Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

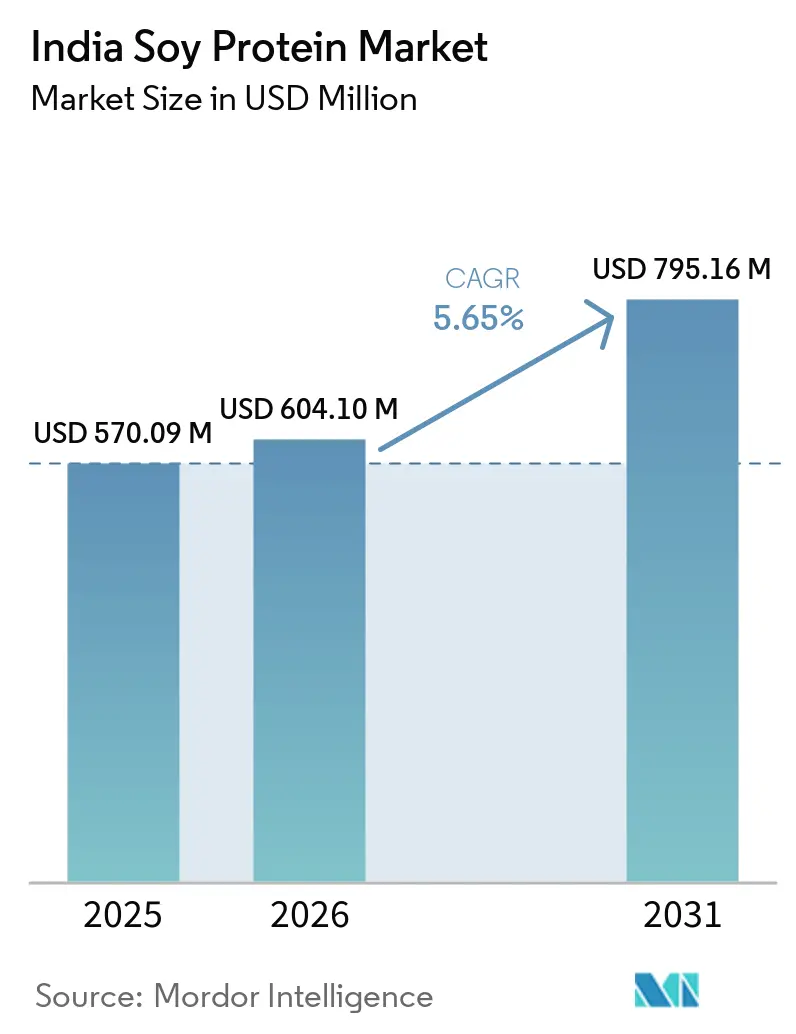

| Base Year Market Size (2025) | USD 570.09 Million |

| Market Size (2026) | USD 604.10 Million |

| Market Size (2031) | USD 795.16 Million |

| Growth Rate (2026 - 2031) | 5.65% CAGR |

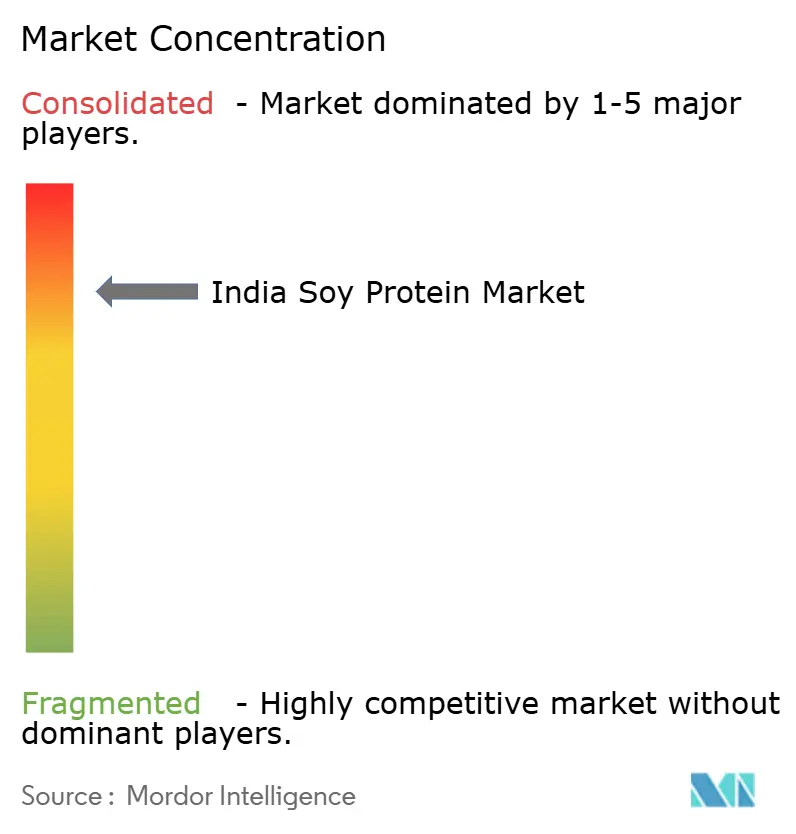

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

India Soy Protein Market Analysis by Mordor Intelligence

The India Soy Protein Market size was valued at USD 570.09 million in 2025 and expected to grow from USD 604.10 million in 2026 to reach USD 795.16 million by 2031, at a CAGR of 5.65% during the forecast period (2026-2031). Larger domestic crushing capacity, a rising flexitarian consumer base, and government incentives that reward value-addition rather than raw-bean exports continue to pull demand for soy protein concentrates, isolates, and textured variants. However, utilization remains below the installed 11.4 million-ton ceiling because volatile feedstock prices compress crush margins and invite substitution with cheaper protein meals. Food and beverage formulators are expanding their use of soy isolates in meat analogues, RTD nutrition beverages, and baked snacks, while sports-nutrition brands push growth in supplements. Policy levers such as the Production-Linked Incentive (PLI) scheme for food processing and the National Mission on Edible Oils (NMEO) promise better availability of raw materials and improved processing economics over the medium term.

Key Report Takeaways

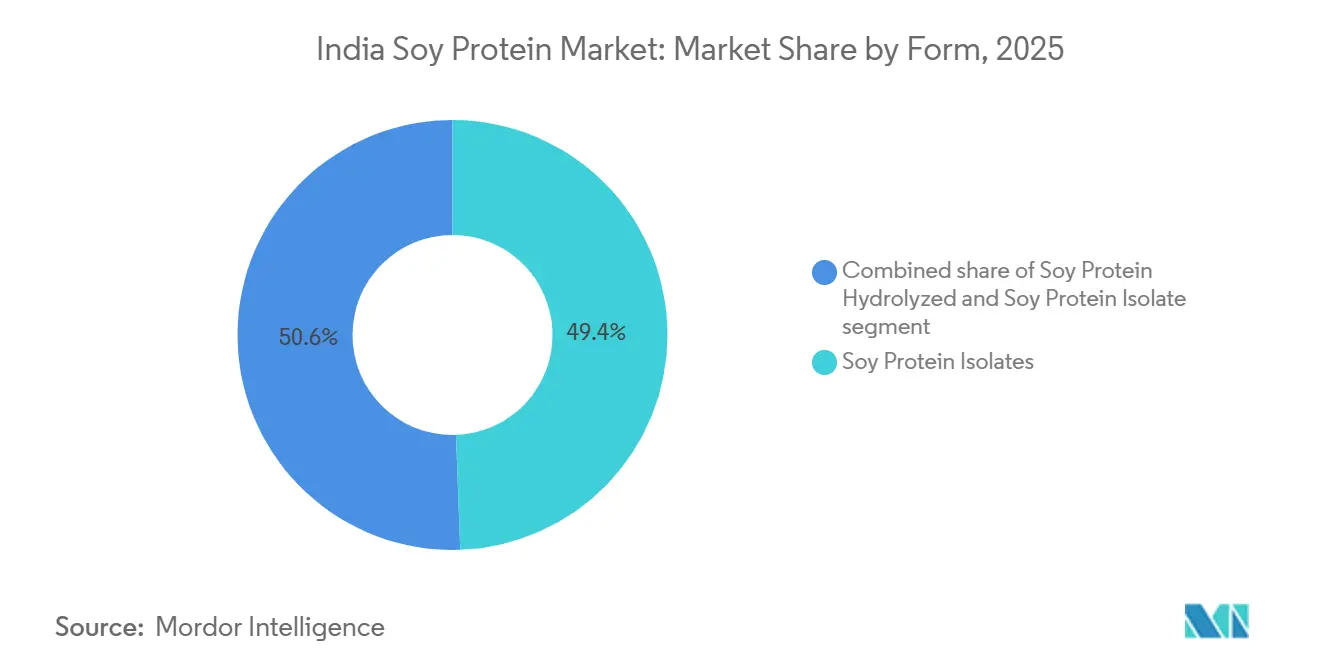

- By form, soy protein isolates led with 49.43% of the India soy protein market share in 2025, while textured and hydrolyzed variants are forecast to expand at a 5.95% CAGR through 2031.

- By category, conventional protein captured a 68.57% share in 2025, whereas organic variants are poised to grow at a 6.44% CAGR through 2031.

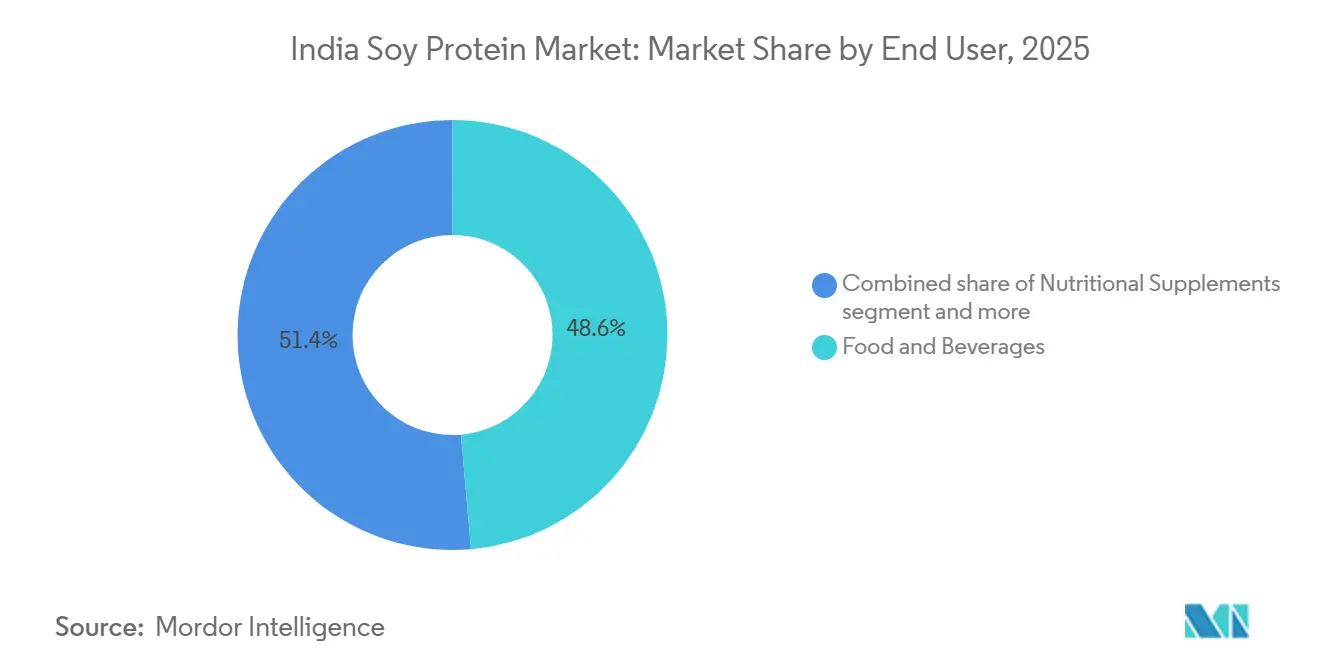

- By end user, food and beverages accounted for 48.63% in 2025, while supplements are set to grow at a 6.24% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

India Soy Protein Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing vegetarian, vegan, and flexitarian diets drive soy protein | +1.2% | National, with concentration in urban metros and Tier-1 cities | Medium term (2-4 years) |

| Rising demand for plant-based protein-fortified snacks, beverages, and ready-to-drink products | +1.4% | National, led by Maharashtra, Karnataka, Delhi-NCR, Tamil Nadu | Short term (≤ 2 years) |

| Adoption of soy-based proteins in Indian pet food and aquafeed | +0.6% | National, early adoption in coastal states (Andhra Pradesh, West Bengal, Tamil Nadu) for aquafeed | Long term (≥ 4 years) |

| Growth of sports nutrition and high-protein supplements | +1.1% | National, urban concentration in metros and Tier-1/Tier-2 cities | Short term (≤ 2 years) |

| Government and industry initiatives to promote plant-based proteins | +0.8% | National, with policy focus in Madhya Pradesh, Maharashtra, Rajasthan (major soy-producing states) | Medium term (2-4 years) |

| Use of soy protein in infant formulas, weaning foods, and dairy-free milks | +0.5% | National, urban and semi-urban markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Growing Vegetarian, Vegan, and Flexitarian Diets Drive Soy Protein

India's protein consumption landscape reveals a structural deficit: 73% of the population falls short of daily protein requirements, with vegetarians showing 91% deficiency and non-vegetarians 85%, according to data released by Country Delight in August 2025. This gap creates latent demand for affordable plant-based proteins, where soy isolates and concentrates offer cost advantages over dairy and meat. The Ministry of Statistics and Programme Implementation's Nutritional Intake in India report (June 2025) quantifies per-capita protein intake by state and identifies regions with the highest cereal-dominant diets as priority markets for soy-fortified staples[1]Source: Office of the Registrar General, “Nutritional Intake in India,” MOSPI, mospi.gov.in. Urban consumers are shifting toward flexitarian diets not solely for ethical reasons but due to rising meat prices and health awareness campaigns linking plant proteins to cardiovascular benefits. Tata Consumer Products entered the plant protein powder segment in September 2022 with Tata GoFit, leveraging brand equity to capture health-conscious consumers. Akshayakalpa Organic announced a protein-focused strategy, targeting Rs 550 crore (USD 66 million) in revenue in fiscal 2025, signaling a pivot by FMCG players toward protein portfolios.

Rising Demand for Plant-Based Protein-Fortified Snacks, Beverages, and Ready-to-Drink Products

The convergence of convenience, nutrition, and clean-label demands is reshaping product development cycles in packaged foods. Country Delight launched a high-protein cow's milk in August 2025, delivering 30 grams of protein per 450 ml serving, positioning it as a meal replacement and addressing the 90% of urban consumers unaware of the recommended daily protein intake. While dairy-based, this innovation signals broader acceptance of protein fortification across beverage categories, creating adjacency opportunities for soy protein isolates in plant-based RTD shakes and protein waters. Patanjali Foods' Food & FMCG segment, which explicitly includes textured soy protein, grew revenue 57% year-on-year to Rs 6,938.71 crore (USD 829 million) in the nine months ending December 2023, with biscuits alone contributing Rs 1,225.72 crore (USD 146 million), suggesting soy protein's integration into mass-market snack formulations according to Patanjali Foods Limited. The Production Linked Incentive scheme for food processing, announced in December 2024, incentivizes capacity expansion and technology upgradation for processed food manufacturers, lowering barriers to soy protein adoption in snack extrusion and beverage fortification, according to the Press Information Bureau. FSSAI's labeling regulations mandate allergen declaration for soy and compositional thresholds for protein claims, ensuring transparency but also raising compliance costs for smaller players.

Adoption of Soy-Based Proteins in Indian Pet Food and Aquafeed

Aquaculture expansion and premiumization in pet food are unlocking niche but high-growth demand for soy protein concentrates and isolates. The FAO's State of World Fisheries and Aquaculture 2024 highlights global aquaculture's shift toward plant proteins to reduce reliance on fishmeal, a trend India mirrors as domestic aquaculture intensifies. India's livestock and aquaculture sectors, documented in the Department of Animal Husbandry & Dairying's Annual Report 2023-24, face rising feed costs and seasonal constraints on soybean meal availability, prompting formulators to explore processed soy protein concentrates with higher digestibility and lower anti-nutritional factors. Pet food remains a nascent segment, but urbanization and nuclear-family structures are driving pet ownership and the willingness to pay for premium, protein-rich formulations. Anand Agro's 275 tons-per-day organic soybean processing facility, certified under NPOP and APEDA, produces extruded soy meal with 47-48% protein and 6% fat, positioning it for feed applications where higher energy density and amino acid profiles justify premiums over solvent-extracted meal. However, feed-sector substitution with distillers dried grains and de-oiled rice bran, driven by ethanol policy and rice milling byproduct availability, is eroding soymeal's share in poultry rations, with feed consumption forecast at 6.15 million metric tons for 2025/26, down from 6.99 million metric tons, according to the FAS New Delhi (USDA)[2]Source: Das S., “Oilseeds and Products Update,” USDA FAS, usda.gov.

Growth of Sports Nutrition and High-Protein Supplements

The sports nutrition segment is transitioning from a gym-centric niche to a mainstream wellness category, catalyzed by strategic M&A and brand extensions. Zydus Wellness's Rs 390 crore (USD 46.6 million) acquisition of Naturell, maker of Ritebite Max Protein bars, in October 2024 underscores corporate recognition of the segment's scalability and margin profile. Naturell reported revenues of Rs 129 crore (USD 15.4 million) in FY24, and Zydus expects distribution synergies to accelerate penetration beyond metro gyms into Tier-2 and Tier-3 retail. While whey protein dominates the powder segment, soy protein isolates are gaining traction among vegan and lactose-intolerant consumer cohorts, as well as in bar formulations where cost and allergen profiles matter. Tata Consumer Products' entry into the plant protein market with Tata GoFit plant protein powder in September 2022 leverages the Tata brand's trust to address skepticism about plant protein efficacy[3]Source: Tata Consumer Products, “Tata GoFit Plant Protein Powder,” Tata Consumer Products, tataconsumer.com. The segment's growth is also demographic: rising disposable incomes, greater female participation in fitness, and awareness of protein's role in aging and chronic disease management are expanding the addressable base. FSSAI's health claims regulations require scientific substantiation for protein quality and functional claims, creating a compliance moat that favors established brands with R&D capabilities over unorganized players.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Soybean price volatility | -0.9% | National, acute in Madhya Pradesh, Maharashtra, Rajasthan (major producing states) | Short term (≤ 2 years) |

| High processing and isolation costs | -0.7% | National, affecting small and mid-sized processors | Medium term (2-4 years) |

| Stringent FSSAI and regulatory scrutiny around soy safety, labeling, and health claims | -0.4% | National | Medium term (2-4 years) |

| Limited domestic soybean processing capacity | -0.6% | National, capacity constraints in non-traditional states | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Soybean Price Volatility

Raw material cost instability is the most immediate threat to processor margins and downstream pricing competitiveness. Soybean production for the marketing year 2025/26 fell to 10.7 million metric tons, down 12% from initial forecasts of 12.1 million metric tons, due to untimely rainfall, re-sowing delays, and farmer shifts to rice, sugarcane, and corn, according to the FAS New Delhi (USDA). The government raised minimum support prices 9% to Rs 5,328 per quintal (USD 62.6 per quintal) in May 2025, yet market-yard prices in July-August 2025 hovered at Rs 5,500-5,600 per quintal, expected to climb toward Rs 5,900-6,000 per quintal as lower production tightens supplies. Crushers face a double squeeze: higher input costs and reduced import duty on crude edible oils (effective 16.5% from 27.5% per the May 30, 2025, notification), which increases the competitiveness of imported soybean oil and depresses domestic crush incentives. Soymeal ending stocks for 2025/26 are forecast at 455,000 metric tons, a 52% reduction from prior levels, which will constrain availability for food-grade protein extraction. Weather variability and limited irrigation in rainfed soybean belts of Madhya Pradesh and Maharashtra amplify year-to-year production swings, preventing processors from securing long-term fixed-price contracts with food manufacturers. The National Mission on Edible Oils aims to stabilize supply through higher yields and expanded acreage, but its impact will materialize only over the medium term.

High Processing and Isolation Costs

Producing soy protein isolates and concentrates requires capital-intensive extraction, purification, and drying equipment, creating scale economies that favor large integrated players. Anand Agro's 275 tons-per-day extruder-based facility, sourcing machinery from Bronto (Ukraine) and Buhler, demonstrates the infrastructure investment needed to produce high-protein (47-48%) extruded meal with controlled urease activity and protein dispersibility index. Isolation processes for 90%+ protein content isolates involve additional steps, aqueous extraction, pH adjustment, centrifugation, and spray drying—that multiply energy and water costs. Smaller processors operating solvent extraction plants for commodity soybean meal lack the technical expertise and capital to retrofit for isolate production, limiting domestic supply and forcing food manufacturers to import or substitute with lower-purity concentrates. Energy costs in India, while lower than in developed markets, are rising, and water scarcity in soybean-producing regions adds operational risk. The Production Linked Incentive scheme's capital subsidy and technology upgradation support can partially offset these barriers, but eligibility criteria and bureaucratic processes may exclude smaller players. Bunge Limited's 2024 annual report emphasizes global investments in processing capacity and downstream ingredient capabilities, signaling that multinationals are positioning to supply India's growing demand for higher-margin soy protein products.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Form: Isolates Lead, Textured Variants Accelerate

Soy protein isolates captured 49.43% of the market share in 2025, reflecting their dominance in applications that demand high protein purity, neutral flavor, and superior emulsification properties, such as meat analogues, protein bars, and clinical nutrition formulas. Textured and hydrolyzed soy proteins, while holding smaller shares, are expanding at a 5.95% CAGR through 2031, driven by ready-to-eat snacks, extruded meat substitutes, and convenience foods where texture and chewiness are critical. Soy protein concentrates occupy the middle ground, offering 70% protein content at a lower cost than isolates, and find use in bakery, dairy analogues, and animal feed where extreme purity is unnecessary. The shift toward textured forms is evident in Patanjali Foods' Food & FMCG segment, which explicitly includes textured soy protein and grew 64% year-on-year in Q3FY24, with biscuits and snacks contributing significant volumes to market share in 2025, reflecting their dominance in applications that demand them.

Processing technology differentiates from performance: isolates require aqueous extraction and spray drying, concentrates use alcohol washing or acid leaching, and textured variants employ extrusion cooking under high temperature and pressure. Anand Agro's extruder-based plant, producing 220 metric tons per day of soya meal with 47-48% protein and 6% fat, demonstrates the technical capability to produce higher-fat, higher-energy extruded products suitable for feed and food applications. Hydrolyzed soy proteins, produced via enzymatic or acid hydrolysis, offer improved solubility and reduced allergenicity, positioning them for infant formula and medical nutrition, though regulatory scrutiny around allergen labeling under FSSAI rules remains stringent. The Production Linked Incentive scheme's support for technology upgradation is expected to accelerate adoption of advanced extrusion and isolation equipment, narrowing the cost gap between domestic and imported soy protein forms.

By Category: Conventional Dominates, Organic Gains Momentum

Conventional soy protein accounted for 68.57% of market share in 2025, underpinned by cost competitiveness, established supply chains, and broad acceptance across feed, food, and industrial applications. Organic soy protein, certified under APEDA's National Programme for Organic Production, is growing at a 6.44% CAGR through 2031, propelled by export demand from Europe and North America, premium domestic positioning, and consumer willingness to pay for non-GMO and pesticide-free credentials. Anand Agro's NPOP and APEDA-certified organic soybean processing facility, with 275 tons-per-day capacity, exemplifies the infrastructure needed to capture organic premiums, though organic soybean acreage remains a small fraction of total cultivation[4]Source: Agricultural & Processed Food Products Export Development Authority, “NPOP Standards,” apeda.gov.in.

Organic certification imposes additional costs, conversion periods, input restrictions, third-party audits, and traceability documentation that limit participation by smallholder farmers and smaller processors. However, APEDA's 2023-24 annual report highlights export promotion activities, laboratory upgrades, and capacity-building initiatives for organic exporters, thereby reducing compliance friction. The National Mission on Edible Oils' emphasis on high-yielding varieties and value-chain clusters does not explicitly prioritize organic cultivation, suggesting conventional production will continue to dominate domestic supply. Conventional soy protein benefits from economies of scale in crushing and processing, lower input costs, and broader farmer adoption, but faces reputational risks in premium segments where GMO and pesticide concerns influence purchasing decisions. Organic soy protein's growth trajectory depends on expanding certified acreage, improving yield parity with conventional varieties, and maintaining price premiums that justify higher production costs.

By End User: Food and Beverages Anchor Demand, Supplements Surge

Food and beverages commanded 48.63% end-user share in 2025, spanning bakery, dairy analogues, meat substitutes, ready-to-eat meals, and snacks, where soy protein serves as a functional ingredient for texture, emulsification, and protein fortification. The supplements segment, encompassing sports nutrition, infant formula, and medical nutrition, is expanding at a 6.24% CAGR through 2031, driven by acquisitions such as Zydus Wellness's Rs 390 crore (USD 46.6 million) purchase of Naturell in October 2024 and Tata Consumer Products' entry with Tata GoFit plant protein powder. Animal feed remains a significant but slower-growing end user, constrained by substitution with distillers' dried grains and de-oiled rice bran. Feed consumption of soymeal is forecast at 6.15 million metric tons for 2025/26, down from 6.99 million metric tons, according to FAS New Delhi (USDA).

Within food and beverages, meat analogues and dairy-free milks are high-growth niches, though absolute volumes remain modest. Country Delight's August 2025 launch of a 30-gram protein cow's milk, while dairy-based, signals broader acceptance of protein fortification, which benefits plant-based RTD beverages. Patanjali Foods' biscuit segment, which contributed Rs 1,225.72 crore (USD 146 million) in nine months ending December 2023, likely incorporates soy protein for cost reduction and protein enrichment. The supplements segment's growth is demographic and behavioral: rising disposable incomes, greater female participation in fitness, and awareness of protein's role in aging and chronic disease management are expanding the addressable base beyond gym-goers. FSSAI's health claims regulations require scientific substantiation for protein quality and functional claims, creating a compliance moat that favors established brands with R&D capabilities. Animal feed demand is tied to livestock and poultry production growth, documented in the Department of Animal Husbandry & Dairying's Basic Animal Husbandry Statistics 2025, which provides state-wise livestock counts and production volumes that drive compound feed demand.

Geography Analysis

India's soy protein market is geographically anchored in the soybean-producing belt of Madhya Pradesh, Maharashtra, and Rajasthan, which together account for over 77% of national oilseed output, with Madhya Pradesh alone contributing approximately 52% of soybean production according to the National Mission on Edible Oils, Press Information Bureau[5]Source: Press Information Bureau, “National Mission on Edible Oils,” pib.gov.in. Crushing capacity is concentrated in these states, creating logistics advantages for processors and reducing transportation costs for raw materials. However, demand is increasingly urban and dispersed, with metros and Tier-1 cities in Karnataka, Tamil Nadu, Delhi-NCR, and Gujarat driving consumption of soy-based meat analogues, protein supplements, and dairy-free beverages. The National Mission on Edible Oils targets expanding soybean cultivation into non-traditional areas by utilizing rice and potato fallows and promoting intercropping, aiming to add 4 million hectares by 2030-31, thereby decentralizing processing capacity and reducing regional supply bottlenecks. Coastal states such as Andhra Pradesh, West Bengal, and Tamil Nadu are emerging demand centers for aquafeed applications, where soy protein concentrates and isolates are substituting fishmeal in intensive shrimp and fish farming systems, as highlighted in the FAO's State of World Fisheries and Aquaculture 2024.

Regional disparities in protein consumption, documented in the Ministry of Statistics and Programme Implementation's Nutritional Intake in India report (June 2025), reveal states with higher cereal-dominant diets and lower pulse and dairy intake as priority markets for soy-fortified staples and supplementary foods. The government's November 2025 announcement of grants for soy processing units across Madhya Pradesh, Rajasthan, Maharashtra, and Assam signals intent to expand capacity beyond traditional hubs, though Assam's inclusion suggests exploratory efforts to establish processing in the Northeast. Export competitiveness has eroded, with soymeal shipments forecast at 15.5 lakh tonnes for 2025/26 versus 22.75 lakh tonnes the previous year, as Argentine soymeal undercuts Indian prices and geopolitical disruptions in Iran and Bangladesh curtail traditional buyers. Domestic consumption is rising, with food-grade soybean use forecast at 820,000 metric tons for 2025/26, reflecting incremental demand from tofu, soy milk, and soy-based snacks, particularly in urban markets according to the FAS New Delhi (USDA).

Infrastructure constraints, seasonal production, limited storage, and inadequate cold chains, amplify regional price volatility and force farmers to sell immediately post-harvest, depressing prices and discouraging quality premiums. The National Mission on Edible Oils' emphasis on post-harvest infrastructure, including 50 new seed storage units and support for collection and extraction facilities, aims to stabilize regional supply chains. APEDA's export promotion activities, documented in its 2023-24 annual report, include trade delegations, participation in overseas food shows, and market intelligence dissemination, which support soy protein exporters in accessing premium international markets. However, customs duty increases on crude edible oils from 5.5% to 16.5% and on refined oils from 13.75% to 35.75%, implemented to protect domestic processors, also raise input costs for food manufacturers reliant on imported soy oil, creating regional cost differentials.

Competitive Landscape

The India soy protein market exhibits high concentration, with the top five players commanding 88% combined share, reflecting scale economies in crushing, integrated supply chains, and brand equity that create formidable entry barriers. Ruchi Soya Industries, rebranded as Patanjali Foods following Patanjali Ayurved's Rs 4,350 crore (USD 520 million) acquisition in December 2019, leverages the largest integrated soy-protein and soya-foods production infrastructure in India, coupled with Patanjali's extensive retail distribution and consumer trust. Sonic Biochem Extractions dominates the non-GMO soya functional-protein segment, serving export markets and premium domestic customers requiring NPOP or equivalent certifications.

Cargill India and Bunge India, as subsidiaries of global agribusiness giants, supply industrial-grade soy protein ingredients to feed mills and food processors, benefiting from global sourcing networks and technical expertise in protein isolation and concentrate production. Marico, traditionally an FMCG edible oil player, has entered soy-protein-based foods with its Saffola Soya Bhurji and Meal Maker brands, targeting mass-market consumers with affordable, branded soy products. White-space opportunities exist in higher-margin segments, organic soy protein isolates, hydrolyzed soy proteins for infant formula, and textured soy proteins for premium meat analogues, where domestic supply is limited and imports or substitutes dominate. Emerging disruptors include GoodDot, Blue Tribe Foods, and AS-IT-IS Nutrition, which focus on plant-based meat alternatives and direct-to-consumer protein supplements, leveraging e-commerce and social media to bypass traditional retail.

GoodDot received investment from Sixth Sense Ventures in July 2021 to scale production and expand distribution of plant-based minced meat, kebabs, and nuggets. Technology adoption is a competitive differentiator: extruder-based processing, as demonstrated by Anand Agro's 275 tons-per-day facility, produces higher-protein, lower-moisture soy meal with superior amino acid profiles compared to solvent extraction, justifying premiums in feed and food applications. Compliance with FSSAI's labeling, allergen declaration, and health claims regulations creates a moat for established players with in-house quality assurance and regulatory affairs teams, while smaller entrants face delays and rejections.

India Soy Protein Industry Leaders

Sonic Biochem Extractions Pvt. Ltd

Ruchi Soya Industries Ltd

Cargill India

Agro Solvent Products Pvt Ltd

Marico Ltd

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- August 2025: Country Delight launched a high-protein cow's milk delivering 30 grams of protein per 450 ml serving, targeting the 73% of Indians who fall short of their daily protein requirements, with plans to extend the product line to include high-protein paneer, dahi, whole-grain breads, and fresh batters.

- October 2024: Zydus Wellness acquired Naturell, maker of Ritebite Max Protein bars and snacks, for Rs 390 crore (USD 46.6 million) in an all-cash deal, positioning Zydus to expand its healthy-snacking portfolio and leverage distribution synergies to scale the brand beyond metro gyms into Tier-2 and Tier-3 retail.

- July 2024: Patanjali Ayurved sold its food retail business to Ruchi Soya (now Patanjali Foods) for Rs 690 crore (USD 82.5 million), consolidating Ruchi Soya's retail and food portfolio and expanding its distribution footprint for soy-derived products.

India Soy Protein Market Report Scope

Soy protein is the protein found in soybeans, a legume native to East Asia. It is one of the few plant‑based proteins that provides all nine essential amino acids, making it a “complete” protein similar in quality to animal proteins. Soy protein is extracted from dehulled and defatted soybeans and then processed into different commercial forms. The report on the India Soy Protein Market offers a detailed assessment of market dynamics, including key growth drivers, restraints, opportunities, and emerging trends influencing industry development. It provides market size estimates and forecasts for value and volume, along with an analysis of the competitive landscape and the regulatory environment in India. The study's scope encompasses segmentation by form, category, and end user to provide comprehensive insights into demand patterns across various applications. By form, the market is classified into soy protein concentrates, soy protein hydrolyzed, and soy protein isolates. Based on category, the market is divided into organic and conventional products. Regarding end users, the report covers applications in animal feed, food and beverages, and nutritional supplements. The food and beverages segment is further analyzed across bakery, beverages, breakfast cereals, condiments and sauces, confectionery, dairy and dairy alternatives, meat, poultry, seafood and meat alternative products, ready-to-eat and ready-to-cook foods, and snacks. The nutritional supplements segment includes baby and infant formula, elderly and medical nutrition, and sport and performance nutrition.

By Form

| Soy Protein Concentrates |

| Soy Protein Hydrolyzed |

| Soy Protein Isolates |

By Category

| Organic |

| Conventional |

By End User

| Animal Feed | |

| Food and Beverages | Bakery |

| Beverages | |

| Breakfast Cereals | |

| Condiments/Sauces | |

| Confectionery | |

| Dairy and Dairy Alternatives | |

| Meat/Poultry/Seafood and Meat Alternative Products | |

| RTE/RTC Foods | |

| Snacks | |

| Nutritional Supplements | Baby and Infant Formula |

| Elderly and Medical Nutrition | |

| Sport/Performance Nutrition |

| By Form | Soy Protein Concentrates | |

| Soy Protein Hydrolyzed | ||

| Soy Protein Isolates | ||

| By Category | Organic | |

| Conventional | ||

| By End User | Animal Feed | |

| Food and Beverages | Bakery | |

| Beverages | ||

| Breakfast Cereals | ||

| Condiments/Sauces | ||

| Confectionery | ||

| Dairy and Dairy Alternatives | ||

| Meat/Poultry/Seafood and Meat Alternative Products | ||

| RTE/RTC Foods | ||

| Snacks | ||

| Nutritional Supplements | Baby and Infant Formula | |

| Elderly and Medical Nutrition | ||

| Sport/Performance Nutrition | ||

Market Definition

- End User - The Protein Ingredients Market operates on a B2B basis. Food, Beverages, Supplements, Animal Feed, and Personal Care & Cosmetic manufacturers are considered to be end-consumers in the market studied. The scope excludes manufacturers buying liquid/dry whey to be used for application as a binding agent or thickener or other non-protein applications.

- Penetration Rate - Penetration Rate is defined as the percentage of Protein-Fortified End User Market Volume in the Overall End User Market Volume.

- Average Protein Content - Average protein content is the average protein content present per 100 g of product manufactured by all end-user companies considered under the scope of this report.

- End User Market Volume - End-user market volume is the consolidated volume of all types and forms of end-user products in the country or region.

| Keyword | Definition |

|---|---|

| Alpha-lactalbumin (α-Lactalbumin) | It is a protein that regulates the production of lactose in the milk of almost all mammalian species. |

| Amino acid | It is an organic compound that contains both amino and carboxylic acid functional groups, which are required for the synthesis of body protein and other important nitrogen-containing compounds, such as creatine, peptide hormones, and some neurotransmitters. |

| Blanching | It is the process of briefly heating vegetables with steam or boiling water. |

| BRC | British Retail Consortium |

| Bread improver | It is a flour-based blend of several components with specific functional properties designed to modify dough characteristics and give quality attributes to bread. |

| BSF | Black Soldier Fly |

| Caseinate | It is a substance produced by adding an alkali to acid casein, a derivative of casein. |

| Celiac disease | Celiac disease is an immune reaction to eating gluten, a protein found in wheat, barley, and rye. |

| Colostrum | It is a milky fluid that’s released by mammals that have recently given birth before breast milk production begins. |

| Concentrate | It is the least processed form of protein and has a protein content ranging from 40-90% by weight. |

| Dry protein basis | It refers to the percentage of "pure protein" present in a supplement after the water in it is completely removed through heat. |

| Dry whey | It is the product resulting from drying fresh whey which has been pasteurized and to which nothing has been added as a preservative. |

| Egg protein | It is a mixture of individual proteins, including ovalbumin, ovomucoid, ovoglobulin, conalbumin, vitellin, and vitellenin. |

| Emulsifier | It is a food additive that facilitates the blending of foods that are immiscible with one another, such as oil and water. |

| Enrichment | It is the process of addition of micronutrients that are lost during the processing of the product. |

| ERS | Economic Research Service of the USDA |

| Extrusion | It is the process of forcing soft mixed ingredients through an opening in a perforated plate or die designed to produce the required shape. The extruded food is then cut to a specific size by blades. |

| Fava | Also known as Faba, it is another word for yellow split beans. |

| FDA | Food and Drug Administration |

| Flaking | It is a process in which typically a cereal grain (like corn, wheat, or rice) is broken down into grits, cooked with flavors and syrups, and then pressed into flakes between cooled rollers. |

| Foaming agent | It is a food ingredient that makes it possible to form or maintain a uniform dispersion of a gaseous phase in a liquid or solid food. |

| Foodservice | It refers to the part of the food industry which includes businesses, institutions, and companies which prepare meals outside the home. It includes restaurants, school and hospital cafeterias, catering operations, and many other formats. |

| Fortification | It is the deliberate addition of micronutrients that are not found in them naturally or which are lost during processing, to improve a food product's nutritional value. |

| FSANZ | Food Standards Australia New Zealand |

| FSIS | Food Safety and Inspection Service |

| FSSAI | Food Safety and Standards Authority of India |

| Gelling agent | It is an ingredient that functions as a stabilizer and thickener to provide thickening without stiffness through the formation of gel. |

| GHG | Greenhouse Gas |

| Gluten | It is a family of proteins found in grains, including wheat, rye, spelt, and barley. |

| Hemp | It is a botanical class of Cannabis sativa cultivars grown specifically for industrial or medicinal use. |

| Hydrolysate | It is a form of protein manufactured by exposing the protein to enzymes that can partially break the bonds between the protein's amino acids and break down large, complicated proteins into smaller pieces. Its processing makes it easier and quicker to digest. |

| Hypoallergenic | It refers to a substance that causes fewer allergic reactions. |

| Isolate | It is the purest and most processed form of protein which has undergone separation to obtain a pure protein fraction. It typically contains ≥ 90% of protein by weight. |

| Keratin | It is a protein that helps form hair, nails, and the outer layer of skin. |

| Lactalbumin | It is the albumin contained in milk and obtained from whey. |

| Lactoferrin | It is an iron‑binding glycoprotein that is present in the milk of most mammals. |

| Lupin | It is the yellow legume seeds of the genus Lupinus. |

| Millenial | Also known as Generation Y or Gen Y, it refers to the people born from 1981 to 1996. |

| Monogastric | It refers to an animal with a single-compartmented stomach. Examples of monogastric include humans, poultry, pigs, horses, rabbits, dogs, and cats. Most monogastric are generally unable to digest much cellulose food materials such as grasses. |

| MPC | Milk protein concentrate |

| MPI | Milk protein isolate |

| MSPI | Methylated soy protein isolate |

| Mycoprotein | Mycoprotein is a form of single-cell protein, also known as fungal protein, derived from fungi for human consumption. |

| Nutricosmetics | It is a category of products and ingredients that act as nutritional supplements to care for skin, nails, and hair natural beauty. |

| Osteoporosis | It is a medical condition in which the bones become brittle and fragile from loss of tissue, typically as a result of hormonal changes, or deficiency of calcium or vitamin D. |

| PDCAAS | Protein digestibility-corrected amino acid score (PDCAAS) is a method of evaluating the quality of a protein based on both the amino acid requirements of humans and their ability to digest it. |

| Per-capita consumption of animal protein | It is the average amount of animal protein (such as milk, whey, gelatin, collagen, and egg proteins) that is readily available for consumption by each person in an actual population. |

| Per-capita consumption of plant protein | It is the average amount of plant protein (such as soy, wheat, pea, oat, and hemp proteins) that is readily available for consumption by each person in an actual population. |

| Quorn | It is a microbial protein manufactured using mycoprotein as an ingredient, in which the fungus culture is dried and mixed with egg albumen or potato protein, which acts as a binder, and then is adjusted in texture and pressed into various forms. |

| Ready-to-Cook (RTC) | It refers to food products that include all of the ingredients, where some preparation or cooking is required through a process that is given on the package. |

| Ready-to-Eat (RTE) | It refers to a food product prepared or cooked in advance, with no further cooking or preparation required before being eaten. |

| RTD | Ready-to-Drink |

| RTS | Ready-to-Serve |

| Saturated fat | It is a type of fat in which the fatty acid chains have all single bonds. It is generally considered unhealthy. |

| Sausage | It is a meat product made of finely chopped and seasoned meat, which may be fresh, smoked, or pickled and which is then usually stuffed into a casing. |

| Seitan | It is a plant-based meat substitute made out of wheat gluten. |

| Softgel | It is a gelatin-based capsule with a liquid fill. |

| SPC | Soy protein concentrate |

| SPI | Soy protein isolate |

| Spirulina | It is a biomass of cyanobacteria that can be consumed by humans and animals. |

| Stabilizer | It is an ingredient added to food products to help maintain or enhance their original texture, and physical and chemical characteristics. |

| Supplementation | It is the consumption or provision of concentrated sources of nutrients or other substances that are intended to supplement nutrients in the diet and is intended to correct nutritional deficiencies. |

| Texturant | It is a specific type of food ingredient that is used to control and alter the mouthfeel and texture of food and beverage products. |

| Thickener | It is an ingredient that is used to increase the viscosity of a liquid or dough and make it thicker, without substantially changing its other properties. |

| Trans fat | Also called trans-unsaturated fatty acids or trans fatty acids, it is a type of unsaturated fat that naturally occurs in small amounts in meat. |

| TSP | Textured soy protein |

| TVP | Textured vegetable protein |

| WPC | Whey protein concentrate |

| WPI | Whey protein isolate |

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: Identify Key Variables: The quantifiable key variables (industry and extraneous) pertaining to the specific product segment and country are selected from a group of relevant variables & factors based on desk research & literature review; along with primary expert inputs. These variables are further confirmed through regression modeling (wherever required).

- Step-2: Build a Market Model: In order to build a robust forecasting methodology, the variables and factors identified in Step-1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set and the model is built on the basis of these variables.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms