Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

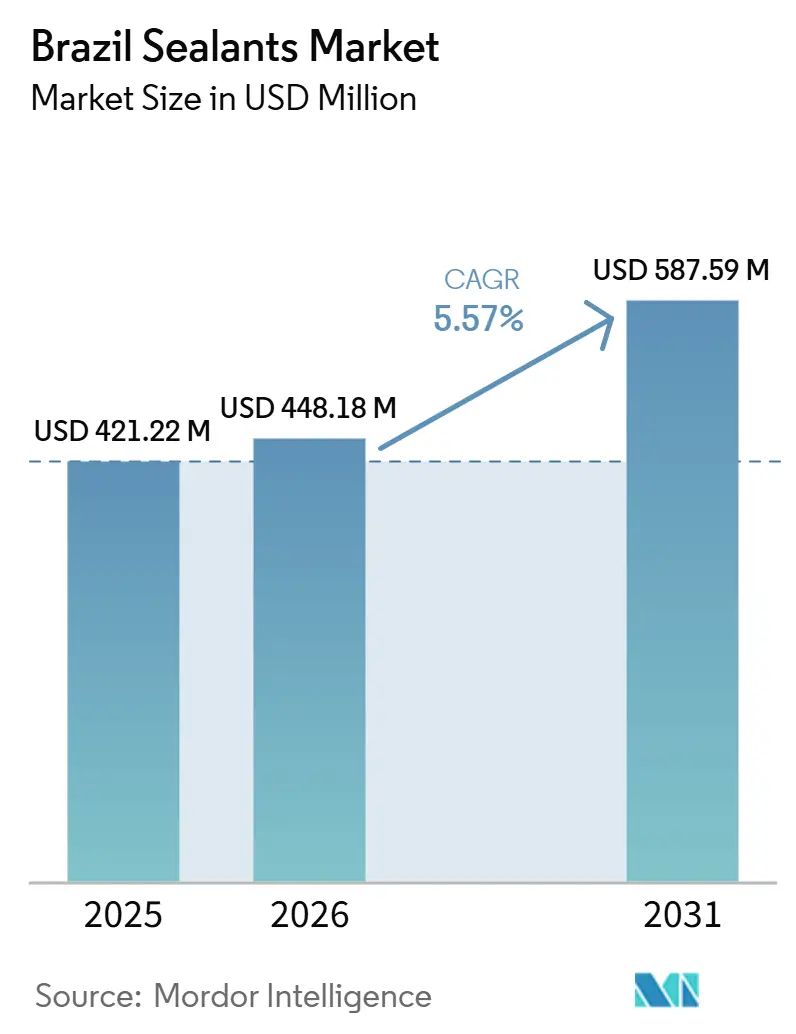

| Base Year Market Size (2025) | USD 421.22 Million |

| Market Size (2026) | USD 448.18 Million |

| Market Size (2031) | USD 587.59 Million |

| Growth Rate (2026 - 2031) | 5.57% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Brazil Sealants Market Analysis by Mordor Intelligence

The Brazil Sealants Market size is expected to increase from USD 421.22 million in 2025 to USD 448.18 million in 2026 and reach USD 587.59 million by 2031, growing at a CAGR of 5.57% over 2026-2031. The five-year outlook is animated by multi-billion-dollar highway concessions, Petrobras’ long-cycle offshore maintenance program, and the roll-out of stricter volatile-organic-compound (VOC) caps that reward hybrid chemistries. Hybrid silyl-modified polymer (SMP) systems are winning specifications in humid coastal worksites because they bond on damp substrates and release almost no VOCs. Silicone products, while still dominant in façade glazing and sanitary uses, face margin pressure from imported cartridges that undercut domestic prices by up to 40%. Meanwhile, polyurethane and polysulfide chemistries are being locked into highway bridges, tunnel linings, and pre-salt production platforms, where operators value multi-decade service lives over first-cost savings.

Key Report Takeaways

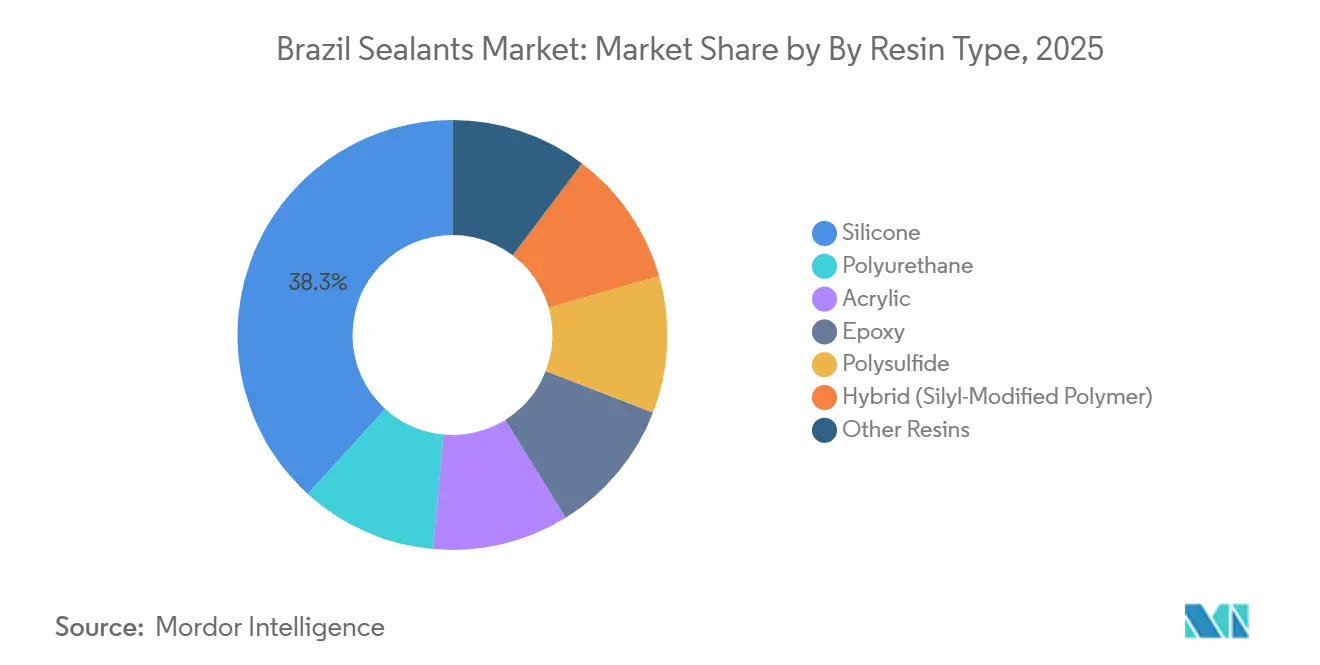

- By resin type, silicone captured 38.25% of the Brazil sealants market share in 2025, and hybrid SMP systems are forecast to rise at a 6.67% CAGR between 2026 and 2031.

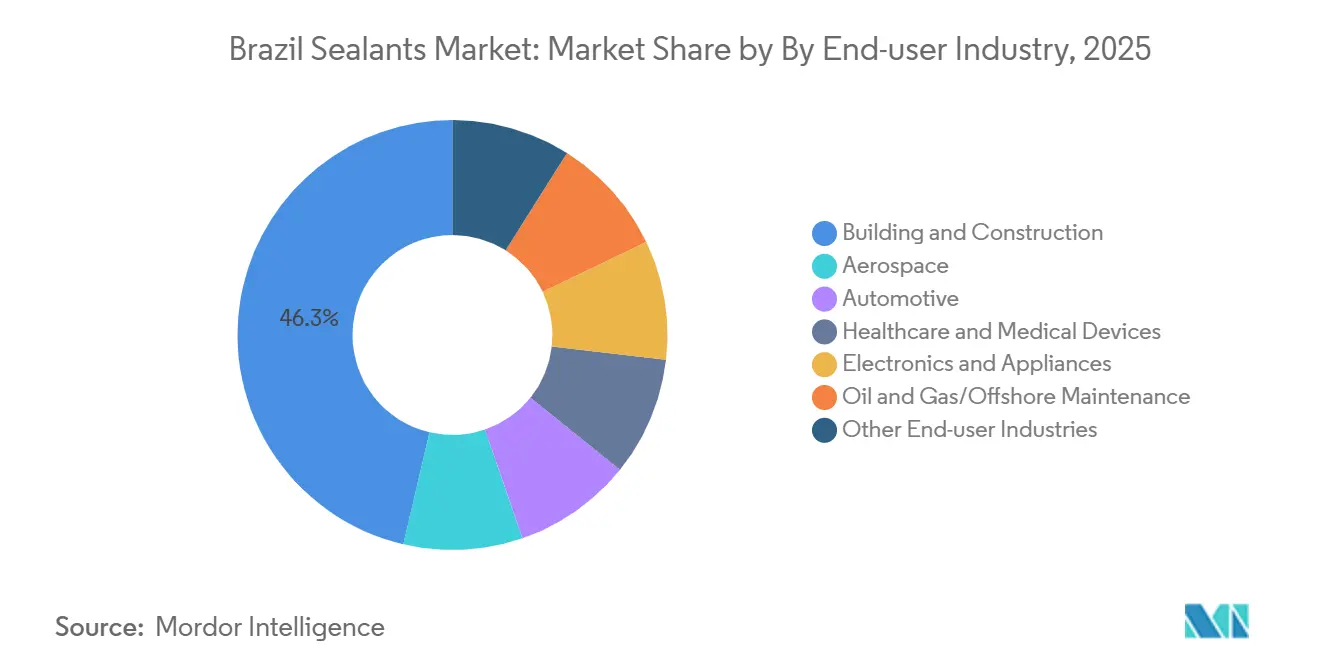

- By end-user industry, building and construction led with 46.32% revenue share in 2025; oil and gas/offshore maintenance is advancing at a 6.01% CAGR between 2026 and 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Brazil Sealants Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Resurgent Residential Construction Surge | +1.40% | Brazil, metro growth corridors | Medium term (2-4 years) |

| Federal Highway-Rail Concessions Accelerating Infrastructure Build-out | +1.10% | National trunk routes | Long term (≥4 years) |

| Automotive Output Rebound Under Rota 2030 Incentives | +0.90% | São Paulo and Minas Gerais auto clusters | Medium term (2-4 years) |

| Sanitation PPP Wave Raising Demand for Elastomeric Sealants | +0.80% | Northeast and Center-West water districts | Short term (≤2 years) |

| Cold-Chain Warehouse Boom in Brazil’s Agribusiness Belts | +0.60% | Mato Grosso, Goiás, Paraná logistics hubs | Short term (≤2 years) |

| Source: Mordor Intelligence | |||

Resurgent Residential Construction Surge

Federally subsidized mortgages under a recalibrated Minha Casa Minha Vida program have accelerated housing launches, especially 60-100 square meters apartments in secondary cities. Developers of these towers are specifying acrylic-latex and silicone façade sealants to meet airtightness rules, while low-VOC hybrid SMPs are chosen to reduce labor by curing without primers. Distributors in the South report double-digit cartridge sales growth in the mid-price tier, confirming that hybrid chemistries are now mainstream in mass-housing specifications.

Federal Highway-Rail Concessions Accelerating Infrastructure Build-Out

The 2026 concession round awarded 25-30-year highway and rail contracts that contain strict maintenance key performance indicators (KPIs), pushing operators toward polyurethane and polysulfide sealants with 20-year warranties. Sealant consumption curves are extending past 2030 because maintenance ramps up only after initial asset commissioning, effectively locking in chemistry platforms for two decades.

Automotive Output Rebound Under Rota 2030 Incentives

Thanks to the Rota 2030 tax credits, vehicle assemblies experienced significant growth in 2025 and are expected to continue increasing by 2026. Original equipment manufacturers (OEMs) are converting windshield bonding to two-component polyurethanes to eliminate metal fasteners, while aftermarket installers still favor one-component silicones for cost reasons. The looming 2030 sunset of Rota 2030 raises capacity-utilization risk that converters must hedge via export channels[1]AeroTime, “Embraer Targets 255 Aircraft Deliveries in 2026,” aerotime.aero.

Sanitation Public-Private Partnership Wave

State concessions in Ceará, Paraíba, Goiás, and Minas Gerais mandate leak-rate ceilings that render cement-mortar joints obsolete. Contractors now specify polysulfide sealants that tolerate chlorine exposure and wide thermal swings, ensuring compliance with 90% sewage-coverage targets due by 2033. Converters with local field teams in Teresina and João Pessoa are winning because approvals hinge on site-specific adhesion tests.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile Silicone (PDMS) Input Costs Squeezing Converters | -0.70% | Nationwide import-dependent converters | Short term (≤2 years) |

| Tighter CONAMA VOC Caps on Construction Chemicals | -0.50% | Urban building sites | Medium term (2-4 years) |

| Chronic Shortage of Domestic Isocyanate Feedstock | -1.00% | Petrochemical complexes, Southeast | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Volatile Silicone (Polydimethylsiloxane) Input Costs Squeezing Converters

Double-digit Polydimethylsiloxane (PDMS) price swings in 2024-2025 squeezed gross margins because Brazil imports all silicone intermediates. Some converters switched to silane-terminated polyethers, formulating hybrid silyl-modified polymer (SMP) lines that dilute silicone volume by up to 40% without sacrificing adhesion, a flexibility that small domestic firms cannot match.

Tighter CONAMA VOC Caps on Construction Chemicals

CONAMA is preparing federal Volatile Organic Compound (VOC) ceilings, and municipal buyers in São Paulo already reference draft limits in their bids. Converters face capex to retrofit mixers and reformulate toward water-borne systems; early movers hope to secure green-label premiums, but late adopters risk sudden obsolescence once binding caps arrive.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Resin Type: Hybrid SMPs Close Gap on Silicones

Silicone sealants delivered 38.25% of 2025 demand. Despite generating revenue, retail cartridges are experiencing limited growth due to import discounting challenges. Hybrid SMPs are accelerating at 6.67% CAGR between 2026 and 2031. Hybrid SMPs benefit from primer-free adhesion on wet concrete, drawing market share from low-end silicones in coastal worksites. Polyurethanes retain niche dominance in bridge joints, while polysulfides ride aerospace and fuel-containment niches that demand extreme solvent resistance. Epoxies and acrylics are losing share except in repainting, yet remain staples where paintability and cost override longevity. Emerging bio-based butyl and castor-oil chemistries currently hold a minimal share but are gaining traction through their use in green-building project pilots.

In 2025, distributors in Manaus and Belém observed a significant increase in SMP cartridge volumes, which outpaced the modest growth recorded for silicone. Converters able to switch filler packages between silicone, SMP, and polyurethane on the same filling line are safeguarding margins against polydimethylsiloxane (PDMS) price volatility. This agile manufacturing is dominated by multinationals that leverage global raw-material contracts, leaving small domestic players exposed to spot-market swings.

By End-User Industry: Infrastructure and Offshore Lead Volume Growth

Construction consumed 46.32% of 2025 demand and remains the specification gatekeeper, but volume is tilting toward infrastructure projects funded by concessionaires. Concession contracts embed 25-year maintenance liabilities, favoring high-performance chemistries and driving a mix upgrade that lifts value ahead of volume. Offshore maintenance will grow fastest at 6.01% CAGR between 2026 and 2031. Petrobras has initiated a significant shutdown program, set to run until 2029. As part of this effort, the company mandates the use of fuel-immersion-resistant polysulfides and fluorosilicones on its pre-salt floating production units.

Automotive demand is steady, but gram-per-vehicle usage is falling as adhesives replace seam sealers in electric vehicle (EV) battery packs. Appliance and electronics sealant volumes are rebounding in São Paulo and Santa Catarina export corridors because the Brazilian real’s weakness has restored global price competitiveness. Aerospace remains a low-tonnage but premium-margin niche anchored by Embraer, whose 255-aircraft 2026 delivery target will consume more than 400 tons of polysulfide and epoxy sealants certified to flame-spread and fuel-tank standards[2]The Rio Times, “Brazil's Embraer 2025: Record USD 7.6 Billion Revenue,” riotimesonline.com.

Geography Analysis

São Paulo's demand surged, driven by its concentrated hubs in automotive assembly, appliance manufacturing, and silicone synthesis, capturing a significant share of the market. The state’s construction codes drive national specification trends, and Wacker’s 2025 expansion at Jandira strengthens the local supply of specialty fluids used downstream in façade sealants. Yet growth is decelerating because land prices push new industrial parks into the interior.

Northeast states Ceará, Paraíba, and Bahia are posting the fastest gains as sanitation concessions fund trunk-line pipelines that require chlorine-resistant polysulfides. Contractors prequalify vendors who can stage cartridges within 48 hours of remote jobsites, so converters are adding depots in Fortaleza and João Pessoa. The Brazil sealants market share tied to Northeast water projects is expected to double by 2031.

In the Center-West, agribusiness logistics are driving a surge in demand. From Goiás to Mato Grosso, cold-chain warehouses are being built with a focus on food-safe silicone gaskets and thermal-break Silyl Modified Polymers (SMPs). Although the region represents a smaller share of national demand, its growth rate is projected to exceed the national average. Meanwhile, southern states, buoyed by machinery exports and the MERCOSUR auto trade, are seeing consistent consumption, leading to a high turnover of polyurethane joint sealers.

Rio de Janeiro’s sealant volumes have flatlined, but Braskem’s USD 840 million ethylene expansion slated for 2028 could revive downstream formulation by securing local feedstocks and lowering ethylene-vinyl-acetate costs. Across all regions, infrastructure concessions and sanitation mandates are shifting procurement from price to lifecycle value, favoring suppliers with on-the-ground technical teams over pure distributors.

Competitive Landscape

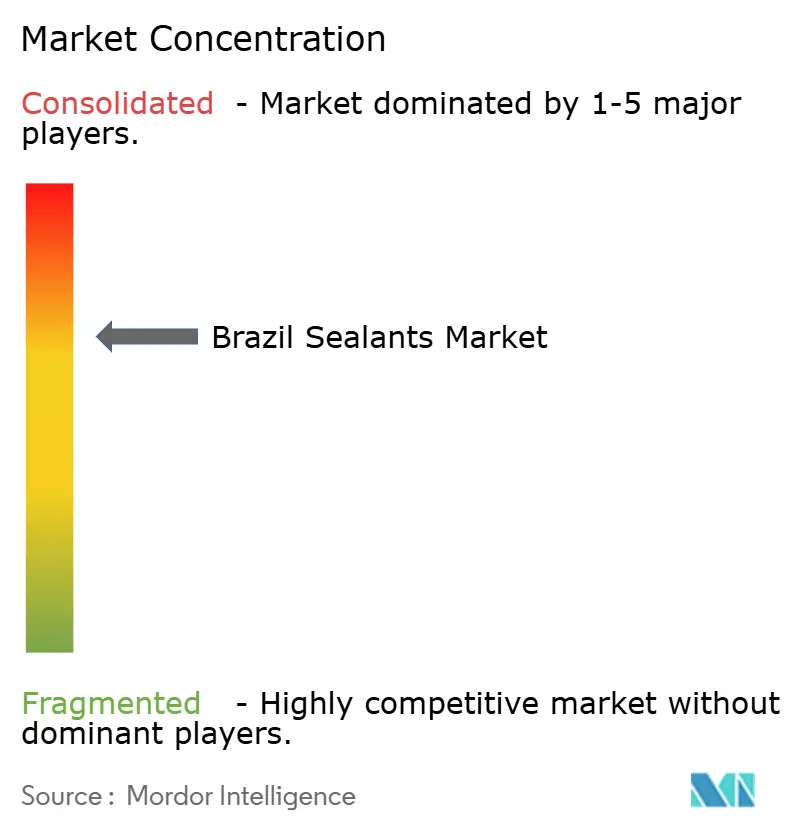

The Brazil Sealants Market is moderately consolidated. Domestic mid-tier player Brascola is undergoing judicial recovery, creating continuity risks for retailers that rely on its polychloroprene adhesives. Private-label specialist Chemiseal is gaining mindshare with biodegradable SMPs derived from sugarcane silica and is piloting blockchain traceability on municipal green-procurement bids. Chinese exporters, leveraging their Most-Favored-Nation tariff status, are importing silicone cartridges at significantly lower prices than local brands. This pricing advantage compels domestic firms to focus on differentiating themselves through enhanced technical services and extended warranty periods.

Brazil Sealants Industry Leaders

3M

Dow

Henkel AG & Co. KGaA

Sika AG

Saint-Gobain

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Henkel inaugurated its EUR 38 million (USD 40.5 million) Adhesive Technologies Inspiration Center in Jundiaí, Brazil, significantly impacting the sealants market by advancing industrial and construction technologies.

- April 2025: Cascola, a subsidiary of the Henkel group, celebrated 70 years in Brazil and launched Construção, Portas e Janelas, and Acabamentos, strengthening its position in Brazil's sealants market.

Brazil Sealants Market Report Scope

A sealant is a flexible substance applied to surfaces, joints, or openings to block the passage of fluids, air, dust, and contaminants. Unlike rigid adhesives, sealants remain elastic after curing, allowing them to withstand movement and temperature changes. Common types include silicone and polyurethane, used in construction, automotive, and industrial applications to provide waterproofing, insulation, and durable environmental protection.

The Brazil Sealants Market is segmented by resin and end-user industry. By resin type, the market is segmented into silicone, polyurethane, acrylic, epoxy, polysulfide, hybrid (silyl-modified polymer), and other resins. By end user industry, the market is segmented into aerospace, automotive, building and construction, healthcare and medical devices, electronics and appliances, oil and gas/offshore maintenance, and other end-user industries. For each segment, the market sizing and forecasts have been done on the basis of value (USD).

By Resin Type

| Silicone |

| Polyurethane |

| Acrylic |

| Epoxy |

| Polysulfide |

| Hybrid (Silyl-Modified Polymer) |

| Other Resins |

By End-User Industry

| Aerospace |

| Automotive |

| Building and Construction |

| Healthcare and Medical Devices |

| Electronics and Appliances |

| Oil and Gas/Offshore Maintenance |

| Other End-user Industries |

| By Resin Type | Silicone |

| Polyurethane | |

| Acrylic | |

| Epoxy | |

| Polysulfide | |

| Hybrid (Silyl-Modified Polymer) | |

| Other Resins | |

| By End-User Industry | Aerospace |

| Automotive | |

| Building and Construction | |

| Healthcare and Medical Devices | |

| Electronics and Appliances | |

| Oil and Gas/Offshore Maintenance | |

| Other End-user Industries |

Market Definition

- End-user Industry - Building & Construction, Automotive, Aerospace, Healthcare, and Others are the end-user industries considered under the sealants market.

- Product - All sealant products are considered in the market studied

- Resin - Under the scope of the study, resins like Polyurethane, Epoxy, Acrylic, Silicone, and Others are considered

- Technology - For the purpose of this study, One component and Two component sealant technologies are taken into consideration.

| Keyword | Definition |

|---|---|

| Hot-melt Adhesive | Hot melt adhesives are generally 100% solid formulations, based on thermoplastic polymers. They are solid at room temperature and are activated upon heating above their softening point, at which stage they are liquid, and hence, can be processed. |

| Reactive Adhesive | A reactive adhesive is made up of monomers that react in the adhesive curing process and do not evaporate from the film during use. Instead, these volatile components become chemically incorporated into the adhesive. |

| Solvent-borne Adhesive | Solvent-borne adhesives are mixtures of solvents and thermoplastic, or slightly cross-linked polymers, such as polychloroprene, polyurethane, acrylic, silicone, and natural and synthetic rubbers (elastomers). |

| Water-borne Adhesive | Water-borne adhesives use water as a carrier or diluting medium to disperse a resin. They are set by allowing the water to evaporate or be absorbed by the substrate. These adhesives are compounded with water as a diluent, rather than a volatile organic solvent. |

| UV Cured Adhesive | UV curing adhesives induce curing and create a permanent bond without heating by using ultraviolet (UV) light or other radiation sources. An aggregation of monomers and oligomers is cured or polymerized by ultraviolet (UV) or visible light in a UV adhesive. Because UV is a radiating energy source, UV adhesives are often referred to as radiation curing or rad-cure adhesives. |

| Heat-resistant Adhesive | Heat-resistant Adhesives refer to those that do not break down under high temperatures. One aspect of a complicated system of circumstances is the adhesive's capacity to withstand disintegration brought on by high temperatures. As the temperature rises, adhesives may liquefy. They can withstand stresses resulting from differing coefficients of expansion and contraction, which might be an additional advantage. |

| Reshoring | Reshoring is the practice of moving commodity production and manufacturing back to the nation where the business was founded. Onshoring, inshoring, and back shoring are further terms used. Offshoring, the practice of producing items abroad to lower labor and manufacturing costs, is the opposite of this. |

| Oleochemicals | Oleochemicals are compounds produced from biological oils or fats. They resemble petrochemicals, which are substances made from petroleum. The oleochemical business is built on the hydrolysis of oils or fats. |

| Nonporous Materials | Nonporous materials are substances that do not permit the passage of liquid or air. Nonporous materials are those that are not porous, such as glass, plastic, metal, and varnished wood. Since no air can get through, less airflow is required to raise these materials, negating the requirement for high airflow. |

| EU-Vietnam Free Trade Agreement | A trade agreement and an investment protection agreement were concluded between the European Union and Vietnam on June 30, 2019. |

| VOC content | Compounds with limited solubility in water and high vapor pressure are known as Volatile Organic Compounds (VOCs). Many VOCs are human-made chemicals that are used and produced in the manufacture of paints, pharmaceuticals, and refrigerants. |

| Emulsion Polymerization | Emulsion polymerization is a method of producing polymers or connected groups of smaller chemical chains known as monomers, in a water solution. The method is often used to make water-based paints, adhesives, and varnishes, in which the water stays with the polymer and is marketed as a liquid product. |

| 2025 National Packaging Targets | In 2018, the Australian Environment Ministry set the following 2025 National Packaging Targets: 100% of the packaging must be reusable, recyclable, or compostable by 2025, 70% of plastic packaging must be recycled or composted by 2025, 50% of average recycled content must be included in packaging by 2025, and problematic and unnecessary single-use plastic packaging must be phased out by 2025. |

| Russian Government’s Import Substitution Policy | The Western sanctions suspended the distribution of several high-tech items to Russia, including those required by the raw material export sectors and the military-industrial complex. In response, the government launched an "import substitution" scheme, appointing a special commission to oversee its implementation in early 2015. |

| Paper Substrate | Paper substrates are paper sheets, reels, or boards with a base weight of up to 400 g/m2 that has not been converted, printed or otherwise altered. |

| Insulation Material | A material that inhibits or blocks heat, sound, or electrical transmission is known as Insulation Material. The variety of insulation materials includes thick fibers like fiberglass, rock and slag wool, cellulose, and natural fibers as well as stiff foam boards and sleek foils. |

| Thermal Shock | A temperature change known as thermal shock generates stress in a material. It commonly results in material breakdown and is especially prevalent in brittle materials like ceramics. When there is a quick temperature change, either from hot to cold or vice versa, this process occurs abruptly. It occurs more frequently in materials with poor heat conductivity and insufficient structural integrity. |

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: Identify Key Variables: The quantifiable key variables (industry and extraneous) pertaining to the specific product segment and country are selected from a group of relevant variables & factors based on desk research & literature review; along with primary expert inputs. These variables are further confirmed through regression modeling (wherever required).

- Step-2: Build a Market Model: In order to build a robust forecasting methodology, the variables and factors identified in Step-1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set and the model is built on the basis of these variables.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms