Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

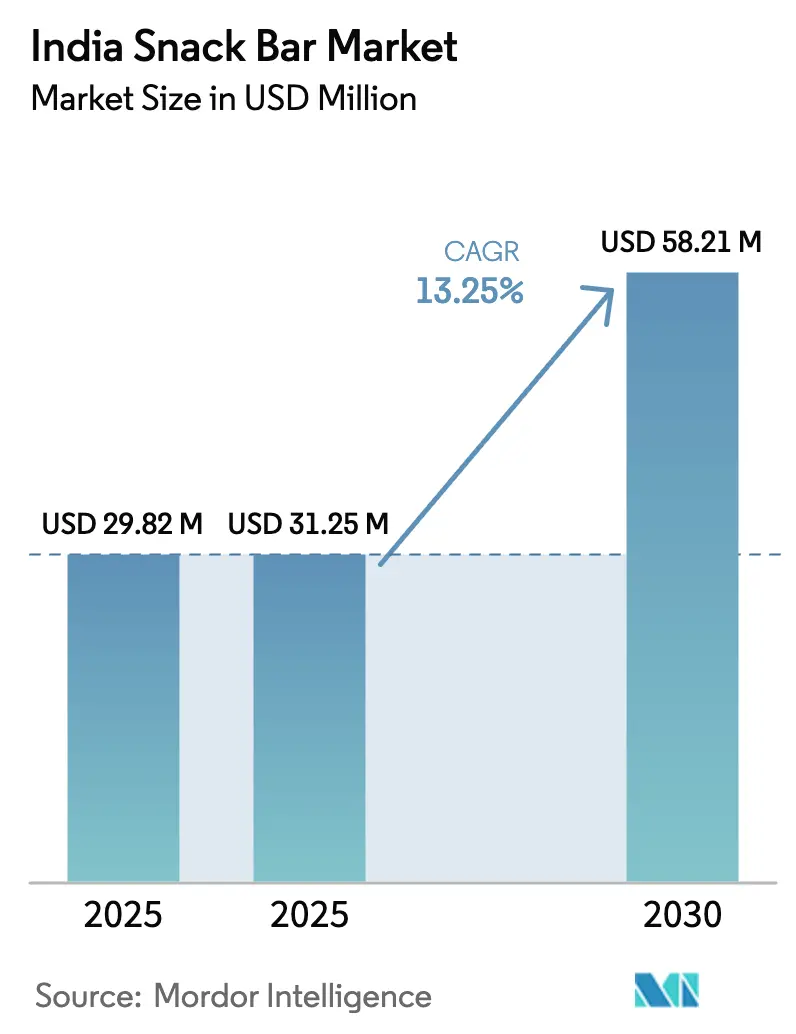

| Base Year Market Size (2025) | USD 29.82 Million |

| Market Size (2025) | USD 31.25 Million |

| Market Size (2030) | USD 58.21 Million |

| Growth Rate (2026 - 2031) | 13.25% CAGR |

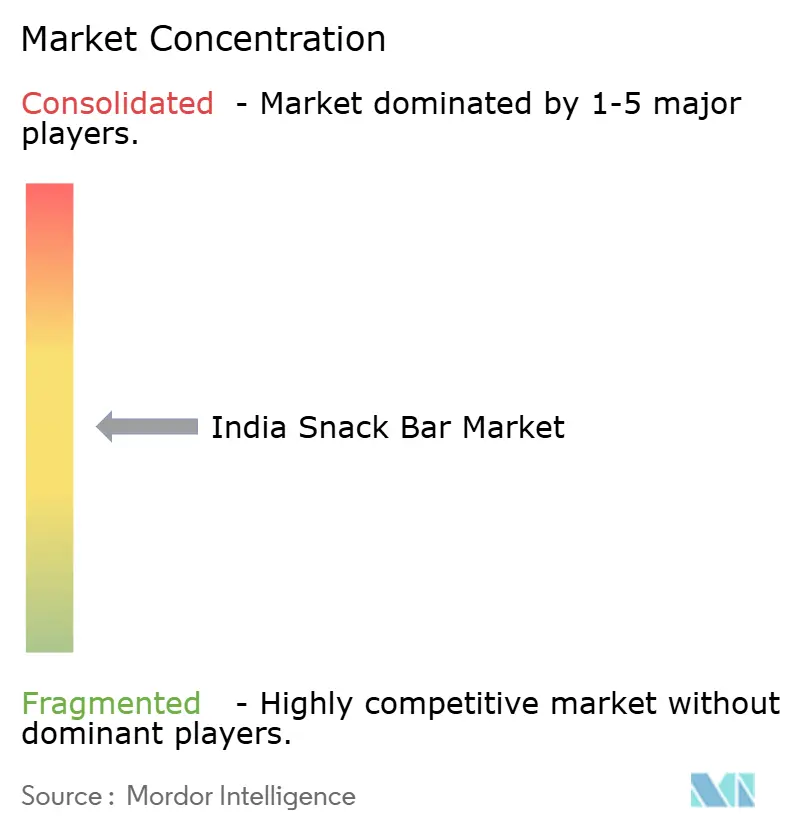

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

India Snack Bar Market Analysis by Mordor Intelligence

The India snack bar market size is expected to increase from USD 29.82 million in 2025 to USD 31.25 million in 2026 and reach USD 58.21 million by 2031, growing at a CAGR of 13.25% over 2026-2031. Urban consumers are embracing on-the-go nutrition, spurred by fitness culture, long commutes, and front-of-pack sugar warnings that take effect in February 2026. Quick commerce platforms such as Blinkit and Zepto shorten the discovery cycle to 10-15 minutes, pushing manufacturers to design SKUs that ship well in dark-store formats. Ingredient innovation, millets, plant proteins, and alternative sweeteners help brands sidestep label warnings while meeting clean-label expectations. Competitive intensity remains moderate; deep-pocketed FMCG incumbents expand through acquisition, while digital-native brands court Gen Z on Instagram with transparency narratives.

Key Report Takeaways

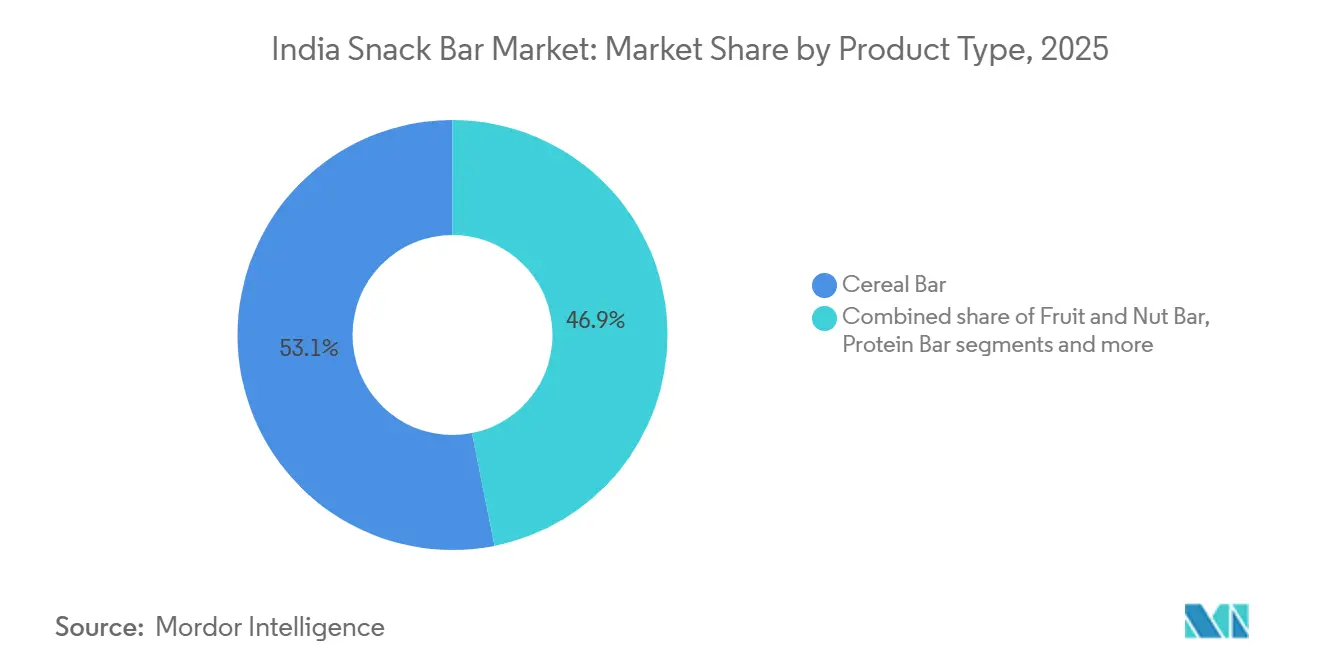

- By product type, Cereal bars led the Indian snack bar market with 53.12% share in 2025; fruit and nut bars are forecast to expand at a 14.52% CAGR through 2031.

- By Functionality, Breakfast purposes captured 45.25% revenue in 2025, whereas sports/performance and recovery uses are set to grow at 15.26% CAGR to 2031.

- By End User, Adults held 72.39% consumption in 2025, but the children’s segment is accelerating at 14.28% CAGR as parents favor protein-dense school snacks.

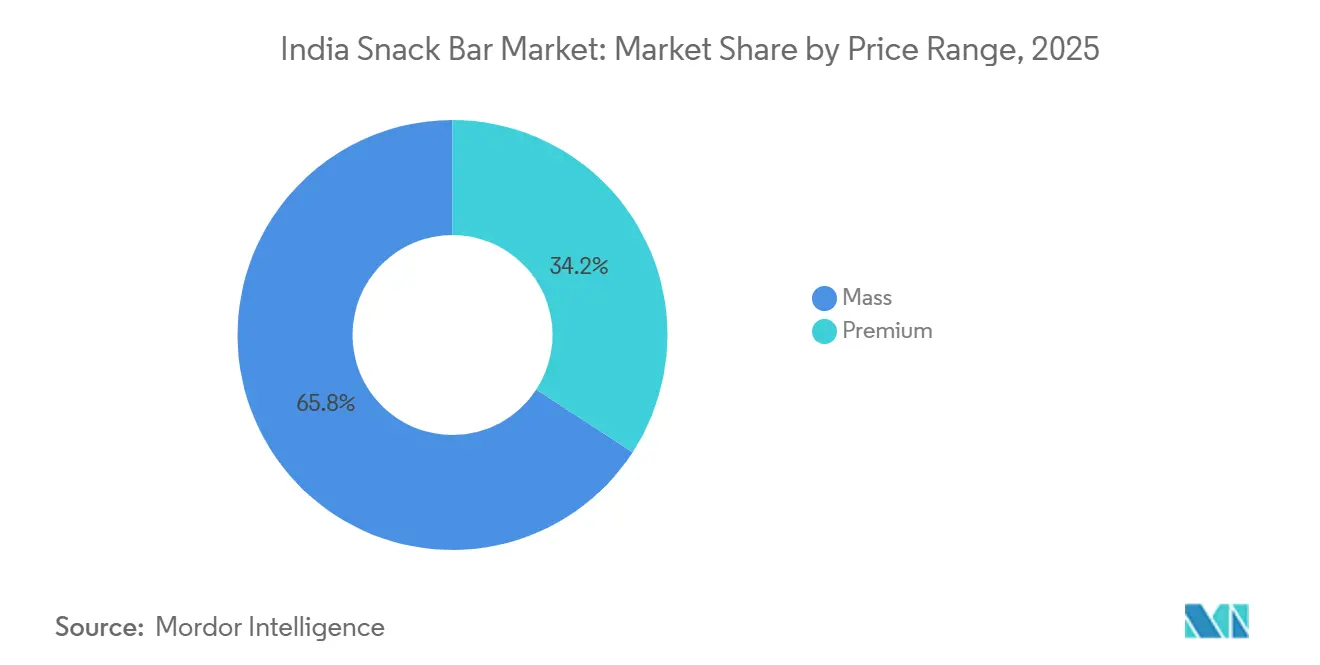

- By price range, Mass-priced products accounted for 65.82% of 2025 volume; premium variants are projected to rise at 14.58% CAGR.

- By distribution channel, Convenience stores controlled 80.52% distribution in 2025, yet online retail channels are climbing at 15.71% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

India Snack Bar Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecasts | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Health And Wellness Awareness Towards High-Protein And High-Fibre Snack Options | +2.8% | National, with stronger adoption in metros (Mumbai, Delhi-NCR, Bengaluru, Hyderabad) | Medium term (2-4 years) |

| Increasing Popularity Of Protein And Energy Bars Due To Fitness Culture And Gym Usage | +2.5% | Urban India, particularly Tier-1 cities with gym penetration exceeding 8% | Short term (≤ 2 years) |

| Innovation In Flavors, Ingredients, And Formats | +1.9% | National, with millet-based variants gaining traction in Tier-2 cities | Medium term (2-4 years) |

| Meal Replacement Trends Among Diet-Conscious Consumers | +1.6% | Metro cities with high working-professional density | Short term (≤ 2 years) |

| Growth In Premium Gifting And Curated Snack Hampers | +1.2% | Urban centers during festive seasons (Diwali, corporate gifting cycles) | Long term (≥ 4 years) |

| Rising Aspiration Among Gen Z For Healthy Yet Instagrammable Snacks | +1.5% | Tier-1 and Tier-2 cities with high social-media penetration | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Health and Wellness Awareness Towards High-Protein and High-Fiber Snack Options

Protein consumption in India is experiencing a demographic-driven transformation. According to data from the Ministry of Statistics, per capita protein intake increased from 60.9 grams per day in 2011-12 to 64.2 grams in 2022-23, indicating gradual changes in dietary patterns. Urban millennials and Gen Z are increasingly opting for snack bars, promoted as high-protein and high-fiber alternatives, instead of traditional biscuits and namkeen, reflecting their growing focus on macronutrient profiles. A 2024 study by Mondelēz India revealed that 82% of respondents choose snacks that align with their fitness goals, while 79% prefer smaller portions of indulgent snacks, a trend referred to as “mindful indulgence.” This behavioral shift creates opportunities for brands that clearly communicate protein and fiber content. This is particularly relevant with the Food Safety Standard Authority of India's February 2024 front-of-pack labeling mandate, which requires clearer disclosures of saturated fat, salt, and added sugars[1]Source: Food Safety and Standards Authority of India, “Labelling and Display Amendments 2024,” fssai.gov.in. However, brands face the challenge of balancing taste with nutrition; bars perceived as chalky or overly health-focused often struggle to compete with the rich sensory appeal of traditional Indian snacks.

Increasing Popularity of Protein and Energy Bars Due to Fitness Culture and Gym Usage

India's fitness industry, valued at INR 16,200 crore in 2024, is projected to grow to INR 37,700 crore by 2030. During this period, gym memberships are expected to nearly double, increasing from 12.3 million to 23.3 million. A major catalyst for this growth was the September 2025 GST reduction on gym and fitness services from 18% to 5%, which lowered entry barriers and drove membership growth, particularly in Tier-2 cities. Boutique fitness studios, growing at a strong 18.8% CAGR, are fostering communities where post-workout nutrition is gaining importance as a social trend. Protein bars have become a popular recovery option in this context. Reflecting the expanding appeal of fitness culture, ITC's Right Shift brand, launched in August 2024 and targeting consumers aged 40+, offers high-protein snacks, millet oats, and jaggery cookies. This highlights the brand's recognition that fitness now appeals to a broader age group. Further emphasizing this trend, Zydus Wellness acquired Naturell (Ritebite Max Protein) in October 2024 for INR 390 crore, signaling confidence that sports nutrition is shifting from a niche market to mainstream adoption. However, the industry faces the challenge of market saturation. As competition intensifies in the protein-bar segment, brands will need to stand out through bioavailability claims, innovative flavors, and endorsements from credible fitness influencers.

Innovation in Flavors, Ingredients, and Formats

Millet-based formulations gained momentum following the International Year of Millets 2023, with government procurement and distribution through public distribution systems and mid-day meal programs sustaining demand into 2024-2026. Kellanova relaunched Chocos as Multigrain Chocos in July 2024, blending wheat, jowar, rice, and corn to deliver high-protein, high-fiber, zero-maida positioning. Britannia introduced NutriChoice 100% millet cookies, while Nestlé expanded millet-based porridges, signaling that legacy FMCG players view ancient grains as a credibility signal for health-conscious consumers. Alternative sweeteners, such as stevia, jaggery, dates, and monk fruit, are proliferating as brands reformulate to avoid FSSAI's front-of-pack warning labels on high-sugar products. Plant-based proteins (pea, soy, hemp) are entering formulations, tapping into the 85% of Indians who expressed willingness to try plant-based foods in a 2024 survey. Format innovation includes single-serve sachets priced below INR 30 to penetrate price-sensitive semi-urban markets, and multi-pack bundles for e-commerce subscriptions. The interplay between ingredient premiumization and affordability will determine whether millet and plant-based bars remain niche or achieve mass-market traction.

Meal Replacement Trends Among Diet-Conscious Consumers

Urban India's fast-paced work culture is driving a shift toward meal skipping. Approximately 70% of Gen Z consumers now prefer multiple small meals instead of the traditional three-meal structure. In cities like Bengaluru, Pune, and Gurgaon, where long commutes and flexible work-from-home schedules disrupt regular meal patterns, snack bars offering 200-300 calories with balanced macros are becoming popular as meal replacements among working professionals. ITC's Right Shift brand caters to this audience by providing nutrient-dense snacks tailored for individuals over 40 focused on managing metabolic health. Quick commerce platforms are accelerating this trend. For example, Blinkit's 10-15 minute delivery windows support impulse purchases of these meal replacements. The platform's average order values, ranging from INR 450-500, suggest that consumers frequently bundle these bars with beverages or yogurt. However, portion control remains a concern; many bars marketed as meal replacements contain 15-20 grams of sugar, raising issues about satiety and potential energy crashes after consumption. Brands that incorporate complex carbohydrates and fiber to deliver sustained energy are likely to secure repeat purchases, while those relying on simple sugars risk negative consumer feedback.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecasts | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Price Sensitivity In India Limits Mass Adoption | -2.1% | National, with acute impact in rural and Tier-3+ markets | Short term (≤ 2 years) |

| Intense Competition From Traditional Indian Snacks | -1.8% | Pan-India, particularly in North and West regions with strong namkeen culture | Medium term (2-4 years) |

| Elevated Sugar Content In Certain Bars | -1.3% | Urban markets with high health awareness | Short term (≤ 2 years) |

| Regulatory Compliance For Nutrition Claims, Fortification, And Labelling | -0.9% | National, affecting all manufacturers | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Price Sensitivity in India Limits Mass Adoption

Snack bars, priced between INR 50-150, face direct competition from traditional snacks costing INR 10-50. In FY24, Haldiram's achieved revenue exceeding INR 9,000 crore, reflecting an annual growth of 15-18%. Similarly, Bikaji Foods reported FY24 revenue of INR 2,882 crore, with a year-on-year growth of 22.8%. These numbers highlight the strong consumer loyalty and extensive distribution network of traditional snacks like namkeen, bhujia, and chivda. In rural and semi-urban regions, where disposable income is limited, consumers consider snack bars as indulgent purchases rather than necessities. To address this, brands are offering smaller pack sizes—20-30 gram bars priced below INR 30—to encourage trials. However, this approach compresses profit margins. Rising raw material costs, including nuts, dried fruits, and whey protein, further strain pricing strategies. Manufacturers are now forced to choose between reducing margins or sacrificing volumes. The segmentation between mass and premium brands is expected to persist, with premium brands focusing on metropolitan markets, while mass brands compete with traditional snacks in Tier-2 and smaller markets.

Intense Competition from Traditional Indian Snacks

Valued at over INR 40,000 crore, the traditional snacks category thrives due to its cultural significance, regional flavor preferences, and an extensive distribution network covering 12-13 million kirana stores. Leading brands like Haldiram's and Bikaji, along with regional players such as Bikanervala, have modernized their packaging, obtained hygiene certifications, and expanded into organized retail, reducing the perceived quality gap with branded snack bars. Traditional snacks provide instant sensory satisfaction, savory, spicy, and crunchy qualities that snack bars often struggle to replicate, particularly for consumers accustomed to bold flavors. In Q2 FY2025, ITC's Bingo! The brand introduced new variants, including Tedhe Medhe Xtraa Teekha and Mad Angles Red Alert, highlighting the need for even health-focused brands to cater to Indian taste preferences. The challenge lies not only in pricing but also in flavor appeal. Snack bars, often seen as bland or overly Western, face difficulties in markets where 'namkeen' is a daily staple. Brands that successfully incorporate localized flavors, such as masala, tangy, and chatpata, while maintaining nutritional value, could bridge this gap, though execution risks remain significant.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Cereal Bars Anchor Breakfast, Fruit and Nut Bars Surge

In 2025, cereal bars held a substantial 53.12% market share, driven by their convenience as quick breakfast options for urban commuters, especially when paired with milk or yogurt. Expected to grow at a 14.52% CAGR through 2031, fruit and nut bars are gaining popularity due to rising demand for clean-label products and consumer preferences for natural ingredients like dates, almonds, and cranberries instead of processed grains. Energy and protein bars, while serving gym-goers and athletes in the performance nutrition segment, are facing increasing commoditization as more brands enter the market with similar whey-based formulations. The "Others" category, which includes seed-based bars (such as chia, flax, and pumpkin) and keto-friendly options, remains niche but is steadily gaining traction among diet-conscious millennials exploring low-carb diets.

In August 2024, Bagrry's launched a 7-in-1 Superfood Trail Mix, combining cereal, fruit, and nut components, positioning itself across multiple sub-categories. The growing demand for fruit and nut bars reflects a broader clean-label trend, with consumers increasingly favoring products that contain fewer than ten ingredients. Brands that transparently source nuts and dried fruits from traceable supply chains are likely to secure premium pricing, while those relying on generic ingredients may face margin pressures.

By Functionality: Sports Nutrition Outpaces Breakfast as Gyms Proliferate

In 2025, breakfast purposes held a 45.25% market share, emphasizing the increasing preference among professionals and students for snack bars as convenient alternatives to traditional sit-down breakfasts. Sports, performance, and recovery applications are expected to grow at a 15.26% CAGR through 2031. This growth is driven by India's fitness industry, which is projected to expand from INR 16,200 crore in 2024 to INR 37,700 crore by 2030. Simultaneously, gym memberships are anticipated to rise significantly, increasing from 12.3 million to 23.3 million. The "General Health" segment appeals to a broad audience seeking nutrient-dense snacks without specific athletic goals, while "Meal Replacement Purposes" caters to calorie-conscious consumers. Additionally, the "Others" category includes snacking and weight management, with portion-controlled bars offering a guilt-free indulgence.

In October 2024, Zydus Wellness announced its INR 390 crore acquisition of Naturell (Ritebite Max Protein), highlighting a corporate belief that sports nutrition is set to shift from niche specialty stores to mainstream retail outlets. A September 2025 GST reduction on gym services from 18% to 5% further lowered barriers to fitness adoption, driving increased demand for post-workout recovery products. However, breakfast-focused bars face the risk of market saturation as established cereal and biscuit brands defend their dominance in the morning meal segment. Differentiation for these bars will depend on protein content, sustained energy release, and taste. Sports nutrition bars must balance efficacy, offering over 20 grams of protein and branched-chain amino acids, with palatability, as chalky textures can discourage repeat purchases. Meal replacement bars face potential regulatory challenges if marketed with weight-loss claims without clinical evidence, particularly under FSSAI's increasingly stringent oversight.

By End User: Children's Segment Accelerates as Parents Prioritize Protein

Adults commanded 72.39% share in 2025, encompassing working professionals, fitness enthusiasts, and health-conscious consumers aged 25-55. According to the United Nations Population Fund data from 2025, the population aged between 15 and 64 in India was 68 million[2]Source: United Nations Population Fund, "India Population 2025", unfpa.org. The Children's segment is growing at 14.28% CAGR through 2031, driven by parental demand for protein-dense, low-sugar school snacks that compete with traditional biscuits and chips. Brands targeting children must navigate dual gatekeepers: parents prioritize nutrition, while children demand taste and visual appeal. Packaging innovations like cartoon characters, collectible wrappers, and interactive QR codes enhance shelf appeal, yet FSSAI's February 2026 front-of-pack labeling mandate will expose high-sugar products to parental scrutiny.

ITC's Right Shift brand, launched in August 2024, targets adults aged 40+ with nutrient-dense snacks addressing metabolic health, illustrating age-specific segmentation strategies. The children's segment faces regulatory headwinds; FSSAI prohibits health claims on products with high sugar, salt, or saturated fat, forcing reformulation. Brands that engineer taste without compromising nutrition, using natural sweeteners like dates or stevia, will capture parental trust. Adult-focused bars must differentiate beyond generic wellness claims; functional ingredients like adaptogens, probiotics, or omega-3s offer avenues for premiumization.

By Price Range: Premium Gains as Gifting and Instagram Culture Converge

In 2025, mass-priced offerings accounted for 65.82% of the market share, highlighting affordability constraints that restrict most consumers to bars priced below INR 50. At the same time, premium variants are experiencing significant growth, with a 14.58% CAGR projected through 2031. This growth is driven by a gifting culture during festivals like Diwali and Raksha Bandhan, corporate cycles, and Instagram-driven discovery among Gen Z. The younger generation's readiness to spend on exotic ingredients, such as quinoa, chia, and imported nuts, further accelerates this trend. While mass brands focus on distribution density and competitive price-per-gram value, premium brands differentiate themselves through artisanal sourcing, clean labels, and visually appealing packaging designed for social media.

Open Secret demonstrated impressive growth, achieving INR 37 crore in revenue in FY23, nearly tripling its performance. True Elements, with Marico holding a 54% stake, also showed strong results, reporting INR 57 crore in revenue in FY23, a 24% increase. These figures underscore growing investor interest in premium wellness brands. Reflecting the availability of capital for brands targeting affluent urban consumers, Farmley secured USD 42 million in Series C funding in 2025, while Natraj raised USD 30.9 million. However, premium brands face challenges, including margin pressures from rising input costs, such as imported nuts and organic certifications. To justify their pricing, these brands are leveraging storytelling, focusing on origin narratives, sustainability credentials, and functional benefits. Meanwhile, mass brands face the risk of commoditization but can defend their market share by innovating on flavor or format while maintaining price points below INR 30 to compete with traditional snacks.

By Distribution Channel: Quick Commerce Disrupts Convenience Store Dominance

In 2025, convenience stores dominated the market with an 80.52% share, underscoring the snack bars' appeal for impulse purchases. These snack bars seamlessly fit into small-format retail spaces, whether in residential neighborhoods, transit hubs, or office complexes. Online retail stores are on a rapid ascent, boasting a 15.71% CAGR projected through 2031. This surge is largely driven by quick commerce platforms like Blinkit, Zepto, and Swiggy Instamart, which have mastered the art of 10-15 minute deliveries in metro areas. E-commerce behemoths, Amazon and Flipkart, further fuel this growth by offering enticing subscription bundles. Supermarkets and hypermarkets cater to bulk-buying households, facilitating brand discovery through in-store sampling. Meanwhile, "other channels" encompass a diverse range, including gyms, pharmacies, and corporate vending machines.

Quick commerce is witnessing a meteoric rise, jumping from USD 5.5 billion in 2024 to a projected USD 9.95 billion in 2025, marking an impressive 81% year-on-year growth. This surge is altering traditional impulse buying patterns; consumers are now opting for same-hour deliveries, ordering snack bars alongside their groceries. As of March 2025, Blinkit boasted 791 operational stores, Zepto surpassed the 550 mark, and Swiggy Instamart held steady with over 600 stores. This collective expansion is not only shortening the brand trial window but also favoring SKUs that align with the economics of 10-minute deliveries. In a strategic move, Mondelēz expanded its footprint by adding 180,000 stores in 2023 and another 120,000 in the first half of 2024. Since 2019, they've installed 700,000 visicoolers to boost visibility in convenience outlets. Direct-to-consumer brands such as Yoga Bar and The Whole Truth are harnessing the power of Instagram and WhatsApp for direct sales, achieving a notable revenue split of 60% offline and 40% online.

Geography Analysis

India's snack bar market demonstrates a clear divide between metropolitan areas and rural regions. Cities such as Mumbai, Delhi-NCR, Bengaluru, Hyderabad, and Pune hold a significant share due to higher disposable incomes, the growing influence of fitness culture, and a dense network of organized retail outlets. These metros benefit from quick commerce infrastructure like Blinkit's 791 stores, Zepto's 550+, and Swiggy Instamart's 600+ as of March 2025, which facilitates 10-15 minute deliveries and lowers trial barriers. Tier-1 cities, including Chennai, Kolkata, and Ahmedabad, are experiencing rapid adoption driven by increasing gym memberships and improved product visibility through modern trade formats such as Reliance Retail's 18,000+ stores and DMart's 360+ outlets, as reported by Business Standard[3]Source: Business Standard, "Nestlé India Announces Rs 6,000-6,500 Crore Investment Plan." business-standard.com.

In contrast, Tier-2 and Tier-3 cities face challenges related to affordability and distribution. Traditional kirana stores, which account for over 90% of retail, often lack refrigeration for perishable goods or shelf space for niche SKUs. To address this, brands are introducing smaller pack sizes, 20-30 gram bars priced below INR 30, to penetrate these markets, though profitability remains difficult to achieve. Regional taste preferences add complexity: North and West India favor savory snacks like namkeen and bhujia, while South India exhibits a greater preference for health-focused products. Rural markets remain largely untapped due to low awareness, limited purchasing power, and a strong inclination toward traditional snacks, resulting in high customer-acquisition costs. The geographic expansion strategy prioritizes metro consolidation, Tier-1 growth, selective Tier-2 entry, and a patient approach to rural areas.

Government initiatives, such as the "International Year of Millets 2023," along with promotions through public distribution systems and mid-day meals, are driving demand for millet-based bars. This trend is particularly evident in states like Karnataka, Rajasthan, and Maharashtra, where millet consumption is deeply rooted in cultural practices. Nestlé's investment plan of INR 6,000-6,500 crore for 2020-2025, which includes establishing a 10th factory in Odisha with an investment of INR 8-9 billion, highlights its confidence in Eastern India's growth potential. E-commerce, expected to grow from 2.5% of grocery sales in 2024 to 4.5% in 2025, is enabling brands to bypass traditional distribution challenges and directly reach consumers in smaller cities. The evolution of Tier-2 and beyond markets will depend on the integration of organized retail expansion, quick commerce advancements, and direct-to-consumer strategies.

Competitive Landscape

Key players such as ITC Ltd., Kellanova, and Mondelēz International Inc. are capitalizing on their strong presence in biscuits, cereals, and confectionery to establish themselves in India's snack bar market. At the same time, startups like Yoga Bar, RiteBite, and MuscleBlaze are gaining traction by emphasizing ingredient transparency and fostering direct consumer connections. ITC's acquisition of Yoga Bar in June 2024 and the launch of Sunfeast Farmlite Protein Bars reflect its strategy to penetrate high-growth niches. Similarly, Mondelēz is addressing consumer concerns about wellness product flavors through its Cadbury Fuse extensions, which focus on taste.

Opportunities are expanding in meal-replacement bars designed for working professionals, regional flavors catering to local preferences, and the underdeveloped Rs 30-50 mid-premium price segment. Startups are leveraging data-driven direct-to-consumer models to adapt quickly to consumer demands, enabling them to introduce new flavors and limited-edition products while minimizing inventory risks. However, their reliance on third-party quick commerce platforms continues to pressure profit margins. Stricter Food Safety and Standards Authority of India (FSSAI) regulations on nutrient claims are likely to benefit companies with strong compliance frameworks, potentially driving market consolidation in the near future.

Large multinational corporations are leveraging their scale and extensive distribution networks, while startups are making an impact through social media engagement and community building. Collaborations with fitness influencers are helping smaller players enhance credibility and lower customer acquisition costs. Investment in research and development for sugar-reduced products is becoming a competitive edge as stricter sugar content regulations are anticipated. Over the forecast period, companies prioritizing premium product differentiation and regulatory compliance are expected to outperform those relying solely on widespread availability.

India Snack Bar Industry Leaders

-

General Mills Inc.

-

Mondelēz International Inc.

-

Bagrrys India Pvt Ltd

-

ITC Limited

-

Kellanova

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Zydus Wellness launched RiteBite Max Protein Millet Wafer Protein Bars, featuring 10g of protein from millets like jowar in a crunchy, guilt-free wafer format free from maida, added sugar, and palm oil.

- February 2025: EatFit introduced its new energy bar line, Hustl, designed to cater to the growing demand for convenient and nutritious snack options. The launch was made in collaboration with Indian cricketer Mayank Agarwal, adding a touch of credibility and appeal to the product.

- November 2024: Bollywood actor Ranveer Singh introduced a new brand named 'SuperYou' in collaboration with entrepreneur Nikunj Biyani. This partnership marked Singh's foray into the lifestyle and wellness segment, aiming to cater to the growing demand for products that promote self-care and personal well-being.

- August 2024: Pakka Limited partnered with Brawny Bear to launch India's first Date Energy Bars packaged in compostable flexible material, made from premium dates without added sugars.

India Snack Bar Market Report Scope

Snack Bars are small bites of food that are consumed during exercise, snacking, and other purposes. India snack bar market is segmented into product type, functionality, end user, price range, and distribution channels. By product type, the market is segmented into cereal bar, protein/energy bar, fruit and nut bar, and others. By functionality, the market is segmented into breakfast purposes, sports/ performance and recovery, general health, meal replacement purposes, and others. By end user, the market is segmented into adults and children. By price range, the market is segmented into mass and premium. By distribution channels, the market is segmented into supermarkets/ hypermarkets, convenience stores, online channels, and others. The market sizing has been done in value terms in USD for all the abovementioned segments.

By Product Type

| Cereal Bar |

| Energy/Protein Bar |

| Fruit and Nut Bar |

| Others |

By Functionality

| Breakfast Purposes |

| Sports/Performance and Recovery |

| General Health |

| Meal Replacement Purposes |

| Others(Snacking, weight management) |

By End User

| Adults |

| Children |

By Price Range

| Mass |

| Premium |

By Distribution Channel

| Supermarkets/Hypermarkets |

| Online Retail Stores |

| Convenience Stores |

| Other Channels |

| By Product Type | Cereal Bar |

| Energy/Protein Bar | |

| Fruit and Nut Bar | |

| Others | |

| By Functionality | Breakfast Purposes |

| Sports/Performance and Recovery | |

| General Health | |

| Meal Replacement Purposes | |

| Others(Snacking, weight management) | |

| By End User | Adults |

| Children | |

| By Price Range | Mass |

| Premium | |

| By Distribution Channel | Supermarkets/Hypermarkets |

| Online Retail Stores | |

| Convenience Stores | |

| Other Channels |

Market Definition

- Milk and White Chocolate - Milk chocolates is a solid chocolate made with milk (in the form of either milk powder, liquid milk, or condensed milk) and cocoa solids. White chocolate is made from cocoa butter and milk and contains no cocoa solids whatsoever. The scope includes regular chocolates, low-sugar, and sugar-free variants

- Toffees & Nougats - Toffees include hard, chewy, and small or one-bite candies marketed with labels as toffee or toffee-like confectionery. Nougat is a chewy confection with almond, sugar, and egg white as a basic ingredient; and it originated in Europe and Middle East countries.

- Cereals Bars - A snack composed of breakfast cereal that has been compressed into a bar shape and is held together with a form of edible adhesive. The scope includes snack bars made with cereals such as rice, oats, corn, etc. mixed with a binding syrup. These also include products labeled as cereal bars, cereal treat bars, or grain bars.

- Chewing Gum - This is a preparation for chewing, usually made of flavored and sweetened chicle or such substitutes as polyvinyl acetate. The types of chewing gums included in the scope are sugar-chewing gums and sugar-free chewing gums

| Keyword | Definition |

|---|---|

| Dark Chocolate | Dark chocolate is a form of chocolate containing cocoa solids and cocoa butter without the milk. |

| White Chocolate | White chocolate is the type of chocolate containing the highest percentage of milk solids, typically around or over 30 percent. |

| Milk Chocolate | Milk chocolate is made from dark chocolate that has a low cocoa solid content and higher sugar content, plus a milk product. |

| Hard Candy | A candy made of sugar and corn syrup boiled without crystallizing. |

| Toffees | A hard, chewy, often brown sweet that is made from sugar boiled with butter. |

| Nougats | A chewy or brittle candy containing almonds or other nuts and sometimes fruit. |

| Cereal bar | A cereal bar is a bar-shaped food product, made by pressing cereals and usually dried fruit or berries, which are in most cases held together by glucose syrup. |

| Protein bar | Protein bars are nutrition bars that contain a high proportion of protein to carbohydrates/fats. |

| Fruit & Nut bar | These are often based on dates with other dried fruit and nut additions and, in some cases, flavorings. |

| NCA | The National Confectioners Association is an American trade organization that promotes chocolate, candy, gum and mints, and the companies that make these treats. |

| CGMP | Current good manufacturing practices are those conforming to the guidelines recommended by relevant agencies. |

| Unstandardized foods | Unstandardized foods are those that do not have a standard of identity or that deviate from a prescribed standard in any manner. |

| GI | The glycemic index (GI) is a way of ranking carbohydrate-containing foods based on how slowly or quickly they are digested and increase blood glucose levels over a period of time |

| Skimmed milk powder | Skimmed milk powder is obtained by removing water from pasteurized skim milk by spray-drying. |

| Flavanols | Flavanols are a group of compounds found in cocoa, tea, apples, and many other plant-based foods and beverages. |

| WPC | Whey protein concentrate- the substance obtained by the removal of sufficient nonprotein constituents from pasteurized whey so that the finished dry product contains greater than 25% protein. |

| LDL | Low density Lipoprotein- the bad cholesterol |

| HDL | High density Lipoprotein- the good cholesterol |

| BHT | butylated Hydroxytoluene is a lab-made chemical that is added to foods as a preservative. |

| Carrageenan | Carrageenan is an additive used to thicken, emulsify, and preserve foods and drinks. |

| Free form | Not containing certain ingredients, such as gluten, dairy, or sugar. |

| Cocoa butter | It is a fatty substance obtained from cocoa beans, used in the manufacture of confectionery. |

| Pastellies | A type of of Brazilian candy made from sugar, eggs, and milk. |

| Draggees | Small, round candies that are coated with a hard sugar shell |

| CHOPRABISCO | Royal Belgian Association of the chocolate, pralines, biscuit, and confectionery industry- A trade association that represents the Belgian chocolate industry. |

| European Directive 2000/13 | A European Union directive that regulates the labeling of food products |

| Kakao-Verordnung | The German chocolate ordinance, a set of regulations that define what can be labeled as "chocolate" in Germany. |

| FASFC | Federal Agency for the Safety of the Food Chain |

| Pectin | A natural substance that is derived from fruits and vegetables. It is used in confectionery to create a gel-like texture. |

| Invert sugars | A type of sugar that is made up of glucose and fructose. |

| Emulsifier | A substance that helps to mix to liquids that does not mix together. |

| Anthocyanins | A type of flavonoid that is responsible for the red, purple, and blue colors of confectionery. |

| Functional Foods | Foods that have been modified to provide additional health benefits beyond basic nutrition. |

| Kosher certificate | This certification verifies that the ingredients, production process including all machinery, and/or food-service process complies with the standards of Jewish dietary law |

| Chicory root extract | A natural extract from the chicory root that is a good source of fiber, calcium, phosphorous, and folate |

| RDD | Recommended daily dose |

| Gummies | A chewy gelatin-based candy that is often flavored with fruit. |

| Nutraceuticals | Food or dietary supplements that are claimed to have health benefits. |

| Energy bars | Snack bars that are high in carbohydrates and calories are designed to provide energy on the go. |

| BFSO | Belgian Food Safety Organization for the food chain. |

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: Identify Key Variables: In order to build a robust forecasting methodology, the variables and factors identified in Step 1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set, and the model is built on the basis of these variables.

- Step-2: Build a Market Model: Market-size estimations for the forecast years are in nominal terms. Inflation is not a part of the pricing, and the average selling price (ASP) is kept constant throughout the forecast period for each country.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables, and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms