Indonesia Cold Chain Logistics Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

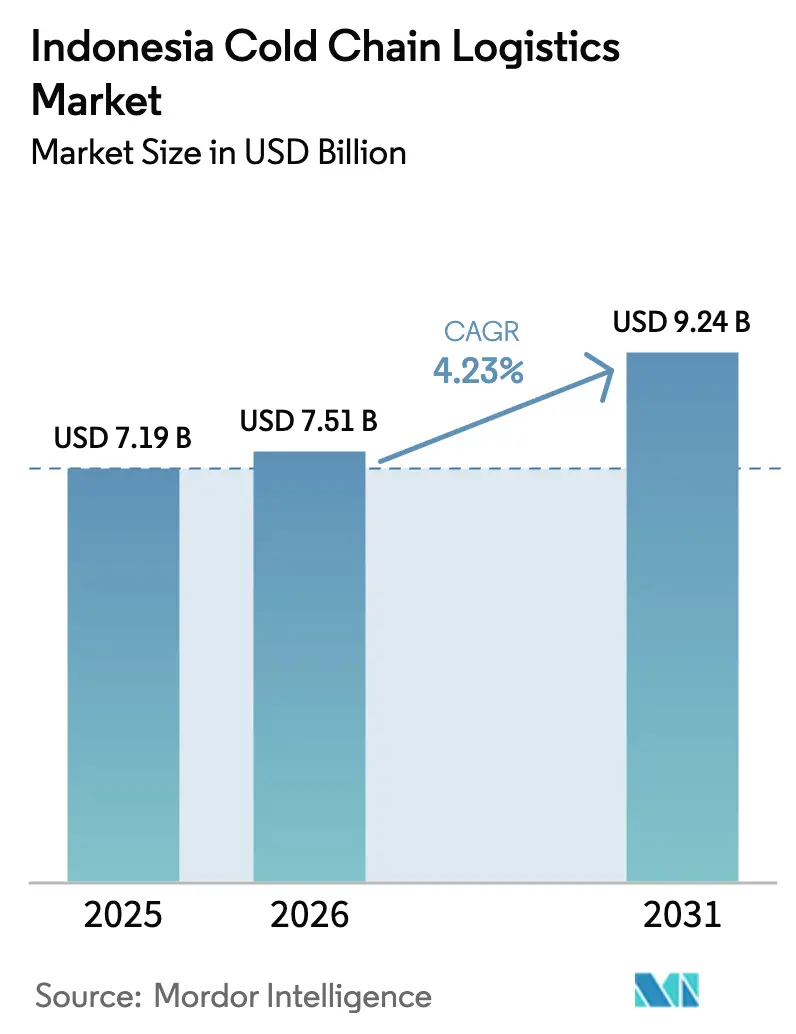

| Base Year Market Size (2025) | USD 7.19 Billion |

| Market Size (2026) | USD 7.51 Billion |

| Market Size (2031) | USD 9.24 Billion |

| Growth Rate (2026 - 2031) | 4.23% CAGR |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Indonesia Cold Chain Logistics Market Analysis by Mordor Intelligence

The Indonesia Cold Chain Logistics Market size is expected to grow from USD 7.19 billion in 2025 to USD 7.51 billion in 2026 and is forecast to reach USD 9.24 billion by 2031 at 4.23% CAGR over 2026-2031.

Investment signals from multinational logistics providers, sustained export momentum in seafood, and ongoing upgrades in pharmaceutical distribution are shaping near-term capacity additions and service innovations across both storage and transport nodes. The national logistics modernization agenda, including initiatives that target cost reductions and infrastructure upgrades, anchors private capital commitments into cold storage at ports and inland distribution centers, as well as certified pharma hubs that meet strict handling and traceability requirements. As the fisheries sector deepens integration with export markets and as healthcare distribution grows more complex, the competitive landscape is tilting toward operators that combine compliance, network reach, and digital visibility. On-the-ground execution also benefits from targeted government programs that equip regional nodes with cold logistics assets and from policy alignments that favor standards adoption and faster flows at gateway ports.

Key Report Takeaways

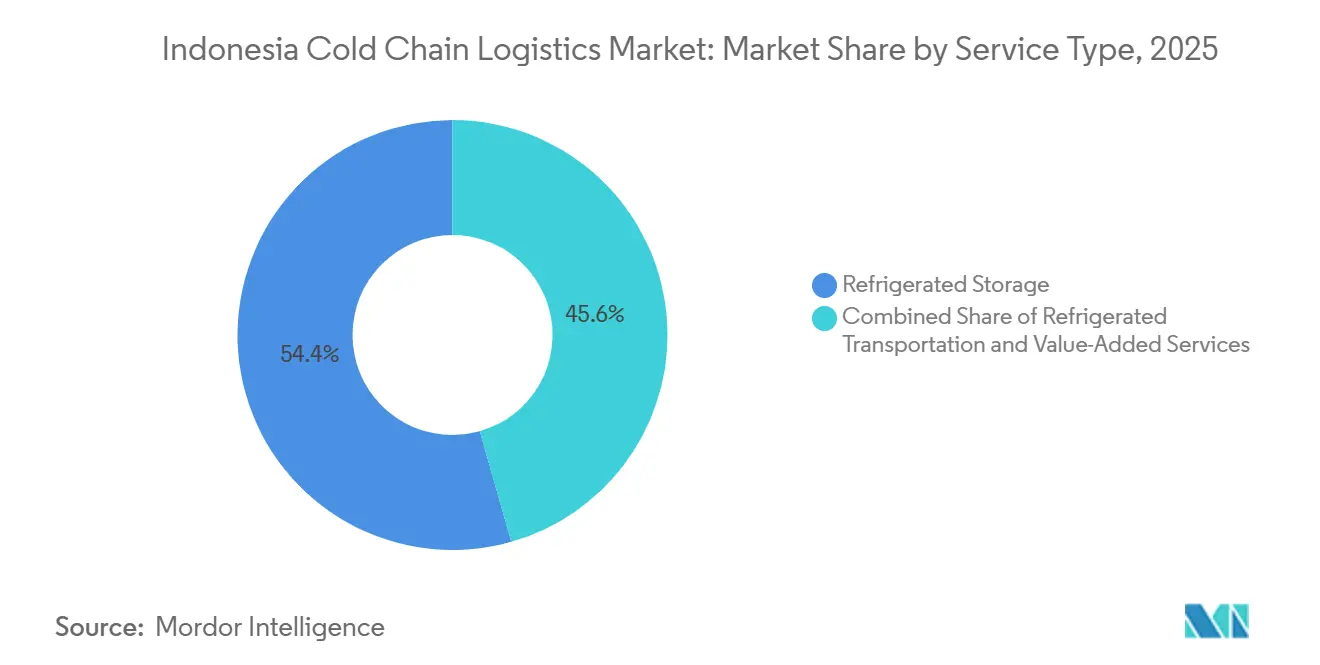

- By service type, refrigerated storage held 54.40% of the Indonesian cold-chain logistics market size in 2025, while value-added services are forecast to record a 4.75% CAGR through 2031.

- By temperature range, frozen storage accounted for a 57.35% share in 2025, and the ambient cold chain is projected to expand at a 5.54% CAGR through 2031.

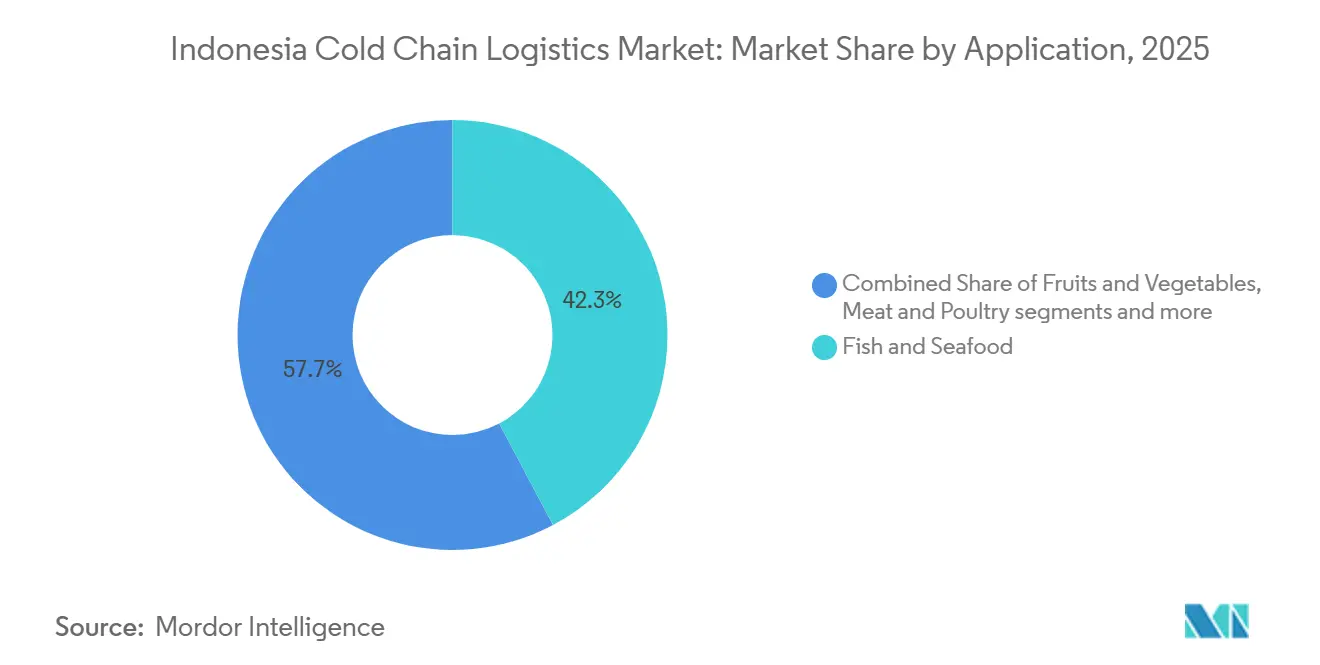

- By application, fish and seafood led with 42.25% of the Indonesian cold-chain logistics market share in 2025, while pharmaceuticals and biologics are set to grow at a 6.21% CAGR through 2031.

- By geography, Java commanded a 62.10% share in 2025, and Sulawesi is expected to post the fastest regional CAGR of 4.33% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Indonesia contributes to a system defined not by any single country or region but by the interaction of many. The global cold chain logistics market data by Mordor Intelligence represents that combined structure.

Indonesia Cold Chain Logistics Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Expanding pharma and vaccine distribution infrastructure | +0.9% | Java core and spill-over to Sulawesi and Sumatra secondary hubs | Medium term (2-4 years) |

| Rapid growth of online grocery and fresh food delivery | +1.1% | Greater Jakarta, Surabaya, Medan; expanding to tier-2 cities | Short term (≤ 2 years) |

| Rising middle-class demand for imported perishables | +0.7% | Java urban centers and Bali tourist zones | Medium term (2-4 years) |

| Government investment in cold storage hubs and ports | +0.8% | National, including West Java and eastern fishing ports | Long term (≥ 4 years) |

| Growth of modern retail chains and hypermarkets | +0.5% | Java, Bali, and select Sumatra cities | Medium term (2-4 years) |

| Increasing aquaculture and seafood export volumes | +0.7% | Coastal provinces and inter-island lanes | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Expanding Pharmaceutical and Vaccine Distribution Infrastructure Unlocks Specialized Cold Capacity

Pharmaceutical logistics is scaling with new certified facilities, tighter standards, and deeper integration with public health platforms, which directly expands specialized storage at 2–8°C, controlled room temperature, and ultra-low ranges. Indonesia’s health supply chain modernization includes digital interoperability through national systems and the SMILE platform, which links thousands of health centers to improve inventory accuracy and last-mile service reliability. Global logistics providers are also committing new capital to GDP-compliant hubs, with investments earmarked for the Asia Pacific and a regional role for Jakarta in healthcare flows, which strengthens the handling of biologics and time-critical products. These network upgrades complement domestic distributors that maintain nationwide footprints and oversight by regulators to ensure Good Distribution Practice adherence, which elevates service baselines for temperature-controlled handling. Taken together, these actions set higher compliance standards and unlock new capacity, which supports growth in vaccines and high-value therapeutics across the Indonesian cold-chain logistics market.[1]“Indonesia Confirms World’s First GDST-Compliant National Traceability System,” Global Dialogue on Seafood Traceability, thegdst.org

Rapid Growth of Online Grocery and Fresh Food Delivery Propels Hyperlocal Fulfillment Networks

Urban consumers are shifting to quick delivery for perishables, which compresses fulfillment cycles and raises the bar for temperature control in dark stores and neighborhood cross-docks. Policy support and public programs that deploy cold assets to provincial nodes help stabilize food prices and mitigate spoilage, while also increasing throughput for chilled and frozen staples. As retailers and platforms expand in dense corridors, operators scale refrigerated last-mile fleets and adopt visibility tools that assure product integrity during rapid handoffs and short hauls. Logistics companies that offer integrated warehousing, transport, and digital tools are positioned to win contracts from grocers and convenience chains that require high service levels and traceability. Investments in asset-light aggregation models and shared capacity also enable faster geographic coverage increases, which are critical to serving volatile fresh categories in the Indonesian cold-chain logistics market.

Government Investment in Cold Storage Hubs and Ports Strengthens National Food Security Architecture

The national logistics agenda prioritizes lower system costs and faster trade flows, which translates into targeted upgrades at ports, deeper inland networks, and standardized operating practices for cold cargo. New gateway capacity in West Java is scheduled to come online with phased expansions, which will redistribute load from congested terminals and offer specialized support for reefer containers. Strategic fishing port investments and program budgeting also help reduce post-harvest losses by enabling cold storage and handling standards in regions that ship large volumes of seafood[2] “Indonesia Cold Chain Infrastructure Summit 2025 Dorong Penguatan Ekosistem Rantai Pendingin Nasional,” Indonesia Manufacturing Center, imc.kemenperin.go.id. Cross-ministerial coordination and industry forums have aligned fiscal measures, standards, and digitalization, which creates a clearer pathway for private operators to commit long-duration capital to cold assets. These developments reduce friction in the flow of perishables and support consistent service levels, which strengthen the foundation for the Indonesian cold-chain logistics market.

Increasing Aquaculture and Seafood Export Volumes Necessitate Upgraded Port-to-Market Cold Chains

Seafood remains a high-volume and high-value export category, which calls for uninterrupted temperature control from vessel to port gate and through international corridors. Export earnings increased in 2025, with the United States remaining the largest buyer, while approvals for more processing units have expanded access to additional markets. National traceability adoption aligned with the GDST Standard enables interoperable data exchange across the seafood chain, which strengthens compliance and improves buyer confidence in key destinations. As coastal provinces scale aquaculture, demand grows for pre-cooling, frozen warehousing, reefer plugs, and shorter inter-island transits that protect quality and shelf life. The sector’s global position and the scale of fisheries output make it a structural anchor for capacity planning and export-focused service models within the Indonesian cold-chain logistics market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High electricity costs and unreliable power supply | -0.9% | Eastern Indonesia and intermittent grids in selected islands | Short term (≤ 2 years) |

| Fragmented cold chain infrastructure across archipelago | -0.6% | Outer islands and complex multi-island routes | Long term (≥ 4 years) |

| Limited trained workforce for temperature-controlled operations | -0.4% | National, more acute in rural and emerging cold zones | Medium term (2-4 years) |

| High capital expenditure for refrigerated fleet and warehouses | -0.5% | Nationwide, especially for SME operators and tier-2 entrants | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Electricity Costs and Unreliable Power Supply Constrain Efficiency Improvements

Electricity remains a large component of cold storage operating expenses, and supply reliability varies by region, which complicates the design of energy-efficient operations. Grid variability raises back-up power and maintenance needs, while also slowing the payback of newer refrigeration systems that reduce consumption. Facility operators respond by phasing in efficiency retrofits and selective use of on-site generation where feasible, which then depends on local permitting and economics. Industry groups have highlighted the cost pressures on operating models and the implications for service pricing in less dense markets. These factors slow both greenfield expansion and upgrades in weaker grid areas, which weighs on service quality and growth in the Indonesian cold-chain logistics market.

Fragmented Cold Chain Infrastructure Across the Archipelago Extends Lead Times

The country’s multi-island geography introduces handoff complexity and uneven asset distribution, which leads to variable service levels between primary and secondary corridors. Limited cold capacity in several outer islands increases reliance on longer routes or multiple transshipments that can extend lead times for sensitive cargo. National efforts to standardize and expand cold assets are progressing, yet private operators still face higher costs to position equipment across remote lanes. Coordination programs and port upgrades are reducing friction at key nodes, but fragmentation still challenges end-to-end temperature assurance across distant origins. These constraints require careful network planning and partnerships with local operators, which increases complexity in scaling the Indonesian cold-chain logistics market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Value-Added Services Gain Traction as Halal Mandates Reshape Operational Models

Refrigerated storage held 54.40% of the Indonesian cold-chain logistics market share in 2025, reflecting the core role of bulk capacity in national food security buffers and export flows. Storage operators are upgrading systems and procedures to align with evolving standards, including segregation practices for halal handling and documentation that supports export certifications. As ports and inland nodes add cold capacity, storage providers integrate closely with freight forwarders and national distributors that run multi-temperature networks serving retailers, processors, and health facilities. At the same time, service differentiation increasingly hinges on quality assurance, traceability, and the ability to support export-grade seafood and regulated pharmaceuticals, which favors operators with established compliance programs. This depth of capability gives incumbents leverage in contract wins and aligns with the Indonesian cold-chain logistics market orientation toward standards-driven growth.

Value-added services are the fastest-growing service type at a 4.75% CAGR through 2031 within the Indonesian cold-chain logistics market size, driven by demand for labeling, portioning, blast freezing, and validation services that offload complexity from shippers. Regulatory and buyer requirements that call for segregation in processing lines and clean documentation are increasing the share of outsourced, certified workflows. This shift allows producers and importers to focus resources on product and market development, while cold-chain specialists run in-warehouse processes under audited procedures that reduce risk at export checkpoints. Digital records and interoperable traceability systems further support claim management and buyer assurance, especially for seafood shipments into the United States and Europe. As more shippers prefer turnkey cold solutions, asset-light marketplaces and integrated 3PLs are expanding capacity and transport options to serve peaks, which reinforces momentum in value-added services.

By Temperature Type: Frozen Dominance Reflects Fishery Strength; Ambient Surges on Pharma Stability Shifts

Frozen storage at -18 to 0°C accounted for 57.35% of the Indonesian cold-chain logistics market in 2025, consistent with the country’s standing as a top global fisheries producer and exporter. Seafood categories, including shrimp and tuna, move in large volumes to key destinations, which underpins continuous demand for frozen warehousing, refer plugs, and quick vessel turnaround. As coastal regions scale output, producers focus on cold integrity from landing to container gate and rely on traceability frameworks that facilitate access to high-value markets. Frozen processed foods are also expanding their footprint with modern retail and foodservice networks that prefer consistent quality and extended shelf life. These patterns support the procurement of trailers and containers with reliable temperature control features and visibility tools that align with retailer standards in the Indonesian cold-chain logistics market.

Ambient cold chain is the fastest-growing band at a 5.54% CAGR through 2031, supported by the pharmaceutical sector’s shift toward controlled room temperature stability and large-scale public health programs that rely on reliable distribution. Healthcare distribution upgrades now emphasize dedicated temperature zones and monitoring to align with good national distribution practice oversight. Retail and e-commerce nodes also favor multi-temperature facilities that better orchestrate dry, chilled, and frozen SKUs for consolidated last-mile operations. As asset operators invest in modular layouts and WMS-controlled environments, temperature compliance becomes more repeatable at scale, which helps reduce spoilage and strengthens buyer confidence. These advancements shape a more resilient temperature mix within the Indonesian cold-chain logistics market.

By Application: Fish and Seafood Lead on Export Momentum; Pharmaceuticals Surge with Biopharma Ambitions

Fish and seafood led with a 42.25% share in 2025 within the Indonesian cold-chain logistics market size, supported by rising export value and sustained international demand. The United States remained the top destination for fishery exports in 2025, while approvals enabled additional processing units to serve China and Turkey with compliant cold-chain practices. National seafood traceability systems compliant with GDST strengthen interoperability and compliance with buyer requirements across the supply chain from pre-production to distribution. As coastal provinces expand into aquaculture hubs, operators invest in frozen and chilled capacity near harvest sites to shorten lead times and protect quality. These actions align logistics execution with export market standards and support consistent throughput in the Indonesian cold-chain logistics market.[3]“Fisheries Country Profile: Indonesia 2025,” SEAFDEC, seafdec.org

Pharmaceuticals and biologics are the fastest-growing application with a 6.21% CAGR forecast through 2031, reflecting domestic healthcare investments and heightened requirements for certified handling. Distributors that operate national footprints have strengthened cooperation with regulators to meet stringent standards while serving a broad network of outlets. International providers are committing capital to life science logistics platforms in the Asia Pacific, and Jakarta is positioned as a regional node for airfreight and clinical-trial support. Public health digitalization efforts and platform interoperability across the provider network strengthen stock visibility and last-mile performance for temperature-sensitive products. These shifts create predictable demand for multi-zone facilities and validated transport solutions within the Indonesian cold-chain logistics market.

Geography Analysis

Java held 62.10% of the Indonesian cold-chain logistics market share in 2025, anchored by the Greater Jakarta cluster of cold-chain companies and the presence of large distributors and retailers with multi-temperature networks[4]“Rantai Dingin Jadi Kunci: Badan Pangan Nasional Dorong Inovasi dan Kolaborasi,” Badan Pangan Nasional, badanpangan.go.id. Capacity additions at ports and the upcoming expansion of a major terminal in West Java are expected to redistribute loads from congested facilities and support higher flows of reefer containers. As the region hosts a dense concentration of pharmaceutical distribution and modern retail networks, suppliers and 3PLs maintain broader fleets and more sophisticated warehouse operations to meet delivery windows. This focus has supported sustained investments in storage modernization and qualified handling, and it continues to attract new services that favor compliant operations in Java’s primary corridors across the Indonesian cold-chain logistics market.

Sumatra is scaling faster on the back of aquaculture expansion and retail growth in cities such as Medan and Palembang, which drives demand for new cold storage nodes and reefer-equipped transport. National programs that distribute cold facilities to provincial beneficiaries help reduce post-harvest losses and stabilize prices, while encouraging private operators to commit more trucks and portable units. Domestic 3PLs with nationwide fleets extend services to these cities to support modern trade and food processors, and they leverage centralized control towers for trip visibility and compliance. As throughput rises, cold capacity near fishing grounds and processing sites reduces dependence on longer inter-island hauls and supports export timing to international markets that require strict cold integrity across the Indonesian cold-chain logistics market.

Sulawesi is projected to post the fastest regional CAGR at 4.33% through 2031, supported by fishing port development, tuna and skipjack exports, and Makassar’s increasing role as a logistics gateway for the east. Eastern regions, including Maluku and Papua, still face infrastructure gaps and power reliability issues, which increase operating costs and slow adoption of higher-efficiency refrigeration systems. Government support for cold storage assets and better port handling standards aims to reduce losses and improve readiness for export, while standards and traceability requirements push more operators to align with compliant practices across the Indonesian cold-chain logistics market.

The cold chain logistics market is analyzed by Mordor Intelligence across multiple other geographies, with in-depth regional assessments available for Africa and South America. This is complemented by country-specific insights for Thailand, Mexico, Sweden, and Netherlands, reflecting various localized market behavior and policy environments' coverage.

Competitive Landscape

The Indonesian cold-chain logistics market remains highly fragmented, with the top five providers collectively accounting for a relatively small share of the market in 2025, while numerous regional and local operators handle distribution across provinces and specialized product categories. Competition is largely based on service coverage, pricing, and the ability to manage temperature-controlled storage and transportation for perishable goods such as seafood, meat, and pharmaceuticals. While multinational logistics providers participate in export-oriented and pharmaceutical logistics segments, a significant portion of domestic cold chain activities continues to be managed by smaller operators serving localized supply chains. As a result, the Indonesian cold-chain logistics market is characterized by diverse service providers and varying infrastructure capabilities across regions.

Strategic moves emphasize network expansion and technology-enabled orchestration. DHL Group announced EUR 500 million (USD 540 million) in Asia Pacific investments by 2030 for integrated healthcare solutions, which complement Jakarta’s position as a regional hub for life science logistics. The company has also committed global capital of EUR 2 billion (USD 2.2 billion) by 2030 to upgrade pharma and cold-chain capabilities, reinforcing compliance at scale across its network. Domestic platforms are extending asset-light cold aggregation, with investments in third-party capacity and fleet solutions to accelerate coverage and meet rising service-level expectations in grocery and fresh categories.

Cross-border collaboration is increasing as regional logistics groups seek entry into Indonesia’s growth corridors. One major Thailand-listed logistics company disclosed a roadmap to expand cold storage investments across high-growth ASEAN countries, including Indonesia, which signals continued cross-border interest in partnerships and implements-roadmap-further-expanding-cold-storage-investment-base-from-clmv--china-to-high-growth-asean-countries). Domestic providers continue to professionalize operations through documented procedures and technology rollouts across large fleets of reefer trucks and multi-temperature warehouses serving modern retail and food service. As the Indonesian cold-chain logistics market matures, differentiation will favor integrated network control, verifiable compliance, and credible sustainability steps in energy management, which are becoming buyer expectations rather than optional features.

Indonesia Cold Chain Logistics Industry Leaders

Kiat Ananda Group

Enseval Putera Megatrading Tbk

MGM Bosco Logistics

Samudera Logistics

Pluit Cold Storage

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: The Ministry of Marine Affairs and Fisheries expanded market access for Indonesian fishery products to Turkey and China, securing approval numbers for 57 fish processing units that comply with HACCP and cold-chain standards.

- November 2025: Indonesia confirmed its national seafood traceability system is fully compatible with the GDST Standard, enabling interoperable data exchange with international trading partners.

- August 2025: The Ministry of Industry hosted the Indonesia Cold Chain Infrastructure Summit to harmonize fiscal incentives and non-fiscal policies for cold-chain development and local content priorities.

- April 2025: DHL Group announced EUR 500 million (USD 540 million) in Asia Pacific healthcare logistics investments by 2030, reinforcing Jakarta’s role in regional flows.

Indonesia Cold Chain Logistics Market Report Scope

Cold chains are supply chain that specializes in storing, transporting, and preserving cargo that needs to be maintained at a specific temperature or within an acceptable temperature range. It has evolved due to a growing need for temperature-controlled logistics to transport large quantities of food over great distances safely.

The Indonesia Cold-Chain Logistics Market Report is Segmented by Service Type (Refrigerated Storage, Refrigerated Transportation, and Value-Added Services), by Temperature Type (Chilled 0–5 °C, Frozen -18–0 °C, and More), by Application (Fruits & Vegetables, Meat & Poultry, and More), and by Geography (Java, Sumatra, Kalimantan, Sulawesi, Bali & Nusa Tenggara, Others). The Market Forecasts are Provided in Terms of Value (USD).

| Refrigerated Storage | Public Warehousing |

| Private Warehousing | |

| Refrigerated Transportation | Road |

| Rail | |

| Sea | |

| Air | |

| Value-Added Services |

| Chilled (0–5 °C) |

| Frozen (-18–0 °C) |

| Ambient |

| Deep-Frozen / Ultra-Low (less than-20 °C) |

| Fruits & Vegetables |

| Meat & Poultry |

| Fish & Seafood |

| Dairy & Frozen Desserts |

| Bakery & Confectionery |

| Ready-to-Eat Meals |

| Pharmaceuticals & Biologics |

| Vaccines & Clinical Trial Materials |

| Chemicals & Specialty Materials |

| Other Perishables |

| Java (Jakarta & BOD) |

| Sumatra |

| Kalimantan |

| Sulawesi |

| Bali & Nusa Tenggara |

| Others |

| By Service Type | Refrigerated Storage | Public Warehousing |

| Private Warehousing | ||

| Refrigerated Transportation | Road | |

| Rail | ||

| Sea | ||

| Air | ||

| Value-Added Services | ||

| By Temperature Type | Chilled (0–5 °C) | |

| Frozen (-18–0 °C) | ||

| Ambient | ||

| Deep-Frozen / Ultra-Low (less than-20 °C) | ||

| By Application | Fruits & Vegetables | |

| Meat & Poultry | ||

| Fish & Seafood | ||

| Dairy & Frozen Desserts | ||

| Bakery & Confectionery | ||

| Ready-to-Eat Meals | ||

| Pharmaceuticals & Biologics | ||

| Vaccines & Clinical Trial Materials | ||

| Chemicals & Specialty Materials | ||

| Other Perishables | ||

| By Region (Indonesia) | Java (Jakarta & BOD) | |

| Sumatra | ||

| Kalimantan | ||

| Sulawesi | ||

| Bali & Nusa Tenggara | ||

| Others | ||

Key Questions Answered in the Report

What is the current size and growth outlook for the Indonesian cold-chain logistics market?

The Indonesian cold-chain logistics market stands at USD 7.19 billion in 2025 and is projected to reach USD 9.24 billion by 2031 at a 4.23% CAGR.

Which service and temperature segments are leading and growing fastest in Indonesia?

Refrigerated storage leads with 54.40% share, while value-added services are the fastest-growing at 4.75% CAGR; frozen dominates with 57.35% share, and ambient is the fastest-growing at 5.54% CAGR.

Which applications drive the most cold-chain volume and value in Indonesia?

Fish and seafood hold 42.25% share, backed by export demand, while pharmaceuticals and biologics show the fastest expansion at a 6.21% CAGR through 2031.

Which region is the largest hub for cold-chain activity in Indonesia?

Java commands 62.10% share, supported by concentrated distribution networks and retail activity, with Sulawesi expected to post the fastest growth at 4.33% through 2031.

How is government policy influencing cold-chain infrastructure expansion?

National initiatives align fiscal incentives and standards for cold nodes and ports, while regional deployments of cold assets stabilize food prices and reduce losses.

What developments are shaping pharmaceutical cold-chain services in Indonesia?

Certified hubs and digitalized public health logistics are expanding, with international providers investing in Asia Pacific healthcare platforms centered around Jakarta.

Page last updated on: