Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

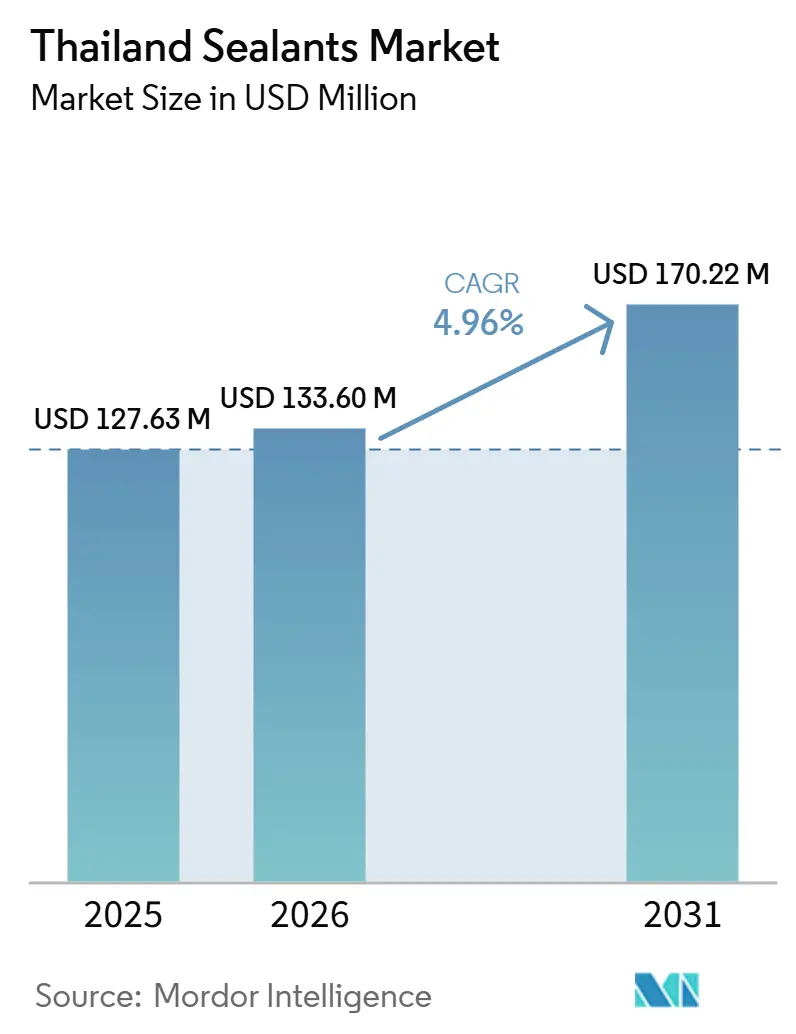

| Base Year Market Size (2025) | USD 127.63 Million |

| Market Size (2026) | USD 133.60 Million |

| Market Size (2031) | USD 170.22 Million |

| Growth Rate (2026 - 2031) | 4.96% CAGR |

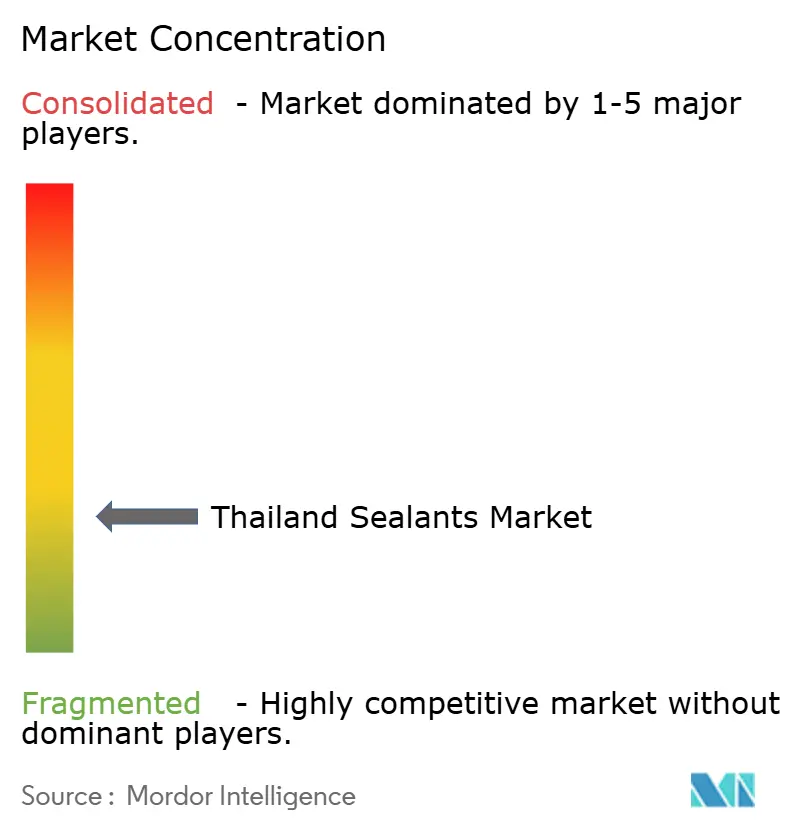

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Thailand Sealants Market Analysis by Mordor Intelligence

The Thailand Sealants Market size is projected to grow from USD 127.63 million in 2025 to USD 133.60 million in 2026, and reach USD 170.22 million by 2031, growing at a CAGR of 4.96% from 2026 to 2031. Momentum is coming from Eastern Economic Corridor (EEC) infrastructure, electric-vehicle platforms led by Chinese and Japanese OEMs, and a renovation upcycle across Bangkok’s high-rise stock. Hybrid chemistries are earning share as formulators blend polyurethane strength with silicone weatherability, while supply-chain localization lowers lead times for automotive and electronics clusters. Margin pressure persists because volatile naphtha, propylene, and PVC prices collide with stricter VOC rules that require costly reformulation and third-party testing. Competitive intensity is moderate yet rising: multinationals are acquiring Thai assets to capture Board of Investment incentives, and local champions are upgrading product lines to protect distribution strongholds.

Key Report Takeaways

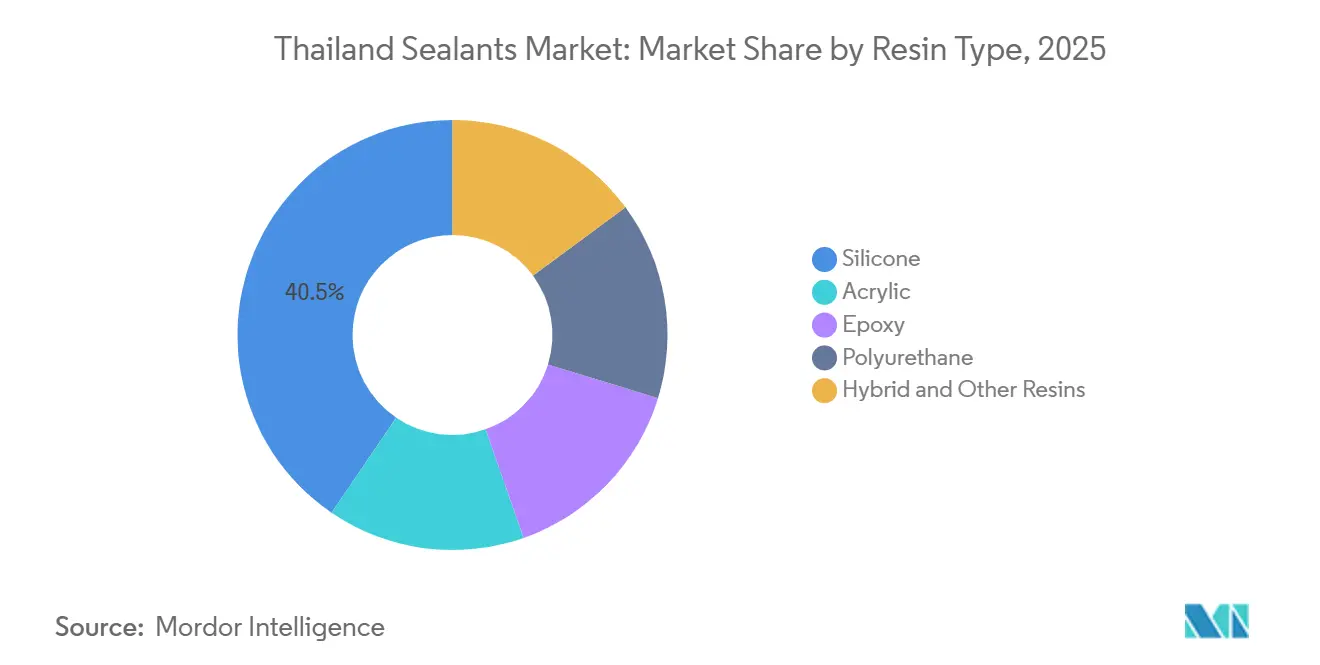

- By resin type, silicone commanded 40.50% of the Thailand sealants market share in 2025. Hybrid and other resins are projected to advance at a 6.76% CAGR through 2031.

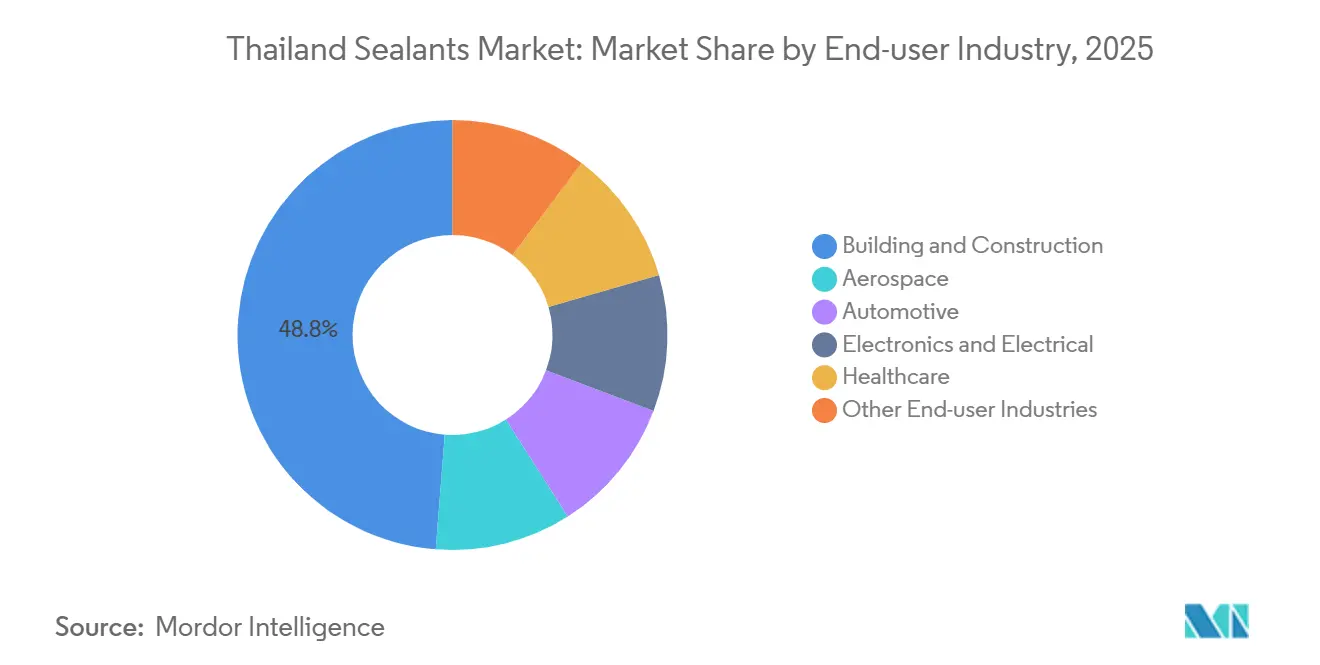

- By end-user industry, building and construction led with 48.75% revenue share in 2025. The electronics and electrical segment is forecast to expand at a 6.23% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Thailand Sealants Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Infrastructure boom under Thailand's Eastern Economic Corridor (EEC) programme | +1.2% | EEC provinces (Chonburi, Rayong, Chachoengsao), spillover to Bangkok metropolitan region | Medium term (2–4 years) |

| Automotive-EV production expansion by OEMs | +1.0% | Rayong, Samut Prakan, Chonburi (auto clusters) | Medium term (2–4 years) |

| Urban high-rise and condominium renovations demanding premium weatherproofing | +0.8% | Bangkok, Phuket, Pattaya, Chiang Mai (urban centers) | Short term (≤ 2 years) |

| Electronics export clusters fueling demand for high-purity silicone sealants | +0.9% | Chonburi (Laem Chabang), Ayutthaya, Pathum Thani (electronics hubs) | Long term (≥ 4 years) |

| DIY-retail surge via e-commerce platforms boosting small-pack acrylic sales | +0.5% | National, with early gains in Bangkok, Nonthaburi, Samut Prakan | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Infrastructure Boom Under Thailand’s Eastern Economic Corridor

The EEC attracted USD 60.23 billion of investment applications in 2025, channeling capital into smart estates such as WHA ESIE 5[1]Iconic Research Thailand, “EEC Investment Dashboard 2025,” iconicresearchthailand.com. Data-center shells specify fire-rated joint sealants and cable-penetration firestops, while battery cleanrooms call for ionic-controlled silicone formulations. Thailand FastPass cuts permit times by up to 50%, favoring suppliers that hold local inventory and offer on-site technical service. Framework agreements now dominate procurement, locking in performance specifications early and reducing mid-project substitutions.

Automotive-EV Production Expansion by OEMs

BYD and GAC Aion inaugurated Thai assembly in July 2024, underpinning a national 30@30 target that ties incentives to domestic content. Battery-pack sealing requires silicone and polyurethane chemistries that retain adhesion from -40 °C to +90 °C and meet UL 94 V-0. Covestro’s planned acquisition of the Vencorex HDI site in Rayong secures aliphatic isocyanate supply for two-component polyurethane systems. Automated six-axis robots on EV lines demand tight viscosity control, raising quality-system thresholds for local compounders.

Urban High-Rise and Condominium Renovations

Bangkok’s 2010-2015 tower boom is moving into a refurbishment wave focused on façade weatherproofing. TOA Paint upgraded its 201 Roofseal to a PU-hybrid in 2024, raising service life to 7 years and complying with TIS 3056-2563. Developers such as Sansiri now specify silane-modified polymer sealants certified to ISO 11600 25HM, boosting upfront costs yet cutting long-run maintenance. Third-party Environmental Product Declarations are increasingly mandatory for LEED and WELL points.

Electronics Export Clusters Fueling High-Purity Silicone Demand

Seven data centers secured BOI approval in early 2026, spurring demand for low-ionic silicones that avoid server-rack corrosion. Regional capacity additions by Wacker in South Korea escalate performance benchmarks to sub-10 ppm chloride[2]ChemEngOnline, “Wacker Starts Up Specialty Silicones Lines,” chemengonline.com. Edge-AI servers elevate thermal-interface requirements, opening white space for Thai mixers that can process boron-nitride-filled gap fillers above 3 W/m·K.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Petrochemical feedstock price volatility compressing margins | -0.7% | National, with acute impact on Map Ta Phut and Rayong petrochemical clusters | Short term (≤ 2 years) |

| Stricter VOC and chemical compliance raising reformulation costs | -0.5% | National, with early adoption in Bangkok and EEC green-building projects | Medium term (2–4 years) |

| Shortage of certified applicators | -0.3% | National, concentrated in secondary cities (Chiang Mai, Hat Yai, Khon Kaen) | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Petrochemical Feedstock Volatility Compressing Margins

Naphtha averaged USD 674 per ton in 2024, dipping to USD 607 in H1 2025, yet propylene and PVC remained high, trimming converter gross margins by 200-300 bps. Extended inventories to 120 days, as practiced by TOA Paint, reflect supply-risk hedging. Increased recycled-HDPE use introduces certification costs under ISCC Plus, adding further variability.

Stricter VOC and Chemical Compliance

Thai green-building councils are adopting the EU’s 0.080 mg/m³ formaldehyde ceiling effective August 2026, forcing extra EN 16516 chamber testing at TÜV Rheinland’s Bangkok lab, where lead times can stretch to six weeks. Category 2 and 3 chemical registration under the Hazardous Substance Act also adds paperwork for foreign entrants.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Resin Type: Silicone Dominance Reflects Electronics and Façade Specifications

Silicone captured 40.50% of the Thailand sealants market in 2025, ruled by electronics clusters that require less than 10 ppm ionic contamination and urban façades that demand UV stability. Hybrid and other resins are advancing at a 6.76% CAGR through 2031 as contractors value ±25% movement and over-paintability. Sika’s Hybriflex SMP demonstrates this shift by blending polyurethane toughness with silicone weatherability. Polyurethane systems remain entrenched in EV battery packs, where aliphatic isocyanates sourced from Covestro’s soon-to-close Rayong site reduce cure-time variability. Acrylic dominates DIY channels, though household debt curbs discretionary renovations. Epoxies stay niche for Map Ta Phut chemical plants that need strong chemical resistance.

Regulatory and capacity moves reinforce these patterns. Wacker’s new specialty-silicones complex in Zhangjiagang and Jincheon lines ratchet purity benchmarks, pressing local mixers to match. Bostik’s 46% bio-based hybrid with EC1 PLUS and M1 certification signals the sustainability pivot transforming premium bids. The Thailand Industrial Standards Institute’s TIS 1321-2566 enforcement from March 2024 adds adhesion-test hurdles that smaller compounders must outsource, lengthening product-launch cycles.

By End-User Industry: Construction Leads, Electronics Accelerates

Building and construction accounted for 48.75% of Thailand sealants market size in 2025, driven by EEC megaprojects and Bangkok refurbishment. Electronics and electrical is the fastest climber at a 6.23% CAGR through 2031, as seven data centers approved in 2026 and semiconductor packaging sites in Ayutthaya demand low-outgassing silicones. Automotive share is smaller but rising quickly: BYD and GAC Aion aim for 320,000 EVs per year at full ramp, introducing UL 94 V-0 sealant specifications. Healthcare remains a niche but strictly regulated under ISO 10993 and GMP, limiting entrants. Aerospace usage is minor, confined to MRO at U-Tapao.

WHA ESIE 5’s forward sales underline the industrial pull that buffers against retail volatility. TOA Paint set aside THB 700 million (USD 20 million) for factory upgrades and new waterproofing capacity, signaling local players’ response to higher-spec demand. AICA’s majority stake in ADB Sealant provides instant access to a 40-year export network spanning ASEAN and beyond, illustrating consolidation as a route to distribution breadth.

Geography Analysis

EEC provinces, Chonburi, Rayong, and Chachoengsao, collectively capture a significant share of new industrial-estate supply and dominate Thailand's sealants market demand. Chonburi leads data-center builds thanks to Laem Chabang port connectivity, while Rayong hosts EV assembly and petrochemical feedstocks, highlighted by Covestro’s HDI acquisition slated for close in 2025. Chachoengsao positions itself as a smart-city hub, boosting demand for interior and façade weatherproofing in commercial projects.

Greater Bangkok remains the single largest renovation market, with aging condos undergoing façade resealing to secure LEED or WELL points. Phuket, Pattaya, and Chiang Mai show moderate growth in hospitality developments, where coastal humidity and salt necessitate premium silicone. Provincial clusters benefit from FastPass permit acceleration, shortening build windows and favoring suppliers with in-country stock. BASF’s Bangpakong alkyl-polyglucosides plant in Chonburi supplies bio-surfactants that double as rheology modifiers in sustainable sealants.

Supply-chain clustering breeds agility yet heightens systemic risk: any port congestion or energy outage could ripple through converters and end-users within the same corridor. Momentive’s second Rayong silicones facility, announced for 2026 completion, adds redundancy and reduces import reliance.

Competitive Landscape

The Thailand sealants market is fragmented. Covestro’s Vencorex deal secures critical aliphatic isocyanates, signaling upstream integration to ensure supply for polyurethane sealants. TOA Paint leverages a 77-province dealer network plus modern-trade ties with HomePro and Thai Watsadu, turning distribution reach into a moat. AICA’s ADB purchase demonstrates mergers and acquisitions as an avenue for immediate market share and export licenses.

Sustainability is a differentiator. SCG Chemicals’ 45,000 tons per annum recycled-HDPE line offers ISCC Plus feedstock, yet most converters hesitate over batch consistency. Henkel’s 2025 Shanghai Inspiration Center underscores the research and development gap Thai formulators face. Momentive’s 2026 Asia-Pacific silane joint venture highlights the shift toward “in-region for region” sourcing that buffers currency risk.

Regulation shapes barriers. TIS 1321-2566 demands in-house adhesion labs or expensive outsourcing, tilting the advantage to large players. Large contractors now pre-qualify suppliers at master-planning, making early engagement essential to win multi-year framework deals.

Thailand Sealants Industry Leaders

3M

Dow

Henkel AG & Co. KGaA

Sika AG

H.B. Fuller Company

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: TOA Paint upgraded 201 Roofseal to a PU-hybrid that meets TIS 3056-2563 and lengthens service life to 7 years.

- September 2024: AICA Asia Pacific agreed to acquire 51% of ADB Sealant to strengthen its Southeast Asian adhesive and sealant portfolio.

Thailand Sealants Market Report Scope

Sealants are elastomeric materials used to fill gaps, joints, or cracks, preventing water, air, dust, and fluid passage. Widely applied in construction and industrial sectors, they ensure waterproofing and structural flexibility in buildings, windows, automotive components, and appliances.

The Thailand sealants market is segmented by resin type and end-user industry. By resin type, the market is segmented into acrylic, epoxy, polyurethane, silicone, and hybrid and other resins. By end-user industry, the market is segmented into aerospace, automotive, building and construction, electronics and electrical, healthcare, and other end-user industries. For each segment, the market sizing and forecasts have been done based on revenue (USD).

By Resin Type

| Acrylic |

| Epoxy |

| Polyurethane |

| Silicone |

| Hybrid and Other Resins |

By End-user Industry

| Aerospace |

| Automotive |

| Building and Construction |

| Electronics and Electrical |

| Healthcare |

| Other End-user Industries |

| By Resin Type | Acrylic |

| Epoxy | |

| Polyurethane | |

| Silicone | |

| Hybrid and Other Resins | |

| By End-user Industry | Aerospace |

| Automotive | |

| Building and Construction | |

| Electronics and Electrical | |

| Healthcare | |

| Other End-user Industries |

Market Definition

- End-user Industry - Building & Construction, Automotive, Aerospace, Healthcare, and Others are the end-user industries considered under the sealants market.

- Product - All sealant products are considered in the market studied

- Resin - Under the scope of the study, resins like Polyurethane, Epoxy, Acrylic, Silicone, and Others are considered

- Technology - For the purpose of this study, One component and Two component sealant technologies are taken into consideration.

| Keyword | Definition |

|---|---|

| Hot-melt Adhesive | Hot melt adhesives are generally 100% solid formulations, based on thermoplastic polymers. They are solid at room temperature and are activated upon heating above their softening point, at which stage they are liquid, and hence, can be processed. |

| Reactive Adhesive | A reactive adhesive is made up of monomers that react in the adhesive curing process and do not evaporate from the film during use. Instead, these volatile components become chemically incorporated into the adhesive. |

| Solvent-borne Adhesive | Solvent-borne adhesives are mixtures of solvents and thermoplastic, or slightly cross-linked polymers, such as polychloroprene, polyurethane, acrylic, silicone, and natural and synthetic rubbers (elastomers). |

| Water-borne Adhesive | Water-borne adhesives use water as a carrier or diluting medium to disperse a resin. They are set by allowing the water to evaporate or be absorbed by the substrate. These adhesives are compounded with water as a diluent, rather than a volatile organic solvent. |

| UV Cured Adhesive | UV curing adhesives induce curing and create a permanent bond without heating by using ultraviolet (UV) light or other radiation sources. An aggregation of monomers and oligomers is cured or polymerized by ultraviolet (UV) or visible light in a UV adhesive. Because UV is a radiating energy source, UV adhesives are often referred to as radiation curing or rad-cure adhesives. |

| Heat-resistant Adhesive | Heat-resistant Adhesives refer to those that do not break down under high temperatures. One aspect of a complicated system of circumstances is the adhesive's capacity to withstand disintegration brought on by high temperatures. As the temperature rises, adhesives may liquefy. They can withstand stresses resulting from differing coefficients of expansion and contraction, which might be an additional advantage. |

| Reshoring | Reshoring is the practice of moving commodity production and manufacturing back to the nation where the business was founded. Onshoring, inshoring, and back shoring are further terms used. Offshoring, the practice of producing items abroad to lower labor and manufacturing costs, is the opposite of this. |

| Oleochemicals | Oleochemicals are compounds produced from biological oils or fats. They resemble petrochemicals, which are substances made from petroleum. The oleochemical business is built on the hydrolysis of oils or fats. |

| Nonporous Materials | Nonporous materials are substances that do not permit the passage of liquid or air. Nonporous materials are those that are not porous, such as glass, plastic, metal, and varnished wood. Since no air can get through, less airflow is required to raise these materials, negating the requirement for high airflow. |

| EU-Vietnam Free Trade Agreement | A trade agreement and an investment protection agreement were concluded between the European Union and Vietnam on June 30, 2019. |

| VOC content | Compounds with limited solubility in water and high vapor pressure are known as Volatile Organic Compounds (VOCs). Many VOCs are human-made chemicals that are used and produced in the manufacture of paints, pharmaceuticals, and refrigerants. |

| Emulsion Polymerization | Emulsion polymerization is a method of producing polymers or connected groups of smaller chemical chains known as monomers, in a water solution. The method is often used to make water-based paints, adhesives, and varnishes, in which the water stays with the polymer and is marketed as a liquid product. |

| 2025 National Packaging Targets | In 2018, the Australian Environment Ministry set the following 2025 National Packaging Targets: 100% of the packaging must be reusable, recyclable, or compostable by 2025, 70% of plastic packaging must be recycled or composted by 2025, 50% of average recycled content must be included in packaging by 2025, and problematic and unnecessary single-use plastic packaging must be phased out by 2025. |

| Russian Government’s Import Substitution Policy | The Western sanctions suspended the distribution of several high-tech items to Russia, including those required by the raw material export sectors and the military-industrial complex. In response, the government launched an "import substitution" scheme, appointing a special commission to oversee its implementation in early 2015. |

| Paper Substrate | Paper substrates are paper sheets, reels, or boards with a base weight of up to 400 g/m2 that has not been converted, printed or otherwise altered. |

| Insulation Material | A material that inhibits or blocks heat, sound, or electrical transmission is known as Insulation Material. The variety of insulation materials includes thick fibers like fiberglass, rock and slag wool, cellulose, and natural fibers as well as stiff foam boards and sleek foils. |

| Thermal Shock | A temperature change known as thermal shock generates stress in a material. It commonly results in material breakdown and is especially prevalent in brittle materials like ceramics. When there is a quick temperature change, either from hot to cold or vice versa, this process occurs abruptly. It occurs more frequently in materials with poor heat conductivity and insufficient structural integrity. |

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: Identify Key Variables: The quantifiable key variables (industry and extraneous) pertaining to the specific product segment and country are selected from a group of relevant variables & factors based on desk research & literature review; along with primary expert inputs. These variables are further confirmed through regression modeling (wherever required).

- Step-2: Build a Market Model: In order to build a robust forecasting methodology, the variables and factors identified in Step-1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set and the model is built on the basis of these variables.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms