Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

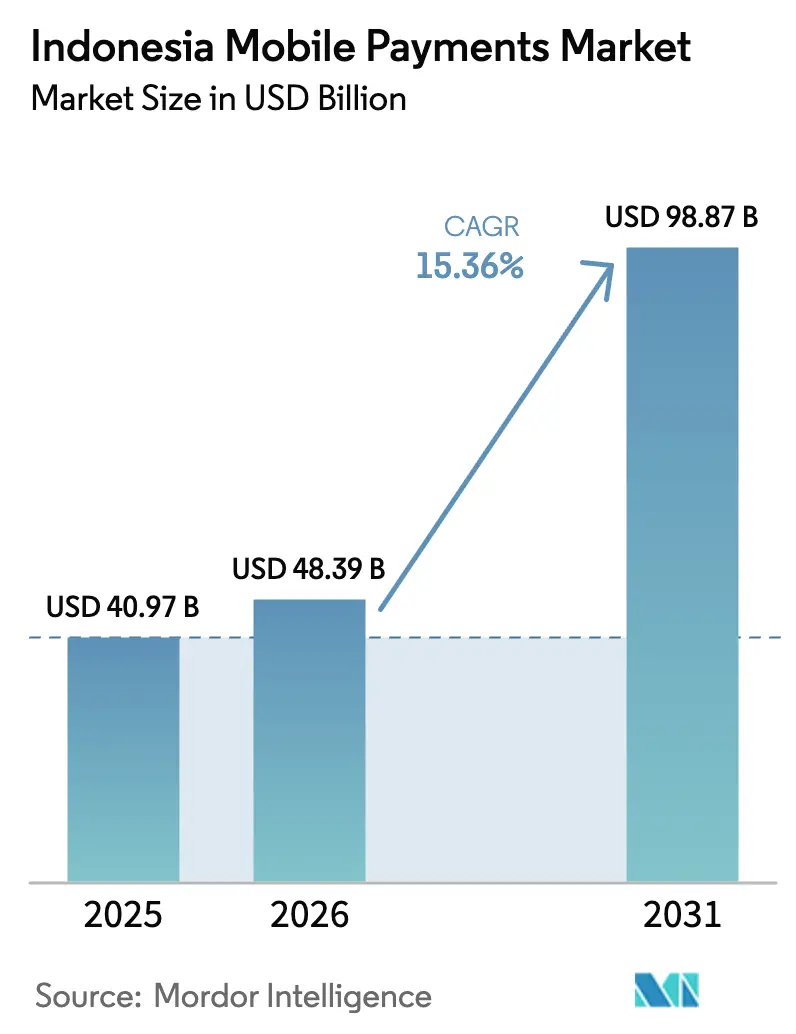

| Base Year Market Size (2025) | USD 40.97 Billion |

| Market Size (2026) | USD 48.39 Billion |

| Market Size (2031) | USD 98.87 Billion |

| Growth Rate (2026 - 2031) | 15.36% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Indonesia Mobile Payments Market Analysis by Mordor Intelligence

The Indonesia mobile payments market size is projected to expand from USD 40.97 billion in 2025 and USD 48.39 billion in 2026 to USD 98.87 billion by 2031, registering a CAGR of 15.36% between 2026-2031. Domestic QR code standardization, real-time transfer rails and super-app bundling are reinforcing a behavioral shift away from cash, while cross-border QR interoperability is opening new tourist-spend corridors. Competitive pressure is rising as wallet operators pivot from interchange fees to embedded lending, insurance and investments, a transition that makes proprietary data the primary source of differentiation. Government cashless mandates in public transportation and social-commerce adoption in tier-2 and tier-3 cities are widening the daily use case mix and accelerating merchant onboarding. Fraud mitigation and float-balance ceilings remain structural frictions, yet the continued decline in data costs and the completion of Palapa Ring fiber connectivity are gradually reducing rural acceptance barriers.

Key Report Takeaways

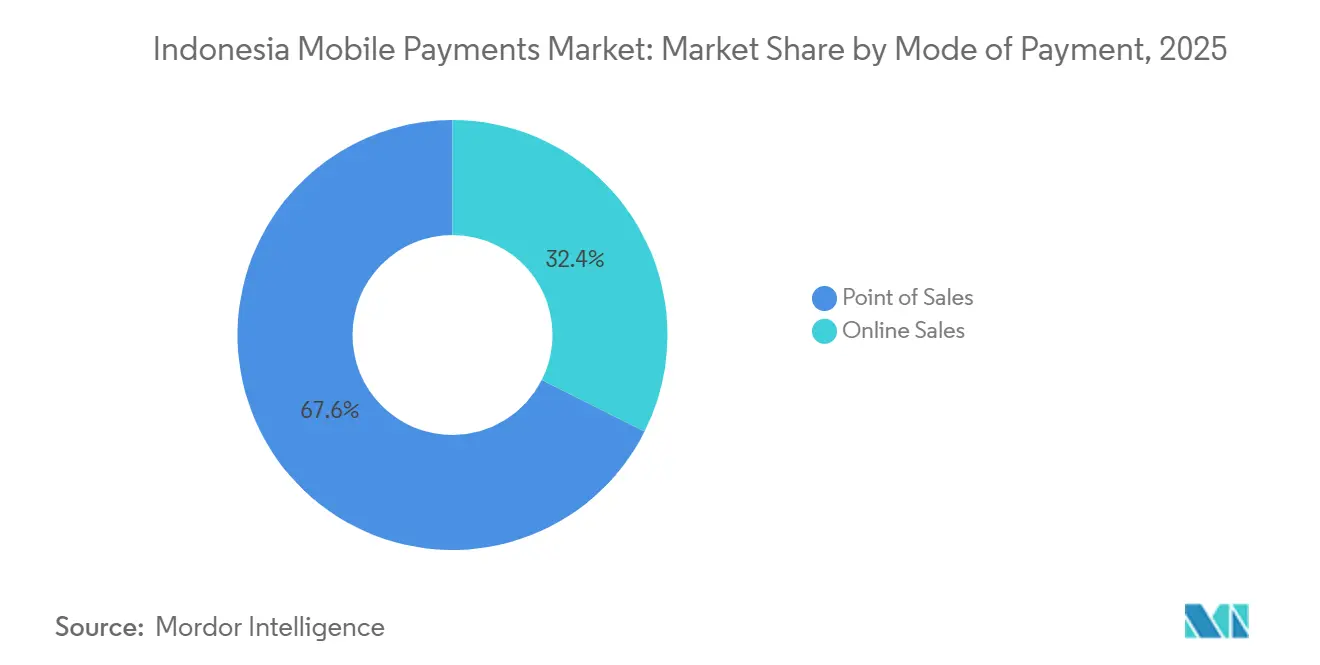

- By mode of payment, Point of Sales led with 67.59% of Indonesia mobile payments market share in 2025, while Online Sales is forecast to advance at a 17.43% CAGR through 2031

- By payment type, Other Payment Types commanded 48.67% share of the Indonesia mobile payments market size in 2025; QR-Based payments are expanding at a 16.24% CAGR over 2026-2031.

- By transaction type, Peer-to-Peer transactions dominated with 63.92% share in 2025, whereas Person to Business flows hold the fastest growth outlook at a 16.17% CAGR to 2031.

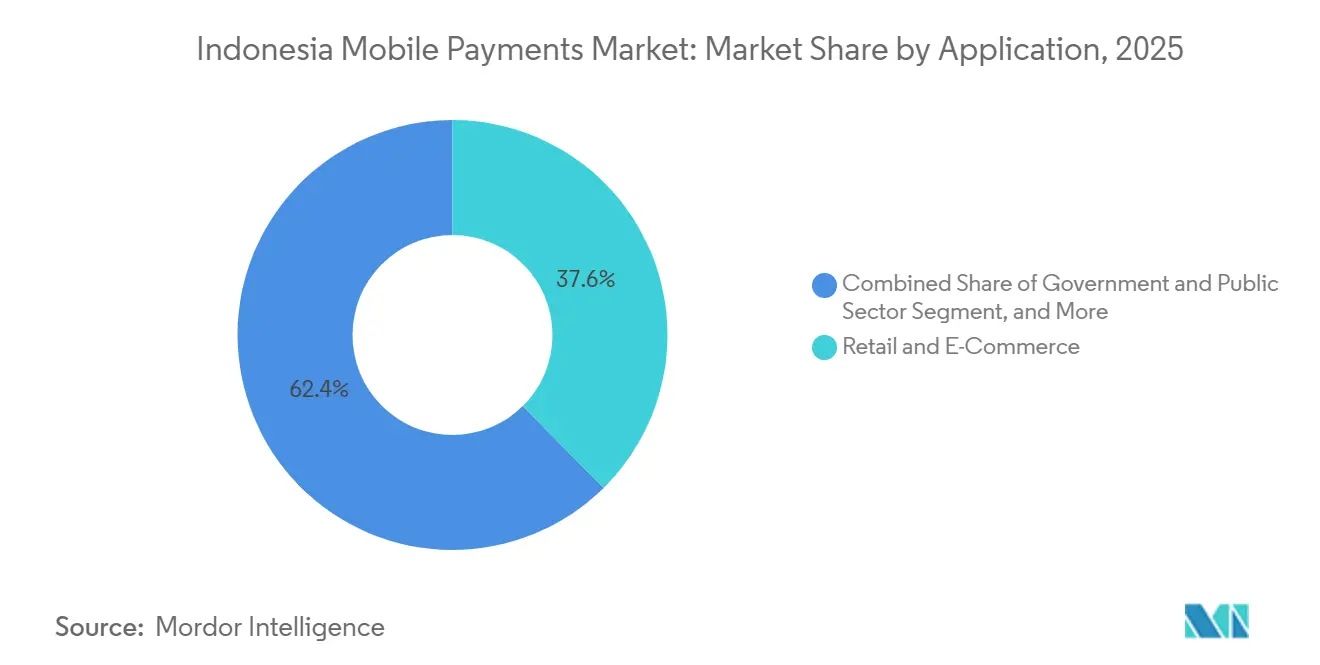

- By application, Retail and E-Commerce contributed 37.59% revenue share in 2025, yet Transportation and Logistics is projected to climb at an 18.56% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Indonesia Mobile Payments Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Bank Indonesia’s Nationwide QRIS Mandate Accelerating Merchant On-Boarding | +3.8% | National, Java and Sumatra Focus | Short Term (≤ 2 Years) |

| Social-Commerce Boom in Tier-2/3 Cities Expanding Wallet GMV | +2.9% | Kalimantan, Sulawesi, Eastern Indonesia | Medium Term (2-4 Years) |

| Government Cashless Incentives in Public Transport (JakLingko) Driving Daily Use-Cases | +2.4% | Jakarta, Bandung, Surabaya | Medium Term (2-4 Years) |

| BI-FAST Real-Time Transfer Fee Reduction Stimulating Account-to-Wallet Payments | +2.1% | Urban Banking Corridors | Short Term (≤ 2 Years) |

| Rise of Embedded Finance in Indonesian Super-Apps Unlocking New Merchant Categories | +2.5% | Java Urban Centers, Outer Islands | Medium Term (2-4 Years) |

| Cross-Border QR Code Linkages with Malaysia and Singapore Boosting Inbound Tourist Spend | +1.7% | Bali, Jakarta, Batam | Long Term (≥ 4 Years) |

| Source: Mordor Intelligence | |||

Bank Indonesia’s Nationwide QRIS Mandate Accelerating Merchant On-Boarding

The zero-MDR policy for sub-IDR 500,000 (USD 29.7) transactions removed cost barriers for micro-merchants, adding 34.23 million new outlets and lifting quarterly QR volumes by 148.5% in 2025.[1]Bank Indonesia, “Merchant Discount Rate Waiver for QRIS Transactions,” bi.go.id Standardized QR formats now let consumers pay with any wallet using a single scan, pushing providers to compete on loyalty perks and credit add-ons rather than exclusivity. Closed-loop operators are therefore leveraging transaction data to launch working-capital loans and inventory-planning dashboards that sit inside the payment flow, reinforcing stickiness among small retailers while offsetting lost interchange revenue.

Social-Commerce Boom in Tier-2/3 Cities Expanding Wallet GMV

Live-stream retail on Shopee Live and TikTok Shop created an impulse-buy channel in secondary cities where logistics costs once restrained e-commerce adoption. ShopeePay’s one-click integration cut cart abandonment by 28% in 2025, and social-commerce GMV in Makassar, Pontianak and Manado grew 62% year on year as buyers settled within the video feed instead of switching apps.[2]Sea Group, “ShopeePay One-Click Checkout Reduces Cart Abandonment,” seagroup.com Relaxed KYC thresholds for low-ticket sellers lowered entry hurdles for informal entrepreneurs, fostering a fresh long-tail of merchants that feed recurring wallet inflows.

Government Cashless Incentives in Public Transport (JakLingko) Driving Daily Use-Cases

JakLingko’s cashless-only rule from January 2025 converted 3.2 million commuters into habitual wallet users, with ridership among digital payers up 35% six months after launch.[3]Jakarta Provincial Government, “JakLingko Cashless Mandate Increases Ridership,” jakarta.go.id Bundling route planning, ticket purchase and real-time tracking inside GoPay, OVO and LinkAja apps removed the friction of reloadable tap cards. The model’s success in Jakarta catalyzed similar mandates in Surabaya and Bandung, embedding wallets into daily mobility and reinforcing payment frequency beyond discretionary shopping.

BI-FAST Real-Time Transfer Fee Reduction Stimulating Account-to-Wallet Payments

A flat IDR 2,500 (USD 0.16) fee democratized instant interbank transfers, driving BI-FAST volumes to 1.22 billion in Q3 2025. Users now prefer topping up wallets through mobile banking rather than paying higher convenience-store cash-deposit fees, while gig workers benefit from immediate earnings settlement. Banks have responded by embedding one-tap wallet reload buttons into digital apps, further tightening the linkage between traditional accounts and super-app ecosystems.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Persisting OTP and Social-Engineering Fraud Undermining Consumer Trust | -2.3% | Urban Centers | Short Term (≤ 2 Years) |

| High MDR for Micro-Merchants Outside Subsidized Schemes | -1.8% | Rural and Peri-Urban Zones | Medium Term (2-4 Years) |

| Regulatory Ceiling on E-Money Float Balances Limiting Ticket Size | -1.4% | National | Medium Term (2-4 Years) |

| Low NFC-Enabled Smartphone Penetration in Rural Indonesia | -1.2% | Eastern Indonesia, Remote Kalimantan | Long Term (≥ 4 Years) |

| Source: Mordor Intelligence | |||

Persisting OTP and Social-Engineering Fraud Undermining Consumer Trust

Fraud losses reached IDR 7 trillion (USD 0.42 billion) between late 2024 and 2025, with OTP phishing and SIM-swap schemes representing 68% of cases.[4]Otoritas Jasa Keuangan, “Digital Payment Fraud Losses Reach IDR 7 Trillion,” ojk.go.id Biometric logins and transaction velocity caps have reduced incident severity, but older users in tier-3 cities still favor cash due to fear of digital theft. OJK’s September 2024 mandate for real-time fraud monitoring adds compliance costs for wallets, though conviction rates below 12% continue to hinder deterrence.

High MDR for Micro-Merchants Outside Subsidized Schemes

Transactions above the subsidy threshold attract MDR fees up to 2.5%, eroding slim margins for rural motorcycle dealers and furniture sellers. A Lampung dealer highlighted that a 1.5% fee on a IDR 15 million (USD 0.89 thousand) scooter equates to three days of profit, prompting cash discounts to sidestep digital rails. Without tiered MDR relief or volume-based rebates, many high-ticket merchants opt to stay offline, capping rural penetration for the Indonesia mobile payments market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Mode of Payment: Physical Retail Anchors Volume, Digital Channels Drive Value

Point of Sales accounted for 67.59% of 2025 volume, anchoring the Indonesia mobile payments market on in-store groceries, fuel and quick-service restaurants. QRIS’s zero-fee regime below IDR 500,000 lets small vendors accept wallets without margin sacrifice, preserving cashflow certainty. Online Sales, though smaller today, is forecast to compound at 17.43% as social-commerce embeds one-tap checkouts and subscription platforms scale video, software and cloud storage packages. The divergence signals that while brick-and-mortar will keep headline volume, digital channels will capture a larger slice of discretionary spending value over the forecast horizon, expanding total addressable reach for the Indonesia mobile payments market.

Physical retail also benefits from behavioral overlap: shoppers who scan a QR code to pay for groceries often top up their wallets via BI-FAST in the same session, closing a data loop that enables targeted promotions on their next store visit. Conversely, online users generate richer SKU-level insights, letting marketplaces bundle pay-later offers and loyalty cashbacks that lift average order value. Together, the two channels reinforce a blended payment habit, cushioning seasonality shocks and widening reachable GMV for the Indonesia mobile payments industry.

By Payment Type: QR Codes Democratize Access, NFC Awaits Infrastructure

Legacy text-based options such as USSD and SMS held 48.67% share in 2025, reflecting continued feature-phone usage and consumer preference for visible confirmation messages. However, QR-Based flows are on track for a 16.24% CAGR, energized by QRIS interoperability and bilateral links that let Malaysian and Singaporean tourists pay Indonesian merchants in native wallets. The simplicity of printed codes, costing a fraction of NFC terminals, keeps merchant capex minimal and accelerates rural rollout.

NFC lags because sub-USD 125 devices lack chipsets, and merchants resist buying dedicated readers when QR achieves network ubiquity. Yet as handset prices fall and mass-market Android models add NFC modules, tap-to-pay could emerge for transit gates and high-footfall retail, particularly where speed trumps camera alignment. Over the forecast period, QR will remain the universal denominator, but NFC may carve premium urban niches, nudging blended acceptance that further enlarges the Indonesia mobile payments market.

By Transaction Type: P2P Dominates Volume, P2B Captures Commercial Growth

Peer-to-Peer transfers held 63.92% share in 2025, underscoring cultural norms of mutual assistance and the convenience of splitting bills instantly. Low float-balance ceilings keep ticket sizes modest, yet high frequency sustains engagement and generates behavioral data for credit scoring. Person to Business transactions, growing at 16.17% CAGR, ride on public-sector mandates and merchant QR absorption. As P2B volumes scale, wallets can monetize through merchant analytics dashboards, inventory financing and targeted advertising, enriching revenue streams while deepening the Indonesia mobile payments market’s commercial relevance.

The social quotient of P2P also seeds network effects: users who receive transfers are nudged to leave balances in-app for future purchases, creating an internal liquidity loop that lowers wallet providers’ funding costs. In turn, providers channel float balances into money-market instruments within regulatory caps, subsidizing rewards that attract still more users, a virtuous cycle strengthening wallet defensibility in the Indonesia mobile payments market.

By Application: Retail Leads Today, Transport Shapes Tomorrow

Retail and E-Commerce contributed 37.59% of 2025 market value, buoyed by convenience stores and online marketplaces integrating cashback and loyalty engines. Transportation and Logistics is the breakout vertical, projected at an 18.56% CAGR as ride-hailing, courier and public-transit platforms embed fare collection, route guidance and surge pricing within payment layers. Wallets gain daily stickiness through multi-modal commutes, while couriers leverage instant payouts to retain riders, creating intertwined supply-and-demand incentives that enlarge throughput for the Indonesia mobile payments market size.

Beyond these anchors, hospitality, education and healthcare are integrating QR invoicing to ease reconciliation, while government portals accept wallets for taxes and permits, widening everyday relevance. Each incremental use case nudges cash-first users toward digital familiarity, gradually lifting the Indonesia mobile payments market penetration curve even in cash-entrenched rural segments.

Geography Analysis

Java generated roughly 60% of 2025 transaction volume, powered by 145 million residents, dense banking networks and smartphone penetration above 75% among 18-45-year-olds. Sumatra ranks second, buoyed by remittances and cross-border trade that normalize digital settlement with Malaysia and Singapore. Kalimantan, Sulawesi and Papua lag due to patchy 4G and merchant density below 40% outside capitals, but Palapa Ring backhaul is closing the gap, enabling wallets to deploy QR kits through post-office agents that onboarded 1.8 million rural merchants in 2025.

Jakarta remains the innovation flywheel, hosting 38% of fintech startups and 52% of VC allocation. Pilots such as JakLingko’s cashless transit debut in the capital before replicating in Surabaya, Bandung and Medan, accelerating spillover diffusion. Eastern islands face cultural inertia favoring face-to-face transactions, yet digital remittances from urban migrant workers are injecting liquidity and demonstrating convenience, gradually eroding cash primacy.

Tourist destinations illustrate cross-border potential: Bali merchants processed 18% of tourist-facing volume via Alipay+ and WeChat Pay in 2025, bypassing currency exchange and batching delays. Batam and Bintan leveraged Singaporean day-tripper flows to pilot QRIS acceptance for GrabPay and Touch ’n Go, handling USD 47 million in the first half of 2025. These corridors validate ASEAN’s regional QR blueprint, scheduled to add Thailand, Vietnam and the Philippines by 2027, a development set to expand inbound GMV and cement Indonesia’s leadership in the wider Southeast Asian payment stack.

Uniform consumer-protection rules mandate receipts, 14-day dispute windows and IDR 500,000 (USD 29.7) liability caps, yet enforcement varies outside Java where regulator field units are thin. Inconsistent oversight enables occasional rogue operators to offer low-fee wallets without deposit insurance, posing trust risks that hamper adoption in remote zones. Nevertheless, digital remittances saved households USD 280 million in fees during 2025, capital redirected to education and healthcare, underscoring tangible welfare gains and bolstering the inclusive growth narrative for the Indonesia mobile payments market.

Competitive Landscape

The Indonesia mobile payments market is moderately fragmented; the top five, GoPay, OVO, ShopeePay, DANA and LinkAja, controlled about 70% share in 2025, but no single wallet exceeds 25%. Super-apps harvest captive user bases from ride-hailing and e-commerce to cross-sell credit, insurance and mutual funds, moving revenue reliance from interchange to embedded finance. GoPay’s 2024 tie-in with Mandiri Livin’ gives customers savings yields and overdraft lines while granting Mandiri exposure to 50 million Gojek users, a template emulated by ShopeePay’s linkage with SeaBank and DANA’s marketplace integrations.

PayLater specialists Kredivo and Akulaku target thin-file millennials with BNPL at checkout, yet portfolio resilience is untested against macro slowdown. Meanwhile, bank-led wallets from BCA, BRI and Mandiri compete on deposit insurance and higher transaction ceilings, appealing to affluent users constrained by e-money float caps. Foreign entrants Alipay+ and WeChat Pay build tourist beachheads before teaming with local partners for domestic acceptance, adding cross-border cachet and pressuring incumbents to match UX polish.

Regulatory sandboxes allow year-long pilots in blockchain settlements and AI fraud scorers, speeding iteration but also injecting compliance uncertainty for graduates seeking full licenses. Technology bifurcation persists: Jakarta pilots biometric logins and tokenization, whereas tier-3 cities lean on QR simplicity and SMS receipts. Rural merchant acceptance remains the largest white space, with wallets and banks racing to deploy low-cost QR kits that bring micro-retail into the Indonesia mobile payments market fold.

Indonesia Mobile Payments Industry Leaders

PT Dompet Karya Anak Bangsa (GoPay)

PT Espay Debit Indonesia Koe (DANA)

PT Nusa Satu Inti Artha (DOKU)

PT Fintek Karya Nusantara (LinkAja)

PT Veritra Sentosa Internasional (PayTren)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: Bank Indonesia added South Korean KakaoPay to QRIS cross-border program, expanding tourist acceptance and reinforcing regional payment harmonization.

- December 2025: OJK issued POJK 32/2025 that formalizes BNPL licensing, caps monthly interest at 0.5%, and mandates 5% loan-loss coverage.

- August 2025: Bank Indonesia launched QRIS acceptance with Japan’s PayPay and LINE Pay, simplifying tourist spend in Bali.

- July 2025: Jalin and Visa rolled out tokenized-card acceptance across 200,000 ATMs.

Indonesia Mobile Payments Market Report Scope

Mobile payment is a payment made for a product or service through a portable electronic device such as a tablet or cell phone. The study tracks the application of mobile payment based on transaction type, which is Proximity and Remote payment. The study tracks key market metrics, underlying growth influencers, and significant industry vendors, providing support for Indonesia's mobile payments market estimates and growth rates throughout the anticipated period.

The Indonesia Mobile Payments Market Report is Segmented by Mode of Payment (Point of Sales, Online Sales), Payment Type (NFC, QR-Based, Other Payment Types), Transaction Type (Peer-to-Peer, Person to Business), Application (Retail and e-Commerce, Transportation and Logistics, Hospitality and Food-Service, Government and Public Sector, Other Applications), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

By Mode of Payment

| Point of Sales |

| Online Sales |

By Payment Type

| NFC |

| QR-Based |

| Other Payment Types |

By Transaction Type

| Peer-to-Peer (P2P) |

| Person to Business |

By Application

| Retail and e-Commerce |

| Transportation and Logistics |

| Hospitality and Food-Service |

| Government and Public Sector |

| Other Applications (Education, Healthcare) |

| By Mode of Payment | Point of Sales |

| Online Sales | |

| By Payment Type | NFC |

| QR-Based | |

| Other Payment Types | |

| By Transaction Type | Peer-to-Peer (P2P) |

| Person to Business | |

| By Application | Retail and e-Commerce |

| Transportation and Logistics | |

| Hospitality and Food-Service | |

| Government and Public Sector | |

| Other Applications (Education, Healthcare) |

Key Questions Answered in the Report

How fast is digital payment value growing in Indonesia?

The Indonesia payments infrastructure market is projected to expand at a 9.83% CAGR from 2026 to 2031, rising from USD 127.32 billion in 2026 to USD 203.47 billion by 2031.

Which payment instrument is gaining share quickest?

E-money, propelled by super-app wallets and QRIS acceptance, is increasing at an 11.21% CAGR, outpacing card-based options.

Why do merchants prefer QRIS to traditional cards?

QRIS carries merchant discount rates below 0.7% and settles within 24 hours, whereas card interchange often exceeds 1.5% and clears on a T+2 cycle.

What role does BI-FAST play in corporate disbursements?

The real-time rail's flat IDR 2,500 (USD 0.15) fee and sub-second settlement are pushing payroll and supplier payments away from expensive RTGS channels.

Which vertical shows the fastest digital-payment growth?

Transportation and mobility leads with an 11.02% CAGR, driven by ride-hailing and delivery apps embedding closed-loop wallets.

How fragmented is the competitive landscape today?

Five super-app or API-gateway leaders process about 60% of wallet volume, giving the market a moderate concentration score of 6.

Page last updated on: