Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

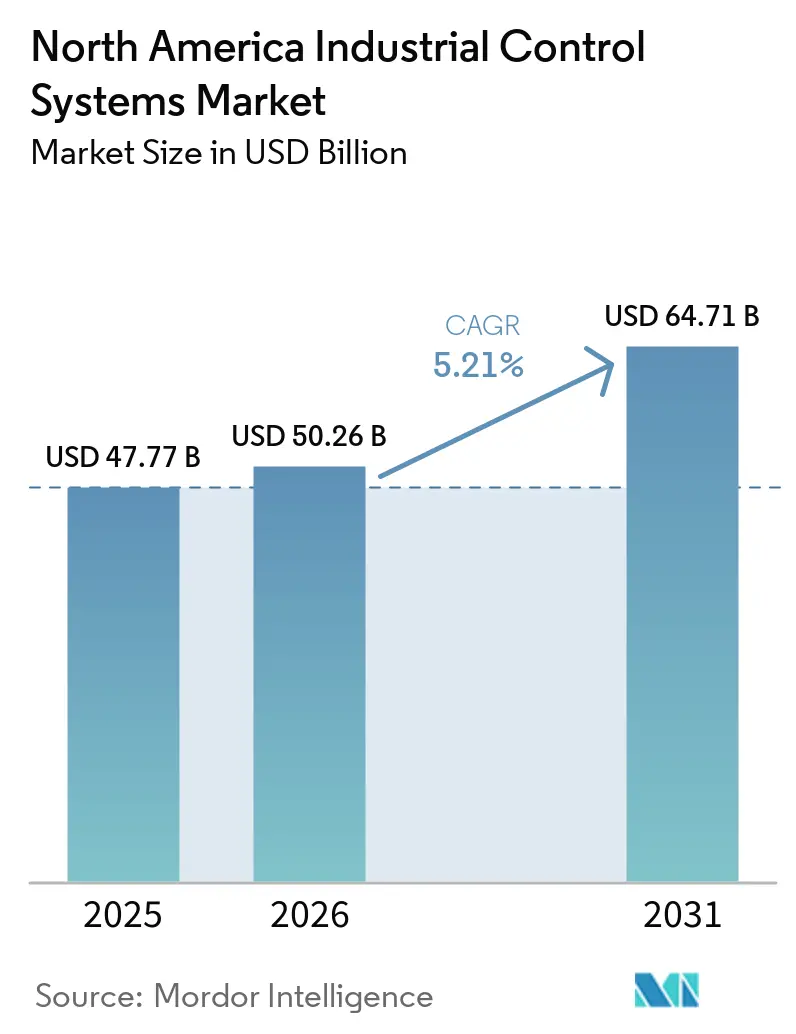

| Base Year Market Size (2025) | USD 47.77 Billion |

| Market Size (2026) | USD 50.26 Billion |

| Market Size (2031) | USD 64.71 Billion |

| Growth Rate (2026 - 2031) | 5.21% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

North America Industrial Control Systems Market Analysis by Mordor Intelligence

The North America Industrial Control Systems Market size was valued at USD 47.77 billion in 2025 and is estimated to grow from USD 50.26 billion in 2026 to reach USD 64.71 billion by 2031, at a CAGR of 5.21% during the forecast period (2026-2031).

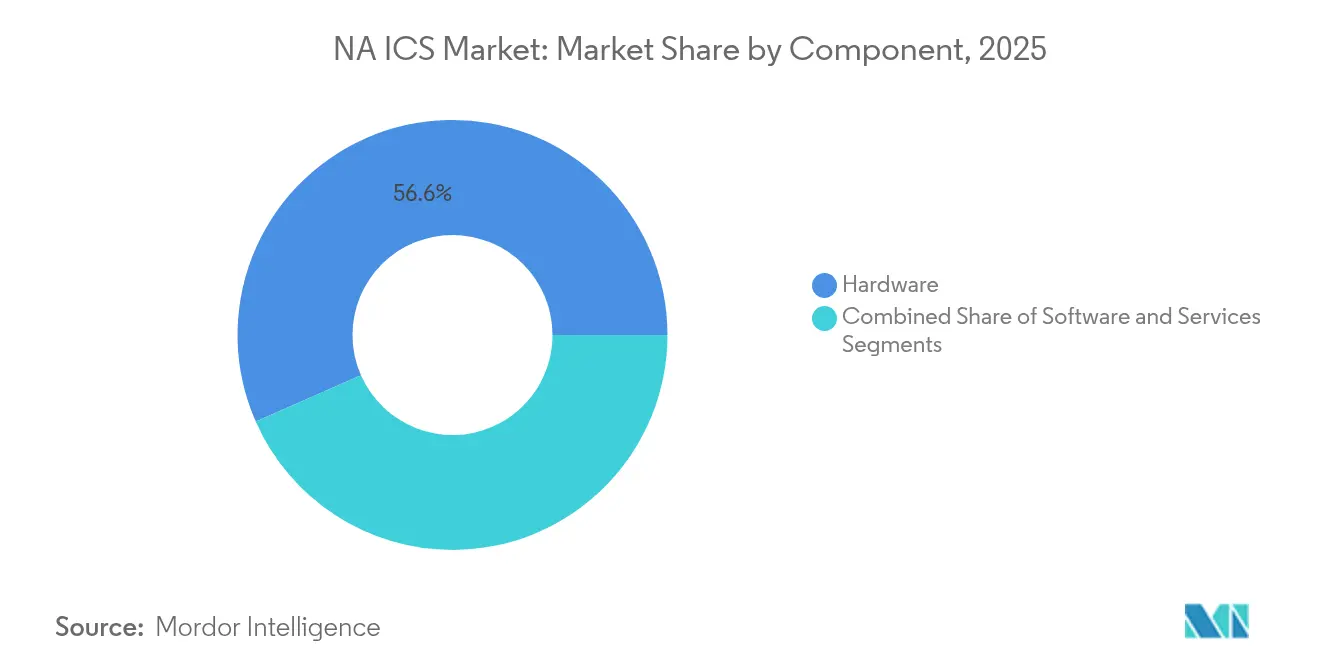

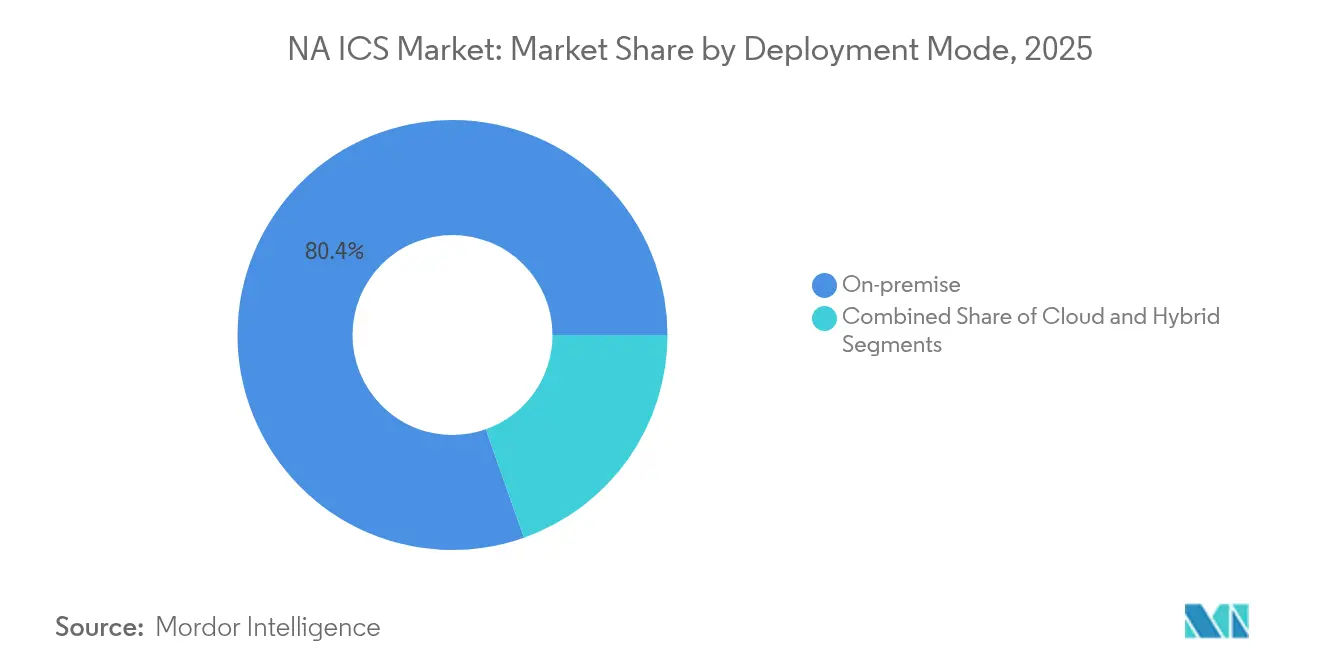

Hardware retains the largest revenue share at 57.2% in 2024, underpinned by steady investment in PLCs, distributed control hardware, and I/O modules. Demand is reinforced by the U.S. CHIPS Act, which has mobilized USD 450 billion of announced semiconductor capacity investments, easing component shortages and spurring new automation roll-outs. Industrial Ethernet accounted for 48.9% of installed communications in 2024, while wireless protocols advanced at a 10.4% CAGR as plants sought flexible connectivity. Although cloud deployments are expanding at 9.31% CAGR, 81% of installations remain on-premise because of latency-sensitive control loops and strict security policies. Automotive producers captured 18.6% of demand, yet pharmaceuticals are the fastest-growing end user at 9.1% CAGR as quality-by-design mandates intensify.

Key Report Takeaways

- By component, hardware led with 56.60% revenue share in 2025; the services segment is forecast to expand at an 8.35% CAGR through 2031.

- By type of system, PLCs held 30.85% of the North America ICS market share in 2025, while MES is poised for a 7.15% CAGR to 2031.

- By communication protocol, industrial Ethernet dominated with 48.25% share in 2025; wireless is on track for a 9.85% CAGR.

- By deployment mode, on-premise installations controlled 80.40% of the North America industrial control systems (ISC) market size in 2025, whereas cloud deployments are rising at 8.78% CAGR.

- By end-user industry, automotive led with 18.15% revenue share in 2025; pharmaceuticals are projected to grow at a 8.62% CAGR.

- By geography, the United States commanded 63.70% of 2025 revenue; Mexico is the fastest-growing country at a 7.36% CAGR.

- ABB, Siemens, Rockwell Automation, and Honeywell jointly captured about 39.5% of 2025 revenue in the North America industrial control systems market.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

North America Industrial Control Systems Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Accelerated Brown-Field Modernization across U.S. Automotive Plants | 1.9% | United States, with concentration in Michigan, Ohio, Tennessee | Medium term (2-4 years) |

| Growing Cyber–physical Safety Standards (ISA/IEC 62443) Adoption | 1.4% | Global, with strongest adoption in United States and Canada | Medium term (2-4 years) |

| U.S. CHIPS Act–fuelled Semiconductor Capacity Build-out | 1.6% | United States, with spillover benefits to Canada and Mexico | Long term (≥ 4 years) |

| Canada's Net-Zero Grid Mandate Driving Utility Automation | 1.1% | Canada, with concentration in Ontario, Quebec, British Columbia | Long term (≥ 4 years) |

| Rising Mid-stream LNG Investments in Gulf Coast | 0.8% | United States (Texas, Louisiana) | Medium term (2-4 years) |

| Edge-enabled Predictive Maintenance Roll-outs in Mexican OEMs | 0.5% | Mexico, with concentration in automotive manufacturing hubs | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Accelerated brown-field modernization across U.S. automotive plants

Automotive manufacturers are replacing fragmented control layers with unified architectures to boost flexibility and uptime. Audi’s U.S. body shop adopted Siemens Simatic S7-1500V virtual controllers connected to its private cloud, merging IT and OT workflows and shortening change-over times. Only 31% of domestic factories have fully automated a function, highlighting large headroom for modernization. Kimberly-Clark’s phased PLC-to-DCS migration illustrates the cautious pace: one line per year over a decade to limit downtime while embedding cybersecurity-ready platforms.[1]Matthew DiDominica & Clare Lau, “Rockwell Automation,” Notre Dame Investment Club, investmentclub.nd.edu

Growing cyber-physical safety standards adoption

Ninety-three percent of OT facilities reported an intrusion in the past 12 months, prompting rapid uptake of ISA/IEC 62443 frameworks that define zones, conduits, and continuous monitoring. The February 2025 ANSI/ISA-62443-2-1 update introduced a maturity model, allowing asset owners to tailor controls to risk profiles. Utilities and discrete manufacturers alike are structuring multi-layer defenses, reducing unplanned outages and insurance premiums.

U.S. CHIPS Act-fuelled semiconductor capacity build-out

More than USD 450 billion of announced wafer-fab projects across 28 states is set to triple domestic chip output within a decade, easing shortages of mature-node MCUs vital for drives and I/O cards. TSMC is investing USD 100 billion in three Arizona fabs and two advanced-packaging sites, while the National Semiconductor Technology Center coordinates joint R&D. Capital expenditure on U.S. fabs rose 40% post-Act, anchoring a resilient component supply chain for the North America ICS market.

Canada’s net-zero grid mandate driving utility automation

Ottawa’s January 2025 Clean Electricity Strategy calls for 140-190 GW of new clean generation by 2050, effectively doubling current capacity. Utilities are digitising substations, deploying synchrophasors, and integrating distributed energy resources. Hydro Ottawa’s 2021-2025 roadmap accelerates digital platforms to orchestrate virtual power plants and demand response. These initiatives lift control-system spending in generation, transmission, and distribution assets.

Restraints Impact Analysis*

| RESTRAINTS | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Legacy Brown-field Systems with Proprietary Protocol Lock-in | -1.1% | United States, Canada, with highest impact in mature industrial regions | Long term (≥ 4 years) |

| Capital-intensive Retrofit Costs for OSHA Functional-Safety | -0.8% | United States, with spillover impact to Canada | Medium term (2-4 years) |

| Shortage of ISA-Certified OT-Cybersecurity Workforce | -0.7% | Global, with acute impact in United States and Canada | Medium term (2-4 years) |

| North American Supply-Chain Exposure to Rare-earth Magnet Imports | -0.5% | United States, Canada, Mexico, with highest impact on automotive and renewable energy sectors | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Legacy brown-field systems with proprietary protocol lock-in

Plants built in the 1990s still rely on vendor-specific buses that complicate data acquisition and cloud connectivity. Phoenix Contact advises staged I/O migration to minimise shutdowns, yet integration crews must map thousands of legacy registers to modern object models—an effort that prolongs project timelines and inflates labor costs. Wood PLC notes that process-site lifecycles of 30 years make wholesale replacement impractical, obliging owners to fund dual-stack architectures for years.[2]Phoenix Contact, “Migration from Old Plants to New,” phoenixcontact.com

Capital-intensive retrofit costs for OSHA functional-safety

Upgrading to SIL-rated logic solvers and adding redundant sensors represent multi-million-dollar outlays that smaller manufacturers often defer. NEMA’s maintenance guidelines emphasise scheduled verification but warn that deferred retrofits heighten unplanned downtime risk. Public transport operators echo similar challenges: APTA’s OT maturity framework shows many agencies remain at Level 1 due to budget constraints, leaving gaps in zoning and incident response. Limited capital envelopes slow the refresh cycle in the North America industrial control systems market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Hardware retains dominance while services gain momentum

Hardware contributed 56.60% of 2025 revenue, led by sustained orders for PLC racks, DCS nodes, and motor drives. ABB’s Process Automation unit posted USD 6.8 billion of 2024 sales, showing continued appetite for capital equipment. Integration of edge analytics into controllers, such as Honeywell’s ControlEdge PLC with embedded OPC UA and MQTT, is boosting sell-through of premium SKUs.

Services, though smaller, are scaling rapidly at 8.35% CAGR as owners outsource lifecycle support. Rockwell Automation’s Lifecycle Services backlog reached USD 1.70 billion in September 2024, reflecting demand for outcome-based contracts that tie fees to availability gains. Skills shortages, 3.5 million cybersecurity roles lacking by 2025, push maintenance and remote-monitoring agreements higher, elevating recurring revenue in the North America industrial control systems industry.

By Type of System: PLCs maintain leadership while MES links the digital thread

PLCs held 30.85% of the North America industrial control systems (ICS) market size in 2025, valued for deterministic control and proven reliability. Rockwell’s Logix controller family anchors automotive and food lines across the region. Vendors now ship PLCs with native CIP-Security and TLS encryption, reducing gateway dependencies.

MES platforms are expanding at 7.15% CAGR as manufacturers seek lot-level genealogy and order-to-batch synchronisation. Industry 4.0 roll-outs nearly doubled connected devices to 17 billion globally in 2024, creating data sets that MES converts into actionable production KPIs. Automotive OEMs use MES to coordinate robotic paint, battery assembly, and final inspection, shortening launch cycles and connecting enterprise resource planning.

By Communication Protocol: Industrial Ethernet extends reach, wireless accelerates flexibility

Industrial Ethernet captured 48.25% market share in 2025, propelled by Gigabit-capable cabling and TSN upgrades that deliver nanosecond-level determinism to motion loops. Vendors add software-defined segmentation to stop lateral malware movement, an emerging must-have as IT and OT converge.

Wireless traffic is forecast to rise 9.85% CAGR as private 5G and Wi-Fi 6E enable mobile cobots, AGVs, and condition-monitoring sensors. Chemical producers deploy ISA100-compliant devices in hazardous zones to avoid costly conduit runs. Predictive-maintenance programs in Mexico leverage wireless gateways at stamping presses to stream vibration spectra into cloud models, reducing mean-time-to-repair.

By Deployment Mode: On-premise dominates, cloud scales analytics workloads

On-premise architectures represented 80.40% of installations in 2025, reflecting operator preference for deterministic latency and physical control of safety I/O. High-availability edge servers now host AI algorithms locally, trimming inference delays. MachineMetrics’ edge appliance, for example, normalises OPC and proprietary PLC data in-plant before exporting compressed time-series to Azure for asset benchmarking.

Cloud control-system instances, though only 19.60% today, are expanding at 8.78% CAGR. Siemens’ virtual PLC running on Audi’s Edge Cloud 4 production proves that additive workloads, twin modelling, scheduling, SPC, can migrate first, leaving real-time loops onsite. Vendors bundle zero-trust gateways and PKI to satisfy pharmaceutical GMP data-integrity rules, easing CIO concerns.

By End-user Industry: Automotive leads, pharmaceuticals grow on compliance rigor

Automotive producers retained 18.15% revenue share in 2025, bolstered by EV platform launches that need reconfigurable body-in-white lines. BMW and GM apply machine-learning vision to detect weld-bead defects in milliseconds, lifting first-time-through quality. AI-assisted torque control also trims rework costs.

Pharmaceutical plants, the fastest-growing end user at 8.62% CAGR, invest in continuous manufacturing skids and electronic batch records. Control-system vendors ship pre-validated libraries that support CFR Part 11 audit trails and Annex 11 electronic signatures. Personalised-medicine batches require agile recipe handling, elevating MES-DCS integration spend across the North America industrial control systems market.

Geography Analysis

The United States captured 63.70% of 2025 revenue, supported by a USD 450 billion semiconductor build-out and an influx of reshored manufacturing jobs that doubled between 2017 and 2023. Rockwell Automation’s filings confirm the country remains its largest sales territory, outpacing international regions. However, legacy system lock-in and an estimated 2 million unfilled industrial jobs by 2029 threaten project throughput.

Canada ranks second, energised by a national net-zero grid target that mandates 140-190 GW of new clean generation and heavy investment in substation automation. Hydropower additions such as the Site-C project and digital retrofits at existing dams sustain hardware orders. Provincial utilities deploy synchrophasor-based wide-area control and fault location isolation systems that rely on deterministic Ethernet backbones.

Mexico is the fastest-growing geography with a 7.36% CAGR as near-shoring drives record automotive line installations. Edge computing spend is rising, with global outlays projected to reach USD 378 billion by 2028, and Mexican plants adopt predictive-maintenance apps that cut unscheduled downtime. Adoption gaps persist across Tier-2 suppliers, prompting public-private workforce programs to lift digital-skill density.

Competitive Landscape

The sector is moderately concentrated; ABB, Siemens, Rockwell Automation, and Honeywell jointly held about 40% of 2024 revenue, reflecting a balanced field where no player dominates. Rockwell focuses on its Connected Enterprise platform, integrating control, visualization, and cybersecurity services to protect installed bases. ABB expands modular systems with edge-ready universal I/O to shorten brown-field cutovers.

Siemens pursues software-defined automation, evidenced by the Audi deployment that demonstrates virtualised PLCs running on standard servers. Honeywell captures hybrid and process sites with controllers that embed MQTT and OPC UA to streamline multi-vendor data flow.

Digital differentiation is intensifying. Emerson’s May 2025 launch of generative-AI plant-layout tools positions it against pure-play industrial software providers. M&A appetite is expected to rise as firms pursue analytics, OT-security, and 5G capabilities, reinforcing the position of full-suite vendors in the North America industrial control systems market.

North America Industrial Control Systems Industry Leaders

Rockwell Automation Inc.

Siemens AG

Honeywell International Inc.

ABB Ltd.

Schneider Electric SE

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Emerson unveiled an expanded AI portfolio, including AspenTech Optiplant AI Equipment Layout and DeltaV Revamp, to accelerate autonomous operations for manufacturers.

- March 2025: Siemens and Audi partnered to deploy Simatic S7-1500V virtual controllers on Audi’s Edge Cloud 4 Production platform.

- February 2025: ISA released ANSI/ISA-62443-2-1-2024, adding a maturity-model structure to the cyber-physical security standard.

- January 2025: Canada published its Clean Electricity Strategy outlining steps toward a net-zero grid by 2050.

North America Industrial Control Systems Market Report Scope

Industrial control systems include supervisory control and data acquisition systems used to control geographically dispersed assets, as well as distributed control systems and smaller control systems that use programmable logic controllers to control localized processes. The report provides a detailed account of qualitative and quantitative findings across various market segments and geographies. North America Industrial Control Systems Market is segmented by type of system (SCADA (Supervisory Control and Data Acquisition), DCS ( Distributed Control Systems), PLC (Programmable logic controller), MES (Machine Execution Systems), PLM (Product Lifecycle Management ), ERP (Enterprise Resource Planning), HMI (Human Machine Interface), Others (Operator Training Simulators, Machine Safety Systems)), End-user (Automotive, Chemical & Petrochemical, Utilities, Pharmaceutical, Food & Beverage, Oil & Gas, Others) and Country.

By Component

| Hardware |

| Software |

| Services |

By Type of System

| SCADA (Supervisory Control and Data Acquisition) |

| DCS (Distributed Control Systems) |

| PLC (Programmable Logic Controller) |

| MES (Manufacturing Execution Systems) |

| PLM (Product Lifecycle Management) |

| ERP (Enterprise Resource Planning) |

| HMI (Human Machine Interface) |

| Others (OTS, Machine-safety) |

By Communication Protocol

| Fieldbus |

| Industrial Ethernet |

| Wireless |

By Deployment Mode

| On-premise |

| Cloud |

| Hybrid |

By End-user Industry

| Automotive |

| Chemical and Petrochemical |

| Utilities (Power and Water) |

| Pharmaceutical |

| Food and Beverage |

| Oil and Gas |

| Mining and Metals |

| Pulp and Paper |

| Others |

By Country

| United States |

| Canada |

| Mexico |

| By Component | Hardware |

| Software | |

| Services | |

| By Type of System | SCADA (Supervisory Control and Data Acquisition) |

| DCS (Distributed Control Systems) | |

| PLC (Programmable Logic Controller) | |

| MES (Manufacturing Execution Systems) | |

| PLM (Product Lifecycle Management) | |

| ERP (Enterprise Resource Planning) | |

| HMI (Human Machine Interface) | |

| Others (OTS, Machine-safety) | |

| By Communication Protocol | Fieldbus |

| Industrial Ethernet | |

| Wireless | |

| By Deployment Mode | On-premise |

| Cloud | |

| Hybrid | |

| By End-user Industry | Automotive |

| Chemical and Petrochemical | |

| Utilities (Power and Water) | |

| Pharmaceutical | |

| Food and Beverage | |

| Oil and Gas | |

| Mining and Metals | |

| Pulp and Paper | |

| Others | |

| By Country | United States |

| Canada | |

| Mexico |

Key Questions Answered in the Report

What is the size of the North American industrial control systems market in 2026?

It is valued at USD 50.26 billion, with a forecast CAGR of 5.21% through 2031.

Which component category leads the market?

Hardware leads with 56.60% revenue share, driven by ongoing PLC and DCS upgrades.

Why are on-premise installations still prevalent?

Latency-sensitive loops and stringent cybersecurity requirements keep 80.40% of deployments on-site.

Which end-user industry is expanding fastest?

Pharmaceutical manufacturing is growing at 8.62% CAGR due to strict quality and traceability rules.

How is the CHIPS Act influencing control-system demand?

USD 450 billion of fab investments is easing semiconductor shortages, enabling faster automation roll-outs.

What are the main cybersecurity standards adopted in North America?

ISA/IEC 62443 frameworks are gaining traction, offering zone-based defense models across industrial sites.

Page last updated on: