Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

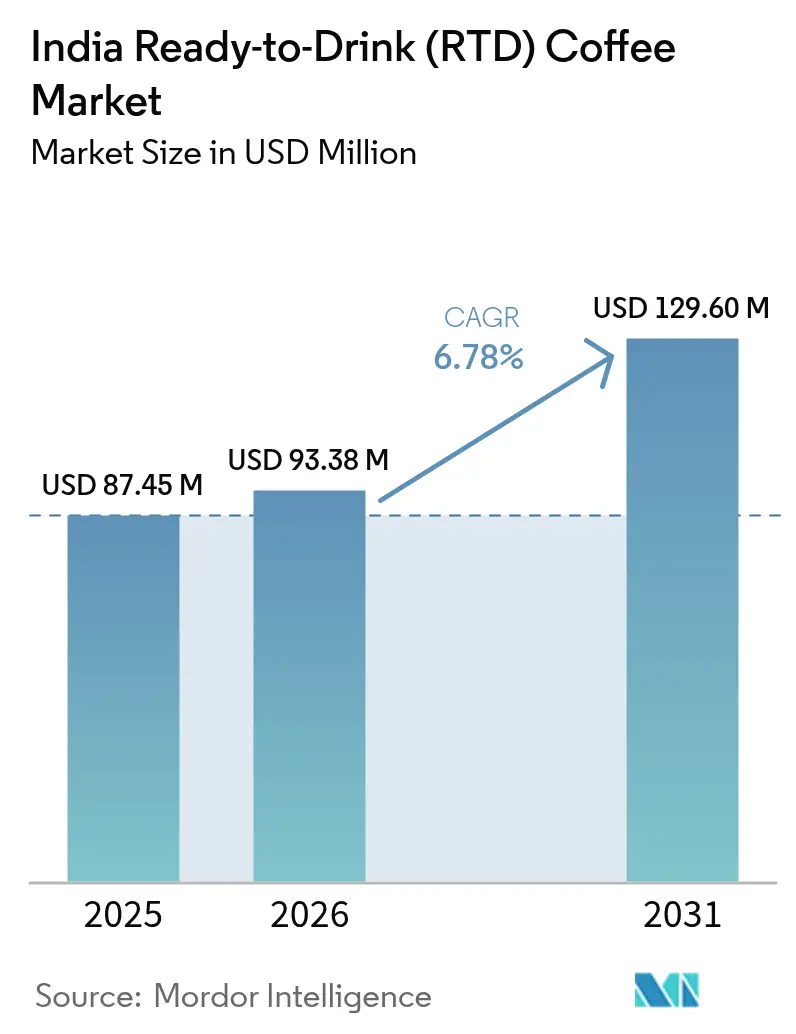

| Base Year Market Size (2025) | USD 87.45 Million |

| Market Size (2026) | USD 93.38 Million |

| Market Size (2031) | USD 129.6 Million |

| Growth Rate (2026 - 2031) | 6.78% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

India Ready-to-Drink (RTD) Coffee Market Analysis by Mordor Intelligence

The India Ready-to-Drink Coffee market size is expected to grow from USD 87.45 million in 2025 to USD 93.38 million in 2026 and is forecast to reach USD 129.6 million by 2031 at 6.78% CAGR over 2026-2031. This growth trajectory reflects a fundamental shift in Indian beverage consumption patterns, where traditional chai dominance faces increasing competition from convenience-driven coffee formats. The Coffee Board of India reported that domestic coffee consumption increased to 191,000 tonnes in 2023, with instant coffee accounting for a significant share of total consumption[1]Source: Coffee Board of India, "Domestic Coffee Consumption", www.indiacoffee.org. Government initiatives supporting value-added coffee exports have simultaneously strengthened domestic processing capacity, creating supply-side advantages for RTD manufacturers. The emergence of functional RTD coffee variants with protein and health-enhancing ingredients creates competition across beverage categories. Cold chain logistics limitations beyond tier-2 cities result in uneven market development, with urban areas experiencing rapid innovation while rural regions remain underserved. The cultural preference for fresh-brewed coffee, particularly in South India, presents opportunities for market expansion through targeted product development and distribution strategies.

Key Report Takeaways

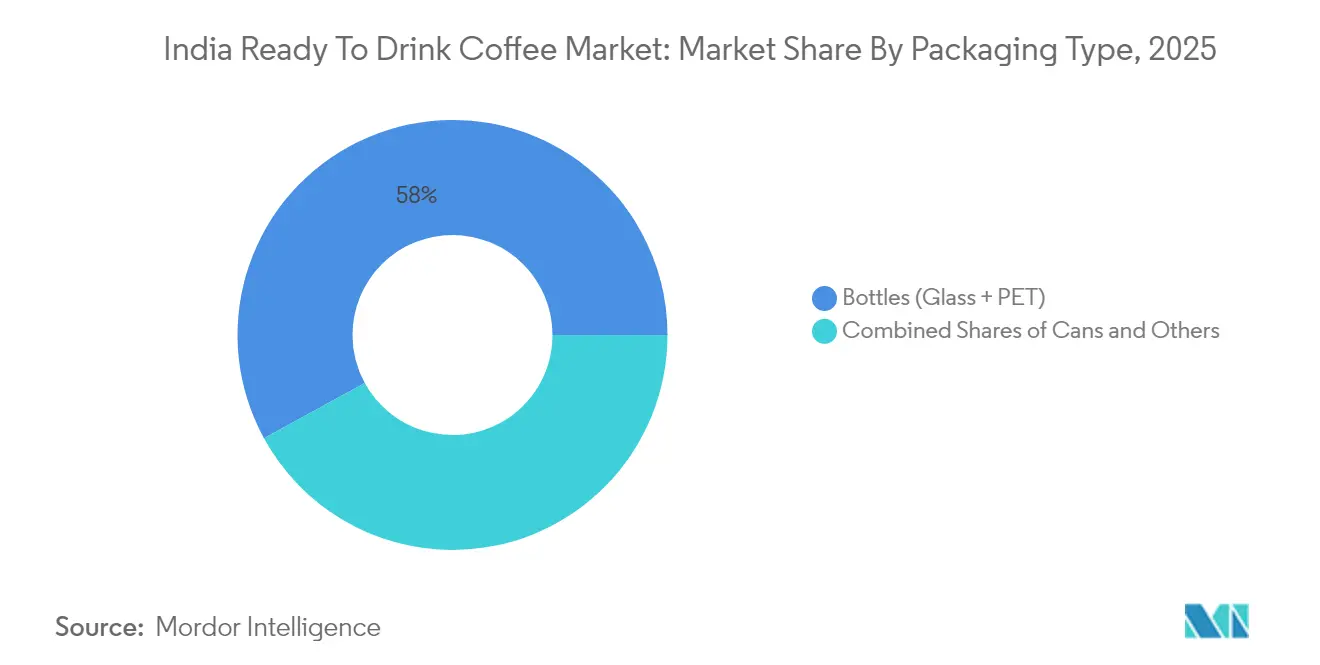

- By Packaging Type, Bottles (glass and PET) dominate with 57.98% market share in 2025, Cans fastest-growing segment at 8.92% CAGR (2026-2031).

- By Product Type, Iced latte/cappuccino variants hold 43.05% market share in 2025, Nitro RTD coffee fastest-growing at 10.12% CAGR (2026-2031).

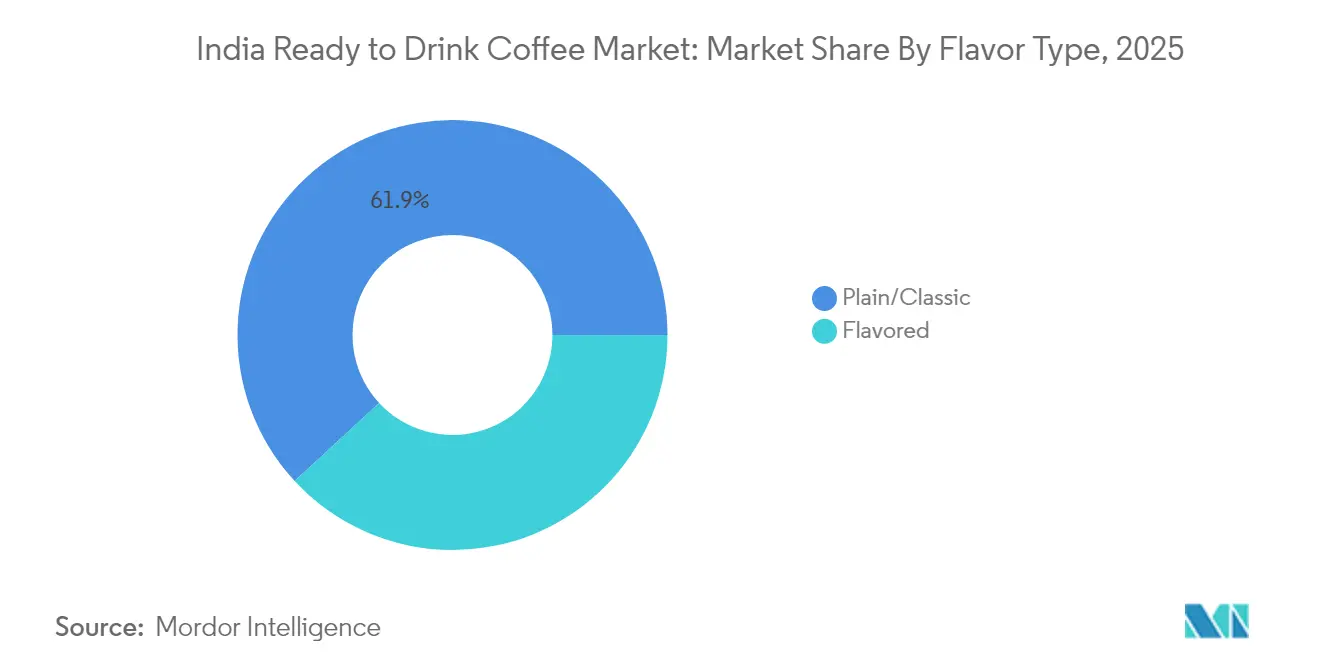

- By Flavor profile, Plain and classic variants maintain 61.88% market share in 2025, Flavored variants fastest-growing at 12.83% CAGR (2026-2031).

- By Ingredient Base, Dairy-based formulations dominate with 64.20% market share in 2025, while Plant-based alternatives fastest-growing at 10.98% CAGR (2026-2031).

- By Price, Mass-market products command 70.66% market share in 2025, while Premium segments are growing at 9.35% CAGR (2026-2031).

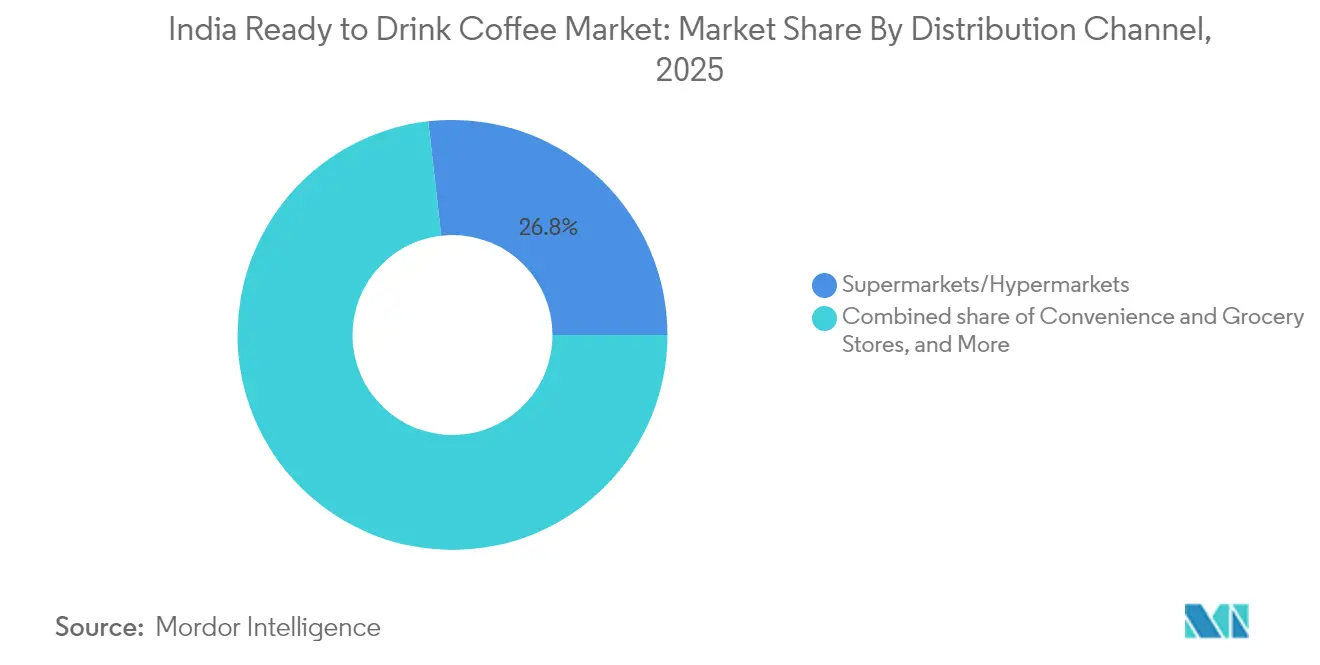

- By Distribution Channels, Supermarkets/hypermarkets maintain 26.80% market share in 2025, Online retail stores fastest-growing at 11.94% CAGR (2026-2031).

- By Region, South India leads with 34.20% market share in 2025, North India fastest-growing region at 10.52% CAGR (2026-2031).

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

India Ready-to-Drink (RTD) Coffee Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecasts | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Convenience and On-the-Go Consumption on the Rise | +1.2% | National, with early gains in Mumbai, Delhi, Bangalore | Medium term (2-4 years) |

| Augmented Expenditure on Advertising and Promotional Activities | +0.8% | Urban centers across all regions | Short term (≤ 2 years) |

| Product Innovation Experiences Notable Surge | +1.5% | South India core, spill-over to West and North India | Medium term (2-4 years) |

| Government Push for Value-Added Coffee Exports Boosting Domestic Processing Capacity | +0.9% | Karnataka, Kerala, Tamil Nadu production hubs | Long term (≥ 4 years) |

| Rising E-Commerce Growth | +1.3% | Tier-1 and Tier-2 cities nationwide | Short term (≤ 2 years) |

| Increasing Coffee Cultures among Gen Z Consumers | +1.1% | Metropolitan areas with high youth population | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Convenience and On-the-Go Consumption on the Rise

The growth in urban mobility has increased the demand for ready-to-drink (RTD) beverages, particularly among working professionals in metropolitan cities. The transition from traditional coffee shops to portable beverage options aligns with busy schedules and flexible work arrangements. The convenience and accessibility of RTD beverages make them an attractive choice for consumers who need quick refreshment during their daily commute or work hours. Tata Consumer Products recorded 17% volume growth in its RTD segment for 2025, demonstrating increased consumer preference for convenient formats as per the financial highlights of Tata Consumer Products. Office buildings and transit hubs serve as key consumption points where RTD coffee provides an alternative to traditional tea vendors. The availability of RTD beverages at these locations ensures easy access for consumers during peak hours. This consumption pattern has expanded beyond major cities into Tier-2 locations, driven by growing corporate presence and evolving workplace practices. The adoption of RTD beverages in smaller cities reflects changing consumer preferences and modernizing lifestyles across urban India.

Augmented Expenditure on Advertising and Promotional Activities

Brand-building investments are intensifying as companies recognize the need to educate consumers about RTD coffee benefits over traditional alternatives. Nestlé's partnership with Starbucks in February 2025 for retail distribution represents a strategic shift toward FMCG marketing approaches rather than café-centric promotion. Digital marketing spend is particularly pronounced as brands target younger demographics through social media platforms and influencer partnerships. Companies in the ready-to-drink (RTD) coffee market are increasingly adopting celebrity endorsements and premium positioning strategies to enhance brand visibility and market presence. For instance, Blue Tokai received investment from actress Deepika Padukone in 2023, demonstrating the growing intersection of entertainment and beverage industries. Marketing campaigns focus on lifestyle associations and aspirational messaging to position RTD coffee as a contemporary beverage choice, moving away from traditional product-centric advertising that emphasizes taste or caffeine content.

Product Innovation Experiences Notable Surge

Brewing method advancements and new packaging formats are driving product differentiation in the iced coffee segment. Advanced filtration systems, temperature-controlled brewing, and innovative extraction techniques are transforming production processes. KCROASTERS pioneered commercial cold brew coffee production in India using 24-hour steeping processes, establishing new quality benchmarks in the market. The market has expanded to include nitrogen-infused coffee and protein-enhanced beverages, appealing to health-conscious consumers seeking improved taste and nutritional benefits. Companies are developing diverse flavor profiles, including regional and seasonal varieties, through extensive research and development investments. This includes experimenting with different coffee bean origins, roasting techniques, and flavor infusion methods to create unique product offerings.

Government Push for Value-Added Coffee Exports Boosting Domestic Processing Capacity

The Coffee Board of India's initiatives to promote value-added exports have created spillover benefits for domestic RTD production through enhanced processing infrastructure. Coffee exports reached USD 1.29 billion in FY 2023-24, nearly doubling from USD 719.42 million in 2020-21, with growing demand for processed products, according to the Ministry of Commerce and Industry[2]Source: Ministry of Commerce and Industry, "Indian Coffee Brews Global Demand", www.pib.gov.in . The Integrated Coffee Development Project (ICDP) focuses on improving yields and expanding cultivation in non-traditional regions, creating supply security for RTD manufacturers. Government certification programs enhance quality standards that benefit both export and domestic markets, with the Coffee Board introducing new national certifications for producers, according to the World Coffee Portal data from 2025. These policy initiatives reduce raw material costs and improve supply chain reliability for RTD coffee producers.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecasts | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Amount of HFSS Sugar Limiting Iced Coffee Growth | -0.7% | National, with stricter enforcement in urban areas | Short term (≤ 2 years) |

| Cold-Chain Logistics Gaps Beyond Tier-2 Cities Inflate Spoilage Costs | -1.1% | Rural and semi-urban areas across all regions | Medium term (2-4 years) |

| RTD Coffee Faces Stiff Competition for Shelf Space from Emerging Alternatives | -0.6% | Modern trade channels in metropolitan areas | Short term (≤ 2 years) |

| Cultural Preference for Freshly Brewed Coffee in India | -0.9% | South India primarily, with spillover to other regions | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Amount of HFSS Sugar Limiting Iced Coffee Growth

FSSAI's mandatory labeling requirements for high-fat, salt, and sugar content in bold fonts create consumer awareness that could limit the growth of sugar-heavy RTD coffee variants. The regulatory framework requires a clear display of nutritional information, potentially deterring health-conscious consumers from high-sugar formulations. Companies must reformulate products or accept reduced market appeal, creating development costs and potential taste compromises. The prohibition of "health drink" terminology on e-commerce platforms further restricts marketing flexibility for functional coffee products. These regulations align with government initiatives to combat non-communicable diseases but create compliance burdens for manufacturers seeking mass-market appeal through sweetened variants.

Cold-Chain Logistics Gaps Beyond Tier-2 Cities Inflate Spoilage Costs

The limitations in cold-chain logistics infrastructure create significant distribution challenges, increasing operational costs and restricting market penetration in smaller cities and rural areas. Power supply disruptions and escalating fuel costs further intensify these distribution challenges, particularly affecting dairy-based ready-to-drink (RTD) coffee products that require consistent refrigeration throughout the supply chain. While the logistics sector contributes 13-14% to India's GDP, organized players hold only 5.5-6% market share, indicating substantial structural inefficiencies and fragmentation in the market, according to India Brand Equity Foundation data from 2024[3]Source: India Brand Equity Foundation, "Transforming India's Logistics Sector: Challenges and Opportunities", www.ibef.org. Although government initiatives under PM Gati Shakti aim to address these infrastructure gaps through improved connectivity and modernization of logistics networks, the implementation timelines extend beyond immediate market needs, potentially impacting the growth trajectory of the RTD coffee segment.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Packaging Type: Bottles Lead Despite Can Innovation

Bottles (glass and PET combined) commanded 57.98% market share in 2025, reflecting consumer preference for resealable packaging and premium positioning opportunities. Glass bottles particularly appeal to health-conscious consumers seeking chemical-free storage, while PET variants offer cost advantages and distribution flexibility. Cans represent the fastest-growing segment at 8.92% CAGR through 2031, driven by convenience factors and extended shelf life capabilities that reduce cold-chain dependencies.

Cartons maintain a stable position in the mass market through cost advantages, though limited premium positioning restricts growth potential. Other packaging formats, including pouches and innovative dispensing systems, remain niche but offer differentiation opportunities for specialized applications. The packaging evolution reflects broader sustainability concerns and regulatory compliance requirements. Aluminum can adoption accelerates through recycling advantages and brand differentiation opportunities, particularly among environmentally conscious consumers. Premium glass packaging enables luxury positioning but increases distribution costs and breakage risks that limit market penetration in rural areas.

By Product Type: Iced Variants Dominate Innovation Pipeline

Iced latte and cappuccino variants secured 43.05% market share in 2025, leveraging familiar flavor profiles that ease consumer transition from traditional hot coffee formats. These products benefit from established taste preferences while offering convenience advantages over café-prepared alternatives. Nitro RTD coffee emerges as the fastest-growing segment at 10.12% CAGR, targeting premium consumers seeking unique sensory experiences and perceived quality differentiation.

Cold brew RTD coffee maintains steady growth through specialty positioning and health-conscious messaging around reduced acidity levels. Functional and protein-enhanced variants represent emerging opportunities, though market education requirements limit immediate adoption rates. Nitro infusion technology requires specialized equipment investments but enables premium pricing strategies that improve unit economics. Functional ingredients like protein enhancement target fitness-conscious consumers, though regulatory compliance around health claims creates marketing constraints under FSSAI guidelines.

By Flavor Profile: Traditional Preferences Drive Flavored Growth

Plain and classic variants maintained 61.88% market share in 2025, reflecting conservative consumer preferences and established taste expectations in the Indian market. These products benefit from broad appeal and simplified production processes that enable cost-competitive positioning. Flavored variants demonstrate the strongest growth trajectory at 12.83% CAGR through 2031, driven by younger demographics seeking variety and experiential consumption. Regional flavor preferences create localization opportunities, with companies developing variants that incorporate traditional Indian tastes and seasonal preferences. Innovation in natural flavoring systems addresses health concerns while maintaining taste appeal across diverse consumer segments.

The flavor development strategy increasingly emphasizes authenticity and cultural relevance rather than international flavor profiles. Companies invest in regional taste research to develop variants that resonate with local preferences while maintaining broad market appeal. Seasonal flavor launches create purchase urgency and brand engagement, though production complexity increases inventory management challenges. Natural flavoring systems command premium pricing but require supply chain investments in specialized ingredients and quality control processes.

By Ingredient Base: Plant-Based Alternatives Gain Momentum

Dairy-based formulations dominated with 64.20% market share in 2025, benefiting from established supply chains and consumer familiarity with traditional coffee preparation methods. These products leverage India's robust dairy infrastructure and cost advantages, though quality consistency challenges persist across regional suppliers. Plant-based milk alternatives represent the fastest-growing segment at 10.98% CAGR, driven by health consciousness, lactose intolerance awareness, and environmental sustainability concerns.

Oat milk and almond milk variants particularly appeal to urban consumers seeking premium positioning and dietary flexibility. The ingredient base evolution reflects broader dietary trend shifts toward plant-based consumption patterns among affluent demographics. The companies are launching new products in the market to cater to the rising demand. For instance, in November 2024, aB Coffee brand launched a range of coconut-based beverages, including coconut-based coffee. The products are available in 75 retail stores across India.

By Price Positioning: Premium Segment Drives Value Creation

Mass-market products commanded 70.66% market share in 2025, reflecting price sensitivity among Indian consumers and the need for accessible entry points into RTD coffee consumption. These products compete directly with traditional beverage alternatives through aggressive pricing strategies and wide distribution networks. Premium segments demonstrate stronger growth at 9.35% CAGR through 2031, driven by affluent consumers seeking quality differentiation and brand prestige. Premium positioning enables higher margins that support innovation investments and brand-building activities.

The price segmentation strategy reflects income inequality patterns and varying willingness to pay across demographic segments. Premium segment development requires a careful balance between quality differentiation and price accessibility to avoid market fragmentation. Companies invest in premium ingredients, specialized packaging, and brand positioning to justify price premiums while maintaining volume growth.

By Distribution Channel: Digital Commerce Transforms Access Patterns

Supermarkets and hypermarkets maintained a 26.80% market share in 2025, providing broad consumer access and impulse purchase opportunities through strategic placement and promotional activities. These channels offer inventory management advantages and established consumer shopping patterns that support consistent sales volumes. Online retail stores represent the fastest-growing channel at 11.94% CAGR through 2031, enabling direct consumer relationships and premium positioning opportunities. Convenience and grocery stores maintain steady performance through location advantages and frequent purchase occasions.

Other channels, including vending machines and forecourt stores, offer specialized access points, though volume limitations restrict overall market impact. The distribution evolution reflects changing consumer shopping behaviors and digital adoption patterns across demographic segments. E-commerce platforms enable market expansion into Tier-2 and Tier-3 cities where physical retail presence remains limited.

Geography Analysis

South India holds a 34.20% market share in 2025, supported by its established coffee culture and consumption patterns that naturally favor RTD coffee adoption. Karnataka and Kerala's status as primary coffee-producing states offers supply chain benefits and consumer understanding of coffee quality. The region's urban centers, particularly Bangalore and Chennai, show higher disposable incomes and lifestyle preferences aligned with convenience products. The traditional filter coffee heritage helps consumers transition to RTD formats, though quality expectations remain high. Tata Starbucks focuses on South Indian markets through localized products and cultural adaptation.

North India exhibits the fastest growth at 10.52% CAGR through 2031, driven by evolving beverage preferences among young consumers and increasing urbanization. Delhi-NCR's high corporate concentration creates consumption opportunities in office complexes and transportation hubs. The region's shift from traditional tea consumption presents growth potential as coffee culture expands through cafes. Cold climate conditions support RTD coffee consumption during winter months. Government support for coffee cultivation in areas like Himachal Pradesh offers supply chain diversification opportunities.

West India, with Mumbai's financial center, shows stable growth through premium positioning and convenience-focused consumption. The region's industrial base creates workplace consumption opportunities in manufacturing and service sectors. Maharashtra's coffee cultivation initiatives support local sourcing and reduce transportation costs. East and Northeast India show growth potential despite infrastructure limitations and traditional tea preferences. Central India maintains steady performance in urban centers, while rural market penetration faces distribution and awareness challenges.

Competitive Landscape

The RTD coffee market in India exhibits moderate concentration with established FMCG giants competing alongside specialized coffee players and emerging startups, creating a dynamic competitive environment. The competitive strategy landscape reveals a bifurcation between scale-driven approaches by multinational corporations and differentiation-focused strategies by specialty coffee brands like Blue Tokai, which recently secured investment from Verlinvest, signaling increased investor interest in India's evolving coffee market, in September 2024.

White space opportunities exist in several underdeveloped segments, including functional RTD coffee with added nutritional benefits, zero-sugar formulations that address health concerns, and regionalized flavor profiles that cater to local taste preferences. The competitive dynamics are increasingly shaped by technology adoption, with digital-first brands leveraging direct-to-consumer models and data analytics to gain consumer insights that inform rapid product innovation cycles. Technology adoption patterns reveal divergent approaches, with traditional players focusing on manufacturing efficiency and supply chain optimization, while newer entrants emphasize digital marketing and e-commerce capabilities to bypass traditional retail constraints.

India Ready-to-Drink (RTD) Coffee Industry Leaders

-

Starbucks Corporation

-

Nestle SA

-

Gujarat Co-Operative Milk Marketing Federation (Amul)

-

Sleepy Owl Coffee

-

Unilever Plc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Nestlé S.A. introduced Starbucks-branded ready-to-drink (RTD) coffee products in India's retail market. This initiative stems from Nestlé's global partnership with Starbucks Corporation, which permits Nestlé to distribute Starbucks' packaged coffee and beverages beyond its café locations.

- February 2025: Nestlé expanded its Nescafé Ready-to-Drink cold coffee range to India and the Middle East and North Africa (MENA) region. The Nescafé Ready-to-Drink range includes latte, cappuccino, and mocha varieties, along with chocolate and caramel flavors.

- October 2024: Tata Consumer Products expanded its beverage line and launched Tata Coffee Grand Cold Coffee. The new products are available in three flavors: Swiss Caramel, French Vanilla, and Belgian Chocolate. These are packaged in 180ml cans and are priced at Rs 70 each.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines India's ready-to-drink coffee market as every packaged, shelf-stable or chilled beverage brewed from coffee and sealed in bottles, cans, or cartons that reaches consumers ready for immediate consumption through retail or e-commerce inside India.

We exclude powdered instant coffee, café-served beverages, RTD tea, energy drinks, and coffee concentrates sold to foodservice from this sizing.

Segmentation Overview

-

By Packaging Type

-

Bottles

- Glass Bottles

- PET Bottles

- Cans

- Cartons

- Others

-

Bottles

-

By Product Type

- Cold Brew RTD Coffee

- Iced Latte / Cappuccino

- Nitro RTD Coffee

- Functional / Protein-Enhanced RTD Coffee

-

By Flavor Profile

- Plain/Classic

- Flavored

-

By Ingredient Base

- Dairy-Based

- Plant-Based Milk

-

By Price Positioning

- Mass

- Premium

-

By Distribution Channel

- Supermarkets / Hypermarkets

- Convenience and Grocery Stores

- Online Retail Stores

- Others (Vending Machine, Forecourt Stores, etc)

-

By Region

- North India

- West India

- South India

- East and North-East India

- Central India

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts conducted interviews with beverage formulators, contract packers, organized retail buyers, and regional distributors spanning multiple metros and Tier-2 clusters. We used these conversations to test volume swings, price corridors, and packaging mix assumptions before locking the model.

Desk Research

We begin with open data from the Coffee Board of India crop bulletins, DGCI&S trade files, FSSAI label approvals, GST Network retail snapshots, and Ministry of Consumer Affairs price trackers. Trade journals such as Food & Beverage News and Packaging South Asia, company filings, and focused pulls from D&B Hoovers and Dow Jones Factiva round out average selling prices and launch counts. The sources listed are illustrative only, and many additional records supported screening, cross-checks, and narrative building.

Market-Sizing & Forecasting

A top-down consumption pool converts annual packaged coffee output, import flows, and measured retail off-take into ex-factory value. Targeted bottom-up checks multiply sampled producer volumes with blended ASPs to fine-tune totals. Key inputs include bottled beverage excise clearances, PET resin prices, cold-chain penetration, e-commerce share, and café density signals. Five-year projections employ multivariate regression anchored to GDP per capita, urban millennial population, and premium SKU penetration.

Data Validation & Update Cycle

Each figure faces two internal reviews, and variance flags reopen source discussions. We refresh every report annually and issue mid-cycle patches when material regulatory or price shocks appear.

Why Our India Ready to Drink Coffee Baseline Earns Trust

We acknowledge that published estimates often diverge because firms mix scopes, price tiers, or channels, yet decision makers need one dependable anchor.

We observe that some publishers fold café pours or allied tea drinks into totals, convert INR sales with single-day rates, or uplift ASPs without validating unit scans.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 87.45 Million | Mordor Intelligence | - |

| USD 1,723.2 Million | Global Consultancy A | Includes foodservice and bulk concentrates |

| USD 2,330 Million | Industry Databank B | Combines RTD coffee with RTD tea and energy variants |

| USD 3,335.4 Million | Market Tracker C | Uses broader beverage basket and aggressive ASP uplift |

These contrasts show that our tightly defined packaged-only scope, multi-source cross-checks, and timely refresh give managers a balanced, reproducible baseline.

Key Questions Answered in the Report

What is the current market size and growth rate of India's RTD coffee market?

The India Ready-to-Drink Coffee market reached USD 93.38 million in 2026 and is projected to grow at a CAGR of 6.78% from 2026-2031, reaching USD 129.6 million by 2031.

Which region dominates the Indian RTD coffee market?

South India commands 34.20% market share in 2025, leveraging deeply embedded coffee culture in states like Karnataka, Kerala, and Tamil Nadu. However, North India is the fastest-growing region with 10.52% CAGR through 2031, driven by changing beverage preferences among younger demographics.

What are the key distribution channels driving market growth?

Supermarkets and hypermarkets maintain 26.80% market share in 2025, while online retail stores represent the fastest-growing channel at 11.94% CAGR through 2031.

Which packaging format is most popular in the Indian RTD coffee market?

Bottles (glass and PET combined) dominate with 57.98% market share in 2025, preferred for resealability and premium positioning. However, cans represent the fastest-growing segment at 8.92% CAGR, driven by convenience factors and extended shelf life capabilities.

Page last updated on: