Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

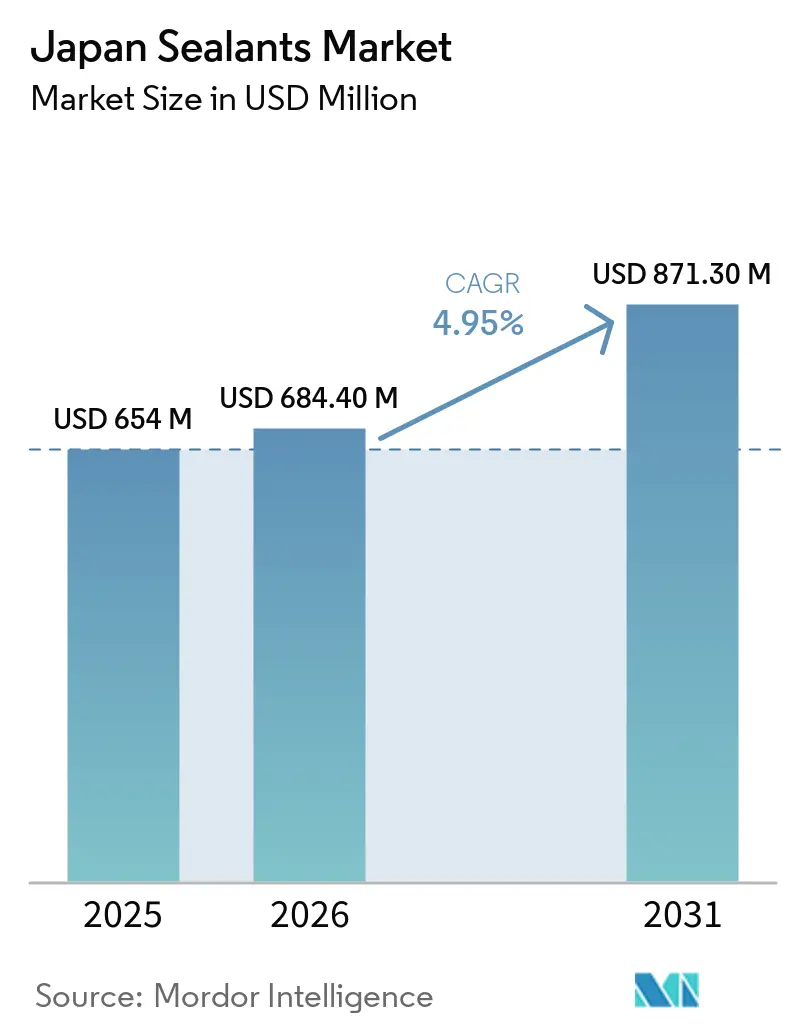

| Base Year Market Size (2025) | USD 654 Million |

| Market Size (2026) | USD 684.40 Million |

| Market Size (2031) | USD 871.30 Million |

| Growth Rate (2026 - 2031) | 4.95% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Japan Sealants Market Analysis by Mordor Intelligence

The Japan Sealants Market size is expected to grow from USD 654 million in 2025 to USD 684.40 million in 2026 and is forecast to reach USD 871.30 million by 2031 at 4.95% CAGR over 2026-2031. Strong retrofit activity under the Green Transformation Zero Energy House (GX ZEH) program, electrified-mobility lightweighting, and the Chuo Shinkansen maglev project are sustaining baseline demand. Silicone chemistries remain the performance benchmark for tunnel waterproofing because they tolerate hydrostatic pressures above 1.5 MPa and resist sulfate attack. Polyurethane systems are outpacing the overall Japan sealants market on the back of moisture-cure variants that cut on-site mixing errors by 40% and two-component grades qualified to UL 94 V-0 for battery enclosures. Medical-grade silicone volumes are rising with Japan’s USD 9 billion device export base as neurosurgical sealants and implantable sensors demand ISO 10993 compliance.

Key Report Takeaways

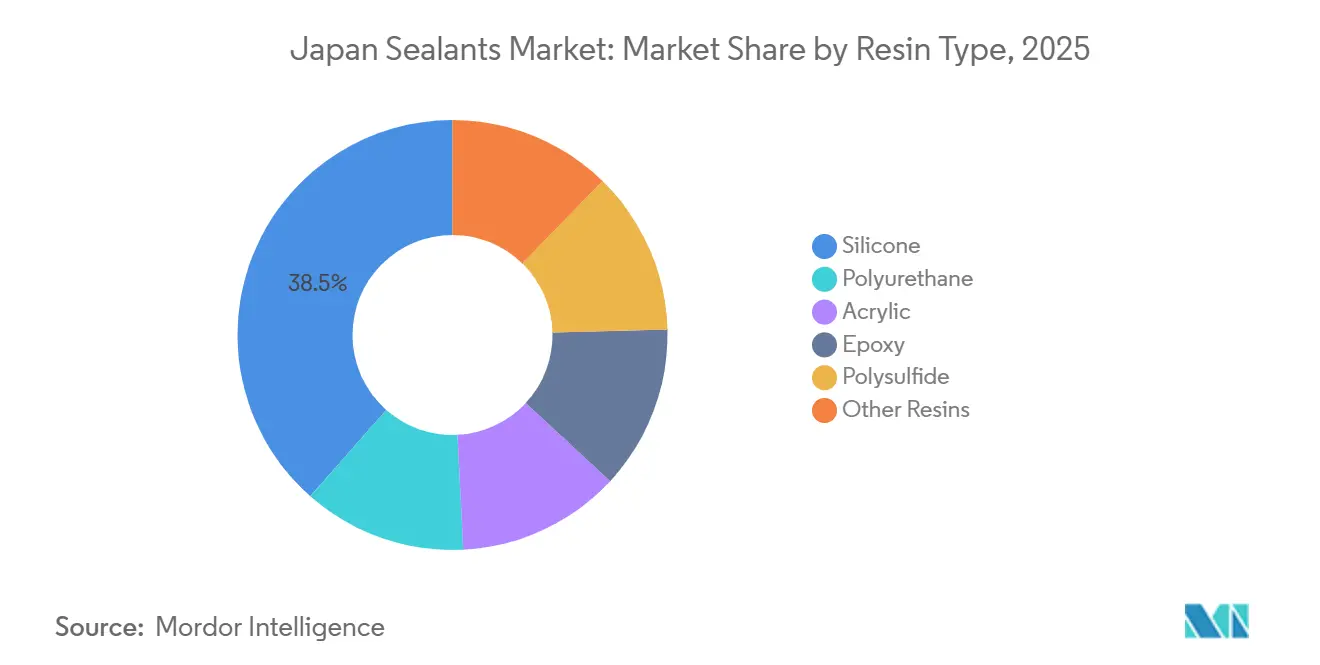

- By resin type, silicone accounted for 38.50% share of the Japan sealants market in 2025, while polyurethane is forecast to grow at a 6.02% CAGR through 2031.

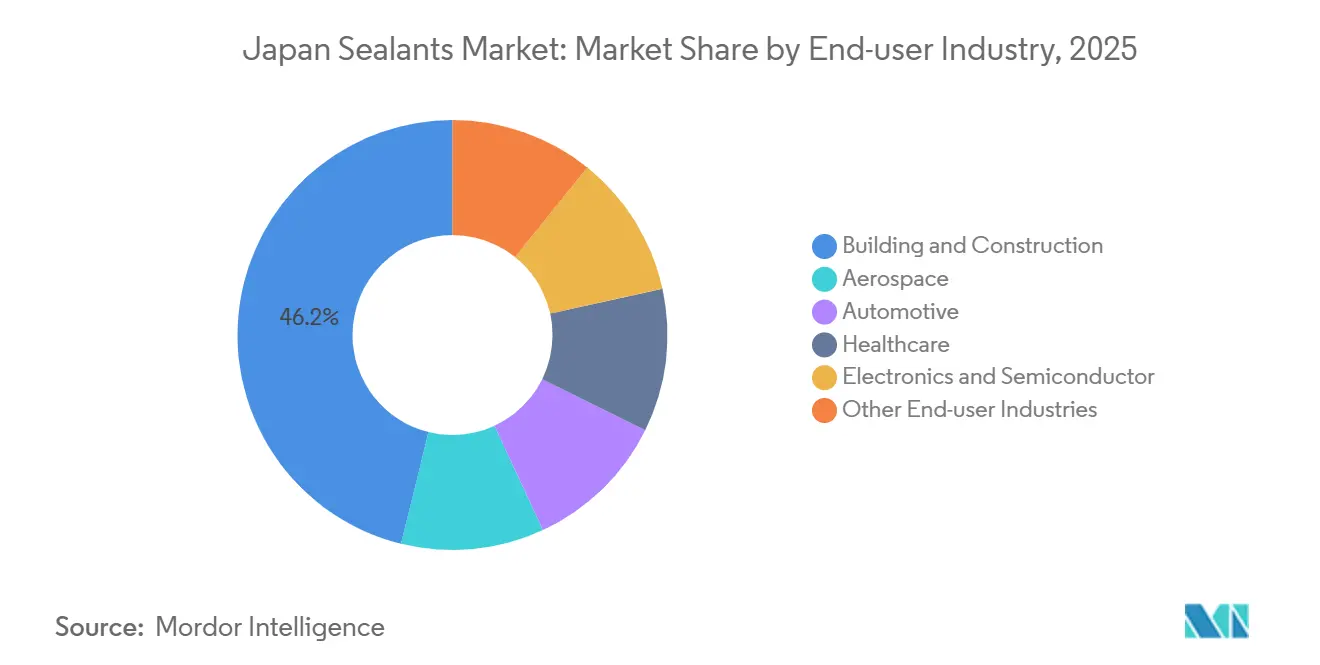

- By end-user industry, building and construction led with 46.15% of the Japan sealants market share in 2025. Healthcare is forecast to expand at a 6.45% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Japan Sealants Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surging renovation spend on earthquake-resilient housing | +1.2% | Tokyo, Osaka, Nagoya metro areas | Medium term (2-4 years) |

| Light-weighting push in EV and hybrid auto sector | +1.0% | Aichi, Kanagawa, Hiroshima prefectures | Short term (≤ 2 years) |

| Medical-grade sealants for advanced device exports | +0.8% | Kanto and Kansai export hubs | Long term (≥ 4 years) |

| Low-VOC incentives for Net-Zero Energy Houses | +0.9% | Urban new-build zones | Medium term (2-4 years) |

| Silicone demand for Shinkansen and maglev tunnels | +0.6% | Chuo Shinkansen corridor | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Surging Renovation Spend on Earthquake-Resilient Housing

Japan’s Ministry of Land, Infrastructure, Transport and Tourism allocated JPY 112.5 billion (USD 755 million) in FY 2025 to subsidize window and insulation retrofits under the GX ZEH scheme[1]Ministry of Land, Infrastructure, Transport and Tourism, “GX ZEH Program FY 2025 Budget,” mlit.go.jp. Seismic upgrades increasingly pair base-isolation systems with high-movement-capacity sealants because rigid joints amplified shear forces during the 2024 Noto Peninsula quake[2]Japan Meteorological Agency, “Noto Peninsula Earthquake 2024,” jma.go.jp. Cemedine’s Scallop Seal polyurethane, launched in 2024 with calcined scallop-shell filler, diverts aquaculture waste and delivers Shore A 30-35 while meeting ±25% joint movement. One-component moisture-cure polyurethanes now dominate retrofit jobs since they eliminate 40% of the mixing errors seen with two-part epoxies. GX ZEH approvals boosted domestic building-sealant shipments 6% year-on-year in Q3 2024.

Light-Weighting Push in Japan’s EV and Hybrid Auto Sector

Nagoya University proved in 2025 that nanocellulose-reinforced epoxy delivers 22 times the impact strength of legacy adhesives, enabling aluminum closures that remove 8-12 kg per vehicle. Toyota will raise adhesive-bonded surface area by 30% on its next battery-electric platform, favoring polyurethanes and modified silicones that prevent galvanic corrosion across –40 °C to +120 °C. Sekisui Fuller’s EV Protect 4006 SFR adds under 2 kg to a 60 kWh pack while meeting UL 94 V-0. Automotive sealant consumption helped lift Japan’s adhesive output 2.7% in 2024, even as emulsion systems fell 6% with the switch to solvent-free reactive hot melts.

Medical-Grade Sealants Demand from Advanced Device Exports

Japan exported USD 9 billion of medical devices in 2025, within a USD 38 billion domestic base, growing 4.2% annually. Kaneka’s SILASCON neurosurgical sealant meets ISO 10993 and keeps extractables below 0.1% by mass, a threshold unmet by tin-catalyzed construction silicones. Shin-Etsu’s KMC encapsulant line employs the same ultra-pure siloxane processes, reducing ionic contaminants that corrode gold bond wires in pacemakers. FDA and CE Mark pathways force adopters to install process analytical technology, which later migrates into domestic construction divisions and cuts field failure rates. Tokuyama silica fillers transferred from dental composites improve thixotropy in vertical joints without sacrificing elongation.

Low-VOC Incentives for Net-Zero Energy Houses

Japan’s Ministry of Health, Labour and Welfare regulates indoor concentrations for 13 VOCs, and Sekisui Fuller markets formulations omitting all listed substances. VOC emissions from domestic adhesive and sealant plants dropped 51% between 2000 and 2024 as solvent-borne systems ceded ground to moisture-cure polyurethanes and silane-terminated polymers. Konishi’s Tochigi expansion for water-based adhesives targets FY 2024 sales of JPY 129 billion and captures the margin premium that low-VOC grades command. Rising compliance costs under the Pollutant Release and Transfer Register Act have narrowed acrylic price premiums to 5-8%, prompting contractors to specify low-VOC systems to avoid paperwork. Sika’s isocyanate-free Sikaflex-591 marine sealant commands a 20-25% premium yet eliminates hazardous-waste disposal fees, accelerating adoption.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Petrochemical feedstock price volatility | –0.7% | Import-dependent refineries nationwide | Short term (≤ 2 years) |

| Stringent PRTR and VOC norms | –0.5% | Compliance burden highest for SMEs | Medium term (2-4 years) |

| Skilled applicator labor shortage | –0.8% | Rural prefectures and ex-urban zones | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Petrochemical Feedstock Price Volatility

Japan’s naphtha fell 12.8% year-on-year to JPY 85,800/ton (USD 575/ton) in Aug 2025 but spiked 66% after the March 2026 Strait of Hormuz disruption. Polyurethane sealants track benzene and propylene, so a USD 30 bbl crude move swings costs 15-20%, and smaller producers cannot hedge effectively. Sekisui Fuller lengthened raw-material lead times to 14-16 weeks and rationed shipments to battery customers in Mar 2026. Multinationals are shifting toward bio-based polyols from castor oil, while domestic SMEs pivot to silicones that depend on local silica-sand feedstock.

Skilled Applicator Labor Shortage Elevating Installation Costs

Japan’s construction workforce shrank 30% from 1997 to 2020, and 35.9% of remaining workers are at least 55 years old. Residential project delays now reach 10 months and installation costs climbed 15-20% since 2024. One-component moisture-cure polyurethanes with 20–30-minute open times help semi-skilled crews achieve acceptable tooling. Government plans to admit 199,500 foreign workers by FY 2028 will ease pressure in metropolitan areas but language barriers make simplified products the main solution through 2031.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Resin Type: Silicone Dominance Anchors Thermal and Movement Demands

Silicones captured 38.5% of the Japan sealants market in 2025, reflecting unmatched UV stability and adhesion to glass, metal, and dissimilar substrates. Polyurethanes are expanding at 6.02% annually through 2031, aided by UL 94 V-0 two-component grades for EV battery packs. Acrylics remain favored in interior joinery but rarely exceed a mid-single-digit share because ±7.5% movement capacity fails seismic codes. Epoxies and polysulfides fill chemical-containment niches yet now represent below 5% combined volume.

Silicones keep commanding premium applications such as maglev tunnel joints, semiconductor encapsulation, and photovoltaic module edge-sealing. Polyurethane innovation, typified by Sekisui Fuller EV Protect 4006 SFR, captures lightweighting demand in automobiles that silicones cannot meet economically. The rise of silane-terminated polymers is eroding polysulfide presence by delivering similar chemical resistance without mixing complexity. Overall, resin diversification has not dented silicone leadership; instead, it is expanding total Japan sealants market size by opening new performance windows.

By End-User Industry: Construction Scale Versus Healthcare Velocity

Building and construction delivered 46.15% of Japan sealants market size in 2025 on the strength of GX ZEH retrofits and maglev infrastructure. Healthcare, however, is advancing at a 6.45% CAGR through 2031 as neurosurgical and implantable-sensor exports grow. Automotive remains pivotal to polyurethane uptake because adhesive bonding replaces welding in aluminum closures, while electronics leverage ultra-pure silicones for thermal-interface materials. Aerospace remains a small niche but drives material qualification standards that cascade to other sectors.

Construction demand hinges on renovation momentum and labor-saving one-component systems that counter an aging workforce. Healthcare volumes, though smaller, command high multipliers given medical-grade price points five to eight times those of construction grades. Automotive OEMs plan larger bonded areas to cut weight and improve crash performance, supporting resin innovations tailored to flame-retardancy and elasticity. Together, these shifts maintain double-digit growth slices within an otherwise mature Japan sealants market.

Geography Analysis

The Kanto and Kansai belts concentrate over two-thirds of Japan sealants market demand given their dense construction pipelines, automotive assembly capacity, and electronics fabrication clusters. The Chuo Shinkansen corridor alone will consume 15,000 tons of silicone and hybrid polymer sealants between 2025 and 2029, underpinning long-term volume in Tokyo, Nagoya, and Osaka. Aichi Prefecture’s JPY 40 billion lightweighting fund is accelerating adhesive-bonded aluminum uptake, further enlarging regional polyurethane demand.

Medical-device production in Saitama and Chiba fuels healthcare-grade silicone uptake, while Wacker’s Tsukuba plant shortens lead times by situating specialty silicone output near semiconductor and medical clusters. Rural prefectures suffer acuter labor shortages, prompting a pivot toward one-component moisture-cure formulations that cure predictably across broad humidity ranges. The foreign-worker visa program may relieve strains in urban metros, yet product simplification remains decisive for hinterland adoption through 2031.

Competitive Landscape

The Japan sealants market is moderately consolidated. Sika vaulted into tier-one status with its 2021 acquisition of Hamatite, instantly gaining Toyota, Nissan, and Honda lines and boosting content per vehicle with glass-bonding polyurethane systems. Technology is the new battleground. Venture-backed nanocellulose adhesives showing 22-fold impact strength are drawing USD 34 million in funding and threatening to rewrite automotive joint design rules. Henkel’s 2026 expansion of its Singapore electronics adhesives hub enables rapid co-development with Japanese OEMs, eroding domestic suppliers’ service advantage. Legacy polysulfide lines continue to cede share to silane-terminated polymers that satisfy low-VOC mandates without mixing complexity, while solvent-borne acrylic producers face shrinking margins after a 51% VOC-emission drop since 2000.

Japan Sealants Industry Leaders

3M

Shin-Etsu Chemical Co., Ltd.

Sika AG

ThreeBond Holdings Co., Ltd.

CEMEDINE Co.,Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Sekisui Fuller curtailed polyurethane sealant shipments after a 66% naphtha price surge linked to the Strait of Hormuz incident, extending raw-material lead times to up to 16 weeks.

- February 2026: Soudal acquired a majority stake in Sharp Chemicals in January 2025, marking its entry into Japan's specialty sealant market. This acquisition enhanced Soudal's global presence by adding Japanese production facilities and strengthened its portfolio in hybrid sealants.

Japan Sealants Market Report Scope

Sealants are elastomeric materials used to fill gaps, joints, or cracks, preventing water, air, dust, and fluid passage. Widely applied in construction and industrial sectors, they ensure waterproofing and structural flexibility in buildings, windows, automotive components, and appliances.

The Japan sealants market is segmented by resin type and end-user industry. By resin type, the market is segmented into silicone, polyurethane, acrylic, epoxy, polysulfide, and other resins. By end-user industry, the market is segmented into aerospace, automotive, building and construction, healthcare, electronics and semiconductor, and other end-user industries. For each segment, the market sizing and forecasts have been done based on revenue (USD).

By Resin Type

| Silicone |

| Polyurethane |

| Acrylic |

| Epoxy |

| Polysulfide |

| Other Resins |

By End-user Industry

| Aerospace |

| Automotive |

| Building and Construction |

| Healthcare |

| Electronics and Semiconductor |

| Other End-user Industries |

| By Resin Type | Silicone |

| Polyurethane | |

| Acrylic | |

| Epoxy | |

| Polysulfide | |

| Other Resins | |

| By End-user Industry | Aerospace |

| Automotive | |

| Building and Construction | |

| Healthcare | |

| Electronics and Semiconductor | |

| Other End-user Industries |

Market Definition

- End-user Industry - Building & Construction, Automotive, Aerospace, Healthcare, and Others are the end-user industries considered under the sealants market.

- Product - All sealant products are considered in the market studied

- Resin - Under the scope of the study, resins like Polyurethane, Epoxy, Acrylic, Silicone, and Others are considered

- Technology - For the purpose of this study, One component and Two component sealant technologies are taken into consideration.

| Keyword | Definition |

|---|---|

| Hot-melt Adhesive | Hot melt adhesives are generally 100% solid formulations, based on thermoplastic polymers. They are solid at room temperature and are activated upon heating above their softening point, at which stage they are liquid, and hence, can be processed. |

| Reactive Adhesive | A reactive adhesive is made up of monomers that react in the adhesive curing process and do not evaporate from the film during use. Instead, these volatile components become chemically incorporated into the adhesive. |

| Solvent-borne Adhesive | Solvent-borne adhesives are mixtures of solvents and thermoplastic, or slightly cross-linked polymers, such as polychloroprene, polyurethane, acrylic, silicone, and natural and synthetic rubbers (elastomers). |

| Water-borne Adhesive | Water-borne adhesives use water as a carrier or diluting medium to disperse a resin. They are set by allowing the water to evaporate or be absorbed by the substrate. These adhesives are compounded with water as a diluent, rather than a volatile organic solvent. |

| UV Cured Adhesive | UV curing adhesives induce curing and create a permanent bond without heating by using ultraviolet (UV) light or other radiation sources. An aggregation of monomers and oligomers is cured or polymerized by ultraviolet (UV) or visible light in a UV adhesive. Because UV is a radiating energy source, UV adhesives are often referred to as radiation curing or rad-cure adhesives. |

| Heat-resistant Adhesive | Heat-resistant Adhesives refer to those that do not break down under high temperatures. One aspect of a complicated system of circumstances is the adhesive's capacity to withstand disintegration brought on by high temperatures. As the temperature rises, adhesives may liquefy. They can withstand stresses resulting from differing coefficients of expansion and contraction, which might be an additional advantage. |

| Reshoring | Reshoring is the practice of moving commodity production and manufacturing back to the nation where the business was founded. Onshoring, inshoring, and back shoring are further terms used. Offshoring, the practice of producing items abroad to lower labor and manufacturing costs, is the opposite of this. |

| Oleochemicals | Oleochemicals are compounds produced from biological oils or fats. They resemble petrochemicals, which are substances made from petroleum. The oleochemical business is built on the hydrolysis of oils or fats. |

| Nonporous Materials | Nonporous materials are substances that do not permit the passage of liquid or air. Nonporous materials are those that are not porous, such as glass, plastic, metal, and varnished wood. Since no air can get through, less airflow is required to raise these materials, negating the requirement for high airflow. |

| EU-Vietnam Free Trade Agreement | A trade agreement and an investment protection agreement were concluded between the European Union and Vietnam on June 30, 2019. |

| VOC content | Compounds with limited solubility in water and high vapor pressure are known as Volatile Organic Compounds (VOCs). Many VOCs are human-made chemicals that are used and produced in the manufacture of paints, pharmaceuticals, and refrigerants. |

| Emulsion Polymerization | Emulsion polymerization is a method of producing polymers or connected groups of smaller chemical chains known as monomers, in a water solution. The method is often used to make water-based paints, adhesives, and varnishes, in which the water stays with the polymer and is marketed as a liquid product. |

| 2025 National Packaging Targets | In 2018, the Australian Environment Ministry set the following 2025 National Packaging Targets: 100% of the packaging must be reusable, recyclable, or compostable by 2025, 70% of plastic packaging must be recycled or composted by 2025, 50% of average recycled content must be included in packaging by 2025, and problematic and unnecessary single-use plastic packaging must be phased out by 2025. |

| Russian Government’s Import Substitution Policy | The Western sanctions suspended the distribution of several high-tech items to Russia, including those required by the raw material export sectors and the military-industrial complex. In response, the government launched an "import substitution" scheme, appointing a special commission to oversee its implementation in early 2015. |

| Paper Substrate | Paper substrates are paper sheets, reels, or boards with a base weight of up to 400 g/m2 that has not been converted, printed or otherwise altered. |

| Insulation Material | A material that inhibits or blocks heat, sound, or electrical transmission is known as Insulation Material. The variety of insulation materials includes thick fibers like fiberglass, rock and slag wool, cellulose, and natural fibers as well as stiff foam boards and sleek foils. |

| Thermal Shock | A temperature change known as thermal shock generates stress in a material. It commonly results in material breakdown and is especially prevalent in brittle materials like ceramics. When there is a quick temperature change, either from hot to cold or vice versa, this process occurs abruptly. It occurs more frequently in materials with poor heat conductivity and insufficient structural integrity. |

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: Identify Key Variables: The quantifiable key variables (industry and extraneous) pertaining to the specific product segment and country are selected from a group of relevant variables & factors based on desk research & literature review; along with primary expert inputs. These variables are further confirmed through regression modeling (wherever required).

- Step-2: Build a Market Model: In order to build a robust forecasting methodology, the variables and factors identified in Step-1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set and the model is built on the basis of these variables.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms