Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

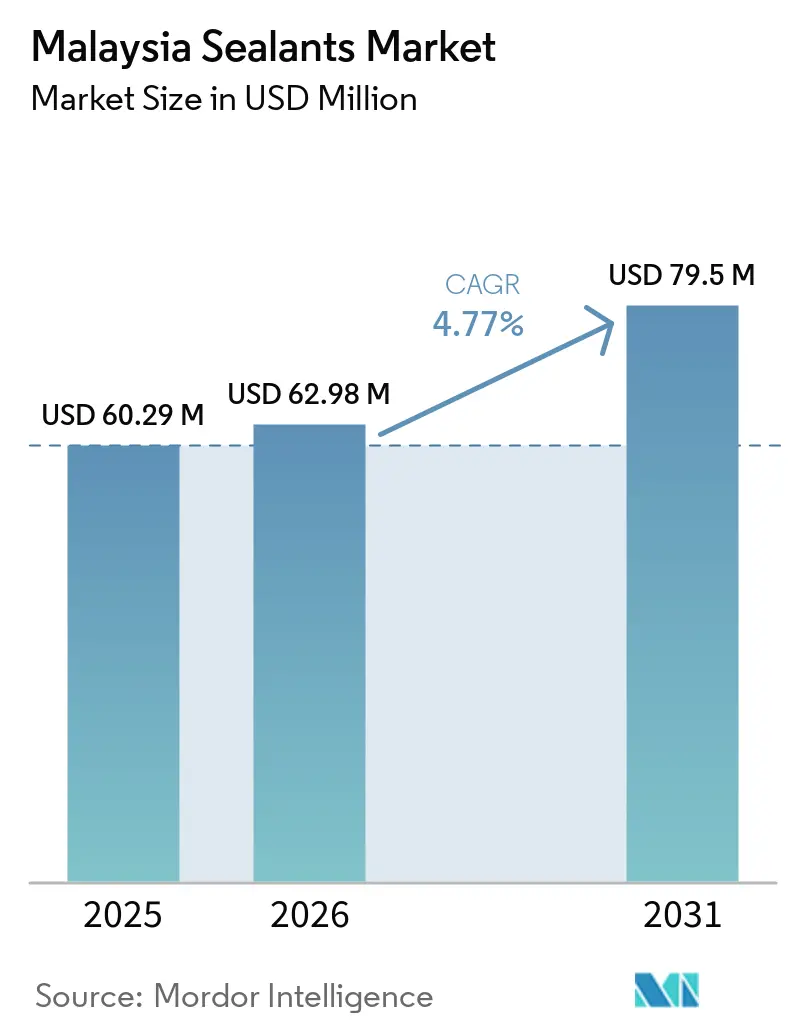

| Base Year Market Size (2025) | USD 60.29 Million |

| Market Size (2026) | USD 62.98 Million |

| Market Size (2031) | USD 79.5 Million |

| Growth Rate (2026 - 2031) | 4.77% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Malaysia Sealants Market Analysis by Mordor Intelligence

The Malaysia Sealants Market size was valued at USD 60.29 million in 2025 and is estimated to grow from USD 62.98 million in 2026 to reach USD 79.5 million by 2031, at a CAGR of 4.77% during the forecast period (2026-2031). The expansion reflects a lasting change in demand patterns rather than a short-lived construction upswing. Public-sector megaprojects such as the 640-kilometer East Coast Rail Link and the Mass Rapid Transit Line 3 are lifting joint-sealing volumes, yet factory-based application under the 70% Industrialised Building System (IBS) mandate is reshuffling the value chain toward controlled environments. Electric-vehicle (EV) assembly growth in Perak and Kedah, coupled with Infineon’s silicon-carbide expansion in Kulim, is unlocking premium demand for low-outgassing polyurethane and silicone chemistries that endure the thermal cycling of battery modules. At the same time, medical-device exports have pushed sterilizable silicone grades into cleanroom construction and autoclavable device assembly. Volatile silicone-monomer pricing, however, is pressuring small and medium-sized enterprises (SMEs) and accelerating consolidation as formulators seek supply security.

Key Report Takeaways

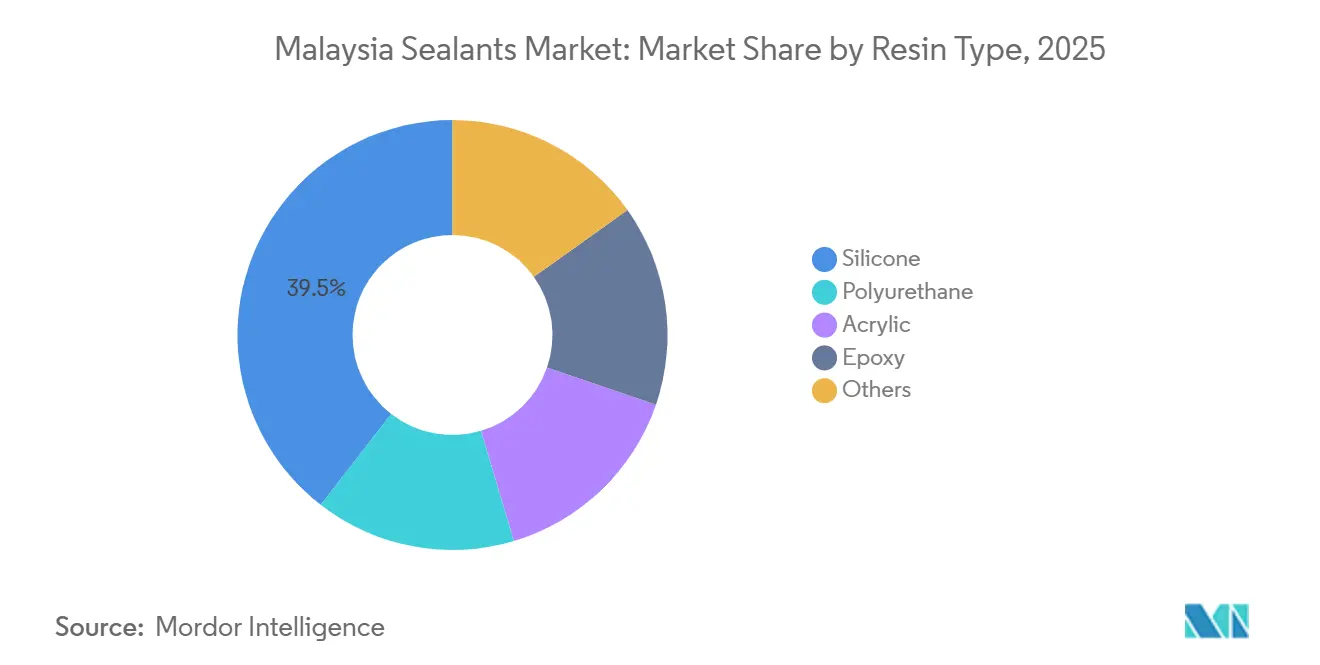

- By resin type, silicone held a 39.50% share of the Malaysia sealants market in 2025, while polyurethane is projected to expand at a 6.02% CAGR through 2031.

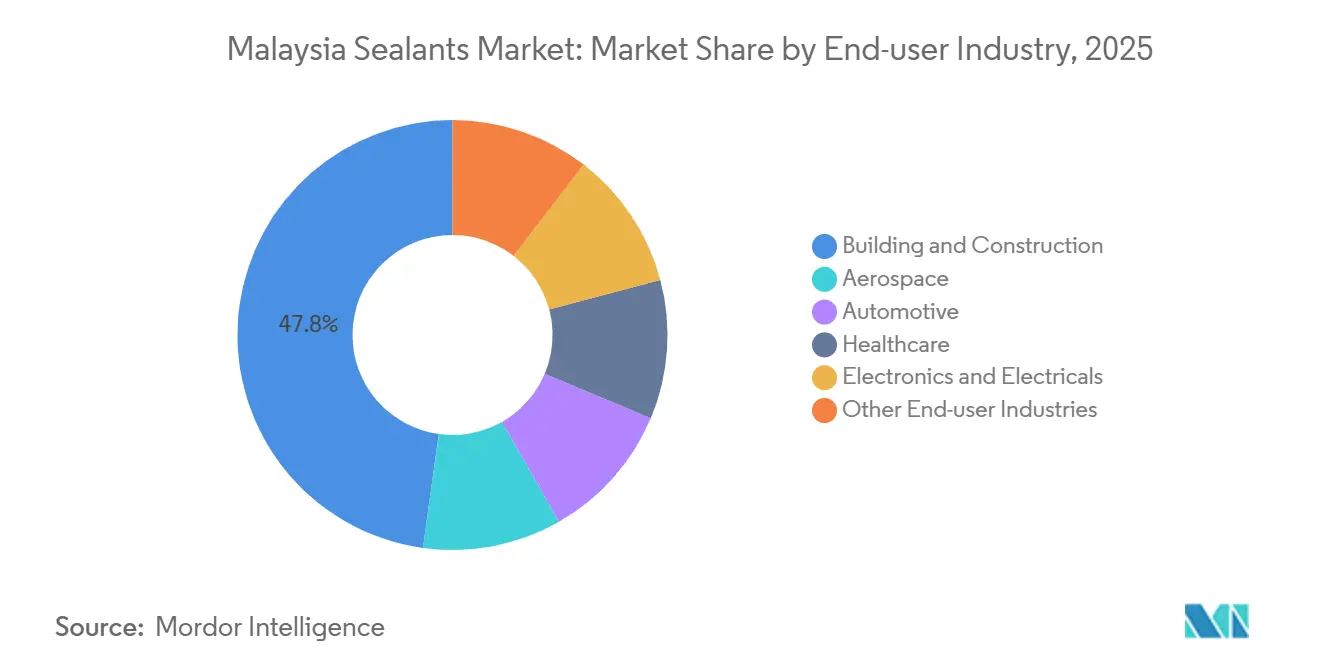

- By end-user industry, building and construction accounted for 47.80% of Malaysia sealants market size in 2025; aerospace is advancing at a 6.56% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Malaysia Sealants Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in public-sector megaproject pipeline boosts construction sealant demand | +1.2% | National, with concentration in Klang Valley, Pahang, Johor | Medium term (2-4 years) |

| Medical-device export boom driving need for sterilizable silicone grades | +0.9% | National, with clusters in Penang, Selangor, Johor | Short term (≤ 2 years) |

| Shift to modular/industrialised building systems accelerates factory-applied joint-sealant usage | +0.8% | National, with early adoption in Kuala Lumpur, Selangor, Johor | Long term (≥ 4 years) |

| Growing EV assembly in Tanjung Malim and Kulim stimulating high-temperature battery-pack sealant uptake | +0.7% | Regional, focused on Perak (Tanjung Malim) and Kedah (Kulim) | Medium term (2-4 years) |

| Aerospace MRO cluster expansion in Selangor fuels demand for fuel-tank and structural sealants | +0.6% | Regional, concentrated in Selangor (Sepang, Subang, Shah Alam) | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Surge in Public-Sector Megaproject Pipeline Boosts Construction Sealant Demand

The East Coast Rail Link reached 92.62% completion in early 2026, injecting RM 50.27 billion (USD 11.3 billion) into sealant-intensive viaducts, tunnels, and station envelopes[1]Malaysia Rail Link, “ECRL Progress Update 2026,” ecrl.my. Parallel programs such as MRT-3 and the Johor Bahru–Singapore Rapid Transit System Link deepen volume, but the real shift stems from the 70% IBS requirement that relocates joint sealing from outdoor sites to climate-controlled factories. Controlled curing cuts rework, shortens project cycles, and favors suppliers skilled in automated dispensing. The Construction Industry Development Board’s (CIDB) 2025 Competency Standard adds Building Information Modeling proficiency to contractor licensing, pushing improper joint design from a warranty concern to a compliance risk.

Medical-Device Export Boom Driving Need for Sterilizable Silicone Grades

Malaysia’s medical-device exports climbed to RM 37 billion in 2024 after RM 20 billion of cumulative investment since 2021, prompting demand for FDA-compliant silicone sealants that tolerate repeated 134 °C steam sterilization without extractables. Continuous-flow sterilization lines require faster tack-free times to avert bottlenecks, shifting preference toward platinum-catalyzed grades. Local formulators that can certify ISO 10993 biocompatibility gain pricing power, particularly as Penang’s cleanroom builders look for seal-and-sensor solutions that streamline validation.

Shift to Modular Building Systems Accelerates Factory-Applied Sealant Usage

The IBS mandate is forecast to cover 90 million square feet of prefabricated floor area by 2030. Factory bays enable robotic bead application, machine-vision inspection, and immediate adhesion testing, driving uptake of single-component, low-VOC systems that cure reliably in 25-35 °C ambient temperatures. Sealant makers providing on-site training in bead geometry and cure profiling are securing preferred-vendor status with turnkey module fabricators.

Growing EV Assembly Stimulates High-Temperature Battery-Pack Sealant Uptake

Proton’s RM 82 million upgrade in Tanjung Malim doubles annual capacity to 45,000 vehicles, while BYD’s RM 1.3 billion plant opens in 2H 2026, together requiring sealants that maintain adhesion after 1,000+ charge cycles and −40°C to 85°C swings[2]Proton Holdings, “Capacity Expansion at Tanjung Malim,” proton.com. Infineon’s €7 billion silicon-carbide line in Kulim adds demand for ultra-low-outgassing encapsulants that preserve semiconductor yield. Automakers are rationalizing vendor lists for traceability, rewarding suppliers with batch-level digital tracking.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile silicone monomer prices squeezing SME formulators' margins | -0.5% | National, with spillover effects on import-dependent formulators | Short term (≤ 2 years) |

| Labour-skill shortages causing improper application and premature joint failures | -0.4% | National, with acute impact in Klang Valley and Johor construction corridors | Medium term (2-4 years) |

| Delayed adoption of Malaysia-specific low-VOC standards creating regulatory uncertainty | -0.3% | National, with early compliance pressure in green-building projects | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Volatile Silicone-Monomer Prices Squeezing SME Formulators’ Margins

Double-digit cost swings since 2024, sparked by Chinese plant outages and feedstock spikes, are eroding margins at SMEs without hedging capacity. Wacker’s incremental builds in South Korea and Japan have not neutralized regional tightness, so local formulators face unpredictable cost baselines. Consolidation is accelerating: integrated producers are acquiring niche brands to lock in distribution. Some SMEs are pivoting to MS-polymer or acrylic systems with steadier input costs but narrower application windows.

Labor-Skill Shortages Causing Premature Joint Failures

Seventy-percent of developers reported higher labor costs in 2024, and 60% cited manpower gaps as project-delay drivers. While CIDB’s 32-hour BIM and drone-survey requirement modernizes planning, it leaves hands-on sealant application undertrained. Adhesion loss and cohesive splits raise warranty payouts and tarnish product reputations. Leading suppliers counter by embedding field engineers to validate substrate prep and bead tooling, turning restraint into differentiation.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Resin Type: Silicone Dominance Challenged by Polyurethane Versatility

Silicone held a 39.50% Malaysia sealants market share in 2025 because aerospace fuel-tank sealing, medical-device cleanrooms, and curtain-wall facades cannot compromise on UV stability and temperature resistance. Polyurethane is forecast to grow at a 6.02% CAGR through 2031, pushed by EV battery-pack modules that bond aluminum cooling plates to composite casings. Acrylic serves mid-rise residential interiors where paintability trumps movement capability, while epoxy fills chemical-resistant flooring niches.

The Malaysia sealants market size for MS-polymer hybrids is small today, but expanding as fabricators seek isocyanate-free systems that still accept paint. VITAL TECHNICAL claims over 50% regional share in MS-polymer sales and is leveraging eight-minute tack-free times to win factory-line approvals. Specialty grades, intumescent, underwater curing, and fire-rated systems, round out the resin palette and are shaped by rising SIRIM certification of low-VOC formulations.

By End-User Industry: Construction Leads, Aerospace Accelerates

Building and construction absorbed 47.80% of Malaysia sealants market size in 2025 on the back of MRT-3 stations, the 118-story Merdeka 118 tower, and a string of data-center campuses. Its growth lags the total market as residential starts moderate, but IBS adoption is trading volume for margin through factory-applied seals.

Aerospace, advancing at 6.56% CAGR to 2031, is the fastest-growing slice of the Malaysia sealants market thanks to GE Aerospace’s doubled engine-overhaul capacity and Airbus’s expansion of heavy-check bays. Automotive demand is split: combustion-engine assembly is flat, yet battery packs for Proton, BYD, and future investors require high-temperature grades. Healthcare leverages silicone’s biocompatibility for RM 37 billion in medical-device exports. Electronics rides Infineon’s silicon-carbide build, using ultra-pure encapsulants that must not outgas even trace siloxanes.

Geography Analysis

Klang Valley anchors the Malaysia sealants market with multi-tower residential projects, MRT-3 alignments, and Southeast Asia’s most concentrated aerospace MRO ecosystem. Johor’s proximity to Singapore propels industrial parks around Iskandar Malaysia and the Johor Bahru–Singapore RTS Link, while Penang’s Bayan Lepas Free Industrial Zone fuels demand for sterilizable silicones in Class 10-100 cleanrooms. Perak’s Tanjung Malim and Kedah’s Kulim car-assembly corridor supply polyurethane and silicone volumes for battery packs as EV output scales.

East Coast states, Pahang, Terengganu, and Kelantan, are benefiting from the 92.62%-complete East Coast Rail Link that spans 640 kilometers of joint-intensive bridges and tunnels. Sabah and Sarawak remain smaller but strategic; Sika’s Kota Kinabalu plant trims delivery lead times to East Malaysian contractors. Geography is also dictated by IBS hub concentration: Selangor’s precast yards, Johor’s modular-wall factories, and Penang’s volumetric pod suppliers are pulling sealants into off-site workflows that prioritize batch consistency and documented cure cycles.

Competitive Landscape

The Malaysia sealants market is moderately consolidated. White-space prospects cluster in three pockets: EV battery-pack sealing where thermal-shock-resistant polyurethane is thinly supplied, aerospace polysulfides that meet 10-year shelf-life criteria, and medical-device cleanroom envelopes that demand FDA-grade silicone able to endure hundreds of autoclave cycles. Integrated producers with captive silicone capacity or supply contracts wield a cost shield against volatile monomer spikes that stress SME rivals.

Malaysia Sealants Industry Leaders

3M

Henkel AG & Co. KGaA

Sika AG

VITAL TECHNICAL SDN BHD

Mohm Chemical Sdn. Bhd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Bostik, a subsidiary of Arkema, inaugurated a new hybrid sealant production line at its Seremban facility in Malaysia, expanding its manufacturing presence in the Asia-Pacific region. This addition enhanced the company's capacity to produce high-performance sealants for industrial and advanced packaging applications.

- May 2025: Sika Malaysia opened a new headquarters in Bangsar South, Kuala Lumpur, centralizing 150 staff to support high-spec construction demand.

Malaysia Sealants Market Report Scope

Sealants are elastomeric materials used to fill gaps, joints, or cracks, preventing water, air, dust, and fluid passage. Widely applied in construction and industrial sectors, they ensure waterproofing and structural flexibility in buildings, windows, automotive components, and appliances.

The Malaysia sealants market is segmented by resin type and end-user industry. By resin type, the market is segmented into silicone, polyurethane, acrylic, epoxy, and other resins. By end-user industry, the market is segmented into aerospace, automotive, building and construction, healthcare, electronics and electricals, and other end-user industries. For each segment, the market sizing and forecasts have been done based on revenue (USD).

By Resin Type

| Silicone |

| Polyurethane |

| Acrylic |

| Epoxy |

| Others |

By End-user Industry

| Aerospace |

| Automotive |

| Building and Construction |

| Healthcare |

| Electronics and Electricals |

| Other End-user Industries |

| By Resin Type | Silicone |

| Polyurethane | |

| Acrylic | |

| Epoxy | |

| Others | |

| By End-user Industry | Aerospace |

| Automotive | |

| Building and Construction | |

| Healthcare | |

| Electronics and Electricals | |

| Other End-user Industries |

Market Definition

- End-user Industry - Building & Construction, Automotive, Aerospace, Healthcare, and Others are the end-user industries considered under the sealants market.

- Product - All sealant products are considered in the market studied

- Resin - Under the scope of the study, resins like Polyurethane, Epoxy, Acrylic, Silicone, and Others are considered

- Technology - For the purpose of this study, One component and Two component sealant technologies are taken into consideration.

| Keyword | Definition |

|---|---|

| Hot-melt Adhesive | Hot melt adhesives are generally 100% solid formulations, based on thermoplastic polymers. They are solid at room temperature and are activated upon heating above their softening point, at which stage they are liquid, and hence, can be processed. |

| Reactive Adhesive | A reactive adhesive is made up of monomers that react in the adhesive curing process and do not evaporate from the film during use. Instead, these volatile components become chemically incorporated into the adhesive. |

| Solvent-borne Adhesive | Solvent-borne adhesives are mixtures of solvents and thermoplastic, or slightly cross-linked polymers, such as polychloroprene, polyurethane, acrylic, silicone, and natural and synthetic rubbers (elastomers). |

| Water-borne Adhesive | Water-borne adhesives use water as a carrier or diluting medium to disperse a resin. They are set by allowing the water to evaporate or be absorbed by the substrate. These adhesives are compounded with water as a diluent, rather than a volatile organic solvent. |

| UV Cured Adhesive | UV curing adhesives induce curing and create a permanent bond without heating by using ultraviolet (UV) light or other radiation sources. An aggregation of monomers and oligomers is cured or polymerized by ultraviolet (UV) or visible light in a UV adhesive. Because UV is a radiating energy source, UV adhesives are often referred to as radiation curing or rad-cure adhesives. |

| Heat-resistant Adhesive | Heat-resistant Adhesives refer to those that do not break down under high temperatures. One aspect of a complicated system of circumstances is the adhesive's capacity to withstand disintegration brought on by high temperatures. As the temperature rises, adhesives may liquefy. They can withstand stresses resulting from differing coefficients of expansion and contraction, which might be an additional advantage. |

| Reshoring | Reshoring is the practice of moving commodity production and manufacturing back to the nation where the business was founded. Onshoring, inshoring, and back shoring are further terms used. Offshoring, the practice of producing items abroad to lower labor and manufacturing costs, is the opposite of this. |

| Oleochemicals | Oleochemicals are compounds produced from biological oils or fats. They resemble petrochemicals, which are substances made from petroleum. The oleochemical business is built on the hydrolysis of oils or fats. |

| Nonporous Materials | Nonporous materials are substances that do not permit the passage of liquid or air. Nonporous materials are those that are not porous, such as glass, plastic, metal, and varnished wood. Since no air can get through, less airflow is required to raise these materials, negating the requirement for high airflow. |

| EU-Vietnam Free Trade Agreement | A trade agreement and an investment protection agreement were concluded between the European Union and Vietnam on June 30, 2019. |

| VOC content | Compounds with limited solubility in water and high vapor pressure are known as Volatile Organic Compounds (VOCs). Many VOCs are human-made chemicals that are used and produced in the manufacture of paints, pharmaceuticals, and refrigerants. |

| Emulsion Polymerization | Emulsion polymerization is a method of producing polymers or connected groups of smaller chemical chains known as monomers, in a water solution. The method is often used to make water-based paints, adhesives, and varnishes, in which the water stays with the polymer and is marketed as a liquid product. |

| 2025 National Packaging Targets | In 2018, the Australian Environment Ministry set the following 2025 National Packaging Targets: 100% of the packaging must be reusable, recyclable, or compostable by 2025, 70% of plastic packaging must be recycled or composted by 2025, 50% of average recycled content must be included in packaging by 2025, and problematic and unnecessary single-use plastic packaging must be phased out by 2025. |

| Russian Government’s Import Substitution Policy | The Western sanctions suspended the distribution of several high-tech items to Russia, including those required by the raw material export sectors and the military-industrial complex. In response, the government launched an "import substitution" scheme, appointing a special commission to oversee its implementation in early 2015. |

| Paper Substrate | Paper substrates are paper sheets, reels, or boards with a base weight of up to 400 g/m2 that has not been converted, printed or otherwise altered. |

| Insulation Material | A material that inhibits or blocks heat, sound, or electrical transmission is known as Insulation Material. The variety of insulation materials includes thick fibers like fiberglass, rock and slag wool, cellulose, and natural fibers as well as stiff foam boards and sleek foils. |

| Thermal Shock | A temperature change known as thermal shock generates stress in a material. It commonly results in material breakdown and is especially prevalent in brittle materials like ceramics. When there is a quick temperature change, either from hot to cold or vice versa, this process occurs abruptly. It occurs more frequently in materials with poor heat conductivity and insufficient structural integrity. |

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: Identify Key Variables: The quantifiable key variables (industry and extraneous) pertaining to the specific product segment and country are selected from a group of relevant variables & factors based on desk research & literature review; along with primary expert inputs. These variables are further confirmed through regression modeling (wherever required).

- Step-2: Build a Market Model: In order to build a robust forecasting methodology, the variables and factors identified in Step-1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set and the model is built on the basis of these variables.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms