Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

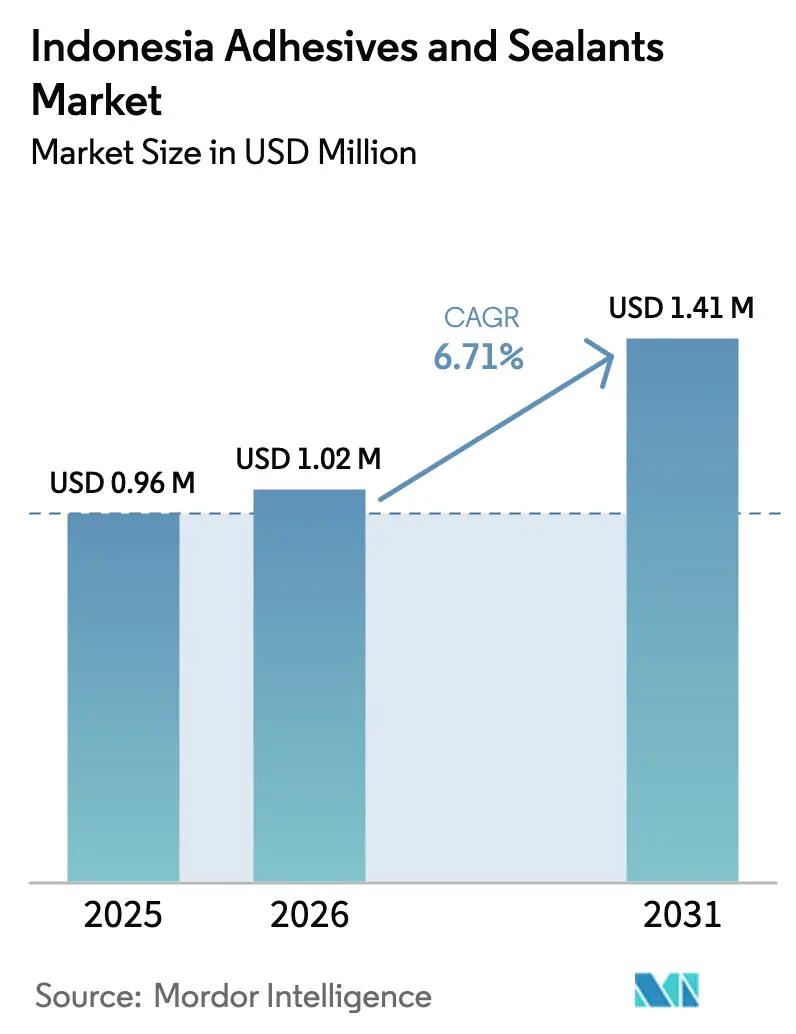

| Base Year Market Size (2025) | USD 0.96 Million |

| Market Size (2026) | USD 1.02 Million |

| Market Size (2031) | USD 1.41 Million |

| Growth Rate (2026 - 2031) | 6.71% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Indonesia Adhesives And Sealants Market Analysis by Mordor Intelligence

The Indonesia Adhesives and Sealants Market size is projected to be USD 0.96 million in 2025, USD 1.02 million in 2026, and reach USD 1.41 million by 2031, growing at a CAGR of 6.71% from 2026 to 2031. Public infrastructure megaprojects, from the IKN Nusantara capital relocation to dozens of toll-road corridors, are lifting construction adhesive volumes, while the footwear, furniture, and electronics clusters in Java are switching to low-VOC (Volatile Organic Compound) and bio-based chemistries to keep export permits valid under emerging European Union (EU) rules. Multinationals now operate regional technology hubs, yet local manufacturers leverage island-wide distributor relationships to reach smaller buyers that demand flexible pack sizes and near-real-time service. In addition, palm-oil-derived polyols, lignin, and used-cooking-oil feedstocks are progressing from pilot trials to semi-commercial batches, signaling a possible leapfrog toward bio-based polyurethane systems within the planning horizon. The combined result is a market where performance, compliance, and sustainability requirements evolve faster than historical five-year formulation cycles, forcing suppliers to accelerate research and development, logistics, and training investments to defend share.

Key Report Takeaways

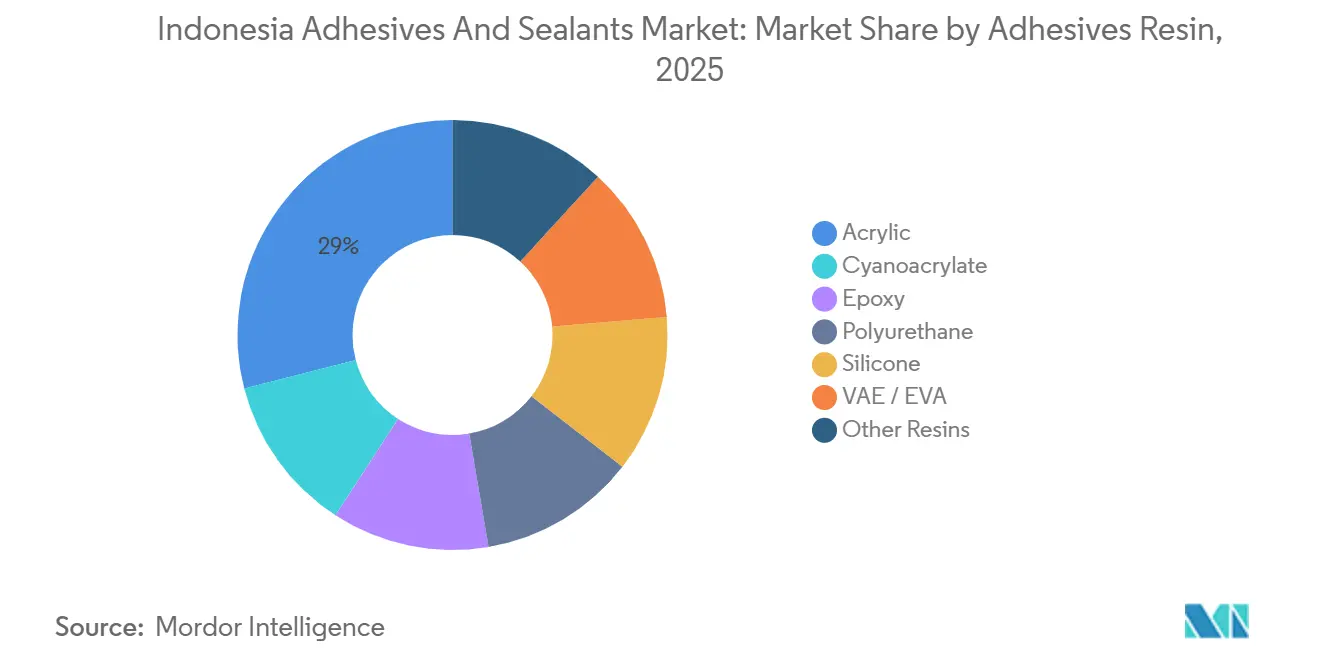

- By adhesives resin, acrylic accounted for 29.00% of the market share in 2025, and the share of polyurethane is expected to increase at a CAGR of 7.02% during the forecast period (2026-2031).

- By adhesives technology, water-borne had a share of 38.40% of the market in 2025, and reactive's share is expected to increase at a CAGR of 6.97% during the forecast period (2026-2031).

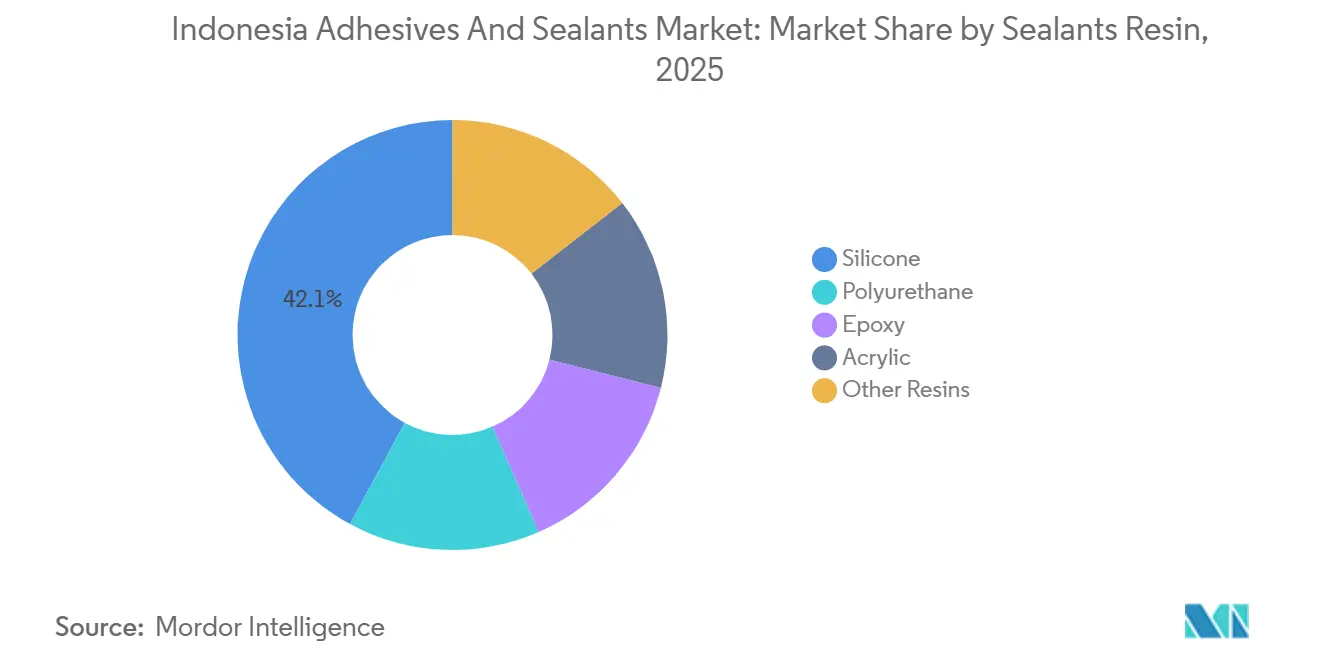

- By sealants resin, silicone had a market share of 42.10% in 2025, and this share is poised to increase at a CAGR of 6.96% during the forecast period (2026-2031).

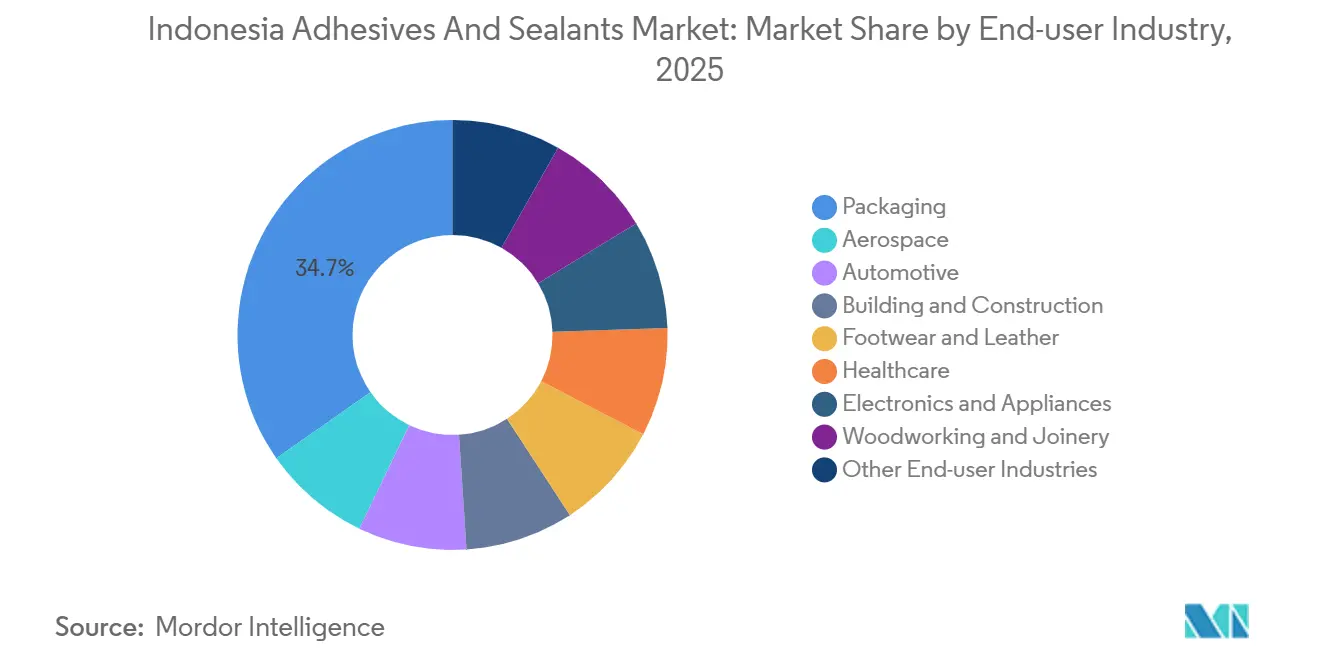

- By End-user Industry, packaging had a share of 34.70% in 2025, and the share of electronics and appliances is expected to grow at a CAGR of 6.89% during the forecast period (2026-2031).

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Indonesia Adhesives And Sealants Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Robust growth in FMCG flexible packaging | +1.2% | Java metropolitan clusters | Medium term (2-4 years) |

| Mega-infrastructure pipeline | +1.8% | Kalimantan and trans-Java corridors | Long term (≥ 4 years) |

| Footwear export-oriented expansion | +0.9% | West Java and Banten industrial estates | Medium term (2-4 years) |

| Hot-melt uptake in e-commerce logistics | +1.1% | Jakarta and Surabaya fulfillment hubs | Short term (≤ 2 years) |

| Furniture SMEs adopting water-based systems | +0.7% | Central Java (Jepara furniture cluster) | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Robust Growth in Indonesia’s FMCG Flexible-Packaging Sector

Flexible packaging output rose to 159.2 billion units in 2024, up from 141.3 billion in 2019, and brand-owner circularity pledges compel laminating and pressure-sensitive adhesive suppliers to guarantee food contact, recycling compatibility, and higher heat-resistance thresholds. Multinationals respond with rapid-cure hot melts optimized for automated case-forming lines, while smaller converters struggle to certify formulations under evolving EU and ASEAN regulations. The volume surge is therefore widening the technology gap and consolidating demand around suppliers that run regional pilot labs, food-contact testing, and digital traceability platforms.

Ongoing Mega-Infrastructure Projects Accelerating Construction Adhesives Demand

Government infrastructure approvals totaling CHF 25 billion (USD 27.84 billion) in 2023 and an overall construction wallet valued at CHF 240 billion (USD 272.69 billion) in 2024 continue to drive tile-adhesive, grout, and structural bonding demand at above-GDP rates[1]Sika AG, “Sika Indonesia Expansion Press Release,” sika.com. Revised SNI performance norms aligned with ISO 13007 now influence public tenders, shifting volume toward ISO-compliant brands that can guarantee long-term durability in humid coastal and seismic zones. Mega-bridges, new airports, and high-rise residential towers thus anchor a long-tail pull for mortar, sealant, and concrete-repair chemistries.

Expansion of Domestic Footwear Manufacturing for Export Markets

Polyurethane formulations earn preference among Indonesia’s athletic-shoe assemblers because they combine peel strength with resistance to flex fatigue under tropical humidity. In-country adhesive academies teach operators consistent coating, drying, and press-curing parameters, reducing delamination rejects at finishing-line quality gates. The parallel migration toward water-borne PU variants to meet EU solvent-emission ceilings, however, splits the market: high-performance lines keep solvent systems, while mid-tier exporters adopt water-based grades that meet cost and compliance constraints.

Rapid Adoption of Hot-Melt Technologies in E-Commerce Logistics Packaging Lines

Same-day parcel delivery targets press fulfillment centers to cut dwell time, favoring sub-second-set hot-melt beads over slower water-based options[2]Henkel Adhesives, “Technomelt E-COM Product Sheet,” henkel-adhesives.com. Reactive moisture-cure hot melts now bond heavier corrugated grades without cold-flow failures, and the rise of right-size packaging limits void fill, further elevating adhesive line-speed expectations. Suppliers must therefore serve both bulk granulate orders for automated lines and small cartridge packs sold via online marketplaces to cottage-scale sellers, forcing dual channel models.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatility in imported petrochemical prices | -1.4% | Java-centric formulators dependent on imported monomers | Short term (≤ 2 years) |

| Persistent rupiah depreciation | -0.9% | Nationwide, especially SME formulators without hedging | Medium term (2-4 years) |

| Fragmented inter-island logistics | -0.6% | Sulawesi, Maluku, Papua distribution routes | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Volatility in Imported Petrochemical Feedstock Prices

Indonesia imports about 42% of polyethylene and 57% of polypropylene, so adhesive grade EVA, VAE, and SB latex prices move with naphtha and exchange fluctuations. Multinationals with captive resin plants hedge risk through multiyear offtake contracts, while small batch blenders rely on spot cargoes, amplifying cost swings. Upcoming domestic cracker expansions may ease shortages after 2027, but near-term exposure remains a working-capital constraint.

Fragmented Inter-Island Logistics Inflating Distribution Costs

Serving 17,000 islands forces multi-modal truck-ferry-truck loops that add 20-30% to delivered cost outside Java, and temperature-sensitive hot melts require reefers seldom available beyond major ports. The situation rewards companies that invest in hub-and-spoke micro-blending stations or contract third-party warehouses in secondary cities, but capital and regulatory barriers deter most local competitors.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Adhesives Resin: Polyurethane Momentum Outpaces Acrylic Dominance

Acrylic maintained a 29.00% share in 2025 of the Indonesia Adhesives and Sealants market. The market size for polyurethane products is projected to expand at a 7.02% CAGR as athletic-shoe exporters specify higher heat resistance and peel strength. Research on palm-oil-derived polyols and lignin-based non-isocyanate routes demonstrated 26.2 MPa shear strength, validating a future shift toward safer, renewable feedstocks.

Indonesia Adhesives and Sealants market gains from acrylic emulsions remain anchored in tapes, labels, and low-cost woodworking glues, but escalating EU VOC ceilings push converters toward water-borne PU grades. Epoxies, cyanoacrylates, and phenol-formaldehyde occupy niche positions in electronics, MRO, and plywood. The widening performance-price spectrum allows multinationals to segment portfolios across chemistry families, while local formulators focus on acrylic or animal-glue lines that require lower capital intensity.

By Adhesives Technology: Water-Borne Systems Lead, Reactive Hot Melts Accelerate

Water-borne products held 38.4% share in 2025 and dominate furniture, footwear, and graphic-arts lamination lines. Hybrid polyurethane-acrylic dispersions improve early green strength, reducing press time. Indonesia Adhesives and Sealants market share for reactive hot-melt technology is set to climb at a CAGR of 6.97% during the forecast period (2026-2031) because e-commerce carton makers value instant green strength and high final bond without ovens.

Solvent-borne lines remain essential for specialty footwear requiring the highest peel, while UV-curable and anaerobic systems serve electronics and maintenance niches. Suppliers now run dual pilot lines, water-borne for training SME users in Central Java and moisture-cure hot melts for Jakarta logistics hubs, to demonstrate line-speed economics before buyers commit.

By Sealants Resin: Silicone Leads Coastal and Electronics Applications

Silicone accounted for 42.1% of volume in 2025 and is forecast at 6.96% CAGR through 2031, driven by curtain-wall glazing and marine infrastructure that demand UV and salt-spray resilience. Indonesia Adhesives and Sealants market size for polyurethane sealants follows, targeting civil-structure expansion joints. Acrylic and butyl offerings remain interior or commodity choices. Hybrid silicone-polyurethane chemistries capable of matching silicone weathering at lower cost represent a white-space innovation prospect.

Electronics assembly further reinforces silicone growth: conformal coatings for smartphones and appliances must survive thermal cycling and high humidity, properties where silicone prevails. Local compounders with vacuum-degassing and precision-metering equipment can differentiate in this segment, but entry costs remain high for small firms.

By End-user Industry: Packaging Dominance, Electronics Fastest-Growing

Packaging contributed 34.7% of 2025 revenue as FMCG groups produced 159.2 billion units, and e-commerce mailers spiked corrugated consumption. Brand-owner recyclability mandates oblige adhesive formulators to validate clean-release and low-odour recipes compatible with rPET and polyolefin recycling streams. Electronics and appliances are expected to generate the highest CAGR at 6.89% during the forecast period (2026-2031), propelled by RFID-enabled smart labels and potting compounds for regional assembly plants run by Samsung and LG.

Construction keeps steady growth within the Indonesia Adhesives and Sealants market, piggybacking government megaprojects. Footwear retains export-led potential, while woodworking and joinery ride EU deforestation-free compliance waves that push SMEs to water-based or bio-based chemistries. Healthcare and hygiene remain minor but stable end-use outlets.

Geography Analysis

Java absorbs the bulk of Indonesia Adhesives and Sealants market demand, reflecting its concentration of FMCG, footwear, and furniture factories. Within Java, West Java and Banten host export-oriented footwear clusters that prioritize polyurethane and water-borne upgrades, while Central Java’s furniture hub drives acrylic and PU dispersions. Tier-one cities Jakarta, Surabaya, and Bandung anchor distributor headquarters and technical service labs that guide the adoption of new chemistries.

Kalimantan’s IKN Nusantara project lifts sealant and mortar pulls for multi-year infrastructure contracts. The island’s humid, high-rainfall climate causes specifiers to mandate silicone weatherproofing and high-flex PS adhesives on bridge expansion joints. Sumatra contributes palm-oil raw-material flow for bio-based initiatives, and planned refinery expansions could see polyol plants co-located with oleochemical complexes by the end of the decade.

Sulawesi, Maluku, and Papua remain underserved due to freight premiums and limited cold-chain warehousing. Suppliers who build micro-hubs in Makassar or Manado can win market entry ahead of expected mining, smelting, and public housing growth. However, any warehouse must carry flexible power backup and humidity control to protect water-borne stocks from tropical degradation.

Competitive Landscape

The Indonesia Adhesives and Sealants market is moderately concentrated. Multinationals such as Sika, Henkel, BASF, and H.B. Fuller control regional R&D centers, ISO-accredited labs, and automated bulk plants. Revised SNI tile-adhesive norms may force small importers out of public tenders, nudging concentration further. Suppliers able to commercialize palm-based bio-resins at scale could capture green-procurement premiums, but pilot-to-plant financing remains the critical bottleneck.

Indonesia Adhesives And Sealants Industry Leaders

3M

H.B. Fuller Company

Henkel AG & Co. KGaA

Sika AG

Arkema

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Avian Brands, through the issuance of new shares, acquired a 16.67% equity stake in PT Dextone Lemindo, an adhesive and glue manufacturer, with an investment of USD 17.9 million. This move not only broadened Avian's product portfolio in the adhesive sector but also capitalized on its strategic distribution foothold for Dextone products.

- March 2025: Hindustan Adhesives' board of directors greenlit an investment in PT. Bagla Group Indonesia. As a result of this investment, PT. Bagla Group Indonesia started operating as a subsidiary of Hindustan Adhesives. This acquisition was likely motivated by objectives of expanding operations in Indonesia's manufacturing and trade sectors.

Indonesia Adhesives And Sealants Market Report Scope

Adhesives are substances that are capable of holding at least two surfaces together in a strong and permanent manner, while sealants are designed to close gaps between surfaces and prevent things such as water, dust, or dirt from entering them.

The Indonesia adhesives and sealants market is segmented into adhesives by resin, adhesives by technology, sealants by resin, and end-user industry. Based on adhesive by resin, the market is segmented into acrylic, cyanoacrylate, epoxy, polyurethane, silicone, VAE/EVA, and other adhesives by resin. Based on adhesive by technology, the market is segmented into hot melt, reactive, solvent-borne, UV-cured, and waterborne. Based on sealant by resin, the market is segmented into polyurethane, epoxy, acrylic, silicone, and other sealants by resin. Based on the end-user industry, the market is segmented into aerospace, automotive, building and construction, footwear and leather, healthcare, packaging, electronics and appliances, woodworking and joinery, and other end-user industries. The market sizing and forecasts for each segment have been done on the basis of value (USD).

Adhesives by Resin

| Acrylic |

| Cyanoacrylate |

| Epoxy |

| Polyurethane |

| Silicone |

| VAE / EVA |

| Other Resins |

Adhesives by Technology

| Hot Melt |

| Reactive |

| Solvent-borne |

| UV Cured |

| Water-borne |

Sealants by Resin

| Polyurethane |

| Epoxy |

| Acrylic |

| Silicone |

| Other Resins |

By End-user Industry

| Aerospace |

| Automotive |

| Building and Construction |

| Footwear and Leather |

| Healthcare |

| Packaging |

| Electronics and Appliances |

| Woodworking and Joinery |

| Other End-user Industries |

| Adhesives by Resin | Acrylic |

| Cyanoacrylate | |

| Epoxy | |

| Polyurethane | |

| Silicone | |

| VAE / EVA | |

| Other Resins | |

| Adhesives by Technology | Hot Melt |

| Reactive | |

| Solvent-borne | |

| UV Cured | |

| Water-borne | |

| Sealants by Resin | Polyurethane |

| Epoxy | |

| Acrylic | |

| Silicone | |

| Other Resins | |

| By End-user Industry | Aerospace |

| Automotive | |

| Building and Construction | |

| Footwear and Leather | |

| Healthcare | |

| Packaging | |

| Electronics and Appliances | |

| Woodworking and Joinery | |

| Other End-user Industries |

Key Questions Answered in the Report

How large will adhesive and sealant demand be in Indonesia by 2031?

The Indonesia Adhesives and Sealants market size is projected at USD 1.41 million in 2031, up from USD 1.02 million in 2026.

Which resin chemistry is growing fastest?

Polyurethane grades lead with a forecast 7.02% CAGR through 2031, largely due to footwear and automotive export requirements.

Why are hot-melt adhesives gaining share?

Same-day e-commerce delivers throughput pressures that favor sub-second-set hot melts and reactive moisture-cure systems.

What is the main restraint facing local formulators?

Cost volatility from imported petrochemical feedstocks and rupiah depreciation compresses margins for Java-based SMEs.

Page last updated on: