Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Historical Data Period | 2021 - 2024 |

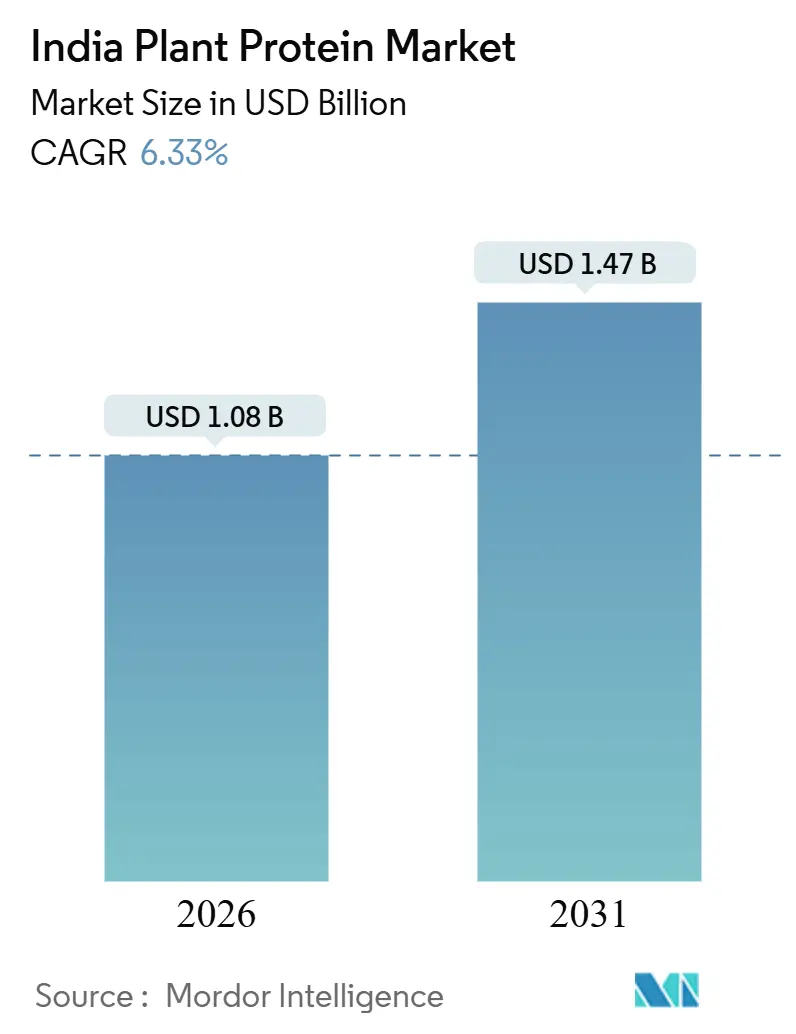

| Market Size (2026) | USD 1.08 Billion |

| Market Size (2031) | USD 1.47 Billion |

| Growth Rate (2026 - 2031) | 6.33% CAGR |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

India Plant Protein Market Analysis by Mordor Intelligence

The India plant protein market size stood at USD 1.08 billion in 2026 and is projected to reach USD 1.47 billion by 2031, registering a 6.33% CAGR over the period. Rising flexitarian habits in metros, a policy thrust on domestic pulses, and capacity expansions by integrated processors continue to reshape sourcing, processing, and consumption patterns. Government incentives such as the INR 11,440 crore Mission for Aatmanirbharta in Pulses ensure dependable feedstock, while import-duty hikes on yellow peas push manufacturers to localize pea-protein supply. Urban consumers are increasingly health-focused, and 84% report prioritizing safer food choices, creating headroom for fortified products and hybrid meat analogues. Investments by conglomerates such as Adani Wilmar and ingredient majors like ADM improve domestic extraction efficiency and lower unit costs. Price volatility in soy and pea commodities, labeling compliance, and limited consumer awareness outside tier-1 cities remain watchpoints, yet the India plant protein market continues to broaden as processors diversify into chickpea, mung bean, and rice proteins.

Key Report Takeaways

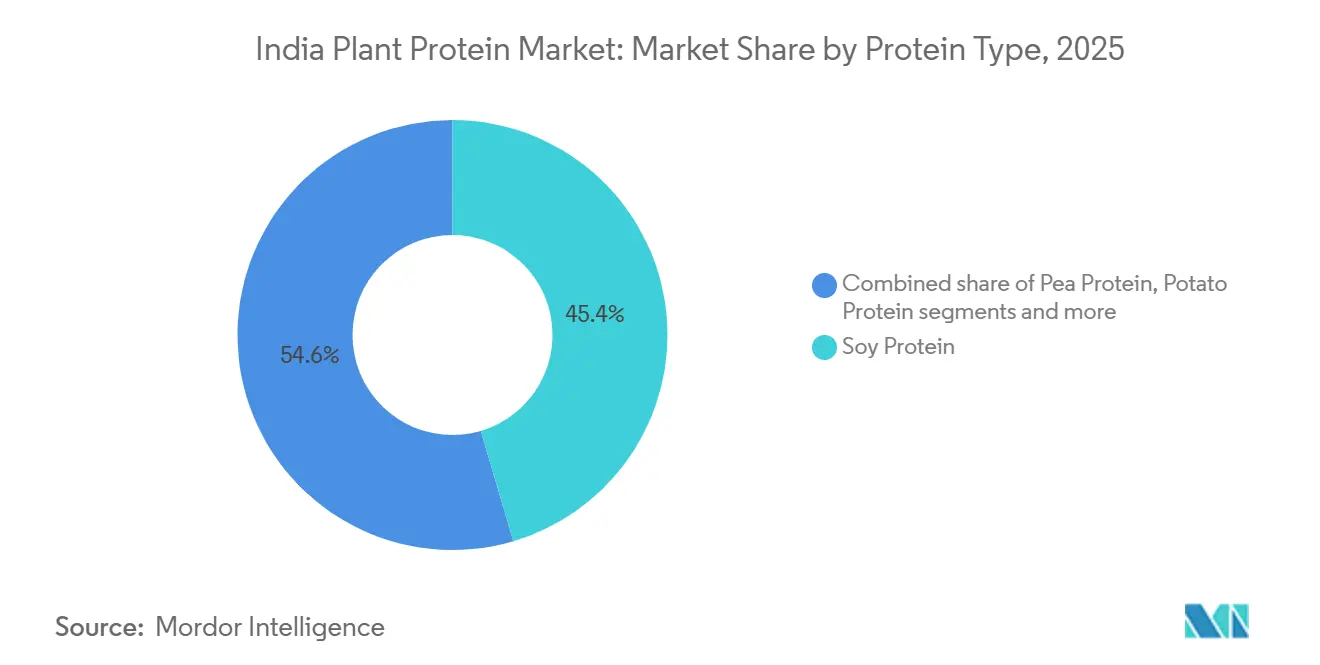

By protein type, soy commanded 45.43% of the India plant protein market share in 2025, and pea protein is forecast to expand at a 7.65% CAGR through 2031.

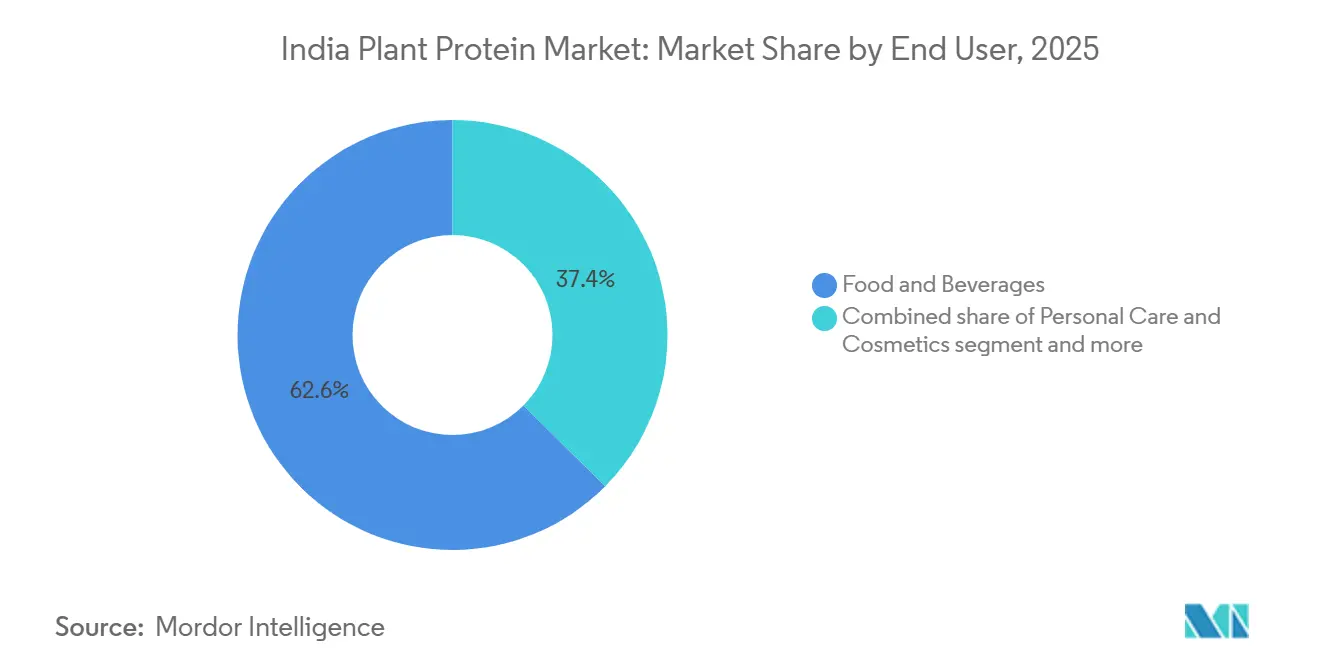

By end user, food and beverages accounted for 62.57% of revenue in 2025, and supplements are projected to record a 6.94% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

India Plant Protein Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growth of plant-based and flexitarian diets | +1.2% | National, concentrated in metros (Mumbai, Delhi, Bengaluru, Chennai) with spillover to tier-2 cities | Medium term (2-4 years) |

| Rising demand for lactose-free protein alternatives | +0.9% | National, particularly urban and semi-urban areas with higher dairy intolerance awareness | Short term (≤ 2 years) |

| Government nutrition and crop-support initiatives | +1.5% | National, with production focus in Madhya Pradesh, Maharashtra, Rajasthan, Uttar Pradesh | Long term (≥ 4 years) |

| Expansion of processed food and beverage and supplements sectors | +1.3% | National, driven by organized retail and e-commerce in urban centers | Medium term (2-4 years) |

| Consumer preferences for clean-label and digestible products | +0.8% | Urban and affluent segments nationwide | Short term (≤ 2 years) |

| Technological innovations in protein development | +0.6% | National, with R&D hubs in Bengaluru, Pune, Hyderabad | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growth of Plant-Based and Flexitarian Diets

Urban India's dietary landscape is undergoing a quiet recalibration, with flexitarian adoption, partial substitution of animal protein rather than wholesale elimination, emerging as the dominant consumption pattern among millennials and Gen Z cohorts. This nuanced shift favors hybrid formats, plant-based kebabs, paneer analogues, and protein-enriched traditional snacks over direct meat replacements, compelling manufacturers to localize formulations around familiar spice profiles and cooking methods. The Ministry of Statistics and Programme Implementation's July 2025 press note on nutritional intake in India documented persistent protein deficiency across population segments, creating policy momentum for fortified plant-protein products in mid-day meal schemes and public distribution systems. This structural protein gap is a key catalyst across the entire India Protein market, where rising health awareness is pushing consumers toward diverse protein sources. Organized retail and quick-service restaurants are accelerating trial by stocking plant-based options alongside conventional offerings, reducing the friction of category switching for price-sensitive consumers.

Rising Demand for Lactose-Free Protein Alternatives

Lactose intolerance prevalence in India, estimated to affect a significant portion of the adult population, has historically been underserved by mainstream dairy, opening a structural opportunity for plant-based milk, yogurt, and paneer analogues. Soy milk and pea-protein beverages are gaining traction in urban households as functional substitutes, with manufacturers emphasizing fortification with calcium, vitamin D, and B12 to address nutritional gaps associated with dairy avoidance. FSSAI's nutrition labeling guidelines mandate a clear declaration of protein content per 100 grams and per serving, enabling direct comparison with animal-derived dairy and supporting consumer confidence in protein adequacy[1]Source: Food Safety and Standards Authority of India, “Guidelines on Nutrition Labelling,” fssai.gov.in. The regulatory requirement for allergen disclosure, particularly for soy, a major allergen, ensures transparency but also necessitates careful formulation and supply-chain controls to prevent cross-contamination. Startups are leveraging e-commerce and subscription models to reach early adopters, bypassing traditional retail gatekeepers and capturing direct consumer feedback to refine taste and texture.

Government Nutrition and Crop-Support Initiatives

The Union Cabinet's October 2025 approval of the Mission for Aatmanirbharta in Pulses, with a six-year budget of INR 11,440 crore (approximately USD 1.37 billion), represents the most significant policy intervention in domestic pulse supply in a decade. The mission aims to raise area, productivity, and post-harvest infrastructure for chickpea, pigeon pea, lentil, and mung bean, directly addressing raw-material constraints for pulse-derived protein concentrates and isolates. NITI Aayog's September 2025 report on strategies for accelerating pulse growth underscored the need for improved seed systems, agronomy extension, and value-chain investments to reduce import dependence and stabilize prices[2]Source: NITI Aayog, “Strategies and Pathways for Accelerating Growth in Pulses,” pib.gov.in. For plant-protein processors, this policy thrust signals predictable feedstock availability and potential downward pressure on pulse prices over the medium term, enhancing the competitiveness of domestic pulse proteins versus imported pea or soy isolates. The mission's emphasis on processing and value addition creates co-investment opportunities for private-sector fractionation facilities and pilot-scale protein extraction plants.

Expansion of Processed Food and Beverage and Supplements Sectors

India's organized food-processing sector is experiencing a structural upgrade, with investments in cold-chain logistics, modern packaging, and retail distribution networks enabling shelf-stable plant-protein products to reach tier-2 and tier-3 cities. APEDA's 2023-24 annual report detailed infrastructure grants and export-promotion schemes that reduce capital expenditure burdens for plant-protein processors, while technical assistance programs support MSMEs in meeting international quality and safety standards[3]Source: Agricultural and Processed Food Products Export Development Authority, “Pulses,” apeda.gov.in . The supplements segment, encompassing sports nutrition, infant formula, and elderly nutrition, is witnessing regulatory evolution, with FSSAI's January 2024 Infant Food Regulations (Version II) setting stringent compositional and allergen-labeling requirements for plant protein inclusion in early childhood products. Manufacturers must demonstrate protein quality via PDCAAS or equivalent metrics and ensure amino acid complementation where plant proteins replace dairy, raising the bar for formulation expertise and clinical substantiation. E-commerce platforms and direct-to-consumer brands are bypassing traditional retail by leveraging digital marketing and influencer partnerships to educate consumers about protein content, clean labels, and sustainability claims.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Price premium over animal protein | -0.8% | National, most acute in rural and semi-urban areas with high price sensitivity | Short term (≤ 2 years) |

| Volatile pea and soy commodity prices | -0.6% | National, with production risk concentrated in Madhya Pradesh, Maharashtra | Medium term (2-4 years) |

| Low awareness and sensory barriers beyond metros | -0.5% | Rural and tier-3 cities, where traditional animal-protein consumption is entrenched | Medium term (2-4 years) |

| Regulatory hurdles related to protein content claims and labeling standards | -0.4% | National, affecting product development timelines and market entry | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Price Premium Over Animal Protein

Plant-based protein products in India typically retail at 20-40% premiums over conventional animal proteins, a gap that limits mass-market adoption and confines growth to affluent urban segments. Soybean wholesale prices averaged Rs 4,825 per quintal in September 2024, while crusher margins remained compressed due to competition from cheaper Argentine soymeal and discounted imported soybean oil, according to the Agricultural Market Intelligence Centre, PJTAU[4]Source: PJTSAU Agricultural Market Intelligence Centre, “Soyabean Outlook – October 2024,” pjtau.edu.in. These input-cost pressures translate into higher retail prices for soy-based protein concentrates and isolates, undermining competitiveness against chicken, eggs, and dairy in price-sensitive households. The government's May 2025 decision to raise the minimum support price for soybeans by 9% to Rs 5,328 per quintal aimed to incentivize farmers but inadvertently elevated feedstock costs for processors, tightening margins and constraining their ability to reduce consumer prices United States Department of Agriculture, Foreign Agricultural Service. Achieving price parity will require scale economies in fractionation, localized sourcing of pulses under the Pulses Mission, and formulation innovations that blend lower-cost rice or wheat proteins with premium pea or soy isolates to optimize cost-performance trade-offs.

Volatile Pea and Soy Commodity Prices

Soybean production in marketing year 2025/26 declined 12% to 10.7 million tonnes due to untimely rainfall, re-sowing delays, and farmer diversion to rice, sugarcane, and maize, tightening domestic soymeal supply and raising feedstock uncertainty for plant-protein manufacturers, according to the United States Department of Agriculture, Foreign Agricultural Service (USDA FAS). Crush volumes fell 6% to 9.5 million tonnes, and soymeal production dropped to 7.6 million tonnes, with ending stocks cut by 52% to 455,000 tonnes, signaling supply-side stress. India's November 2025 increase in import duties on yellow peas, a key feedstock for pea-protein isolates, further constrained alternative sourcing options, compelling domestic processors to absorb higher landed costs or pass them to downstream customers, according to USDA FAS. Madhya Pradesh and Maharashtra's combined 82% share of the national soybean area concentrates production risk in two states, amplifying vulnerability to localized weather shocks and pest outbreaks. Diversifying feedstock portfolios to include chickpea, mung bean, and rice proteins, alongside strategic buffer stocking and forward contracting, will be essential to mitigate price volatility and ensure supply continuity.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Protein Type: Soy Dominance Meets Pea-Protein Momentum

Soy Protein held 45.43% market share in 2025, anchored by India's established soybean cultivation in Madhya Pradesh and Maharashtra, states that collectively account for 82% of the national soybean area, and mature crushing infrastructure capable of producing soymeal, soy flour, and textured vegetable protein at scale according to PJTSAU. Domestic soybean crush reached 9.5 million tonnes in marketing year 2025/26, yielding 7.6 million tonnes of soymeal, a portion of which is diverted to food-grade applications, including soy protein concentrates and isolates for meat analogues, dairy alternatives, and fortified bakery products, as per the USDA FAS. Pea Protein is forecast to expand at a 7.65% CAGR through 2031, driven by import-substitution incentives following India's November 2025 increase in yellow pea import duties, which raised landed costs for imported pea protein and spurred domestic interest in cultivating field peas and investing in fractionation capacity. Pea protein's neutral flavor profile and hypoallergenic properties position it favorably in infant formula and sports nutrition segments, where soy's allergenicity and phytoestrogen concerns can limit adoption.

Rice Protein and Wheat Protein occupy smaller but growing niches, with rice protein appealing to gluten-free and allergen-sensitive consumers, and wheat gluten (vital wheat gluten) serving as a texturizer in plant-based meat analogues and bakery applications. Hemp Protein and Potato Protein remain nascent in India, constrained by limited domestic cultivation of industrial hemp, regulatory approvals for hemp cultivation are state-specific and incomplete, and the absence of large-scale potato-protein extraction facilities. Other Plant Proteins, including chickpea, mung bean, and lentil proteins, benefit from India's status as the world's largest pulse producer (25.238 million tonnes in 2024-25) and offer opportunities for localized ingredient development aligned with traditional dietary patterns according to APEDA. FSSAI's May 2023 standards for solvent-extracted soya flour (minimum 48% protein on dry basis, hexane residue ≤10 ppm) and protein-enriched atta (minimum 15% protein) provide compositional benchmarks that guide formulation and quality control for manufacturers. Technological advances in alkaline extraction and enzymatic hydrolysis are improving protein yields and functional properties, enabling domestic processors to compete with imported isolates on cost and performance.

By End User: Food & Beverages Lead, Supplements Accelerate

Food & Beverages commanded 62.57% end-user share in 2025, reflecting entrenched demand across dairy alternatives (soy milk, pea-protein yogurt, paneer analogues), meat alternatives (plant-based kebabs, burgers, sausages), bakery products (protein-enriched bread, biscuits), ready-to-eat meals, and beverages (protein shakes, fortified drinks). Dairy and Dairy Alternatives represent the largest sub-segment, driven by lactose intolerance prevalence and consumer preference for familiar formats, milk, curd, and paneer, that integrate seamlessly into daily diets. Meat/Poultry/Seafood Alternatives are gaining traction in urban quick-service restaurants and modern retail, with startups like GoodDot, Imagine Meats, and Blue Tribe Foods leveraging direct-to-consumer channels and localized flavors (tikka, keema, biryani) to overcome sensory barriers. Bakery applications benefit from FSSAI's regulatory allowance for up to 15% plant-protein flour (soy, groundnut) in protein-enriched atta and maida, enabling fortified staples to reach mass markets via traditional retail and public distribution systems.

Supplements are forecast to grow at a 6.94% CAGR through 2031, driven by rising health consciousness, the adoption of sports nutrition among millennials, and regulatory clarity on protein-content claims. Sports and Dietary Supplements, whey-alternative protein powders, ready-to-drink shakes, and protein bars, are capturing share from imported whey protein as domestic pea and soy isolates improve in taste and mixability. FSSAI's guidance on sports nutrition and food supplements for sportspersons, issued in 2025, set standards for protein content, amino acid profiles, and permissible additives, reducing regulatory ambiguity and encouraging product launches FSSAI. Baby Food and Infant Formula face stringent regulatory hurdles under FSSAI's January 2024 Infant Food Regulations, which mandate protein quality metrics (PDCAAS thresholds), allergen labeling, and clinical substantiation for plant-protein inclusion, limiting near-term adoption but creating opportunities for specialized formulations targeting lactose-intolerant infants. Elderly and Medical Nutrition products, high-protein, easy-to-digest formulations for geriatric and convalescent populations, are emerging as a niche segment, with manufacturers fortifying plant-protein bases with calcium, vitamin D, and B12 to address age-related nutritional deficiencies.

Animal Feed applications consume a significant portion of soymeal output (6.15 million tonnes in 2025/26), with poultry and aquaculture sectors driving demand for protein-rich feed ingredients according to the USDA FAS. However, feed-sector substitution toward distillers' dried grains (DDGs) and de-oiled rice bran, byproducts of expanding grain-based ethanol production, is reducing soymeal demand, potentially freeing supply for food-grade plant-protein processing. Personal Care and Cosmetics represent a nascent application, with plant proteins (soy, wheat, rice) used as conditioning agents, film-formers, and emulsifiers in hair-care and skin-care formulations, though this segment remains marginal relative to food and feed uses.

Geography Analysis

India's plant-protein market is geographically anchored in Madhya Pradesh and Maharashtra, which together accounted for 82% of the national soybean area in 2024-25 and host the majority of large-scale crushing facilities operated by Ruchi Soya, Sonic Biochem, and regional cooperatives, according to the PJTSAU. Madhya Pradesh alone accounted for 42.14% of soybean area (53.48 lakh hectares), with production concentrated in districts like Indore, Ujjain, and Dewas, where established procurement networks and processing clusters enable efficient conversion of oilseed into soymeal and soy flour. Maharashtra's 40.47% area share (51.36 lakh hectares) supports a parallel processing ecosystem, with facilities in Nagpur, Akola, and Latur serving domestic food manufacturers and export markets. Rajasthan, Karnataka, Gujarat, and Telangana collectively account for the remaining 18%, with Rajasthan contributing 8.87% of the soybean area and emerging as a secondary production hub. Pulse production is more geographically dispersed, with Madhya Pradesh, Maharashtra, Rajasthan, Uttar Pradesh, Gujarat, Karnataka, Jharkhand, Andhra Pradesh, Chhattisgarh, and West Bengal all contributing to the 25.238 million tonnes harvested in 2024-25, providing feedstock diversity for chickpea, pigeon pea, lentil, and mung bean proteins according to APEDA.

Urban consumption is concentrated in metros, Mumbai, Delhi, Bengaluru, Chennai, Hyderabad, and Pune, where modern retail penetration, e-commerce adoption, and exposure to international food trends drive early adoption of plant-based meat analogues, dairy alternatives, and protein supplements. Tier-2 cities, Ahmedabad, Jaipur, Lucknow, Coimbatore, Visakhapatnam, are witnessing gradual diffusion as organized retail expands and consumer awareness grows, though price sensitivity and limited cold-chain infrastructure remain constraints. Rural and semi-urban areas, which account for the majority of India's population, exhibit lower awareness and adoption, with traditional animal-protein consumption patterns and fragmented retail networks limiting plant-protein penetration. Export dynamics are evolving, with India exporting 793,291.51 metric tonnes of pulses valued at USD 854.89 million in fiscal year 2024-25, primarily to Bangladesh, China, UAE, USA, and Sri Lanka, signaling potential for value-added pulse-protein exports if domestic fractionation capacity scales. APEDA's 2023-24 annual report highlighted infrastructure grants and export-promotion schemes that support quality upgrades, testing, and market access for plant-protein processors targeting international markets.

State-level policy initiatives are beginning to shape regional competitiveness, with Madhya Pradesh and Maharashtra offering subsidies for oilseed processing and value-addition infrastructure, while Karnataka and Telangana, home to biotech and food-processing hubs in Bengaluru and Hyderabad, are attracting R&D investments in novel extraction technologies and fermentation-based proteins. The Union Cabinet's October 2025 approval of the Mission for Aatmanirbharta in Pulses, with a six-year budget of INR 11,440 crore, is expected to strengthen pulse production across multiple states, reducing regional supply imbalances and stabilizing feedstock prices for plant-protein manufacturers. Logistics infrastructure, cold-chain networks, warehousing, and port connectivity, remains a bottleneck, particularly for perishable plant-based dairy and meat analogues, with the government's focus on food-processing zones and integrated cold-chain projects under the Ministry of Food Processing Industries aimed at addressing these gaps.

Competitive Landscape

The India plant-protein market is consolidating, with key players like Ruchi Soya (under Patanjali Ayurved), Sonic Biochem, ADM, and Cargill controlling significant soy-crushing and soymeal production capacity, while a growing cohort of startups and mid-sized players targets niche segments with differentiated products and direct-to-consumer strategies. Ruchi Soya, India's largest integrated soy-plant-protein and soya-foods producer, operates crushing facilities, refining units, and branded consumer-product lines, leveraging vertical integration to manage feedstock costs and supply-chain risks.

Sonic Biochem, a leading non-GMO soya functional-protein manufacturer, focuses on export markets and domestic food-ingredient supply, emphasizing quality certifications and traceability to meet international standards. Multinationals like ADM and Cargill supply soy and plant-protein ingredients to Indian food and feed manufacturers, with ADM's January 2025 announcement of sustainable soy production programs in India signaling a strategic commitment to local sourcing and sustainability credentials. PROWISE India, the country's first and only manufacturer of isolated soy protein (ISP), targets premium plant-protein ingredient markets, competing on purity and functional properties. Startups, GoodDot Enterprises, Imagine Meats, Blue Tribe Foods, and Shaka Harry, are disrupting traditional channels by launching plant-based meat analogues tailored to Indian palates, using modern retail, e-commerce, and foodservice partnerships to bypass incumbent distribution networks. These players leverage consumer insights, rapid product iteration, and digital marketing to capture early-adopter segments, though scalability remains constrained by high customer-acquisition costs and limited access to cost-competitive protein isolates.

Adani Wilmar's January 2025 commissioning of a Rs 1,300 crore food-processing plant in Sonepat exemplifies capacity expansion by diversified conglomerates seeking to integrate upstream oilseed crushing with downstream value-added protein products, potentially intensifying competition for feedstock and shelf space. White-space opportunities include pulse-based protein isolates (chickpea, mung bean, lentil), which align with India's domestic production strengths and cultural familiarity, yet remain underdeveloped due to limited fractionation capacity and technical expertise. Technology adoption, wet fractionation, enzymatic hydrolysis, and fermentation, will determine competitive positioning, with early movers in green extraction technologies potentially capturing cost and sustainability advantages as GFI India's March 2025 standardization initiative gains traction.

India Plant Protein Industry Leaders

Ruchi Soya Industries Ltd.

Sonic Biochem Extractions Pvt Ltd.

Archer Daniels Midland Company (ADM)

Cargill, Incorporated

PROWISE India

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Prot has launched Prot Block, a pea‑protein–based ingredient designed as a versatile, allergen‑free solution that bridges the gap between highly processed meat analogues and limited conventional plant proteins, enabling easy integration of plant protein into everyday dishes.

- January 2025: ADM announced programs to support sustainable soy production in India, partnering with farmers, cooperatives, and NGOs to improve yields, soil health, and traceability, aiming to secure long-term, sustainable feedstock supply for plant-protein ingredient manufacturing.

- January 2025: Adani Wilmar commissioned a Rs 1,300 crore (approximately USD 156 million) food-processing plant in Sonepat, Haryana, expanding domestic processing capacity and signaling the entry of diversified conglomerates into the manufacturing of value-added plant-protein products.

India Plant Protein Market Report Scope

Plant protein refers to protein extracted or derived from plant sources such as legumes, grains, seeds, and nuts, used as a nutritional ingredient in foods, beverages, and supplements. This report defines the India Plant Protein Market as the industry focused on the production, processing, and application of proteins derived from plant sources and examines its scope by protein type (hemp, pea, potato, rice, soy, wheat, and other plant proteins) and by end user, including animal feed; food and beverages (bakery, beverages, breakfast cereals, condiments/sauces, confectionery, dairy and dairy alternatives, meat/poultry/seafood and their alternatives, ready-to-eat/ready-to-cook foods, and snacks); personal care and cosmetics; and supplements (baby food and infant formula, elderly and medical nutrition, and sports and dietary supplements).

By Protein Type

| Hemp Protein |

| Pea Protein |

| Potato Protein |

| Rice Protein |

| Soy Protein |

| Wheat Protein |

| Other Plant Protein |

By End User

| Animal Feed | |

| Food and Beverages | Bakery |

| Beverages | |

| Breakfast Cereals | |

| Condiments/Sauces | |

| Confectionery | |

| Dairy and Dairy Alternatives | |

| Meat/Poultry/Seafood and Alternatives | |

| RTE/RTC Foods | |

| Snacks | |

| Personal Care and Cosmetics | |

| Supplements | Baby Food and Infant Formula |

| Elderly and Medical Nutrition | |

| Sport and Dietary Supplements |

| By Protein Type | Hemp Protein | |

| Pea Protein | ||

| Potato Protein | ||

| Rice Protein | ||

| Soy Protein | ||

| Wheat Protein | ||

| Other Plant Protein | ||

| By End User | Animal Feed | |

| Food and Beverages | Bakery | |

| Beverages | ||

| Breakfast Cereals | ||

| Condiments/Sauces | ||

| Confectionery | ||

| Dairy and Dairy Alternatives | ||

| Meat/Poultry/Seafood and Alternatives | ||

| RTE/RTC Foods | ||

| Snacks | ||

| Personal Care and Cosmetics | ||

| Supplements | Baby Food and Infant Formula | |

| Elderly and Medical Nutrition | ||

| Sport and Dietary Supplements | ||

Market Definition

- End User - The Protein Ingredients Market operates on a B2B basis. Food, Beverages, Supplements, Animal Feed, and Personal Care & Cosmetic manufacturers are considered to be end-consumers in the market studied. The scope excludes manufacturers buying liquid/dry whey to be used for application as a binding agent or thickener or other non-protein applications.

- Penetration Rate - Penetration Rate is defined as the percentage of Protein-Fortified End User Market Volume in the Overall End User Market Volume.

- Average Protein Content - Average protein content is the average protein content present per 100 g of product manufactured by all end-user companies considered under the scope of this report.

- End User Market Volume - End-user market volume is the consolidated volume of all types and forms of end-user products in the country or region.

| Keyword | Definition |

|---|---|

| Alpha-lactalbumin (α-Lactalbumin) | It is a protein that regulates the production of lactose in the milk of almost all mammalian species. |

| Amino acid | It is an organic compound that contains both amino and carboxylic acid functional groups, which are required for the synthesis of body protein and other important nitrogen-containing compounds, such as creatine, peptide hormones, and some neurotransmitters. |

| Blanching | It is the process of briefly heating vegetables with steam or boiling water. |

| BRC | British Retail Consortium |

| Bread improver | It is a flour-based blend of several components with specific functional properties designed to modify dough characteristics and give quality attributes to bread. |

| BSF | Black Soldier Fly |

| Caseinate | It is a substance produced by adding an alkali to acid casein, a derivative of casein. |

| Celiac disease | Celiac disease is an immune reaction to eating gluten, a protein found in wheat, barley, and rye. |

| Colostrum | It is a milky fluid that’s released by mammals that have recently given birth before breast milk production begins. |

| Concentrate | It is the least processed form of protein and has a protein content ranging from 40-90% by weight. |

| Dry protein basis | It refers to the percentage of "pure protein" present in a supplement after the water in it is completely removed through heat. |

| Dry whey | It is the product resulting from drying fresh whey which has been pasteurized and to which nothing has been added as a preservative. |

| Egg protein | It is a mixture of individual proteins, including ovalbumin, ovomucoid, ovoglobulin, conalbumin, vitellin, and vitellenin. |

| Emulsifier | It is a food additive that facilitates the blending of foods that are immiscible with one another, such as oil and water. |

| Enrichment | It is the process of addition of micronutrients that are lost during the processing of the product. |

| ERS | Economic Research Service of the USDA |

| Extrusion | It is the process of forcing soft mixed ingredients through an opening in a perforated plate or die designed to produce the required shape. The extruded food is then cut to a specific size by blades. |

| Fava | Also known as Faba, it is another word for yellow split beans. |

| FDA | Food and Drug Administration |

| Flaking | It is a process in which typically a cereal grain (like corn, wheat, or rice) is broken down into grits, cooked with flavors and syrups, and then pressed into flakes between cooled rollers. |

| Foaming agent | It is a food ingredient that makes it possible to form or maintain a uniform dispersion of a gaseous phase in a liquid or solid food. |

| Foodservice | It refers to the part of the food industry which includes businesses, institutions, and companies which prepare meals outside the home. It includes restaurants, school and hospital cafeterias, catering operations, and many other formats. |

| Fortification | It is the deliberate addition of micronutrients that are not found in them naturally or which are lost during processing, to improve a food product's nutritional value. |

| FSANZ | Food Standards Australia New Zealand |

| FSIS | Food Safety and Inspection Service |

| FSSAI | Food Safety and Standards Authority of India |

| Gelling agent | It is an ingredient that functions as a stabilizer and thickener to provide thickening without stiffness through the formation of gel. |

| GHG | Greenhouse Gas |

| Gluten | It is a family of proteins found in grains, including wheat, rye, spelt, and barley. |

| Hemp | It is a botanical class of Cannabis sativa cultivars grown specifically for industrial or medicinal use. |

| Hydrolysate | It is a form of protein manufactured by exposing the protein to enzymes that can partially break the bonds between the protein's amino acids and break down large, complicated proteins into smaller pieces. Its processing makes it easier and quicker to digest. |

| Hypoallergenic | It refers to a substance that causes fewer allergic reactions. |

| Isolate | It is the purest and most processed form of protein which has undergone separation to obtain a pure protein fraction. It typically contains ≥ 90% of protein by weight. |

| Keratin | It is a protein that helps form hair, nails, and the outer layer of skin. |

| Lactalbumin | It is the albumin contained in milk and obtained from whey. |

| Lactoferrin | It is an iron‑binding glycoprotein that is present in the milk of most mammals. |

| Lupin | It is the yellow legume seeds of the genus Lupinus. |

| Millenial | Also known as Generation Y or Gen Y, it refers to the people born from 1981 to 1996. |

| Monogastric | It refers to an animal with a single-compartmented stomach. Examples of monogastric include humans, poultry, pigs, horses, rabbits, dogs, and cats. Most monogastric are generally unable to digest much cellulose food materials such as grasses. |

| MPC | Milk protein concentrate |

| MPI | Milk protein isolate |

| MSPI | Methylated soy protein isolate |

| Mycoprotein | Mycoprotein is a form of single-cell protein, also known as fungal protein, derived from fungi for human consumption. |

| Nutricosmetics | It is a category of products and ingredients that act as nutritional supplements to care for skin, nails, and hair natural beauty. |

| Osteoporosis | It is a medical condition in which the bones become brittle and fragile from loss of tissue, typically as a result of hormonal changes, or deficiency of calcium or vitamin D. |

| PDCAAS | Protein digestibility-corrected amino acid score (PDCAAS) is a method of evaluating the quality of a protein based on both the amino acid requirements of humans and their ability to digest it. |

| Per-capita consumption of animal protein | It is the average amount of animal protein (such as milk, whey, gelatin, collagen, and egg proteins) that is readily available for consumption by each person in an actual population. |

| Per-capita consumption of plant protein | It is the average amount of plant protein (such as soy, wheat, pea, oat, and hemp proteins) that is readily available for consumption by each person in an actual population. |

| Quorn | It is a microbial protein manufactured using mycoprotein as an ingredient, in which the fungus culture is dried and mixed with egg albumen or potato protein, which acts as a binder, and then is adjusted in texture and pressed into various forms. |

| Ready-to-Cook (RTC) | It refers to food products that include all of the ingredients, where some preparation or cooking is required through a process that is given on the package. |

| Ready-to-Eat (RTE) | It refers to a food product prepared or cooked in advance, with no further cooking or preparation required before being eaten. |

| RTD | Ready-to-Drink |

| RTS | Ready-to-Serve |

| Saturated fat | It is a type of fat in which the fatty acid chains have all single bonds. It is generally considered unhealthy. |

| Sausage | It is a meat product made of finely chopped and seasoned meat, which may be fresh, smoked, or pickled and which is then usually stuffed into a casing. |

| Seitan | It is a plant-based meat substitute made out of wheat gluten. |

| Softgel | It is a gelatin-based capsule with a liquid fill. |

| SPC | Soy protein concentrate |

| SPI | Soy protein isolate |

| Spirulina | It is a biomass of cyanobacteria that can be consumed by humans and animals. |

| Stabilizer | It is an ingredient added to food products to help maintain or enhance their original texture, and physical and chemical characteristics. |

| Supplementation | It is the consumption or provision of concentrated sources of nutrients or other substances that are intended to supplement nutrients in the diet and is intended to correct nutritional deficiencies. |

| Texturant | It is a specific type of food ingredient that is used to control and alter the mouthfeel and texture of food and beverage products. |

| Thickener | It is an ingredient that is used to increase the viscosity of a liquid or dough and make it thicker, without substantially changing its other properties. |

| Trans fat | Also called trans-unsaturated fatty acids or trans fatty acids, it is a type of unsaturated fat that naturally occurs in small amounts in meat. |

| TSP | Textured soy protein |

| TVP | Textured vegetable protein |

| WPC | Whey protein concentrate |

| WPI | Whey protein isolate |

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: Identify Key Variables: The quantifiable key variables (industry and extraneous) pertaining to the specific product segment and country are selected from a group of relevant variables & factors based on desk research & literature review; along with primary expert inputs. These variables are further confirmed through regression modeling (wherever required).

- Step-2: Build a Market Model: In order to build a robust forecasting methodology, the variables and factors identified in Step-1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set and the model is built on the basis of these variables.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms