Indonesia Payments Infrastructure Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

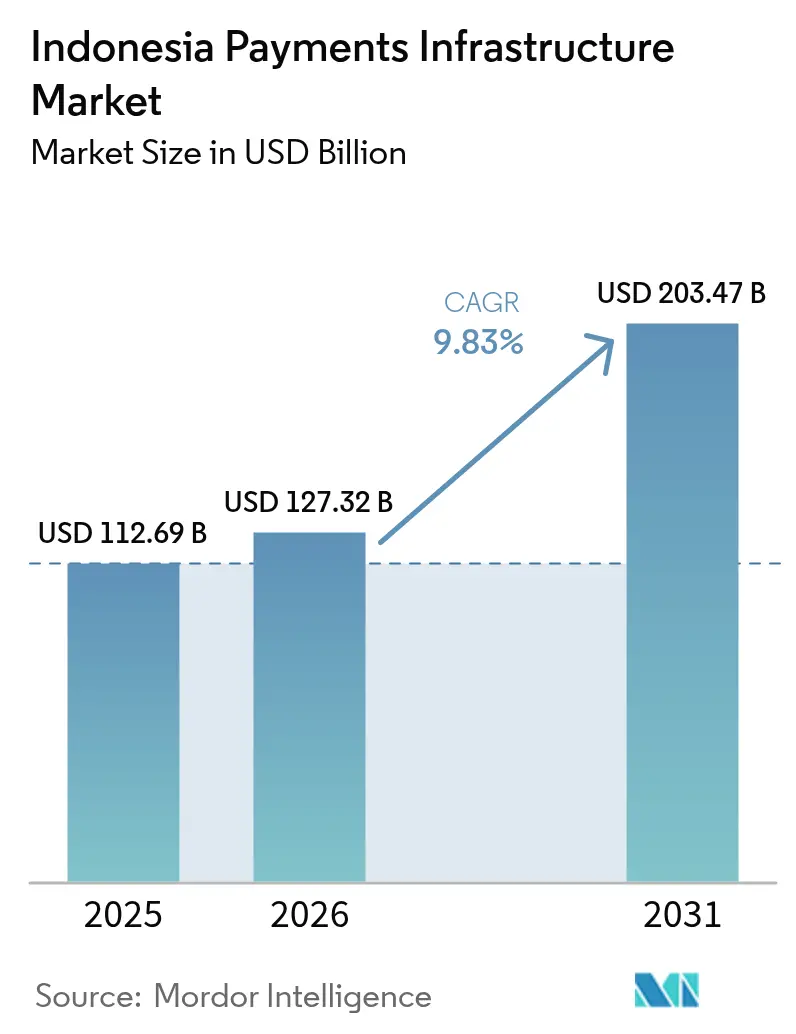

| Base Year Market Size (2025) | USD 112.69 Billion |

| Market Size (2026) | USD 127.32 Billion |

| Market Size (2031) | USD 203.47 Billion |

| Growth Rate (2026 - 2031) | 9.83% CAGR |

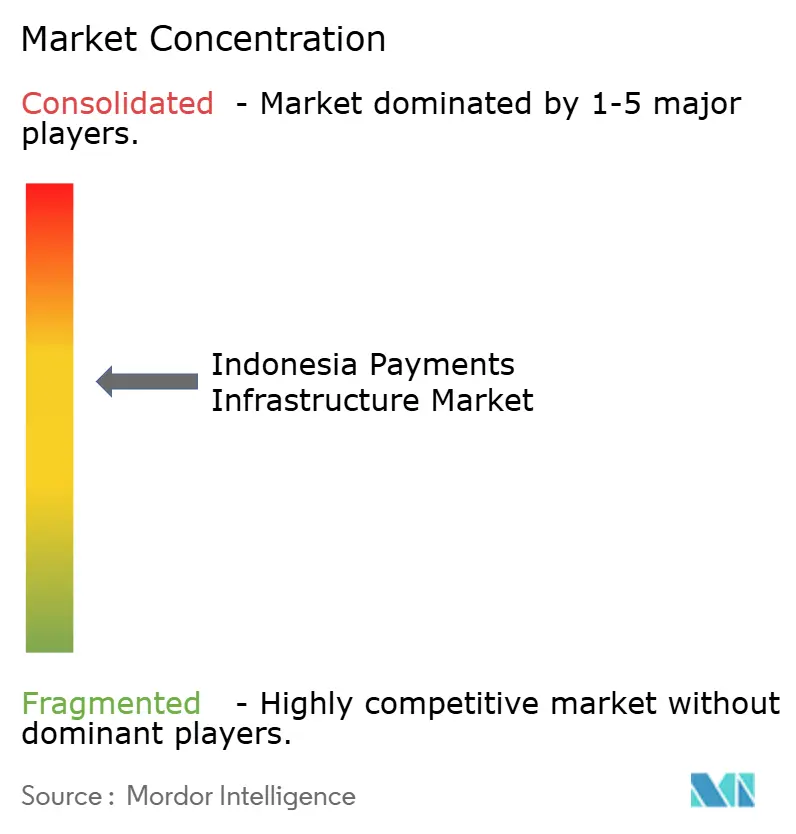

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Indonesia Payments Infrastructure Market Analysis by Mordor Intelligence

The Indonesia payments infrastructure market size is expected to increase from USD 112.69 billion in 2025 to USD 127.32 billion in 2026 and reach USD 203.47 billion by 2031, growing at a CAGR of 9.83% over 2026-2031. The steep growth curve mirrors accelerating QRIS merchant adoption, rapid uptake of the BI-FAST real-time rail, and a structural pivot from hardware to cloud-native orchestration. Super-app ecosystems keep embedding wallets into ride-hailing, e-commerce, and food-delivery flows, reinforcing e-money as the preferred consumer instrument. Foreign acquirers armed with Android-based POS devices continue to compress merchant discount rates and intensify platform consolidation. Telecom investments under the Palapa Ring program, together with cross-border QR operability, are expanding the Indonesia payments infrastructure market’s geographic reach into outer-island economies while supporting inbound tourism spend.

Key Report Takeaways

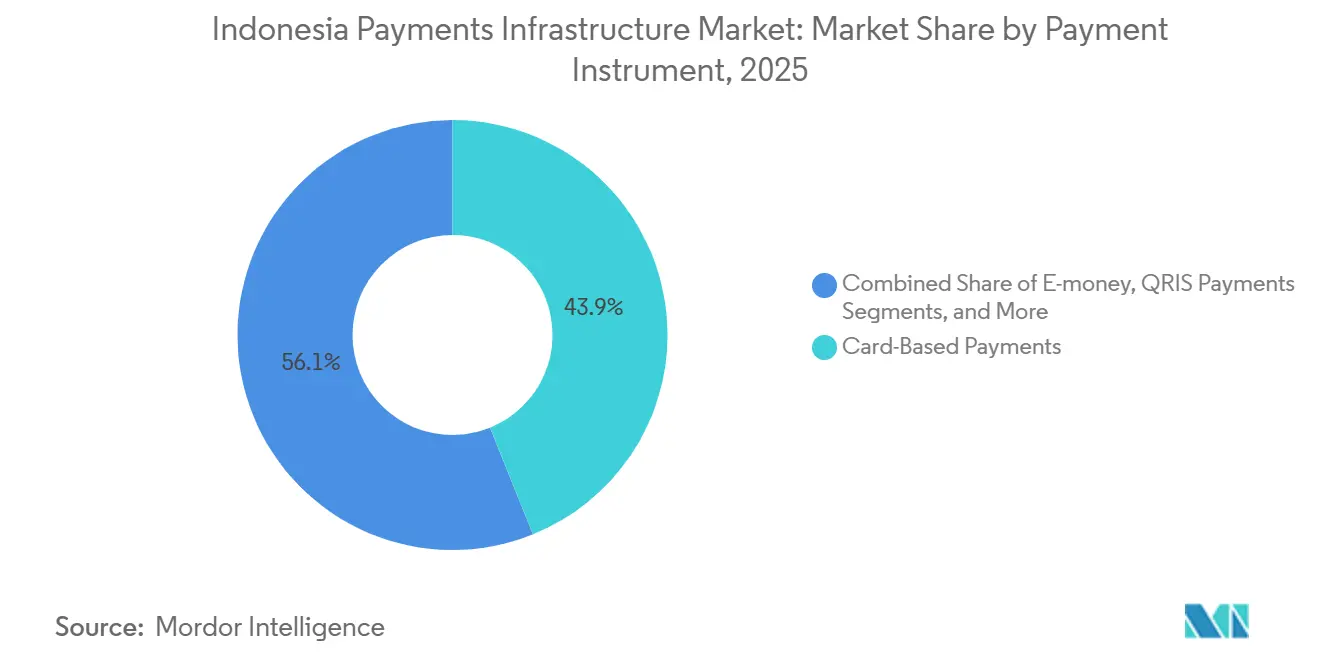

- By payment instrument, Card-based payments led with 43.89% of the Indonesia payments infrastructure market share in 2025, whereas e-money is advancing at an 11.21% CAGR through 2031.

- By component, Software and platform solutions commanded 58.67% of the Indonesia payments infrastructure market size in 2025 and remain the fastest-growing component at a 9.92% CAGR to 2031.

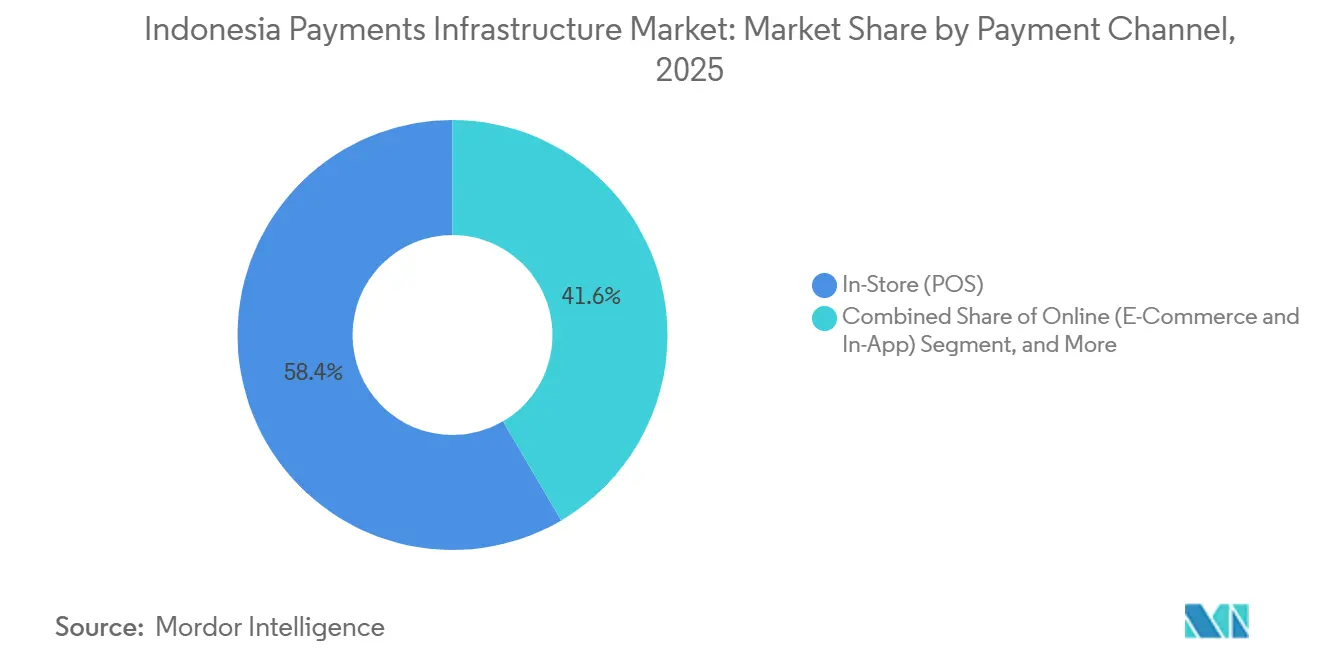

- By channel, In-store point-of-sale channels accounted for 58.43% of the Indonesia payments infrastructure market size in 2025; online and in-app channels are expanding at a 10.43% CAGR through 2031.

- By merchant vertical, Retail and grocery captured 32.92% of end-user spending in 2025, while transportation and mobility is forecast to grow at an 11.02% CAGR, the quickest among verticals.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Indonesia Payments Infrastructure Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Government Push for QRIS Unified QR Code Accelerating Merchant Acceptance | +2.8% | National, with highest density in Java, Bali, and Sumatra; expanding to Kalimantan and Sulawesi | Short term (≤ 2 years) |

| Rapid Expansion of Domestic Real-Time Payment Rail BI-FAST Boosting Bank-Fintech Integrations | +2.3% | National, concentrated in urban centers; spillover to outer islands via mobile-banking apps | Medium term (2-4 years) |

| Increasing Mobile Wallet Adoption Among Unbanked Population in Outer Islands | +1.9% | Outer islands (Papua, Maluku, Nusa Tenggara), Eastern Indonesia provinces | Medium term (2-4 years) |

| Rising Foreign Investment in Indonesia's O2O Payments Acquiring Market | +1.4% | Java and Bali (Jakarta, Surabaya, Bandung, Denpasar); selective expansion to Medan and Makassar | Short term (≤ 2 years) |

| Migration of Government Social Disbursements to Digital Channels in Eastern Indonesia | +0.9% | Eastern Indonesia (Papua, Maluku, Nusa Tenggara Timur); pilot programs in Banyuwangi, East Java | Long term (≥ 4 years) |

| Growth of Embedded Finance Use-Cases in Agritech Cooperatives | +0.5% | Rural Java, Sumatra, and Sulawesi; agricultural cooperatives in Central Java and South Sulawesi | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Government Push for QRIS Unified QR Code Accelerating Merchant Acceptance

Bank Indonesia’s mandate requiring universal QRIS adoption collapsed fragmented proprietary codes into a single rail, cutting merchant friction and turning quick-response payments into the default tender across traditional markets and micro-enterprises.[1]Bank Indonesia, “Regulation 4/2025 on Payment System Governance,” BI.GO.ID Enrollment exceeded 40 million merchants by August 2025, and cross-border operability with Malaysia, Thailand, Singapore, and Japan deepened acceptance for inbound tourism spend. Static and dynamic QR codes now clear within 24 hours, easing working-capital strain for small traders. Merchant discount rates below 0.7% undercut card interchange, hastening cash displacement in food-and-beverage and convenience formats. The uniform code means providers must now compete on loyalty, lending, and embedded services rather than acceptance footprint.

Rapid Expansion of Domestic Real-Time Payment Rail BI-FAST Boosting Bank-Fintech Integrations

BI-FAST processed 1.22 billion transfers worth IDR 3,024 trillion in 3Q-2025, a 32.34% year-over-year lift, evidencing swift migration away from batch-clearing SKNBI. The flat IDR 2,500 fee structure incentivizes corporates to shift payroll and supplier payouts from costlier RTGS channels. Fintech gateways such as Xendit and OY! Indonesia integrated the rail to offer merchants sub-second settlement, shrinking fraud exposure windows and strengthening cash-flow predictability.[2]Reuters Staff, “Licensing Challenges for Cross-Border Wallets,” REUTERS.COM Always-on availability aligns with the mobile-first consumer base, 70% of whose digital spending occurs outside branch hours. As mid-tier banks onboard through 2026, real-time ubiquity will further cement the Indonesia payments infrastructure market’s transition to instant value movement.

Increasing Mobile Wallet Adoption Among Unbanked Population in Outer Islands

Indonesia reported 439.4 million e-money accounts in September 2024, yet branch penetration in Papua and Maluku remains under five per 100,000 adults. Wallets circumvent physical infrastructure, leveraging agent networks from Payfazz and BRI Agen to furnish cash-in and cash-out points in remote villages. Government transfer programs now top-up wallets directly, advancing financial inclusion while cutting leakages. The Palapa Ring expansion lowered mobile-data costs, enabling wallet functionality even in previously offline areas. Super-apps GoPay and ShopeePay are racing to seed these territories, using loyalty incentives to lock in first-mover advantage.

Rising Foreign Investment in Indonesia’s O2O Payments Acquiring Market

Xendit’s USD 300 million Series D led by Coatue and Tiger Global validated Indonesia as a regional hub for API-based acquiring. Pine Labs, Fiserv, and Worldline’s Ingenico unit have rolled out Android POS terminals that natively accept QRIS, tokenized cards, and BI-FAST, trimming merchant costs to as low as 0.5%.[3]Pine Labs, “POS Terminal Deployment in Indonesia,” PINELABS.COM As foreign capital chases urban scale, local acquirers respond by bundling inventory and analytics modules, but thinner discount rates are already triggering consolidation. The capital influx also accelerates geographic reach, with new entrants targeting Medan and Makassar after saturating Java-Bali corridors.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Inter-Island Telecom Infrastructure Gaps Limiting Latency-Sensitive Transactions | -1.2% | Outer islands (Papua, Maluku, Nusa Tenggara), remote areas in Kalimantan and Sulawesi | Medium term (2-4 years) |

| Fragmented Regulatory Oversight Between BI and OJK Complicates Licensing Timelines | -0.9% | National, affecting cross-border entrants and new fintech licensees | Short term (≤ 2 years) |

| High Merchant Attrition Due to Price Wars Among Acquirers | -0.6% | Java and Bali urban centers, competitive metro markets | Short term (≤ 2 years) |

| Limited Consumer Trust Outside Java in Card-Not-Present Transactions | -0.4% | Outer islands, rural Sumatra, Kalimantan, Sulawesi | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Inter-Island Telecom Infrastructure Gaps Limiting Latency-Sensitive Transactions

Despite 4G coverage reaching 90% of the archipelago, satellite backhaul still introduces 300-500 ms delays in Papua and Maluku, clashing with BI-FAST’s sub-100 ms requirement.[4]Ministry of Communication and Informatics, “Palapa Ring Fiber-Optic Project Update,” KOMINFO.GO.ID Timeout rates of up to 12% force merchants to revert to cash, stalling digital uptake where it is needed most. The government allocated IDR 15 trillion in 2025 for undersea cables, but completion is slated for 2027, leaving a near-term gap that tempers the Indonesia payments infrastructure market’s outer-island growth trajectory. Wallet providers must therefore maintain hybrid offline modes and agent cash-points to retain user trust until fiber reaches critical mass.

Fragmented Regulatory Oversight Between BI and OJK Complicates Licensing Timelines

BI for rail connectivity and OJK for e-money or BNPL licensing. Capital reserve duplication IDR 100 billion per license extends market entry to 18 months, deterring smaller cross-border players. POJK 32/2025 further demands 5% loan-loss buffers and caps BNPL rates at 0.5% per month, tightening the compliance vise. Absent a unified sandbox, innovators shoulder duplicated audit and security-testing costs, slowing the Indonesia payments infrastructure market’s ability to absorb novel propositions quickly.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Payment Instrument: E-Money Strengthens Its Lead

Card-based payments still generated 43.89% of 2025 volume, but e-money outpaced every other instrument, expanding at an 11.21% CAGR that will reshape the Indonesia payments infrastructure market size at the instrument level. QRIS standardization lowers acceptance costs for merchants that once balked at interchange fees, while super-apps reinforce switching costs through cashback and loyalty currencies. Real-time BI-FAST transfers continue to cannibalize legacy batch channels, especially for corporate disbursements that value flat fees over tiered RTGS pricing. Tokenized cards, mandated for card-not-present safety, are gaining share but remain a secondary option behind wallets for small-ticket purchases.

Mobile wallets already hold an outsized mindshare in urban Gen-Z cohorts, yet the unbanked population in Papua and Maluku is where incremental upside lies. Agent networks transform kiosks into cash-in points, enabling the Indonesia payments infrastructure market to bridge the last-mile gap. Wallet-to-wallet remittances routed through QRIS cut corridor fees, appealing to migrant workers in Malaysia and Singapore who remit home via Dana. With network effects compounding, e-money’s share of the Indonesia payments infrastructure market size could surpass cards well before 2031.

By Component: Software Platforms Command Investment Momentum

Software solutions captured 58.67% of component revenue in 2025 and are growing at 9.92% through 2031, as merchants demand single-API gateways that reconcile QRIS, BI-FAST, tokenized cards, and BNPL. Xendit’s multicurrency orchestration layer can on-board a merchant in three days, displacing hardware-centric integrators. The Indonesia payments infrastructure industry consequently channels capex from POS terminals toward cloud orchestration that pushes updates in real time.

Hardware retains a resilient niche among grocers and petrol stations that require tactile inputs and compliance-tested devices. Ingenico and PAX Technology have transformed Android terminals into multi-service hubs hosting loyalty, inventory, and tax modules. Managed services, including security audits and mandatory annual penetration testing under Regulation 4/2025, underpin recurring revenue streams for switching networks Artajasa and Finnet. This hybrid model highlights how the Indonesia payments infrastructure market share of software could rise further as merchants prioritize fast deployment and breadth of payment options.

By Payment Channel: Online and In-App Transactions Surge

Brick-and-mortar registers still processed 58.43% of payments in 2025, but omnichannel experiences are pushing merchants to fuse their physical and digital checkout infrastructure. E-commerce platforms Tokopedia and Shopee now auto-embed BNPL, propelling average-order values and sustaining a 10.43% CAGR in online spend. High-value online bookings also benefit from tokenized card security, soothing consumer worries about fraud.

POS lanes are not relinquishing relevance; QRIS has trimmed checkout times for fast-food chains by 50%, while Android POS terminals now support offline mode for regions with patchy connectivity. Cloud registers from Moka POS synchronize inventory and rewards across channels, ensuring that the Indonesia payments infrastructure market can address consumers wherever they choose to transact. The convergence underscores a future where channel distinctions blur, but data unification becomes a competitive moat.

By End-User Vertical: Transportation and Mobility Accelerate

Retail and grocery led spending with 32.92% of 2025 value, thanks to nationwide mini-market chains accepting every digital tender. Still, transportation and mobility is advancing at an 11.02% CAGR as Gojek, Grab, and Blue Bird digitize ride, food, and parcel payments. Closed-loop wallets inside these super-apps lock riders into frictionless payment loops and stimulate adjacent spending such as ticketing and tolls.

Hospitality and travel have leaned into tokenized card mandates, boosting confidence for inbound tourists who increasingly scan QRIS to settle bills. Agriculture cooperatives using BI-FAST for harvest payouts evidence embedded finance momentum in rural economies. By collapsing multi-week cash cycles into same-day transfers, the Indonesia payments infrastructure market enables new vertical use-cases that broaden overall addressable volume.

Geography Analysis

Java anchors the Indonesia payments infrastructure market, housing 60% of QRIS-enabled merchants and the bulk of venture-funded fintech headquarters. Jakarta’s deep consumer wallet penetration catalyzes innovation that later permeates Bandung and Surabaya. Bali’s tourist-centric merchants adopted cross-border QR early, facilitating frictionless payments for Japanese, Malaysian, and Thai visitors, and now expect India’s UPI link to swell volumes further. Sumatra’s Medan and Palembang show quick wallet uplifts as agent networks bridge banking gaps. Mobile broadband costs continue to fall post-Palapa Ring, expanding digital bandwidth for small merchants.

Kalimantan and Sulawesi capitalize on embedded finance for commodity supply chains. Smallholder farmers receive input financing via fintech apps that disburse through BI-FAST, expediting working-capital loops. Nusa Tenggara’s Bali-adjacent economies benefit from QRIS spillovers, while Lombok’s hotel clusters implement tokenized card acceptance to mitigate chargeback risks. Banyuwangi’s GovTech pilot shows how municipal tax payments can migrate to real-time rails, offering a replicable template for resource-strained districts.

Papua and Maluku remain latency-constrained. Merchants still report frequent timeouts, limiting the Indonesia payments infrastructure market’s penetration despite high smartphone ownership. The IDR 15 trillion undersea-cable plan aims to cut network round-trip times below 50 ms by 2027. Once fiber arrives, wallet providers forecast a quick inflection as social-assistance transfers and migrant remittances pivot from cash to QRIS and BI-FAST rails.

Competitive Landscape

Competition is moderate, with the top five wallets holding roughly 60% of 2025 e-money volume but a long tail of specialist acquirers, switch networks, and gateways holding discrete value-chain niches. Xendit’s Series D boosted its firepower to extend multicountry orchestration, intensifying pressure on legacy acquirers reliant on proprietary switch fees. Foreign entrants Pine Labs and Fiserv compress discount rates to 0.5-1.0%, obliging domestic players GHL and Cashlez to layer analytics and inventory modules into their offers.

Infrastructure operators Jalin, Artajasa, and Finnet face BI-FAST fee disruption and therefore pivot to managed compliance services, supporting mid-tier banks lacking cyber talent. Super-apps leverage closed-loop ecosystems to extend beyond payments into credit, insurance, and wealth management, widening user stickiness and data moats. Smaller contenders Payfazz and MC Payment fill last-mile gaps in Papua and Maluku through agent kiosks that convert cash to wallet top-ups, securing flows overlooked by urbancentric rivals.

Fraud prevention has emerged as a key battleground. Midtrans deploys sub-200 ms machine-learning checks, a regulatory requirement for processors exceeding 10 million monthly transactions. BNPL players Kredivo and Akulaku, newly regulated under POJK 32/2025, must hold 5% loan-loss reserves, crystallizing a high-capital moat that freezes out underfunded challengers. By 2027, analysts expect 10-15 scaled platforms to control the lion’s share of the Indonesia payments infrastructure market as price wars and regulatory burdens force smaller firms to exit or merge.

Indonesia Payments Infrastructure Industry Leaders

Xendit

Olsera.com

Edgeworks Solutions Pte Ltd

PT Cashlez Worldwide Indonesia

PT Finnet Indonesia

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: Bank Indonesia expanded QRIS interlinkage to India’s UPI network, granting Indonesian merchants access to 400 million potential payers.

- December 2025: OJK issued POJK 32/2025 that formalizes BNPL licensing, caps monthly interest at 0.5%, and mandates 5% loan-loss coverage.

- August 2025: Bank Indonesia launched QRIS acceptance with Japan’s PayPay and LINE Pay, simplifying tourist spend in Bali.

- July 2025: Jalin and Visa rolled out tokenized-card acceptance across 200,000 ATMs.

Indonesia Payments Infrastructure Market Report Scope

Payments infrastructure is the underlying system of technologies, networks, institutions, and rules that enable money to move between people, businesses, and banks electronically or physically. It is the backbone that makes transactions—like card swipes, online transfers, or mobile payments—secure, fast, and reliable.

The Indonesia Payments Infrastructure Market Report is Segmented by Payment Instrument (Card-Based Payments, Real-Time Bank Transfers, E-Money, QRIS Payments, Other Emerging Instruments), Component (Hardware, Software and Platform, Services), Payment Channel (In-Store POS, Online E-Commerce and In-App, In-App P2P Transfers), End-User Vertical (Retail and Grocery, F and B and Quick-Service Restaurants, Transportation and Mobility, Travel and Hospitality, Other End-User Verticals), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

| Card-Based Payments |

| Real-Time Bank Transfers (BI-FAST, SKNBI, RTGS) |

| E-Money |

| QRIS Payments |

| Other Emerging Instruments (BNPL, Tokenized Cards) |

| Hardware |

| Software and Platform |

| Services |

| In-Store (POS) |

| Online (E-Commerce and In-App) |

| In-App P2P Transfers |

| Retail and Grocery |

| Food, Beverages, and Quick-Service Restaurants |

| Transportation and Mobility |

| Travel and Hospitality |

| Other End-User Verticals |

| By Payment Instrument | Card-Based Payments |

| Real-Time Bank Transfers (BI-FAST, SKNBI, RTGS) | |

| E-Money | |

| QRIS Payments | |

| Other Emerging Instruments (BNPL, Tokenized Cards) | |

| By Component | Hardware |

| Software and Platform | |

| Services | |

| By Payment Channel | In-Store (POS) |

| Online (E-Commerce and In-App) | |

| In-App P2P Transfers | |

| By End-User Vertical | Retail and Grocery |

| Food, Beverages, and Quick-Service Restaurants | |

| Transportation and Mobility | |

| Travel and Hospitality | |

| Other End-User Verticals |

Key Questions Answered in the Report

How fast is digital payment value growing in Indonesia?

The Indonesia payments infrastructure market is projected to expand at a 9.83% CAGR from 2026 to 2031, rising from USD 127.32 billion in 2026 to USD 203.47 billion by 2031.

Which payment instrument is gaining share quickest?

E-money, propelled by super-app wallets and QRIS acceptance, is increasing at an 11.21% CAGR, outpacing card-based options.

Why do merchants prefer QRIS to traditional cards?

QRIS carries merchant discount rates below 0.7% and settles within 24 hours, whereas card interchange often exceeds 1.5% and clears on a T+2 cycle.

What role does BI-FAST play in corporate disbursements?

The real-time rail’s flat IDR 2,500 fee and sub-second settlement are pushing payroll and supplier payments away from expensive RTGS channels.

Which vertical shows the fastest digital-payment growth?

Transportation and mobility leads with an 11.02% CAGR, driven by ride-hailing and delivery apps embedding closed-loop wallets.

How fragmented is the competitive landscape today?

Five super-app or API-gateway leaders process about 60% of wallet volume, giving the market a moderate concentration score of 6.

Page last updated on: