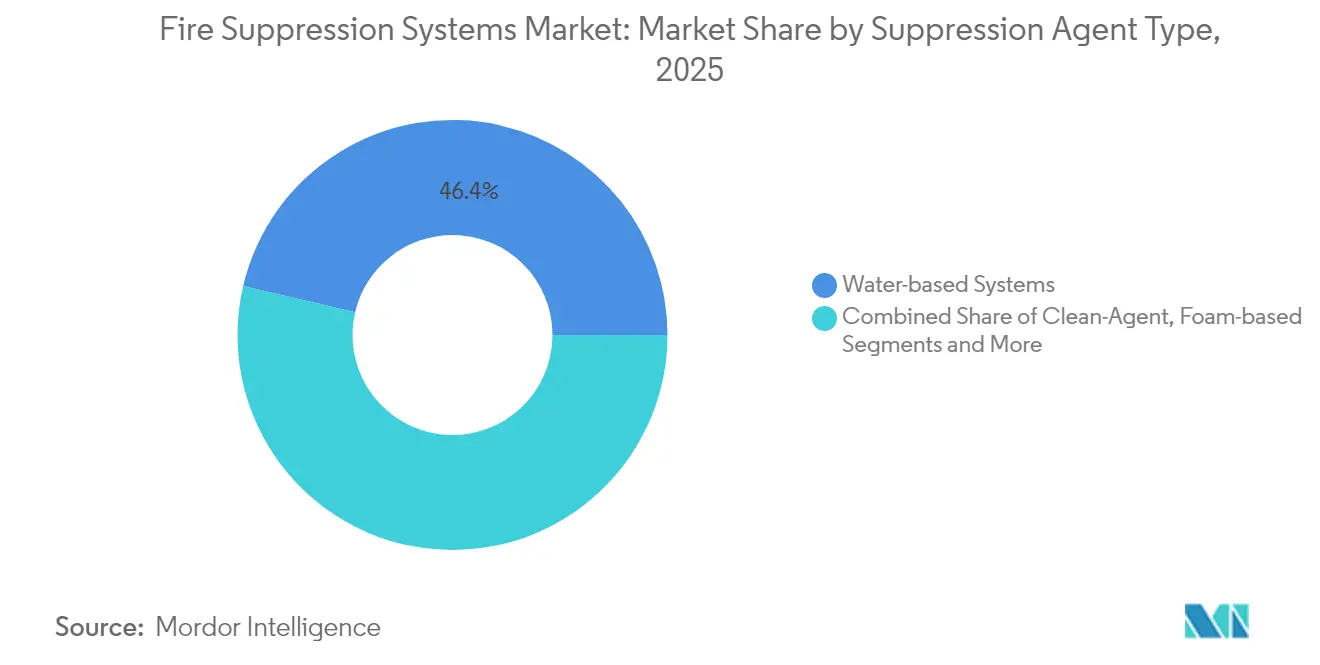

- By suppression agent, water-based products held 46.35% of fire suppression systems market share in 2025, while clean agents are projected to expand at a 6.95% CAGR to 2031.

- By product configuration, fixed installations accounted for 81.20% of the fire suppression systems market size in 2025; portable/mobile solutions are forecast to grow at 5.85% CAGR through 2031.

- By end-use industry, commercial buildings led with a 33.35% revenue share in 2025, whereas oil & gas registered the fastest CAGR at 6.12% during 2026-2031.

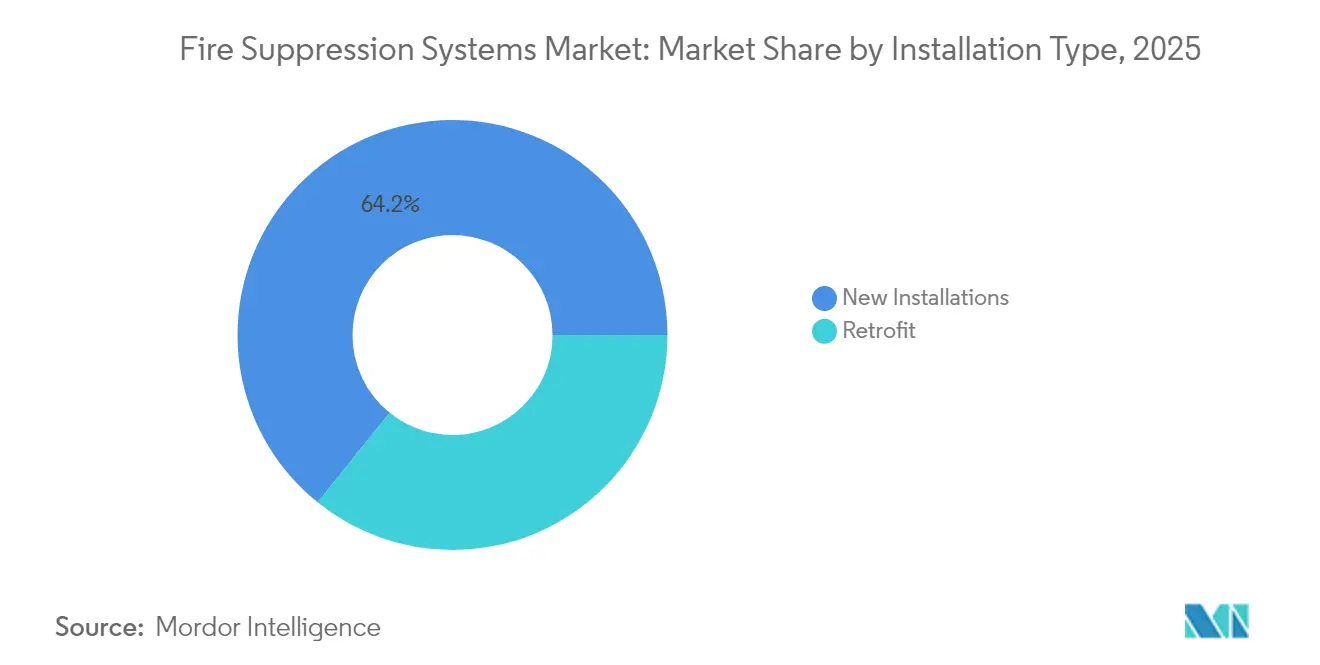

- By installation type, new builds captured 64.20% of 2025 revenue, while retrofit upgrades are set to advance at a 6.75% CAGR over the forecast horizon.

- By distribution channel, system integrators and EPC contractors commanded 51.30% of global turnover in 2025, whereas direct-to-end-user sales are projected to rise at a 5.72% CAGR through 2031.

- By geography, Asia-Pacific captured 35.65% of the fire suppression systems market in 2025 and is expected to remain the largest contributor through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Fire Suppression Systems Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Transition from Halon to Sustainable Clean-Agent Replacements | +0.8% | Europe, North America | Medium term (2-4 years) |

| Insurance Premium Discounts for Automated Suppression in High-Value Assets | +0.6% | North America, Europe | Short term (≤ 2 years) |

| Data-center Boom Spurring Water-less Gaseous Systems | +1.2% | Asia-Pacific, North America | Long term (≥ 4 years) |

| Offshore Oil-&-Gas Fire-safety Mandates | +0.4% | North Sea, GCC, Global offshore | Medium term (2-4 years) |

| Post-Grenfell Residential High-Rise Sprinkler Mandates | +0.3% | UK, US, Europe | Short term (≤ 2 years) |

| EV-Battery Production Lines Requiring Dry-Chemical Suppression | +0.9% | Global, concentrated in Asia | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Transition from Halon to Sustainable Clean-Agent Replacements

EASA’s requirement for halon-free aircraft fire protection by 2026 forces airlines and MROs to retrofit nearly 15,000 aircraft, creating a USD 800 million annual opportunity for Novec 1230, FM-200, and inert-gas systems. Demand concentrates in hangars, telecom hubs, and mission-critical facilities where environmental compliance outweighs life-cycle cost, favoring integrators with multi-agent design expertise.[1]European Aviation Safety Agency, “NPA 2014-26,” easa.europa.eu

Insurance Premium Discounts for Automated Suppression in High-Value Assets

Commercial property insurers grant 5-15% policy discounts for NFPA-compliant automatic systems, a benefit magnified by U.S. tax code Section 179 that allows immediate expensing of up to USD 1.22 million for sprinkler installations. The combined savings reduce payback periods to three years for many data centers and pharma plants.

Data-Center Boom Spurring Water-less Gaseous Systems

Hyperscale operators in China are growing IT floor space above 40% annually, prioritizing Novec 1230 and IG-541 systems that leave no residue on servers. Higher-pressure cylinders cut storage footprints by 60%, a critical advantage in premium urban real estate.

Offshore Oil-and-Gas Fire-Safety Mandates

IMO guidelines introduced in 2020 tighten pump-room and engine-room standards, prompting retrofits worth USD 300 million per year in the North Sea and GCC arenas. Certified vendors with marine-grade corrosion-proof components capture this specialized demand.

Restraints Impact Analysis*

| RESTRAINTS | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| PFAS Ban Driving Costly AFFF Foam Retrofits | -0.7% | Europe, North America, Australia | Short term (≤ 2 years) |

| Scarcity of NFPA-Certified Installers in Emerging Asia | -0.5% | Asia-Pacific emerging markets | Medium term (2-4 years) |

| Semiconductor Component Shortages Delaying Projects | -0.4% | Global | Short term (≤ 2 years) |

| High CAPEX of Inert-Gas Systems for Small Premises | -0.3% | Global, particularly SMEs | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

PFAS Ban Driving Costly AFFF Foam Retrofits

The EU’s impending PFAS prohibition forces airports and petro-chemical depots to swap AFFF for fluorine-free formulations that require 30-50% higher application rates, raising per-site retrofit costs to USD 150,000–500,000.[2]Fire Industry Association, “FIA Guidance on PFAS in Firefighting Foams Restrictions Update September 2024,” fia.uk.com

Scarcity of NFPA-Certified Installers in Emerging Asia

The shortage of NFPA-certified technicians across emerging Asian markets constrains system deployment capacity and inflates installation costs by 25-40% compared to mature markets. NAFED certification programs require 3-year renewal cycles and specialized training that many regional contractors cannot access due to geographic and language barriers.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Suppression Agent Type: Clean Agents Drive Innovation

Water-based sprinklers retained a 46.35% fire suppression systems market share in 2025, buoyed by low cost and proven performance. Clean-agent solutions, although smaller in absolute value, are slated for a 6.95% CAGR, lifting their fire suppression systems market size measurably during 2026-2031. Regulatory pressure to replace halon and PFAS foams accelerates adoption of Novec 1230, FM-200, and IG-541.

Technology convergence is spawning hybrid arrangements that pair water mist with inert gas to tame lithium-ion thermal runaway. UL 9540A trials show water overlays can halt cascading cell failures faster than gas-only discharges. Foam lines, challenged by fluorine-free transition costs, risk incremental share loss, whereas CO₂ and powder systems cling to niche roles in unoccupied or battery-assembly zones.

By Product Configuration: Fixed Systems Dominate Infrastructure

Fixed installations accounted for 81.20% of the 2025 fire suppression systems market, reflecting end-users’ preference for always-on protection in data centers, refineries, and commercial towers. Portables, although smaller, are gaining at 5.85% CAGR as construction sites and events need flexible cover.

High-bay warehouses and cold-storage facilities are adopting Johnson Controls’ Tyco ESFR-25 dry-type sprinkler, which functions at −60 °F and eliminates in-rack heads. IoT-enabled monitors now extend to portables, giving facility managers real-time visibility similar to fixed networks.

By End-Use Industry: Industrial Leads Growth

Commercial real-estate commanded 33.35% of 2025 revenue, yet oil & gas, chemicals, and energy storage are forecast to log the steepest 6.12% CAGR through 2031. The fire suppression systems market in industrial complexes is propelled by production downtime risks exceeding USD 1 million per day.

Residential retrofits expand steadily after the UK and select U.S. states tightened sprinkler codes. Transportation, especially EV manufacturing, is experimenting with embedded suppression hardware such as Hyundai Mobis’ integrated battery module, potentially reshaping system-level demand.

By Installation Type: Retrofits Accelerate Growth

New-builds still form 64.20% of installation value, but retrofits will outpace them at 6.75% CAGR as regulations change faster than building cycles. Seismic bracing and vacuum drain technology included in the 2025 NFPA 13 edition will force upgrades in legacy structures.

Occupied-site retrofits command premium pricing because integrators must stage work to avoid business disruption. Owners often decide that full replacement beats piecemeal upgrades due to compatibility and liability concerns.

By Distribution Channel: Integrators Leverage Expertise

System integrators and EPC contractors captured 51.30% of 2025 sales, a testament to the complexity of sizing, hydraulic calculations, and code approvals in the fire suppression systems market. Direct-to-end-user channels grow near 5.72% CAGR, facilitated by e-procurement portals offering standardized components.

Nonetheless, liability transfer keeps large corporates wedded to integrators who can underwrite design warranties. In emerging Asia, contractor scarcity still tilts bargaining power toward global integrators.

Geography Analysis

Asia-Pacific produced 35.65% of global revenue in 2025 as China, India, and Southeast Asia commissioned hyperscale data centers and megaproject factories. Government incentives and an average USD 2 trillion in annual construction spending ensure the region remains the epicenter of the fire suppression systems market. NFPA-certified labor shortages continue to stretch project timelines and raise installed costs, yet domestic codes are gradually harmonizing with U.S. and EU standards to open cross-border supply chains.

North America enjoys deep installer pools and mature building codes, translating into predictable retrofit volumes tied to insurance incentives. The 2025 NFPA 13 update is expected to inject a new wave of demand across legacy warehouses and healthcare facilities. Component shortages, especially in electronic control panels, have introduced 3-6-month delays, but value-chain resiliency programs underway at leading OEMs should ease the bottleneck during 2026.

Europe records steady uptake as the PFAS foam ban and post-Grenfell rules reshape specifications. Germany’s advanced manufacturing plants demand inert-gas and water-mist hybrids that command premium pricing. Offshore wind farms in the North Sea are another rising niche, requiring marine-grade suppression assemblies. Brexit-related customs frictions persist, yet collaborative agreements with EU-based distributors are smoothing flows of cylinders and valves.

Regulatory Landscape

Fire suppression system specification is anchored to widely adopted consensus standards and insurer-driven requirements, and the 2026 update cycle is tightening inspection and performance expectations across both traditional and newer applications. The NFPA 25:2026 edition updates inspection, testing, and maintenance practices for water-based fire protection systems, while UL published ANSI/UL 2167 Edition 3 in May 2026 to refresh performance requirements for water mist nozzles used in residential, shipboard, and commercial settings.

Mission-critical and energy-transition loads are also showing up in more explicit regulatory definitions. The Hong Kong Fire Services Department (HKFSD) introduced a new classification for "Data Centre" premises in its FSI Code effective August 1, 2025, and India NBCS 2026 formalizes Group E-II Datacentres as a distinct occupancy category, which affects allowable suppression architectures (gas, water mist, sprinkler) and design documentation. In parallel, FM Global revised Data Sheet 2-0 in January 2026 for water-based protection in data centers, including guidance linked to lithium-ion battery storage, and the 2026 edition of NFPA 855 adds Hazard Mitigation Analysis (HMA) as a broad design requirement for stationary energy storage systems.

Value Chain Analysis

The value chain covers commodity and specialty inputs (steel, copper/brass, fittings, mineral wool firestopping, elastomers, cylinders, and clean agents), electronics (detectors, releasing/control panels, supervisory sensors, networking modules), and engineered assemblies (valves, nozzles, pipe networks, pre-action and deluge skids, water mist systems, inert gas and chemical agent cylinders). Downstream, OEMs and subsystem makers sell through system integrators and EPC contractors that complete hazard analysis, hydraulic calculations, commissioning, and code acceptance, and then capture recurring revenue through inspection, testing, maintenance, and retrofit/replacement work, which is a major route to lifecycle margin given that fixed installations represented 81.20% of market configurations in 2025.

Lead times and compliance requalification keep shaping procurement choices. FCIA reported mineral wool supply times reaching up to 27 weeks in April 2024, and metal price volatility for copper/brass components adds cost pass-through complexity for sprinklers, valves, and fittings. When buyers pursue sourcing shifts to reduce tariff and logistics exposure, UL/FM approvals and local AHJ acceptance can slow supplier substitution, because component changes often trigger documentation and re-certification work. For data-center projects, buyers frequently align designs to frameworks such as NFPA 75 and FM Global Data Sheet 5-32, which reinforces demand for larger integrators able to coordinate multi-vendor stacks (aspirating detection, pre-action water, and clean agent) and provide connected monitoring across geographically distributed sites.

Competitive Landscape

The fire suppression systems market is moderately concentrated. Johnson Controls, Siemens, and Honeywell collectively captured roughly 32% of 2024 revenue. Their strengths include broad portfolios, proprietary detection algorithms, and lifelong service contracts. Siemens’ USD 1.8 billion purchase of Danfoss Fire Safety added high-pressure water-mist know-how. Carrier’s USD 1.425 billion divestiture of its industrial fire unit to Sentinel demonstrates ongoing portfolio pruning to focus on core HVAC.

Private equity appetite remains high: Blackstone bought AI Fire for USD 1.1 billion, while ADIA and GIC acquired minority stakes in Pye-Barker Fire & Safety, signaling confidence in aftermarket service margins. Local champions in China and India continue to win green-field contracts where domestic certification or language fluency confers advantage, creating fertile ground for future consolidation.

Technology competition now hinges on sustainable agents and IoT integration. Vendors increasingly bundle analytics dashboards that track cylinder pressure, valve status, and false-alarm trends. Early adopters report maintenance cost cuts near 15%. As cyber-security rules tighten for critical infrastructure, OEMs with UL CAP or IEC 62443 credentials will widen their moat.

Fire Suppression Systems Industry Leaders

Johnson Controls International plc

Siemens AG

Carrier Global Corp.

Minimax Viking Group

Honeywell International Inc.

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Near-term whitespace is concentrated where codes and standards specify requirements for data centers and battery-adjacent infrastructure, increasing the need for engineered, multi-layer suppression packages rather than single-product installations. The Hong Kong Fire Services Department August 1, 2025 Data Centre classification in the FSI Code and India NBCS 2026 Group E-II Datacentres occupancy category shift procurement toward compliant fixed systems (gas suppression, water mist, or sprinklers) supported by design documentation and acceptance testing. In Europe, VdS 6003en:2025-06 applies to orders placed from June 1, 2025 for IT rooms and data centers, creating another specification pathway that favors vendors and integrators able to standardize solutions across multi-country rollouts.

A second opportunity set is tied to agent transition and service compliance, pushing demand toward alternative agent platforms and higher-value maintenance capabilities. In the United States, Emissions Reduction and Reclamation (ER&R) requirements from the Environmental Protection Agency (EPA) effective January 2026 make it unlawful to vent HFCs during servicing, repair, or disposal of fire suppression equipment, and they introduce technician training requirements for HFC-based systems, with a June 2026 training completion deadline for technicians hired on or before January 1, 2026. This expands the addressable scope for connected service offerings and compliance-oriented retrofits, including OEM moves such as Johnson Controls Connected Sprinkler service and the broader shift toward IoT-enabled monitoring that reduces impairments and false alarms. At the same time, the NFPA 25 2026 edition adds annex guidance on timeframes for correcting impairments and critical deficiencies, strengthening the case for digital inspection workflows and predictive maintenance across installed bases.

Recent Industry Developments

- June 2026: Siemens unveiled its Acend Intelligent notification portfolio, emphasizing connected testing and cloud-enabled predictive maintenance workflows. The launch supports building operators and integrators that are standardizing notification and supervision across multi-site portfolios, particularly where downtime and testing disruptions are tightly controlled.

- June 2025: Johnson Controls relaunched its Connected Sprinkler service to provide real-time system insights and a more predictive approach to water-based fire protection maintenance. The update strengthens recurring service attachment in retrofit-heavy environments where compliance and uptime requirements are pushing owners toward digital monitoring.

- December 2024: Carrier completed the USD 3 billion sale of its Commercial and Residential Fire business to Lone Star Funds, forming the independent Kidde Global Solutions. The transaction reshaped competitive dynamics by separating a large installed-base and product portfolio into a standalone fire and life safety player with its own investment and channel priorities.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers revenue generated from fire suppression systems used to control or extinguish fires in buildings, facilities, and transport settings, including equipment and installed system packages across common suppression technologies.

Scope exclusions: We exclude fire detection-only products, stand-alone fire alarm panels, and non-suppression building services that do not directly deliver suppression capability.

Segmentation Overview

- By Suppression Agent Type

- Water-based Systems (Sprinkler, Mist)

- Clean-Agent (FM-200, Novec 1230, Inert Gas)

- Foam-based Systems (AFFF, Fluorine-free)

- Dry-Chemical Powder Systems

- Carbon-Dioxide Systems

- Hybrid Inert-Gas and Water-Mist Systems

- By Product Configuration

- Fixed/Installed Systems

- Portable and Mobile Units

- By End-Use Industry

- Commercial (Offices, Retail, Hospitality)

- Industrial (Oil and Gas, Energy, Manufacturing, Warehouses)

- Residential (Multi- and Single-Family)

- Transportation (Marine, Aviation, Rail, Automotive)

- Public and Institutional (Education, Healthcare, Government)

- By Installation Type

- New Installations

- Retrofit and Replacement

- By Distribution Channel

- Direct to End-User

- System Integrators and EPC Contractors

- OEM/Equipment Manufacturers

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- South Korea

- ASEAN

- Australia

- Rest of Asia-Pacific

- Middle East and Africa

- Saudi Arabia

- South Africa

- Nigeria

- United Arab Emirates

- Rest of Middle East and Africa

- North America

Data Sources, Market Sizing, and Validation

Desk Research

We start by mapping the demand pool using public safety and construction signals, since suppression spend typically follows new builds, retrofit cycles, and how codes are enforced.

For this, we reviewed sources such as NFPA codes and reports, NIST fire research publications, U.S. Census Bureau construction and building permits series, OSHA enforcement guidance, and International Code Council model code references.

Next, we align supply and pricing context using company annual reports, investor presentations, product catalogs, and trade press coverage that references system approvals and agent transitions. Paid subscriptions were used only for company financials and intelligence, plus import and export shipment level checks where relevant for valves, cylinders, and key components. The desk sources listed here are illustrative, and we also used other public documents and disclosures to collect data, validate assumptions, and clarify open questions.

Primary Interviews and Surveys

We then validate what the desk work suggests through interviews and structured surveys with manufacturers, installers and integrators, distributors, and end users involved in commercial, industrial, and transport projects across major regions. The respondent input helped confirm how system mixes vary by site type, how retrofit timing differs between categories, and what installed price ranges are being quoted in current bidding cycles.

We also asked specifically about how clean agent substitutions affect specification choices and replacement timing, so the market model reflects current installer practice rather than only published catalog pricing.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 31% | CXOs: 14% | APAC: 44% |

| Mid tier: 55% | Functional/Unit leaders: 27% | EMEA: 34% |

| Smaller Players: 14% | Managers: 59% | Americas: 22% |

Market-Sizing & Forecasting

We size the market using a top-down approach once the demand pool is rebuilt from construction activity and safety compliance intensity, then converted into suppression adoption and replacement spending. The resulting totals are corroborated with selective bottom-up approximations from sampled installed prices multiplied by plausible unit volumes, with channel checks from integrators and distributors to keep the scale realistic.

Key model inputs include new installation versus retrofit share, agent type mix (water-based, clean agent, foam, dry chemical), end-use exposure (industrial sites, commercial buildings, residential, and transportation), and typical installed cost ranges by system configuration. Because specification changes can move pricing quickly, assumptions on clean agent replacements and component lead times were refreshed using interview feedback before finalizing the base year.

For forecasting, we primarily used scenario analysis tied to construction spending, infrastructure additions like data centers, and the pace of code-driven retrofits, then applied smoothing to reduce the risk of unrealistic spikes. When a bottom-up signal was missing for a niche application, we filled the gap using adjacent end-use ratios from interviews and then rechecked the impact on the total market value.

Data Validation & Update Cycle

We validate results through multiple triangulation steps that compare model outputs against independent indicators, such as permit trends, retrofit cadence discussions, and supplier backlog commentary drawn from public disclosures. Outliers are flagged, and if the variance cannot be explained by regional mix or product mix shifts, we recheck the assumptions through follow-up calls.

Before sign-off, the model goes through a multi-step internal review to ensure calculation logic, units, and currency handling are consistent across regions and years. Reports are refreshed annually, with interim updates triggered by material events like major code changes, supply disruptions, or step changes in agent availability, and a final pre-delivery pass is completed to keep the numbers current.

Mordor Intelligence's Fire Suppression Systems Market Estimate Compared With Other Published Estimates

Published market sizes for fire suppression systems can differ even when they appear to measure the same scope, since scope and counting logic are not always aligned. Variances usually come from what gets included as a system, whether adjacent products are rolled in, and how retrofit spending is handled versus new installations.

Some sources broaden scope by combining suppression with adjacent categories like explosion suppression or by including a wider set of fire protection products. In Mordor Intelligence's model, the total is limited to suppression systems revenue only, with demand built from installation and replacement cycles and then cross-checked by agent type mix and installed price ranges.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 23.71 B (2026) | |

| Industry Publisher A | USD 21.50 B (2023) | This figure is anchored to an earlier year and appears to follow a broader product view that can blend suppression items with other fire protection solutions, which shifts the base and changes the mix assumptions used to move from base year to forecast. |

| Regional Consultancy B | USD 10.75 B (2024) | The scope explicitly includes explosion suppression as part of the total market, and the category bundling and segment definitions are not directly comparable to a suppression-only system spend model, thereby producing a different total even before growth assumptions are applied. |

The comparison shows that year alignment and category bundling are the biggest reasons the numbers spread out. By keeping the scope tied to suppression systems and by using clear demand drivers like installation cycles, retrofit timing, and agent mix, the estimate stays traceable to repeatable steps and practical checks.

Key Questions Answered in the Report

What is the current value of the fire suppression systems market?

The fire suppression systems market is valued at USD 23.71 billion in 2026 and is projected to climb to USD 30.02 billion by 2031.

Which suppression agent type is growing the fastest?

Clean-agent platforms such as Novec 1230 and FM-200 are expanding at a 6.95% CAGR, the quickest among agent categories.

Why are data centers opting for gaseous systems over water sprinklers?

Gaseous agents avoid water damage to electronics, occupy smaller footprints with high-pressure cylinders, and comply with hyperscale operators’ uptime mandates.

How are PFAS regulations affecting foam-based systems?

EU and U.S. bans on PFAS are forcing costly retrofits to fluorine-free foams, raising per-site expenses by up to USD 500,000 and temporarily dampening foam demand.

Which region leads market revenue?

Asia-Pacific contributes 35.65% of global revenue, fueled by large-scale industrialization and data-center construction.

Are integrated detection and suppression platforms becoming standard?

Yes, OEMs increasingly bundle IoT analytics that cut maintenance costs and reduce false alarms, a differentiator in competitive bids.

Page last updated on: