Commercial Security Robot Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

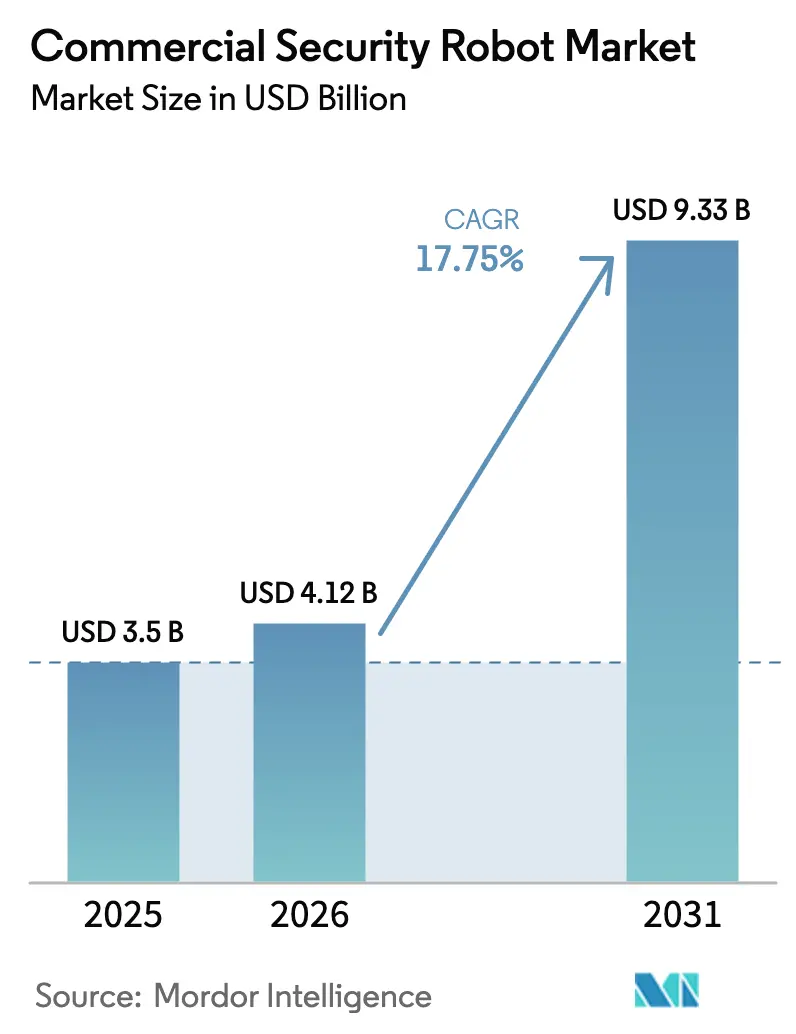

| Market Size (2026) | USD 4.12 Billion |

| Market Size (2031) | USD 9.33 Billion |

| Growth Rate (2026 - 2031) | 17.75% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Commercial Security Robot Market Analysis by Mordor Intelligence

The commercial security robot market size was valued at USD 3.5 billion in 2025 and estimated to grow from USD 4.12 billion in 2026 to reach USD 9.33 billion by 2031, at a CAGR of 17.75% during the forecast period (2026-2031). Falling LiDAR prices, longer-lasting batteries, and an increase in security breaches at critical facilities are prompting enterprises to transition from fixed cameras and human patrols to mobile, autonomous platforms. Insurers now grant premium discounts to sites protected by certified robotic guards, which shortens payback periods and improves return on investment. Municipal green-finance rules increasingly reward low-carbon patrol technologies, so many public agencies treat robots as a sustainability measure rather than a pure security spend. Finally, private 5G rollouts enable ultra-low-latency fleet coordination, expanding the addressable use cases of the commercial security robot market across large campuses and multi-site operations.

Key Report Takeaways

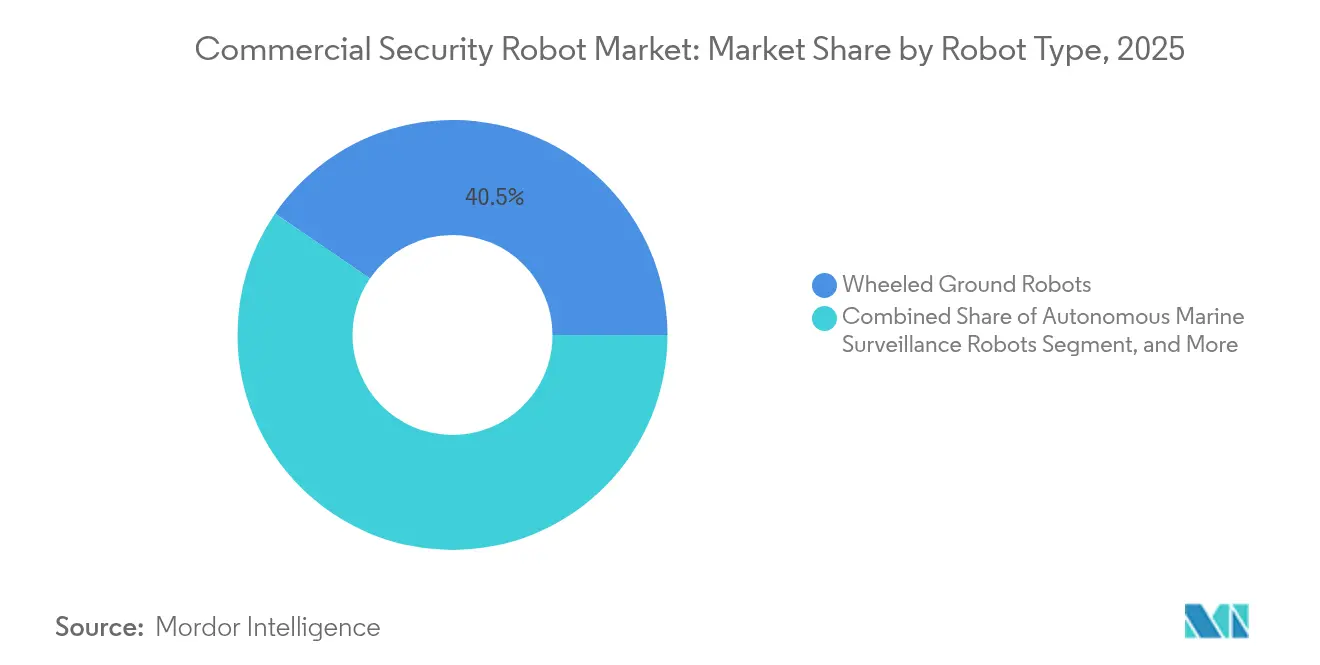

- By robot type, wheeled ground units held a 40.45% share of the commercial security robot market in 2025, whereas aerial security drones are forecast to grow at a 20.89% CAGR through 2031.

- By end user, commercial buildings led with 22.05% revenue share in 2025; public infrastructure and smart city projects are expected to expand at a 19.12% CAGR through 2031.

- By component, hardware accounted for 58.15% of the commercial security robot market size in 2025, while software and services are projected to advance at a 21.34% CAGR.

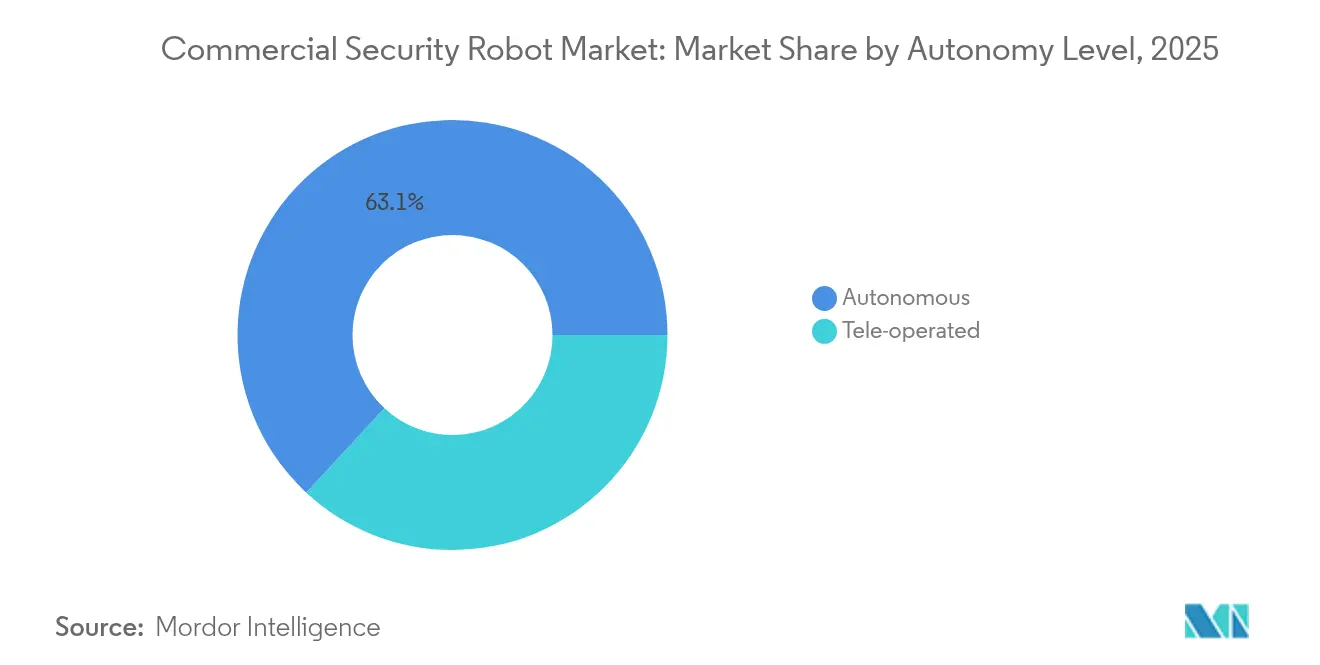

- By autonomy level, autonomous platforms captured 63.10% share of the commercial security robot market size in 2025 and are projected to post a 18.76% CAGR by 2031.

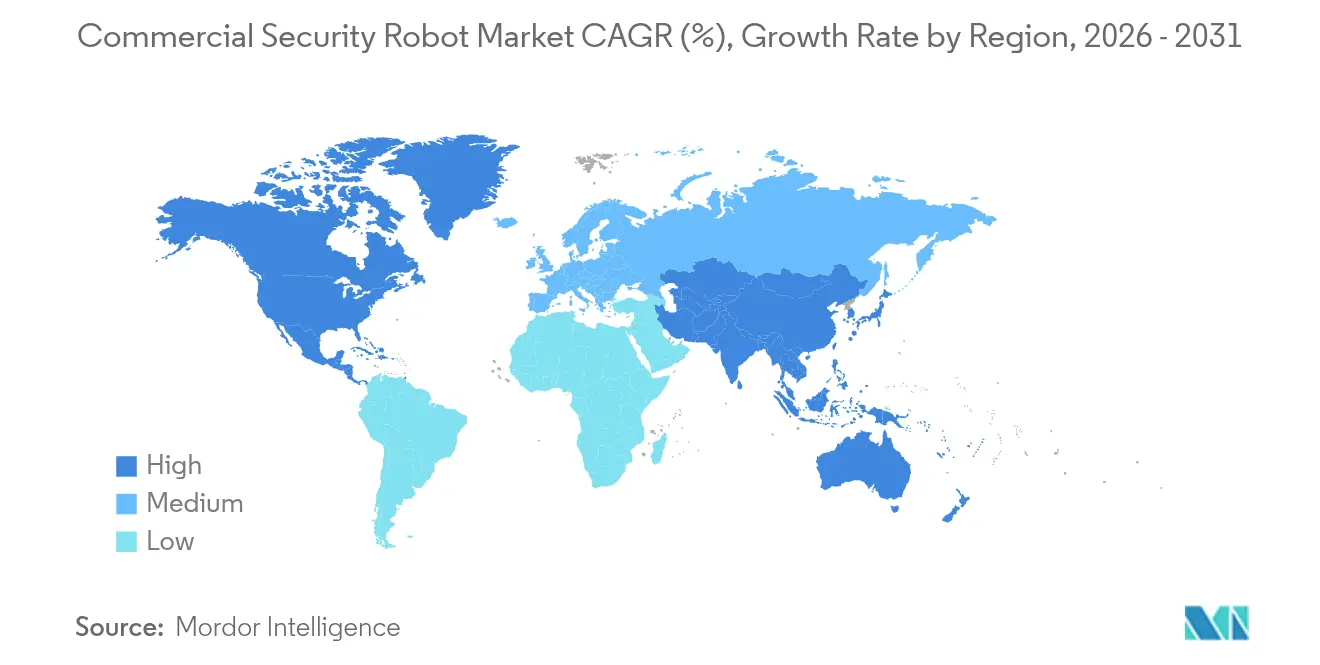

- By geography, North America dominated with a 35.85% share in 2025; the Asia-Pacific region is set to record the fastest growth, with a 19.65% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Commercial Security Robot Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Rising adoption of autonomous patrol robots for perimeter security | +4.8% | Global; early uptake in North America and Europe | Medium term (2-4 years) |

| Declining cost of Li-DAR and battery technologies | +3.2% | Global; manufacturing centered in Asia-Pacific | Short term (≤ 2 years) |

| Surge in security breaches at critical infrastructure and public venues | +3.9% | Global; heightened in North America and Europe | Short term (≤ 2 years) |

| Insurance-premium incentives for certified robotic guards | +2.1% | North America and Europe, expanding to Asia-Pacific | Medium term (2-4 years) |

| ESG-linked financing favoring low-carbon robotic security | +1.8% | Global; led by Europe | Long term (≥ 4 years) |

| Private 5G networks enabling ultra-low latency robot fleets | +2.4% | Asia-Pacific core, spill-over to North America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Adoption of Autonomous Patrol Robots for Perimeter Security

Security teams increasingly deploy autonomous patrol robots to fill blind spots that fixed cameras and roving guards struggle to cover. Asylon’s DroneDog-2 combines quadruped mobility with dock-launched drones, extending surveillance to multilevel terrains and rooftops.[1]Source: Asylon, “DroneDog-2 Platform Specifications,” asylonrobotics.com SMP Robotics proved outdoor resilience when its S5.2 platform maintained 99.2% uptime during harsh-weather pilots in 2024.[2]Source: SMP Robotics, “S5.2 Performance Data,” smprobotics.com Integrated thermal imaging, paired with AI object detection, now identifies intruders beyond 500 meters, effectively raising the perimeter without requiring additional towers or cables. RAD’s ROAMEO Gen 4 layers predictive analytics onto patrol data, alerting operators before a potential breach occurs rather than after an alarm trips. These autonomous capabilities can reduce guard headcount while maintaining 24/7 coverage, a proposition that resonates in large industrial parks and energy assets, where staffing is costly.

Declining Cost of LiDAR and Battery Technologies

Solid-state LiDAR modules have seen a significant drop in price since 2024, as photonics integration and MEMS manufacturing have reached scale. Lower sensor costs make millimeter-level mapping affordable for mid-tier users who once relied on basic ultrasonic collision pairs. Parallel improvements in lithium-ion chemistry now yield 12-hour duty cycles for wheeled robots, removing frequent charging as an operational bottleneck. Vendors are already field-testing solid-state batteries that promise longer runtimes and lower fire risk in indoor deployments. Predictive battery-management software can flag degradation 30 days in advance, allowing planned swaps during lulls instead of emergency shut-offs. Together, cheaper perception and longer endurance widen the commercial security robot market’s pool of viable buyers beyond blue-chip campuses.

Surge in Security Breaches at Critical Infrastructure and Public Venues

The U.S. Cybersecurity and Infrastructure Security Agency reported a rise in physical security incidents at critical sites in 2024.[3]Source: Cybersecurity and Infrastructure Security Agency, “Critical Infrastructure Incidents 2024,” cisa.gov Airports, utilities, and data centers now face blended threats where cyber actors use physical access to plant network implants. Homeland Security guidelines urge 24/7 automated monitoring, positioning robots as force multipliers that never tire. Early trials with the Transportation Security Administration have shown that robots reduce false alarms in baggage halls compared to static camera analytics, freeing agents for higher-value tasks. Scalability is another edge: fleets can surge during elevated threat periods without the logistical hurdles of onboarding temporary guards.

Insurance-Premium Incentives for Certified Robotic Guards

Major underwriters recognize lower incident rates when autonomous patrols document every interaction, as this provides a more comprehensive view of the situation. Zurich Insurance offers premium discounts of 15–25% to facilities that meet the ISO 3691-4 robotic guard standards. SOMPO Holdings introduced blended-coverage policies that combine robot hardware, liability, and cyber intrusion clauses into a single package, streamlining procurement for risk managers. Munich Re’s actuarial models now rate robot-equipped sites as lower exposures, resulting in more favorable deductibles. For high-value warehouses and distribution hubs, these incentives can shave millions from annual risk budgets, accelerating the commercial security robot market’s penetration into price-sensitive verticals.

Restraints Impact Analysis*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| High upfront CAPEX and lifecycle OPEX | -2.8% | Global; acute in cost-sensitive markets | Short term (≤ 2 years) |

| Data privacy and AI liability concerns | -1.9% | Europe and North America; spreading worldwide | Medium term (2-4 years) |

| Vandalism and tampering risk raises TCO | -1.4% | Urban sites globally | Medium term (2-4 years) |

| Edge-AI robustness limits in extreme weather | -1.2% | Harsh-climate regions | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Upfront CAPEX and Lifecycle OPEX

Full-site security robot deployments can cost USD 150,000–500,000, a hurdle for mid-sized enterprises lacking large capital budgets. Annual upkeep, including sensor calibration, software licensing, and drivetrain maintenance, typically accounts for 25-30% of the purchase price, complicating ROI models. When iRobot secured a USD 200 million term loan in 2024, lenders priced it at an interest rate above 9%, underscoring the perceived operational risk in robotics ventures.[4]Source: U.S. Securities and Exchange Commission, “iRobot DEFA14A,” sec.gov Leasing and robotics-as-a-service contracts offer alternatives; however, some buyers hesitate due to long-term commitments and performance guarantees. Until hardware prices fall further or financial products mature, CAPEX remains the most immediate drag on the commercial security robot market.

Data-Privacy and AI-Liability Concerns

Europe’s AI Act mandates risk assessments and human oversight for high-risk systems, including autonomous security robots. Operators must demonstrate compliance with GDPR when facial recognition captures personally identifiable information, a tall order in open public spaces. Vendors now embed privacy-by-design features, such as on-edge redaction and opt-in data retention, to reassure regulators; yet, legal clarity remains unfinished business.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Robot Type: Versatile Platforms Redefine Coverage

Ground robots held a 40.45% share of the commercial security robot market in 2025, cementing their role as baseline perimeter guardians that navigate paved paths and corridors without structural retrofits. Aerial security drones, however, are flying ahead with a projected 20.89% CAGR as private 5G enables split-second path updates and multi-drone swarming.

Legged and hybrid robots such as Boston Dynamics’ Spot prove valuable in sites with stairs, catwalks, or uneven terrain, areas where wheels struggle. Autonomous marine surveillance units, though niche, protect ports and offshore infrastructure where human patrols are cost-prohibitive. Cross-platform orchestration dashboards now allow command centers to task ground, air, and marine units from a single console, making mixed-fleet deployments feasible. Edge AI reduces bandwidth requirements, allowing even remote sites with limited backhaul to deploy intelligent patrols.

By End User: Infrastructure Investment Fuels Uptake

Commercial buildings accounted for 22.05% of 2025 revenue, primarily driven by corporate campuses and shopping centers that prioritize visible deterrence and continuous patrol logs. Yet, public infrastructure projects, such as airports, transit hubs, and city centers, are on track for a 19.12% CAGR as municipalities embed robots into smart-city sensor grids. The commercial security robot market size allocated to government contracts is growing as stimulus funds target resilience upgrades following high-profile attacks.

Industrial and logistics facilities utilize robots to inspect perimeter fencing and loading docks in conjunction with warehouse automation workflows. Healthcare campuses adopt privacy-sensitive patrol bots that also serve as telepresence emergency aids, an attractive dual function amid nurse shortages. Integration with building-management systems triggers automatic door lockdowns or HVAC isolation when robots confirm a threat, demonstrating value beyond pure observation.

By Autonomy Level: AI Supremacy Gains Ground

Autonomous systems accounted for 63.10% of the 2025 volume, and their 18.76% CAGR indicates rising confidence in unsupervised navigation algorithms. Private 5G slices lower latency to under 10 milliseconds, supporting real-time coordination among dozens of units and enabling teleoperation to edge into specialist niches. In the commercial security robot market, tele-operated models persist in nuclear plants or prison yards where policy demands human decision-making for engagement.

Natural-language interfaces powered by large language models enable guards to redirect a robot via speech, thereby closing the usability gap between autonomy and oversight. Swarm intelligence enables fleets to self-assign patrol zones based on heat-map risk scores, thereby boosting coverage without requiring additional units. Edge computing keeps core threat-detection models local, ensuring that robots continue to function even if cloud links fail a critical specification in disaster response plans.

By Component: Software Drives Lifetime Value

Hardware contributed 58.15% of revenue in 2025, but software and services are climbing at 21.34% CAGR as customers pay subscription fees for analytics, cybersecurity hardening, and predictive maintenance. Commercial security robot market share trends indicate that software revenues will overtake hardware by the end of the decade. AI vision modules can be updated over the air, elevating performance without requiring sensor replacements, which extends asset life cycles.

Open APIs facilitate seamless integration with access control panels, fire alarms, and visitor management kiosks, thereby creating a unified security stack. Cyber-hygiene services patch firmware vulnerabilities before threat actors can hijack robots as moving attack vectors. Predictive-maintenance dashboards use vibration and thermal data to forecast drivetrain failures, scheduling fixes during planned downtime and cutting service calls by 30%. As recurring revenue grows, vendors pivot toward software-as-a-service valuation models favored by investors.

Geography Analysis

North America dominates the commercial security robot market, accounting for 35.85% of the revenue in 2025, thanks to early enterprise pilots and a robust robotics investment pipeline. Major airports and third-party logistics centers validate robots for perimeter patrols and baggage-hall analytics, creating reference success stories that shorten procurement cycles. Venture capitalists cluster around Boston and Silicon Valley, providing startups with rapid prototyping resources and channel partnerships.

Asia-Pacific registers the steepest 19.65% CAGR to 2031, led by government smart-city mandates in China and 5G-enabled test corridors in South Korea. Singapore’s regulatory sandboxes fast-track commercial trials, while Japan subsidizes automation grants to mitigate labor shortages. Regional supply-chain advantages in sensors and printed circuits lower bill-of-material costs, making mid-tier robots price-competitive for smaller property managers.

Europe balances opportunity with regulation: GDPR and the AI Act prolong sales cycles, yet vendors that pass conformity assessments gain a barrier to entry over less-compliant rivals. The Netherlands’ EUR 100 million SecFund channels capital to dual-use security robotics, and Germany’s Industry 4.0 initiatives extend their reach into manufacturing showrooms. Meanwhile, Middle East energy exporters are procuring robots for pipeline surveillance in remote deserts, where human patrols are impractical, illustrating adoption beyond urban centers.

Competitive Landscape

Market concentration is at a moderate level, as established players consolidate their share through multi-year deployment records and vertically integrated service bundles. Knightscope’s public listing in 2024 expanded capital for research and development while sharpening its focus on subscription business models. Boston Dynamics diversified from warehouse picking into security patrols by pairing Stretch logistics robots with Spot inspection units, marketing an end-to-end autonomy suite.

Edge-AI specialists disrupt incumbents by offering form-factor-agnostic software that can retrofit older robots, extending fleet life and reducing lock-in. Traditional guarding firms partner with robotics vendors to bundle technology with on-site personnel for hybrid security contracts, blurring competitive lines. Hardware differentiation is receding as vendors emphasize the accuracy of analytics, the depth of integration, and cybersecurity safeguards over raw sensor counts.

Acquisitions shape the field: Amazon’s attempted purchase of iRobot signaled big-tech appetite for autonomous middleware, even as regulatory scrutiny stalled the deal. Smaller startups pivot toward niche sectors, such as healthcare, education, or maritime, and dodge head-to-head battles with giants. The commercial security robot market rewards providers that can demonstrate reliability across seasons, deliver quantifiable ROI, and navigate a complex patchwork of regional privacy laws.

Commercial Security Robot Industry Leaders

Knightscope, Inc.

Cobalt Robotics, Inc.

SMP Robotics Systems Corp.

Secom Co., Ltd.

Johnson Controls International plc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2024: Boston Dynamics deployed Stretch and Spot at Otto Group’s Hermes Fulfillment centers, combining case handling with patrol duties.

- September 2024: FCF Fox Corporate Finance reported European robotics VC funding fell to EUR 737 million (USD 854.61 million) across 130 deals, signaling maturing investment cycles.

- July 2024: iRobot secured a USD 200 million term loan from The Carlyle Group and renegotiated Amazon’s acquisition price to USD 51.75 per share.

- June 2024: Knightscope completed its IPO and unveiled the K1 Hemisphere robot with 360-degree vision analytics.

Global Commercial Security Robot Market Report Scope

| Wheeled Ground Robots |

| Specialized / Premium Platforms (Legged + Hybrid) |

| Aerial Security Drones |

| Autonomous Marine Surveillance Robots |

| Commercial Buildings |

| Industrial and Logistics Facilities |

| Retail and Shopping Malls |

| Airports and Transportation Hubs |

| Public Infrastructure and Smart City |

| Autonomous |

| Tele-operated |

| Hardware |

| Software and Services |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| South-East Asia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

| By Robot Type | Wheeled Ground Robots | ||

| Specialized / Premium Platforms (Legged + Hybrid) | |||

| Aerial Security Drones | |||

| Autonomous Marine Surveillance Robots | |||

| By End User | Commercial Buildings | ||

| Industrial and Logistics Facilities | |||

| Retail and Shopping Malls | |||

| Airports and Transportation Hubs | |||

| Public Infrastructure and Smart City | |||

| By Autonomy Level | Autonomous | ||

| Tele-operated | |||

| By Component | Hardware | ||

| Software and Services | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| South-East Asia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Egypt | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the size of the commercial security robot market in 2026?

It is valued at USD 4.12 billion and is set to reach USD 9.33 billion by 2031.

Which region leads the adoption of commercial security robots?

North America accounts for 35.85% of 2025 revenue, driven by strong venture funding and early airport deployments.

What robot type is growing fastest?

Aerial security drones are forecast to post a 20.89% CAGR because private 5G enables coordinated multi-drone patrols.

Why do insurers favor robotic guards?

Certified robots cut incident claims, so carriers like Zurich grant 15-25% premium discounts to facilities that deploy them.

What is the main barrier to wider uptake?

High upfront CAPEX, often USD 150,000-500,000 per site, remains the biggest hurdle for mid-sized enterprises.

Page last updated on: