Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

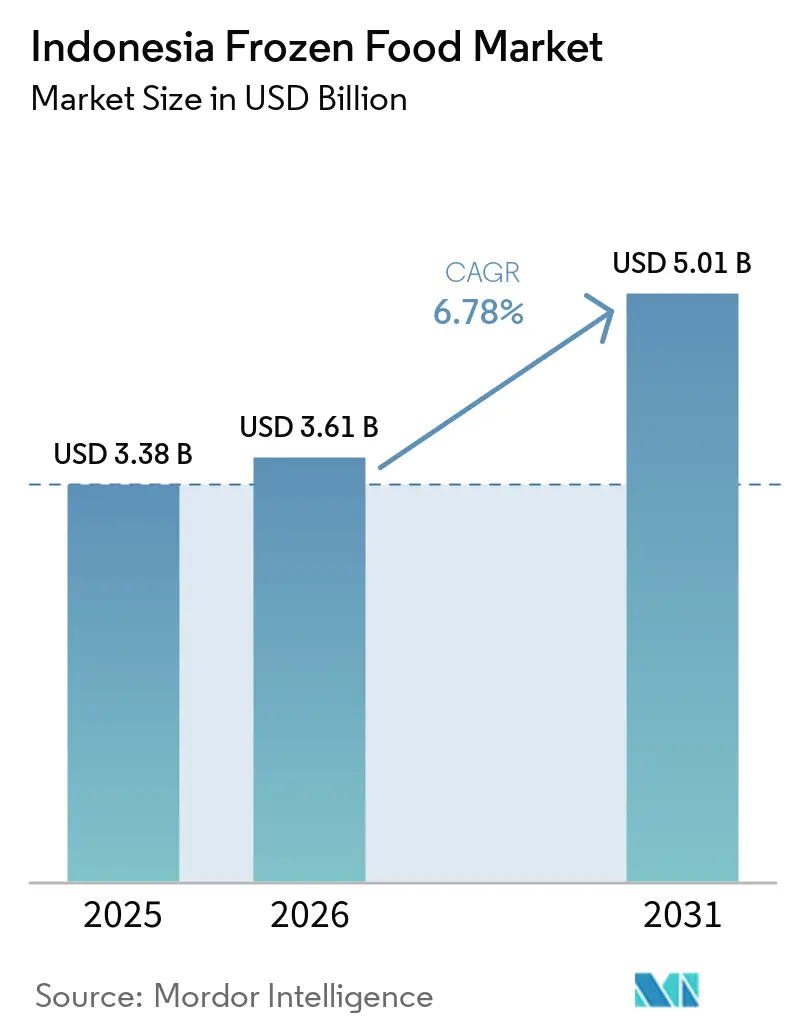

| Base Year Market Size (2025) | USD 3.38 Billion |

| Market Size (2026) | USD 3.61 Billion |

| Market Size (2031) | USD 5.01 Billion |

| Growth Rate (2026 - 2031) | 6.78% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Indonesia Frozen Food Market Analysis by Mordor Intelligence

The Indonesian frozen food market size is expected to grow from USD 3.38 billion in 2025 to USD 3.61 billion in 2026 and is forecast to reach USD 5.01 billion by 2031 at 6.78% CAGR over 2026-2031. The demand for quick-to-prepare meals in Indonesia is being driven by factors such as rapid urban migration, a growing middle class, and extended working hours. This trend is further supported by the expansion of modern retail and a significant rise in e-commerce spending, which simplifies product discovery and broadens choices for consumers. Busy lifestyles, the rise in dual-income households, and the growing number of nuclear families are driving the demand for frozen food products, including ready-to-eat and easy-to-cook options, valued for their time-saving advantages. On the supply side, investments in cold-chain infrastructure are addressing storage limitations and enhancing the reliability of temperature-controlled distribution. Moreover, stricter regulations from BPOM and mandatory halal certification are raising quality standards. Manufacturers are responding by reformulating products, improving traceability, and adopting clean-label claims to attract health-conscious consumers.

Key Report Takeaways

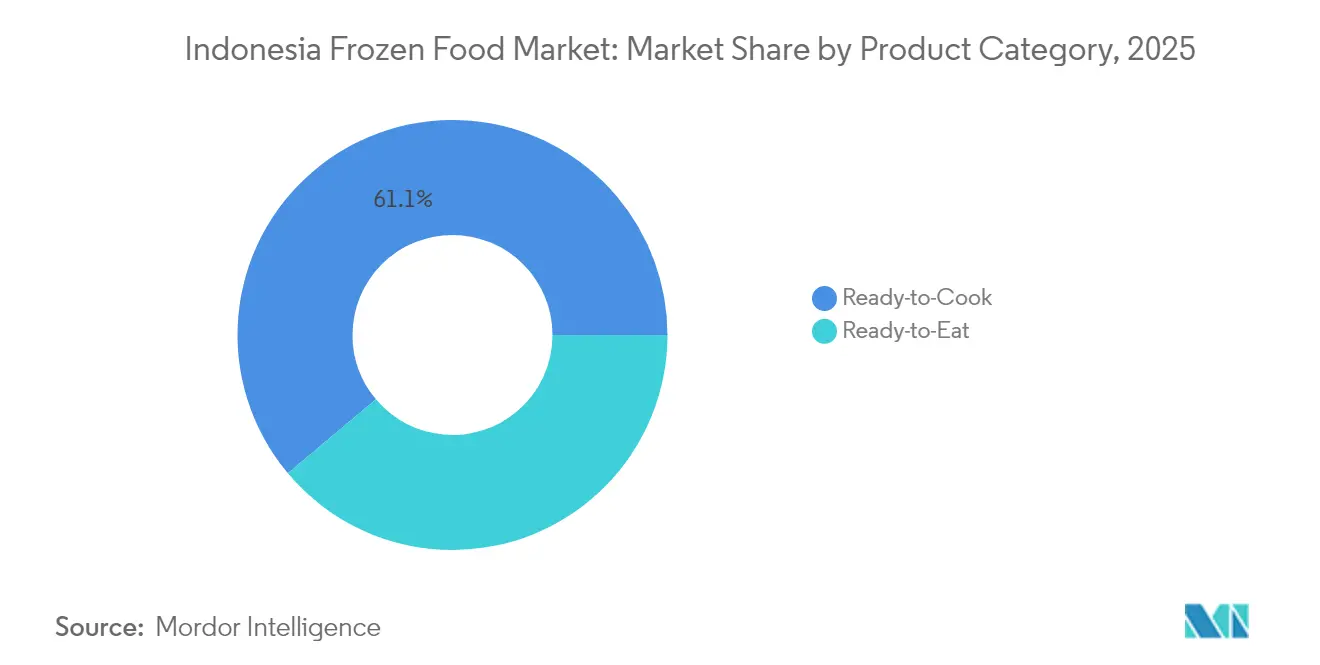

- By product category, Ready-to-Cook captured 61.12% of the Indonesian frozen food market share in 2025, whereas Ready-to-Eat is advancing at a 7.34% CAGR through 2031.

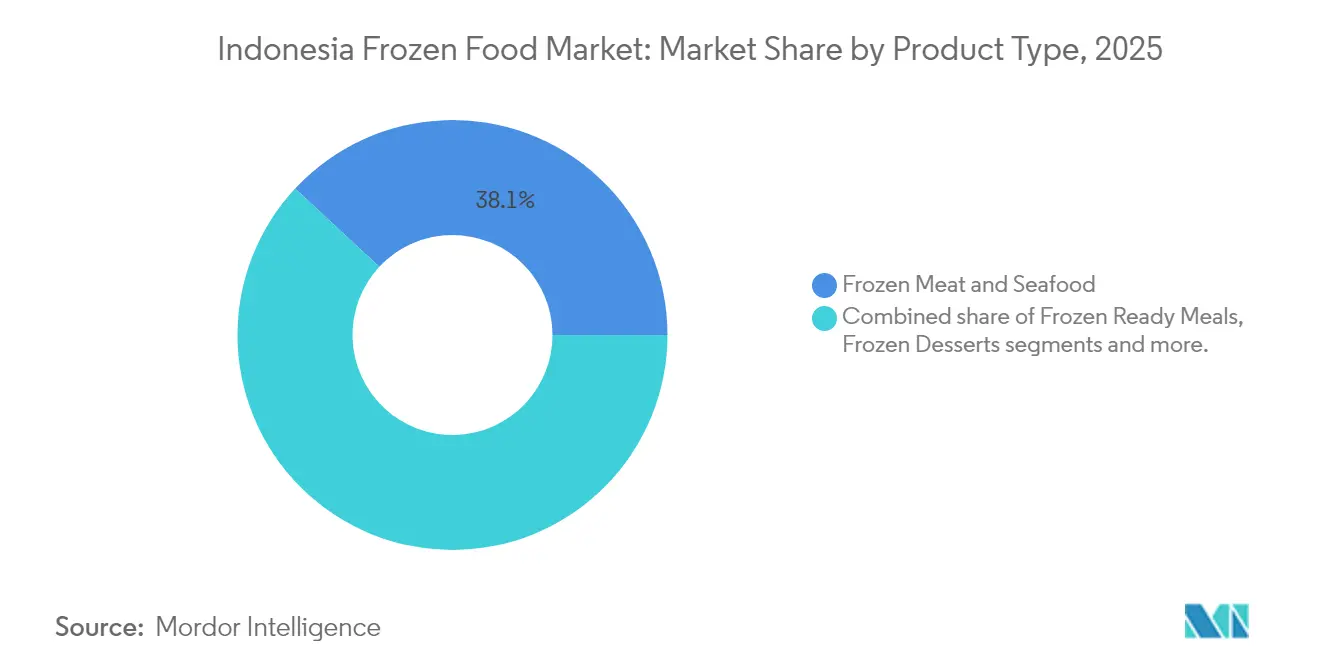

- By product type, Frozen Meat and Seafood held 38.07% share of the Indonesia frozen food market size in 2025, while Frozen Fruits and Vegetables is set to expand at an 8.02% CAGR to 2031.

- By distribution channel, Off-Trade outlets commanded 81.55% of sales in 2025; Off-Trade is projected to rise to 6.98% of total retail transactions by 2027 at the fastest CAGR in the Indonesia frozen food market.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Indonesia Frozen Food Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Popularity of convenient food products | +1.8% | Urban Java and Sumatra | Medium term (2-4 years) |

| Expansion of cold-chain logistics | +1.5% | Jakarta, Surabaya, Medan corridors | Long term (≥ 4 years) |

| Plant-based and functional frozen meal innovation | +1.2% | Jakarta and Bandung | Medium term (2-4 years) |

| Popularity of frozen processed meat and seafood | +1.0% | Coastal regions | Short term (≤ 2 years) |

| Social media and influencer marketing | +0.8% | Gen Z and millennial clusters nationwide | Short term (≤ 2 years) |

| Increasing health consciousness and quality demand | +0.7% | Upper-middle income urban households | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Popularity of Convenient Food Products

Indonesia's consumption landscape is evolving, fueled by a growing demand for convenient food products. Ready-to-eat and ready-to-cook frozen foods have become essential household items, offering a wide range of options from both local and international cuisines. These products meet consumer preferences for nutrition, variety, and time efficiency, driving the frozen ready meal segment to lead the market. Urbanization and the increase in dual-income households have amplified the dependence on these convenient food solutions, particularly in major metropolitan areas like Jakarta and Surabaya. According to Statistics Indonesia, 46.61% of urban expenditure in Indonesia was allocated to food in 2024[1]Source: Central Bureau of Statistics, "Indonesian Residents' Consumption Expenditure", bps.go.id. This shift is further supported by the rise of modern retail formats and the rapid growth of e-commerce, which together enhance product accessibility and variety. Companies are increasingly utilizing digital platforms to connect with younger, time-constrained consumers. For instance, GoFood reported a 30% year-on-year increase in online orders for frozen and ready meals in 2024. As Indonesia's middle class continues to grow and urban lifestyles become more demanding, this trend is expected to persist.

Expansion of cold-chain logistics

Indonesia's frozen food market depends heavily on cold-chain infrastructure, which remains significantly underdeveloped. In 2024, Pelindo's modernization program reduced berth times for non-containerized vessels by 30% and increased reefer plug availability at Tanjung Priok, leading to a 17% rise in chilled cargo throughput. Thirteen smart ports now utilize technologies such as optical character recognition, IoT, and automated gates, enabling cold chain operators to monitor container temperatures efficiently from ship to warehouse[2]Source: International Trade Administration, "Indonesia Infrastructure Smart Port Development", trade.gov. Advanced refrigeration and cold transport reduce spoilage during transit and distribution, ensuring high standards of food safety and quality. This logistical efficiency reassures consumers and addresses concerns about product degradation and contamination. In May 2025, the collaboration between Dalian Bingshan and Thermo Asri Makmur to develop new cold chain facilities highlights a shift toward modern logistics solutions. These advancements are expected to create new growth opportunities, particularly for off-trade and e-commerce sectors that require integrated temperature control and effective last-mile delivery.

Plant-based and functional frozen meal innovation

Plant-based and functional frozen meals are becoming significant growth drivers as health and sustainability gain prominence. The increasing adoption of vegetarian, vegan, and flexitarian diets is boosting the demand for plant-based frozen meals. Ready-to-eat formats now include traditional soy-based foods like tempeh and tofu, along with modern meat substitutes, making them more accessible. This growing demand is driving innovation, with brands introducing fortified, plant-based frozen options tailored to regional preferences. To enhance transparency and consumer trust, BPOM implemented new labeling and nutrient disclosure standards in 2024. Consumers are increasingly prioritizing sustainability and animal welfare in their purchasing decisions. Plant-based frozen foods, with their lower environmental impact, align with ethical eating values and climate action goals, further accelerating their adoption.

Social media and influencer marketing

Social media and influencer marketing are accelerating the adoption of frozen foods among younger demographics. Instagram and TikTok have become essential platforms for product discovery and peer recommendations. In 2024, brands observed a notable increase in engagement and sales following targeted influencer campaigns, particularly for new launches in the plant-based and ready-to-eat segments. These digital initiatives are further strengthened by collaborations with food delivery services, highlighting the link between online visibility and market penetration. The rise in internet usage underpins digital marketing strategies, with social media and influencer engagement serving as key growth drivers for the market. According to the International Telecommunication Union (ITU), 69% of Indonesia's population used the internet in 2023[3]Source: International Telecommunication Union (ITU), "Individuals using the Internet (% of population) - Indonesia", datahub.itu.int. As digital information and recommendations increasingly shape purchasing decisions, frozen food manufacturers are turning to social media and influencer marketing, underscoring a shift in consumer habits.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High electricity and refrigeration costs | –1.5% | Outside Java | Medium term (2-4 years) |

| Competition from fresh and chilled alternatives | –1.2% | Urban and peri-urban districts | Short term (≤ 2 years) |

| Limited consumer awareness in some regions | –0.8% | Rural and tier-2 cities | Long term (≥ 4 years) |

| Concerns over food safety and quality | –0.7% | National | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High electricity and refrigeration costs

Indonesia's frozen food sector faces significant challenges due to high electricity and refrigeration costs, particularly in areas outside major urban centers. The fragmented power grid and elevated energy tariffs substantially increase cold storage and logistics expenses, which, in turn, compress profit margins for producers and distributors. This issue is especially pronounced in eastern Indonesia, where infrastructure deficiencies persist despite government efforts to encourage private-sector investment through various incentives. Although the adoption of energy-efficient technologies and renewable energy sources is gradually helping to optimize cost structures, the sector is unlikely to experience widespread benefits until the medium term.

Competition from fresh and chilled food alternatives

Fresh and chilled food alternatives continue to pose strong competition, particularly among consumers who perceive frozen products as less healthy or lacking in taste. Traditional markets, which still dominate food retail transactions, play a significant role in reinforcing the preference for daily-purchased, freshly prepared foods. In Indonesia, a large segment of consumers views fresh and chilled foods as more flavorful, healthier, and of superior quality compared to frozen options. This preference is especially evident in traditional cuisine and among shoppers who frequent wet markets or urban centers where daily fresh supplies are readily available. However, the COVID-19 pandemic, coupled with evolving urban lifestyles, has started to shift these perceptions. These changes present an opportunity for frozen food brands to reposition themselves by highlighting attributes such as convenience, safety, and nutritional value, which align with the needs of modern consumers.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Category: Ready-to-Cook Retains Dominance, Ready-to-Eat Accelerates

The Ready-to-Cook segment commanded 61.12% of the Indonesian frozen food market share in 2025. With brands increasingly developing regional spice blends tailored to Sundanese and Balinese preferences, this segment is expected to grow steadily. Consumers appreciate the flexibility to adjust final seasonings, making these kits a practical balance between traditional cooking and convenience. Manufacturers are leveraging this trend by introducing family-size packs, which lower per-serving costs and enhance freezer-fill rates in modern retail outlets. Meanwhile, Ready-to-Eat meals are anticipated to grow at a strong 7.34% CAGR through 2031, fueled by the rise in single-person households. Products such as microwaveable rice bowls, Korean-style dumplings, and protein-enriched porridges appeal to students and professionals living in rented accommodations. Additionally, cross-promotions on ride-hailing super-apps encourage impulse purchases, embedding Ready-to-Eat meals into daily routines and strengthening their role in Indonesia's growing frozen food market.

Global suppliers are increasingly collaborating with local partners to align taste and texture with Indonesian preferences. Automated portioning lines ensure consistent quality, while modified-atmosphere packaging extends shelf life to over 18 months. This operational precision supports export goals to neighboring ASEAN markets and establishes the foundation for economies of scale. This enables suppliers to sustain aggressive promotional pricing without compromising margins. Consequently, the combined growth of the Ready-to-Cook and Ready-to-Eat segments strengthens Indonesia's frozen food market, providing resilience against fluctuations in raw material costs.

By Product Type: Frozen Meat and Seafood Anchor, Fruits and Vegetables Lead Growth

Frozen Meat and Seafood generated 38.07% of the Indonesian frozen food market size in 2025, highlighting the country's strong protein preferences and the increasing role of formal-sector food services. Quick-service restaurants, expanding their presence, relied on individually quick-frozen (IQF) chicken and battered fish fillets to maintain consistent menu quality nationwide. Enhanced cold-chain compliance, enforced by the 2024 BPOM regulation, not only reduces spoilage risks but also improves unit economics for animal protein processors. Meanwhile, Frozen Fruits and Vegetables are projected to grow at an 8.02% CAGR, fueled by the middle class's focus on wellness and the growing popularity of smoothie bars and snack bars in urban malls. Local agritech start-ups source blemished but nutrient-rich produce directly from farms, flash-freezing it within six hours of harvest. Their sustainability-focused messaging appeals to eco-conscious millennials, expanding their market share within Indonesia's frozen food sector.

Product innovation is gaining momentum, with importers introducing berry mixes and avocado chunks that were previously unavailable in large quantities. Domestic brands are leveraging these inputs to develop ready-to-blend mixes tailored for health-focused consumers, capitalizing on the global superfood trend. To enhance transparency, food-safety traceability codes are printed on each bag, allowing consumers to verify the farm origin through QR scans. This combination of health, convenience, and digital verification positions Frozen Fruits and Vegetables as a premium segment, helping to mitigate the impact of cyclical fluctuations in meat prices on Indonesia's frozen food market.

By Distribution Channel: Off-Trade Channels Dominate, E-Commerce Surges

In 2025, off-trade outlets, such as supermarkets, hypermarkets, and convenience stores, accounted for 81.55% of the Indonesian frozen food market share. This growth was driven by retail floor-space expansions exceeding 600,000 m² across Java and Sumatra. Retailers strategically position curved-glass freezers at store entrances to improve product visibility. Additionally, private-label SKUs, priced lower than national brands, are enhancing shopper loyalty. However, the fastest growth is occurring online, with e-commerce becoming the most significant revenue driver for Indonesia's frozen food sector. Fulfillment innovations, including insulated totes with gel packs, maintain –18 °C temperatures for six-hour deliveries to peri-urban and rural households. Moreover, BPOM Regulation No. 8/2020 enforces strict labeling and last-mile handling standards, prompting platforms to invest in temperature-monitoring sensors and delivery driver training.

Looking ahead, the off-trade distribution channel is expected to grow at a CAGR of 6.95% through 2031. The synergy between offline and online channels is evident with the implementation of “click-and-collect” lockers at minimarts, which lower shipping costs and improve stock-turn ratios. Additionally, loyalty apps offering digital coupons redeemable in both environments are increasing foot traffic to brick-and-mortar stores. Together, these omnichannel retail strategies enhance market accessibility and reinforce the Indonesian frozen food market's role in mainstream grocery shopping.

Geography Analysis

Java, with its dense urbanization, higher-than-average disposable incomes, and extensive modern-trade network, continues to dominate Indonesia's frozen food market, contributing to over half of the category's turnover. Provinces such as West Java and East Java play a pivotal role by hosting multi-temperature distribution centers capable of reaching 80% of the island's population within 24 hours. Additionally, the widespread penetration of smartphones has significantly boosted e-commerce activity, increasing the frequency of online orders. This trend has enabled frozen food products to penetrate suburban areas that were previously reliant on traditional wet markets.

Sumatra is positioning itself as the next major growth area for the frozen food market. Ongoing infrastructure projects, including the Trans-Sumatra toll road and the expansion of feeder ports, are effectively reducing logistics delays and cutting freight costs by up to 20%. To further accelerate this growth, local governments are providing land-lease incentives to attract cold-store developers, thereby expanding storage capacity across the island. Retailers are also introducing innovative hybrid supermarket-e-commerce hubs in cities like Medan and Palembang. These hubs combine in-store tasting events with app-based delivery services, creating opportunities for consumers to trial frozen food products and driving category growth.

Eastern Indonesia, which includes Sulawesi, Maluku, and Papua, has historically lagged behind but is now making significant strides through collaborative public-private cold-chain initiatives. Japanese ODA funding has facilitated the deployment of micro-grid solar chillers, which stabilize reef-fish harvests and ensure the year-round availability of frozen seafood in key cities such as Makassar and Manado. Furthermore, school-feeding programs in these provinces are incorporating frozen chicken nuggets and fortified vegetable mixes, laying the groundwork for increased demand. The combination of government-led nutrition targets and a rise in tourist inflows is creating a strong foundation for the long-term integration of Eastern Indonesia into the broader frozen food market, signaling substantial growth potential for the region.

Competitive Landscape

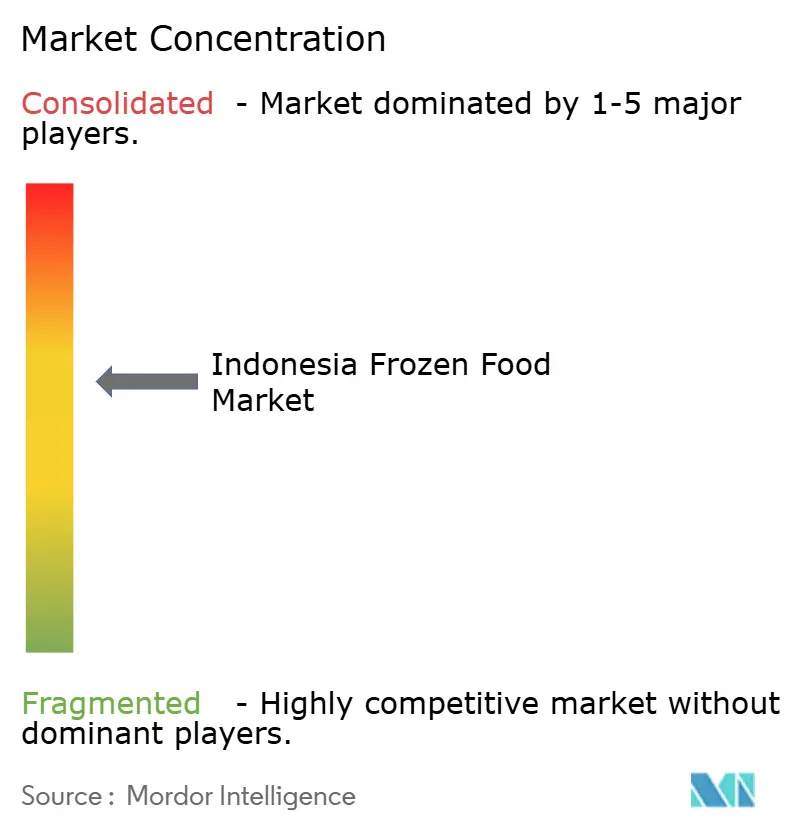

Indonesia's frozen food market is moderately consolidated, highlighting the country's diverse consumer preferences and strong regional brand loyalties. Global players such as Unilever and McCain Foods leverage their extensive global research capabilities to introduce innovative products like plant-based ice creams and air-fry-ready French fries, which cater to the growing demand for health-conscious and convenient food options. On the other hand, domestic leaders Indofood and Japfa Comfeed capitalize on their significant upstream integration, which provides them with cost advantages in raw material procurement. This enables them to offer competitive pricing while maintaining healthy profit margins. Furthermore, Unilever's strategic decision to spin off its ice-cream division in 2024 is expected to free up management resources, potentially accelerating innovation and growth in the savory-frozen food segment. The major players in the market are PT Charoen Pokphand Indonesia Tbk, Gunung Sewu Group, JAPFA Ltd, PT Sekar Bumi Tbk, and Unilever Plc, among others.

Data-driven operational strategies are becoming a critical factor in determining market leadership. Indofood is piloting AI-powered forecasting tools that integrate point-of-sale (POS) sell-through data with weather variables. This approach has significantly improved forecasting accuracy, reducing errors to just 5% and cutting inventory days by 12%. Similarly, Japfa is utilizing blockchain technology to enhance traceability in its chicken supply chain, addressing the increasing consumer demand for transparency and food safety. Compliance with regulatory requirements continues to serve as a strategic advantage for companies. Early adherence to BPOM’s nutrient disclosure regulations and the Halal Product Assurance Law not only facilitates faster market entry but also strengthens brand credibility in Indonesia's competitive frozen food market.

Merger-and-acquisition activity is gaining momentum in the market. Private-equity investors are actively targeting mid-tier regional players that enjoy strong local consumer loyalty but lack extensive national distribution networks. These investors are betting on the potential for consolidation to unlock synergies and achieve greater economies of scale. At the same time, sustainability initiatives are emerging as key differentiators in the market. Efforts such as adopting regenerative agricultural practices and using recyclable mono-material packaging are helping companies build a positive reputation. These sustainability narratives resonate particularly well with urban millennials, who are increasingly aligning their purchasing decisions with environmental and ethical considerations.

Indonesia Frozen Food Industry Leaders

-

PT Charoen Pokphand Indonesia Tbk

-

JAPFA Ltd

-

PT Sekar Bumi Tbk

-

Unilever Plc

-

Gunung Sewu Group (Belfoods Indonesia)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: PT Mayora Indah Tbk has announced a capital expenditure plan of IDR 1 trillion for 2025, aiming to expand its packaged foods and beverages segment and launch new products to enhance its market position.

- November 2024: Unilever has announced the demerger of its ice cream unit in Indonesia, indicating a strategic shift and a potential realignment of the market landscape.

- October 2024: Dalian Bingshan and Thermo Asri Makmur have strengthened their partnership to develop new cold chain facilities, addressing Indonesia's infrastructure deficit.

- March 2022: Traveloka launched an e-grocery market named Mart, which provides products including frozen food, fresh fruit, and personal care items. The company partnered with several supermarkets and grocery stores in Greater Jakarta for its most recent product.

Indonesia Frozen Food Market Report Scope

Frozen food products are complete meals or portions of meals that are precooked, assembled into a package, and frozen for retail sale. They are popular among consumers as they provide a diverse menu and are convenient to prepare.

The market studied is segmented by type and distribution channel. Based on type, the market is segmented into frozen fruits and vegetables, frozen ready meals, frozen processed meat products, frozen processed seafood, frozen bakery products, and other types. Based on distribution channels, the market is segmented into hypermarkets and supermarkets, grocery stores and convenience stores, and online retail stores. The market sizing has been done in value terms in USD for all the above-mentioned segments.

By Product Category

| Ready-to-Eat |

| Ready-to-Cook |

By Product Type

| Frozen Fruits and Vegetables |

| Frozen Meat and Seafood |

| Frozen Ready Meals |

| Frozen Snacks and Bakery |

| Frozen Desserts |

| Other Product Types |

By Distribution Channel

| On-Trade | |

| Off-Trade | Supermarkets/Hypermarkets |

| Convenience Stores | |

| Online Retail Store | |

| Other Off-Trade Channels |

| By Product Category | Ready-to-Eat | |

| Ready-to-Cook | ||

| By Product Type | Frozen Fruits and Vegetables | |

| Frozen Meat and Seafood | ||

| Frozen Ready Meals | ||

| Frozen Snacks and Bakery | ||

| Frozen Desserts | ||

| Other Product Types | ||

| By Distribution Channel | On-Trade | |

| Off-Trade | Supermarkets/Hypermarkets | |

| Convenience Stores | ||

| Online Retail Store | ||

| Other Off-Trade Channels | ||

Key Questions Answered in the Report

What is the projected value of the Indonesia frozen food market by 2031?

The category is expected to reach USD 5.01 billion by 2031.

How fast is online retail growing for frozen products in Indonesia?

E-commerce is projected to capture 21.4% of total retail sales by 2027, the fastest channel expansion within the category.

Which product type currently dominates sales?

Frozen Meat and Seafood leads with 38.07% share of 2025 turnover.

Which segment is forecast to grow quickest?

Frozen Fruits and Vegetables are projected to post an 8.02% CAGR through 2031.

Page last updated on: